Economic Regulation and Corporate Governance: The Case of Wirecard - Scientific ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Modern Economy, 2021, 12, 1386-1423

https://www.scirp.org/journal/me

ISSN Online: 2152-7261

ISSN Print: 2152-7245

Economic Regulation and Corporate

Governance: The Case of Wirecard

Frederick Betz1, Michael Kim2

1

Institute for Policy Models, Seattle, WA, USA

2

Department of International Business, Keimyung University, Keimyung University, Daegu, South Korea

How to cite this paper: Betz, F., & Kim, M. Abstract

(2021). Economic Regulation and Corpo-

rate Governance: The Case of Wirecard. An important normative theory in economics is that all markets are per-

Modern Economy, 12, 1386-1423. fect—perfect in the sense that “prices” in a market should be set by balancing

https://doi.org/10.4236/me.2021.129072

“demand” against “supply”. Certainly, this is a desirable theory, by reducing

Received: August 9, 2021 government interference in pricing in a market to leave economic interac-

Accepted: September 26, 2021 tions as principal forces—particularly so in financial markets. But in reality,

Published: September 29, 2021 this desirable theory does not do away with government regulation, because

Copyright © 2021 by author(s) and

markets can be corrupted or misused (and this has sometimes been called

Scientific Research Publishing Inc. “market imperfections”). Empirically in economic history, money has some-

This work is licensed under the Creative times been made by economic agents in a market through using corruption

Commons Attribution International

or misuse of market forces. Thus, as an empirical reality in economic systems,

License (CC BY 4.0).

http://creativecommons.org/licenses/by/4.0/ the need for regulation always exists. This research analyzes an actual case of

Open Access market corruption on an international scale, the Wirecard scandal. We ana-

lyze this empirical case to expand regulatory theory by investigating the kind

of roles needed to be played by some market forces (e.g. government regula-

tors, corporate auditors, and financial reporters) in order for “imperfections”

of financial markets to be avoided or corrected.

Keywords

Regulatory Economics, Market Imperfections, Corporate Law, Corporate

Governance, Corporate Performance, Corporate Integrity, Corporate Auditing,

Securities Regulation, Global Corporations, Financial Reporting

1. Introduction

Regulatory theory crosses the disciplines of economics, corporate law, and man-

agement science. In economics, the term “regulatory economics” focuses upon

the control by government over corporate activities in accountability, safety, and

DOI: 10.4236/me.2021.129072 Sep. 29, 2021 1386 Modern Economy

F. Betz, M. Kim

monopoly power. In corporate law, regulation focuses upon accountability and

responsibility to shareholders. One of the differences between the two perspec-

tives of economics and of law is based upon two different hypotheses. Tradition-

al economics assumed that “markets-are-perfect” and that government control is

probably harmful to market efficiency. In contrast, corporate law focused on

corporate power, particularly protecting shareholder interests through transpa-

rency of information. Management science has focused on efficiency in organi-

zational operations and leadership.

In any social science theory, explanations can be normative or empirical.

Normative explanations are prescriptions of what-ought-to-be; whereas empiri-

cal explanations are descriptions of what-really-is. Methodologically about social

science theory, this has been called “Idealism versus Realism” in explanation.

In the realism of a historical event, any normative explanation from the social

sciences is often contradicted by what really happened in the historical event.

What we are doing in this research is to analyze a historical event which di-

verged from proper corporate regulation—in order to provide empirical grounds

for validation of theoretical hypotheses about “market perfection” and “corpo-

rate transparency”—occurring in the reality of stock market action. The case of

“Wirecard” is an empirical event in modern economic history.

2. Economic Case History: Wirecard Fraud

Wirecard was a German-based international corporation, in business as an In-

ternet payment processor. Wirecard filed for bankruptcy on 25 June 2020, due to

exposure of financial fraud. The actual performance of the company was only

revealed late in its decade-long history—and only after whistleblower complaints

and a newspaper investigation. Part of the scandal was that the German securi-

ties regulatory agency, Federal Financial Supervisory Authority (BaFin), had

been derelict in its regulatory duties over Wirecard, for several years. BaFin

failed to properly investigate Wirecard’s performance, allowing a corporate scam

to go uncovered.

Only later was it discovered by a newspaper investigator that 1.9 billion euros

were “missing” from Wirecard’s accounts. Then the CEO of Wirecard was ar-

rested. Liz Alderman and Christopher Schuetze wrote: “Markus Braun, the for-

mer chief executive of Wirecard (a German electronic payment platform) has

been arrested in Munich on 25 June 2020. The company admitted that the 1.9

billion euros ($2.1 billion) missing from its accounts probably ‘do not exist.’

Markus Braun, who resigned as chief executive on Friday, traveled from his

home in Vienna to Germany late Monday and turned himself into the authori-

ties. Earlier on Monday, the Munich state attorney had filed a petition for an ar-

rest warrant on suspicion of market manipulation.” (Alderman & Schuetze,

2020a)

Wirecard had been founded in 1999 but came close to bankruptcy in 2002,

when Markus Braun injected capital and became the CEO. Braun focused Wire-

DOI: 10.4236/me.2021.129072 1387 Modern Economy

F. Betz, M. Kim

card on providing internet payment services. Earlier Braun had graduated from

the Technical University of Vienna with a degree in commercial computer

science. In 2000, he earned a PhD in social and economic sciences from the

University of Vienna and also worked as a consultant at Contrast Management

Consulting GmbH. From 1998 to 2001, Braun worked as a consultant KPMG

Consulting AG. And in 2002, Braun next became CEO of Wirecard.

Wirecard began a rapid expansion of services in 2007. And in 2007, Wirecard

was providing payment services for a tour operator TUI and later in 2014 for

KLM Royal Dutch Airlines. Also in 2014, Wirecard offered a “Checkout Portal”

for online purchases in retailers. Also in 2007, Wirecard had expanded in Asia in

Singapore. In 2014, Wirecard expanded into New Zealand, Australia, South

Africa, and Turkey. In 2016, Wirecard acquired a South American Internet

payment service provider in Brazil. In 2014, Wirecard had offered its “Checkout

Portal” as a fully automated application for easily connecting different payment

methods in online shops, with a focus on SMEs and virtual marketplaces. Next

in 2015, Wirecard provided a mobile-payment-app, it called “Boon”. It was a

virtual Mastercard running on either Android or IOS phone operating systems.

