Griffin Energy Ecosafe Biodiesel Summary Investor Presentation - GREEN July 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Griffin Energy

Ecosafe Biodiesel Summary

Investor Presentation

July 2021

GREEN

1

Executive Summary GREEN

Ecosafe, an established energy company, has identified an opportunity to enter the biodiesel market in Europe

for a low entry cost, with a significant opportunity to take advantage of the growing demand for biodiesel.

Their experienced team of Managers and Engineers have an option to acquire and operate a state-of-the-art fully automated Bio Diesel Plant and and tank farm

in Mallorca. Griffin Energy has reached an Agreement In Principle (AIP) to enter into a Joint Venture (JV) with EcoSafe. Griffin will provide all financing to facilitate

the purchasing, renovation, and operation of the site, and will employ the EcoSafe team. Griffin will create a new Spanish company which will be wholly-owned

by Griffin Property Group Ltd.

The Opportunity

CHECK Growing biodiesel marketplace and global economy recovery.

Project Highlights

CHECK Purchase and recommissioning of a biodiesel production facility at 25% of its build cost.

CHECK Production Capacity of 35,000 tons per annum and full production within six months Opportunity

CHECK Swift repayment of capital. Participation in a fast growing European biodiesel

marketplace with increasing demand

Investment Overview Location

CHECK Initial investment of €2 million to secure the site and plant and tank farm. An additional €3m Mallorca, Spain

for plant upgrades, distillation tanks and feed stock.

Biodiesel Produced

CHECK Indicative rates of return (IRR) upwards of 25%.

110,000 litres a day

CHECK Sales into European and domestic market where demand outstrips supply.

Commissioning/Operation

CHECK Feedstock secured.

Within six months of purchase

Unique Selling Points Total Capital Required

€5 million (c. 4.31 million)

CHECK The only biodiesel production facility in the Balearic markets representing a captive source of

feedstock and sales, with global demand outstripping supply by 2 to 1. Internal rate of return

CHECK Statutory regulations mean demand for biodiesel will only increase. Upwards of 25%

2

Spanish Biodiesel Market GREEN

Angle-right The biodiesel market is driven by legislation designed to reduce emissions and improve air quality. The

EU Renewable Energy Directives (RED I & II) set out the targets and a timetable that all European

states must achieve, mandating that all EU member states to source 32% of their energy from

renewable sources by 2030. Specifically the mandate requires that all transport fuels must reach 10%

by 2020 and 14% by 2030. Within this mandate individual member states have also set additional

targets that exceed these levels.

Angle-right The Balearic Islands (including Mallorca) “green manifesto” set a target for 2050 to reduce

emissions by 90%, increase energy consumption by 40% compared to 2005 levels and use 100%

renewable energy is anticipated to contribute to demand growth. There are over one million vehicles

registered in the Balearics of which almost 40% are diesel – first on the governments list for eventual

100% elimination by 2050.

Angle-right The government is working hard towards making public transport on the island more sustainable, with

the fleet of EMT Palma buses currently being considered. While too costly to renew the entire fleet with

electric vehicles, they are considering vehicles powered by cleaner energy and with lower emissions.

Ecosafe’s Bio Diesel exactly fits their criteria, with the Companies production servicing less than 1% of

total Island consumption.

Angle-right Current sales of diesel in Europe are over 200 billion tonnes per annum. This therefore defines the

current biodiesel requirement at 20 billion tonnes per annum rising to 28 billion tonnes per annum by

2030.

Angle-right The EU is the world’s largest producer of alternative biodiesel production capacity and consumption,

with Spain among the top three Member States. Current European Biodiesel production only meets

50% of demand. This gives ample room for new entrants to the market.

Angle-right Globally, demand increases are higher. This affords considerable opportunity for export beyond Europe.

3

The Opportunity GREEN

Angle-right Entry into a growing market in renewable, sustainable fuel where demand outstrips supply by 2 to 1 at a

quarter of the cost of entry.

