Dixon Technologies Initiating Coverage - MarketsMojo.com

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Initiating Coverage

Dixon Technologies

16 OCT 2019

16 OCT 2019 Company Report

Buy

Target Price: Rs 3,649

CMP : Rs. 3,005

Potential Upside : 21%

MARKET DATA

No. of Shares (Cr) : 1.13

Market Cap (Rs Cr) : Rs. 3,395

Dixon Technologies

Free Float : 56%

Avg. daily vol (6mth) : 6526

52-w High / Low : 3230/1831

Bloomberg : DIXON IN

Sector: Consumer Durables

Promoter holding : 38.92%

FII / DII : 7.23%/ 22.38 %

Powering Durable Brands

Price performance

120

80

40

Jul-18 Dec-18 May-19 Oct-19

BSE Sensex Dixon Technolog.

Financial Summary (Consolidated) Shareholding pattern

Y/E Net Sales EBITDA PAT EPS Change P/E RoE Core RoCE EV/EBITDA Jun-19 Q-o-Q Chg

March (Rs Cr) (Rs Cr) (Rs Cr) (Rs) (%) (x) (%) (%) (x)

Promoters 38.92 (0.01)

FY18 2,853 112 61 54.8 26.5 61.1 23.7 34.9 32.8 FIIs 7.23 1.19

FY19 2,984 135 63 55.9 2.1 42.1 18.2 27.4 19.5 MFs / UTI 22.29 (1.43)

FY20E 3,868 181 98 86.6 54.7 34.7 22.9 28.6 18.6 Banks / FIs 0.09 0.05

FY21E 4,754 227 129 114.0 31.7 26.4 24.0 30.4 14.5 Others 31.47 0.2

Source: Company, Axis Securities CMP as on Oct 16, 2019

Hiren Trivedi - CM Research

| hiren.trivedi@axissecurities.com | (+91 22 4267 1759)

2

16 OCT 2019 Company Report

Dixon Technologies

Investment Rationale Sector: Consumer Durables

Dixon Technologies (Dixon) is a leading manufacturer of products for consumer durable brands in India. It has ~9.3% share in

Electronic Manufacturing Services providing cost efficient, end to end solutions to MNC’s and domestic OEM’s. Dixon’s products

include (i)consumer electronics - LED TVs, (ii) home appliances - Washing Machines, (iii) lighting products - LED bulbs (iv) mobile

phones and (v) CCTV & DVR. The company also provides repairs and refurbishment services through its Reverse logistics segment.

Dixon is a leading player in Flat Panel Display (FPD) TV with 50%+ market share; in LED Lighting it accounts for ~35%+ domestic

volumes and commands 40%+ share in the Washing Machines EMS market. Its key customers include Panasonic, Philips Lighting

India, Xiaomi, Samsung, Flipkart, Crompton Greaves Consumer Electricals, Lloyds, Haier, Reliance Retail, Wipro, Syska, Polycab

and Bajaj Electricals.

We expect revenues/earnings to grow at CAGR of 26% / 42.8% respectively over FY19-21E driven by

Higher contribution from

Faster adoption of consumer Strong growth led by backward

Increasing EMS opportunities FPD TV, Lighting & Washing

durables by younger population integrated cost effective

across segments and higher Machines segments; recovery in

propelled by increase in manufacturing and diverse

share of ODM revenues Mobiles and strong growth in

disposable income product offerings

Security Systems

We initiate coverage with “BUY” rating and a target price of Rs 3,649 i.e. 21% upside (implies 32x FY21E)

* OEM / OEM – Original Equipment Manufacturer / Original Design Manufacturer | EMS – Electronic Manufacturing Services

3

16 OCT 2019 Company Report

Dixon Technologies

Investment Rationale Sector: Consumer Durables

Higher growth in global and domestic CEA market

Indian CEA (Consumer Electronics and Appliances) market is expected to grow at a faster pace of ~19% CAGR between FY19-21E while

the global CEA market is expected to grow at a CAGR of ~8% between FY18-24E

Global *EMS/^ODM market is expected to grow at CAGR of 8.5% between FY19-21E, while India’s EMS/ODM segment is expected to

grow at 32.4% CAGR in the same period as many OEM’s outsource their manufacturing requirements in line with their strategy of keeping

asset light business model

High growth in consumer electronics and increasing EMS presents a huge opportunity for players like Dixon

Increasing trend towards ODM manufacturing augur well for Dixon

Dixon, a cost efficient solution provider and a leader in ODM segment is well equipped to capitalize on rising OEM’s demand for ODM

Company’s ODM share increased from ~15% in FY17 to 38% in FY19 owing to its focus on developing value added products for its

customers (20+ ODM products developed)

ODM business fetches ~200-300 bps higher margins than OEM business; EBITDA Margins expanded by 92 bps over FY17-FY19

In Home Appliances ODM share continues to be 100%, in lighting its ODM revenue stood at 71% (vs. 40% in FY18), and Consumer

Electronics ODM share is 9% (vs. 6% in FY18) which is likely to improve further as Dixon has converted large customer Panasonic from

prescriptive mode to ODM mode

^ODM =Original Design Manufacturer |*EMS – Electronic Manufacturing Services

4

16 OCT 2019 Company Report

Dixon Technologies

Investment Rationale Sector: Consumer Durables

Backward integration- improving cost efficiencies & enhancing product offerings

Developed capability in manufacturing critical components, thereby strengthening relationship with customers

Reduced dependency on third party suppliers leading to cost efficiencies

Increased number of product offerings within key segments like LED lighting, washing machines and FPD TV

Ability to provide value added ODM solutions to clients, thus leading to improved margins in key segments

Governmental thrust on domestic manufacturing

Local manufacturing to get a boost from Government steps to promote India as hub for innovation, design and manufacturing

Setting up port-based electronic manufacturing clusters to support local manufacturing and exports

Governments thrust on Electricity For All is expected to provide an impetus for increasing demand for consumer durables in rural and semi-

urban areas

Government push for energy efficient products via Domestic Efficient Lighting Programme (DELP), UJALA have resulted in higher demand

for lighting segment

The recent customs duty increase on CCTV cameras/DVR’s to 20% from 15% will promote local manufacturing and discourage imports

5

16 OCT 2019 Company Report

Dixon Technologies

Investment Rationale… Sector: Consumer Durables

Cost advantage over China

India’s labour cost at $1.7/hour is almost half vis-à-vis China at $3.3/hour making India an attractive manufacturing destination

China is witnessing sharp increase in labour cost as workers focus on highly skilled jobs resulting in lack of manpower at low end of

manufacturing value chain

Indian manufacturing costs to moderate due to economies of scale, government support (SLNP, Customs duty, Subsidies) and availability of

skilled & semi-skilled manpower

Strong client relationships, Acquisition of new customers

Dixon has strong relationship with existing customers, for e.g. half-a decade with Panasonic, almost 10 years with Philips

Similar to global EMS peers Dixon derives higher revenue share from anchor customers, however its constant endeavour is to acquire new

customers through new segments and increase offerings within existing segments (e.g. in Lighting segment its anchor customer Philips now

contributes ~45% to the segment revenues vs. ~90% earlier)

Recent client additions (during FY19) include Xiaomi, Panasonic-Anchor, Syska, Samsung, Flipkart, Crompton Greaves Consumer Electricals,

Lloyds, Wipro

6

16 OCT 2019 Company Report

Dixon Technologies

Investment Rationale… Sector: Consumer Durables

Leading EMS solutions provider

Dixon is a leading player in Flat Panel Display (FPD) TV with 50%+ market share, in LED Lighting it accounts for ~35%+ domestic volumes

and commands 40%+ share in the Washing Machines EMS market.

