Hostile Takeover in Indonesia: Challenges and Prospects - Tilburg University

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Hostile Takeover in Indonesia: Challenges and Prospects

A Comparative Study of Corporate Structure and Takeover Regulations in Indonesia, United

Kingdom and United States.

MASTER THESIS

LL.M. INTERNATIONAL BUSINESS LAW 2017/2018

Written By:

Audi Ayundaputri Susilo

SNR 2016163 | ANR 615941

Supervisor:

Dr. Jing Li

TILBURG LAW SCHOOL

TILBURG UNIVERSITY

TILBURG | 2018

To

My parents, Slamet Susilo and Didiet Damayanti

My sister, Sarah Safira Indah Putri

Aditya Dwiyandi Putra

And all my friends

For their endless support

To my supervisor

Dr. Jing Li

Thank You

TABLE OF CONTENTS

TABLE OF CONTENTS....................................................................................................... i

TABLE OF FIGURES ........................................................................................................ iii

CHAPTER 1...................................................................................................................... 1

INTRODUCTION ..............................................................................................................1

CHAPTER 2...................................................................................................................... 5

INTRODUCTION TO HOSTILE TAKEOVER IN THE CONTEXT OF MARKET FOR

CORPORATE CONTROL AND ITS ALTERNATIVES ............................................................ 5

2. 1. Introduction to Hostile Takeover .......................................................................5

The definition and mechanism of hostile takeover ...............................................5

Hostile takeover as a mechanism for market for corporate control ..................... 6

Arguments against hostile takeover ......................................................................8

2.2. Alternatives to hostile takeover .......................................................................10

Hostile Takeover as the solution of agency problem .................................................. 10

Incentive Contracts ......................................................................................................11

Internal Monitoring......................................................................................................13

External Monitoring .....................................................................................................14

Market Solutions ..........................................................................................................16

2.3. Factors to be taken in consideration in determining the most suitable

alternatives ..............................................................................................................17

Institutional Framework of Corporate Governance .................................................... 17

Difference of corporate governance around the world ..............................................20

Conclusion ................................................................................................................21

CHAPTER 3.................................................................................................................... 24

HOSTILE TAKEOVER PRACTICE IN U.K AND U.S ........................................................... 24

3.1 Hostile Takeover Practice In U.K ........................................................................24

U.K Takeover Regulatory Framework ..................................................................24

Hostile Takeover Practice in U.K ..........................................................................28

3.2 Hostile Takeover Practice In U.S ........................................................................31

U.S Takeover Regulatory Framework ..................................................................31

Comparison and Conclusion .................................................................................... 36

Conclusion ................................................................................................................39

i

CHAPTER 4.................................................................................................................... 41

CHALLENGES AND PROSPECTS OF HOSTILE TAKEOVER IN INDONESIA ....................... 41

4.1. Takeover regulation in Indonesia .....................................................................41

4.2 Challenges of Hostile Takeover in Indonesia ..................................................... 46

4.3 Rationale of Hostile Takeover in Indonesia ....................................................... 50

4.4 Lessons from U.K and U.S Takeover With Regards To Hostile Takeover ...........53

4.6 Alternatives to hostile takeover ........................................................................59

4.7 Conclusion ..........................................................................................................62

CHAPTER 5.................................................................................................................... 65

CONCLUSION ................................................................................................................65

BIBLIOGRAPHY .............................................................................................................68

Literatures .................................................................................................................... 68

ii

TABLE OF FIGURES

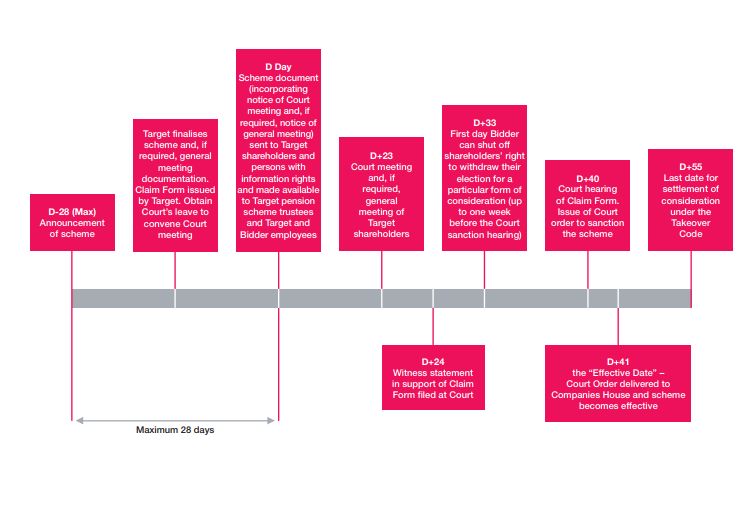

Figure 1: U.K Takeover Scheme ................................................................................... 27

Figure 2: Timeline of U.S Takeover Scheme ................................................................ 33

Figure 3: OECD Foreign Direct Investment Regulatory Restrictiveness South East Asia

Countries ...................................................................................................................... 47

Figure 4: Ownership concentration at company level, as of end 2016 ....................... 48

Figure 5: Indonesia’s Corporate Governance Practice Score Lower Than Those of Its

ASEAN Peers.................................................................................................................49

Figure 6: Strength of Protection for Minority Shareholders .......................................51

Figure 7: The 10 Economies Improving The Most Across Three or More Areas

Measured by Doing Business in 2015/2016 ................................................................ 51

iii

CHAPTER 1

INTRODUCTION

Continuous economic growth in Indonesia, supported by government’s new

economy packages that are aimed to improve competition and attract investments,1

has led to the surge of Merger & Acquisition (“M&A”) activities. The Indonesian

economy grew by 5.19% in the fourth quarter of 2017, the strongest pace since 2013

with M&A deal also growing at 4.3% recording a total deal of 137.2 During the first

half of 2017 one of the largest inbound acquisition transactions took place when Japan

Tobacco Inc acquired PT Karyadibya Mahardika and PT Surya Mustika Nusantara with

a deal value of $677 million, while PT Indika Energy Tbk’s acquisition of PT Kideco Jaya

Agung also headlined a deal of $678 million.3 Despite the rise of M&A activities in

Indonesia and government’s embracement of economic globalization, the deals

consist solely of friendly acquisitions; in fact an attempt of hostile deal is almost

unheard of ever since the acquisition of PT Matahari Putra Prima by Lippo Group in

1997, which by now is still argued as a friendly deal by the former chairman of PT

Matahari Putra Prima himself.4 Hostile takeover has never been an issue in Indonesia.