Angle-right A unique opportunity to acquire a virtually brand new, little used, state of the art biodiesel plant facility,

at less than half of the original cost and raw materials, being available at competitive prices. The plant is

German designed and built in 2005 at a cost of €14M with present day replacement cost of €20m.

Angle-right The plant was commissioned in Mallorca Spain in 2008 by local investors and banks. Its delivery

coincided with the collapse of the global financial markets and the recession that followed and longer

term impact on the Spanish economy and its inability to keep pace with biodiesel subsidy structures

that the rest of Europe adopted. The net result is that the plant has been dormant for most of its history.

The plant ultimately became part of a wider insolvency due to an inability to repay the loans on its €14

million build cost.

Angle-right The facility is the only compliant Bio Diesel plant within the Balearic Islands.

Angle-right Griffin Energy Ecosafe have negotiated with the administrators of the plant to purchase it out of

bankruptcy. In the time since the plant design and build the biodiesel market has evolved. Quality control

has become increasingly important and the economics of production have become tighter as feedstock

supply markets have evolved. As a result of this the plant does require two key upgrades, distillation

and methanol recovery. These upgrades will ensure that it has two saleable products, biodiesel and high

value technical grade glycerine. The upgrades will also reduce the cost of production by recycling the

methanol used in the production process.

4

Management Team GREEN

David Morgan – Chairman

David is a senior executive mechanical engineering background and Management team for delivery and Production Phases

international expertise as Chief Executive in energy process design and

technology. He has spent 25 years in the energy sector focused upon MICHAEL MALLABY (MSc, BEng, IEng, CMgr) – LEAD ENGINEER

waste streams. Successful business venture include coal reclamation and

– Seasoned business professional with 30+ years experience

recycling of marine fuels and oils. Former CEO of oil company, Marine Oil

USA working with – Accomplished Senior Project Management Engineering Consultant

– Prince2® Practitioner PMI - Risk Management Professional

Old National Bank, operating 51 secondary recovery crude wells with a – CITB : MAP HSE for Managers and Professionals CSCS Card Holder

production of 500 BBIs per month. Expanding the business throughout – Internal Quality Auditor BS EN ISO 9001Health & Safety OHSAS /

the US Henderson and Webster County regions. 8001 Implementation

CEO of Coal Processing Inc, USA, processing of coal mine tailings and Roberto Vasquez Lucerga – Consultant Engineer

reclamation. Specialist design and build of Autogenous Process Modules – Management team for delivery and Production Phases

to process reclaim coal from tailings at Australian Coal Technologies PTY. – Roberto has a long career as an engineer and operator of biodiesel

facilities in Europe and China. He has recently completed a Masters

Degree at MIT in Boston

Gary Taylor – Finance Director

José Ma Vicente Martorell – Senior Training Manager

Price Waterhouse trained Chartered Accountant. Results driven, – Presently SUEZ Key Account Manager

corporate finance all rounder with broad-based experience developing

– Sales Manager of SUEZ in Balearic Islands

and managing small business development teams in the North of England.

Successfully built a private small-regulated business with a proven – Responsible of public tenders

track record of raising funds for small PLC’s and Private Equity. Started, – Master in Water Management. Universitat Polit cnica de Catalunya

managed and advised small businesses on finance and business strategy. (2011)

– Master in Environmental Engineering. Institut Qu mic de Sarria IQS

(2000)

– Industrial Engineer. Universidad Ram n Llull (2001)

– Chemical Engineer. Institut Qu mic de Sarria IQS (1998)

5

The Llucmajor Biodiesel Plant GREEN

Angle-right The Llucmajor biodiesel plant cost in excess of €14m and

occupies an area of 2,592 square metres in the Son Noguera de

Llucmajor region.

Angle-right The plant is sized to obtain an annual production of

approximately 35 million litres of fuel.

