EVs/Autonomous Driving - Tesla and the auto revolution

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2022 Outlook | November 29, 2021 EVs/Autonomous Driving Tesla and the auto revolution Yeon-ju Park yeonju.park@miraeasset.com Analysts who prepared this report are registered as research analysts in Korea but not in any other jurisdiction, including the U.S. PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES & DISCLAIMERS IN APPENDIX 1 AT THE END OF REPORT.

Contents I. [EVs] The road to Tesla’s Model 2 3 II. [Autonomous driving] Game changer 12 III. [Auto market] Momentum to be stronger in 1H than in 2H 24 [Conclusion] Tesla and the auto revolution 26 2 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities Research

I. [EVs] The road to Tesla’s Model 2

Upside to market • Global electric vehicle (EV) market forecasts have seen steady upward revisions, especially since the outbreak of

COVID-19, thanks to policy support in major economies and the release of attractive new models.

forecasts

• That said, we still view EV penetration forecasts for 2030—30-40% on average—as conservative.

• As Tesla-led technological innovation accelerates in 2022, we expect EVs to reach price parity with conventional

vehicles sometime around 2023, prompting further boosts to forecasts.

Tesla EV production cost est. (based on standard-range models) EV penetration outlook

(US$) (%)

Battery Non-battery materials/parts Fixed Previous Revised

35,000 60

30,000

25,000

40

20,000

15,000

20

10,000

5,000

0 0

2021F 2023F 2020 2025F 2030F

Source: Mirae Asset Securities Research Source: Mirae Asset Securities Research

3 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities Research

I. [EVs] The road to Tesla’s Model 2

1) Battery innovation: • Since 2021, Tesla’s Model 3 and Model Y manufactured in China have been running on LFP batteries. The

adoption of LFP batteries has helped the automaker increase sales by lowering production costs/ASP. Beginning

LFP batteries going

in 2022, the company will also adopt the batteries in models sold in the US, Europe, etc.

global in 2022 • The adoption of LFP batteries should help: 1) lower battery production costs; 2) encourage competition among

battery suppliers, accelerating cost reductions; and 3) ease battery shortages, which have held back Tesla’s

efforts to expand production.

• LFP battery makers have rapidly expanded capacity recently. Compared to LFP batteries, capacity expansion has

been limited for ternary lithium batteries due to the small number of producers and technological challenges.

LFP vs. ternary lithium batteries (standard-range Model Y) CATL: Battery capacity expansion plans

(GWh)

Cell-to-pack 2170

LFP battery (ternary cylindrical) 800

Energy density (Wh/kg) 125 161

600

Battery weight/kWh (kg) 8.0 6.2

Battery capacity (kWh) 60 55 400

Battery weight (kg) 480 342

200

Battery costs (US$/kWh) 110 170

Battery pack cost (US$) 6,600 9,350 0

2019 2020 2021F 2022F 2023F 2024F 2025F

Note: Battery costs are our estimates. Source: Industry data, Mirae Asset Securities Research

Source: Industry data, Mirae Asset Securities Research

4 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities Research

I. [EVs] The road to Tesla’s Model 2

1) Battery innovation: • LFP batteries cannot be used in long-range models and pickup trucks that require larger battery capacities. As

such, mass production of more powerful 4680 cells is important.

Mass production of

• 4680 cells enable smaller battery packs, as fewer cells are required per vehicle—only one-fifth the number

4680 cells required by existing 2170 batteries. (Battery packs account for a large share of production costs for cylindrical

batteries.) The higher energy density of 4680 cells also means that smaller battery capacities are needed. Overall,

4680 cells will be able to match LFP batteries in terms of cost reductions.

• Panasonic recently stated that it had resolved most of the technological issues associated with 4680 battery

production and would start test production in Mar. 2022. Mass production is expected to begin around 2023 at

Panasonic and LG Chem.

No. of battery cells per vehicle (est.) % of non-cell costs in overall battery pack costs to decline

(No.) (US$/kWh) (%)

5,000 180 Cell costs (L) Non-cell costs (R) Non-cell/pack costs (R) 40

150

4,000

30

120

3,000

90 20

2,000

60

10

1,000

30

0 0 0

2170 4680 Cylindrical (2170) Pouch-type

Source: Industry data, Mirae Asset Securities Research Source: Cairn Energy Research Advisors, Mirae Asset Securities Research

5 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities Research

I. [EVs] The road to Tesla’s Model 2

2) Production innovation: • From 2022, Tesla plans to use Giga Press machines to create front underbody castings (in addition to rear

underbody castings). The EV maker aims to eventually introduce structural battery packs that can be joined with a

Giga Castings

single-piece front/rear underbody casting.

• Single-piece castings (Giga Castings) allow simpler and cheaper underbody production and help reduce fixed

costs by improving yields.

• The use of lightweight aluminum should also help improve driving range and reduce battery costs.

