DSV-Panalpina Market update - April 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

DSV-Panalpina

Market update

April 2021

1 | DSV – Market update Air & Sea April 15th , 2021

Content

1 COVID-19 Overview

Suez Canal Blockage

2 “ripple effect”

3 Ocean freight update

4 Airfreight update

2 | DSV – Market update Air & Sea April 15th , 2021

More than 825 million vaccine doses have been administered

worldwide, equal to 11 doses for every 100 people

The number has growth 3x compared to one month of March and we expect an exponential growth as we have

more vaccines available

Doses Administered Pct. of population

Per 100

Dosis administered per 100 people People Total Vaccinated Fully Vaccinated

World 11 824,878,017 – –

Israel 116 10,290,033 60% 56%

Seychelles 112 108,749 68% 45%

U.A.E. 95 9,156,728 – –

Chile 65 12,259,848 40% 26%

Bhutan 63 476,74 63% –

Bahrain 63 989,363 37% 26%

U.K. 60 40,107,877 49% 12%

United

58 192,282,781 37% 23%

States

Maldives 55 283,753 52% 3.0%

Monaco 53 20,51 30% 23%

San Marino 52 17,707 28% 24%

Malta 52 249,4 36% 15%

Hungary 44 4,327,732 31% 13%

Serbia 41 2,882,854 25% 17%

https://www.nytimes.com/interactive/2021/world/covid-vaccinations-tracker.html

3 | DSV – Market update Air & Sea April 15th , 2021

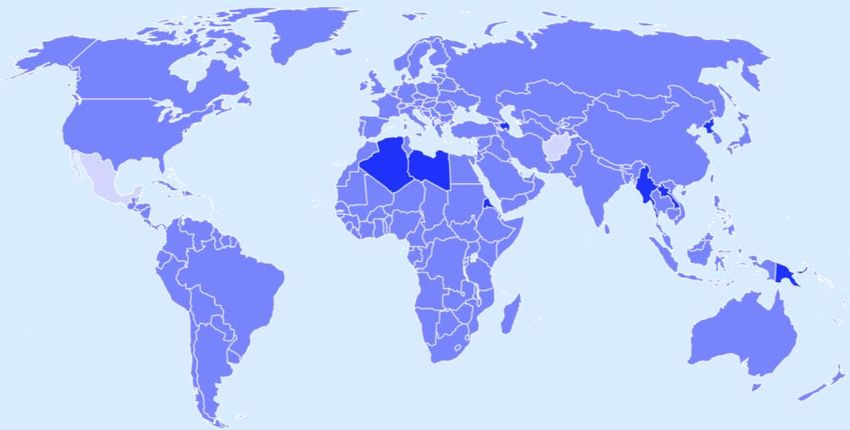

Global COVID-19 Freight Restrictions Overview

Fully vaccinated travellers are less likely to get and spread COVID-19.

COVID-19 Travel Regulations Map as per IATA

ASIA PACIFIC

EUROPE

China: China has restricted entry and

Europe is on lockdown until April 30th transit to all travelers except Chinese

Travelers are subject to a 7-day isolation nationals, Hong Kong, Macau, or Taiwan

period and take another COVID-19 PCR passport holders, and travelers with

test at the end of this period. diplomatic, service, courtesy, or C visas,

or visas issued after March 28, 2020.

UK: From March 8, passenger traveling

abroad will need to carry a new travel South East Asia: Most countries have

declaration form stating that their trip is banned the entry until end of April with

permitted under UK national lockdown potential extension

rules..

INDIAN SUB-CONTINENT.

NORTH AMERICA India:.Until April 30th passenger planes

Source:https://www.iatatravelcentre.com/world.php

are banned to enter the country.

People who has been in EU and UK Cargo planes are allowed to enter the

during last 14 days or residents from country.

those countries are banned the entry to

USA, this does not apply to nationals or Sri Lanka: Flights has been suspended.

permanent residents in USA

Bangladesh and Pakistan: Passengers

LATIN AMERICA AFRICA and MIDDLE EAST must present a negative PCR before

entering

All flights from UK and South Africa are South Africa All passengers must present a negative corona virus test and they are only

suspended to Argentina, Brazil, Chile etc allowed to travel to 3 airports, Cape Town, Durban and Johannesburg.