Angle-right It will produce a biodegradable transport fuel which reduces

greenhouse gas emissions and dependency on conventional

energy.

Angle-right Utilising raw material from used vegetable oils so recycling a

highly polluting waste. All production will service the Balearic

market at the same price as conventional diesel.

Angle-right Testing and quality control are key elements in the success

of a biodiesel facility. All fuel produced must conform to the

EN14214 specification to achieve its full market value. To ensure

this constant testing is required at all stages of the production

process.

Angle-right The facility has its own state of the art laboratory facility.

The plan is to lease this facility to a separate company. As a

condition of the lease they will be responsible for all testing

requirements at a discounted rate to the market. By using an

external company we ensure impartiality and guarantee the

integrity of the testing data. The cost of testing in this manner is

equal to the cost of staffing the laboratory ourselves.

Poligono Son Noguera

07609

Illes Balears

Spain

6

Port Quayside Tank Storage Facility GREEN

Angle-right In addition to a leased tank storage facility which we plan to

use located at the airport and belonging to CLH Group, we have

further submitted outline plans to the Port Authority Director

to acquire a tank storage facility within a section of quay at the

Port of Palma.

Angle-right Currently this location has three disused tanks in situ.

Angle-right This facility would have a twenty year lease.

Angle-right When the plans are accepted this will allow us to receive

feedstock material directly from the delivering tankers, and

would eliminate Ecosafe storage, off loading and loading costs

at the Port, which would be incurred if alternatively we were to

lease a tank facility at the Port (in addition to the leased airport

facility) from CLH Group.

7

Logistics GREEN

Trucking Route from Port Tank Facility to Llucmajor

Port Loading & Unloading Tank Facility

Llucmajor

Bio Diesel Plant

8Logistics GREEN

Trucking Route from Llucmajor to CLH Blending Facility CLH Tank Farm and Griffin Energy

Ecosafe Blending Facility

Llucmajor Bio Diesel Facility

9Feedstock Supply GREEN

Consistency and quality of feedstock is essential for the business to succeed.

To this end supply contracts are available from the following sources.

Sources Volume

– International broker driven feedstock market – Unlimited 3-6 month contracts.

– Domestic UCO collection on the Island. – Up to 10 million litres a year, long term contracts.

Feedstock will be secured using these sources in excess of actual requirements to ensure consistency of

supply. Any surplus could then be sold into the market.

10Go-To-Market – Key Markets GREEN

There are three Go-to-Market opportunities for Griffin Energy Ecosafe to exploit:

1) 2) 3)

Balearics demand for Biofuels International Power generation and

in partnership with the CLH wholesale market Marine Markets.

Group (Global tankering and

logistics company).

1) Balearics demand for biofuels

CLH Group purpose built a 3500 ton tank and blending facility exclusively for the Llucmajor plant in 2006 in order to service the major oil

companies blending requirements. CLH have agreed to renew the agreement with Griffin

Energy Ecosafe for the exclusive use of the facility. This facility is set up to blend bio diesel with the major oil company’s standard diesel. This

will allow Griffin Energy Ecosafe to sign supply contracts directly with any of the Major oil companies on the Island (BP, Shell or Cepsa etc)

and is a significant benefit for the majors as they do not need to import blended fuel into the Balearics.

CHECK This facility has a direct pipeline to The Port of Palma, which would enable the Griffin Energy Ecosafe product to be pumped directly on

board a tanker for overseas sales if required.

11Go-To-Market – Key Markets GREEN

2) The international wholesale market

This is fully functioning international commodity market with primary European trading venues in London and Rotterdam. Within these markets

demand is outstripping supply by a factor of 2 to 1. Market channels include:

CHECK Business to Business International:

This involves direct trades with oil distributors/distillers to allow them to blend standard diesel to 7% - 20% biodiesel mix, in line with EU

mandates.

