Expenditure Guide for Malaysians 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Expenditure Guide for Malaysians

Klang Valley

Johor Bahru

Kota Kinabalu

Kuala Terengganu

Alor Setar

Kuantan

Kota Bharu

Georgetown

Kuching

Ipoh

Melaka

Seremban

2021

BELANJAWANKU 2021 Expenditure Guide for Malaysians Selected Region & Cities Klang Valley Johor Bahru Kota Kinabalu Kuala Terengganu Alor Setar Kuantan Kota Bharu Georgetown Kuching Ipoh* Melaka* Seremban* Research Team Social Wellbeing Research Centre (SWRC), Universiti Malaya Emeritus Professor Datuk Dr. Norma Mansor Nik Noor Ainoon Nik Osman Dr. Halimah Awang Dr. Zulkiply Omar Muhammad Hazim Noran Rashid Ating Hazman Abdul Rahman Faculty of Business and Economics, Universiti Malaya Dr. Sharifah Muhairah Shahabudin En. Nawi Abdullah Dr. Nurul Huda Mohd Satar Dr. Roza Hazli Zakaria Dr. Yong Sook Lu Dr. Ng Yin Mei * Preliminary

TABLE OF CONTENTS

Acknowledgement IV

1. Introduction 1

2. Issues and Challenges 3

3. Objectives 8

4. Use of Belanjawanku 9

5. Data and Method 11

5.1 Focus Group Discussion (FGD) 11

5.2 Questionnaire Survey 12

5.3 Price Survey 12

5.4 Delphi Method 12

6. Constructing Belanjawanku 13

6.1 Defining Standard of Living 13

6.2 Defining Household Categories 14

6.3 Development of Item Baskets 14

6.4 The Agreed Item Baskets 15

6.5 Pricing Criteria 16

7. Development of Item Baskets 17

7.1 Development of Food Basket 17

7.1.1 Pricing Criteria for Food Basket 17

7.2 Development of Housing Basket 18

7.2.1 Pricing Criteria for Housing Basket 19

7.3 Development of Transportation Basket 20

7.4 Development of Utility Basket 22

7.4.1 Pricing Criteria for Utility Basket 23

7.5 Development of Personal Care Basket 24

7.5.1 Pricing Criteria for Personal Care Basket 24

7.6 Development of Healthcare Basket 25

7.6.1 Pricing Criteria for Healthcare Basket 26

7.7 Development of Childcare Basket 27

7.8 Development of Ad-hoc Expenses Basket (allocated as monthly average) 28

7.8.1 Pricing Criteria for Ad-hoc Expenses 28

7.9 Development of Social Participation Basket 30

7.9.1 Pricing Criteria for Social Participation Basket 30

II7.10 Development of Discretionary Expenses Basket 31

7.11 Saving 32

8. Belanjawanku 2021 Estimates by Household Categories 34

8.1 Estimated Monthly Expenses: Single Public Transport User (P.T.U) 34

8.2. Estimated Expenses: Single Car Owner (C.O) 35

8.2.1 Increase in Expenses for a Single Person 35

8.3 Estimated Monthly Expenses: Married Without Children 36

8.4 Estimated Monthly Expenses: Married With One Child 37

8.5. Estimated Monthly Expenses: Married With Two Children 37

8.6. Estimated Monthly Expenses: Senior Single 38

8.7 Estimated Monthly Expenses: Senior Couple 39

8.8 Estimated Monthly Expenses: Single Parent With One Child 40

8.9 Estimated Monthly Expenses: Single Parent With Two Children 41

9. Belanjawanku 2021 Total for All Selected Cities / Region 42

9.1 Comparing Belanjawanku 2021 for Selected Cities Against Klang Valley 42

9.2 Belanjawanku 2021; Comparing Expenses Between Household Categories 43

10. Comparing Years 2020 and 2021 for Klang Valley according to Household

Categories 46

11. Impact of COVID-19 Pandemic on Consumption and Personal Finance 49

12. Conclusion and Recommendations 52

13. Moving Forward 53

LIST OF TABLES 54

LIST OF FIGURES 55

LIST OF DIAGRAMS 55

REFERENCES 56

APPENDICES 59

ANNEX: NOTES ON THE DEVELOPMENT OF ITEM BASKETS i

IIIAcknowledgement

We would like to express our gratitude to those who have contributed their inputs, ideas,

comments and critics to this research project, and for spending their precious time to be our

focus group discussion participants, informants and facilitators as follows:

● The management and staff of Employees Provident Fund (EPF) Malaysia

● Researchers from Universiti Malaya (UM), Universiti Malaysia Terengganu (UMT), Universiti Sultan

Zainal Abidin (UniSZA) Terengganu, Universiti Malaysia Sabah (UMS), Universiti Perguruan Sultan

Idris (UPSI), Universiti Teknologi Mara (UiTM), Seremban, University of Nottingham Malaysia,

Institut Pembasmian dan Pengurusan Kemiskinan (InsPEK), Universiti Malaysia Sarawak (UNIMAS),

The Netherlands Institute of Family Finance and Budgeting (NIBUD).

● Representatives from the following:

● Department of Statistics Malaysia (DOSM)

● Credit Counselling and Debt Management Agency Malaysia (AKPK)

● Economic Planning Unit (EPU), Prime Minister’s Department, Malaysia

● The National Wage Council Malaysia

● Bank Negara Malaysia (BNM)

● Universiti Malaya Medical Centre (UMMC)

● International Centre for Education in Islamic Finance (INCEIF)

● Ministry of Domestic Trade, Co-operatives and Consumerism (KPDNKK)

● Federation of Malaysian Consumers Associations (FOMCA)

● Welfare Department, Ministry of Women, Family and Community Development

(KPWKM), Malaysia

● Yayasan Hasanah Malaysia

● Kesatuan Kakitangan Am Universiti Malaya (KEKAUM)

● Giatmara Malaysia

● ACE Group Sdn Bhd

● Persatuan Ibu Tunggal Kuala Terengganu (PERKIBUT)

● Traders at Larkin Sentral, Mazlee Express, A-Mart and Pandan City Wholesale

Market, Johor Bahru, Johor

● Traders at Pasar Payang, Warong Kuala Ibai, Terengganu

● Traders at Warong Taman PKNK, Pasar Kampung Berjaya, Kampung Nelayan and

Pasar Teluk Wanjah, Alor Setar, Kedah

● Traders at Pasar Lido and Pasar Besar Kota Kinabalu, Sabah

● Traders at Pasar Besar Kota Bharu, Pasar Siti Khadijah, Pasar Jelawat and Pasar

Bachok, Kota Bharu, Kelantan

● Traders at Pasar Besar Kuantan, Pasar Taman Peramu Jaya, Pasar Tanjung Api,

Gading Jaya Wet Market, Kuantan, Pahang

● Traders at Bertam Market, Bayan Baru, Seberang Jaya, Bukit Mertajam, Chai Leng,

Samagagah, Tun Sardon, Batu Lanchang, Chowrasta and Pulau Tikus Public

Market, Penang

● Traders at Pasar Besar Ipoh, Pasar Gunung Rapat Pasar Kampung Bercham and

Pasar Kampung Simee, Ipoh, Perak

● Reference persons representing selected households in the Focus Group

Discussions

● Enumerators involved in the recruitment of participants in the selected cities and

regions

● Facilitators during the Focus Group Discussions in various cities and regions

IVWe wish to express our utmost gratitude to EPF for funding the research and development of

Belanjawanku. Last but not least, our sincere appreciation to the management and staff of

Social Wellbeing Research Centre, Universiti Malaya for their relentless support in the data

collection, organising and facilitating questionnaire surveys, focus group discussions, price

surveys as well as face-to-face and telephone interviews for verification at the selected cities

throughout Malaysia.

