Hosking Post Taking on the blob - a case study in active engagement (Dec 2021) - Tandem - At Length, or How long is the Cycle (Nov 2021) The ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Hosking Post

• Taking on the blob – a case study in active

engagement (Dec 2021)

• Tandem – At Length, or How long is the

Cycle (Nov 2021)

• The Green Energy Revolution – trying to

see the wood for the trees (Oct 2021)

1

Hosking Post

Taking on the blob

A case study in active engagement

1

TAKING ON THE BLOB 1

Publicly-listed corporates are at a disadvantage. Unlike private firms, public companies face

intense and increasing scrutiny from an array of observers, intermediaries and other helpers.

Proxy advisors, institutional investors, environmental groups, politicians and NGOs are all now

vocal in lobbying the public company. A consequence of this trend is that boards of public

companies spend more time responding to the ever longer compliance agenda than in stewarding

the core business. Whilst this might (or might not) be appropriate for an oil major, many small-

and mid-cap public companies are increasingly disadvantaged. This is galling for practitioners of

public equity investing such as ourselves because asset allocators appear, inconsistently, to

accept differing standards of behaviour in the public and private spheres: in high-fee private

equity investments all manner of ruthless, goal-orientated behaviours are not just permissioned

but actively incentivised. Yet in the public equity bucket we see a relentless ratchet of compliance.

The result is a pattern of ‘lost’ public companies where the original corporate purpose is obscured

by a muddy Blob that has evolved in reaction to various external pressures.

Private equity has ruthlessly exploited this compliance arbitrage to take over these lost corporate

souls. Once private, these companies are then re-invigorated by refocussing management on the

core business, with incentives reset outside the harsh public glare. The public-to-private-merry-

go-round often comes full circle when, often just a few years later, these same companies

reappear, at higher valuations, to be re-sold to the good old public equity investors. Whilst this is

not particularly ‘new news’ – and we abstain here from commenting on the societal level inequality

driven by this low-to-high fee enrichment process – the opportunity for public market investors is

to resist this patsy-at-the-table position through the practice of genuine active management. By

joining forces with other shareholders it is possible to cut through the Blob and have a real impact.

1

Blob is a phrase made popular by UK politician Michael Gove

2

Foxtons: a £1bn brand

Foxtons is an ongoing case study of this approach. As an exceptional, category-defining private

company it ticked many of the lollapalooza boxes with a founder-led culture and win-win

stakeholder incentive framework that led to industry dominance. With positive capital cycle

tailwinds from a consolidating UK estate agency market (see quarterly report) and a leading

deployment technology platform (the MyFoxtons portal has over 700,000 active users), Foxtons

is well-positioned to transition into a digital-first agent model. However, its 8-year history as a

public company has seen the original sense of corporate purpose slowly calcify.

Founded in Notting Hill by Jon Hunt in 1981, Foxtons is one of the most recognised real estate

brokers in London and the South-East of England. Built on a brash, high-energy, sales-led

culture, the model historically generated c.2x the profitability of peers whilst simultaneously

achieving c.8% higher average selling price for clients than what was achieved by traditional

brokers: a client-centric, win-win business model. It achieved this result by putting the client – the

house seller – first. Traditional agency models contain an inherent conflict between the competing

interests of the vendor and purchaser. Although it is the vendor that pays the selling agent’s fees,

traditional agents often appear to act on behalf of the purchaser. In explaining the Foxtons’ model,

an early Foxtons pioneer relayed the following story:

“I used to go to dinner parties in Notting Hill where people would say to me ‘I hate Foxtons. They

are too pushy. I would never buy from them. But I would let them sell my house’. This was gold

dust for me. All I wanted were listings as that is what you ultimately get paid for. And the people

that give you listings are the people selling their house!”.

Sadly, for Foxtons, the Jon Hunt culture has started to wilt. Post-listing, a top heavy and

expensive C-suite has overseen a continuous ceding of market share to more nimble private

players. Where Foxtons used to be the number one agent by a large margin, it has started to

3

lose ground in key central London postcodes, despite having some of the best branch locations.