Saudi Arabia Restrictions to travellers coming from Argentina ,Brazil, India South Africa

and United Kingdom

4 | DSV – Market update Air & Sea April 15th , 2021

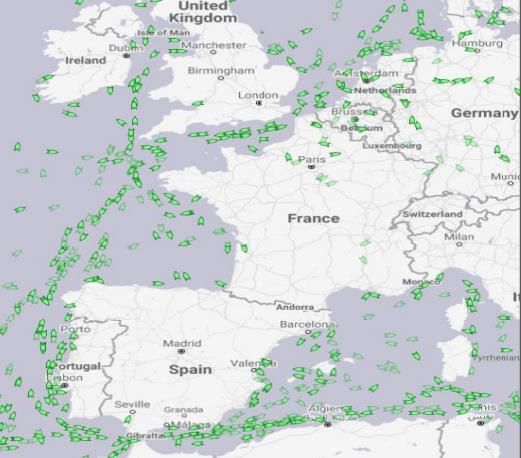

Suez Canal Blockage “ripple effect” 5 | DSV – Market update Air & Sea April 15th , 2021

A total of ~340k TEU is estimated to have been delayed by

the Suez Canal blockage

Raw materials and consumer goods form more than half of containerized Suez ocean trade

Breakdown of AsiaEurope containerized ocean trade by commodity Delayed demand is about to arrive in

% of Teus Europe, potentially overwhelming ports…

Container vessels in European waters, April 7th

Source: Marinetraffic.com

Note: Shares of TEUs rounded to the nearest percentage; 1) Based on historical average (2017-2019, excluding 2020 due to COVID effects) volumes (bidirectional) between Asia

and Europe in March, assuming trade was blocked for seven days; Source: Seabury Cargo Global Ocean Trade database, Seabury Cargo analysis (April 2021)

6 | DSV – Market update Air & Sea April 15th , 2021

Suez blockage: Suez Canal blockage by Ever Given impacts

the available vessel capacity in April and May heavily

Change in weekly capacity from before to Change in weekly capacity from before to Change in weekly capacity from before to

after Suez Blockage ASIA-MED after Suez Blockage ASIA-N.Europe after Suez Blockage N.Europe-ASIA

• Even though the Ever Given has been freed, the direct –and substantial -operational ripple effects are now clearly visible for the

coming months on the Asia-Europe services, in both directions. Blank sailings announced for week 15 and week 18

• As a consequence of the blockage, vessels have already been diverted around Africa and will continue on this routing,impacting

the ability to maintain the schedules announced just a few weeks ago. And this impacts the trade through Suez in both directions.

• We can see a drop of capacity (depending of the shipping line) of -20% to 30% on week 19-21 and for the exports out of Europe the effect is

happening now. This will have a consequence as well on equipment repositioning Source: Seaintel

7 | DSV – Market update Air & Sea April 15th , 2021

Declaration of General Average of the Ever Given vessel

Additional cost for cargo owners without cargo insurance to release their cargo from Ever Given in the future.

• General Average is special for transport by sea, as it means that all

parties having anything of value on board a ship shall participate to the

costs for saving the ship and cargo.

• Lloyd’s List has reported that Egypt is looking to claim around

$1bn in compensation for the casualty that closed the Suez Canal

for six days last month, according to the head of the Suez Canal

Authority.

• The shipowner has declared GA for the costs incurred, including for

the salvage operation, to protect the ship and the cargo and to

continue the intended voyage.

• These costs will eventually be divided proportionally between the

cargo interests based on the values of the cargo.

• The shipowner will have a lien on the cargo and shippers as cargo

owner may only have their cargo released from the shipowner when

proper security inform of an Average Guarantee (signed by cargo

Insurers) have been completed, signed and forwarded to the Average

Adjuster.

• If cargo is not insured ,the security in form of an Average Bond shall

be completed and signed and a cash deposit will be required instead

of an average guarantee. The security is needed by the shipowner to

secure their payment of contributions for their costs incurred.

8 | DSV – Market update Air & Sea April 15th , 2021

Suez canal blockage: A small fraction of impacted ocean demand

Asia-Europe trade could shift to air, for either of two main

reasons

High demand for finished articles Components to finish

Example: Laptops Example: Laptops

• In addition, short shelf life of

products (e.g. perishables)

may require air transport

Note: Showing average value densities for Westbound (Asia Pacific to Europe) air and ocean trade in March 2017, 2018 and 2019; 1) 50% of the average air value

density of $150/kg; Source: Seabury Cargo Global Air and Ocean trade databases; Seabury Cargo analysis (April 2021)

9 | DSV – Market update Air & Sea April 15th , 2021

Ocean freight

Update

10 | DSV – Market update Air & Sea April 15th , 2021MSC well on track to become the world’s largest container line

MSC vs Maersk Group – Fleet capacity history

• MSC currently operates a fleet of 587 containers ships which have

a total carry-ing capacity of 3,892,732 teu.