V1. Introduction

Belanjawanku is an expenditure guide which provides estimated minimum monthly expenses

on various types of goods and services for different family sizes in Malaysia. It is a budget that

can be used as information or a guide to one’s personal finance. Elsewhere, it is known as a

reference budget or budget standard that contains household expenditures, basket lists of

goods and services, and its cost thereof, that are needed for a family of a specific size and

composition to be able to live at a reasonable and acceptable level.

The circumstances of individuals and families are strongly influenced by both their income and

expenditure as well as by their needs. As such, apart from providing information, reference

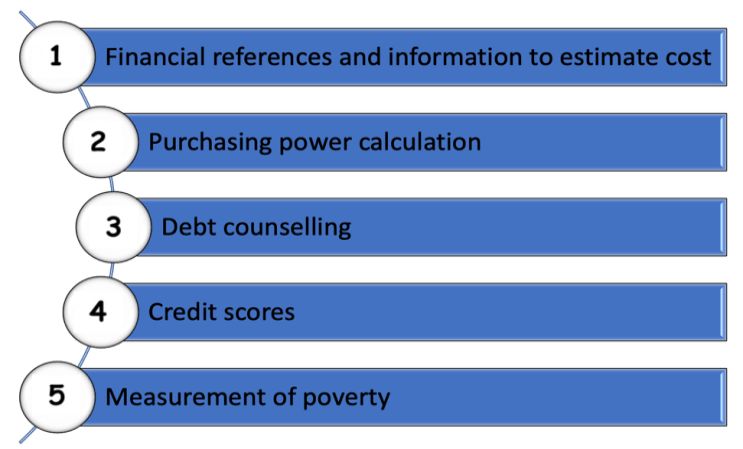

budgets are also useful for personal financial planning and debt management for individuals.

On the other hand, financial institutions and debt counselors will find this useful for credit

scores and debt counselling. For policy makers, it can facilitate poverty measurement,

determinants of minimum wage and costs of living indicators.

The underlying motivation for the development of Belanjawanku is the concern related to poor

personal financial management among Malaysians and the rising costs of living. The way a

person manages his finances is significantly related to his financial literacy. Poor financial

management makes a person highly vulnerable to the impact of a financial shock such as loss

of employment, illness, disability, loss of loved ones or any unexpected events or emergencies.

The consequence of poor financial management leads to problems of over-indebtedness, low

savings and bankruptcy especially among youths. Having the capability to manage personal

finances is an essential life attribute in order to attain good financial wellbeing.

This study explores the spending patterns of Malaysian households, their needs, wants and

costs according to different compositions, disposable incomes and other characteristics that

reflect their circumstances. Based on the actual spending patterns, this study aims to identify

a specific basket of goods and services which can represent a particular standard of living or

wellbeing for individuals and families from various households in the country.

Since the circumstances of individuals depend very much on their income and expenditure,

this study provides details in terms of goods and services and the amount of money required

to have nutritious food, decent housing, access to utilities, adequate healthcare, personal care,

proper childcare, and to some extent, discretionary expenses. These outlay account for not

only needs that are basic, but also allow people to be involved in community activities as well

as gatherings of families and friends in order to engage with their society for a purposeful and

meaningful life.

Besides providing minimum monthly expenses required for people to attain a reasonable and

acceptable standard of living, Belanjawanku is able to indicate the actual costs of living as

evidenced from the spending patterns of households that were involved in the study.

Consequently, the expense guide provided by Belanjawanku can be used as a tool for financial

literacy education.

1The first wave of Belanjawanku (2019) covers the cities and districts in Klang Valley, namely

the Federal Territory of Kuala Lumpur, Putrajaya and the urban districts in the state of Selangor

which include Gombak, Hulu Langat, Petaling, Klang, Kuala Langat and Sepang. The

Belanjawanku Klang Valley 2019 was jointly launched by the Employees Provident Funds

(EPF), Malaysia and Universiti Malaya, officiated by the then Finance Minister, YB Mr Lim Guan

Eng.

The second wave of Belanjawanku was conducted between April 2019 to March 2020 covering

additional cities which include Alor Setar, Kota Kinabalu, Johor Bahru and Kuala Terengganu.

This study has since been expanded to include seven more cities comprising Kuching,

Georgetown, Kuantan, Kota Bharu, Ipoh, Seremban and Bandaraya Melaka. The current study

began in July 2020 and ended in May 2021, albeit impacted by intermittent disruptions to the

data collection process due to the Movement Control Orders (MCOs) resulting from the

COVID-19 pandemic. The objective of the expansion is to examine the differences in spending

patterns in different locations nationwide and to obtain a more precise indication of the cost of

living in those locations.

22. Issues and Challenges

The challenge of low financial literacy and increasing costs of living lead to over-indebtedness,

youth bankruptcy, low savings and fragile financial protection. Malaysia is one of the countries

where the financial literacy level among its citizens is relatively low. Governments around the

world have expressed concern about the low level of financial literacy among their citizens

(Atkinson & Messy, 2011).

In a national study for financial literacy, one of the findings associated low-income level with

relatively low financial knowledge (Financial Education Network (FEN), 2019). Bad habits or

poor attitudes toward personal financial management however, can be mitigated through

financial education. Evidence has shown that one in three Malaysians rated themselves as

having poor financial knowledge (FEN, 2019) and majority of them feel insecure with their

financial situations (FEN, 2019 and Mahdzan et. al., 2020). Financial literacy will enhance an

individual's ability to handle monetary issues and should reduce the negative consequences

of poor financial decisions that otherwise might take years to overcome (Yoong et. al., 2012;

Jonubi & Abad, 2013 and Idris et. al., 2017).

Malaysians have also experienced significant fluctuations in inflation rates due to higher prices

of food, fuel and transportation costs in the last decade. Between 2011 to 2020, the inflation

rate has fluctuated, reaching a high of 3.87 percent in 2017 before declining to 0.88 percent

in 2018 and hovering around 0.7 percent in 2019. Since March 2020, the MCO has indirectly

affected prices leading to a negative inflation of 1.2 percent in 2020 (Figure 2.1).