Proximity of manufacturing plants to OEM’s, end to end services including ODM solutions, cost efficient production along with reverse

logistics has led to Dixon becoming a preferred EMS partner with strong client relationships

Key customers include Panasonic, Philips Lighting India, Xiaomi, Samsung, Flipkart, Crompton Greaves Consumer Electricals, Lloyds, Haier,

Reliance Retail, Wipro, Syska, Polycab and Bajaj Electricals

Cost efficient manufacturing with lean working capital management

Optimum utilisation of assets :Flexible manufacturing lines with standardised equipment used for diverse products has led Dixon to derive

benefits of scale while remaining asset light leading to cost efficiencies

Lean working capital : Dixon has maintained lean working capital despite increasing product offerings within segments and addition of new

product segments due to efficient inventory management and favourable credit terms from suppliers

New client addition along with capex and expenditure related to ramp up in capacities to led to stretching of working capital in FY19

Improved collections and efficient inventory management along with asset light nature of the business will allow Dixon to maintain lean

working capital days going forward

7

16 OCT 2019 Company Report

Dixon Technologies

Higher growth opportunity led by strong domestic CEA market Sector: Consumer Durables

Growth of Indian CEA market Indian CEA market to grow at faster pace

Global demand for consumer electronics goods is set to grow

FY21E due to:

Innovative product offerings leading to faster replacement

FY20E of consumer goods

Adoption of smart technologies integrated into the product

FY19 Proliferation of e-commerce

The global consumer electronics market was valued at $

FY18 1,172 bn in 2017 as per Zion Market Research, is expected

(Rs bn)

to touch $1,787 bn by 2024 at CAGR of 6%.

FY17 Global consumer electronics growth is expected to be driven

by increasing demand from Smartphone, Television, DVD

FY16 Players, Refrigerators, Washing Machines, Digital Cameras,

and Hard Disk Drives

FY15 Indian CEA market grew at CAGR of ~14% between FY13-

FY19, is expected to grow faster at CAGR of 19% between

FY14

FY19-21E, from Rs 4,178 bn in FY2019 to Rs 5,940 bn in

FY2021E due to

FY13

Increasing working population

Early adoption of consumer goods

0 2,000 4,000 6,000 8,000

Easy availability of finance

Total CEA Market Consumer Electronics Appliances

Source: Company, Axis Securities

8

16 OCT 2019 Company Report

Dixon Technologies

Indian EMS/ODM growth to outpace Global EMS/ODM growth Sector: Consumer Durables

Global EMS/ODM Market by Value Indian EMS/ODM Market by Value

800 10.0

670 8.1

700 615

569 8.0

600 502 532 6.1

455 478

500 436 444 6.0 4.7

($ bn)

($ bn)

400 3.8

4.0 3.0

300 2.2

1.6 1.9

200 2.0 1.4

100

0.0

0

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

FY21

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

FY21

Global EMS/ODM market to grow at CAGR of 8.5% between

OEM’s preference for strategic tie-up with EMS players like

FY19-21E led by OEM’s focus on : Dixon to meet domestic demands will lead Indian EMS/ODM

Differentiation via new product innovation market to grow at robust 32.4% during FY19-21E

Brand building India’s EMS market is just 0.6% of the global EMS market and

Marketing and distribution is expected to reach 1.6% by CY2021, aided by

Global EMS market growth will be driven by higher electronics Rising per capita income and affluent middle class

consumption by end user industries like IT & Telecom, Consumer Increasing nuclear families

Enhanced features and availability of finance leading to early

Electronics, Automotive, Healthcare and Industrial.

adoption of consumer electronics

Top categories that are expected to drive Indian EMS segment Make In India thrust

are Mobile phones, Telecom, Consumer electronics and Subsidies and incentives by central/state governments

Appliances Rationalisation of duties and taxes

Dixon being the 2nd largest EMS company to benefit from robust growth in domestic EMS demand

Source: Company, Axis Securities 9

16 OCT 2019 Company Report

Dixon Technologies

Enhancing capabilities through backward integration Sector: Consumer Durables

Segment Backward Integration Advantage - Dixon Segments Key Products offerings

Plastic moulding, Increased capacity will cater

Home Appliances LED TV’s–19’’to 65’’& 4K2K technology, Home Theatres– 2.1&

panels, control table, to 33% of the Indian Market Consumer Electronics

( Washing Machines) 4.1channel, FPD, Smart TVs

twin tubs, Motors requirement, Value Addition

Increased ODM share to

Sheet metal, plastic LED Lights, Ballast, Tube lights, Batten, Down lighters, CFL/LED

Lighting 90%, led to customer Lighting Products

moulding and wound Drivers

( LED bulbs, battens ) additions, enabled providing

components

end to end solutions

Became largest LED TV Mfg Home Appliances Semi-automatic washing machine ranging from 6.2kg to 8.2kg

Backlight units, plastic in India, capacity can cater

Consumer Electronics

moulding, circuits, to 26% of Indian market Mobile Phones Feature & smart phones (2G, 3G, 4G/LTE, VoLTE & CDMA)

(FPD TV's)

LCM, SMT needs, Improvement in

Margins Security Systems CCTV Cameras, DVRs

Critical components that

Mobile Phones Repair –mobile phones, LCD/LED TVs, LED panel, home theatre,

PCB Manufacturing contributes to ~50% of the Reverse Logistics

( Feature & Smart phones) computer peripherals and other devices

value addition in a phone

Strategic product portfolio diversification

CFL Lighting, Washing CCTV,

Colour TV

Reverse logistics Machines Digital Video Recorder

2017

1994 2007 2008 2010 2010 2016

LCD TV LED TV Mobile Phones

1016 OCT 2019 Company Report

Dixon Technologies

Dixon’s manufacturing strength in key segments Sector: Consumer Durables

Dixon manufactures majority of end product components Dixon is able to offer cost effective solutions due to:

in-house : Backward Integrated manufacturing

60% of LED Lamps (components like Circuits & Plastic moulded parts) Flexible manufacturing lines used for diverse products with

50% of Washing Machines standardised equipment

32% of LED TV’s Economies of scale

Availability of skilled man power

Domestic Domestic/

Dixon Dixon Imported

Imported/ Dixon

Domestic

10% Imported 12% 12% Imported 10%

30% 10%

11%

5% Semi Automatic

30% LED Lamps LED TV 50%

9% Washing

Machines

25%

56%

30%

Circuit Plastics LED Others Circuit Plastics BLU LED Glass Others Plastic Parts Electronic motor Gear Box Timers Others

1116 OCT 2019 Company Report

Dixon Technologies

Well diversified leading EMS player Sector: Consumer Durables

Dixon’s market leadership in key segments Key EMS players and their offerings

EMS Market Focus &

Segment Companies Offerings Products

Share Competence

Consumer Electronics (FPD TV's) 50% +

Global companies

Lighting (LED Lights - volumes) 35%+

Home Appliances (Semi Automatic Washing Machines) 40%+ S/w Develop, Global & Indian Mobiles, Set top