Tesla’s aluminum alloy vs. ultra-high-strength steel: Strength and

Tesla’s Giga Castings (rear underbody)

body weight comparison

(x, kg)

300 Ultra-high-strength steel Tesla’s aluminum alloy

250

200

150

100

50

0

Strength-to-weight ratio (x) Body weight (kg)

Source: Tesla Battery Day, Mirae Asset Securities Research Source: Limiting Factor, Mirae Asset Securities Research

6 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities Research

I. [EVs] The road to Tesla’s Model 2

2) Production innovation: • Structural battery packs are designed to make batteries a structural component of a vehicle, thus reducing

overall weight and simplifying production processes.

Structural battery packs

• With this new battery architecture, Tesla is aiming for a 7% reduction in battery costs and a 10% reduction in

weight.

• Reducing overall vehicle weight helps save costs by creating room to pack more LFP batteries or enabling a

reduction in battery capacity.

Existing battery pack vs. structural battery pack Chg. in Tesla’s EV architecture and its effects

Battery costs 7% reduction

Range 14% improvement

No. of parts 370 fewer parts

Weight 10% reduction

Source: Tesla Battery Day, Mirae Asset Securities Research Source: Tesla Battery Day, Mirae Asset Securities Research

7 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities Research

I. [EVs] The road to Tesla’s Model 2

Road to the Model 2 • We estimate that Tesla’s technological innovations, if successful, will allow the firm to cut battery costs by roughly

25% (lighter vehicle weight, less battery consumption) and fixed costs by around 50% (stemming from sales

volume growth and architecture changes). As such, Tesla may achieve its US$25,000 target price for the Model 2.

• Cost competition will likely intensify in the EV industry as the Model 2 moves closer to production. The broader

adoption of LFP/4680 cells across the industry and increasing sales volumes should allow automakers to enjoy

economies of scale. Of note, Volkswagen is highly anticipated to introduce its next-generation Scalable Systems

Platform (SSP) earlier than planned; the new platform is designed to markedly improve production yields.

• EVs are forecast to achieve price parity with conventional cars around 2023 (starting with Tesla).

Tesla EV production cost est. (based on standard-range models) Volkswagen SSP: Cost reduction through integration

(US$)

Battery Non-battery materials/parts Fixed

35,000

30,000

25,000

20,000

15,000

10,000

5,000

0

2021F 2023F

Source: Mirae Asset Securities Research Source: Volkswagen, Mirae Asset Securities Research

8 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities Research

I. [EVs] The road to Tesla’s Model 2

Implications: • Tesla is forecast to sell 1.3-1.4mn units in 2022. However, we see ample room for growth, assuming the Berlin

and Texas factories go online.

1) Tesla’s sales volume

• Notably, sales volume could increase sharply once Tesla begins to roll out LFP battery-powered models in global

growth to surprise to the markets, such as the US and Europe. In China, EV sales jumped following the adoption of LFP batteries.

upside • Over the medium term, Tesla should be able to maintain its competitive edge over rivals. While battery

technology innovations should gradually spread across the industry, major architectural changes, such as Giga

Castings, do not seem easy for rivals to adopt due to a lack of alloy technology or equipment/machinery.

Tesla Giga Shanghai: Sales volume trends Tesla’s China sales volume (by anode material)

('000 units) ('000 units)

Domestic Exports 2020 Jan.-Sep. 2021

60 120

100

50

80

40

60

30

40

20

20

10

0

Model 3 Model Y Model 3 Model Y

0

1/21 4/21 7/21 10/21 NCM LFP

Source: CPCA, Mirae Asset Securities Research Source: Tesla, Mirae Asset Securities Research

9 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities Research

I. [EVs] The road to Tesla’s Model 2

Implications: • As cost competition intensifies, automakers may cut prices to compete against Tesla, delaying EV profitability.

2) Profitability to vary • Also, profitability could vary widely among automakers, depending on their scale, dedicated platforms, etc.

across automakers • Accordingly, companies may deploy various strategies in an effort to secure cost competitiveness, sharing EV

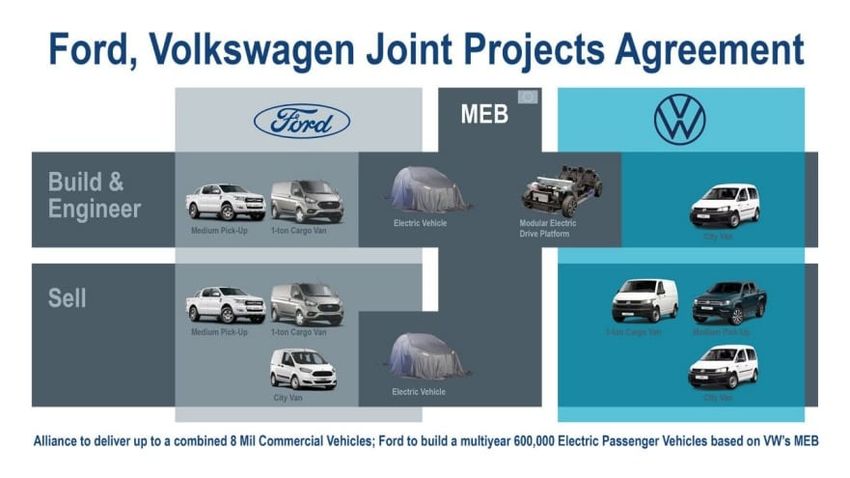

platforms (Volkswagen and Ford) and/or outsourcing components production or part of manufacturing.