This has led to falling sales and profits. Shortly after its IPO in 2013 the share price peaked at

376p, representing an enterprise value of £1 billion – a multiple of around 20x the £45m of pre-

tax earnings. Fast forward to today and the business is on track to earn £15-20m of pre-tax profits

with the enterprise value shrinking to c. £100m. We are cognisant of the challenges facing the

group but see the £900m of value erosion post-IPO as an opportunity. Over the past two years

we have acquired c.13% of the company, doubling our stake during a Covid-related share issue

at 40p in May 2020.

Source: Hosking Partners, FactSet. Share price from 20 Sep 2013 to 09 Nov 2021. The portfolio holds this security. Not all purchases have been

included. This does not represent all the securities purchased or sold. Further details of the calculation methodology and a list showing every holding’s

contribution to overall performance during the period is available upon request. Past Performance is not a reliable guide to future performance.

Driving Board change

The market share losses, profitability declines and £900m of equity shrink post-IPO appear to

have had little impact on the board of Foxtons or the executives it oversees. The Board actually

increased CEO Nic Budden’s pay over this period, and in 2020 Mr Budden (in situ since 2014)

earned £1.6 million in total compensation – an extraordinary perverse reward structure that has

been overseen by a complicit board which collectively own less than 1% of the outstanding

shares. The incentive alignment issues are clear as day and we venture that no private equity

firm would have permissioned such rewards for failure.

4

Motivated by the inequity of management compensation, Hosking Partners engaged with the

board of Foxtons; the aim being to re-set the incentive framework. In early 2021 we started a

robust campaign of board lobbying. Initially this took the form of discussions with the (then)

chairman. An underwhelming response led us to write to the board in its entirety on three separate

occasions, setting out our view of the unacceptable nature of the CEO rewards and questionable

capital allocation. These letters are available upon request. Concurrent with this board pressure,

we reached out to other shareholders and encouraged them to censure management. At the

AGM over 40% of shareholders voted against the CEO’s remuneration report. In a letter of 17

May 2021, we called for the chairman to conduct a full review of Mr Budden’s tenure as CEO.

This was closely followed by a letter on 4 June where we expressed our disappointment at a

Foxtons capital markets event which failed to address our concerns over market share and

profitability erosion.

Having been frustrated by the lack of board responsiveness, we entered into a full-scale

collaboration with a group of other large shareholders accounting for around one third of the share

capital. 2 This was notified to and discussed with the UK Takeover Panel to avoid so-called concert

party rules – rules that put off most public equity investor engagement in such dialogue. In this

letter, dated 30 June, we requested an opportunity to discuss replacements for the chairman and

non-executive appointments. On 7 July, chairman Ian Barlow announced his decision to resign

and two months later it was announced that veteran property executive Nigel Rich would take

over as the new chairman.

2 Platinum Asset Management, 3G Capital Management, Catalyst Partners.

5A new chapter

As a former CEO of Hong Kong Land, chair of Hamptons International and also Segro PLC, Mr

Rich brings vast experience and a value creation mindset. He has already moved to appoint a

new non-executive in the form of Peter Rollings, a former Foxtons executive from the Jon Hunt

heyday, who joined on 1 December. This appointment should lead to an aggressive focus on

regaining market share. There are encouraging signs Mr Rich sees value in the business. He has

bought 500,000 shares in the past 6 weeks alone, whilst Mr Rollings has also recently bought

shares. Should Mr Rich succeed in reinvigorating Foxtons, the return on his investment could be

substantial. Pruning of the excessive central costs (a major feature of the Blob) together with a

return to historic transaction levels in the sales and rental sector could see the business achieve

pre-tax earnings north of £60 million. With a net cash balance sheet and current enterprise value

of just £100m the upside is clear. Not least, given the huge digital customer acquisition costs

required to replicate over 700,000 MyFoxtons portal users; conservatively we believe the

embedded value of the customer base alone accounts for more than the current equity value.

We think the value of this customer set will not be lost on potential acquirors of the business,

representing probably the best digital footprint in UK residential real estate. Whilst it is unlikely

the business would return to its prior peak multiple of 20x, an 8x multiple of the recovered

earnings would see the investment return near fivefold.