CHECK Business to Business Domestic:

There is strong potential demand in both the power generation and transport infrastructure on the Island. This is being driven by national and local

policy mandates requiring the emissions reduction. Management have already commenced early sales development discussions with e.g. the Port,

a Mallorca biofuels distributor for heating boilers, an operator to the network of gas stations supply to large fleets of vehicles (public transport

companies).

CHECK Business to Consumer Domestic:

The General Directorate of Energy of the Balearic Government is carrying out a series of steps to realise direct sales points to the consumer public

transport sector, independent of the gas stations, this presents a further domestic opportunity for Griffin Energy Ecosafe.

3) Global Development Markets

CHECK The Power Generation Market.

This developing market will use biodiesel in place of mineral diesel to address the issue of peak demand on electricity grids. Given the limitations

of renewable power (Wind and Solar) and the cost of battery storage (approx. $750k per mw) this form of ‘instant’ power will still be required.

Biodiesel is the obvious choice and is already being adopted in many EU states for this purpose. Additional financial incentives are in place to

encourage its use.

CHECK The Marine Market.

Global regulation on marine emissions are forcing the shipping industry to address the issue of emissions. This is a developing market that we are

monitoring. We have already received strong interest from the port authority in Mallorca as well as several port authorities in the UK.

12Go-To-Market – Sales Strategy GREEN

Long-term contracts

The sales strategy will be to focus on the highest returns with the longest possible commitments.

CHECK Sales contracts will aim to be set three months in advance to lock in feedstock and finished product prices. This removes the need for any hedging

strategy and associated costs. This is in line with existing market trading conventions. The international wholesale market is the most liquid market

and will always have huge demand.

CHECK Higher margin trades will develop in the domestic market once the product is available. We will therefore aim to quickly develop a diversified

trading profile to minimise risk.

Pricing

CHECK Demand-driven market, whereby supply doesn’t meet demand levels.

CHECK Not competing on price. Biodiesel pricing is a regulated market, such that pricing is controlled and linked to diesel pricing.

CHECK Biodiesel subsidy rates received, provide an attractive margin buffer.

CHECK Penalties levied on diesel blenders for non-compliance in meeting minimum mandated biodiesel percentage-mix contained within all diesel blends.

This provides a further driver for biodiesel consumption.

CHECK Feedstock price inelasticity. This is driven by the fact that without the biodiesel industry all waste feedstocks used in biodiesel production, such as

Used Cooking Oil (UCO), would become a cost by virtue of the need to safely dispose of them, with storage cost and storage capacity (timeframes)

being prohibitive.

13Summary Post-Financing P&L

Summary Post-Financing P&L GREEN

The investment required is in the region of €5 millio

Year 1 Year 2 Year 3

TheThese funds

investment can be

required divided

is in intooftwo

the region €5 forms, Capex

Sales £ £ £ million (c. 5.31million). These funds can be divided

Biodiesel Total tons 25,988 34,650 34,650

CAPEX:

into►two forms, Capex Initial investment of €2 million

and Opex. to se

plant and tank farm. An additional €2m for pl

Biodiesel Total Income 21,992943 29,323,924 29,323,924

Angle-right CAPEX:distillation tanks.of €2 million to

Initial investment

Glycerin Total Tons 2,784 3,713 3,713 secure the site and plant and tank farm.

The offer

An additional

► price

€2m for ofupgrades

plant the assetandversus value on

Glycerin Total Income 1,101,220 1,468,294 1,468,294 distillation tanks.

market offers an opportunity to both de-risk t

Total Income 21,992,943 29,323,924 29,323,924 well asoffund the business

Angle-right The offer price the asset versus valuebyonleveraging the i

Cost of Goods Sold 16,420,706 21,883,463 21,883,463 sheet market

the secondary value.offers

For details of the to

an opportunity cost versus va

both de-risk the investment

market, see slide 17. as well as fund the

Port Storage 314,016 376,819 376,819

business by leveraging the incremental balance

Transport 196,429 235,714 235,714 sheet value.