Volkswagen vs. Toyota: 2019 sales volumes and 2030 EV sales targets Volkswagen and Ford share MEB platform

('000 units)

2019 sales volume 2030 EV sales target

12,000

10,000

8,000

6,000

4,000

2,000

0

Volkswagen Toyota

Note: Volkswagen targeting 50% EV share in 2030 sales; Toyota targeting over 1mn EV sales Source: Ford, Mirae Asset Securities Research

Source: Volkswagen, Toyota, Mirae Asset Securities Research

10 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities ResearchI. [EVs] The road to Tesla’s Model 2

Implications: • The EV supply chain has seen valuations steadily expand alongside end-market growth. We expect EV stocks’

multiple premiums to widen around 2023 as market forecasts are further revised upward.

3) Multiple expansion

• Meanwhile, lithium supply will likely tighten further, driven by faster-than-expected demand growth and wider

and lithium supply adoption of LFP batteries. Supply growth will be limited over the next two to three years, due to limited new

crunch investments amid plummeting prices in 2018-20. Furthermore, LFP batteries require more lithium per kWh than

ternary lithium batteries due to their lower energy density.

Lithium price trends Lithium supply/demand growth outlook

(US$/tonne) (%)

30,000 100 Demand growth Supply growth

80

20,000

60

40

10,000

20

0 0

12 14 16 18 20 22 21F 22F 23F 24F

Source: Korea Resources Corp., Mirae Asset Securities Research Source: Industry data, Mirae Asset Securities Research

11 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities ResearchII. [Autonomous driving] Game changer

Autonomous driving • We view autonomous driving software as a game changer for the auto industry. Indeed, we think software

competitiveness (rather than EV hardware) will be the key re-rating driver for auto stocks, as we see greater

software to be a game

upside (in terms of profit growth and multiple expansion) in automotive software than in EV manufacturing. Also,

changer the widening technological gaps among industry players could bring major changes to the competitive

landscape.

• We expect the auto industry to undergo a transformation like the one brought about by smartphones. As mobile

phones evolved from simple calling devices to handheld computers, the mobile device industry’s profits

expanded sharply. Subsequently, multiples expanded as software services began to contribute to profits.

• Nokia (no. 1 feature phone vendor) had a market cap of W175tr in 2007. In 2020, Apple’s exceeded W2,000tr.

Nokia vs. Apple: Market cap comparison Apple: Services revenue contribution and P/B

(US$bn) (%) (x)

2,500 25 Contribution of services revenue (L) 40

P/B (R)

2,000 20

30

1,500

15

13x 20

1,000

10

500 10

5

0

Nokia (38% M/S) Apple (14% M/S)

0 0

2007 2020 11 12 13 14 15 16 17 18 19 20

Source: Bloomberg, Mirae Asset Securities Research Source: Bloomberg, Mirae Asset Securities Research

12 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities ResearchII. [Autonomous driving] Game changer

Level 2+ autonomous • As cars evolve into computers on wheels, the industry’s profits and valuation multiples are likely to expand

sharply. Tesla is leading this evolution, with Level 2+ autonomy expected to play a pivotal role.

driving

• Tesla’s Level 2+ subscription service (US$199/month) still requires the driver to monitor the vehicle at all times,

but it helps reduce fatigue and improve safety. Its benefits will become even greater once urban autonomous

driving becomes commercially available.

• Assuming 40% of vehicles adopt Level 2+ subscription services globally over the medium term, the auto industry’s

profits and market cap are estimated to grow 4x and more than 20x, respectively.

Tesla: Breakdown of software-based service business Level 2+ subscription service market size and market cap estimates

Category Units Estimates

Category Notes

Annual sales mn units 97

ASP US$‘000 25

Autonomous

Level 2+ Full Self-Driving (FSD) option (US$10,000) Annual market size US$bn 2,425

driving

Conventional

Avg. OP margin % 6

vehicles/EVs

Avg. OP US$bn 146

Infotainment upgrade (US$2,500)

Infotainment P/S x 0.5

Premium connectivity (US$1,000)

Market cap US$bn 1,213

No. of vehicles in

mn units 1,500

Performance operation globally

Acceleration boost (US$2,000)

upgrade

Subscription service

% 40

penetration

Insurance Launched in California; further expansion likely Level 2+ Annual fee US$/unit 2,388

subscription

service Annual revenue US$bn 1,433

Robotaxi Ride-hailing service (scheduled to launch)

OP margin % 40

Platform Platform service operating on in-house-developed OS OP US$bn 573

P/S x 20.0

Other Charging, maintenance, gaming, etc.

Market cap US$bn 28,656

Source: Mirae Asset Securities Research Source: Mirae Asset Securities Research

13 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities ResearchII. [Autonomous driving] Game changer

Market size forecasts • In addition to the Level 2+ subscription service, Tesla offers various software-based services, including premium

connectivity, acceleration boost, and insurance. Once autonomous driving technology reaches Level 5, the firm’s

robotaxi and automotive OS-based platform services will also gain ground.

• Volkswagen projects its auto revenue to grow to EUR5tr in 2030 (from EUR2tr in 2020), with software contributing

EUR1.2tr.