Victory is not assured. But without robust and concerted engagement, the value present in

Foxtons, and many mid- and small-cap equities, will continue to pass into the private equity

sphere. With the private equity boom showing no sign of slowing, public equity investors will be

required to be ever more active. We stand ready for that task, motivated by the prospect of

retaining for our clients the significant upside rewards.

Django Davidson and Sam Traill

December 2021

6Hosking Post

Tandem – At Length, or How

Long is the Cycle

1As we write, in the final quarter of 2021, the world is waking up from Covid-induced lockdowns,

global leaders are meeting at the COP26 Conference, and newspaper headlines are dominated

by the twin topics of supply chain disruption and energy price spikes. The inside pages meanwhile

are engaged in endless debates about inflation - what it means, how to measure it and whether

it is “transitory” (as Federal Reserve Chair Jerome Powell puts it) or longer lasting.

Against this backdrop, a number of stocks in the Hosking Partners portfolio have enjoyed some

long-awaited strong performance. In particular this applies to capital intensive companies,

whether those in “old economy” industries or, similarly reliant on their balance sheets, banks.

They include names such as Pacific Basin and Diana Shipping (both in dry bulk shipping), mining

names such as Teck, Freeport, First Quantum and Alcoa, oil stocks such as ConocoPhillips,

Apache and Canadian Natural Resources as well as a collection of companies in such disparate

areas as car rental (Avis Budget even before its meme explosion) and silicone (Ferroglobe).

Among our banking exposure, Bank of America and Wells Fargo have made strong contributions.

There might be a temptation to reach for today’s news topics of inflation (transitory or not),

disruption from the energy transition or logistics bottlenecks to provide the reasons why these

stocks have done well, but as students of behavioural finance we should be alert to the false

allure of availability bias. Rather what all the aforementioned stocks have in common - whether

they sit within shipping, mining, oil and gas or banking industries - is that they have suffered long

periods of poor returns on capital. This has led to investment being turned off, and now those

returns on capital are picking up sooner, to the surprise of the market. This can all be foreseen

by rudimentary capital cycle analysis.

Briefly described, the capital cycle framework predicts that an industry with high returns on capital

attracts new entrants, enticed by the prospect of enjoying those high returns. The consequence

2of this is that the rising competition causes returns to fall, eventually in some cases to below the

cost of capital; investment declines, capital stock becomes obsolescent, firms consolidate,

withdraw or close down. In time, an improving supply side causes returns to rise above the cost

of capital and the cycle begins again. At the same time, the equity market is tracking its own

cycle: investors are optimistic when returns are high, but share prices fall as industry returns

suffer from rising competition, reaching a nadir as returns bottom and capital exits, and finally

share prices pick up in anticipation of rising returns again. The opportunities for capital cycle

investors arise in two broad areas. Firstly, where the market anticipates the high returns of certain

companies will turn down sooner than in fact they do. Secondly, where the market underestimates

the likelihood of returns recovering in beaten up industries, when the supply side is already

improving.

Chart 1: The Capital Cycle

Source: Hosking Partners

3This chart highlights the two valuation anomalies which capital cycle analysis helps identify. We

have started with the example of capital intensive industries surprising the market with attractive

returns following historic underinvestment. While the Hosking Partners portfolio contains a

greater share of such capital intensive stocks than is the case with many of our competitors, a

glance at the largest positions in our portfolio will see names such as Amazon, Alphabet, Tinkoff

Credit, Costco and TSMC, all showing higher and more stable returns. As any contrarian needs

to be, we are foxes rather than hedgehogs1. What makes the capital cycle so versatile as a tool

is that as well as providing a framework for investing in companies with low but volatile returns

which are likely to recover sooner than the market credits, it also highlights the opportunity in

companies with high and stable returns which enjoy barriers to the supply of new capacity which

will mean that those returns will resist the gravity of mean reversion for longer than their share

price suggests. What we are less good at is investing in companies without positive returns in the

past and only the prospect of positive returns at some distant point in the future: we leave those

to cleverer investors.