• Since Maersk’s fleet of 711 ships has a slot ca-pacity of 4,126,740

teu, the ‘gap’ between the two partners of the ‘2M Vessel Sharing

Agreement’ now stands at ‘only’ 234,000 teu.

• Irrespective of past de-velopments and fleet growth, the carriers’

opposing stance on container vessel newbuilding is expected to

see MSC overtake its Danish competitor and claim the global top-

spot some time in 2022

• MSC’s pipeline could grow even further, since a number of big

new buildings are believed to be joining the MSC fleet under long

term charters that have yet to be confirmed. Maersk meanwhile is

not expected to place any large orders soon.

Source: Alphaliner

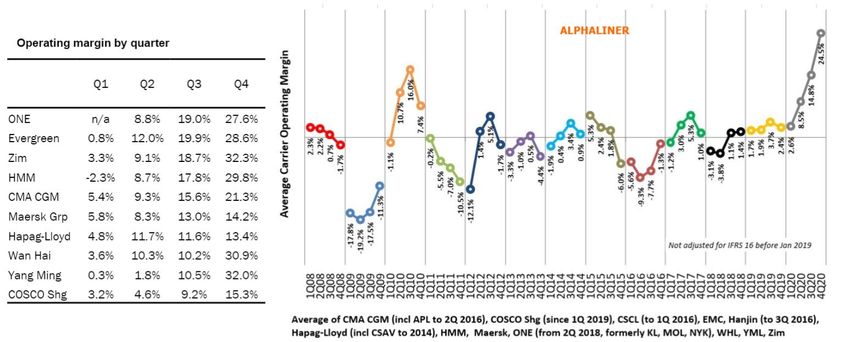

11 | DSV – Market update Air & Sea April 15th , 2021Aggregate operating earnings top Shipping lines USD 15 Bn in

2020

Main carriers: Average core EBIT margin by quater

• The container shipping operations of the nine leading carriers reporting public numbers recorded an aggregated operating income of USD 15.1 Bn

in 2020, up from USD 4.8 Bn recorded in 2019, underlining the stark impact of COVID-19.

Source: Alphaliner

12 | DSV – Market update Air & Sea April 15th , 2021USA and EUROPE port Congestion is not improving

Terminal congestion is not improving and in North America Intermodal congestion is also not improving

Average US Port congestion (New York, Savannah, Houston and Los

Average port congestion 5 days, Europe Main ports

Angeles, 10 days delay

• Port congestion is becoming an issue in Europe with delays above 5 days and in north America reaching to almost two weeks

• We are reaching all time high in terms of port congestion and it is not improving, it seems that it is maintaining a plateau level

• Carriers are still announcing void sailings to avoid more congestion on the ports (both Asia, US and Europe)

Source: Alphaliner and Seabury

13 | DSV – Market update Air & Sea April 15th , 2021Trade Update

Asia Pacific Equipment Situation

Container shortage & Poor schedule reliability:

• All equipment types remain tight across Asia.

• Capacity discipline among carriers is expected to

continue.

• Shipper should consider booking as early as

possible 3-4 weeks in advance.

S= SURPLUS OF CONTAINERS

D= DEFICIT OF CONTAINERS

14 | DSV – Market update Air & Sea April 15th , 2021Worst vessel performance ever recorded: 34,9%

Global Port congestion is increasing transit time to now almost 7 days

Schedule Reliability Average delay of late vessels

8.00

90.0%

80.0% 7.00

70.0% 6.00

60.0% 5.00

50.0% 2020

2020 4.00

40.0% 2021

2021

3.00

30.0%

2.00

20.0%

10.0% 1.00

0.0% 0.00

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

Source: Sea-Intelligence Maritime Analysis

15 | DSV – Market update Air & Sea April 15th , 2021Bunker price continue upward momentum