During these early years, Wirecard looked successful, and Wirecard’s rapid

growth had made its CEO famous. Liz Alderman and Christopher F. Schuetze

wrote: “In the elite corridors of corporate Germany, Markus Braun had become

a legend. A little-known entrepreneur until just a few years ago, Mr. Braun had

forged an obscure Bavarian company called Wirecard into a German tech icon,

winning a coveted spot on the benchmark DAX stock index in Germany. Wire-

card provided the invisible financial plumbing that, with a wave of plastic over a

card reader almost anywhere in the world, made transactions happen. Hedge

funds and global investors scrambled to buy shares.” (Alderman & Schuetze,

2020a)

But its supposedly rapid growth had not been real. Liz Alderman and Chris-

topher Schuetze wrote: “When critics raised red flags about the company’s see-

mingly miraculous success, questioning murky accounts and income that could

not be traced, Mr. Braun, an executive from Austria who was the company’s

biggest shareholder, hit back repeatedly, and the stock price skyrocketed. But on

Thursday (June 25), Mr. Braun’s empire came crashing down after Wirecard

filed for insolvency proceedings, days after the financial technology company

acknowledged that 1.9 billion euros ($2.1 billion) that it claimed to have on its

balance sheets probably never existed. Its longtime auditor, EY (formerly known

as Ernst & Young) said the company had carried out ‘an elaborate and sophisti-

cated fraud.’ Mastercard and Visa said Friday that they were considering cutting

ties.” (Alderman & Schuetze, 2020a)

Wirecard’s rapid rise in the German stock market was due to a perception that

Wirecard services were growing worldwide, particularly in Asia. Yet problems

had emerged about Wirecard’s operations. Olaf Storbeck wrote: “But in 2018, a

KPMG audit showed that activities under the company’s direct control yielded

DOI: 10.4236/me.2021.129072 1388 Modern EconomyF. Betz, M. Kim

€74 m in operating losses, compared with losses of €3 m a year earlier. This loss

was masked by profits attributed to outsourced activities in Asia, where Wire-

card said it relied on third-party business partners because it did not possess its

own licenses to operate. Now in 2020, these outsourced activities are at the cen-

ter of an accounting scandal that has rocked German finance. Wirecard warned

investors last month that this part of the business may not have ‘actually been

conducted for the benefit of the company’ and was misrepresented to investors.

But the activities outside Asia have failed to generate a profit since 2016, when it

made €20 m, contributing just 8 per cent to group earnings before interest and

tax. The poor operating performance outside Asia highlights the challenges fac-

ing Wirecard’s administrator in finding buyers for the remaining business.”

(Storbeck, 2021a)

In 2020, Wirecard’s shares fell in value when its auditor EY finally found that

its previous audits of Wirecard were in error. Kevin Granville wrote: “Shares of

Wirecard have fallen 90 percent over the last week after the company’s auditor,

EY, refused to sign off on its 2019 annual report. That prompted Markus Braun,

Wirecard’s longtime chief executive, to step down last Friday. He was then ar-

rested this week by Munich authorities on suspicion of market manipulation.

After his arrest, Mr. Braun was released on bail of 5 million euros.” (Granville,

2020)

Wirecard went into bankruptcy, triggered by reporting in the Financial Times.

Liz Alderman and Christopher Schuetze wrote: “When the reports emerged of

suspected wrongdoing at Wirecard, Mr. Braun and his team responded by de-

laying EY’s annual report for 2019 and hiring KPMG to provide an independent

assessment of the company’s books. In its report, released in April, KPMG said it

could not provide sufficient documentation to address all allegations of irregu-

larities. In the most serious finding, covering 2016-18, KPMG said it had been

unable to verify the existence of €1 billion in revenue that Wirecard booked

through three obscure third-party acquiring partners. The findings led to calls by

some investors for Mr. Braun’s ouster. The KPMG report then attracted the at-

tention of Germany’s financial regulator, BaFin, which had previously prevented

short-sellers from manipulating Wirecard’s stock price. On June 5, prosecutors

raided the company’s headquarters and opened proceedings against manage-

ment as part of the inquiry initiated by BaFin. Prosecutors said in a statement

that the company was suspected of releasing misleading information that may

have affected Wirecard’s share price.” (Alderman & Schuetze, 2020b)

3. Methodology

For the social science disciplines to use societal histories as the basis for scientific

empiricism, a historical event needs to be analyzed in terms of the societal fac-

tors generalizable from one historical event to another. In this research, we ana-

lyze a historic case of corporate fraud in the German stock market. This case

provides empirical evidence about the validity and depth of current theory in

DOI: 10.4236/me.2021.129072 1389 Modern EconomyF. Betz, M. Kim

corporation practice and law.

The methodological parallel (to basing social science theory on historical ex-

amples of societal events) is in the physical science disciplines the research tech-

nique of analyzing all physical phenomena as observations in physical space/time.

(e.g., a physical event is observed as motion of an object through space and over

time.) To scientifically describe a change event in a society’s history (historical

event), the social sciences (including economics and law) need an analogy to the

physical perceptual space—an analogy but a different kind of perceptual space—a

functional space for observing functional phenomena. Such a general societ-

al-function space has been constructed from three of basic dichotomies in the dis-

ciplines of social sciences: individual-society, groups-processes, reason-action

(Betz, 2011).

The first basic idea in the social sciences literatures is that every social science

discipline distinguishes between individuals and the society in which they

live—the dichotomy of individual & society. For example, in economics, this di-

chotomy is called—an “economic agent” and an “economic market”. In man-

agement science, this dichotomy is called a “manager” and an “organization”. In

psychology, this dichotomy is called an “individual” and a “society”. In anthro-

pology, this dichotomy is called an “individual” and a “culture”.

The second basic idea in the social sciences distinguishes within a society how

individuals associate into groups within a society and the processes a group incul-

cates in members—the dichotomy of group & process. A social process is a series

of actions coordinated to produce an outcome planned by a group. For example,

in economics, this dichotomy distinguishes between a “financial institution” and a

“financial process”. In sociology and in management science, this dichotomy dis-

tinguishes between “masses/groups/corporations” and “operations”. In anthro-

pology, this dichotomy distinguishes between “culture” and “traditions”.

The third basic idea found in the social sciences is about individuals and their

behavior in society. Individuals are described as sentient (or cognitive) beings

acting according to perceived reasons—the dichotomy of action & reason. For

example, in economics, this dichotomy distinguishes between economic transac-

tions and economic rationality. In management science, this dichotomy distin-

guishes between “implementation” and “strategy”. In psychology, this dichoto-

my distinguishes between “behavior” and “rationalization”.

These three dichotomies have been used to construct three-dimensional so-

cietal-event space in which to analyze the historical activities in terms of six ba-

sic factors (individual-society, groups-process, and action-reason (Betz, 2011).