Considering the example of our capital intensive stocks which have recently performed well, the

reasons for the historic poor returns on capital date back in many cases to the years before the

Global Financial Crisis, when the combination of cheap and plentiful capital, the emergence of a

China-driven commodity “supercycle” and wasteful capital allocation by many management

teams led to massive overexpansion and the creation of excess capacity. This was later cruelly

exposed by the ensuing worldwide recession. Asset lives are long: it may take a decade for a

mine to receive necessary permissions and complete necessary capex before any revenues are

generated, followed by decades of production, and at least a couple of years will pass between

an order being made for a ship to be built and it being delivered, following which it will have a

Archilochus, via Isaiah Berlin: πόλλ' οἶδ' ἀλώπηξ, ἀλλ' ἐχῖνος ἓν μέγα - a fox knows many things, but a hedgehog

knows one big thing.

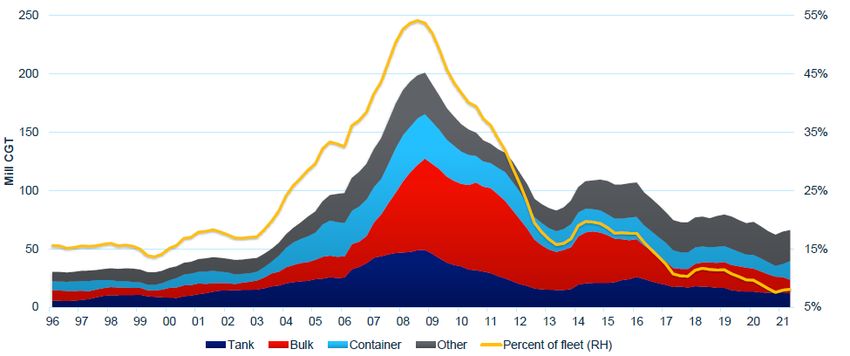

4useful life of 20 years. Shipping provides a vivid example of the length of time it has taken for the

supply demand equation to have balanced: the size of the global order book for new shipping in

relation to the scale of the fleet already on the water has been in decline for ten years (from a

peak as high as 50%), but in absolute terms the size of the fleet has continued to grow, and it is

only in recent years that new shipping has been growing at a rate which is the same or less than

demand for shipping.

Chart 2: Orderbook for World Merchant Fleet

Source: Clarksons Research – in million compensated gross tons (CGT)

In other cases, overcapacity comes from state actors such as China prioritising investment as a

strategic objective for reasons of economic self-sufficiency. Aluminium is the stand-out example,

with the energy generated by stranded coal assets in Western China being converted into

aluminium which can both be consumed locally and exported globally, destroying the returns on

capital of international competitors for the past two decades. China’s recent announcement that

it is committed to CO2 emissions peaking by 2030 and carbon intensity reducing by 65% over the

same period provides some comfort that a turning point may be on its way. In the meantime, the

energy crisis being experienced in China is providing a short-term benefit to Hosking Partners’

5portfolio constituent Alcoa, as less Chinese aluminium is dumped on world markets. Viewed

through the capital cycle lens, however, it becomes clear that the China power squeeze is the

result of longer-term underinvestment in traditional energy markets globally, in the mistaken belief

that renewable capacity would be able to scale quickly to create replacement capacity more

cleanly and with lower prices.

In this way, the capital cycle and an ESG focus work together: industries are punished for poor

historic investment performance in the former framework and they are also rationed for excessive

emissions according to sustainability criteria. The result is the same - an extended period of

higher returns. Restricted supply of reliable power generation meets recovering demand post-

Covid, resulting in high returns for LNG and coal, as well as for what aluminium smelting capacity

in developed markets has managed to survive two decades of dumping by Chinese competitors

who have now been turned off (for a while at least). A similar dynamic is at play in silicone

markets, expressed through our investment in Ferroglobe.

Faced with examples of such obstinate overcapacity it is no surprise that over the last decade

capital has been attracted to opportunities in less capital intensive industries. Here, intangible

assets cannot be replicated so easily and the prospect of increasing demand is enough to offset

worries about capacity surpluses. Investment pundits may characterise this flow of capital as the

triumph of “growth” over “value”, or of “quality” over “cyclicals”. In reality it is simply the

punishment of certain industries and their management teams for squandering investors’ capital,

and the rewards being handed instead to other industries which have either earned higher

valuations through careful stewardship of capital, or at least the promise to do so.