Medium/long-term robotaxi market forecasts Volkswagen: Auto market outlook

Units Est.

No. of vehicles in operation globally mn units 1,000

Adoption rate % 40

No. of robotaxis in operation mn units 400

Annual revenue per vehicle US$ 10,512

Annual miles driven Miles 35,040

Utilization % 20

Distance/hour Miles 20

Revenue per mile US$ 0.30

Annual revenue US$bn 4,205

OP margin % 30

OP US$bn 1,261

Source: Mirae Asset Securities Research Source: Volkswagen, Mirae Asset Securities Research

14 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities ResearchII. [Autonomous driving] Game changer

Competitiveness gap to • The shift from hardware to software in the auto industry should widen the competitiveness gap among players.

widen • The proliferation of smartphones led to significant advances in hardware and software technologies.

• Of note, key software (including OS) segments came to be dominated by just two players, Apple and Google, due

to technological barriers and network effects. The two firms reap an outsized share of smartphone profits.

• As for smartphone hardware suppliers, Samsung Electronics (SEC) gained market share and profits thanks to its

partnership with Google. However, Nokia and Motorola lost ground as they wasted time trying to develop their

own OS.

Cell phone (hardware) M/S trends after smartphone revolution Smartphone OS M/S breakdown (2020)

(%)

40 Apple SEC Nokia LGE Motorola

iOS, 15.9%

30

20

10

Android,

84.1%

0

05 07 09 11 13 15

Source: IDC, Mirae Asset Securities Research Source: IDC, Mirae Asset Securities Research

15 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities ResearchII. [Autonomous driving] Game changer

Competitiveness gap to • In order to generate software-based revenue, automakers need to work on developing more centralized

architectures (allowing centralized vehicle control/operations) via integrated OS, the consolidation of

widen

engine control units (ECUs), etc.

• Going forward, we expect technological difficulty and funding needs to increase sharply (no. of code lines to

jump from 100mn to more than 500mn).

• Volkswagen channeled significant human/financial resources into building a partially integrated architecture

(VW.OS 1.1), but software issues caused problems in early mass production. The firm plans to invest W30tr to

strengthen its software competitiveness.

Electrical/electronic architecture evolution

Source: Yole, Mirae Asset Securities Research

16 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities ResearchII. [Autonomous driving] Game changer

Competitiveness gap to • Given automakers’ lack of experience in software development, it remains to be seen how successful they will be

in securing advanced software technology. In the case of smartphones, companies decided to partner with tech

widen firms in light of technological difficulties, long development times, and the importance of network effects.

• Furthermore, not all automakers have the means (both financial and technological) to develop their own

software. Indeed, companies selling a small number of cars will not be able to enjoy scale and network effects.

For these reasons, some will likely choose to partner with tech firms (as Daimler did with Nvidia).

• Given the time required for software development, we think strategic decisions that will be made over the next

couple of years could significantly affect competitive dynamics over the medium/long term. We also believe the

automotive software market will be more oligopolistic and create add more value than the hardware market.

Daimler to launch centralized architecture (2024) in partnership

Nvidia: Automotive pipeline

with Nvidia

Source: Bloomberg, Mirae Asset Securities Research Source: Nvidia, Mirae Asset Securities Research

17 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities ResearchII. [Autonomous driving] Game changer

Competition to intensify • With the introduction of Dojo (Tesla’s AI training supercomputer) in 2022, autonomous driving will likely capture

increased attention due to rapidly advancing technology.

• Dojo is designed to facilitate the development of self-driving technology. With Dojo, the speed of learning will be

several times faster than that achieved by rivals relying on existing supercomputers.

• At Level 2 autonomy (self-driving under limited conditions, such as highways), Tesla’s technological advantages

do not stand out much. Once autonomous driving in urban environments becomes available, however, the

adoption of self-driving subscription services—and the consumer preference for Tesla—should rise sharply,

further strengthening the automaker’s earnings performance and competitiveness over the medium/long term.

Training tiles of Dojo Dojo road map

Source: Tesla AI Day, Mirae Asset Securities Research Source: Tesla AI Day, Mirae Asset Securities Research

18 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities ResearchII. [Autonomous driving] Game changer

Competition to intensify • Tech giants such as Apple are expected to make inroads into autonomous driving, given: 1) their strength in

software; and 2) the market’s huge upside.

• As deep learning helps advance autonomous driving technology, securing real driving data is becoming

increasingly important. Moreover, securing an early lead in the market is also crucial due to network effects. As

such, we think tech firms need to make haste in their push into autonomous driving.

Key to deep learning lies in data quality Bloomberg report on the Apple Car

Source: Sumo Logic, Mirae Asset Securities Research Source: Bloomberg, Mirae Asset Securities Research

19 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities ResearchII. [Autonomous driving] Game changer

Competition to intensify • The overall performance of autonomous driving is improving with advances in AI technology and computing

power.

• In 2021, Mobileye disclosed footage of its test vehicles navigating New York City streets using only cameras,

showing significant improvements in performance. GM Cruise’s robotaxis have also reported major progress in

performance. Indeed, increasingly sophisticated deep learning algorithms and computer performance upgrades

are facilitating advancements in self-driving technology.