► TheFor details of the

Laboratory willcost versussave

further valuecosts and in

on secondary market, see slide 17.

16,931,150 22,495,996 22,495,996 efficiency.

Gross Margin 5,061,793 6,827,928 6,827,928

Angle-right The Laboratory will further save costs and

increaseOPEX:

► €1million.

production Almost all Opex

efficiency. is held in t

23% 23% 23% That will either be UCO, methanol or resulta

Senior Leadership 179,085 179,085 179,085 Angle-right OPEX: €1million. Almost all Opex is held in the

form of Biodiesel or Glycerine.

form of stock. That will either be UCO, methanol

Consultancy/Service Contracts 200,000 200,000 200,000 or resultant production

§ These rawinmaterial

the formproducts

of Biodiesel

will always reta

Depreciation 234,375 281,250 281,250 or Glycerine.conservative estimate of Opex risk is 10% of

€100k..products will always retain

These raw material

Other Overheads 212,946 214,286 214,286

their full value. A conservative estimate of Opex

risk is 10% of the principal i.e. €100k.

Profit/Loss Before Tax 3,646,915 5,336,540 5,336,540

Corporation Tax 911,729 1,333,509 1,333,509

Profit/Loss After Tax 2,780,186 4,000,526 4,000,526

► Assumes 100% UCO raw feedstock @ £494 futures price

Assumes 100% UCO raw feedstock @ 494 futures price

14Corporate Structure GREEN

UK Holding Company

Griffin Property Group Limited

UK Registered

CHECK All assets & IP owned by UK Holding Company

CHECK Investment into UK Holding Company

CHECK Assets leased into Griffin Energy Ecosafe acting as

trading entity.

Ecosafe Biofuels sl.

Spanish Registered

100% Owned by

Griffin Property Group Limited

15Current Financing & Use of Funds GREEN

Current Raise

CHECK Initial investment of €2 million to secure the site and plant and

Leveraging the Asset Value

tank farm. An additional €3m for plant upgrades, distillation

tanks and feedstock.

Initial Purchase

The offer price of the asset vs the value offers an opportunity

Use of Funds / Key Milestones to leverage finance to fund the business and reduce exposure.

The cost vs value can be seen as below.

CHECK Purchase the Plant and the tank farm

CHECK Upgrade the production facility Upgrades and final valuation

CHECK Secure dock tanks

The plant upgrades and new tanks will cost €2 million.

CHECK Arrange sales of product

CHECK Feed stock Contracts This increases the total asset and business value resulting

in an enhanced balance sheet value.

CHECK Complete the assessment and re-commissioning of plant prior

to start up (Siemens)

CHECK Employ key personnel full time

CHECK Enter CLH tank storage agreement

16Disclaimer GREEN

DISCLAIMER NOTICE – PLEASE READ

This presentation and all information disseminated under it is the property of Griffin Property Group Limited (the “Company”). This presentation is being made on

the basis that the recipients keep confidential any information contained herein or otherwise made available, whether orally or in writing, in connection with the

Company. These presentation materials are confidential and must not be copied, reproduced, published, distributed, disclosed or passed to any other person at any

time without the prior written consent of Griffin Property Group Limited.

The presentation is being made for general corporate informational purposes only. These presentation materials do not constitute or form part of any offer for sale or

subscription or any solicitation for any offer to buy or subscribe for any securities nor shall they or any part of them form the basis of or be relied upon in connection

with any contract or commitment whatsoever. While all reasonable care has been taken to ensure that the facts stated in these presentation materials are accurate

and that any forecasts, opinions and expectations contained therein are fair and reasonable, the Company has not independently verified the contents of these

presentation materials and no reliance whatsoever should be placed on them. Accordingly, no representation or warranty express or implied is made to the fairness,

accuracy, completeness or correctness of these materials or opinions contained therein and each recipient of these presentation materials must make its own

investigation and assessment of the matters contained therein. In particular, but without prejudice to the generality of the foregoing, no representation or warranty

is given, and no responsibility or liability is accepted, as to the achievement or reasonableness of any future projections or the assumptions underlying them, or any

forecasts, estimates, or statements as to prospects contained or referred to in these presentation materials. Any investment decision in relation to the arrangements

described herein should be made on the basis of the contents and matters to be referred to in a separate investment-related document.

