Customs in the Two Congos: A connected history of colonial taxation in Africa (1885-1914)

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Customs in the Two Congos: A connected history of colonial

taxation in Africa (1885–1914)

Bas De Roo

Journal of Colonialism and Colonial History, Volume 19, Number 1, Spring

2018, (Article)

Published by Johns Hopkins University Press

DOI: https://doi.org/10.1353/cch.2018.0005

For additional information about this article

https://muse.jhu.edu/article/689966

[ This content has been declared free to read by the pubisher during the COVID-19 pandemic. ]Customs in the Two Congos: A connected history of colonial

taxation in Africa (1885–1914)

Bas De Roo

Universität Leipzig

Abstract

Fiscal history is a booming field of research that shines a new light on colonial state

formation, the relationship between the colonizer and the colonized and the political

economy of colonialism in Africa. The fiscal history of colonial Africa has been

interpreted on different levels: local, colonial, imperial and global. This case study on

colonial taxation in the Congo Basin emphasizes the importance of an additional

historical layer. I argue that trans-colonial and trans-imperial connections are essential

to take into account in order to fully understand the fiscal histories of the Congo Free

State and the Belgian Congo, and the French Congo. The two Congos continuously

had to adjust their customs policies to fiscal decision-making across the border.

Introduction

In the past two decades, a growing number of contributions to African colonial history

have demonstrated that a fiscal perspective is essential to understanding colonialism.

Fiscal necessity fundamentally determined colonial state formation and policymaking.

Metropolitan governments were reluctant to spend domestic tax revenue overseas. As

a result, colonial administrations had to collect taxes to finance their activities.

Taxation in its turn required the development of an administration.1 Depending on the

political and economic context colonial administrations taxed specific people, goods or

services. Specific revenue raising strategies required a specific state apparatus to

enforce tax compliance. Taxing international trade, for example, required a customs

service that controlled borders and ports, whereas the taxation of subjects depended

upon a strong colonial presence throughout the colony. Moreover, particular tax

strategies triggered specific spending policies. Most colonial administrations, for

example, tried to boost the performance of those economic sectors that generated

taxable wealth through the development of infrastructure such as railways.2 Taxation

© 2018 Bas De Roo and The Johns Hopkins University Pressalso served the civilizing mission. Paying taxes would transform African subjects into

disciplined, wage-earning, hardworking people.3 From the perspective of the colonized,

colonial rule mainly manifested itself in the form of (forced) labor and cultivation

policies, market intervention on the local and regional level, the imposition of

limitations on personal mobility and the collection of hut, head or poll taxes—activities

that directly and indirectly served colonial revenue raising strategies.4

This article clearly demonstrates how a fiscal perspective adds to our

understanding of colonialism. This rather complex case study on the alignment of

customs tariffs between the French Congo—created in 1882, renamed Middle Congo

in 1903, and incorporated in French Equatorial Africa in 1910—and the Congo Free

State of Leopold II—established in 1885 and annexed by Belgium in 1908—helps us

explain why both colonies implemented extremely violent exploitation systems that

forced Africans to harvest rubber, resulting in the deaths of millions of Africans, a

horrible colonial legacy that France and Belgium still struggle to come to terms with

today.5 As in most African colonies, import and export duties were considered one of

the main sources of colonial revenue on both sides of the Congo and Ubangi Rivers.

Policymakers preferred to tax international trade as this form of taxation required a

relatively small administrative effort. 6 Yet in both Congos the colonial scope to

maximize customs revenue was fundamentally constrained by a deep-rooted conviction

that tariff differences had to be avoided at all cost. Policymakers strongly believed that

higher tariffs on one side of the border stimulated smuggling and the relocation of

commerce to the colony with the lowest tax burden. As a result, customs revenue would

substantially decrease. The fear of the detrimental fiscal and commercial effects of tariff

differences led policymakers in the French Congo and in the Free State and the Belgian

Congo to adjust colonial customs strategies to fiscal decision making across the border.