• Accordingly, we expect to see autonomous commercial vehicles in 2022-23, with some limitations (Level 3

autonomy under certain conditions only; Level 2 with more sophisticated functions).

Nvidia: Performance of autonomous vehicle platforms Commercial operation plans for autonomous vehicles (2022-23)

Company Plans

GM Commercial robotaxis in San Francisco (2022): Five

Cruise robotaxis between 10pm and 6am at speeds of up to

48km/h

Google Level 4 robotaxi business in Arizona since 2018;

Waymo commercial operation of driver-supported robotaxis in

San Francisco (2022)

Driverless commercial robotaxis in Las Vegas in 2023, in

Motional

partnership with Lyft (pilot operation to expand in 2H22)

Aurora Horizon (2023), a truck subscription service;

Aurora Aurora Connect (2024), a subscription-based ride-hailing

service

Source: Sumo Logic, Mirae Asset Securities Research Source: Press reports, Mirae Asset Securities Research

20 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities ResearchII. [Autonomous driving] Game changer

• Addressing edge cases is essential to the validation of autonomous driving technology. Deep learning algorithms

Tesla’s competitive are used to train AI to handle edge cases.

advantages • Tesla collects vast quantities of real-world driving data from its fleet of camera-equipped vehicles and uses the

data to train its autonomous driving AI. For this process, it is essential to accumulate large quantities of quality

data, design AI neural networks that can accurately handle such large amounts of data, and improve AI-training

supercomputer performance.

• Key factors differentiating Tesla from rivals include scalability (thanks to the relatively low cost of its camera-

based autonomous driving system) and vertical integration across hardware (EVs) and software (AI training).

Notably, the Dojo supercomputer (set to be operational in 2022) should markedly speed up the training of AI.

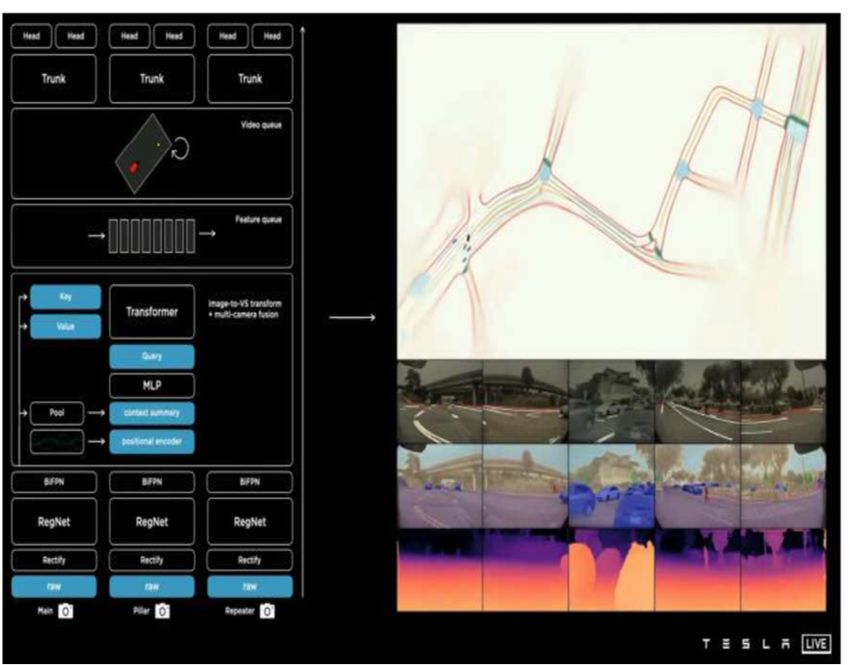

Tesla’s autonomous driving AI Tesla’s AI neural network architecture that processes driving data

Source: Tesla, Mirae Asset Securities Research Source: Tesla, Mirae Asset Securities Research

21 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities ResearchII. [Autonomous driving] Game changer

Implications: • Just as the rise of smartphones drove dramatic profit/valuation re-ratings in the mobile phone sector, we expect

the auto industry’s shift to software (e.g., autonomous driving) to drive up profit potential and multiples across

1) Tesla’s valuation

the sector.

• In the automotive software market, high technological requirements, robust data collection/processing

capabilities, and network effects could give rise to a winner-takes-most scenario.

• Tesla has been leading the industry’s transition and should maintain its competitive advantage over the medium

term, justifying its lofty valuation. We see further upside to its valuation, depending on how much and how

quickly autonomous driving technology advances.