No responsibility or liability whatsoever is accepted by any person for any loss howsoever arising from any use of, or in connection with, these presentation materials

or their contents or otherwise arising in connection therewith. In issuing these presentation materials, the Company does not undertake any obligation to update

or to correct any inaccuracies which may become apparent in these presentation materials. These presentation materials are being supplied to you for your own

information and may not be distributed, published, reproduced or otherwise made available to any other person, in whole or in part, for any purposes whatsoever. In

particular, they should not be distributed to or otherwise made available to persons with addresses in Canada, Australia, Japan, the Republic of Ireland, the Republic

of South Africa or the United States, its territories or possessions or in any other country outside the United Kingdom where such distribution or availability may lead

to a breach of any law or regulatory requirements.

The distribution of these presentation materials in other jurisdictions may be restricted by law, and persons into whose possession these presentation materials

come should inform themselves about, and observe, any such restrictions. Any failure to comply with these restrictions may constitute a violation of the laws of the

relevant jurisdiction. Any person attending this presentation should seek their own independent legal, investment and tax advice as they see fit.

17Appendix

18Biodiesel Production Process GREEN

Angle-right Biodiesel is “liquid solar energy”, it is a 100% biodegradable fuel, which Angle-right The biodiesel process of transesterification was developed over a hundred

disappears in less than 28 days, whose toxicity is lower than that of years ago the chemical process is therefore understood, efficient and

common table salt and with reduced particulates, carbon monoxide and optimised. This is not new technology. It is also the industry standard by

greenhouse gas emissions, with best carbon footprint (from soil to tailpipe). which billions of litres a year are produced globally.

Angle-right An ecological fuel which reduces net CO2 emissions by 80% when Angle-right The reaction can either use a sodium or potassium catalyst. Potassium is

compared to common petroleum diesel. more expensive but produces a premium quality biodiesel. The primary

commodities produced are biodiesel and glycerine. The waste stream is a

Angle-right Biodiesel blends can be used in existing and new technology diesel engines small amount of water and potassium salts and disposal costs are minimal.

without modification and provides high quality fuel from sustainable

sources. It further reduces imports and power of oil cartels.

Schematic of Biodiesel Production Path

Vegetable Oil / Animal Fat / Waste

Methanol

Transesterification Crude Biodiesel Refining Biodiesel

plus Catalyst

Crude Glycerine

Methanol

Glycerine Recovery Glycerine

Recovery

19Market Problem

Market Problem GREEN

All the market opportunity is currently:

CHECK Production shortfall of almost 50%

Theagainst

marketdemand.

opportunity is currently:

CHECK EU renewables mandates in place

• Production

until 2030. shortfall of almost 50% against dema

• EU renewables mandates in place until 2030.

20Plant Upgrades GREEN

Key upgrades are required. The upgrade program reduces the cost of production and

increases the value and range of the output products.

The principal upgrades are as follows;

Distillation

A distillation system has two functions.

a. Improves the quality of the fuel

b. Allows purification of the glycerin byproduct.

The purification of the glycerin is crucial. The glycerin represents 10% of the output material and will contain

30% biodiesel. This is reclaimed in the process. The remaining glycerin will be above 95% purity and can be

sold as technical grade product. This increase its value 10 fold and should realise 450 a tonne.

Methanol Recovery

Methanol is used at 16% of the reacted volume. It is also very expensive. Methanol recovery allows the re-use

of methanol and greatly reduces the overall cost of production. Each upgrade requires a budget of 1mil but

returns on its capital cost within 18 months.