In combination with other factors such as disappointing commercial outputs,

policymakers’ fear of fiscally fueling smuggling and the relocation of commerce

limited the amount of revenue that could be raised through tariff collection. Because

of disappointing customs receipts France and the Congo Free State had to find

alternative sources of income. Both colonies conceded large parts of their territories to

monopolistic companies and forced Africans to produce rubber, a system that was

characterized by wide-scale abuse against the African population.7

© 2018 Bas De Roo and The Johns Hopkins University PressA growing field of literature has demonstrated that the fiscal aspects of

colonialism are too important to be overlooked. This article adds to the fiscal history of

colonial Africa by demonstrating that it is essential to think outside the traditional

spatial containers of the colonial state and the empire to fully understand colonial

taxation. Some of the existing fiscal histories of colonial Africa have studied taxation

at a scale other than the colonial and the imperial. During the 1990s and 2000s, a group

of scholars has demonstrated that fiscal practice was made and remade locally, through

the interaction between the tax collecting colonial administration and African

communities, mediated by the African elite.8 Moreover, colonial taxation was adapted

to local modes of production and monetary practices. Fiscal practice in turn influenced

the development of local economies. 9 More recent contributions have focused on

colonial taxation from a broader perspective. Some scholars have analyzed how

colonies within the Portuguese, British or French realm tried to collect sufficient tax

revenue to cover the cost of colonization in an attempt to become financially

independent from a metropolitan government that was reluctant to invest in its

colonies. 10 Other publications have compared the fiscal trajectories of African

colonies.11 This second, more recent set of publications does not really expand beyond

the analytical confines of the colony and the empire. However, these authors have

demonstrated that the fiscal fates of African colonies were determined by global

commodity prices to a considerable extent. Economically and hence fiscally, most

colonies depended on the export of a limited set of primary goods. If global demand for

these products faltered, an economic depression could trigger a fiscal crisis.12

Colonial taxation in Africa has been analyzed at a local, colonial, imperial and

global scale. This article focuses on a new layer in the fiscal history of colonial Africa.

Based on reports and correspondence in the archives of the Ministries of Colonies and

Foreign Affairs in France and Belgium I argue that the histories of taxation in the two

Congos can only be fully understood if the close interaction between both colonies is

taken into account.13 Part one of this contribution studies the fiscal race to the bottom

that initially took place between the Free State and the French Congo. Policymakers in

both colonies consecutively lowered customs duties because they feared that exports

would be smuggled across the border—which would force trading companies to

relocate—if the tax burden was higher on their side of the Congo and Ubangi Rivers.

The second and third parts of this article demonstrate that the negotiation and

© 2018 Bas De Roo and The Johns Hopkins University Pressrenegotiation of common tariffs ended the fiscal competition between the two Congos

but required fiscal compromises from both parties. Moreover, the tariff agreement

substantially limited the colonial scope to independently develop customs policies that

best suited the fiscal and commercial needs of the colony, which in the end proved to

be its downfall. This article demonstrates that the fiscal histories of the two Congos

were closely intertwined whether or not their customs departments competed or

cooperated. This important trans-colonial and trans-imperial layer in the fiscal history

of colonialism deserves far more attention from fiscal historians.

The connected history of customs in the two Congos was not exceptional. In

his comparison of British and German fiscal strategies in the Gold Coast and Togoland,

Arthur Knoll briefly mentions a series of customs agreements that were concluded in

West Africa before World War I. In 1887, German Togoland and French Benin

established a customs union. Germany and France deliberately kept import tariffs lower

than in the Gold Coast to divert trade from the British part of the Volta Basin to the

ports of Lomé and Cotonou. In 1890, the French withdrew from the union because it

needed to increase tariffs in Benin to raise more tax revenue. In 1894, the Germans and

the British unified the Volta-borderland in a single customs zone. In 1904, Togoland

backed out of the agreement. The Germans wanted to raise import duties in an attempt

to generate more tax income. Moreover, German policymakers aimed to use their

customs policies to divert trade from the British-controlled Keta port to Lomé.14

This article exclusively studies the interconnected fiscal histories of the two

Congos. This focus reveals only part of the trans-colonial or trans-imperial history of

colonial taxation in the Congo. The French Congo and the Free State and the Belgian

Congo were part of the Congo Free Trade Zone or Bassin Conventionnel du Congo

which encompassed a large part of Central and East Africa. The Berlin Conference

(1885) and the Brussels Convention (1892) substantially limited the colonial

sovereignty to tax international trade in this zone—for example, by imposing maximum

tariffs and prohibiting transit duties or preferential tax policies. The fiscal fates of the

British, French, Portuguese, German and Italian colonies in the Congo Free Trade Zone

and the Free State and Belgian Congo were tied by these two international treaties.