Jabil,

product design, market - technical - Boxes, Telecom

Foxconn, Flex ,

Level of diversification – Dixon vs. Peers Sanmina , Wistron

prototyping, SMT, High Value add solutions, PC's,

PCBA, logistics products Desktops

Washing Lighting

LED TVs Mobile

Machine products

Large Indian Companies

Dixon Tech High High High Medium

ELIN India - - Low -

H/w design, S/w Mobile, Lighting

NTL, SFO Techno.,

MEPL Low develop, assembly, Domestic market - Products, Medical

ELIN , PG Group,

prototyping & Value add products & Defence,

DetlaLight - - Medium - Kaynes, Dixon

testing WM,FPD TV’s

Opetiemus - - - High

NTL Small Indian Companies

- - Medium -

electronics

Noble Low Medium - - SGS Tekniks, Local markets & LED Lighting ,

Sheet metal, plastic

Amara Raja exports medical electronics,

Videotex Medium - - - moulding,

Electronics, Hical -Low value HUPS systems,

transformers

Tech products inverters

Vimal Plast - Low - -

Source: Company, Axis Securities

Dixon’s leadership in key segments stems from integrated manufacturing capabilities across its business segments.

1216 OCT 2019 Company Report

Dixon Technologies

Governmental thrust on Domestic Manufacturing Sector: Consumer Durables

Make In India Ease of doing business - Aiding FDI Inflows

*M-SIPS: capital subsidy of 20% in SEZ (25%-non SEZ areas) India is among the top 10 countries globally, showing

Electronics manufacturing clusters: Financial assistance of up to improvement in World Bank’s ease of doing business index

50% and 75% of project cost for setting manufacturing clusters jumping 23 notches to 77th place in 2019

Preferential market access: government to prefer domestically

manufactured products FDI inflows in electronics in India increased 2.3X in 2018-19 at

Phased Manufacturing program: Government providing tax $ 451.9 mn vs.$196.9 mn in 2017-18 led by initiatives like

reliefs and rationalisation of customs duty

National Policy on Electronics - $400 bn turnover in domestic 100% FDI in Electronics Systems design & manufacturing sector -

electronics manufacturing by CY2025 automatic route

Promote EMS activities such as engineering and design of

PCBs, PCB assembly 100% FDI In contract manufacturing -automatic route

Led Lighting – lighting up manufacturing in India Rationalization of duties & taxes – a shot in the arm

With energy saving as objective, under #SNLP over 85.67 lakh Cut in duty of Open Cell to 0% from 5% - to promote local

street lights in 1400 cities across India have been replaced as manufacturing of LED TV’s

of July 2019 – aim to replace 1.34 cr street lights

Customs duty hike on Washing Machines (less than 10 kg) from

Under ^UJALA scheme total 34.76 crore LEDs distributed to

10% to 20% will make domestic production competitive

rural households through EESL –target of 77 cr LED lights to be

distributed going forward Customs duty increase on CCTV cameras/DVR’s to 20% from

Subsidies, incentives led to reduction in price of 9W led bulb to 15%, will promote local manufacturing and discourage imports

~Rs 70 vs Rs 160 thus prompting higher adoption aided by Reduction of Corporate Tax rate to 22% (15% for new units)

power for all initiative of government

Local production +demand generation+ attracting capital = Growing opportunities for Dixon

*Modified Special Incentive Package Scheme(M-SIPS) ^ UJALA- Unnat Jyoti by Affordable LEDs for All,#SLNP - Street Light National Programme

1316 OCT 2019 Company Report

Dixon Technologies

Labour cost advantage to aid local manufacturing Sector: Consumer Durables

India’s labour cost is among lowest in the world Indian manufacturing costs to moderate due to economies of

50 scale, government support (SLNP, Customs duty, Subsidies)

40.5 China’s salaries, since 2013 have risen between 21% to 41% in

38.0 its manufacturing hubs and expected to increase further due

40

worker’s preference for hi-tech jobs

(USD/hr)

30 24.0 India is better placed to attract OEM’s as China’s cost to rise due

20.7 to withdrawal of subsidies, shift to higher level jobs and higher

20 rate of increase in labour costs

9.4 Low cost of production in India will incentivize brands to

10

3.3 1.7 manufacture locally/depend on domestic manufacturers

0 Dixon is well placed to cater to brands being an end-to-end cost

efficient solutions provider in FPD TV’s, LED Lamps & Washing

US Germany Japan S.Korea Taiwan China India

Machines segment

Labour and Overheads cost differentials favour manufacturing in India Increasing Average Manufacturing wages in China

20 19% 80000

16.5%

72,088

*LOH as % of total cost

15 13% 13% 60000

12.5%

64,452

12%

(CNY/Year)

59,470

55,324

10

51,369

40000

46,431

41,650

36,665

5

30,700

20000

26,599

0

FY14 FY17 FY21E

0

India China 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Source: Deloitte Global Manufacturing Competitiveness Index 2016 ,National Bureau of Statistics China, Company , Axis Securities.,*LOH = Labour & Overheads

1416 OCT 2019 Company Report

Dixon Technologies

Lower Penetration & Low localization –huge opportunity Sector: Consumer Durables

Penetration of Consumer Durables Huge potential for higher penetration

100% 89% 85% Government’s thrust on Electricity For All is expected to provide an

80% 70% impetus for increasing demand in rural and semi-urban areas

60%

60% Easy availability of credit, increasing urbanisation, will lead to higher

demand

40% 30%

25% TV industry in India is estimated to grow from Rs 660 bn in CY2017 to

17% 20%

20% 10% reach Rs 862 bn in CY2020

4%

0% Dixon has the largest TV manufacturing capacity in India at 36 lakh TV

Washing FPD TV Room AC Air Cooler Refrigerator sets per anum

Machine Large opportunity for EMS players like Dixon in under penetrated

India Global

segments like Washing Machines (60% scope) and FPD TV’s (~30%

scope)

Localization levels in appliances

Increased scope for localization

Washing Machine 65 Rising cost of imports (increased customs duties) to push brands to

35

increase their localization content to fulfil growing demand for consumer

FPD TV 30

70 goods

90 Lower cost, end to end solutions, innovative product offerings, value

Air Coolers

10 added aftermarket services to aid higher localization

Residential ACs 65 Dixon better placed than peers to capitalize on growing localization

35

needs of customers due to

Refrigetaor 70

30 Leading EMS manufacturer in three segments

0 20 40 60 80 100 Fungible manufacturing capabilities across segments

Fully backward integrated facility

Localisation levels in Appliances Import

Strong R&D capabilities to offer innovative value added solutions

Source: Company, Axis Securities

1516 OCT 2019 Company Report

Dixon Technologies

Rising affluence - driver of increasing consumption Sector: Consumer Durables

Increasing per capita income leading to higher discretionary spends Key Drivers of Demand

3500 65% of the consumer durables demand comes from first time

3000 buyers as per industry reports

Rising affluent middle class population is estimated to form ~69%

3,023

2500

2,791

2,578

of total population by 2020

(In USD)