Nonetheless, further insights revealed that, in terms of CPI, despite a substantial decrease

mainly in the costs of transportation (-8.4 percent), housing, water, gas and other fuels (-3.3

percent), the prices of other main groups such as food and non-alcoholic beverages,

miscellaneous goods and services as well as health had registered an increase of 1.4 percent,

2.2 percent and 1.0 percent, respectively, when compared to the previous year (Department

of Statistics, Malaysia (DOSM, 2021a).

Figure 2.1: Malaysia: 10-Year Inflation Rate

Malaysia, 10 Year Inflation, 2011 to 2020

3.7

4.0 3.2 3.2

3.0

2.1 2.1 2.1

Inflation Rate (%)

2.0 1.6

1.0

0.7

1.0

0.0

2011 2012 2013 2014 2015 2016 2017 2018 2019 -1.2

2020

-1.0

-2.0

Year

Source: Department of Statistics Malaysia, various years

3Far from helping the situation is the issue of low wages among a large segment of Malaysians.

Although the income growth of the top 20 percent of the population (T20) since 1990 is in

tandem with the national GDP growth, the bottom 40 percent (B40) households experienced

the slowest growth (Samad & Mansor, 2017).

Although the median household income has improved from RM2,841 in 2009 to RM5,873 in

2019, more than 30 percent of Malaysian households were earning below RM4,000 a month

(DOSM, 2019). The DOSM, (2019) report also revealed that between 2016 to 2019, the income

growth (compounded annual growth rate, (CAGR) of the B40 was 1.8 percent, lagging behind

the M40 and T20 which enjoyed 4.1 percent and 4.5 percent growth respectively.

Despite the 2019 revision of the minimum wage to RM1,200 per month, its current adequacy

continues to be debated; yet on the other hand, concerns over productivity persists. The last

decade has seen the economy of Malaysia buffeted by a series of shocks which had

undermined productivity growth.

Post 2009 global financial crisis, Malaysia recorded a positive productivity growth of 3.4

percent in 2014 and maintained its growth of above 3 percent until 2017 before declining to

2.3 percent in 2018 and 2019 and subsequently plunged into negative territory of -5.5 percent

in 2020 (Malaysia Productivity Report (MPC), 2021). The COVID-19 pandemic is the latest jolt

that has negatively affected the economy. Our alarming labour productivity contraction was

the first since the 2009 global financial crisis and the lowest in ten years (MPC, 2021).

Following the problem of low financial literacy and increasing costs of living, over-indebtedness

is another thriving problem that can jeopardise health, family life, access to housing and

employment. Malaysia has emerged as the country with the highest household debt within the

ASEAN region, the highest among eight markets surveyed in Asia, which was more than

double the regional average of 33 percent (Mainal et. al., 2016). In 2020, the Malaysia

household Debt-to-Gross Domestic Product (GDP) surged to a record peak of 93.3 percent

(Figure 2.2). Bank Negara Malaysia (BNM) explained that it was due to the normalisation of

household debt to pre-pandemic levels in the second half of 2020, whereas the GDP remained

below pre-COVID-19 levels.

4Figure 2.2: Malaysia Household Debt-to-GDP Ratio

Malaysia Household Debt-to-GDP, 2014-2020

96.0 93.3

94.0

Debt-to-GDP Ratio

92.0

90.0

86.9 86.5

88.0

84.8

86.0

82.7 82.0 82.7

84.0

82.0

80.0

78.0

76.0

2014 2015 2016 2017 2018 2019 2020

Year

Source: Bank Negara Malaysia Annual Report, various years

However, BNM (2020) stated that that the high level of household debt-to-GDP ratio is

manageable as it expects households to stay reasonably resilient despite the impact of the

pandemic. This is reflected by the continued maintenance of comfortable levels of financial

assets and liquid financial assets (LFA) at 2.2 times and 1.5 times of debt in the second half of

2020 respectively, as relief measures introduced by the Government released extra disposable

cash to households (BNM, 2020)

While the level of household debt may be manageable, indebtedness or the inability to meet

recurrent expenses without the need to borrow more may put borrowers in vulnerable

situations. Research has shown that over-indebtedness, poverty and social exclusion are

found to be closely interrelated (Mainal et. al., 2016). BNM in 2019 highlighted that the risks of

financial distress relating to household debt exposure were higher among the lower income

group, i.e those whose monthly earnings are less than RM3,000 as well as for those with

variable income. BNM cautioned that this group remains stretched financially as it appears that

their financial buffers are relatively much lower, judging from their liquid financial assets (LFA)-

to-debt-ratio of 0.7, and a substantially higher leverage (of 10 times) compared to those in the

higher income groups, as of December 2020 (Figure 2.3).

At the same time, according to BNM, those earning less than RM5,000 monthly appear to be

showing signs of financial stress, judging from the profile of those seeking financial assistance

under the loan moratorium programme, of which, 54 percent consists of borrowers from this

income group. The central bank also cautioned that these borrowers are likely to face

continued challenges in 2021, given their low financial buffers and relatively higher leverage;

along with the uneven labour market recovery (Figure 2.3).

5Figure 2.3: Household Sector - Leverage and LFA-to-Debt Ratios

Household Sector - Leverage and LFA-to-Debt Ratios

12.0

10.0

9.5

8.0 7.1 7.4

Times

5.5 5.6

4.0 4.1

4.0

1.4 1.5

0.7 1.0

0.0active EPF members are unlikely to achieve the recommended minimum amount of basic

savings of RM240,000, at the age of 55, which allows a monthly withdrawal of RM1,000 for 20

years post retirement. This amount, however, still falls short of the current National Minimum

Wage of RM1,200 per month and below the National PLI of RM2,208 per month. With life

expectancy expected to keep on rising as a result of advancement in healthcare facilities,

inadequate retirement savings could pose a serious threat to the wellbeing of the elderly and

aging population (FEN, 2019).

Another red flag is the Malaysia gross household savings as a percentage of disposable

income which was recorded to be low even with compulsory retirement savings under

Employees Provident Fund (EPF). The Khazanah Research Institute (KRI) reported that in 2013

(the last year for which such data was publicly available), household savings stood at 1.4

percent of adjusted disposable income, and averaged at 1.6 percent for the years between

2006 to 2013 (Figure 2.4).

Figure 2.4: Comparing Household Savings as Percentage of Adjusted Disposable

Income - Malaysia and other Countries

Household Savings as Percentage of Adjusted Disposable Income, 2013

12.0

9.8

Gross Household Savings

10.0

8.0

5.6

6.0 5.0 4.7

4.0

2.0 1.4

0.0

0.0

Chile Korea US EU Malaysia Japan

Country

Source: Khazanah Research Institute, The State of Households II, 2016 (pg 78)

73. Objectives

Belanjawanku serves as a kick-start to the development of a guide for individual and family

finance and budgeting for different types of households. Belanjawanku is a reference budget

that translates individual needs and wants into goods and services that represent a reasonable

consumption level, hence allowing people to attain a designated standard of living and able to

fully participate in the society.