Earnings and valuation comparison: Nokia vs. Apple Tesla’s autonomous driving business value projections (2030F)

(US$bn) (x)

Base case Bear case Bull case

300 Revenue (L) GP (L) P/S (R) 10

Cumulative sales (‘000 units) 61,010 61,010 61,010

8

Adoption (%) 60 30 100

200 FSD price (US$) 25,000 15,000 35,000

6

Monthly subscription

(depreciated over eight- 260 156 365

year period, US$)

4

Revenue (US$bn) 114 34 267

100

P/S (x) 20 20 20

2

Value (US$bn) 2,288 686 5,338

0 0 Present value (US$bn) 1,182 355 2,759

2007 Nokia (38% M/S) 2020 Apple (14% M/S)

Note: Discount rate of 8.6% was derived by applying risk-free rate of 1.1%, beta of 1.6x, and

Source: Bloomberg, Mirae Asset Securities Research expected market return of 5.7%

Source: Mirae Asset Securities Research

22 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities ResearchII. [Autonomous driving] Game changer

Implications: • New players find it relatively easy to enter the EV market thanks to the low barriers to entry. Of note, EV start-ups

are more agile than legacy automakers in responding to consumer needs and gaining market share. Recently,

2) Start-ups vs. Tesla

Rivian and Lucid have delivered robust share performances thanks to their compelling product features.

• Although EV start-ups are likely to grab a certain share of the market from legacy automakers, we think that

software competitiveness will assume greater importance than EV manufacturing in the medium term. In

particular, Tesla’s accumulated driving data and superior software technology will make it difficult for

competitors to catch up in the near future. As such, we prefer Tesla over EV start-ups.

2023F sales volume and market cap by EV maker Tesla: Est. market cap breakdown by business unit (12-month forward)

Market 2023 sales Market cap/

Company cap volume sales volume Services (other)

(US$bn) (‘000 units) (‘000 US$/units) 11% Hardware

17%

Tesla (total) 1,114 2,300 484

Tesla

446 2,300 194

(only hardware)

NIO 73 300 243

XPeng 44 400 110

Li Auto 33 300 109

Services

(autonomous

Rivian 107 200 534 driving)

72%

Lucid 86 90 959

Note: Based on the assumption that hardware accounts for 40% of Tesla’s corporate value Source: Mirae Asset Securities Research

Source: Sumo Logic, Mirae Asset Securities Research

23 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities ResearchIII. [Auto market] Momentum to be stronger in 1H than in 2H

Surge in demand vs. • In 2021, global auto demand has rebounded more sharply than expected, as high consumer savings (following

the pandemic-driven contraction in spending on services, such as travel) have supported spending on durable

limited supply

goods, including cars. Meanwhile, production has not kept up amid chip shortages, leaving supply/demand tight.

• Despite increased fixed costs arising from lower utilization, automakers have defended margins by expanding

the revenue mix of high-end segments and cutting sales incentives.

• We expect auto demand to remain solid in 2022, as: 1) global demand is still lower than normal; and 2)

inventories remain significantly low due to supply disruptions in 2021 (supply failing to meet demand by 7-8%).

US consumer expenditure by category US avg. new car price and incentives

(1/00=100) (US$) (US$)

280 Total Durable goods Nondurable goods Services 45,000 Avg. new vehicle transaction price (L) 6,000

Avg. incentive/unit (R)

5,000

42,000

240

4,000

39,000

200 3,000

36,000

2,000

160

33,000

1,000

120 30,000 0

19 20 21 19 20 21

Source: Bloomberg, Mirae Asset Securities Research Source: JD Power, Mirae Asset Securities Research

24 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities ResearchIII. [Auto market] Momentum to be stronger in 1H than in 2H

2022F momentum: • Auto market to be solid in 1H22 and weaken in 2H22: In the event the pandemic eases toward the middle of 2022,

we expect consumption to shift from durables to services in 2H. We also anticipate increased supply with the

Stronger in 1H than in 2H

operation of new capacity by chipmakers.

• We expect the stocks of domestic automakers to be range-bound, given: 1) elevated earnings expectations; and 2)

the dissipation of momentum from new model releases. Accordingly, we think medium/long-term strategies and

multiple expansion are needed in order to see meaningful share price growth.

• Risks: An earlier-than-expected Fed rate hike could lead to a slowdown in emerging market auto demand.

HMC: 12-month forward EPS and adj. share price US money supply (M1) and inflation trends

(W) (W) (US$tr) (%, YoY)

40,000 12FM EPS (L) Adj. share price (R) 300,000 25 US M1 (L) US PPI (R) US CPI (R) 10

8

20

30,000

6

200,000

15

4

20,000

2

10

100,000

0

10,000

5

-2

0 0 0 -4

06 08 10 12 14 16 18 20 22 17 18 19 20 21

Source: Mirae Asset Securities Research Source: Bloomberg, Mirae Asset Securities Research

25 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities Research[Conclusion] Tesla and the auto revolution