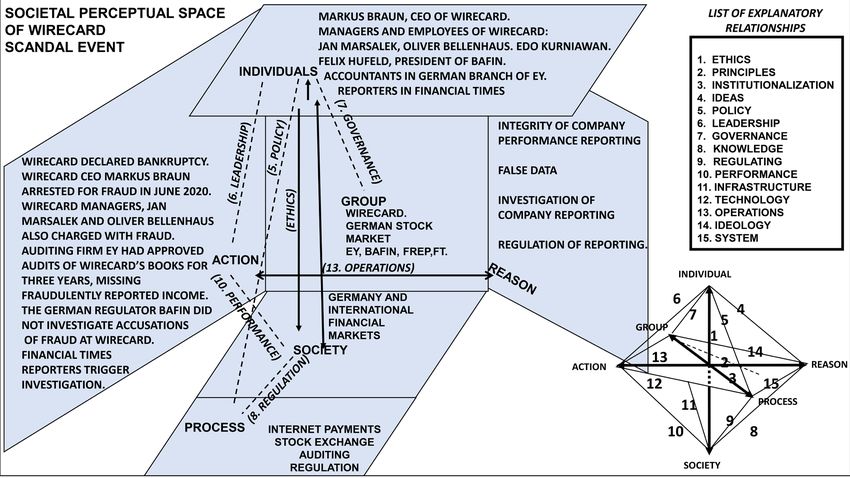

This is graphically shown as a three-dimensional societal-event perceptual space,

Figure 1.

In any historical event, the event can be generally analyzed in these six factors

and interactions between them. To conveniently describe the analysis of events

in the social-science perceptual space, one can show the areas around the di-

mensional axes as a kind of historical event-box—in Figure 2.

DOI: 10.4236/me.2021.129072 1390 Modern EconomyF. Betz, M. Kim

Figure 1. Observational space for analyzing historical change events in a societal struc-

ture.

Figure 2. Societal perceptual space event box with 15 topological explanations.

A note on the research methodology shown in Figure 2.

The construction of a three-dimensional observational space for analyzing

historical events in a society facilitates the abstraction of important (signif-

icant) societal factors occurring in the event. The six factors are:

DOI: 10.4236/me.2021.129072 1391 Modern EconomyF. Betz, M. Kim

The Individuals involved in the event, and the Society in which the

event occurs.

The Groups involved in the event, and the Processes in the event used

by the groups.

The Actions that occur in the event, and the Reasoning by Individuals

and Groups about these actions.

To highlight the factors in a historical event, one can build a box around the

axis-arrows, in order to have surfaces for conveniently listing the factors

which happened in the event. Since this box is three dimensional, opening

up the box shows all surfaces in one view.

As an additional analytical tool to explanation occurrences in the event, one

can next construct a topological graph of this 3-dimentional space. This

topological graph shows the connections between any two factors in an

event. Since the concept of “explanation” connects two factors in an obser-

vation, this graph shows that there are 15 possible functional explanations,

in a societal event. The list of the 15 kinds of explanations is shown in Fig-

ure 2. One can find the derivation of the explanations in the reference

(Betz, 2011).

An event box provides an analytical technique for abstracting and summa-

rizing the key factors in the societal change event (historical event which

changes structure-function in a society).

Expressing the connections between the key factors provides a graphical

model of the kinds of explanations which can analyze the change

event—fifteen possible explanations in the historical event (of why the his-

tory occurred).

This analysis of a historical event facilitates the abstraction of generalizable

explanations out of the descriptive complexity of the event.

We will use this research technique to analysis the Wirecard scandal—a fail-

ure in a stock market due to improper auditing and regulation. As shown in

Figure 3, we apply the analytical technique of a societal dynamics event analysis

to summarize the key societal factors and explanations in the Wirecard historical

event.

INDIVIDUAL—Markus Braun was the chief executive of Wirecard, having

grown the company to international recognition; but later he was arrested in

Munich on 25 June 2020 for fraud in Wirecard.

SOCIETY—The society was the German nation and the international market.

GROUP—The group in the event was a company called Wirecard and Ger-

man regulator, BaFin, and auditing group EY.

PROCESS—The business process of Wirecard provided an Internet payment

platform in different countries.

REASON—Wirecard told its auditor and German regulator that it had more

sales than it really had and listed a billion dollars in profits it didn’t have.

ACTION—Markus Braun was accused of fraud in the operation of Wirecard

DOI: 10.4236/me.2021.129072 1392 Modern EconomyF. Betz, M. Kim

Figure 3. Analysis of Wirecard Bankruptcy in 2020.

and was arrested in Munich, Germany, on 25 June 2020. Wirecard then declared

bankruptcy.

This analysis highlights how the bankruptcy of Wirecard occurred. The Ac-

tion in the event was bankruptcy triggered by the Individual Markus Braun

as CEO of the company, which was listed on the stock market of the Ger-

man Society. The Reason for the bankruptcy was deception by the CEO

about the profitability of the company’s operations. The CEO published

profits which did not in fact exist, as Wirecard as an Internet payment

Process failed to create customers and sales. The Groups involved in the

historical event were the company Wirecard, the auditors for Wirecard and

the regulatory agency over the German stock market.

4. Historical Case (Continued): Wirecard Operations

It turned out that the reason that Wirecard was not successful at its payments

business was that its operations were neither efficient nor effective. Olaf Storbeck

wrote: “It was Wirecard’s biggest deal—and its most controversial. In October 2015,

the German technology company agreed to pay up to €340 m for a collection of

small, barely profitable Indian payment groups. Two of the companies, Hermes I

Tickets and GI Technology, had been involved in processing payments for just a

couple of years. Wirecard chief executive Markus Braun hailed the deal, saying at

the time that it would strengthen the company’s position in one of the world’s

DOI: 10.4236/me.2021.129072 1393 Modern EconomyF. Betz, M. Kim

most rapidly growing electronic payment markets... The companies were sold to

Wirecard by an entity based in Mauritius called Emerging Markets Investment

Fund 1a (EMIF1a), which was only incorporated in February of that year.