Firstly, the objective was to investigate the actual spending behaviour and consumption levels

of individuals and families according to the specific size and composition of households.

Secondly, Belanjawanku sought to establish baskets of goods and services and its costs

thereof, that represent an 'agreed upon' minimum expenditure or consumption level required

for a reasonable and acceptable ‘standard of living' in Malaysia.

Thirdly, Belanjawanku is intended to provide analysis on the cost of each item basket

comprising of food, housing, transportation, utilities, personal care, healthcare, childcare,

annual / ad-hoc expenses, social participation, discretionary expenses, and estimate the

expenditures required therein, and subsequently to arrive at a consensus on what is a

recommended reference budget for Malaysians.

Last but not least, Belanjawanku is to provide information for people to understand their own

financial capabilities before making big financial decisions that may affect their short to long

term financial commitments, as well as their future financial security. The objectives of

Belanjawanku are summarised in Diagram 3.1.

Diagram 3.1: Objectives of Belanjawanku

84. Use of Belanjawanku

As summarised in Diagram 4.1, for individuals, Belanjawanku is useful as a guide in making

informed financial decisions before committing on big ticket purchases or having large loan

obligations. Besides that, Belanjawanku provides indications on additional expenses (e.g.,

when family size grows) as people move along their life cycle from being a single person to a

family man and into their old age.

The different guide for different cities as provided in Belanjawanku will enable individuals to

assess their purchasing power, as opposed to their (potential) income, given the different costs

of living in different cities, if they were to relocate.

For policy makers, Belanjawanku has the potential to provide a benchmark against which to

assess individual spending patterns, and the appropriateness of the poverty threshold of a

country. It can be used not only as a guiding tool for an individual's prudent financial planning,

but also for policy makers to employ as an instrument to prevent and address the problems of

households’ over-indebtedness, reviewing poverty line incomes as well as in designing

appropriate minimum wage policies and adequate income support.

As for financial institutions, Belanjawanku is potentially useful for credit scores which can be

utilised as an assessment tool for loan capability repayment and for debt counselling for those

who are at risk of being financially distressed.

Diagram 4.1: Use of Belanjawanku

The Malaysian government has revised the Poverty Line Income (PLI) in June 2020 from

RM980 to RM2,208 per household per month (DOSM, 2019). The revision was to reflect a

more accurate poverty measurement in the country and that move was positively viewed by

various parties including the World Bank Group. Given the extensive data available to gauge

the ‘minimum required’ as outlined by Belanjawanku, it is hoped that policymakers could

further implement and craft targeted policies to overcome ongoing social issues such as

poverty and inequality in Malaysia. Social assistance policies such as Bantuan Sara Hidup

(BSH) and Bantuan Prihatin Nasional (BPN) are primary examples of how targeted policies

would be able to alleviate financial burden of the needy groups.

9In view of the above, it is evident that Belanjawanku is well poised to provide a scientific, yet

participative budget guide and offer valuable tools to assess the financial wellbeing of

households along with other social benefits as part of the government's effort to ensure social

inclusion among all Malaysians.

Bearing in mind though, a reference budget is not a prescription to solve an individual's

financial problems, nor is it a ‘standard’ that one has to follow. In this case, Belanjawanku

serves as a detailed guide as to the expenses required to attain the desired standards of living

with optimum expenses minus the luxuries.

105. Data and Method

This study adopted both quantitative and qualitative approaches using primary and secondary

data. The primary data collection was done via focus group discussions, questionnaire surveys

and price surveys at actual business premises. Secondary data was obtained through

published documents from various ministries and agencies, as well as online platforms. The

first wave of data collection for the development of Belanjawanku Klang Valley 2019, was

conducted from November 2017 to July 2018. The second wave of data collection was done

between June 2019 to September 2020.

The target groups were working adults between 18 to 40 years of age, and senior citizens

aged 60 years and above (working and not working) living within a 30-kilometer radius from

the city centre. A total of nine household categories were selected, as listed below:

● Single-person (public transport user)

● Single-person (car owner)

● Married without children

● Married with one child

● Married with two children

● Senior single

● Senior couple

● Single Parent with one child

● Single Parent with two children

5.1 Focus Group Discussion (FGD)

The first wave of data collection began in Klang Valley, of which 11 (eleven) Focus Group

Discussions (FGDs) comprising 69 participants were conducted. The first two FGDs were

intended to develop the definition of the designated costs of living as well as a pre-test for

developing the survey questionnaires. Subsequent FGDs were carried out to obtain the basic

understanding on expenditure patterns and categories of expenditures for urban households,

to validate the survey results and to arrive at a consensus on the basket of items and its costs

thereof.

The participants included researchers from local universities, representatives from Employees

Provident Fund (EPF), Credit Counseling, Debt Management Agency (AKPK), Economic

Planning Unit (EPU), The National Wage Council, NGOs, Bank Negara Malaysia (BNM),

practitioners from various industries including financial institutions and real estates, financial

planners, nutritionists, and reference individuals from specific households.

The second wave of data collection was performed via FGDs with the objective of developing

Belanjawanku for additional cities in Malaysia, namely Alor Setar, Kota Kinabalu, Johor Bahru

and Kuala Terengganu. A total of 97 (ninety-seven) FGDs were conducted involving 491

participants living and working within a 30-kilometer radius of the cities concerned. The series

of FGDs were conducted between July 2019 to March 2020.

115.2 Questionnaire Survey

A survey was conducted in Klang Valley to investigate the actual spending patterns of

individuals and families using structured questionnaires adapted from the Household Income

and Expenditure Survey (HIES) 2009 questionnaire, Department of Statistics, Malaysia; as well

as inputs from the earlier section of the qualitative study. A purposive sampling method was

employed targeting working individuals and couples between the ages of 18 to 40 years old

working in Klang Valley and living within a 30-kilometer radius from their workplace.

In the interest of time and cost, the survey was conducted via self-administered as well as face-

to -face interviews. A total of 1,200 structured questionnaires were distributed where 756

(63%) questionnaires were returned and 677 (56%) were found to be usable. The data

collected between March to July 2018 generated valuable information towards the

development of Belanjawanku 2019 for Klang Valley.

As for Belanjawanku 2020, for Klang Valley, telephone interviews were conducted with

reference individuals from past FGD groups. For Belanjawanku 2021, a survey was conducted

online to update the figures for Klang Valley as well as for additional cities included in our study

for 2020 namely Alor Setar, Kota Kinabalu, Kuala Terengganu and Johor Bahru. The survey

was conducted via Google forms and sent to selected existing email contacts of which a total

of 69 had responded.

