Experian Consumer Services - 17 June 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Experian Consumer Services 17 June 2021 ©2021 Experian Information Solutions, Inc. All rights reserved. Experian and the Experian marks used herein are trademarks or registered trademarks of Experian Information Solutions, Inc. Other product and company names mentioned herein are the trademarks of their respective owners. No part of this copyrighted work may be reproduced, modified, or distributed in any form or manner without the prior written permission of Experian. Experian Public.

Experian North America Consumer Services Jeff Softley President, D2C

Our strategic priorities and growth agenda are ambitious

• We are developing a deeper relationship

We will be the with consumers; playing a more central

pre-eminent role in their day-to-day lives

platform for

• Our brand and our data give us the

consumers to license to support consumers across many

manage their areas to enhance their financial lives

financial lives

• We are taking share across markets as

we scale

• We are accessing substantial new

growth markets through accelerating

product innovation

3 © Experian

We are evolving our consumer value proposition, our role,

and our brand to achieve scale and growth

Direct to Phase 1 Phase 2 Phase 3

Consumer

Growth Commoditization Business Model Scaling Ambition • Use our unique role and

Horizons & Disruption Stabilization position to build “first, best,

only” products which give

Timeframe FY10 to FY16 FY17 to FY19 FY20+ consumers more control

• Scale our customer base

TAM $1bn+ $2bn+ $10bn+ and expand our brand

• Harness consumer

Member Base contributed data value

Size 2m to 5m 5m to 25m 25m to 100m+ propositions to access and

disrupt broader markets

Member Few times Every other Monthly

Engagement per year month • Franchise expansion to

access further growth

Verticals

Targeted 1 3 10+

4 © Experian

Macro trends play to Experian’s advantage

Accelerating digital Consumer contributed Consumers need help

transformation everything • 2 out of 3 consumers say they

• Generational and technology • Consumers are getting more are worried about their finances

Macro shifts advancing rapid adoption comfortable with sharing their

data for benefits

• Consumers have grown less

optimistic about the short-term

Trends • The COVID-19 pandemic is

accelerating need for digitized • More and more “real world” outlook for the economy and

processes outcomes are being realized labor market and remain

through consumer contributed concerned about their financial

data prospects

Experian’s Unique Experian Boost and Consumer Trust as

Position More Foundation

• Experian’s assets and leading • First mover advantage and an • Consumers trust Experian to

role in foundational financial expanding set of use cases produce financial health products

processes paired with our that they would trust and use

Experian growing consumer business

• New value propositions in

development against a backdrop • Consumers have a confidence in

Advantage create new opportunities to of digital transformation in the Experian’s ability to meet their