EMIF1a had bought the Indian companies six weeks earlier for a fraction of the

price. The ultimate beneficial owners of the Mauritius entity, which reaped prof-

its from selling the payment groups to Wirecard, have remained a mystery... For

years, questions have lingered over whether one or more Wirecard executives

were behind EMIF1a...” (Storbeck, 2021b)

Markus Braun was chief operating officer (CEO) of Wirecard, and Jan Marsa-

lek was the chief operating officer (CEO) of Wirecard, and apparently he had

encouraged the purchase of EMIF by Wirecard. Olaf Storbeck wrote: “According

to emails reviewed by the Financial Times, Marsalek (Wirecard manager) was

introduced to the co-founders of the payment groups by Henry O’Sullivan, a

British businessman who advised Wirecard in Asia and entered at least one

partnership with the company in the region. The Briton was among those be-

lieved to have controlled EMIF1a... It was in late 2014 that O’Sullivan put Mar-

salek in touch with Palani Ramasamy, who with his brother Ramu had

co-founded Hermes and GI Technology. … Marsalek met Palani Ramasamy in

December 2014 at Vienna’s Hotel Sacher. In March 2015, Marsalek began rede-

signing the website of Hermes. Wirecard’s former chief operating officer com-

missioned a Munich-based designer, provided pictures and text, and personally

oversaw the work. Hermes was equipped with a state-of-the-art website, and

both Hermes and GI Technology were given modern logos... Emails show that

Wirecard footed the bill for the revamp, about €25,000. Weeks after the new

Hermes site went online, Wirecard began the takeover talks with EMIF 1a.

Dubbed ‘Project Peacock’ within Wirecard, Marsalek was keen to get the deal

done quickly... But it appears that Wirecard may have vastly overpaid EMIF 1a

for the Indian companies. In the days leading up to Wirecard’s implosion, an

internal restructuring team put the value of GI Technology at zero, according to

a presentation seen by the Financial Times.” (Storbeck, 2021b)

Marsalek, who encouraged Wirecard to purchase EMIF1a, may also have

owned an interest in EMIF. Olaf Storbeck wrote: “In early 2016, a Wirecard em-

ployee based in India told EY auditors that ‘senior executives’ of the German

payments group (Wirecard) directly or indirectly held stakes in EMIF1a.... Early

last year, EY’s anti-fraud team suggested that Marsalek might be one of the

owners—an allegation he vehemently denied. Mauritian regulators suspended

the fund’s license after Wire-card’s collapse.... Marsalek absconded in June last

year and is on Interpol’s most-wanted list.” (Storbeck, 2021b)

Also Wirecard’s business growth in Asia was a fraud. Wirecard reported

business revenue it never earned nor obtained. Some of Wirecards’ employees

“cooked-the-books”. One of these employees was an Indonesian, who ran ac-

counting and finance for Wirecard in Asia. Dan McCrum and Stefania Palma

wrote: “A preliminary report by a top law firm has unveiled a pattern of sus-

pected book-padding across the group’s Asian operations. Edo Kurniawan, a

DOI: 10.4236/me.2021.129072 1394 Modern EconomyF. Betz, M. Kim

jovial 33-year-old Indonesian who runs the Asia-Pacific accounting and finance

operations for global payments group, Wirecard AG, called half a dozen col-

leagues into a Singapore meeting room. He picked up a whiteboard pen and be-

gan to teach them how to cook the books... He said the task at hand was to create

figures that would convince regulators at the Hong Kong Monetary Authority to

issue a license so Wirecard could dole out prepaid bank cards in the Chinese ter-

ritory of Hong Kong... The group was seeking to take over payment operations

from Citigroup, covering 20,000 retailers in 11 countries stretching from India

to New Zealand. Regulatory approvals in every territory were crucial, even if it

meant inventing numbers to be used in the Hong Kong license application.”

(McCrum & Palma, 2019)

The problem for Wirecard was that it needed a license in each nation in Asia

to operate in that nation. Wirecard was having problems with Hong Kong au-

thorities who would not issue a license to operate in China. Dan McCrum and

Stefania Palma wrote: “Mr. Kurniawan then sketched out a practice known as

‘round tripping’. A lump of money would leave the bank Wirecard owns in

Germany, show its face on the balance sheet of a dormant subsidiary in Hong

Kong, depart to sit momentarily in the books of an external ‘customer’, then

travel back to Wirecard in India, where it would look to local auditors like legi-

timate business revenue.” (McCrum & Palma, 2019)

The employee was proposing to “cook” Wirecard’s accounts with revenue that

did really come in—but was only Wirecard’s money circulating around in ac-

counts and back to Wirecard. Publicly calling this a business income is “fraud”.

But was the employee secretly doing this on his own or did upper management

know about this? McCrum and Stefania Palma wrote: “Mr. Kurniawan’s scheme

might have appeared to be the act of a rogue employee in the provincial outpost

of a little known financial group. But the account of what happened, in a pre-

liminary report on the investigation by one of Asia’s most eminent legal firms,

indicated it was part of a pattern of book-padding across Wirecard’s Asian oper-

ations over several years” (McCrum & Palma, 2019)

Apparently the senior executives did know about the scheme. Dan McCrum

and Stefania Palma wrote. “Documents seen by the Financial Times show two

senior executives in the Munich head office had at least some awareness of the

round-tripping scheme: Thorsten Holten and Stephan von Erffa, respectively the

company’s head of treasury and head of accounting.” (McCrum & Palma, 2019)

In addition, some business associates of Wirecard assisted Wirecard in its

fraud. Stefania Palma, Olaf Storbeck, and Dan McCrum wrote: “A Singaporean

businessman with multiple ties to Wirecard has been charged with falsification

of accounts, marking the first set of charges issued by the city-state since it

kicked off an investigation into the collapsed German payments company last

year. R Shanmugaratnam is suspected of being a key figure in an alleged mul-

ti-year fraud, accused of playing the role of trustee for fake bank accounts, which

Wirecard told auditors were filled with cash. Wirecard collapsed into insolvency

DOI: 10.4236/me.2021.129072 1395 Modern EconomyF. Betz, M. Kim

in June after it admitted that €1.9 bn of cash in so-called trustee accounts proba-

bly did ‘not exist’.... Singapore police last month charged Mr. Shanmugaratnam

with falsifying ‘willfully and with intent to defraud’ letters to Wirecard saying

that his company, Citadelle Corporate Services, was holding hundreds of mil-

lions of euros in escrow accounts ‘when in fact [they] did not hold such balance’,

according to charge sheets. Mr. Shanmugaratnam, a Singaporean, was accused of

forging three letters in March 2016 and one a year later, claiming Citadelle was

holding a total of €321 m in three separate escrow accounts. If convicted, Mr.

Shanmugaratnam could face up to 10 years in prison and a fine for each of the

four charges.” (Palma, Storbeck, & McCrum, 2020)

Also, it turned out that Wirecard’s fraudulent tendencies were not new.