2,379

2000

2,199

2,036

1500 2,014 Changing lifestyle causing early adoption of white goods in young

1,762

1,640

1,610

1000 population, a strong demand generator

500 Increasing Per Capita Income in India leading to higher spends on

0 aspirational goods including consumer durables like FPD TV’s,

CY 14 CY 15 CY 16 CY 17 CY 18 CY 19E CY 20E CY 21E CY 22E CY 23E Washing Machines and Mobile phones

Source: IMF

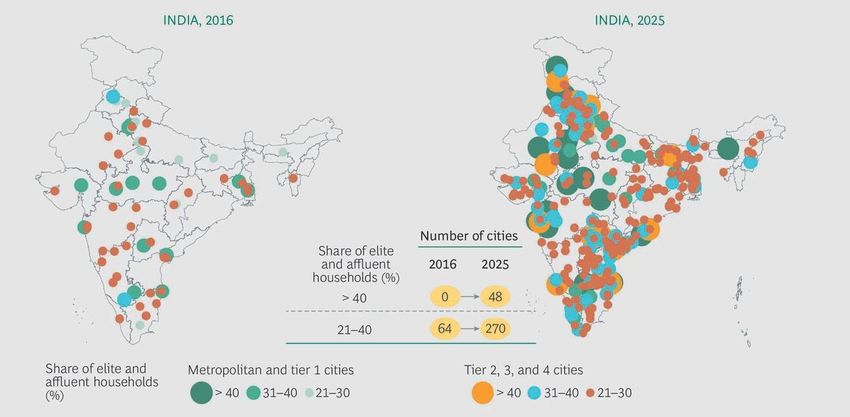

Wide spread affluence to drive consumer

spending across India

Elite and affluent households—will become

the largest combined segment by 2025,

accounting for 40% of consumption

compared with 27% in 2016

The number of cities having greater than

40% elite and affluent households will

increase to 48 in 2025 (vs. Nil in 2016)

while cities having 21-40% elite and affluent

households will increase to 270 in 2025

( vs. 64 in 2016)

Source: BCG Centre for Customer Insight

1616 OCT 2019 Company Report

Dixon Technologies

Company Profile Sector: Consumer Durables

Dixon Technologies started manufacturing operations in the year 1994

with production of colour TVs

Has over the years evolved into fully integrated end-to-end product and

solution provider to OEM’s ranging from global sourcing,

manufacturing, quality testing and packaging to logistics Dehradun (4 Units)

Diversified into 5 segments like LED TV, Smart TV, LED bulbs & Tube Noida (4 Units)

lights, down lighters, Semi-Automatic Washing machines, Feature

phones & Smart Phones, CCTV camera’s & DVR’s, with various offerings

in each segment

Dixon has 10 state of the art manufacturing facilities supported by 3

R&D centres (2 in India and 1 in China) that focus on value addition to

its products

Strategic location of plants:

Near customer’s facility ensuring prompt response to clients manufacturing Tirupati (2 Units)

requirements Manufacturing Units

In proximity to Chennai & Krishnapatman ports - ability to cater to South East

Head Office

Asian markets through exports

Having flexible and cost efficient manufacturing capabilities with

availability of skilled and unskilled manpower

Plant Location Products manufactured currently Year Estb Focus on making Tirupati a mother plant

Noida-I LED bulbs, LED drivers, PCB assembly of Airconditionals 1996 Area 12 acres, 2 lakh sq feet construction space

Noida-II Mobile phones 2016 Focus Product & Geographical expansion

Noida-III Reverse logistics, LED Bulbs 2009 Benefits SGST exemption for 8 years (refund method)

Noida-IV LED bulbs and parts 2009 Subsidies on land rent, electricity & water

Proximity to Chennai port ( ~ 136 kms)

Dehradun - I facility LED bulbs, Battens, T-LEDs, Down Lighter, Ballast, etc. 2007

Dehradun - II facility Semi -automatic washing machines 2010 Products LED TV’s; Dixon expanded capacity from 2.4 mn to 3.4 mn p.a

CCTV’s capacity 6 lakh per month

Backward integration of plastic parts,Sheet metal DVR’s capacity 1.5 lakh per month

Dehradun - III facility 2009

components

Dehradun -IV facility Washing Machines 2018 Planned

Fully Automatic Washing Machine line with 5 lakh units annually

Tirupati LED TVs; Security systems (CCTVs, DVRs) 2017 Expansion

Source: Company, Axis Securities

1716 OCT 2019 Company Report

Dixon Technologies

Management Team Sector: Consumer Durables

♦ Has more than 2 decades of experience in the EMS industry. He has held positions like chairman of the

Sunil Vachani,

Executive Chairman Electronics and Computer Software Export Promotion Council of India and Co-Chair of the CII ICTE

Committee. He is currently the vice president of CEAMA

Atul B. Lall, ♦ 26+ years of experience in the EMS industry; significant contribution to the overall growth of the Company

Managing Director and successful completion of IPO, he is responsible for company’s overall business operations

Saurabh Gupta, ♦ Over 17 years of experience in finance & strategy. He is associate of the ICAI & an MBA from MDI,

Chief Financial Officer Gurgaon. Honored with Business World-Yes Bank most promising Future CFO in Large Corporate category

Mr. Vineet Kumar Mishra, ♦ Over 22 years experience in the manufacturing industry; worked with Samsung India, Hotline Witties

President - COO Lighting Electronics and Onida Savak

♦ Around 3 decades of experience in factory operations, manufacturing, supply chain, global sourcing, and

Mr. Pankaj Sharma,

business development. Has worked with Bestavision Electronics, Samsung, Jain Tube Company , Bigesto

President - COO Mobile Phone

Foods, Satkar Exports,Shirllon

♦ More than 30 years of experience in the field of plastics moulding. He has worked with Dipty Lal Judge

Mr. Rajeev Lonial,

Mal, Noble Moulds, Evershine Moulding, Ever Shine Plastic Industries, Essen Fabrication & Engineering and

President COO Washing Machine

Shree Krishna Keshav Lab

♦ He has a rich and extensive experience of 28+ years of across Manufacturing, Technology, Business

Mr. Abhijit Kotnis,

Development and sourcing fields. He was associated with Videocon Group for close to three decades in

President COO Television

various roles

Source: Company, Axis Securities

1816 OCT 2019 Company Report

Dixon Technologies

Key clients across various segments Sector: Consumer Durables

Segments Key Clients

Consumer Electronics

Lighting Products

Home Appliances

Mobiles

Security Systems

1916 OCT 2019 Company Report

Dixon Technologies

Consumer Electronics Sector: Consumer Durables

FPD TV market (mn units) EMS Opportunity in FPD TV

30 12.5

26.2 10.8

25 10.0

(mn Units)

(mn Units)

20 17 7.5

15

5.0 4.2

10

5

5 2.5

0.1

0 0.0

FY13 FY18 FY21E FY13 FY18 FY21E

Replacement demand, multiple TVs in household and upgradation to Consumer Electronics segment revenue growth

new features is expected to drive FPD TV market growth at CAGR of

15.5% in volume terms and 14.3% CAGR in value terms between 1600

FY18-21E

OEMs focus on marketing & rural penetration will lead the EMS/ODM 1,194

segment in consumer electronics industry to grow at a CAGR of 37% 1200 1,073

thus providing huge opportunity to Dixon

845

(Rs Cr)

Dixon is the leader in FPD TV ODM segment with 50%+ share, while 776 770

800 698

the nearest competitor’s share stands at ~ 8%

Further the contract with Xiaomi to manufacture TV’s is expected to

drive revenues in the consumer electronics segment going forward.