21Feedstock and Sales GREEN

Feedstock Purchasing

The feedstock and biodiesel markets are fully functioning, liquid and international. As a consequence price

transparency and forward ordering is a simple function of the industry. We have built relationships with

the major brokers such as GreenEA and SPA to ensure that feedstock supply will be at the correct price

and securable on long term contracts. Letters of intent and contracts can be delivered subject to finance

agreement.

Biodiesel Sales

As with feedstock there is a fully mature international sales market. We will be using brokers alongside direct

sales to the primary consumers in the market. The largest buyer in the UK, Greenergy, has already signalled

their openness to buy the product.

It is worth noting that current supply in Europe only satisfies 50% of demand. This is therefore a market that

welcomes new sources of product.

22Biodiesel Pricing – 1 GREEN

Biodiesel pricing is contingent upon three factors;

Angle-right The wholesale market price - published by the standard commodity indexes Ultimately the final sale price is actually a function of a retro-pricing

such as Platts. This is calculated from data collated on over the counter mechanism. Biodiesel pricing is effectively controlled so that it is in line

trading. In this it is no different to the pricing mechanism for other energy with mineral diesel. The downward pressure in this calculation is put on the

commodities such as gasoline and natural gas feedstock price. Without the biodiesel industry all waste feedstocks such as

Biodiesel

Biodiesel Pricing

Pricing

Angle-right The 11 in the country of sale –which varies in line with demand

subsidy market

UCO would become a cost by virtue of the need to safely dispose of them.

(i.e. higher demand equals a higher subsidy rate).

(See graph on Page 19)

The FX rate - which is a minor factor given that FX rates fluctuate within

Angle-right

g is contingent relatively

upon three factors;

narrow bands. This is usually mitigated in trading by hedging or

contingent upon three factors;

A good way to understand how retro pricing works is to look at a worked example.

forward back to back trades of feedstock and biodiesel.

sale market price - published by the standard A good way to understand how retro pricing works is to look at a worked example.

ymarket

indexes price

such as- Platts.

published

This by the standard

is calculated from data Here we see the price derived from the current UK market.

dexes such as Platts. This is calculated from

n over the counter trading. In this it is no differentdata

to Here we see the price derived from the current UK market.

ermechanism

the counterfortrading.

other In

energy this it is no

commodities

A good way to understand how retrodifferent

such to

as

chanism

nd naturalfor

gas otherworks

pricing energy

is tocommodities

look at a workedsuch as

example. Here we see the price derived

atural gas from the current UK market.

dy market in the country of sale –which varies in line

nd (i.e.inhigher

arket demandof

the country equals a higher varies

sale –which subsidyinrate).

line

i.e. higher demand equals a higher subsidy rate). The calculation includes the cost of blending the biodiesel and a small profit in line with the

e - which is a minor factor given that FX rates

within relatively narrow bands. This is usually expectations of the bulk fuel market. The underlying cost of sale is shown in the following

which is a minor factor given that FX rates The calculation includes the cost of blending the biodiesel and a small profit in line with the

n trading by hedging or forward back to back trades table.

n relativelyThe

narrow bands. This is usually expectations of the bulk fuel market. The underlying cost of sale is shown in the following

ck and biodiesel. calculation includes the cost of blending

table.

ading by hedging or forward

the biodiesel back

and a small toinback

profit trades

line with

nd biodiesel.

final the expectations of the bulk fuel market.

sale price is actually a function of a retro-pricing

The underlying cost of sale is shown in the

odiesel pricing is effectively

following table. controlled so that it is in

lalsale price

diesel. Theis downward

actually a pressure

functioninofthis

a retro-pricing

calculation is

sel pricing is effectively controlled so thatallitwaste

dstock price. Without the biodiesel industry is in

hiesel. The downward pressure in this calculation is

as UCO would become a cost by virtue of the need

se of them. (See graph

ck price. Without on Page 20industry

the biodiesel ) all waste

23

UCO would become a cost by virtue of the need

them. (See graph on Page 20 )et using our broker network. Bulk deliveries will be made to the tank storage facility

ows for delivery

Cost and bySourcing

tanker. Tanker

of UCOsized loads offer

Feedstock – 2the best value and convenience. GREEN

ck and plant by road tanker.