5.3 Price Survey

In order to obtain indicative costs of goods and services, price surveys on the proposed item

baskets were done prior to conducting the FGDs in all the respective cities. The price surveys

were carried out at actual business premises such as supermarkets, wet markets, local

sundries / convenience stores and pharmacies.

Additionally, information was also gathered from published documents from Department of

Statistics Malaysia (DOSM), BNM, various ministries and their agencies, local energy and utility

providers and reports from local governments in various states across Malaysia.

The prices were used as indicative costs for the item baskets and as a guide for facilitators

during the FGDs. However, caution was exercised by the facilitators in order not to influence

the participants' responses, thus avoiding researcher bias.

5.4 Delphi Method

Due to the MCO which began on 18 March 2020, data collection via FGDs could not be

employed for the remaining cities, namely Kuantan, Kota Bharu, Georgetown, Kuching, Ipoh,

Melaka and Seremban. A Delphi Method was instead utilised, via a series of interactive

questionnaires sent to reference individuals from each household category as per the nine

target groups mentioned above. Experts comprising of academicians in the selected cities

were also recruited as participants. This method of data collection was used with a goal of

reaching a group consensus.

126. Constructing Belanjawanku

The construction of Belanjawanku involved seven stages. Each phase involved various groups

of discussants as follows:

Table 6: Construction of Belanjawanku

Stage Group Purpose

1 Orientation Group To discuss and agree on an acceptable minimum and the

• Experts definition of designated standards of living

• Academicians

• Research Team

2 Experts Consultation To identify and develop item baskets and classify

& Research Team household components

3 Task Group To discuss, negotiate and agree on acceptable minimum

• Representatives from items required and the costs thereof, so as to provide an

various household indication of the minimum acceptable amount

categories

• Facilitators

4 Consensus Group To review and adjust item compositions, prices and life

• Representatives selected span of baskets of goods and services in order to obtain a

from each household consensus

group

• Facilitators

5 Check back / Review Group To review the budgets, look at anomalies in budget

• Academicians patterns on the total budget costs and challenge the

• Experts consensus, if need be, to draft budget estimates

• Researchers

6 Research Team & Workshops and discussion for presentation and approval

Stakeholders’ by stakeholders

Representatives

7 Research Team Final draft of budget estimates for approval by

stakeholders

6.1 Defining Standard of Living

In stage one of the Belanjawanku preparation, participants in the ‘Orientation Group’ which

consist of academicians and experts agreed that the standard of living in question be defined

as:

“Having adequate financial resources to afford not just the minimum basics

but also the ability to participate in a society for a reasonable and dignified living”

(Social Wellbeing Research Centre, 2019)

136.2 Defining Household Categories

In order to allow for varying needs of different household categories, in stage two, the FGD

participants of expert group and researchers agreed that the age groups and composition of

household members be referred to as follows:

● Single individuals, single parents and married couples: 18 to 40-year-old males and

females

● Child 1: newborn to 6-year-old males and females

● Child 2: 7 to 13-year-old males and females

● Married with one child: male and female partners with Child 1

● Married with two children: male and female partners with Child 1 and Child 2

● Senior single and couples: 60-year-old and older, males and females

● Single parent with one child: male or female parent with Child 1*

● Single parent with two children: male or female parent with Child 1 and Child 2*

As for Klang Valley, updates were made to include the changes in costs for 2021 as well as

the new categories of households, *namely single parents with one and two children. This was

made after obtaining feedback and inputs from stakeholders, taking into consideration the

costs of living and different amounts of expenses incurred by these two categories of

households.

6.3 Development of Item Baskets

Item baskets herein refer to baskets of goods of consumer products and services of which the

selection is adapted from the DOSM’s Household Income and Expenditure Survey (HIES),

2009. Participants agreed that the following general assumptions be used as a basis for

development of item baskets:

● Access to healthcare services is universal

● Access to primary and secondary education is universal

● Housing cost for a single person is based on rental value

● Housing cost for families is based on estimated monthly mortgage repayment or rental

value, whichever is lower

● Children are sent to babysitters (no domestic maid)

● Where price survey is not possible, the pricing criterion for basket will be the price

unanimously agreed by participants of the FGDs

● Couples are assumed to own a car and a motorcycle

● Travel distance to and from work is within 30 km radius

● People are generally healthy

● People are informed and have the necessary competence to make informed decisions

● The retailers / shops are reachable and accessible for all households

● Households are not expected to buy second-hand goods, nor are they dependent on

receiving free items from friends or families

146.4 The Agreed Item Baskets

Participants in the focus groups also agreed that the item baskets should include food and

non-alcoholic beverages, housing, transportation, utilities, personal care, healthcare,

childcare, ad-hoc expenses, social participation and to some extent, discretionary expenses

(Diagram 6.1).

Diagram 6.1: Item Baskets

Basket Description

Food & non-alcoholic beverages consisting of groceries for home cooking,

eating out and takeaways

1. Single person - cost is based on monthly rental for fully furnished rooms

2. Married / Families / Elderly Single / Couples / Single Parents - cost is

based on monthly housing loan repayment / rent, whichever is lower

Monthly bills for water, electricity, pre / postpaid telephone / internet /

personal data plan and ASTRO TV

1. Public - all public transportation using season tickets or monthly passes

(where available)

2. Private vehicles - including vehicle loan instalment, fuel, highway tolls

and parking charges

Includes care for body, hair and feminine hygiene, oral hygiene and basic

personal grooming

3 x visits to private doctors (general practitioners) and 1 x visit to private

dentists a year for treatment of common non-acute illnesses or injuries

(annual total divided by 12 months)

1. Child 6 years and below - baby-sitting, diapers, milk and baby food

2. Child 7-13 years - including daycare, pocket money, tuition, religious

classes and extra-curricular activities

Ad-hoc / one off expenses consisting of vehicle maintenance, road tax &

insurance, school registration fees, clothing & footwear, instalment of

furniture & domestic appliances, maintenance of household furniture &

appliances (annual total divided by 12 months)

Includes festive celebrations, birthdays, anniversaries, invitations to

weddings etc. (annual total divided by 12 months)

Includes contribution to parents, medical insurance, sports and recreation

as well as vacation, depending on individual priorities (annual total divided

by 12 months)

15Amount allocated for each household is based on the focus group

participants’ indication of their ability to save and how much is deemed to

be sufficient

6.5 Pricing Criteria

The data on prices of goods and services (items in the basket) were obtained via online

shopping sites, catalogues and surveys at selected business premises. The sites for obtaining

data on prices, whether online or at the business premises, are taken from popular examples

which include Lazada, Shopee, Tesco, Giant, Mydin, Guardian, Watsons and local

supermarkets popular among the locals.

For cost calculation, the first quartile (25th percentile) price on product brands range was

taken as the cut-off point. Where product choices are limited, the average price was used.

Special offers and festive season prices were not considered in order to eliminate seasonal

fluctuations.