800

700

600

• Following a sharp drop in bunker fuel

VLSFO prices in Mar-Apr 2020 due to the

500

IFO380 pandemic, prices then have started to

rebound and stabilize

400

• Fuel price have begun to increase

300 significantly Jun – early Nov 2020

200 • Can anticipate for BAF increase in line

with the continuing upward trend in

100 VLSFO price

0

Source: Ship&Bunker

16 | DSV – Market update Air & Sea April 15th , 2021Ocean Freight Asia - Europe

Suez Canal blockage by Ever Given impacts the available vessel capacity in April

and May heavily

SCFI – North Europe WB Rate Index Rates remain stable at slow pace

(US$/40ft)

SCFI Levels Week 14-2021:

• Shanghai – North Europe: USD 7,928/ FEU

$9.300

• Shanghai – Mediterranean: USD 8,052/ FEU

$8.300

$7.300

Spot market rates are on high level, with challenges to

find space

$6.300

$5.300 • Empty Equipment flow is disrupted by the Suez Canal

blockage

$4.300

$3.300 • Previous equipment situation in March was under

control but tight. Going forward, carriers will have

$2.300

severe equipment issues in Q2 again.

$1.300

• Demand is not strong but exceeding the limited

allocation by far.

Source: SCFI Week 14

17 | DSV – Market update Air & Sea April 15th , 2021Ocean Freight Asia - North America

Strong demand and lack of equipment maintains rates in all time high

SCFI Transpacific EB Rate Index (US$/40ft)

$4.300 All lines are now short on equipment, 40‘HC boxes are

in short supply.

$3.800 SCFI Levels Week 14-2021:

• Shanghai – US West Coast: USD 3,931/ FEU

$3.300 • Shanghai – US East Coast: USD 5,334/ FEU

Lines are now blanking sailings to LAX due to the

$2.800 congestion

$2.300

• There is still a strong demand in the trade and it is

expected new services and capacity to be added.

$1.800 • We expect demand to remain strong after could remain

into October and beyond

Source: SCFI Wekk 14 2021

18 | DSV – Market update Air & Sea April 15th , 2021Ocean Freight Asia – South America (East Coast)

The ocean freight market is far from stable and rates are going up/down everyday.

SCFI to Santos Brazil (US$/40ft)

$17.000

$15.000

SCFI Levels Week 10-2021:

$13.000 • Shanghai – Santos: USD 14,310/ FEU

$11.000

Capacity remains unchanged, except for announced blank

$9.000

sailings, equipment in Asia is an issue eventhough demand

$7.000 is not strong

$5.000 - ECSA: Average of 30K TEU/week supply + European

routing (adding up to 8-10%).

$3.000

$1.000

- WCSA/MEX : average of 78K TEU/week supply.

Source: SCFI Week 14-2021

19 | DSV – Market update Air & Sea April 15th , 2021Ocean Freight Europe – Asia

Full ship scenario continues

Drewry Rotterdam Shanghai (US$/40ft)

$2.000

Drewry Levels Week 14-2021:

$1.900

• Rotterdam – Shanghai: USD 1,465/ FEU

$1.800

$1.700

Allocation of space is a big problem in the trade

$1.600

$1.500 • Some carriers have introduced temporary booking stops

$1.400 in order to cope with the surging export demand

$1.300 • Port congestion and the on-going equipment shortage is

$1.200 creating massive operational challenges

$1.100

• Several Post-CNY blank sailings expected for 2nd half

$1.000 of March/early April. Details to follow

Source: Drewry Week 14-2021

20 | DSV – Market update Air & Sea April 15th , 2021Ocean Freight Europe – North America

Rates are increasing – Bookings required well in advanced

Drewry Levels Week 14-2021:

• Rotterdam – New York: USD 2,601/ FEU

Drewry Rotterdam New York (US$/40ft)

$4.000

$3.800 Bookings need to be places 6-8 Weeks in advanced

$3.600

• Rates are being added various surcharges like PSS,

$3.400 EIS, EBS etc. Expect a GRI to be announced in

$3.200 February to become effective by latest April 1, 2021

$3.000 • Equipment deficit in most origin regions in Europe. This

$2.800 will remain the biggest issue for quite some time.

Carriers charge EIS/EBS to cover empty moves,

$2.600

although no guarantee from carriers that they can

$2.400 provide the needed containers.

$2.200

• Port concession is adding to the problem, situation is

$2.000

critical

• Bunker oil prices are on a upturn, we expect carriers to

charge higher BAF in March + Q2

Source: Drewry Week 10-2021

21 | DSV – Market update Air & Sea April 15th , 2021Ocean freight market overview – High rates will remain on Q2

TRADE LANE COMMENTS RATES AND SPACE

• Empty Equipment flow is disrupted by the Suez Canal blockage

ASIA to Europe • Spot Market rates are on a high level anyway already.