Reports from International Financial Law Review (“IFLR”) and Thomson Reuters have

brought to light that even renowned law practitioners in Indonesia view hostile

takeover as implausible due to (i) concentrated structure of company ownership and

(ii) Indonesian Takeover Regulation that is in favor of controlling shareholders. 5 As

pointed out by Chatib Basri in his review of business environment in Indonesia, the

disciplining role of hostile takeover when a company is not performing does not

1

Antonia Timmerman, ‘Indonesia 2016: Riding on inbound deals, M&A activity sees big

recovery’(Deal Street Asia , 1 January 2017) https://www.dealstreetasia.com/stories/61648-61648/>

accessed 25 February 2018.

2

Duff & Phelps Singapore Pte Ltd, Transaction Trail Annual Issue 2017 (Annual Issue 2017) 13.

3

Ibid.

4

Ardian Wibisono and Pudji Lestari, ‘Hari Darmawan, Matahari’s Acclaimed Founder, is Making His

Retail Comeback’ Forbes Indonesia (Jakarta, April 2011) 50.

5

International Financial Law Review, ‘2017 Mergers and Acquisitions Report: Indonesia’ (International

Financial Law Review, 28 March 2017) http://www.iflr.com/Article/3673242/2017-Mergers-and-

Acquisitions-Report-Indonesia.html accessed 25 February 2018.

1

function in Indonesia’s shareholders’ concentrated environment.6 This raises question

of an undeveloped disciplinary role of takeover in Indonesia. Whether the lack of

hostile takeover translates to a not functioning market for corporate control in

Indonesia and if so should Indonesia encourage the occurrence of hostile takeover.

Hostile takeover is a takeover practice where an offer is initiated without any

prior communication to or consent of the target company and often used as a control

mechanism in the theory of market for corporate control.7 The underlying premise of

market for corporate control is that the control of companies constitutes a valuable

asset, in which this asset exists without any relation to any interest in either economy

of scale or monopoly market that many great mergers are actually the result of this

special market. When an existing company is poorly managed, the market price of the

shares declines relative to the shares of peer companies in the same industry or

market as a whole. The takeover market then will act as a monitoring platform for the

management of public companies. Failure of management to run the company gives

a room for takeover by others who are more capable. A bidder may revive companies

by overthrowing their incompetent directors. Further, the threat of a hostile takeover

instigates the management to increase the share price and act in the shareholders’

interests, since a low share price will make the company a target of an alert hostile

bidder.8 Thus, market for corporate control is very beneficial both for companies and

overall social welfare since it lessens wasteful bankruptcy proceedings and more

efficient managers of corporation.9

Unlike the almost non-existent nature of hostile takeovers in Indonesia, the

practice or at least attempts of hostile takeovers have occurred overtime in United

Kingdom (“U.K”) and United States (“U.S”). Throughout 1990 to 2005, a total of 312

and 187 hostile takeovers occurred in U.K and U.S respectively. 10 These numbers

6

M Chatib Basri and Pierre van der Eng, Business in Indonesia: New Challenges, Old Problems

(Institute of Southeast Asian Studies Publication, 2004) 187.

7

Alexandro Seretakis, ‘Hostile takeovers and defensive Mechanisms In The United Kingdom and the

United states: A Case Against the United States Regime’ (2013) 3.

8

Henry G. Manne, ‘Mergers and the Market for Corporate Control’ (1965) JSTOR <

http://links.jstor.org/sici?sici=0022-

3808%28196504%2973%3A2%3C110%3AMATMFC%3E2.0.CO%3B2-3> accessed 25 February 2018.

9

Seretakis (n 7) 5.

10

John Armour and David A. Skeel, Jr, ‘Who Writes the Rules for Hostile Takeovers, and

2reflect the level of leniency towards hostile takeover from respective countries based

on the approach and view their ownership structure and the difference in decision-

making power.11 In U.K for example takeover defenses are viewed negatively by the

market and many academic studies have concluded that they are associated with

lower firm value.12 The role of institutional investors have played an important part in

this view since the decision making power of company takeover in U.K is in the hands

of shareholders. Moreover, U.K also regulate the prohibition of post-bid takeover

defense that allows hostile takeover to occur and succeed. In the U.S, the decision

making power is granted to Board of Directors (“B.O.D”), therefore despite their

companies’ ownership structure the decision will be taken by the managers.13 Unlike

U.K, U.S regulation gives bidders complete flexibility to bid for as small or as large of a

percentage of the target company’s stock as they wish. U.S. law have never imposed

a “mandatory bid” rule requiring bidders who acquire a large block of target shares to

make an offer for all of the target company’s shares. U.S. tender offer regulation does

require, however, that the bidder pay the same price for each of the shares it acquires;

that the bidder purchase a pro rata amount of the shares of each shareholder who

tenders her shares; and that it keep the bid open or at least twenty days. Nevertheless,

U.K and U.S have active markets for corporate control.14

Indonesia, however, has not yet seen the light of hostile takeover in the

context of market for corporate control despite the increase of M&A activities.