For consistency, special offers/discounts/seasonal prices are not considered. Prices are

applicable during the specific survey period.

Expenses that are not incurred monthly are calculated based on annual total divided by 12

months to get an average monthly cost

167. Development of Item Baskets

Based on the agreed number of item baskets and their pricing criteria, the individual item

baskets were further developed with the following details:

7.1 Development of Food Baskets

Food Baskets refer to food and non-alcoholic beverages. The baskets comprises of home

cooked food, dine in and takeaway. As a general principle for food security1, the development

of the food baskets is based on the Malaysian Dietary Guideline (MDG) 2017, set by the

Ministry of Health, Malaysia. The MDG is the official healthy eating guide for Malaysians which

is based on nutritional requirements according to the Recommended Nutrient Intakes (RNI,

2017). The energy intake recommended by the MDG is between 1,500 – 2,500 calories per

person per day (with reference to age group of between teen children to adults).

For the purpose of this study, an average of 2,000 calories per person per day is applied for a

reference family of four. Based on the RNI 2017, we listed the items according to the

recommended Malaysian Food Pyramid 2010 and allocated the quantity required for

consumption and its costs, on a monthly basis. In order for the food baskets to be adequate,

the underlying premise for the construction food baskets are as follows:

● The function of the food is for fulfilling basic nutrition as well as for a reasonable

amount of social and gastronomic purpose (pleasure)

● People have the capacity and time to cook healthy meals at least once a day

● Food baskets are healthy, varied and balanced

● Costs of take-away meals and dining out is traded off with costs of home cooking

● Baskets only cover costs directly related to food - other costs (such as

transportation or getting sufficient information) are to be covered by other baskets

● Individuals and households consume food 5 times a day, namely breakfast, lunch

and dinner, as well as morning and afternoon tea breaks

7.1.1 Pricing Criteria for Food Baskets

Prices for baskets of food and groceries for home cooking were obtained from the actual

business premises of popular wet markets, supermarkets and local sundry shops

encompassing various locations in the cities selected for Belanjawanku study. The product

choice was taken from four (4) or more popular product brands. The 25th percentile price is

taken for calculation of costs and cross checked online for comparison with DOSM’s selected

CPI list of selected goods and services, Federal Agricultural Marketing Authority (FAMA),

Fisheries Development Authority of Malaysia (LKIM) and Ministry of Domestic Trade and

Consumer Affairs (KPDNHEP).

1

Food security refers to the condition in which all people have access to sufficient safe and nutritious food that

meet their dietary needs and food preferences for an active and healthy life – United Nations Committee on World

Food Security, 1996

17Costs for dining out and takeaways were obtained from the average food prices at food courts,

and mid-range restaurants as well as food delivery services sites (Grab and Food Panda)

serving mixed rice (nasi campur), cooked / fried rice or noodles, across various locations in

the selected cities.

While Klang Valley prices were updated based on comparison with the prevailing price listing

and verification from former participants of FGDs, prices for the other cities were collated via

actual visits to the business premises in Kota Kinabalu, Johor Bahru, Kuala Terengganu, Alor

Setar, Kuantan, Kota Bharu, Georgetown, Kuching, Ipoh, Seremban and Melaka.

The focus group participants comprising reference persons of each household categories

agreed that the amount of monthly expenses to be allocated on food and beverage are as

follows (Table 7.1):

Table 7.1: Estimated Monthly Expenses (RM): Food

Household Category

Single Single Married Married Married Senior Senior Single Single

(Public (Car (w/o (1 (2 Single Couple Parent Parent (2

City /Region Transport Owner) Children) Child) Children) (1 Children)

User) Child)

Klang Valley 580 580 920 1350 1610 580 890 1010 1270

Alor Setar 500 500 790 1100 1310 500 760 820 1030

K. Kinabalu 550 550 850 1200 1430 550 830 900 1120

Johor Bahru 580 580 900 1330 1590 580 890 1010 1270

K. T'ganu 540 540 840 1170 1390 540 820 880 1100

Kuching 540 540 840 1170 1390 540 820 870 1090

Kuantan 540 540 840 1170 1390 540 820 880 1100

Kota Bharu 510 510 810 1120 1330 510 780 830 1040

Georgetown 560 560 880 1310 1560 560 860 990 1240

Ipoh* 550 550 850 1190 1430 550 830 890 1120

Seremban* 550 550 860 1220 1450 550 840 900 1140

Melaka* 550 550 850 1200 1430 550 830 890 1120

*Preliminary

7.2 Development of Housing Baskets

Housing is the largest monthly expenditure for any household in Malaysia. On average, it

commands around 24 percent of total monthly expenditure (DOSM, 2016). Housing

affordability is one common concern in discussing the issues related to urban housing. Based

on the standards set by the Office of the United Nations Office of The High Commissioner for

Human Rights (OHCHR), there are six central elements of adequate housing which must, at a

minimum, meet the following criteria:

● Security of tenure

● Affordability

● Habitability

18● Accessibility of location

● Cultural adequacy and social acceptability

● Availability of services, materials, facilities and infrastructure

The locations of accommodations are taken from within 30km radius of the urban districts of

Klang Valley, Kota Kinabalu, Johor Bahru, Kuala Terengganu, Alor Setar, Kuantan, Kota Bharu,

Georgetown, Kuching, Ipoh, Seremban and Melaka. Although there are no detailed profiles in

terms of specific neighbourhoods, the locations chosen in this study, must generally at the

very least, have access to employment and important amenities such as education and

healthcare, as outlined by the United Nations OHCHR (2014).

For the calculation of the reference budgets, as much as possible, we evaluate the adequate

housing principles outlined by the United Nations OHCHR, with particular emphasis on aspects

of affordability, which refer to ‘Personal or household financial costs associated with housing

should not threaten or compromise the attainment and satisfaction of other basic needs.”

(OHCHR, 2014: 4).

7.2.1 Pricing Criteria for Housing Baskets

Calculation of the housing costs is based on the following assumptions:

● A single person rents a fully furnished room

● Couples and families rent or own a 3-bedroom apartment/single/double storey link

house

● Except for a single person, the calculation of accommodation costs for families is taken

from the market rental values of unfurnished property or monthly mortgage

repayments, whichever is lower. For the latter, the property is low to medium cost of

RM200,000

● The costs of maintenance of the property, furniture and fittings, electrical appliances

and utilities are not included as part of the rental, as these are covered by other

baskets

The data collected were average room rental and house rental rates for four types of houses

namely flats, apartments and single / double storey link-houses from the selected districts used

in this study. References were also made to the National Property Information Centre (NAPIC)

to obtain insights on the current trend of real estate prices in Malaysia. Property prices were

also calculated based on prevailing market prices of PR1MA, Rumawip and affordable housing

under the Rumah Selangorku program as well as the individual states’ affordable housing

programs. Based on our calculation, the following are the estimates for housing costs for

different households (Table 7.2):