Wirecard’s upper management had even been stealing from Wirecard—for a

long time. Olaf Storbeck wrote: “Wirecard’s fraud started more than a decade

before the German payments company imploded, when some senior managers

began establishing a network of offshore companies that were used to siphon off

millions of euros, a former top executive has told prosecutors. Oliver Bellenhaus

has informed Munich prosecutors that starting in 2010 he created an array of

shell companies based in Hong Kong and the British Virgin Islands, according

to people with knowledge of the matter. He said that he did so at the behest of

Jan Marsalek, Wirecard’s former chief operating officer who is now on Interpol’s

most wanted list... Bellenhaus has told prosecutors that from 2011, he and Mar-

salek shifted funds out of Wirecard and into bank accounts in the name of the

shell groups. Some years later, Bellenhaus moved millions of these funds to a

private foundation.” (Storbeck, 2021c)

Markus Braun, the head of Wirecard, denied involvement in those thefts.

Storbeck wrote: “Munich prosecutors have used testimony from Bellenhaus to

build a prosecution case. They accuse Wirecard’s former chief executive Markus

Braun of being the linchpin of a criminal racket that allegedly inflated Wirecard’s

revenue in an attempt to deceive investors. Braun denies any wrongdoing. The

former chief, who also was Wire-card’s single largest shareholder, last summer

said the company had been the target of ‘fraud of considerable proportions’. In

November, he told MPs that he hoped prosecutors would succeed in tracing the

missing money.” (Storbeck, 2021c)

The amounts of cash stolen from Wirecard were large. Olaf Storbeck wrote:

“Wirecard employees hauled millions of euros of cash out of the group’s Munich

headquarters in plastic bags over many years... The practice started as early as

2012, with six-digit sums in banknotes often moved in Aldi and Lidl plastic bags,

former staff told the police... As demand for cash grew over time, Wirecard Bank

bought a safe located in the group’s headquarters in a Munich suburb. At one

point in May 2017, €500,000 in cash was delivered when the safe was full, ac-

cording to emails seen by the FT. Some of the cash was hidden elsewhere in the

offices.... An employee, who worked at the headquarters for almost two years

until 2018, told police that amounts of €200,000 - €700,000 were removed fre-

DOI: 10.4236/me.2021.129072 1396 Modern EconomyF. Betz, M. Kim

quently, sometimes several times a week, according to people familiar with the

investigation. That suggests more than €100 m could have been removed.”

(Storbeck, 2021c)

The theft of money by Wirecard employees continued up to the final weeks of

Wirecard. Olaf Storbeck, Richard Milne, and Stefania Palma wrote: “Prosecutors

suspect that a Lithuanian payments company, Finolita, was used to steal more

than €100 m from Wirecard weeks before it collapsed, with some of the money

channeled to the German group’s fugitive second-in-command Jan Marsalek...

Prosecutors suspect that part of a €100 m loan granted by Wirecard in March

2020 to a subsidiary of Finolita’s owner, and processed by the Lithuanian com-

pany, was channeled to Marsalek, Wirecard’s former chief operating officer who

is wanted by Interpol.” (Storbeck, Milne, & Palma, 2021)

Beginning in 2017, real information about Wirecard’s operations began to

leak out, due to a “whistle-blower”, Pav Gill. Gill had been hired by Wirecard as

an in-house lawyer for the Asian operations. Dan Mccrum, Stefania Palma, and

Olaf Storbeck wrote: “Gill was hired in September 2017 as Wirecard’s first

in-house lawyer responsible for the Asia-Pacific region, reporting directly to

Munich. Within months he was approached by two Wirecard employees who

accused colleagues of cooking the books.” (Mccrum, Palma, & Storbeck, 2021)

Gill began an internal investigation into Asian operations: Dan Mccrum, Ste-

fania Palma, and Olaf Storbeck wrote: “A probe was launched, codenamed

Project Tiger, that focused on a young Indonesian, Edo Kurniawan, whom Gill

described as Wirecard’s ‘third most important finance and accounting employee

globally’. Gill found it odd that someone with as little experience as Kurniawan

held such an important job. He recalls that Kurniawan regularly flew to Munich

for meetings, but at the time, Gill’s focus was on Asia. ‘I don’t think anyone at

the initial stage thought the entire company was diseased,’ he said. An outside

law firm, Rajah & Tann, was hired to investigate and copies were taken of Kur-

niawan’s email inbox on the authority of Daniel Steinhoff, then Wirecard’s dep-

uty general counsel responsible for compliance. In that trove of data lay evidence

of the fake customers behind Wirecard’s facade. ‘Nothing would have happened

if we hadn’t had the go-ahead by Steinhoff,’ Gill said. The investigation, Project

Tiger, quickly uncovered misconduct. Staff were emailing themselves logos, fak-

ing contracts and invoices.” (Mccrum, Palma, & Storbeck, 2021)

The legal staff had not engaged in the fraudulent activities, and their probe

began to uncover suspicious activity. But the top management of Wirecard made

no move to stop the fraud. Instead, they stopped the investigation. Dan Mccrum,

Stefania Palma, and Olaf Storbeck wrote: “Wirecard top brass took no action

against the suspected perpetrators. Instead, Jan Marsalek seized control of the

probe. Gill was shocked. ‘Any normal company, especially a listed company,

would have suspended these people, even if it was just for show.’” (Mccrum,

Palma, & Storbeck, 2021)

Pav Gill found that top management really did not appreciate his efforts to

DOI: 10.4236/me.2021.129072 1397 Modern EconomyF. Betz, M. Kim

identify the internal fraud. Dan Mccrum, Stefania Palma, and Olaf Storbeck

wrote: “As the months progressed, Gill’s job became untenable. In September he

was presented with a choice: resign with a positive reference or be fired. Gill

lacked the strength or resources to fight, and felt out of options... In October

2018, Gill was forced out of Wirecard, after executives had stonewalled an inter-

nal investigation into fraud allegations.” (Mccrum, Palma, & Storbeck, 2021)

But the Wirecard’s impact upon Gill’s career did not stop there. Wirecard

management pursued him. And finally, Pav Gill talked to Financial Times re-

porters. Dan Mccrum, Stefania Palma, and Olaf Storbeck wrote: “Gill said, ‘they

tried to destroy me, manfully, professionally, emotionally’. He suspected he was

being followed. Neighbors reported strange men taking an interest in his flat.

Bad references were paid to his job prospects. Some job interviews felt like traps

to lure him into breaking his non-disclosure agreements, with an excessive focus

on the reasons he left Wirecard... In 2018, the reluctant Gill decided that for the

fraud to be properly exposed, he had to be involved. In encounters in out-of-the

way coffee shops and Singapore hotel lobbies, he explained to the Financial

Times what had happened to him... For Gill, the Financial Times played a role.