Such punishment takes the form of starving the capital base of the investment needed to grow,

or at least maintain, production in old economy industries. Equity valuations are depressed, and

access to the capital markets is restricted as prospective returns on new investments are

6extrapolated from rock-bottom levels. The cure for low prices is low prices, however, and in time

the structural underinvestment leads to higher returns for what capital that remains.

A key question for investors, then, is how long returns remain in the doghouse, in effect what is

the (wave)length of the capital cycle? For Hosking Partners specifically, the question is whether

and how quickly we should be taking profits in these winners, or how much further is there to

run? The answer varies from industry to industry, depending in large part on asset lives, as the

passage of time is needed for capital stock to be depreciated, but other factors can extend the

time in the doldrums. In the case of shipping, for example, the arrival in the middle of the last

decade of private equity investors trying to anticipate the inflection in returns resulted in a self-

defeating wave of new capacity. This extended the downcycle by several years, the stocks

continued to trade at a discount to replacement cost and the investment tap has only flowed at a

trickle.

In contrast to these examples of excess capacity, supply constraints can cause returns to recover

sooner than priced by the market and to be sustained higher and for longer. For example, a lack

of suppliers to equip new entrants may hold back new capacity. As a case study: since the

bursting of the US housing bubble and the collapse in demand for lumber, there are now only two

manufacturers of sawmill equipment, resulting in long lead times for new sawmills to come on

line. In Europe, paper manufacturers such as UPM-Kymmene have finally realised there is little

point chasing volumes in the face of secular demand decline and have been closing down paper

mills ahead of time.

Alternatively, the supply constraint may derive from funding being withheld. Depressed equity

valuations rule out the issue of shares to fund expansion, while lenders have long memories and

may restrict credit for expansion long after industry returns have recovered: in the case of

shipping, many of the northern European speciality lenders who fuelled the pre-Lehman boom

7have gone bust while others have closed their shipping desks. Other stakeholders may impose

supply constraints, particularly in the case of capital intensive industries which face emission

challenges: governmental authorities’ cancellation of oil pipelines in North America and

imposition of restrictions on new drilling have held back oil production and brought on industry

consolidation.

Even the prospect of future regulations can have an impact upon supply: shipowners are reluctant

to order new ships if they do not know what future technology specifications will be needed to

comply with changing emissions regulations over the course of their economic life. Geopolitics

plays its part too: as tensions lead to local supply chain networks replacing global ones, capacity

is reduced by such displacement.

Chart 3: Historic return on capital for selected capital intensive companies

Alcoa CFROI % Pacific Basin Shipping CFROI %

10.0 20.0

17.5

7.5

15.0

5.0 12.5

10.0

2.5 7.5

5.0

0.0

2.5

-2.5 0.0

2008

2019

2001

2002

2003

2004

2005

2006

2007

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2020

2017

2021e

2022e

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2018

2019

2020

2021e

2022e

Anglo American CFROI % Bank of America CFROE %

15.0 30.0

12.5 25.0

20.0

10.0

15.0

7.5

10.0

5.0

5.0

2.5 0.0

0.0 -5.0

2004

2009

2001

2002

2003

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021e

2001

2002

2003

2004

2005

2006

2007

2008

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2022e

2021e

2022e

Source: Holt.

8The key benefit of using the capital cycle as an analytical framework through which to view

industries’ returns and valuations is not only that it explains the link between supply of capital,

future returns and asset valuations, but also that by doing so it creates the necessary confidence

for us as investors to accumulate ownership positions in companies when returns are at trough

levels. Being contrarian is by definition lonely, and being contrarian merely for its own sake leads

almost inevitably to value traps. However, combined with a bottom-up approach, the capital cycle

provides a rationale for making a bet against consensus just when the odds are most attractive

and the course of play is about to switch. Of course, timing is never perfect (and anyway, perfect

is the enemy of the good), but with respect to those commentators who say that to be right too

early is to be wrong, we say that you will never own a stock at the bottom unless you are prepared

to be early. Our diversified portfolio and our long-term performance fee help to provide scope for

such behaviour and to reinforce the merits of focusing on the longer horizon.