400

We expect revenues to grow at 14% CAGR and stable margins

between FY19-21E

The key brands catered to by Dixon include Xiaomi, Panasonic, Marq, 0

Koryo, Lloyd, TCL, Philips etc. FY14 FY15 FY16 FY17 FY18 FY19

Source: Company, Axis Securities , LCM = Liquid Crystal Monitor , SMT= Surface Mount Technology

2016 OCT 2019 Company Report

Dixon Technologies

Lighting Products Sector: Consumer Durables

LED Lighting volume growth As per TechSci, the Lighting products market in India is expected to

1600 1482 grow at CAGR of 24.6% during CY2016- CY2022 touching $ 3.76 bn

The demand for LED is expected to be driven by:

Increasing adoption due energy savings & longer life of LED lighting vis-

1200

(mn Units)

a-vis incandescent lighting

Government initiatives like Unnat Jyoti by Affordable LEDs for All (UJALA)

800 664 scheme, Street lighting National Program (SLNP) – for replacing old

bulbs by LED lights

400 Higher adoption due to increasing affordability as EESL offers subsidy on

LED lights to the end customer

67

The EMS/ODM segment is expected to grow at a CAGR of 43.9% in

0

FY13 FY18 FY21E

value terms thus providing huge opportunity to Dixon

Dixon caters to major brands in the lighting segment viz Panasonic – Lighting Products segment revenue growth

Anchor, Bajaj, Wipro, Syska, Usha, Polycab, Jaguar, C&S, RR Cables,

Luminous 1000 919

Dixon’s capacity of 20 mn bulbs p.m can cater to ~54% of Indian 774

market requirement 800

Dixon is among the top 5 global manufacturers in terms of scale in LED

Bulbs 600 551

(Rs Cr)

Dixon caters to 90% of Philips lighting requirements –it is also planning 430

to increase the relationship and supply LED’s for exports 400 308 301

71% of Dixons revenues are on ODM basis vs. just 4% in FY14

200

Dixon witnessed margin improvement from 3.1% in FY17 to 7.18% in

FY19 due to innovative product offering and increase in ODM share

0

We expect revenues to grow at 19%CAGR and margins the range of

7.2-7.3% between FY19-21E FY14 FY15 FY16 FY17 FY18 FY19

Source: Company, Axis Securities

2116 OCT 2019 Company Report

Dixon Technologies

Home Appliances Sector: Consumer Durables

Washing Machine market growth As per Frost & Sullivan Report semi-automatic washing machine

12 dominates the category with 56% volume market share

9.9

10 Dixon having dominant market share in EMS is better placed to cater

to global brands which may not have semi-automatic washing machines

(mn Units)

8 6.5 in their product portfolio

6 With a strategy to drive top-line and margin growth Dixon plans to

3.8 manufacture fully automatic washing machines adding to product

4

diversification

2

The key brands serviced by Dixon for semi-automatic washing machine

0 include Samsung, Panasonic, Godrej, Marq, Koryo, Thomson, Akai etc.

FY13 FY18 FY21E

Increasing product awareness, rising rural penetration (first time Home Appliances Revenues witnessed steady growth

buyers), affordable pricing and availability of finance to drive washing

machines market growth at a CAGR of 15.1% in volume terms to 9.9 400 374

mn units and 16.3% CAGR to Rs 163.7 bn in value terms between

FY19-21E

300

More companies opting for outsourcing to cater to local market & 250

exports will lead to EMS/ODM segment growth at CAGR of 41%

(Rs Cr)

between FY19-21E 188

200

Dixon derives 100% revenues from Washing Machines on an ODM 131

basis and offers the largest bouquet of ODM models in WM segment 107

100 85

Dixon is the leader in Semi Automatic Washing Machine EMS market

with ~42% share

0

We expect revenues to grow 13% CAGR with improvement in margins

between FY19-21E FY14 FY15 FY16 FY17 FY18 FY19

Source: Company, Axis Securities

2216 OCT 2019 Company Report

Dixon Technologies

Mobiles Sector: Consumer Durables

Mobile Phone contribution in overall electronics production in India Increasing domestic production & declining imports of mobile sets

400 2,000

2014-15 2018-19

300 1,500

(Mn units)

Contribution 9.93% 37.12%

(Rs bn)

200 1,000

Number of Mobile Assembly Plants 2 270 100 500

0 0

PMP by the government revived mobile phone manufacturing after shut 2015 2016 2017 2018 2019

down of Nokia plant in 2014

Imports ( In mn units) Production (In mn units)

Domestic production of mobile phones increased 5x volume wise and

Imports (Rs bn) Domestic Production (Rs bn)

~9.6x value wise between 2015-2019 while Imports declined from

216 mn units to just 20 mn

India is currently the 2nd largest smart phone handset manufacturing

Mobile Phones segment revenues to recover

country after China 1000

811

Smart phone users to double in India (829 mn by 2022) and feature 800

phone sales to reach 1bn globally, with higher demand from India 670

presents huge opportunity for players like Dixon

600

(Rs Cr)

Dixon’s acquisition of balance 50% in Padget Technologies(JV partner)

400 355

along with backward integration in mobile PCB’s will enable it to cater

to growing opportunity

200

We expect mobile segment revenues to grow at 32% CAGR during

20

FY19-21E led by recovery in the segment and acquisition of new

0

clients

FY16 FY17 FY18 FY19

Source: Company, Axis Securities, PMP = Phase Manufacturing Program

2316 OCT 2019 Company Report

Dixon Technologies

Security Systems (CCTV & DVRs) Sector: Consumer Durables

As per I.H.S market study the organized market for surveillance Key Demand Drivers

equipment was ~Rs 3500 cr in CY2017 and expected to touch

Rs 5,000cr – Rs 6000 cr in CY2020 led by increasing use of Increasing safety & surveillance measures being adopted by:

surveillance technologies in prevention and detection of theft & crime Government

Dixon entered security cameras and surveillance systems segment in Corporations

FY2018 as JV manufacturer with Aditya Infotech

Educational Institutes

Aditya Infotech owns CP Plus cameras and is also a distributor for

Chinese brand Dahua Technology (largest surveillance brands Residential associations & individuals

globally) Declining prices of electronic security systems

Dixon’s Security Systems segment witnessed robust growth during

FY18-19 and is expected to witness strong growth with improved Installation of surveillance by governments at public places

margins

Security Systems segment witnessed robust revenue growth Market for surveillance equipment

8000

120 112

6000

6000

80

3500

(Rs Cr)

(Rs Cr)

4000

49

40

2000

0

0

2017 2020

FY18 FY19

Source: ICEA, Axis Securities

2416 OCT 2019 Company Report

Dixon Technologies

Reverse Logistics – maintaining customer stickiness Sector: Consumer Durables

Reverse Logistics segment accounted for ~1% of revenues in FY19

OEMs prefer EMS players with end to end solutions including reverse logistics for after sales services , repairs & refurbishment