‘It felt like a burden was lifted. It’s no longer you who carries the weight of that

information.’ The first story took nerve-racking months to appear. When it did,

Wire-card called it ‘another inaccurate, misleading and defamatory media re-

port’. A few days later, then chief executive Markus Braun changed tack, admit-

ting the gist but attacking the source.” (Mccrum, Palma, & Storbeck, 2021)

5. Corporate Case History (Continued): Auditing Wirecard

Yet over the years of 2016, 2017, 2018, the auditors of Wirecard, the accounting

firm Ernst & Young Global Limited (EY) had audited Wirecard’s performance

and had suspected nothing. EY’s audits were, in fact, faulty.

Olaf Storbeck, Tabby Kinder, and Stefania Palma wrote: “Ernst & Young

Global Limited (EY) failed for more than three years to request crucial account

information from a Singapore bank where Wirecard claimed it had up to €1 bn

in cash—a routine audit procedure that could have uncovered the vast fraud at

the German payments group. The accountancy firm, which audited Wirecard for

a decade, has come under fire after the once high-flying financial tech company

filed for insolvency this week, revealing that €1.9 bn in cash probably did ‘not

exist’. People with first-hand knowledge told the Financial Times that the audi-

tor between 2016 and 2018 did not check directly with Singapore’s OCBC Bank

to confirm that the lender held large amounts of cash on behalf of Wirecard. In-

stead, EY relied on documents and screenshots provided by a third-party trustee

and Wirecard itself.” (Storbeck, Kinder, & Palma, 2020)

The false information about sales and profits were large amounts. Olaf Stor-

beck wrote: “According to its EY-audited financial reports, between 2016 and

2018 Wire-card generated operating margins of around 22 per cent and almost

doubled annual earnings before interest and taxes to €439 m. The company last

DOI: 10.4236/me.2021.129072 1398 Modern EconomyF. Betz, M. Kim

year in 2018 also promised investors a fivefold increase in profits by 2025. But

such profits appear to have existed largely on paper, according to data in the

confidential appendix of a special audit conducted by KPMG and seen by the

Financial Times... Wirecard’s internal numbers reveal that the operating per-

formance of its core business—mainly payments processing in Europe and is-

suing credit cards in Europe and North America—was far worse than previously

known. The figures show that those activities have also become increasingly

lossmaking, despite accounting for half the company’s reported revenue and al-

most two-thirds of transaction volumes.” (Storbeck, 2021d)

For several years, Wirecard had not been making profits, while claiming to be

very profitable. Wirecard was really losing money. Olaf Storbeck wrote: “Later

KPMG’s special audit showed that profits existed largely on paper, with Wire-

card’s Asia units being lossmaking since 2016. The KPMG special audit was

launched last year in 2019. EY, the group’s original auditor, reported that earn-

ings almost doubled from 2016 to 2018. But really, Wirecard’s core business in

Europe and the Americas was lossmaking for years, casting doubt on the eco-

nomic substance of the parts of the company not directly affected by its ac-

counting scandal.” (Storbeck, 2021d)

The accounting firm EY had failed in its accounting responsibility; and later

another accounting firm KPMG had performed an accurate audit. Why had EY

not done its proper job? Olaf Storbeck, Tabby Kinder, and Stefania Palma wrote:

“A senior banker at a lender with credit exposure to Wirecard said, ‘The big

question for me is what on earth did EY do when they signed off the accounts?’

A senior auditor at another firm said that obtaining independent confirmation

of bank balances was ‘equivalent to day-one training at audit school’.” (Storbeck,

Kinder, & Palma, 2020)

This was a scandal in international accounting firm’s performances. Olaf

Storbeck, Tabby Kinder, and Stefania Palma wrote: “A ‘Big Four’ accounting firm,

EY, had issued unqualified audits of Wirecard for a decade despite—increasing

questions over suspect accounting practices from journalists and short sellers.”

(Storbeck, Kinder, & Palma, 2020)

It turned out that in 2016, Wirecard’s attempts to generate payments business

in Asia had not succeeded. But Wirecard lied about this. Olaf Storbeck, Tabby

Kinder, and Stefania Palma wrote: “The accounts at Asian banks play a pivotal

role in Wirecard’s accounting fraud that culminated in the group filing for in-

solvency. According to the company’s former management, the accounts were

used to settle transactions with partners who acted on Wirecard’s behalf in

countries where it did not have its own licenses to process electronic payments.

Yet it is now unclear if the accounts—let alone the money allegedly deposited

there—ever existed.” (Storbeck, Kinder, & Palma, 2020)

Wirecard’s lies about Asian business were deliberate, and desperate, to keep

the company going. EY argued that it was not its fault that it had not detected

the fraud. Later in 2019, after other auditors in EY looked at the situation, EY

DOI: 10.4236/me.2021.129072 1399 Modern EconomyF. Betz, M. Kim

still tried to justify itself. Olaf Storbeck, Tabby Kinder, and Stefania Palma wrote:

“In a statement issued on Thursday (March 2020), EY said there were ‘clear in-

dications that this was an elaborate and sophisticated fraud, involving multiple

parties around the world in different institutions, with a deliberate aim of decep-

tion’. The company EY argued that ‘even the most robust audit procedures may

not uncover this kind of fraud’.” (Storbeck, Kinder, & Palma, 2020)

But examination of EY’s auditing of Wirecard showed poor auding perfor-

mance not once but over several years. Olaf Storbeck wrote: “EY’s audits of de-

funct payments group Wirecard suffered from serious shortcomings over a pe-

riod of years, the German investigation found. The Big Four firm is said to have

failed to spot fraud risk indicators, did not fully implement professional guide-

lines.” (Storbeck, 2021e)

In Germany, the consequence of EY’s poor performance about Wirecard was

a loss of other customers. Olaf Storbeck wrote: “Deutsche Bank may drop EY as

its auditor after the Wirecard scandal left the Big Four firm under investigation

and battling to restore its reputation. In an unusual move, Germany’s biggest

lender is inviting firms to compete for its 2022 audit just two years after hiring

EY to replace KPMG, which had vetted the bank’s books for more than 60

years... EY has been under siege since Wirecard collapsed last June 2020 in one

of Europe’s largest accounting frauds of recent decades... EY billed 580,000

hours to Deutsche during its 2020 audit of the bank.” (Storbeck, 2021e)

6. Case History (Continued): Failure of Regulation by the

German Agency (BaFin)

Wirecard was based in Germany. And in Germany, the Federal Financial Super-

visory Authority (BaFin) was the principle regulatory agency for the supervision

of German banks and insurance companies and for also for the proper trading of

corporate securities. BaFin supervised about 2700 banks, 700 insurance firms,

and 800 financial services institutions. BaFin was established in 2002, with the

intention to have one agency cover all financial markets in Germany. But when

accusations about Wirecard’s accounting were made in 2008, 2015, 2016, and

2019. BaFin defended Wirecard, seeing no wrong in it. Then in 2020, Wirecard

went bankrupt and its CEO was arrested. Then BaFin was criticized for failing a

proper regulation of Wirecard.