• Cell phones evolve from calling devices to handheld computers

2007 • Hardware/software sophistication leads to higher revenue/profits; 2020

Nokia Apple

software-based service revenue leads to multiple expansion

• Technological difficulty and network effects rising profit share for

no. 1 player

• Cars evolving from a mode of transportation to computers on wheels

• Hardware/software sophistication to lead to higher revenue/profits

2021 2030

• Software-based service revenue (self-driving) to lead to multiple

Auto expansion

• Technological difficulty and network effects rising profit share for

Auto 2.0

market no. 1 player

26 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities ResearchAPPENDIX 1 Important disclosures and disclaimers Disclosures As of the publication date, Mirae Asset Securities Co., Ltd. and/or its affiliates do not have any special interest with the subject company and do not own 1% or more of the subject company's shares outstanding. Analyst certification The research analysts who prepared this report (the “Analysts”) are registered with the Korea Financial Investment Association and are subject to Korean securities regulations. They are neither registered as research analysts in any other jurisdiction nor subject to the laws or regulations thereof. Each Analyst responsible for the preparation of this report certifies that (i) all views expressed in this report accurately reflect the personal views of the Analyst about any and all of the issuers and securities named in this report and (ii) no part of the compensation of the Analyst was, is, or will be directly or indirectly related to the specific recommendations or views contained in this report. Mirae Asset Daewoo Co., Ltd. (“Mirae Asset Securities”) policy prohibits its Analysts and members of their households from owning securities of any company in the Analyst’s area of coverage, and the Analysts do not serve as an officer, director, or advisory board member of the subject companies. Except as otherwise specified herein, the Analysts have not received any compensation or any other benefits from the subject companies in the past 12 months and have not been promised the same in connection with this report. Like all employees of Mirae Asset Securities, the Analysts receive compensation that is determined by overall firm profitability, which includes revenues from, among other business units, the institutional equities, investment banking, proprietary trading, and private client divisions. At the time of publication of this report, the Analysts do not know or have reason to know of any actual, material conflict of interest of the Analyst or Mirae Asset Securities except as otherwise stated herein. Disclaimers This report was prepared by Mirae Asset Securities, a broker-dealer registered in the Republic of Korea and a member of the Korea Exchange. Information and opinions contained herein have been compiled in good faith and from sources believed to be reliable, but such information has not been independently verified and Mirae Asset Securities makes no guarantee, representation or warranty, express or implied, as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein or of any translation into English from the Korean language. In case of an English translation of a report prepared in the Korean language, the original Korean language report may have been made available to investors in advance of this report. The intended recipients of this report are sophisticated institutional investors who have substantial knowledge of the local business environment, its common practices, laws, and accounting principles, and no person whose receipt or use of this report would violate any laws or regulations or subject Mirae Asset Securities or any of its affiliates to registration or licensing requirements in any jurisdiction shall receive or make any use hereof. This report is for general information purposes only and is not and shall not be construed as an offer or a solicitation of an offer to effect transactions in any securities or other financial instruments. The report does not constitute investment advice to any person, and such person shall not be treated as a client of Mirae Asset Securities by virtue of receiving this report. This report does not take into account the particular investment objectives, financial situations, or needs of individual clients. The report is not to be relied upon in substitution for the exercise of independent judgment. Information and opinions contained herein are as of the date hereof and are subject to change without notice. The price and value of the investments referred to in this report and the income from them may depreciate or appreciate, and investors may incur losses on investments. Past performance is not a guide to future performance. Future returns are not guaranteed, and a loss of original capital may occur. Mirae Asset Securities, its affiliates, and their directors, officers, employees, and agents do not accept any liability for any loss arising out of the use hereof. Mirae Asset Securities may have issued other reports that are inconsistent with, and reach different conclusions from, the opinions presented in this report. The reports may reflect different assumptions, views, and analytical methods of the analysts who prepared them. Mirae Asset Securities may make investment decisions that are inconsistent with the opinions and views expressed in this research report. Mirae Asset Securities, its affiliates, and their directors, officers, employees, and agents may have long or short positions in any of the subject securities at any time and may make a purchase or sale, or offer to make a purchase or sale, of any such securities or other financial instruments from time to time in the open market or otherwise, in each case either as principals or agents. Mirae Asset Securities and its affiliates may have had, or may be expecting to enter into, business relationships with the subject companies to provide investment banking, market-making, or other financial services as are permitted under applicable laws and regulations. No part of this document may be copied or reproduced in any manner or form or redistributed or published, in whole or in part, without the prior written consent of Mirae Asset Securities. For further information regarding company-specific information as it pertains to the representations and disclosures in this Appendix 1, please contact compliance@miraeasset.us.com or +1 (212) 407-1000. Distribution United Kingdom: This report is being distributed by Mirae Asset Securities (UK) Ltd. in the United Kingdom only to (i) investment professionals falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”), and (ii) high net worth companies and other persons to whom it may lawfully be communicated, falling within Article 49(2)(A) to (E) of the Order (all such persons together being referred to as “Relevant Persons”). This report is directed only at Relevant Persons. Any person who is not a Relevant Person should not act or rely on this report or any of its contents. United States: Mirae Asset Securities is not a registered broker-dealer in the United States and, therefore, is not subject to U.S. rules regarding the preparation of research reports and the independence of research analysts. This report is distributed in the U.S. by Mirae Asset Securities (USA) Inc., a member of FINRA/SIPC, to “major U.S. institutional investors” in reliance on the exemption from registration provided by Rule 15a-6(b)(4) under the U.S. Securities Exchange Act of 1934, as amended. All U.S. persons that receive this document by their acceptance hereof represent and warrant that they are a major U.S. institutional investor and have not received this report under any express or implied understanding that they will direct commission income to Mirae Asset Securities or its affiliates. Any U.S. recipient of this document wishing to effect a transaction in any securities discussed herein should contact and place orders with Mirae Asset Securities (USA) Inc. Mirae Asset Securities (USA) Inc. accepts responsibility for the contents of this report in the U.S., subject to the terms hereof, to the extent that it is delivered to a U.S. person other than a major U.S. institutional investor. Under no circumstances should any recipient of this research report effect any transaction to buy or sell securities or related financial instruments through Mirae Asset Securities. The securities described in this report may not have been registered under the U.S. Securities Act of 1933, as amended, and, in such case, may not be offered or sold in the U.S. or to U.S. persons absent registration or an applicable exemption from the registration requirements. Hong Kong: This report is distributed in Hong Kong by Mirae Asset Securities (HK) Limited, which is regulated by the Hong Kong Securities and Futures Commission. The contents of this report have not been reviewed by any regulatory authority in Hong Kong. This report is for distribution only to professional investors within the meaning of Part I of Schedule 1 to the Securities and Futures Ordinance of Hong Kong (Cap. 571, Laws of Hong Kong) and any rules made thereunder and may not be redistributed in whole or in part in Hong Kong to any person. India: This report is being distributed by Mirae Asset Capital Markets (India) Private Limited (“MACM”) in India to the customers based in India and is personal information only for those authorised recipient(s). MACM is inter alia a Securities and Exchange Board of India (“SEBI”) registered Research Analyst in India and is not registered outside India. MACM and Mirae Asset, Korea are group entities. MACM makes no guarantee, representation or warranty, express or implied, as to the fairness, accuracy, completeness or correctness of the information and opinions contained herein. The user assumes the entire risk of any use made of this information. This report has been provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Recipient must read the entire Appendix 1 to the report carefully for Important Disclosures & Disclaimers. All other jurisdictions: Customers in all other countries who wish to effect a transaction in any securities referenced in this report should contact Mirae Asset Securities or its affiliates only if distribution to or use by such customer of this report would not violate applicable laws and regulations and not subject Mirae Asset Securities and its affiliates to any registration or licensing requirement within such jurisdiction. 27 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities Research