Leading on from this, the capital cycle also gives us the confidence to say that while the high

returns currently being enjoyed by these capital intensive companies are not permanent and will

in time be eroded as new capacity is inevitably attracted in pursuit of those high returns, they may

not be as short-lived as some valuations suggest. Market participants who measure their own

performance over the shortest of time periods are quick to characterise the earnings power

currently being enjoyed by these companies as a one-off blip due to the transient factors in

today’s newspapers (inflation fears, energy prices, port delays etc). At Hosking Partners, on the

other hand, we have an eye on the bigger picture: what are the constraints on the entry of fresh

capital and so what are the implications for capacity expansion? Analysts may try to estimate

future demand to the last decimal point, but we are happy making broad estimates of supply

based on more easily observed phenomena such as capital markets activity, capex projects and

hiring announcements, all of which give forward notice of the arrival of new supply, or lack thereof.

9Chart 4: Capital spending-to-depreciation ratio for developed market mining stocks

4.5

4.0

3.5

3.0

2022 E

2.5

2021 E

x

2.0

1.5

1.0

0.5 Parity

0.0

52 56 60 64 68 72 76 80 84 88 92 96 00 04 08 12 16 20

Capital Spending : Depreciation

Source: Empirical Research Partners Analysis. Metals & Mining stocks - U.S. stocks used as a proxy for developed markets prior to

1987. Capital Spending-to-Depreciation - aggregate data smoothed on a trailing six-month basis.

The noise which results from false connections being made between daily price movements and

companies’ intrinsic values throws up opportunities. If profits really are one-offs then a low

valuation multiple should be applied, which is why cyclical industries often experience tiny p/e

multiples when profits are at their peak, and nose-bleed multiples when profits are lowest, if not

actually losses. But if supply constraints (also known as barriers to entry) mean that returns will

persist a while longer before they revert to the mean - and no doubt then overshoot to the

downside - then a valuation anomaly is waiting to be exploited.

By way of vivid portfolio example, Pacific Basin, a dry bulk shipping company, is trading on a

forward p/e of 3.2 and its chairman has just spent half a million dollars adding 9% to his existing

ownership of the stock. This kind of insider behaviour should be catnip to the patient outside

investor, and is to the four portfolio managers who own this within your portfolio.

Luke Bridgeman

November 2021

10Hosking Post

The Green Energy Revolution

Trying to see the wood for the trees

1Fund managers receive a lot of advice from the “sell-side”. During the serial lockdowns of the

past 18 months the proportion of that advice which obtains to improving the “ESG” scores of

fund managers has leapt, as far as this writer can tell, to about 70% of all incoming material.

Almost all of it relates to the E of ESG, that part of the acronym which is most difficult to pin

down. Whereas the Hosking Partners investment team has always been motivated by a belief

in the positives of a cleaner environment, sustainability of business models and engagement

with management that improves outcomes, for us this was a behavioural activity motivated

by the likelihood that these objectives enhanced client outcomes. However, ESG is now A

Thing, and as with all nouns this thing should be capable of description in specific terms, just

as a carrot is an orange vegetable with a green top. Notwithstanding ESG’s new “Noun”

status, definitional issues still abound (for example, scope and basis adjustments to CO2

emission measurements, or ambiguity related to the externality that is represented by the

Chinese thermal power industry), not to mention political questions of how to settle multi-

dimensional trade-offs, leading to extra levels of uncertainty, complexity and confusion.