Reverse Logistics is an important end-customer support function

Dixon provides B2B reverse logistics for Set Top Boxes, Mobile Phones and LED TV panel, CCTVs through 17 service centres spread across different

states in India

Reverse logistics is supported by R&D team giving the company an advantage for repairs & refurbishment of Mobile phones, LED TV’s and products

like STB’s and Computer peripherals unlike competition

Return rates of Mobiles (9%), FPD TV (8%), washing machines (8%), STB’s (16%), will lead to growth of the reverse logistics with increasing sales of

these products

Reverse Logistics Market Share of products in Reverse logistics Market

70 30

60 25

(Vol mn units)

50 34.1

30.4 20

40 27.4 16.1

13.6

(Rs bn)

25.4 15

30 23.9 11.3

10

20

10 9.4

17.6 19.1

7.9 7.9

10 5 2.9 3.4

1.8 2.1 2.5

0.9 1.4

0 0

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY13 FY14 FY15 FY16 FY17 FY18 FY19

Computer Peripherals WM FPD TV Set Top Boxes Mobile Phones Computer Peripherals WM FPD TV Set Top Boxes Mobile Phones

Source: Company, Axis Securities

2516 OCT 2019 Company Report

Dixon Technologies

SWOT Analysis Sector: Consumer Durables

Strength Opportunities

An EMS supplier with leadership in Low penetration of consumer

3 fast growing segments durables in India

Strong & sticky customer

Increasing localization due to Make

relationships

in India, inherent cost advantage

Economies of Scale Opportunities Increasing demand for EMS

Cost efficiencies due to backward services

integration

Strategy of growing ODM revenues

Strong R&D capabilities, developed

20+ ODM solutions

SWOT

Strength Weaknesses

Threats

Threats

Weaknesses

Brands resorting to in house

production Client concentration, dependence

on anchor customers

Increase in competition

Relatively lower bargaining power

Higher imports by OEMs in OEM business

Source: Company, Axis Securities

2616 OCT 2019 Company Report

Dixon Technologies

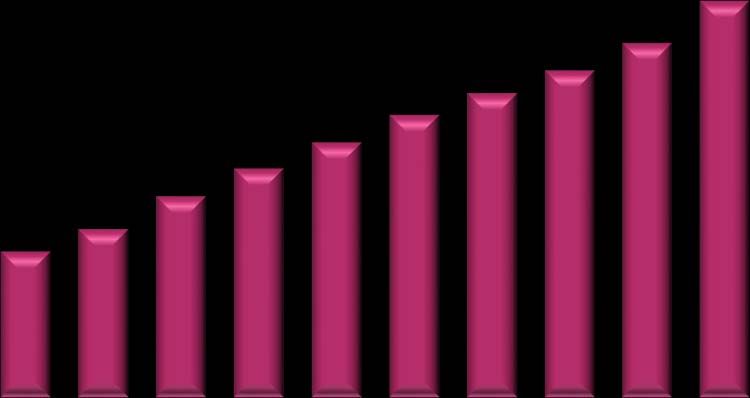

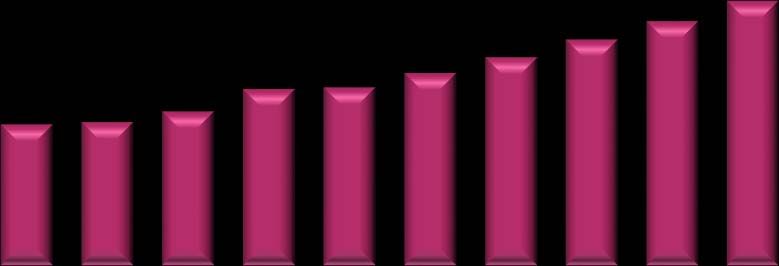

Robust growth in key segments to drive profitability Sector: Consumer Durables

Segment wise revenue Break-up Segment wise EBITDA contribution

4,754

5,000

300

3,868

4,000 227

2,890 2,984 200 181

3,000 2,457

135

(Rs bn)

(Rs bn)

91 112

2,000 100

1,000

0

0

FY17 FY18 FY19 FY20E FY21E

FY17 FY18 FY19 FY20E FY21E -100

Consumer Electronics Lighting Products Home Appliances Consumer Electronics Lighting Products Home Appliances

Mobile Phones Reverse Logistics Security Systems Mobile Phones Reverse Logistics Security Systems

Segment wise Margins

Key segments viz Consumer Electronics(40% FY19 revenues), Lighting

25.0 (31% FY19 revenues) and Home Appliances (13% FY19 revenues) to

20.0 continue contributing to top-line growth going forward

15.0

Operating efficiencies along with backward integration will lead to

10.0

higher contribution of operating profits by key segments

(%)

5.0

0.0 We expect increasing contribution to top-line from mobile segment led by

-5.0 growth recovery aided by cost effective backward integration

-10.0

Security systems is expected to grow faster (on a low base) with

FY17 FY18 FY19 FY20E FY21E

increasing revenue share and improved margins

Consumer Electronics Lighting Products

Home Appliances Mobile Phones Reverse logistics, a strategic offering to maintain stickiness of OEMs, is

expected to return to positive EBITDA with improved margins

Reverse Logistics Security Systems

2716 OCT 2019 Company Report

Dixon Technologies

Higher margin on increasing ODM support robust revenue growth Sector: Consumer Durables

Healthy top line growth Strong growth in EBITDA

5,000 4,754

250 4.8 6.0

3,868 4.5 4.7

4,000 200 4.2 3.9

3.7

2,853 2,984 4.0

3,000 2,499 150 2.6 181 227

2.5 2.3

2,000 1,410 100 135

1,119 1,220 112 2.0

816 91

1,000 50

59

20 26 32

0 0 0.0

FY16

FY18

FY13

FY14

FY15

FY17

FY19

FY20E

FY21E

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20E FY21E

Net Sales ( Rs Cr) EBITDA ( Rs cr) EBITDA (%)

Increasing ODM share in revenues aid margin expansion… We expect top line to grow at a CAGR of 26 % between FY19-21E, on

strong growth in key segments Consumer Electronics, Lighting and Home

100

Appliances and new client additions across segments backed by rising

80 wallet share with existing customers

62 Additionally, we expect mobile segment to return to growth path, with

(%)

60 78 73 77

85 top-line CAGR of ~32% between FY19-21E led by company’s efforts to

40 add new popular clients

Security Systems segment to post robust growth going forward

20 38

22 27 23 contributing ~7% of top-line from current ~3.8% led by growing

15

0 demand for surveillance equipments

FY15 FY16 FY17 FY18 FY19 We expect EBITDA margins to improve driven by higher cost efficiencies