BaFin was run by a Board consisting of the President, Felix Hufeld, and four

executive directors: Elisabeth Roegele (securities division), Raimund Röseler

(banking supervision), Dr. Frank Grund (insurance supervision), and Beatrice

Freiwald (cross-functional areas and internal administration).

In 2021, Guy Chazan and Olaf Storbeck wrote: “Felix Hufeld and Elisabeth

Roegele depart as heads of Germany’s financial regulator BaFin (Federal Finan-

cial Supervisory Authority or Bundesanstalt für Finanzdienstleistungsaufsicht).

Hufeld, head of Germany’s financial watchdog BaFin, and his deputy Roegele

have been pushed out over their handling of the Wirecard scandal, the worst

DOI: 10.4236/me.2021.129072 1400 Modern EconomyF. Betz, M. Kim

accounting fraud in the country’s postwar history. In a statement, Olaf Scholz,

finance minister, said the Wirecard affair had revealed that Germany’s system of

financial regulation ‘needs to be re-organized, so that it can fulfil its supervisory

role more effectively’.” (Chazan & Storbeck, 2021).

Instead of discovering the fraud at Wirecard, the principles in BaFin stood by

Wirecard for a long time—before Wirecard’s fraud was unveiled. Guy Chazan

and Olaf Storbeck wrote: “For months, BaFin has been under fire for ignoring

early warnings about fraud at Wirecard, and targeting journalists and short sel-

lers who pointed out misconduct at the payments processor. In April 2019, the

watchdog filed a criminal complaint against two Financial Times reporters, trig-

gering an investigation that was only dropped months after Wirecard’s collapse.

Last year, the European Securities and Markets Authority criticized BaFin for its

‘deficient’ handling of the scandal.” (Chazan & Storbeck, 2021)

Still the head of BaFin, Mr. Hufeld, defended BaFin’s behavior about Wire-

card. Guy Chazan and Olaf Storbeck wrote: “In the months that followed

(Wirecard’s collapse), however, Mr. Hufeld adopted a defiant tone and repeat-

edly defended BaFin’s handling of the affair. The FT revealed this week that he

had suggested Wirecard might be the victim of an elaborate plot by short sellers,

even after the company itself acknowledged the hole in its balance sheet. Pres-

sure on BaFin has steadily mounted, especially after the German Bundestag last

year established a full committee of inquiry into the regulatory failings that al-

lowed the Wirecard scandal to happen.” (Chazan & Storbeck, 2021)

In 2021, the German Federal Ministry of Ministry disclosed that some of Ba-

Fin’s staff had engaged in private investments, some of which included interest

in Wirecard. It was late in 2020 (September) when BaFin finally banned its staff

from trading shares and other securities of the companies that it oversees. Guy

Chazan and Olaf Storbeck wrote: “Meanwhile, the actions of some of BaFin’s

staff have also provoked outrage in Berlin. Just this week (in March 2021), BaFin

disclosed that it filed a criminal complaint against an employee for insider

trading with Wirecard shares in June last year (2020). The FT on Friday also

reported that the authorities’ decision to ban the shorting of Wirecard shares

in 2019 was based on flimsy oral evidence provided by the company itself.”

(Chazan & Storbeck, 2021)

In 2021, Hufeld, the head of BaFin, was fired. Guy Chazan and Olaf Storbeck

wrote: The German Finance Minister, Mr. Scholz, had initially resisted pressure

to ditch the head of BaFin, Mr. Hufeld—focusing instead on a sweeping plan to

reform BaFin and so restore confidence in Germany’s system of regulation.

However, as evidence of regulatory failures at BaFin continued to mount, the

finance minister, Scholz, was forced to take more drastic action. In a statement

on Friday, Mr. Sholz said that he and Mr. Hufeld had discussed the situation and

reached a mutual decision “that, alongside organizational changes, there should

also be a change at the top of BaFin”. The planned reform of BaFin could only

succeed with a “change at the top”, Mr. Scholz said (Chazan & Storbeck, 2021).

DOI: 10.4236/me.2021.129072 1401 Modern EconomyF. Betz, M. Kim

Political pressure from the German parliament had forced the German

Finance Minister, Mr. Scholtz, to make changes at BaFin. Guy Chazan and Olaf

Storbeck wrote: “Fabio De Masi, an MP for the hard-left Die Linke party, had

earlier called Mr Hufeld’s departure ‘overdue’, and said the position of his depu-

ty, Ms Roegele, had also become ‘untenable’. As the head of BaFin’s securities

department, she was behind the controversial decision to ban the short selling of

Wirecard shares in 2019.” (Chazan & Storbeck, 2021)

Earlier, the managers of BaFin, Mr Hufeld and Ms Rogele, had even defended

Wirecard to the European Union Securities and Market Authority (Esma). Olaf

Storbeck wrote: “Documents seen by the Financial Times show that BaFin told

Esma that the selling pressure on Wirecard stocks could destabilize the wider

German stock market. BaFin gave the Esma selective and incomplete informa-

tion when making its case for the ban on shorting Wirecard shares.... ‘BaFin

presented the facts to Esma in a highly distorted way,’ Danyal Bayaz, an MP for

the Greens, told the Financial Times, adding that the regulator’s ‘biased argu-

ments’ probably tricked Esma into approving the short-selling ban.” (Storbeck,

2021f)

Also in 2019, BaFin had tried to take legal action against the newspaper, Fi-

nancial Times, for reporting in Wirecard’s fraud. Olaf Storbeck wrote: “In the

year leading to its insolvency, Wirecard raised €1.4bn of fresh debt which pros-

ecutors think is largely ‘lost’. Investors and creditors took the short-selling ban,

and a criminal complaint by BaFin against two FT journalists who reported

whistleblower allegations against Wirecard, as a vote of confidence for the con-

troversial German company. The investigation against the reporters was only

dropped months after Wirecard’s insolvency.... In 2020, Esma lambasted BaFin

for its ‘deficient’ handling of the Wirecard scandal. BaFin president Felix Hufeld

and his deputy Elisabeth Roegele, who headed the watchdog’s securities depart-

ment, were pushed out last week (in 2021).” (Storbeck, 2021g)