ccreditedUCO

tocan

ensure

be sourcedthat itOur

globally. is aim

compliant withas 25%

is to source as much regulation

of the toThe

claim subsidy

objective certificates

will be to source UCO that is 5/2 quality (less than 5% moisture

required feedstock locally. Additional volume will be purchased in bulk on the and less than 2% impurities. Purchase prices will be adjusted to account for

European market using our broker network. Bulk deliveries will be made to the moisture and impurities. The plant is equipped with a UCO pre-processing

tank storage facility that we have secured at the dock. This allows for delivery facility. This will allow for the use of cheaper unrefined product that can be

by tanker. Tanker sized loads offer the best value and convenience. polished before introduction to the production process. This ability affords a

s 5/2 quality

UCO will(less

then be than 5%

transferred moisture

between andby less

dock and plant than 2% impurities. Purchase prices will

road tanker.

considerable economic benefit.

mpurities. The purchased

All product plant is willequipped withtoaensure

be fully ISCC accredited UCO thatpre-processing

it is compliant facility. This will allow

that can be polished before introduction to the production process. This ability

with regulation to claim subsidy certificates on the finished product.

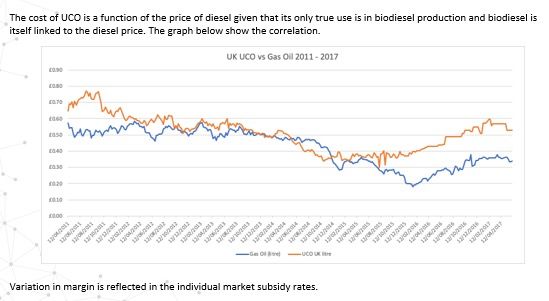

The cost of UCO is a function of the price of diesel given that it’s the only true use of biodiesel production and biodiesel is itself

linked to diesel price. The graph below shows the correlation.

Variation margin is reflected in the

individual market subsidy rates.

24

25Chemicals and Associated Costs GREEN

There are three chemicals required in the production process.

Catalysts

Angle-right Methanol: This will be sourced on the mainland. Spain is one of the key European producers of Methanol.

This means that we can purchase directly from the production plants. This will be shipped in ISO

containers as freight and transshipped from the dock on our own vehicles.

Angle-right Potassium: This will be purchased in granular form in bulk and pre-mixed on site.

Angle-right Polishing finished product.

Angle-right Amberlite: Amberlite is an ion exchange resin used to polish finished biodiesel. It removes any residual

glycerin and methanol bound into the glycerin. This process is called ‘dry washing’. We will be using a

renewable version that has a long life to reduce waste streams.

All of these products are available ‘off the shelf’, as such there are no supply issues.

25Risk Analysis 2 GREEN

Wider market risk

It is always worth considering the broader macro risk perspective.

Issue Comments

Oil market volatility Biodiesel and its feedstock are retro priced against diesel to keep them

pegged. The price therefore moves with the mineral diesel price preserving

the producer’s margins.

Change in regulation Very unlikely. CO2 reduction targets are internationally agreed by treaty.

These targets also have huge public support.

Removal of subsidies Very unlikely. The subsidy is included in the price of blended fuel and amounts

to a tenth of a cent per litre. It is hardly perceptible.

Phasing out of mineral diesel It will take 20 years to phase out diesel. Biodiesel has non of the emissions

issues of mineral diesel. Its use is likely to increase overall and as a proportion

of diesel use as a consequence of this.

26You can also read