19Table 7.2: Estimated Monthly Expenses: Housing

Household Category

Single Single Married Married Married Senior Senior Single Single

(Public (Car (w/o (1 (2 Single Couple Parent Parent (2

City /Region Transport Owner) Children) Child) Children) (1 Children)

User) Child)

Klang Valley 370 370 1000 1000 1000 700 700 1000 1000

Alor Setar 200 200 580 580 580 400 400 580 580

K. Kinabalu 250 250 750 750 750 580 580 750 750

Johor Bahru 250 250 750 750 750 580 580 750 750

K. T'ganu 220 220 620 620 620 400 400 620 620

Kuching 250 250 670 670 670 460 460 670 670

Kuantan 230 230 600 600 600 410 410 600 600

Kota Bharu 200 200 580 580 580 400 400 580 580

Georgetown 300 300 900 900 900 680 680 900 900

Ipoh* 240 240 600 600 600 440 440 600 600

Seremban* 280 280 800 800 800 540 540 800 800

Melaka* 250 250 700 700 700 470 470 700 700

*Preliminary

In calculating the acceptable housing expenditure, comparisons were made between the

monthly costs of room / house rental to mortgages. For rental rates, the average flat / house /

room rental for several districts were obtained online at www.mudah.my and www.ibilik.com

as well as from the focus group discussions

7.3 Development of Transportation Baskets

Transportation is an essential element in estimating the costs of living in cities. People need

transport to get to work, to get access to goods and services that they need as well for social

engagements.

Living in a city that is highly populated means higher transportation costs due to the possibility

of living farther away from the workplace, as well as higher costs of parking and petrol

consumption. Calculating transportation costs is in general rather complicated as there are

various options or modes of transportation available.

There are also other different costs involved with each transportation mode for instance driving

involves tolls, petrol and parking fees which are not applicable to public transportation.

However, given the norms of the society where public transportation more often than not

becomes the second best alternative due to relatively inefficient systems as well as our climate

factor, we do include in our reference budget, the case where a single individual household

owns a car instead of using public transportation.

20Bearing in mind that the objective of this budget is to offer a guideline for an acceptable

standard of living with minimum expenditure, several assumptions were adopted in estimating

the transportation costs:

● Singles from 2 categories, either public transport users who commute using public

transportation such as buses, LRTs, MRT or commuter trains, or private car owners

● Couples who own a car and a motorcycle

● The type of car owned for single individuals and couples is a 1,000cc engine, while the

motorcycle is a 125cc engine. The assumption on type of car ownership is important

for estimation of petrol costs and vehicle maintenance, as well as the monthly

installment for the vehicles

● For senior couples, we assume that they own one car, hence, the lower transportation

costs for the seniors

● Transportation is mainly used for commuting to the workplace, running errands and

occasional visits to meet families and friends. The travelling distance is taken as 30km

to and from making a total of 60km per day, 30 days a month

● Transportation costs for other purposes are covered in other baskets

7.3.1 Pricing Criteria for Transportation Baskets

For public transportation, we take the average for all modes of transportation covering various

destination terminals within 30km radius.

As mentioned earlier, estimating expenses for private transportation involve more than one

component. Firstly, the monthly installment. Again, for the purpose of meeting the minimum

expenditure, we base such calculation on a vehicle loan with 100 percent margin of finance

(zero down payment) at the cheapest (prevailing) interest rate offered in the market at the time

of study for a tenure of 9 years. The same method is adopted in estimating the motorcycle

monthly installment, but with a shorter tenure of 5 years.

Meanwhile, the calculation of toll rates for cars is based on what is available on the official

website of Lembaga Lebuh Raya Malaysia. Parking rates are estimated using the season

parking rates for city councils, e.g. for Klang Valley, DBKL Car Monthly Parking Rental.

Based on the focus group discussions and our calculation, the monthly installment of a new

1,000cc car and 110cc motorcycle obtained from market surveys, plus the fuel, highway tolls

and parking charges; the estimated expenses for transportation are as follows (Table 7.3):

21Table 7.3: Estimated Monthly Expenses: Transportation

Household Category

Single Single Married Married Married Senior Senior Single Single

(Public (Car (w/o (1 (2 Single Couple Parent Parent (2

City /Region Transport Owner) Children) Child) Children) (1 Children)

User) Child)

Klang Valley 140 760 990 1000 1010 490 490 770 780

Alor Setar 130 620 840 850 860 490 490 630 640

K. Kinabalu 110 590 820 830 840 490 490 600 610

Johor Bahru 130 620 840 850 860 490 490 630 640

K. T'ganu 150 640 860 870 880 490 490 650 660

Kuching 90 580 810 820 830 490 490 590 600

Kuantan 140 620 840 850 860 490 490 630 640

Kota Bharu 120 650 870 880 890 490 490 660 670

Georgetown 140 690 910 920 930 490 490 700 710

Ipoh* 80 630 850 860 870 490 490 640 650

Seremban* 90 630 850 860 870 490 490 640 650

Melaka* 130 630 850 860 870 490 490 640 650

*Preliminary

It is noteworthy that when making comparisons for transportation expenses, the amount

increased almost threefold when a single person chooses to buy his own car instead of using

public transportation.

7.4 Development of Utility Baskets

The utility baskets consist of expenses on:

● Mobile telephones

● Cable TVs

● Internet

● Water

● Electricity

In considering the cost for each utility basket, we include the functions of utilities as an integral

part of human existence. Water for instance is used for drinking, cooking, washing and

cleaning. Electricity is used for lighting, cooking, heating, cooling, refrigeration; and operating

appliances such as computers, electronics and machinery. Whereas internet, communication

and entertainment are essential for human interactions and communication, education,

shopping and leisure. as well as entertainment. Therefore, in developing costs for the utility

baskets, the following pricing criteria was used:

227.4.1 Pricing Criteria for Utility Baskets

For calculation of household electricity cost, the underlying premises are:

● A single person shares the monthly bill with other 'housemates’

● For couples and families, the pricing of electricity bills is calculated based on the tariff

per kWh of total power consumption on a list of common household electrical

appliances obtained from the official website of Tenaga Nasional Berhad (TNB) for

states in Peninsular Malaysia, Sabah Energy Corporation Sdn Bhd for Sabah and

Sarawak Energy Berhad for Sarawak

For the pricing of internet, communication and entertainment, the following assumptions are

applied:

● A single person subscribes to a personal data plan package for telephone and internet,

and does not subscribe to home internet package and cable TVs

● Couples and families individually use personal data plan for mobile telephones, and

one household member subscribes to a home internet package and private cable TV

for the house

● The choice of product is made based on the relative value-for-money and the breadth

of coverage which may not necessarily be the cheapest

● It is also assumed that the head of household pays for a family pack basic TV

entertainment and internet plans

The source of pricing is obtained online from the official websites of local mobile data

providers, (e.g., Maxis, Unifi and Digi) and the official websites of the energy and water

providers of the states where the cities are located.