Although the two premises of climate change – (1) global warming and (2) the degree of

responsibility of CO2 emissions for this – are more the product of empirical observation and

inductive reasoning than objective proof, they have increasingly been adopted as such by

society. More relevant to us is the growing acceptance of this diagnosis and associated

prescriptions by our clients, as well as by investee companies. Commercially then, a firm like

Hosking Partners needs to make certain adjustments to its processes and these, as you

would expect, are being made. However, as thoughtful investors we like to think about this

development in conceptual terms, such as what are the likely consequences of the current

paradigm, can we predict some of them and how can we ensure a firm like Hosking Partners

enjoys a competitive advantage along the way. On the face of it this is not a straightforward

task; for example, many of the alternative technologies associated with the need to address

the threat of climate change by reducing carbon emissions are as complex as those which

have underlain the digital transition in business practices. These would appear to require

detailed attention from focused specialists rather than generalist all-rounders with

backgrounds in the social sciences. On the other hand, the ability to see connections which

are not visible to a more focused study is an advantage: who would have predicted that the

high price of gas would cause the UK government to offer subsidies for the production of CO2

(vital for the food industry and a by-product of ammonia plants idled due to high feedstock

costs)? The ability to hop between silos and find opportunities in the cracks between them

should present us with an advantage here.

2But wait a second, the climate change revolution is different from previous technological

revolutions. One recent corporate presentation invoked the transition from fixed line

telephony to a mobile framework in India as a useful analogy for the present required

transition. What this fails to reflect, however, is that most waves of innovation represented

leaps forward in efficiency, and were exercises which involved consumer choice and

competitive markets. The energy transition is not quite the same, representing a cultural shift,

for sure, but also drastic interventions from public authorities which distort pre-existing price

structures via taxes, subsidies and other constraints and incentives. Whisper it quietly, but in

moving towards ditching fossil fuels (albeit for understandable reasons) countries are

replacing a highly efficient energy supply system with a less efficient alternative. It is an

alternative which is undefined in terms of activity mix, but which in any event will require far

more inputs from an equally long supply chain, all the links of which involve economic activity

and their own associated emissions. The fact that the supply of the majority of the world’s

solar panels involves the burning of large quantities of Chinese-sourced coal is simply an

extreme example of a general phenomenon. It is entirely possible that one unintended

consequence of the energy transition may be not just more expensive energy, but also

actually accelerated CO2 emissions. Already electricity prices in the UK are 40% higher than

in the counterfactual absence of “green” policies. And that price premium is before the recent

explosion in the gas price and the consequently greater relative attractiveness of coal as a

source of cheap backup power!

Partly as a result of pressure from institutional investors, our universe of investable

companies find themselves in two transitions simultaneously, namely both the digital

technology and climate transformations. The former is voluntary/commercial, the latter is not.

The oil company BP has embarked on a 50 GW renewable energy investment (by 2030) and

Daimler AG envisages being all electric vehicle based by 2030, having ceased all investment

in internal combustion engine vehicles as early as 2025. The pitch to investors by both these

firms is that this mix shift will be accomplished seamlessly and will be associated with

business quality improvement, i.e. higher normalised ROCE and lower cyclical volatility. If

either were achieved this would undoubtedly produce much higher valuations. The problem

is that this forecast does not pass the sniff test. After all, BP and Daimler didn’t produce cost-

of-capital-earning businesses when they had just one technology to manage! For a company

like BP a dual analysis is appropriate. Investors should value the growth-oriented renewable

expansion (8%-10% returns according to the company, less according to other observers) on

a different spreadsheet to the harvesting of returns from the depleting fossil fuel asset base.

It is likely that any shareholder value gains will be produced not by the new investments but

3by the massive free cash flows produced by (definitely) low capex and (possibly) higher oil

and gas prices in the fossil fuel division. Already BP has raised its dividend and started share

buybacks. This pattern is likely to be repeated elsewhere, in our opinion, with shareholder

value creation via supply-constrained mature activities turbo-boosted by inelastic consumer

demand for the product in question.

While previous technology revolutions produced lower selling prices for consumers via

operating efficiency (who can forget the Federal Reserve’s hedonistic quality adjustments for

improved product capabilities?), the energy transition is likely to have the opposite effect.