Reflecting to the practice in U.K and U.S, countries with active markets of corporate

control. This thesis is intended to provide legal analysis of whether Indonesia, as a

country where M&A have been increasingly carried out, should introduce specific

rules and regulations that will accommodate the occurrence of hostile takeover in the

context of market for corporate control. While taking into account all the relevant

factors that could support the enactment of new rules and regulations regarding

Why?—The Peculiar Divergence of U.S. and U.K. Takeover Regulation’ (2007) 12.

11

Ibid.

12

Seretakis (n 7) 9.

13

Paul L Davies, The Principles of Modern Company Law (Sweet & Maxwell Ltd 2008) 20.

14

John Armour, Jack Jacobs & Curtis Milhaupt, ‘The Evolution of Hostile Takeover Regimes in

Developed and Emerging Markets: An Analytical Framework’ (2011) 2.

3hostile takeover in Indonesia, and all the relevant factors that do not. To address these

issues, this thesis will try to answer these derivative research questions:

1. How crucial is the implementation of hostile takeover in the context of

market of corporate control in Indonesia?

2. In countries that have active markets for corporate control, how is hostile

takeover regulated and treated?

3. To what extent does the current takeover regulation and environment in

Indonesia accommodate the occurrence of hostile takeover?

The research questions of this thesis will be answered using a combination of

normative and empirical methodology, accordingly the research questions will not

only be analyzed based on literature review, but it will also be analyzed based on

empirical data. Furthermore, a comparative study will also be required to consider

how the regulators in other jurisdictions handle hostile takeover, including the costs

and benefits of such options. Thus, this thesis will be structured as follows. The second

chapter consists of literature review and the introduction of hostile takeover in the

context of market for corporate control. The third chapter provides an overview of

the various regulatory options of takeover in U.K and U.S, including the purpose and

the results of the implementation of their regulatory responses. Based on the previous

chapters, the fourth chapter analyzes the answers to these questions: how takeover

is structured in Indonesia, the challenges of market for corporate control in Indonesia,

what are the rationale for market for corporate control in Indonesia, what can be

learned from other jurisdictions’ regulatory responses and experiences, and if there’s

any potential of hostile takeover in Indonesia. Finally, the last chapter concludes.

4CHAPTER 2

INTRODUCTION TO HOSTILE TAKEOVER IN THE CONTEXT OF MARKET FOR

CORPORATE CONTROL AND ITS ALTERNATIVES

2. 1. Introduction to Hostile Takeover

The definition and mechanism of hostile takeover

Hostile takeover occurs when a bidder launches a takeover offer without the

consent of and contested by target’s company management, for the purpose of

acquiring control of target’s company.15 The theory does not specify the legal status

of companies in which hostile takeovers take place however, in practice, hostile

takeovers only occur in public companies due to shares being accessible to public. The

distinguishing feature between hostile and friendly takeovers lies in the negotiation

strategy. Hostile takeover is commonly perceived when an offer is made public that is

aggressively rejected by the target firm. Subsequently, perception of hostile takeover

is closely related to takeover negotiations that are far from completion.16

Hostile takeovers are popularly done through aggressive tactics namely: bear

hug, proxy contest, or hostile tender offer. Through bear hug, the bidder attempts to

limit the options of the target’s senior management by making a formal acquisition

proposal involving a public announcement to the board of directors of the target that

demands rapid decision. The board, bearing fiduciary duty to the target’s

shareholders, are prompted to a negotiated settlement. In this tactic, bidder usually

set the offer at a substantial premium to the target’s current stock price, subjecting

the board to a lawsuit from target shareholders when immediately rejecting the

offer.17 The second hostile takeover tactic is proxy contest, whereas the bidder use

solicitation method to influence shareholders’ votes to support bidder’s proposal.18

15

Donald Depamphilis, Mergers, Acquisitions, and other Restructuring Activities (5th edition, Academic

Press Advanced Finance Series 2009) 10.

16

G William Schwert, ‘Hostility in Takeovers: In the Eyes of the Beholder?’ (The Journal of Finance

2000) 2600.

17

Jarrad Harford, ‘Takeover bids and target directors’ incentives: The impact of a bid on directors’

wealth and board seats’. (2003) 69: 51-83.

18

Depamphilis (n15) 97.

5Lastly, hostile takeovers are usually conducted through hostile tender offer where

usually potential bidders purchase stock in a target before a formal bid to accumulate

stock at a price lower than the eventual offer price. These purchases are kept secret

to avoid driving up the price. Once the bidder has established a toehold ownership

position in the voting stock of the target, bidder may attempt to call a special

shareholders’ meeting to remove takeover defense and subsequently launch the

hostile bid.19

Hostile takeover as a mechanism for market for corporate control

Typically, takeover regulation acts as sentinel in corporate governance

function of market for corporate control. When a company is found undervalued, or

considered cheap relative to what it could potentially be if it was run better, a bidder

would find it profitable and they would turn it around, and re-sell it at profit.

Furthermore, changes in corporate control is claimed as an effective governance

mechanism due to the free-rider problem, the hazard of overpayment of target

company, and the unreasonable takeover cost which makes acquisitions useful only

in correcting more serious governance problems. 20 There have been tremendous

literatures that analyze hostile takeover as mechanism of market for corporate

control. The focus of these literatures mostly are about the feasibility, benefit as well

as efficiency of hostile takeover in the context of market for corporate control,

whereby they argue that hostile takeover is necessary for strengthening control over

managers’ efficiency, maximizing company’s welfare and promoting strong economy.

Provided in his paper, Henry G Manne remarked that hostile takeovers give small

shareholders power and protection commensurate with their interest in corporate

affairs, which is the solution for small shareholders’ insignificant control relationship

with corporate. 21 He believe that stock market is the only access for outsiders to

objectively assess the management’s efficiency of a company thus the hostile

takeover scheme will give some assurance of competitive efficiency among corporate

19

Depamphilis (n 15) 99.