For calculation of water bills, prices are obtained from the official websites of the local water

concessionaires. In Klang Valley for example, the estimates were obtained from calculation of

average 26 cubic meters for 30 days of domestic use by Air Selangor. On average, a Malaysian

uses about 220 litres of water each day. For comparison purposes, calculation for other states,

however, shows negligible difference.

After taking into consideration all three main items as above, the focus groups participants

proposed that the amount of monthly expenses to be allocated on total utility bills are as follows

(Table 7.4):

23Table 7.4: Estimated Monthly Expenses: Utilities

Household Category

Single Single Married Married Married Senior Senior Single Single

(Public (Car (w/o (1 (2 Single Couple Parent Parent (2

City /Region Transport Owner) Children) Child) Children) (1 Children)

User) Child)

Klang Valley 90 90 310 320 330 150 290 270 280

Alor Setar 90 90 300 310 320 150 290 250 260

K. Kinabalu 90 90 280 290 300 130 260 240 250

Johor Bahru 90 90 300 310 320 150 290 250 260

K. T'ganu 90 90 300 310 320 150 290 250 260

Kuching 90 90 280 290 300 130 260 240 250

Kuantan 90 90 300 310 320 150 290 250 260

Kota Bharu 90 90 300 310 320 150 290 250 260

Georgetown 90 90 300 310 320 150 290 250 260

Ipoh* 90 90 300 310 320 150 290 250 260

Seremban* 90 90 300 310 320 150 290 250 260

Melaka* 90 90 300 310 320 150 290 250 260

*Preliminary

7.5 Development of Personal Care Baskets

The underlying premise for construction of a personal care basket is that they are essential for

good daily hygiene and that different parts of the body require different considerations with

regard to hygiene. Therefore, we make a distinction between the following:

● Hand hygiene

● Oral hygiene

● Body hygiene

● Intimate hygiene for women

● Shaving

● Hair care

● Skin care

● Haircuts / basic personal grooming

● Basic bathroom equipment

7.5.1 Pricing Criteria for Personal Care Baskets

For the development of this basket, people are assumed to be generally in good health and

have no particular allergy or disability. The baskets only cover costs directly related to personal

care. For products and brands and the choice of shops, the basket takes into consideration

the price, quality, variety and number of stores for easy accessibility. The shops chosen are

popular ones available such as Watsons, Guardian Pharmacy, Caring Pharmacy, Giant and

Tesco. The product choices are taken from the top sellers / leading popular brands. Again, the

2425th percentile price applies, however wherever the number of products or brands are limited,

the average prices are used.

Although there are slight variations in the focus group discussions between men and women

in terms of personal care needs, participants agreed that the amount of monthly expenses to

be allocated for personal care are as follows (Table 7.5):

Table 7.5: Estimated Monthly Expenses: Personal Care

Household Category

Single Single Married Married Married Senior Senior Single Single

(Public (Car (w/o (1 (2 Single Couple Parent Parent (2

City /Region Transport Owner) Children) Child) Children) (1 Children)

User) Child)

Klang Valley 70 70 100 120 140 60 90 90 110

Alor Setar 70 70 100 120 140 60 90 90 110

K. Kinabalu 70 70 100 120 140 60 90 90 110

Johor Bahru 70 70 100 120 140 60 90 90 110

K. T'ganu 70 70 100 120 140 60 90 90 110

Kuching 70 70 100 120 140 60 90 90 110

Kuantan 70 70 100 120 140 60 90 90 110

Kota Bharu 70 70 100 120 140 60 90 90 110

Georgetown 70 70 100 120 140 60 90 90 110

Ipoh* 70 70 100 120 140 60 90 90 110

Seremban* 70 70 100 120 140 60 90 90 110

Melaka* 70 70 100 120 140 60 90 90 110

*Preliminary

7.6 Development of Healthcare Baskets

Although the general premise is that healthcare is universal, it is not realistic to expect people

to visit government hospitals every time they contract a common illness such as the common

cold, influenza, sore throat and toothache. Therefore, the recommended medical care (adults

and children) includes a limited number of private general practitioners (GP) and dentist

consultations a year.

Healthcare baskets also take into consideration contraception for women and men as well.

Besides it being important for couples to plan their family size, contraception also helps to

reduce the risks of pregnancy related morbidities and unplanned pregnancies; thus, promoting

physical, mental and emotional wellbeing for mothers and fathers. The distinction between the

functions that the baskets should fulfill are:

● Care for common illnesses and minor injuries

● Oral / dental care

● Male and female contraception

● A basic family medical chest

257.6.1 Pricing Criteria for Healthcare Baskets

Household members are assumed to generally be in good health and not suffering from

chronic illnesses or severe allergies. They are also assumed to be well-informed about how to

use health care safely and effectively.

The indicative prices for private medical consultations with GPs are taken from Malaysian

Medical Association Fee Guideline (MMA), 2017; as well as from price checks with several GP

clinics for each city, via telephone calls and verification through focus group discussions.

The calculation of care and budget estimations for common illnesses and minor injuries are

for an average of three visits per annum for each individual / family member. As for dental

examinations / treatment, each household member is assumed to make one visit per year. In

addition, the contents for basic family medical chests include aspirin / paracetamol for fever,

antiseptic creams for small cuts and wounds along with a basic first aid-kit which can be

purchased from local pharmacies.

On a different note, the costs for contraception (male and female), include the costs of

Implanon (for women) and 36 condoms per year (for men and women). The costs for

contraception (for women) were taken from the official website of the Family Planning &

Fertility Treatment division of the Ministry of Women, Family & Community Development,

Malaysia.

During the focus group discussions, participants agreed that since expenses on healthcare is

not necessarily a regular occurrence, the amount of expected expenses to be allocated over

a monthly average are as follows (Table 7.6):

Table 7.6: Estimated Monthly Expenses: Healthcare

Household Category

Single Single Married Married Married Senior Senior Single Single

(Public (Car (w/o (1 (2 Single Couple Parent Parent (2

City /Region Transport Owner) Children) Child) Children) (1 Children)

User) Child)

Klang Valley 30 30 70 100 120 70 140 60 80

Alor Setar 20 20 40 60 70 50 100 40 50

K. Kinabalu 20 20 40 60 80 60 120 40 60

Johor Bahru 30 30 60 90 110 60 130 60 80

K. T'ganu 20 20 40 60 80 60 120 40 60

Kuching 20 20 40 60 80 60 120 40 60

Kuantan 20 20 40 60 80 60 120 40 60

Kota Bharu 20 20 40 60 80 60 120 40 60

Georgetown 30 30 60 90 110 60 130 60 80

Ipoh* 30 30 60 80 100 50 110 50 70

Seremban* 30 30 60 90 110 50 110 60 80

Melaka* 30 30 60 80 100 50 110 50 70

*Preliminary

26You can also read