enable consumer control and market evolving needs during times of

serve partners uncertainty

5 © Experian Sources: ECS COVID-19 & Consumer Confidence Survey, March 2020

EY-Parthenon PFM Dynamics Consumer Survey

The Experian advantage: Our consumer-contributed data

strategy creates value for consumers, partners and the business

Experian Boost Momentum Favorability Engagement Monetization

% Aware of Experian Boost Awareness of Return rate is Free customers

Experian Boost improved for who complete

54% greatly improves customers who Boost generate

favorability use Boost higher revenue

42%

25%

13%

FY20 H1 FY20 H2 FY21 H1 FY21 H2

6 © Experian Sources: Brand Health Tracker Report by Northstar Research Partners

The Experian advantage: Scale is creating new opportunities

and more ways to engage consumers

Free Customer Base Total Login Volume Average Number of Overall Upsell Rate*

Free Members Logins per Customer Free Members

41M per month

Free Members

37%

Growth

YOY

FY17 FY18 FY19 FY20 FY21

Scale enables the business More customers Customers are More customers

to create meaningful entry are engaged engaged are invested

into new markets more often

7 © Experian *Rate of consumers upgrading to one of our paid membership products

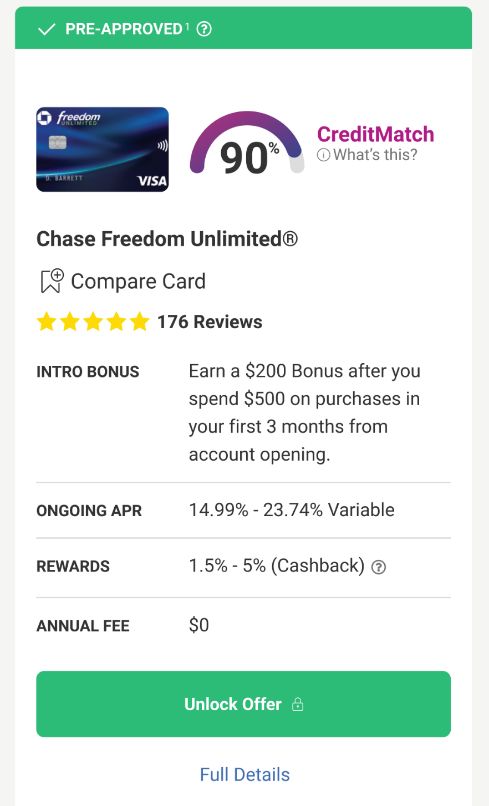

The Experian advantage: Partners trust our quality and

consumers trust Experian

COVID has created a unique market opportunity to

serve consumers and partners in meaningful, new ways

Partner • Lending guidance in uncertain market

CreditMatch is Needs • Access to high quality new customers

growing; while • Confidence in long term value and profitability

Bankcard

inquiries have Partners maintained their relationships with CreditMatch even

declined while reducing their network and marketing spend

CreditMatch onboarded 5 new partners and 6 new credit

FY21 H2 YOY product offerings during COVID

Growth

• Advice on how to safeguard their credit

Consumer

Bankcard Hard Needs • Access to tools that promote financial wellness

Inquiries • Confidence to gain credit

CreditMatch

Approvals Net Promotor Score is elevated for CreditMatch consumers,

indicating that access to tools that help them manage their

financial lives creates a more favorable view of the brand

Expanded Experian Boost to include additional credit line

options, e.g., streaming services

8 © Experian

Source: Experian State of the Market Trends

Our growth agenda will extend into large and adjacent markets

where we are competitively positioned

FINANCIAL

HEALTH $5bn+ IDENTITY

MANAGEMENT $3bn+ MARKETPLACE

$10bn+ *

$

We will help consumers manage Identity services are more than just Consumers can use their data and

their financial lives, not just their a passive insurance and protection financial profiles to access new

credit, with new freemium features proposition. Consumers can products across more areas of their

that assist consumers in manage their privacy and financial lives.

improving their financial control their data across new and Partners can access a stream of

position and saving money. expanding use cases. qualified, high value customers.

9 © Experian Note: Sizing estimates are preliminary. Shaded circles are the markets we currently operate in.

*Includes first-party & third-party lead gen

We are expanding with a new breed of “Smart” financial

health products; fueled by consumer contributed data

FINANCIAL 8:00 8:00 8:00

HEALTH

Personal Finances

$

1.4M $1M 50M+

Connected Saved Credit Score

Accounts points added

Financial Health Bill Negotiation

(during Beta test)

Experian Boost

Provide consumers with capabilities Help consumers eliminate costs Improve credit scores instantly – now

to build their financial profile and and save money by negotiating utilizing streaming service accounts

manage their financial lives bills on their behalf.

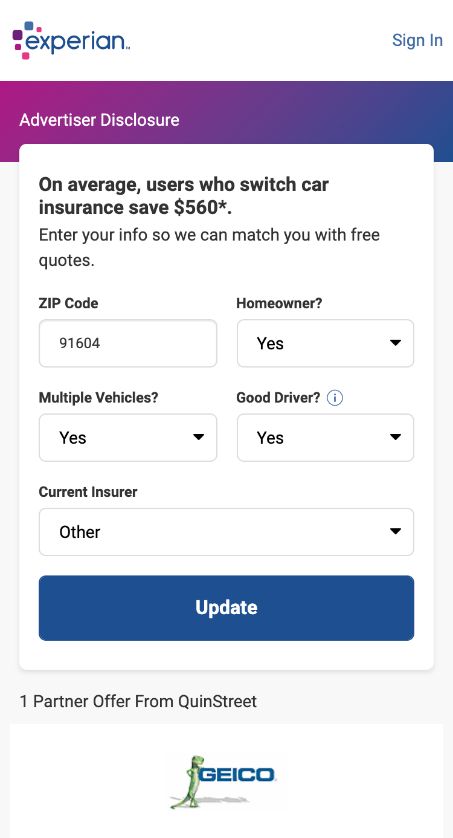

10 © ExperianOur marketplace is expanding, creating opportunities to help

consumers save money in a whole new way

MARKETPLACE 8:00 8:00 Auto Insurance Revenue

Lead Generation

+71%

H2 vs H1

FY21 H1 FY21 H2

Partner Response

“CreditMatch, in the span of

less than 3 months, have

become a T1 partner and are

getting attention and priority all

the way up to the CEO level”

~ Auto Insurance Partner

Lender Integrations Auto Insurance

Consumers benefit from pre-

Marketplace

approved offers generated through Better credit can save

integrated partner relationships consumers money in our

auto insurance marketplace

11 © ExperianWe have a clear path ahead of us, strong momentum and

substantial new opportunities which play to our advantage

Growth agenda is working - we are taking

We will be the share in core markets

pre-eminent

platform for Uniquely positioned to address macro trends

consumers to and evolving consumer needs

manage their

financial lives

Substantial franchise expansion opportunities

available to accelerate growth

12 © ExperianExperian Brazil Consumer Services Silvio Frison Vice President, Brazil Consumer Services

Credit Landscape in Brazil

Punitive interest rates and strict credit policies penalise the population.