Moreover, some of the signatories of the Berlin Act and the Brussels Convention did

not even possess African colonies. As a signatory of both agreements, the Netherlands

© 2018 Bas De Roo and The Johns Hopkins University Presshad a big influence on the fiscal histories of the French Congo and the Free State and

the Belgian Congo.15 In addition to the multilateral links forged by the Berlin Act and

the Brussels Convention, the customs strategy of each of the two Congos was

determined by the bilateral interaction with other neighbors. Fiscal decision-making in

Angola, for example, affected the customs system in the Free State and vice versa. A

similar connection existed between German Cameroon and the French Congo.

Unfortunately, it is not feasible to provide an all-encompassing oversight of this tangled

web of multilateral and bilateral fiscal interactions in a single article. Therefore, this

contribution focuses on the interconnection between customs in the French Congo and

the Free State and the Belgian Congo.

A Fiscal Race to the Bottom (1886–90)

From the onset tax collection was high on the colonial agenda in the Congo. An

indebted King Leopold could not bear the rising cost of colonization and expected his

colony to become financially self-sufficient as soon as possible. Within weeks after its

creation, the Free State introduced export duties on rubber, ivory and cash crops.

Exports had to be declared in the main ports. Exports from other colonies—transit

goods—could freely be re-exported via the ports of the Free State if a certificate proved

the foreign origin of the products.16 The Berlin Act banned transit duties in the Congo

Free Trade Zone.17 While developing a system to collect export duties, decision makers

realized that the Free State faced a huge problem. The French Congo, the Free State

and Angola had divided the Lower Congo, the coastal region between the Atlantic and

Stanley Pool. 18 Trading firms suddenly found themselves doing business in three

different colonies. 19 The French and the Portuguese had not yet introduced export

duties. As a result, trading posts in Angola, Cabinda and the French Congo could offer

higher prices for African exports than their counterparts in the Congo Free State.

Leopold and his administrators were convinced that the tariff difference stimulated

contraband and reduced customs receipts, the main source of colonial income.20

Initially, the administration of the Free State was predominantly worried about

smuggling to and from Angola. According to the central administration in Brussels and

the Governor General, Congolese products were smuggled to Portuguese trading

centers because the Angolan activities of the trading firms that were active in the Congo

Estuary were not subjected to export duties.21 Contraband was believed to be rampant.

© 2018 Bas De Roo and The Johns Hopkins University PressThe consequences for the colonial treasury appeared devastating. In addition, the Free

State noticed that trading firms abandoned their posts in the Free State. Having posts

in Leopold’s Congo was no longer necessary as the firms bought Congolese exports in

their establishments across the border in Angola. In the eyes of some policymakers,

wide scale smuggling had given rise to a “commercial exodus”.22

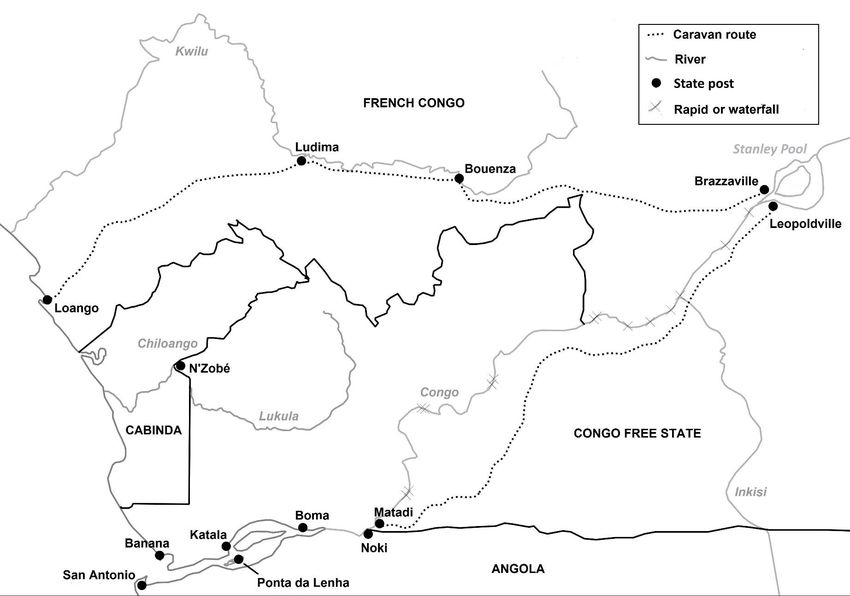

© 2018 Bas De Roo and The Johns Hopkins University PressFigure 1: Trade routes and colonial borders in the lower Congo (1885–90).