Firstly, as the Jevons paradox works backwards, there will be higher levels of inflation due to

reduced production (relative to demand) of price inelastic products. Second, the energy

transition will be funded by price distortions introduced from Government enthusiasm to

identify a new source of excise revenue and impose “green taxes” on consumers on the basis

that this will change behaviours (on the assumption that alternatives to those behaviours are

available, not always the case). It also seems likely that over time more geopolitical attention

will shift to China’s relentless expansion of its domestic coal industry. This has the potential

to reverse the globalisation to which most companies and investors have become addicted,

most likely as a result of “carbon border adjustment tax” imposed by developed markets on

Made in China products.

It is clear that the energy transition and its consequences will play out over many years. These

consequences will often be unintended and produce a significant number of investible shocks.

Many of them are likely to arise from the price instability caused by unintended shortages or

surpluses, and will be difficult to predict via specialist-type analysis. The corporate ecosystem

has become much more unpredictable and complex, and with government-imposed targets,

quotas, taxes and the changes made to them via political expediency, the environment that

investors have to navigate will be dominated by the only safety valve in place, namely

unexpected price moves, many of which may be in commodity type products, and the growing

prevalence of temporary spread-based corporate profits from price arbitrage activity.

Jeremy Hosking

October 2021

4Contact Details

Hosking Partners

2 St James’s Market

London SW1Y 4AH

Tel: +44 (0)20 7004 7850

info@hoskingpartners.com

Legal & Regulatory Notice

Hosking Partners LLP (“Hosking”) is authorised and regulated by the Financial Conduct Authority and is also registered as an Investment Adviser

with the Securities and Exchange Commission. The investment products and services of Hosking Partners LLP are only available to Professional

Clients for the purpose of the Financial Conduct Authority’s rules and this document is intended for Professional Clients only. “Hosking Partners” is

the registered trademark of Hosking Partners LLP in the UK and on the Supplemental Register in the U.S.

Opinions expressed are current as of the date appearing in this document only. This document is produced for information purposes only and does

not constitute advice, a recommendation, an offer or a solicitation to purchase or sell any securities (including shares or units of any pooled fund

managed or advised by Hosking) or any other financial instrument or to invest with Hosking or appoint Hosking to provide any financial services, nor

shall it form the basis of or be relied upon in connection with any contract or commitment whatsoever. In addition, this document does not constitute

legal, regulatory, tax, accounting, investment or other advice.

Opinions included in this material constitute the judgment of the author at the time specified and may be subject to change without notice. Hosking

is not obliged to update or alter the information or opinions contained within this material. Hosking has taken all reasonable care to ensure that the

information contained in this document is accurate at the time of publication; however it does not make any guarantee as to the accuracy of the

information provided. While many of the thoughts expressed in this document are presented in a factual manner, the discussion reflects only the

author’s beliefs and opinions about the financial markets in which it invests portfolio assets following its investment strategy, and these beliefs and

opinions are subject to change at any time.

Any issuers or securities noted in this document are provided as illustrations or examples only for the limited purpose of analysing general market or

economic conditions and may not form the basis for an investment decision nor are they intended as investment advice. Such examples will not

necessarily be sold, purchased or recommended for portfolios managed by Hosking. Nor do they represent all of the investments sold, purchased

or recommended for portfolios managed by Hosking within the last twelve months; a complete list of such investments is available on request.

Partners, officers, employees or clients of Hosking may have positions in the securities or investments mentioned in this document.

Certain information contained in this material may constitute forward-looking statements, which can be identified by the use of forward-looking

terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “target,” “project,” “projections,” “estimate,” “intend,” “continue,” or “believe,” or the

negatives thereof or other variations thereon or comparable terminology. Such statements are not guarantees of future performance or activities.

Due to various risks and uncertainties, actual events or results or the actual performance may differ materially from those reflected or contemplated

in such forward-looking statements.

Please note that different types of investments, if contained within this material, involve varying degrees of risk and there can be no assurance that

any specific investment may either be suitable, appropriate or profitable for a client or prospective client’s investment portfolio.

This document may include statistical data and other information received or derived from third party sources, and Hosking makes no representation

or warranty as to the accuracy of that third party data or information. The information contained in this document is strictly confidential and is intended

only for use of the person to whom Hosking Partners LLP has provided the material. No part of this report may be divulged to any other person,

distributed, and/or reproduced without the prior written permission of Hosking Partners LLP.

5You can also read