• Long term rates will increase

• Rates steady at historical highest levels.

ASIA to NAM • Equipment shortage, specially in Vietnam and South east Asia.

• Ships are waiting at anchor in LAX, Oakland and Savannah

• The need of equipment is affecting all trades globally

• Vessel are full and less capacity available

Europe to NAM

• Congestion (Port facility) surcharge for the port of New York applied by Ocean Carriers. This

is applicable for all cargo to and from Europe

• Low vessel-transit-time reliability, and congestion at major terminals.

Exports from • Post-Suez vessel bunching expected at key India ports, causing more downstream delays.

India Suggested booking 15-20 days prior to CRD.Space is tight

• Booking needs to be placed one month in advance

ASIA to LATAM • ASIA to LATAM due to longer transit times needs to offset with higher rates

• Rates are stable

• Port congestion at most of Asian ports

INTRA ASIA • New bunker level. Australian ports are still congested but improving

• Average Intra asia rate level have eased slightly and stabilised but is still overall higher

22 | DSV – Market update Air & Sea April 15th , 2021Airfreight Update 23 | DSV – Market update Air & Sea April 15th , 2021

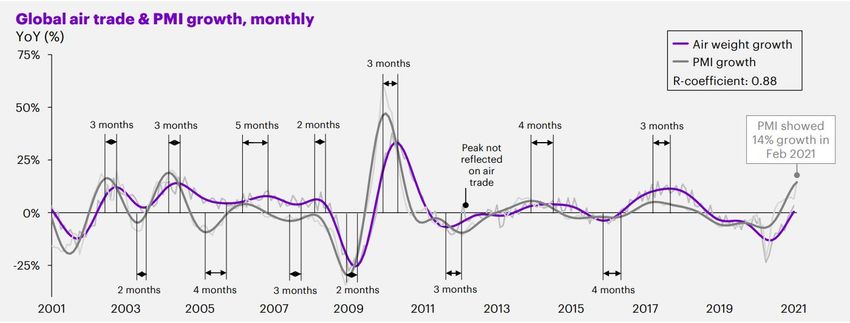

The Purchasing Managers Index hints at strong air freight

demand in the coming months

Global air trade & PMI growth, monthly

YoY (%)

Double-digit PMI

growth has not been

recorded for almost

10 years

Notes: Air trade values until January 2021 (in weight); PMI values until February 2021; PMI is JP Morgan Global Manufacturing PMI

Source: Market Economics, Seabury Cargo Global Air Trade Database; Seabury Cargo analysis (April 2021)

24 | DSV – Market update Air & Sea April 15th , 2021Leading indicators for China, USA and EU indicate a

recovery at different speeds in the short term

Capacity

constraints will

be the limiting

factor to air

cargo export

demand

Note: forecasts made based on following correlation factors (R): China=0.79; USA=0.80; EU=0.85; Air trade values until December 2020 (in weight); PMI values

until February 2021, CLI values until February 2021; This forecast does not consider potential impacts of the coronavirus outbreak on air trade Source: Markit

Economics; OECD; Seabury Cargo Global Air Trade Database; Seabury Cargo analysis (April 2021)

25 | DSV – Market update Air & Sea April 15th , 2021Air cargo capacity still down 7% YoY in Q1 2021

After strong declines in 2020, air cargo demand completed

its recovery to 2019 levels in January

International air cargo capacity growth, Jan – Mar 2021

% growth vs last year

Global capacity decline: -7%

The Transpacific and Asia to Europe were the only trade lanes showing positive capacity growth rates in Q1 2021

Note: Arrow thickness representative of May 2020 capacity, direct flights only; all flows indicate region-to-region capacity; regions are indicated by color coding; all dates measured in UTC; 1) Total cargo capacity includes

international widebody passenger and all freighter flights; 2) Comparing capacity between 22 Feb- 7 Mar 2021 to capacity the same weeks in 2019; Source: Seabury Consulting Capacity Tracking database, Seabury Consulting Source: Seabury

analysis (March 2021)

26 | DSV – Market update Air & Sea April 15th , 2021The air cargo demand-supply imbalance has pushed load factors

and yields to historically high levels

International load facto development Gross airline yields

FTK/ATK (%) $/kg (quarterly average)