20

Nenova Tatiana, ‘Takeover Laws and Financial Development, World Bank Policy Research Working

Paper’ (2006) 8.

21

Manne (n 8) 5.

6managers and therefore provide strong protection to the interests of small, non-

controlling shareholders.22 Based on such premise hostile takeovers can improve the

performance of the targeted company, providing a corrective mechanism for

replacing under-performing managers and often the threat of a hostile bid by itself

can boost up performance of the target company.23

Another benefit of hostile takeover as maintained by scholars is that it

promotes wealth-maximizing principle for a company. Pointed out in a number of

studies that examined the correlation between state anti-takeover laws and the

wealth effects of shareholders, allowing hostile takeover will give higher benefit for

the shareholders. Jonathan Karpoff and Paul Malatesta provide an empirical analysis

of the second generation antitakeover statutes in U.S and the effects on the

shareholders’ wealth, it was found that there was a corresponding reduction in

shareholder and bondholder value in the emergence of their enactment. 24 Early

studies and surveys of takeover defenses such as poison pills and shark-repellent also

generally accepted that installing takeover defenses resulted in the reduction of

shareholders’ wealth. 25 In their paper, Bertrand and Mullainathan found that

countries with takeover laws that allow the companies to easily install anti-takeover

defenses have negative productivity and profitability.26 Further studies also find that

hostile takeovers are expected to create higher value than friendly ones.27

Hostile takeovers also seem to promote overall stronger economy. Empirical

evidence indicates that there is a positive association between the strength of

takeover market and management turnover, resulting the discipline of

22

Ibid.

23

Sudi Sudarsanam, Creating Value From Mergers and Acquisition: The Challenges, (Pearson

Education Limited 2003) 55.

24

Jonathan M Karpoff and Paul H. Malatesta, ‘The Wealth Effects of Second-Generation State

Takeover Legislation’ (1989) 294-303.

25

Paul Migrom and John Roberts Milgrom, ‘Economics, Organization and Management’ (Prentice Hall;

U.S.Edition 1992) 56.

26

Marianne Bertrand and Sendhil Mullainathan, ‘Executive Compensation and Incentives: The Impact

of Takeover Regulation’, National Bureau of Economic Research (1998) 5.

27

Balachandran, Balasingham and Duong, Huu Nhan and Luong, Hoang and Nguyen, Lily, ‘M&A Laws

and Stock Price Crash Risk: International Evidence’ (2018) SSRN

accessed 1 March 2018.

7management.28 In practice, the best way a market for corporate control can operate

is when the takeover regime is neutral for the best management to win. When the

takeover regulation enables a healthy market for corporate control it will override

personal interests of management that hinders the welfare of the company. As stated

by Sudi Sudarsanam, a well-developed regulatory regime for the market for corporate

control increases the scope of competition for corporations and empowers

shareholders that led to a stronger economy.29

Arguments against hostile takeover

In spite of the aforementioned benefit of hostile takeover, a number of

scholars have expressed strong criticism against hostile takeover as means of market

for corporate control. For example in its theory, market for corporate control

presumes that hostile takeovers targets’ are companies that are not efficiently

managed that the bidder can restructure, thus resulting in gains for the target

company. However, in Julian Franks and Colin Mayer ‘s study of U.K’s hostile bids, it is

found that targets of hostile takeovers are not poor managed companies with regards

to targets of negotiated takeovers or independent companies active in the same

industry.30 They also noted that there is no evidence of either high bid premiums or

poor pre-bid performance when takeovers involve managerial control changes and

concluded that the market for corporate control does not function as a disciplinary

device for poorly performing companies.31 This argument is also confirmed by Blanaid

Clarke who claimed that the application of the theory of market for corporate control

is limited for (i) the unlikeliness of minor mismanagement to impact on company’s

share price and thus the theory does not seem to apply in relation to hostile takeovers

for companies that are not seriously perform poorly (ii) the unlikeliness of a bidder to

28

Ugur Lel and Darius P. Miller, ‘ Does takeover activity cause managerial discipline? Evidence from

international M&A laws’ (2015) Review of Financial Studies

accessed 25 February 2018.

29

Sudarsanam (n 23) 56.

30

Julian Franks and Colin Mayer, ‘Hostile Takeovers and The Correction Of Managerial Failure’ (1995)

Journal of Financial Economics, 164.

31

Guoxiang Song, ‘Is the Market for Corporate Control of Large Banks Effective?’ (2018).

SSRN accessed 5 March 2018.

8risk acquiring a company that has severe poor performance, since most often the

losses that caused by such poor performance are irreversible. For these reasons,

poorly performing companies affected by the substantial level of managerial

inefficiency will not be targets of hostile takeovers. 32 Blanaid also added that the

challenges to the practice of market for corporate control are significant. These

challenges stem both from the nature of the theory itself and its reliance upon market

efficiency and also from the barriers, which may be erected by corporate

stakeholders.33

Over and above, even if there are beneficial effects on corporate governance

arising from market for corporate control, hostile takeovers do not offer a long-term

permanent solution to mismanagement of managers, since they are not frequent and

involve heavy costs for the bidder. As has been observed by Andrei Shleifer and Robert

Vishny, hostile takeovers may harm the bidder’s shareholders where an active market

for corporate control will allow managers of bidding companies to pursue an empire

building tactic through takeovers and not for the purpose of correcting the target’s

management.34 In addition, fear of takeover and the associated employment risk may

cause managers to take actions that are focused on maximizing short-term price

rather than long-term value. Michael C. Jensen states that “when numbers are

manipulated to tell the market what they want to hear rather than the true status of

the company, it is lying, and and stakeholders (such as creditors).35

Furthermore, there are other ways to discipline companies’ managements

other than hostile takeover. Davidoff wrote about the adaptability of corporate law.