ODM Revenue Share OEM Revenue Share and growing share of ODM revenues

Source: Company, Axis Securities

2816 OCT 2019 Company Report

Dixon Technologies

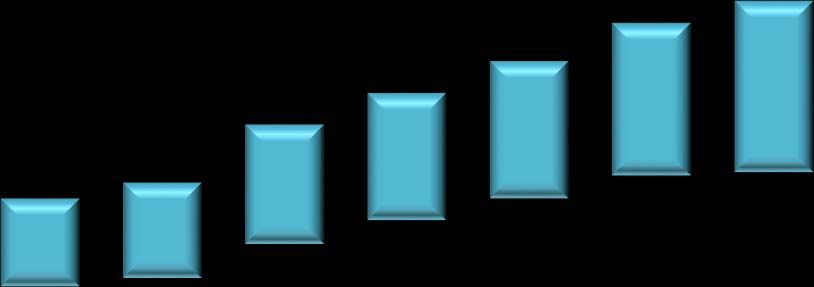

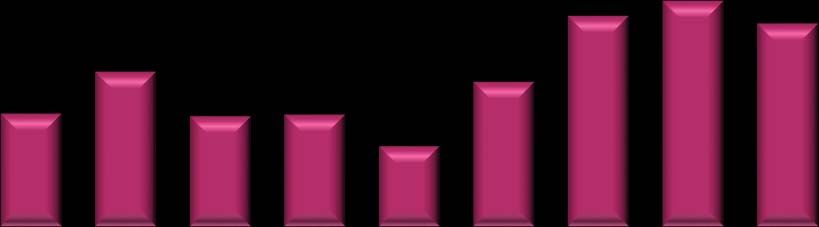

Astute working capital management with superior returns profile Sector: Consumer Durables

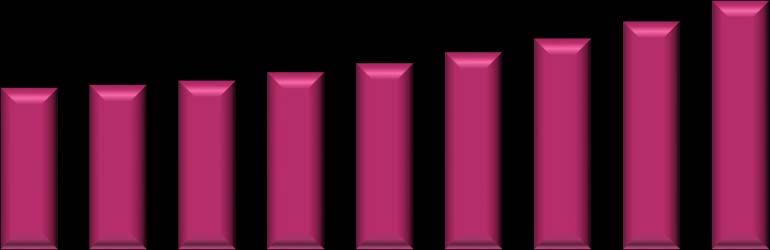

PAT to grow at CAGR of 42.8% Lean working Capital days

150

129 25

98 20

20 19 18

100

61 63 14 13

15

43 47 10 10 10

50 10 7

14 12

5 5

0

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20E FY21E 0

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20E

FY21E

PAT (Rs Cr)

Improving return ratios superior earnings trajectory

New Client addition led to stretching of working capital in FY19 which

50.0

is expected to improve going forward

40.0 Improved collections and efficient inventory management along with

asset light nature of the business will allow Dixon to maintain lean

30.0 working capital days going forward

The recent government announcement of reduction in corporate tax

20.0

rate is expected to bring down effective tax rate positively impacting

10.0 EPS & Bottom line by ~9%.

With superior earnings growth led by strong order book and focus on

0.0 acquiring new clients we expect Dixon to report strong revenue

FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20E FY21E growth.

We expect PAT to grow at CAGR of ~42.8% between FY19-FY21E

RoE (%) Core RoCE (%)

Source: Company, Axis Securities

2916 OCT 2019 Company Report

Dixon Technologies

Valuations Sector: Consumer Durables

P/E band Valuation

6000 We estimate Dixon Technologies to post topline CAGR of 26%

and bottom-line CAGR of 42.8% over FY19-FY21E

4000

We expect EBITDA margins to improve from 4.5% in FY19 to

2000 4.8% in FY21E due to operating leverage

0 ROE is estimated to increase to 24% in FY21E from 18.2% in

FY19, while Core ROCE is expected to increase to 30.4% from

Mar-18

Mar-19

Jul-18

Jul-19

Sep-17

Nov-17

Sep-18

Jan-18

May-18

Nov-18

Jan-19

Sep-19

May-19

27.3% in FY19 driven by improved business performance

Price 5x 10x 15x 20x

We value Dixon Technologies at 32x FY21E EPS as we expect it

to report Revenue/EBITDA/PAT CAGR of 26%/30%/42.8%

12mth fwd P/E (x) respectively over FY19-21E and thus arrive at a price target of

100 Rs 3,649 ( 21% Upside)

80

60

Risk Factors

40

20

Volatility in raw material prices

Competition from domestic and overseas players

0

Forex volatility

Mar-18

Mar-19

Sep-17

Jul-18

Jul-19

Nov-17

Sep-18

Nov-18

Sep-19

Jan-18

Jan-19

May-18

May-19

Customers resorting to higher in-house manufacturing

PE Mean Mean+1Stdev Mean-1Stdev Change in government policies

Source: Company, Axis Securities

3016 OCT 2019 Company Report

Dixon Technologies

Financials (Consolidated) Sector: Consumer Durables

Profit & Loss (Rs Cr) Balance Sheet (Rs Cr)

Y/E March FY18 FY19 FY20E FY21E Y/E March FY18 FY19 FY20E FY21E

Net sales 2,853 2,984 3,868 4,754

Other operating income 0.0 0.0 0.0 0.0 Total assets 363 535 616 731

Total income 2,853 2,984 3,868 4,754 Net Block 179 241 264 293

Cost of goods sold 2,741 2,850 3,687 4,526 CWIP 12.8 18.8 30.0 32.5

Contribution (%) 3.9% 4.5% 4.68% 4.78% Investments 17.2 9.7 9.7 9.7

Advt/Sales/Distrn O/H 0.0 0.0 0.0 0.0

Wkg. cap. (excl cash) 110 229 256 275

Operating Profit 112 135 181 227

Cash / Bank balance 44.1 36.7 56.6 120.6

Other income 4 6 5 7

Misc. Assets 0.0 0.0 0.0 0.0

PBIDT 116 141 186 234

Depreciation 15 22 26 34

Interest & Fin Chg. 13 25 26 24 Capital employed 363 535 616 731

E/o income / (Expense) 0 0 0 0

Equity capital 11.3 11.3 11.3 11.3

Pre-tax profit 88 94 134 177

Tax provision 27 30 36 48 Reserves 304 367 462 589

PAT befor Comprehensive Income 61 63 98 129

Pref. Share Capital 0.0 0.0 0.0 0.0

(-) Minority Interests 0 0 0 0

Minority Interests 0.0 0.0 0.0 0.0

Associates 0 0 0 0

Other Comprehensive Income (0.1) (0.1) 0.0 0.0 Borrowings 44 141 136 123

Adjusted PAT 60.8 63.3 98.0 129.1

Reported PAT 61 63 98 129 Def tax Liabilities 4.1 16.0 6.7 7.9

Source: Company, Axis Securities

3116 OCT 2019 Company Report

Dixon Technologies

Financials (Consolidated) Sector: Consumer Durables

Cash Flow (Rs Cr) Ratio Analysis (%)

Y/E March FY18 FY19E FY20E FY21E Y/E March FY18 FY19E FY20E FY21E

Sales growth 14.2 4.6 29.6 22.9

Sources 83 96 117 158

Cash profit 89 110 150 186 OPM 3.9 4.5 4.7 4.8

Oper. profit growth 22.8 20.4 34.2 25.5

(-) Dividends 0 3 3 3

COGS / Net sales 96.1 95.5 95.3 95.2

Retained earnings 89 107 147 184 Overheads/Net sales 0.0 0.0 0.0 0.0

Depreciation / G. block 7.4 7.5 7.6 8.4

Issue of equity 0.3 0.0 0.0 0.0

Change in Oth. Reserves 55.9 2.7 0.0 0.0 Net wkg.cap / Net sales 0.04 0.07 0.07 0.07

Net sales / Gr block (x) 13.9 10.3 11.5 11.9

Borrowings (2) (2) 5 (3)