Low credit penetration, due to limited competition, restricted to five major banks

Huge latent potential for collections and credit services

Household Credit/GDP Ratio (%) Serasa: Challenging the status quo

Data

75% 84%

30%

Local Brand

Brazil USA UK

Market

Defaulters in Brazil (2020) Position

62 million

Global IP

Positive Data

14 © Experian * Source: Bank for International Settlements (BIS), 2019 | Serasa Experian.Consumer Services Strategy: Credit for All

Our mission is to provide credit access to the entire Brazilian population regardless of their score

Consumer’s Financial Life Timeline and Target Products

Engagement: Serasa “Free”

Free ID Financial Positive

Score

Report Education Data

Transactional Products

Collection Marketplace Credit Marketplace Premium Subscription

0 300 700 1000

Distribution

Serasa Media/e-wallet

15 © ExperianEngagement Strategy: Serasa “Free”

Serasa has connected with more than 1/3 of the Brazilian Population

Free Member Enrollments (millions)

+51%

37% of

Brazilian

45 59 adult

32 population

22

11

FY17 FY18 FY19 FY20 FY21

Brazilian Population (millions)

Total

Adult

Banked 212

157

112

16 © Experian * Source: IBGE, 2020.Collection Marketplace (Limpa Nome)

Limpa Nome solution is already the go-to solution for Brazilians to negotiate their debt and pay their bills

Limpa Nome: Partners Limpa Nome: Discounts Conceded (US$ billions)

+102%

53 +341%

34

13

FY19 FY20 FY21

Limpa Nome: Transactions (millions) 13

+299%

26

4

8

2 1

FY19 FY20 FY21 FY19 FY20 FY21

17 © Experian *Source: Team analysis | LNO came to ECS in FY19 | FY21 Fx rate: R$ 4.12.Serasa Score Turbo

Bills paid within our ecosystem boost consumers score.

Gamification strategy through bills payments

Real time financial education

It differs from USA Boost, which is based on behaviour

More deals

HIGHER CREDIT

RATING

BUREAU DEBT

Limpa

Nome

PAYMENT

NON-BUREAU DEBT

eWallet REGULAR BILLS

FINANCIAL

EDUCATION

More deals

18 © ExperianCredit Marketplace (eCred)

eCred completes the Serasa ecosystem (pay your bills, boost your score and get back to the credit market).

Brazil: 2020 Credit Market Size (US$) eCred: Confirmed Orders (millions)

+66%

$840 billion 3

5

2

FY19 FY20 FY21

eCred: Loans (US$ millions) eCred: Credit Cards (thousands)

+21%

+240%

44 1,594

33

23

138 362

FY19 FY20 FY21 FY19 FY20 FY21

19 © Experian * Market size source: Bacen/Febraban; Feb, 2020 | Source: Team analysis | eCred operation began in Sep/18 | FY21 Fx rate: R$ 4.12.Key Results

We are already the largest Brazilian fintech from an audience standpoint

Web Visits (millions) Financial Audience Share (%) *Nov/20

589 20%

+82%

433

291 65% 10% 10% 10%

Organic 9%

194 Traffic 6%

54

FY17 FY18 FY19 FY20 FY21 Caixa Serasa Bradesco Itaú Santander Nubank

Unique Web Users: Monthly Average App: Active Users

(millions) +31%

(millions)

20 +34%

8

16

6

12

FY19 FY20 FY21 Mar/20 Mar/21

20 © Experian *Source: Google Analytics; Similar Web; Team analysis | Organic Traffic: Direct access to the website | Financial Audience: searches on Google; nov 2020.What is next?

Serasa will be the one-stop-shop for financial life

SERASA

• Comprehensive • Score improvement

credit scan

• Renegotiate debts • Personal credit

• Get special discounts • Credit card

• E-wallet • Financing

• Financial education • ID monitoring

Score 0 Score 1000 • Cashback

21 © ExperianIn summary, very attractive prospects for our business

in Brazil

1 Strong position in the market

2 Winning strategy in place

3 Clear competitive advantages to address an evolving credit space

4 Good momentum enhanced by positive data

5 Plenty of opportunities in addition to positive data

22 © ExperianYou can also read