He theorized that even if companies’ use of takeover devices was severely restricted,

corporations and practitioners would manage to resolve those restrictions. The

markets could create their own monitoring devices to substitute for a more restricted

32

Seretakis (n 7) 25.

33

Blanaid Clarke, ‘Reinforcing The Market For Corporate Control’ (2010) 39/2010 UCD Working

Papers in Law, Criminology & Socio-Legal Studies Research Paper <

https://ssrn.com/abstract=1661620> accessed 5 March 2018.

34

Andrei Shleifer & Robert W. Vishny, ‘A Survey of Corporate Governance’ (1997) 52(2) J.

FIN. 737 accessed 10 March 2018.

35

Ibid.

9takeover market, such as independent directors and institutional shareholders.36 In

addition, bidders of hostile takeovers may find that in successfully acquiring the target

company they may be taking a long shot in the target’s market share price and may

have little to show their own shareholders, thus according to Sudi Sunarsanam with

an efficient market for corporate control, profitable acquisitions may be harder to

accomplish.37

Based on the aforementioned literature, it can be argued that there’s still a

huge debate of establishing clear regulation of hostile takeover in the context of

market for corporate control. On one hand hostile takeover is seen as an effective

external corporate control but on the other hand it is viewed as harmful practice for

the companies. This thesis aims to analyze further the need of hostile takeover in the

context of market for corporate control in Indonesia by providing more details on the

state of Indonesia’s corporate governance. In order to support the research of this

thesis, it is important to consider the aforementioned literature, especially

highlighting the costs, benefits and practicality of hostile takeover and its various

regulatory approaches.

2.2. Alternatives to hostile takeover

Hostile Takeover as the solution of agency problem

The idea of hostile takeover as market for corporate control stems from the

notion that hostile takeover can be a monitoring mechanism from external parties

having interest in acquiring the company.38 This monitoring mechanism is claimed to

be a solution for separation of ownership issue, known as agency problem, in such

company. This agency problem usually arises when (i) there is lack of alignment

between desires and objectives of the management and, (ii) there is information

asymmetry between shareholders and management of the company. For the first

reason, shareholder’ interest is always about maximizing their value, primarily

36

Steven M. Davidoff, ‘Takeover Theory and the Law and Economics Movement’ (2011) Research

Handbook On The Economics of Corporate Law accessed 10

March 2018.

37

Sudarsanam (n 23) 56.

38

Manne (n 8) 7.

10obtaining as much return on their investment. On the other hand, management will

often make decisions that maximize their utility function, which will not always align

with maximizing shareholders’ value. For example, shareholders’ and management

have different attitude in facing risks. Shareholders typically diversify their investment

by only investing small portion of their wealth in one company so that if one

investment fails it can be offset by the profit of other investment. Meanwhile,

management works only for one company and their value depends on the

performance of that one company only, consequently management is more risk-

averse than shareholders especially in choosing projects and strategy for the company

and therefore creates different alignment between their objectives and shareholders’

objectives. Secondly, the agency problem arises from information asymmetry

between shareholders and management. For instance, management are directly

involved in the operation of the company, inevitably they are more exposed to

detailed crucial information about the company than shareholders, which will lead to

different valuation and decision of management and shareholders. Hostile takeover,

in this sense, is seen as a mechanism to control these issues through the corporate

market. As discussed beforehand, hostile takeover is viewed as a way to align

shareholders’ interest with management and also narrow the information asymmetry

between them. However, there are other alternatives to overcome agency problem

depending on the institutional framework of the business environment. Douma and

Schreuder divided the alternatives into four categories namely, (i) incentive contracts,

(ii) internal monitoring, (iii) external monitoring, and (iv) market solutions that include

the functioning of various markets. 39 The compatibility of these alternatives also

depends on the institutional framework of the business environment, whether or not

it is within the market-oriented framework or network-oriented framework.40

Incentive Contracts

39

Sytse Douma and Hein Schreuder, Economic Approached to Organization, (sixth edition, Pearson

Education Limited 2018) 300.

40

Ibid 305.

11In countries that have rather inadequate institutional framework of corporate

governance the issue lies in the enforcement of the law, not the law itself. 41 For

example, Russia and China are the two countries that have similar problem. Both

countries experience trouble in implementing their corporate governance. For Russia,

its politicized and malfunctioning legal system is the biggest hurdle and the

government is making tremendous effort in doing something about their bad

reputation in the business world by planning legislation surrounding their corporate

governance. 42 Meanwhile in China, the government is unwilling to enforce the

corporate governance evenhandedly due to its low confidence in the stock market.43

In both countries, what needs to be improved is the enforcement of corporate

governance law to allow their companies to participate entirely in the global

economy. 44 As mentioned by Douma and Schreuder, the possible solution to

overcome the issue of enforcing corporate governance can be by way of using

organizational solution, which is through incentive contracts. These incentive

contracts can be in the form of cash bonuses, share plans, stock options and

temporary contracts. These forms of incentive contracts can be structured in a way

that management will get incentives if shareholders’ goals are met.45 For example,

giving cash bonuses to management when certain goals are met, including equity

based compensation in management’s composition to ensure their long-term vision,

providing stock option that’s vested in their compensation component as well as

limiting the duration of management’s position in the company. However giving

incentive contracts as a way to solve agency problem is restricted since there are

outside factors that play into determining incentives for management behavior, worse

41

Ibid 310.

42

Financial Times. ‘Russia: Laws do exist but enforcement is patchy’ (Financial Times, 6 October 2010)

accessed 5 March 2018.

43

The Economist, ‘Seeing the forest for the trees’ (The Economist, 4 February 2012)

accessed 5 March 2018.

44

Financial Times. ‘Russia: Laws do exist but enforcement is patchy’ (n 42).