• Load factors have

increased 20% since the

beginning of the pandemic

Notes: Gross yields based on IATA cargo eChartbook (until October 2019), WACD yield data (until Feb 2021); FTK & ATK data based on IATA Carrier Tracker CTK

and ACTK, respectively, through Jan 2021; Source: IATA eChartbook; IATA Monthly Traffic Results; IATA Air Freight Monthly Analysis; WorldACD website;

Seabury Cargo analysis (April 2021

27 | DSV – Market update Air & Sea April 15th , 2021A year after the outbreak of COVID-19, freighters (+25%)

keep driving global capacity recovery

Weekly international air cargo capacity, Feb 2020 – Mar 2021

Thousand of tons

• Belly cargo capacity

recovers slowly; though is

still 47% below pre-COVID-

19 levels

Note: Direct international capacity only; All freighters and widebody passenger aircraft only; 1) Comparing capacity between Jan – Mar 2021 vs Jan – Mar 2020

Source: Seabury Cargo Capacity Tracking database, Seabury Cargo analysis (April 2021

28 | DSV – Market update Air & Sea April 15th , 2021Air exports recovery is no longer exclusive to North East Asian

countries

Air exports by origin region, Jan 2020 – Jan 2021

Index (Jan 2020 = 100)

• The speed of recovery

still varies by region;

North America and Asia

Pacific (excl. NEA) are

the latest regions to

return to pre-pandemic

levels

Source: Seabury Cargo Global Trade Database, Seabury Cargo analysis (April 2021)

29 | DSV – Market update Air & Sea April 15th , 2021Automotive (+24% YoY increase) and high tech (+8%) led demand

recovery in the last quarter

Industry summary, Nov 2020 – Jan 2021 Top/bottom commodities, Nov 2020 – Jan 2021

Air weight change (tonnes) and growth (%) Air weight change (thousand tonnes) and % growth

Source: Seabury Cargo Global Air Trade Dashboard; Seabury Cargo analysis (April 2021)

30 | DSV – Market update Air & Sea April 15th , 2021Many widebody passenger aircraft orders have been deferred

while freighter orders have increased vs. last year

Change in planned widebody aircraft deliveries 1 Apr 2020 vs. 1 Apr 2021

Number of Aircraft

• ~1,900 widebody

passenger aircraft are

still parked despite the

belly capacity

Note: Snapshot of order book as of the first day of the month; Showing widebody aircraft only; 1) Including aircraft that are already delivered in 2020; 2) Aircraft ordered

by UPS, FedEx and DHL; 3) Difference of total orders as of 1 April 2021 and orders as of 1 April 2020. Aircraft orders that have been deferred to after 2029 are

considered as cancellations; 4) Total planned deliveries from 2020 to 2029, including aircraft already delivered in 2020; Source: Cirium Fleet Database, Seabury Cargo

analysis (April 2021)

31 | DSV – Market update Air & Sea April 15th , 2021Asia Pacific has shown the strongest recovery in air

imports, registering positive YoY growth in Jan’21

Global air import change by region, Jan 2020 – Jan 20211

Thousand tonnes change

Air imports of all other

regions have (almost)

recovered to Jan’20

levels

Notes: 1) Comparing against same month previous year

Source: Seabury Cargo Global Air Trade Database, Seabury Cargo analysis (April 2021

32 | DSV – Market update Air & Sea April 15th , 2021Air freight market overview

Many shipper

TRADE LANE COMMENTS RATES AND SPACE

• The story in Asia continues to be capacity. With market demand at peak levels,

Exports from

capacity is being further constrained pushing rates to the highest levels of the

China / Hong Kong

year. We see a ramp up of volumes by the beginning Q2.

• North Asia (Korea/Japan) and Southeast Asia markets are very busy and yields

Exports from JP, KR and continue to climb as demand exceeds available capacity.

South Asia • The yield difference between these markets and China is approaching $4-5 per

kg.

Exports from • Lack of space and high rates

India/Bangladesh • Limited capacity available (limited PAX) and strong demand at the moment

• Trans-Atlantic market continues to be very strong in both directions as demand

outstrips capacity.

Export from Europe

• Cargo is taking between 5-7 days minimum for uplift so please plan ahead and

be patient with transit times.

• US Export market is strong to both Europe and Asia. The backlogs to Europe

are especially acute and transit times are much longer than normal. With the

Exports from NAM

continued drought of belly capacity, expect these conditions to continue into the

foreseeable future.

33 | DSV – Market update Air & Sea April 15th , 2021You can also read