A governmental investigation of the scandal focused upon BaFin’s attack on

financial reporters. Guy Chazan and Olaf Storbeck wrote: “A key focus of the

investigation has been BaFin’s controversial decision in February 2019 to impose

a ban on the short selling of Wirecard shares, despite misgivings expressed by

the Bundesbank, Germany’s central bank. ‘That... was probably the biggest mis-

take our authorities made,’ says Danyal Bayaz, a Green MP on the committee. ‘It

was at that moment that they sided with criminals, and investigated journalists

and market participants who were posing critical questions.’ The Munich pros-

ecutors’ role in the BaFin short selling ban has also proved controversial. The

chief prosecutor Hildegard Bäumler-Hösl told MPs that two years ago she had a

curious phone call with a star Munich lawyer who was working for Wirecard. He

told her that Bloomberg reporters had attempted to blackmail the payments

company: they purportedly threatened to ‘take up an offer from the FT’ and

publish negative stories about Wirecard, unless it paid them €6 m. Bäumler-Hösl

sent a memo to BaFin summarizing the information. Fearing a so-called ‘short

DOI: 10.4236/me.2021.129072 1402 Modern EconomyF. Betz, M. Kim

attack’ on Wirecard, BaFin then issued its now infamous short selling ban,

which appeared to suggest Wirecard’s biggest problem was the speculators

betting on its falling share price rather than the allegations of fraud swirling

round the company. But the blackmail story was a fiction.” (Chazan & Stor-

beck, 2021)

7. Historical Case (Continued): German Regulation

of Accounting Firm

The accounting firm EY had failed to properly audit Wirecard and did not detect

its fraudulent operations. Accounting firms also need proper oversight. In Ger-

many, accounting firms operating there were overseen by a voluntary regulating

committee called the Financial Reporting Enforcement Panel (FREP). Olaf Stor-

beck and Guy Chazan wrote: “Germany is to overhaul accounting regulation af-

ter the Wirecard collapse. The government will terminate its contract with the

country’s accounting watchdog, the Financial Reporting Enforcement Panel

(FREP)... The power to launch investigations into companies’ financial reporting

would then be handed to BaFin, Germany’s financial regulator.” (Storbeck &

Chazan, 2020)

FREP was recently created and lightly staffed. Olaf Storbeck and Guy Chazan

wrote; “FREP was founded in 2004 in response to the Enron accounting scandal

but has only 15 employees and a small annual budget of €6 m... Under German

law, BaFin could ask FREP to open a probe into a company’s financial reporting

but has no sway over the actual process. The Bonn-based regulator needs to wait

for the result of a FREP probe before it can start its own investigation. BaFin in

early 2019 asked FREP to start a probe into Wirecard after the Financial Times

(FT) reported accusations by whistleblowers of accounting manipulations, ac-

cording to people briefed on the matter. However, only one investigator at FREP

has been working on the case and little progress was made.” (Strobeck & Cha-

zan, 2020)

FREP failure on EY had raised questions about reform. Olaf Strobeck and Guy

Chazan wrote: “Jörg Kukies, Germany’s deputy finance minister, told the Finan-

cial Times: ‘What the Wirecard affair has shown is that… self-regulation by the

auditors doesn’t work properly. So we will inevitably have to question whether

the bodies that currently regulate the industry should continue to do so in their

current form’.” (Strobeck & Chazan, 2020)

8. Case Study Continued: Wirecard and Politics

The Wirecard scandal impacted politics in Germany about proper regulation

of stock markets. Guy Chazan and Olaf Storbeck wrote: “As a parliamentary

investigation reaches its climax—with the appearance of Angela Merkel and

Olaf Scholz this week—MPs are asking why Germany’s establishment was

taken in by the collapsed group. It was an innocuous question, posed shortly

before midnight some nine hours into an exhausting parliamentary hearing

DOI: 10.4236/me.2021.129072 1403 Modern EconomyF. Betz, M. Kim

into the Wirecard scandal. ‘Did you ever actually own Wirecard shares?’ Can-

sel Kiziltepe, the Social Democrat MP, asked Ralf Bose, head of Germany’s au-

ditor watchdog Apas. His answer caused a political earthquake and brought an

abrupt end to his more than 30-year career. A former partner at KPMG, Bose

ran a government agency that is normally protected from public scrutiny by

stringent secrecy laws. But those laws do not apply to the Bundestag’s inquiry

into Wirecard. Bose disclosed that he had bought and sold the company’s

stock while Apas was investigating its auditor EY. Just hours later the German

government started to probe the transactions. And within a matter of weeks

Bose had been fired. His late-night admission last December was one of the

high points of an inquiry that has electrified Berlin’s political class and led to a

swath of resignations among top regulators and financial executives.” (Chazan

& Storbeck, 2021)

The politics of the Wirecard scandal even reached the German Prime Mi-

nister. Guy Chazan and Olaf Storbeck wrote: “MPs will want to know why

Merkel lobbied for Wirecard in China when reports about suspected fraud at

the company had been in the public domain for months. Scholz will be asked

to explain how BaFin, the financial regulator he oversees, not only failed to

uncover the fraud but went after short-sellers and Financial Times journalists

who first highlighted irregularities at the company. Scholz, who is running as

the Social Democrats’ candidate for chancellor in September’s election, has

placed the bulk of the blame on Wirecard’s auditors... MPs have expressed

amazement at the scale of the Wirecard lobbying operation, with its network

of former police chiefs, ministers and spymasters, and at revelations that BaFin

employees traded Wirecard shares while the company was under investigation.

They also expressed shock at the fanciful stories cooked up by Wirecard law-

yers alleging journalists’ attempts to blackmail the company.” (Chazan &

Storbeck, 2021)

9. Expanded Analysis of Historical Case of Wirecard

Next in Figure 4, we expand the analysis of the Wirecard event to include the

understanding of operations and groups in the event.

We can now add into the analysis of the historical event of Wirecard the ac-

tions of the auditor Ernst & Young Global Limited (EY) and the German regu-

lator Federal Financial Supervisory Authority (BaFin) and the German auditors

supervisory committee and the Financial Times investigatory reporting.

INDIVIDUALS—Markus Braun was the chief executive of Wirecard, having

grown the company to international recognition. He was arrested in Munich on

25 June 2020. The President Felix Hufeld of the German regulatory agency Ba-

Fin defended Wirecard and later was forced to resign. The head of the German

office of the auditor EY of Wirecard failed to perform proper audits of Wirecard

from 2015 to 2018. Several employees or business associates of Wirecard assisted

the fraudulent income reporting, such as Edo Kurniawan and R. Shanmugaratnam.

DOI: 10.4236/me.2021.129072 1404 Modern EconomyYou can also read