45

Lucian Arye Bebchuck and Jesse M Fried, ‘Executive Compensation As Agency Problem’ (2003) 17

Journal of Economic Perspectives

accessed 5 March 2018.

12incentives can result in additional agency problem.46 Thus, it is only a partial way into

solving the agency problem and it should be followed by other means of corporate

governance.

Internal Monitoring

As previously discussed, using incentives alignment will not totally eliminate

agency problem. Shareholders remain relatively have less information than the

managerial insiders. Therefore it is necessary to find ways to reduce the information

asymmetry between shareholders and managers, which can be done through

monitoring either internally or externally.

Internal monitoring can be done by shareholders, outside board of directors,

non-executive board member and the two-tier board system. Monitoring by

shareholders can be effective if there’s block-holders in the company however not so

much in a company with widely distributed ownership since they will not have much

impact in the voting of company’s agenda.47

The second type of internal monitoring is by board of directors. It is claimed

that considering the increased pressure from institutional shareholders, more

government regulations, greater threats of litigation, boards have become more

independent and diligent. Thus, directors are willing to monitor. This raises the

probability that boards also will hire external person for the CEO position consisting

of inside and outside directors.48 The inside directors, known as executive directors,

are full time manager of the company. Meanwhile the outside directors, also called as

non-executive directors or independent directors are mostly senior managers of other

large companies. The composition of inside directors and outside directors can be

structured by one-tier board or two-tier board. In a two-tier board system there are

46

Ibid.

47

Douma and Schreuder, (n 39) 325.

48

Renee Adams, Benjamin E. Hermalin, and Michael S. Weisbach, ‘The Role of Boards of Directors in

Corporate Governance: A Conceptual Framework and Survey’ (2010) XLVIII Journal of Economic

Literature < http://www.nber.org/papers/w14486.pdf> accessed 6 March 2018.

13two levels of boards that separate the executive and supervisory duties. Meanwhile

in one-tier board the duties of executive and supervisory are combined in one board.49

In one-tier board system, the board consists of executive and non-executive

members. Meanwhile the board as a whole is responsible for running the company,

the non-executive board members have the additional task of monitoring the

executives. The board is responsible for decision management as well as decision

control. The main tasks of a supervisory board are to monitor the members of the

executive and to ratify certain decisions.

Internal monitoring in a two-tier board system, there are two boards with a

separation of executive and supervisory duties. The main role of the executive board

is to run the company while the supervisory board is there to monitor the executive

board as well as giving the executive board advises on a broad range of subjects,

including the company’s strategic direction. Usually important decisions, such as large

investments, acquisitions, and choice of the company’s auditor, require the prior

approval of the supervisory board. Thus, there is a separation of decision management

and decision control. The executive board is responsible for decision management,

the supervisory board for decision control.

A study by Graziano and Luporini shows that companies with two-tier board

have higher profit than those installing one-tier board. This is because the two-tier

board encourage initiative from lower level board which as a result require higher

effort for manager to gather information on projects compared to companies with

one-tier board where large shareholder controls the board.50

External Monitoring

Other than from internal body of the company, monitoring can also be

executed through parties outside of the companies known as external monitoring.

These outside parties can be auditors, stock analysts, debt holders and credit-rating

49

Douma and Schreuder, (n 39) 330.

50

Clara Graziano and Annalisa Luporini, ‘Ownership Concentration, Monitoring and Optimal Board

Structure’ (2005) 1543 CESifo Working Paper Series accessed 6

March 2018.

14agencies. External monitoring helps to reduce information asymmetry in markets and,

thus, improves their functioning. 51 External monitoring can be done by auditing

companies, stock analysts, and debt holders.

External monitoring by auditing companies play an important monitoring role

as they audit company’s financial statements and compliance with the law and other

relevant regulations. The existence of independence is important for management, as

they will increase the credibility of the companies. As claimed by many studies, public

disclosures have been seen as a method of overseeing the monitoring hypothesis. An

independent auditor can be hired to inspect the information environment. Thus,

auditing is one form of controlling for the monitoring hypothesis. The audit reduces

the agent’s chances to withhold material information from the shareholders. 52

Furthermore, the independent audit committees are regarded to be a method that

enhances the auditor’s independent position in negotiations and increases the

effectiveness and quality of the audit engagement.53

External monitoring by stock analysts play the role of analyzing company’s

performance and making predictions based on it. Usually stock analysts make reports

of it in which can significantly influence company’s share prices. Through the share

price, shareholders can acquire information of how the company is doing. Therefore,

stock analysts play an important role, yet an indirect one; they help to reduce

information asymmetry between shareholders and CEO.54

The last type of external monitoring is monitoring by debt holders. Companies

that conduct their business in mature industries usually have problem of free cash

flow. One way to reduce this problem is to change the capital structure of the

company by taking large loans and distributing the cash obtained to shareholders. This

way, the cash generated by the company is necessary to service the debt such as

51

Douma and Schreuder, (n 39) 340.

52

Wanda Wallace, ‘The economic role of the audit in free and regulated markets:

a look back and a look forward’ (1980) 2 Open Educational Resources <

https://scholarworks.wm.edu/oer/2> accessed 6 March 2018.

53

Terence Bu-Peow Ng and Hun-Tong Tan, ‘Effects of authoritative guidance availability and audit

committee effectiveness on auditors' judgments in an auditor-client negotiation context’(2003) 78

The Accounting Review < https://doi.org/10.2308/accr.2003.78.3.801> accessed 19 March 2018.

54

Douma and Schreuder, (n 39) 345.

15payment of interest and amortization. Thus, managers can no longer invest in projects

with a negative net present value. Further, debt holders will often attach conditions

to the loans they make such as debt covenants. These conditions often require that

the company should maintain a number of financial ratios at or above a certain level.