Others (60) (12) (36) (22) Core RoCE 34.9 27.4 28.6 30.4

Debt / equity (x) 0.13 0.36 0.28 0.20

Effective tax rate 31.0 32.5 27.0 27.0

Applications 83 96 117 158 RoE 23.7 18.2 22.9 24.0

Payout ratio (Div/NP) 0.0 4.3 2.7 2.1

Capital expenditure 4.5 94.6 60.0 65.0

Investments 28.3 (11.0) 0.0 0.0 EPS (Rs.) 54.8 55.9 86.6 114.0

EPS Growth 26.5 2.1 54.7 31.7

Net current assets 21.5 20.0 36.8 29.3

CEPS (Rs.) 67.1 75.0 109.2 143.7

Change in cash 28.8 (7.4) 19.9 64.0 DPS (Rs.) 0.0 2.0 2.0 2.0

Source: Company, Axis Securities

3216 OCT 2019 Company Report

Dixon Technologies

Disclaimer Sector: Consumer Durables

Disclosures:

The following Disclosures are being made in compliance with the SEBI Research Analyst Regulations 2014 (herein after referred to as the Regulations).

1. Axis Securities Ltd. (ASL) is a SEBI Registered Research Analyst having registration no. INH000000297. ASL, the Research Entity (RE) as defined in the Regulations, is engaged in the business of

providing Stock broking services, Depository participant services & distribution of various financial products. ASL is a subsidiary company of Axis Bank Ltd. Axis Bank Ltd. is a listed public

company and one of India’s largest private sector bank and has its various subsidiaries engaged in businesses of Asset management, NBFC, Merchant Banking, Trusteeship, Venture Capital,

Stock Broking, the details in respect of which are available on www.axisbank.com.

2. ASL is registered with the Securities & Exchange Board of India (SEBI) for its stock broking & Depository participant business activities and with the Association of Mutual Funds of India (AMFI) for

distribution of financial products and also registered with IRDA as a corporate agent for insurance business activity.

3. ASL has no material adverse disciplinary history as on the date of publication of this report.

4. I/We, Hiren Trivedi– CM, Research, MBA (Finance) author/s and the name/s subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect

my/our views about the subject issuer(s) or securities. I/We (Research Analyst) also certify that no part of my/our compensation was, is, or will be directly or indirectly related to the specific

recommendation(s) or view(s) in this report. I/we or my/our relative or ASL does not have any financial interest in the subject company. Also I/we or my/our relative or ASL or its Associates may

have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of the Research Report. Since associates of ASL are

engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/companies mentioned in this

report. I/we or my/our relative or ASL or its associate does not have any material conflict of interest. I/we have not served as director / officer, etc. in the subject company in the last 12-month

period.

Any holding in stock – No

5. ASL has not received any compensation from the subject company in the past twelve months. ASL has not been engaged in market making activity for the subject company.

6. In the last 12-month period ending on the last day of the month immediately preceding the date of publication of this research report, ASL or any of its associates may have:

i. Received compensation for investment banking, merchant banking or stock broking services or for any other services from the subject company of this research report and / or;

ii. Managed or co-managed public offering of the securities from the subject company of this research report and / or;

iii. Received compensation for products or services other than investment banking, merchant banking or stock broking services from the subject company of this research report;

ASL or any of its associates have not received compensation or other benefits from the subject company of this research report or any other third-party in connection with this report.

Term& Conditions:

This report has been prepared by ASL and is meant for sole use by the recipient and not for circulation. The report and information contained herein is strictly confidential and may not be altered in

any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ASL. The report is based on the

facts, figures and information that are considered true, correct, reliable and accurate. The intent of this report is not recommendatory in nature. The information is obtained from publicly available

media or other sources believed to be reliable. Such information has not been independently verified and no guaranty, representation of warranty, express or implied, is made as to its accuracy,

completeness or correctness. All such information and opinions are subject to change without notice. The report is prepared solely for informational purpose and does not constitute an offer document

or solicitation of offer to buy or sell or subscribe for securities or other financial instruments for the clients. Though disseminated to all the customers simultaneously, not all customers may receive this

report at the same time. ASL will not treat recipients as customers by virtue of their receiving this report.

Instead of a company visit, we have done a conference call with the company’s management.

3316 OCT 2019 Company Report

Dixon Technologies

Disclaimer Sector: Consumer Durables

Disclaimer:

Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to the recipient’s specific circumstances.

The securities and strategies discussed and opinions expressed, if any, in this report may not be suitable for all investors, who must make their own investment decisions, based on their own

investment objectives, financial positions and needs of specific recipient.

This report may not be taken in substitution for the exercise of independent judgment by any recipient. Each recipient of this report should make such investigations as it deems necessary to arrive at

an independent evaluation of an investment in the securities of companies referred to in this report (including the merits and risks involved), and should consult its own advisors to determine the merits

and risks of such an investment. Certain transactions, including those involving futures, options and other derivatives as well as non-investment grade securities involve substantial risk and are not

suitable for all investors. ASL, its directors, analysts or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any

action taken on basis of this report, including but not restricted to, fluctuation in the prices of shares and bonds, changes in the currency rates, diminution in the NAVs, reduction in the dividend or

income, etc. Past performance is not necessarily a guide to future performance. Investors are advice necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document

to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and

may be subject to change without notice.

ASL and its affiliated companies, their directors and employees may; (a) from time to time, have long or short position(s) in, and buy or sell the securities of the company(ies) mentioned herein or (b)

be engaged in any other transaction involving such securities or earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) discussed herein or

act as an advisor or investment banker, lender/borrower to such company(ies) or may have any other potential conflict of interests with respect to any recommendation and other related information

and opinions. Each of these entities functions as a separate, distinct and independent of each other. The recipient should take this into account before interpreting this document. The Research reports

are also available & published on AxisDirect website.

ASL and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, the recipients of this report should be aware that ASL

may have a potential conflict of interest that may affect the objectivity of this report. Compensation of Research Analysts is not based on any specific merchant banking, investment banking or

brokerage service transactions. ASL may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither this report nor any copy of it may be taken or transmitted into the United State (to U.S. Persons), Canada, or Japan or distributed, directly or indirectly, in the United States or Canada or

distributed or redistributed in Japan or to any resident thereof. If this report is inadvertently sent or has reached any individual in such country, especially, USA, the same may be ignored and brought

to the attention of the sender. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other

jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject ASL to any registration or licensing requirement within such

jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors.

The Disclosures of Interest Statement incorporated in this document is provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. The

Company reserves the right to make modifications and alternations to this document as may be required from time to time without any prior notice. The views expressed are those of the analyst(s)

and the Company may or may not subscribe to all the views expressed therein.

Copyright in this document vests with Axis Securities Limited.

Axis Securities Limited, Corporate office: Unit No. 2, Phoenix Market City, 15, LBS Road, Near Kamani Junction, Kurla (west), Mumbai-400070, Tel No. – 022 – 4050 8080 / 022 6148 0808,

Regd. off.- Axis House, 8th Floor, Wadia International Centre, Pandurang Budhkar Marg, Worli, Mumbai – 400 025. Compliance Officer: Anand Shaha, Email: compliance.officer@axisdirect.in,

Tel No: 022-42671582. SEBI-Portfolio Manager Reg. No. INP000000654

34You can also read