Mirae Asset Securities International Network Mirae Asset Securities Co., Ltd. (Seoul) Mirae Asset Securities (HK) Ltd. Mirae Asset Securities (UK) Ltd. One-Asia Equity Sales Team Units 8501, 8507-8508, 85/F 41st Floor, Tower 42 Mirae Asset Center 1 Building International Commerce Centre 25 Old Broad Street, 26 Eulji-ro 5-gil, Jung-gu, Seoul 04539 1 Austin Road West Kowloon London EC2N 1HQ Korea Hong Kong United Kingdom Tel: 82-2-3774-2124 Tel: 852-2845-6332 Tel: 44-20-7982-8000 Mirae Asset Securities (USA) Inc. Mirae Asset Wealth Management (USA) Inc. Mirae Asset Wealth Management (Brazil) CCTVM 810 Seventh Avenue, 37th Floor 555 S. Flower Street, Suite 4410, Rua Funchal, 418, 18th Floor, E-Tower Building New York, NY 10019 Los Angeles, California 90071 Vila Olimpia Sao Paulo – SP 04551-060 USA USA Brazil Tel: 1-212-407-1000 Tel: 1-213-262-3807 Tel: 55-11-2789-2100 PT. Mirae Asset Sekuritas Indonesia Mirae Asset Securities (Singapore) Pte. Ltd. Mirae Asset Securities (Vietnam) LLC District 8, Treasury Tower Building Lt. 50 6 Battery Road, #11-01 7F, Saigon Royal Building Sudirman Central Business District Singapore 049909 91 Pasteur St. Jl. Jend. Sudirman, Kav. 52-54 Republic of Singapore District 1, Ben Nghe Ward, Ho Chi Minh City Jakarta Selatan 12190 Vietnam Indonesia Tel: 62-21-5088-7000 Tel: 65-6671-9845 Tel: 84-8-3911-0633 (ext.110) Mirae Asset Securities Mongolia UTsK LLC Mirae Asset Investment Advisory (Beijing) Co., Ltd Beijing Representative Office #406, Blue Sky Tower, Peace Avenue 17 2401B, 24th Floor, East Tower, Twin Towers 2401A, 24th Floor, East Tower, Twin Towers 1 Khoroo, Sukhbaatar District B12 Jianguomenwai Avenue, Chaoyang District B12 Jianguomenwai Avenue, Chaoyang District Ulaanbaatar 14240 Beijing 100022 Beijing 100022 Mongolia China China Tel: 976-7011-0806 Tel: 86-10-6567-9699 Tel: 86-10-6567-9699 (ext. 3300) Shanghai Representative Office Ho Chi Minh Representative Office Mirae Asset Capital Markets (India) Private Limited 38T31, 38F, Shanghai World Financial Center 7F, Saigon Royal Building Unit No. 506, 5th Floor, Windsor Bldg., Off CST Road, Kalina, 100 Century Avenue, Pudong New Area 91 Pasteur St. Santacruz (East), Mumbai – 400098 Shanghai 200120 District 1, Ben Nghe Ward, Ho Chi Minh City India China Vietnam Tel: 86-21-5013-6392 Tel: 84-8-3910-7715 Tel: 91-22-62661336 28 | [2022 Outlook] EVs/Autonomous Driving Mirae Asset Securities Research

You can also read