Therefore providers of debt will be keen to monitor management at this point.55

Market Solutions

Aside from organizational arrangements such as incentive contracts and

monitoring, as mentioned earlier, agency problem may be constrained by markets.

Companies are always linked tight to market whether in the product market,

managerial labour market, stock market and eventually corporate control market

which has been discussed extensively earlier. Competition in these markets forces

companies to be efficient and to some extent is able to discipline managers. 56 The

mechanism of market solution can be done by competition in the product market,

competition in the managerial labor market, and competition in the stock market.

Overcoming agency problem can be done through competition in the product

market, which is the market for the company’s products. A company that sells its

products in a perfectly competitive market will reduce manager’s chance of engaging

in on-the-job consumption, simply because that would result in negative profits and

the company would go bankrupt. In a perfectly competitive market, companies have

to minimize costs, including agency costs, if they want to survive. However there are

very few markets that are perfectly competitive. Competition in very many markets

is far from perfect, which means that companies can make profits without entrants

being able to step in and take a share of the market. In such an environment, managers

can engage in on-the-job consumption. That will mean lower profits, but, as long as

there is sufficient profit left, the company can continue.57

Companies’ management may also be disciplined by competition in the market

for their own services, which is the managerial labour market. In this alternative CEO

55

Ibid 348.

56

Ibid 350.

57

Ibid 355.

16of a small company who creates substantial wealth for her shareholders may be asked

to become CEO of a bigger company in which they will be offered larger

compensation. The competition between CEOs of small companies for top positions

in large companies can possibly motivate CEOs of small companies to act in the

interests of shareholders. Consequently, such competition can also discipline

managers.58

Stock market competition can also be a way to solve agency problem

particularly for public companies with shares that are traded on the stock market.

Through this market, investors will put pressure on companies to operate efficiently

and maximize the value of the company. Fast growing companies in new industries

have to attract additional equity capital by issuing new shares. The pricing of new

shares is heavily dependent on the company’s prospects, but potential investors also

take a good look at its past performance.59

2.3. Factors to be taken in consideration in determining the most suitable

alternatives

Institutional Framework of Corporate Governance

As can be observed by the various alternatives of overcoming agency problem

it can be concluded that there are different corporate governance systems used in

various parts of the world. The differences can be seen by (i) the features of the

societies they are embedded in and (ii) the economic and political developments that

have been incorporated in their institutional frameworks. From said differences and

the system can be divided into two categories namely market-orientated systems and

network-orientated systems.60

Market Oriented System

The main characteristics of market-orientated systems of corporate

58

Ibid 356.

59

Douma and Schreuder, (n 39) 358.

60

William W. Bratton and Joseph A. McCahery, Joseph, ‘Comparative Corporate Governance and the

Theory of the company: The Case Against Global Cross Reference’ (1999) 38 (2) Columbia Journal of

Transnational Law

accessed 10 March 2018.

17governance are the existence of large, efficient stock markets, disperse share-

ownership structure, strong legal protection of minority shareholders and separation

of ownership from control. In this system all large companies are listed on a stock

exchange where there is no shareholders that hold a controlling block and managers

tend to own a small percentage of companies they manage. This description more or

less fits the situation in Anglo-American countries such as the USA, the UK, Canada,

Australia and New Zealand. For example, in the USA more than 50% of the shares of

listed companies are owned by households while the rest are owned mainly by

financial institutions. However a single financial institution rarely owns more than 10%

of the shares in a non-financial company. In a typical market-orientated system of

corporate governance, each single investor owns a small percentage of a company’s

stock. Consequently, the market for corporate control may arguably be effective in

this system since there is no block-holders it is possible to acquire companies shares

by majority investors.61

Network Oriented System

On the other hand the main characteristic of network-orientated systems of

corporate governance is the presence of block-holders. In a typical network-

orientated system of corporate governance, not all large companies are listed on a

stock exchange and many of the listed companies have one or a few large

shareholders. These large shareholders do not actively trade their shares.

Consequently, the free float is significantly less than 100% even 50% for many

companies. Large shareholders or their proxies sit on the board. These block-holders

have power to monitor managers and use their voting power if they are dissatisfied

with a manager’s performance. The disciplining role is done by these block-holders

instead of the market for corporate control. This description more or less fits the

situation in most non-Anglo-American countries, in both emerging markets and more

developed countries namely Japan and countries in continental Europe.

In a network-oriented system, the typical company has a small number of large

61

Douma and Schreuder, (n 39) 362.

18shareholders who have a long-term relationship with the company and its

management and are represented on the company’s Board. These block-holders

usually have other interest besides maximizing company value of the shares, such as

family ties or strategic. That’s why in countries with a network-orientated system of

corporate governance, the effectiveness of the market for corporate control is limited

not only by the institutional setting but also by the typical ownership structure in such

countries. In countries such as Germany, France, Italy, Spain, Japan, Korea and India,

shares in large corporations are not as widely distributed as in the USA and UK.62

While there are important differences between the corporate governance

systems in countries with less dispersed share-ownership there is also a common

feature which is block-holders. Companies with the same institution or person as

block-holders can be viewed as forming a network, which is where the term has been

derived.

In countries with a network-orientated system, the laws for insider trading are

generally not very strict. This allows block-holders to confer with management and,

thus, influence managerial decisions. Often even these block-holders sit on the board.

Thus, in a network-orientated system of corporate governance, managers are

disciplined mainly by organizational arrangements. 63

Comparison of the two institutional framework

In market-orientated systems of corporate governance, severe

underperformance by managers is restricted mainly by the fear of a hostile takeover.

The board of directors is probably less important in this respect because outside

directors may lack the incentive to perform their functions as monitors well. That may

be especially true when the CEO is also chair of the board. Thus, the market for

corporate control is the most important mechanism for reducing the agency problem

between shareholders and managers.

In network-orientated system of corporate governance, the monitoring of

62

Jeroen Weimer and Joost C. Pape, ‘A Taxonomy of Systems of Corporate Governance’ (1998) 7 (2)

Blackwell Publishers 19.

63

Douma and Schreuder, (n 39) 363.

19management by independent board member may be the most important mechanism

for reducing the agency problem since block-holders have the incentives to perform

their monitoring role in an effective way. The market for corporate control play

insignificant role in terms of disciplining managers which is why there are virtually no

hostile takeovers in this system. The fundamental ground for this is probably that a

hostile bidder has to convince owners of large blocks of shares, who are also board

members or are represented on the board that selling their shares is in their best

interests. However there’s a disadvantage of network-oriented system which is an

under developed market for equity capital. This under development may prevent

optimal allocation of equity capital in countries in which network-orientated systems

prevail. Further, another disadvantage may arise when the main private shareholders

in a company do not act in the best corporate interests for private reasons, such as

retaining family influence or prestige.

There are studies conducted on the relationship between firm ownerships and

corporate governance which was concluded that major institutional ownership

adversely affects a firms’ financial performance and value, while dispersed ownerships

improves a firm’s performance and mitigates agency problems.64 However based on

a recent study with regards to ownership structures and control mechanism in

Indonesia, it is concluded that the presence of institutional investors in the ownership

structure has an adequate control mechanism to improve return on assets.65

Difference of corporate governance around the world

Provided in the previous section that different institutional framework affects

difference in corporate governance around the world Other than that several factors

also play part in the basis of implementing corporate governance including (i) Social

and cultural values, (ii) the concept of corporation, (iii) institutional arrangement, (iv)

and lessons from evolution.

64

Randall Morck, Randall, Andrei Shleifer, and Robert W. Vishny, ‘Management ownership and

market valuation’ (1988) 20 Journal of Financial Economics 293-315.

65

Nila Firdausi and Chitra Sriyani De Silva Lokuwaduge, ‘Do Ownership Structures Really Matter? A

Study Of Companies Listed On The Indonesia Stock Exchange’ (2017) 24 Asia Pacific Development 5.

20Social and cultural values differ substantially from one country to another. For

example, Anglo-American countries tend to have a more individualistic value set than

many other countries (Hofstede 2001). 66 However recently countries that are not

form Anglo-American also have shifted their view of their institutional framework

towards market-oriented as can be seen by the emerging hostile takeover that

occurred in both countries.67

Secondly the concept of the company, whether it is viewed from the

perspective of the stake-holder model or the shareholder value model. Third, the

institutional arrangements as previously discussed whether the countries adopt the

market-oriented system or the network-oriented system. Lastly, lessons from

evolution where corporate governance will develop and incorporate lessons from the

past overtime.

Conclusion

In theory, the role of hostile takeover in the context of market for corporate

control is a sign of strong corporate governance and takeover rule. This is because it

requires an effective capital market for hostile takeovers as a monitoring mechanism

to function.68 In light of this, good corporate governance has always been an issue in

Indonesia as it is considered weak in comparison with other South East Asian

Countries. Hostile takeovers in the context of market for corporate control offer

solutions to weak corporate governance namely (i) strengthening protection of

minority shareholder (ii) promoting wealth maximization of company and (iii)

objectively monitoring management efficiency. Firstly, Henry G Manne remarked that

hostile takeovers give small shareholders power and protection commensurate with

their interest in corporate affairs. This is the solution for small shareholders’

insignificant control relationship with corporate management. 69 As stated by Sudi

Sudarsanam, a well-developed regulatory regime for the market for corporate control

66

Geert Hofstede, Culture’s Consequences: International Differences In Work-Related Values (second

edition, Sage Publications 2001) 2.

67

Armour, Jacobs & Milhaupt (n 14) 12.

68

Sudarsanam (n 23) 56.

69

Manne (n 8) 13.

21increases the scope of competition for corporations and empowers shareholders.70

Secondly, hostile takeover is said to promote wealth maximization of company. A

number of studies have claimed that countries with takeover laws that allow the

companies to easily install anti-takeover defenses have negative productivity and

profitability.71 Further studies also find that hostile takeovers are expected to create

higher value than friendly ones. 72 Based on such premise hostile takeovers can

improve the performance of the targeted company, providing a corrective mechanism

for replacing under-performing managers and often the threat of a hostile bid by itself

can boost up performance of the target company.73 Lastly, hostile takeover is claimed

to give access to public to objectively monitor companies ‘management. Management

can be disciplined by competition in the market for corporate control and provide

public a mechanism to objectively monitor companies’ management.74 Consequently,

in theory, hostile takeover in the context of market for corporate control can help

Indonesia attain stronger corporate governance.

After scanning through the aforementioned literature, it can be argued that

the role of hostile takeover as market for corporate control is a sign of strong

corporate governance and takeover rule. Even in countries with concentrated share

ownership that previously showed no sign of allowing hostile takeover such as Japan

and India have shifted their view towards enabling the implementation of market for

corporate control in order to strengthen the protection of minority shareholders as

well as monitoring managements’ efficiency. Despite the benefits, there are also cost

in implementing hostile takeover. An active market for corporate control is not the

main characteristic of either company law reform or financial and economic

development. There is possibility of harmful implication the growth prospect in

developing countries affected by the economic and social costs associated with

restructuring driven by hostile takeover bids. The market for corporate control play

70

Sudi Sudarsanam (n 23) 56.

71

Bertrand and Mullainathan (n 26) 11.

72

Balachandran, Balasingham and Duong, Huu Nhan and Luong, Hoang and Nguyen, Lily (n 27) 8.

73

Sudarsanam (n 23) 55.

74

Bebchuck and Fried (n 45) 14.

.

22You can also read