© 2018 Bas De Roo and The Johns Hopkins University PressIn 1888, Angola introduced the same export tariffs as the Free State. This decision

eliminated smuggling incentives and ended the panic in Leopold’s administration.23 However,

trading firms such as Daumas, Béraud et Compagnie, the Nieuwe Afrikaansche Handels-

Vennootschap and the Société Anonyme Belge steadily ventured deeper into the Upper

Congo—the region upstream from Stanley Pool. These firms used steamers to develop a

network of trading posts along the main Congolese rivers. As a result, exports could be bought

closer to the producer. By circumventing African middlemen trading firms managed to cut

costs considerably.24 As a result of this evolution, smuggling to the French Congo became the

new issue. Contraband and the related commercial exodus to Angola had alarmed Leopold’s

administration. The Free State took drastic steps to prevent history from repeating itself.25

In December 1887, the French introduced export duties in the Congo—France also

expected its colonial administrations to stand on their own feet. Exports were taxed at 5% ad

valorem.26 The Free State and Angola collected a similar export tax. However, France collected

export duties only in its main posts along the coast such as Loango.27 As a result, the Free State

had no other option but to exempt exports from its part of the Upper Congo at the start of 1888.28

Leopold’s administration explained to France why it had exempted exports from the Upper

Congo. Steamers shipped products from the Congolese interior to Stanley Pool. Porters had to

carry the goods from Stanley Pool to the Congo Estuary as rapids and waterfalls blocked the

river between Leopoldville and Yalala. Smuggling was easy. The French Congo and the Free

State taxed exports only along the coast and not in Stanley Pool, and neither state had the

capacity to control the long border that separated both colonies. Merchants and trading houses

had but to drop anchor at Brazzaville instead of Leopoldville with exports from the Free State

and acquire a certificate of origin that falsely stated that the goods were in fact French. This

would allow a firm to export the goods via the Free State without paying customs duties, as the

Berlin Act exempted transit trade. Likewise, trading houses could move French products to

Leopoldville, falsely claim that the exports came from the Free State so as to obtain a certificate

of origin, which would allow them to export the merchandise via Loango without paying

customs duties.29 Shortly after the decision of Leopold’s administration, France also exempted

exports from their part of the Upper Congo.30

The Free State tried to stop the fiscal race to the bottom which substantially reduced its

customs revenue in a time when every franc counted. Leopold’s administration suggested the

following solution to Paris. If both colonies agreed not to hand out certificates of origin in

© 2018 Bas De Roo and The Johns Hopkins University PressBrazzaville and Leopoldville without collecting customs duties, and taxed all exports without

a certificate in their seaports, smuggling between the two colonies would no longer be

lucrative.31 The French did not agree with this solution. The governor-general of the French

Congo, de Brazza, fiercely opposed the deal for a number of reasons. First of all, a tariff treaty

would constrain the French scope to develop a fiscal strategy that best suited their fiscal and

commercial interests. Secondly, French ivory tariffs were slightly higher than in the Free State.

Taxing ivory in Brazzaville would hence create incentives to smuggle French tusks to

Leopold’s colony. Thirdly, the tariff exemption was to promote the commercial development

of the Congolese interior. Fourthly, trade in the Upper Congo was underdeveloped.

Consequently, export duties would not yield much revenue anyway. 32 However, the main

reason why de Brazza blocked any form of customs-related cooperation with the Free State

concerned the race to Stanley Pool that was taking place at that time, at least in his mind.

Having the fastest and cheapest route to the Congolese interior was a key factor in de

Brazza’s development plans. Frustrated, de Brazza had to sit by and watch the steady

materialization of Leopold’s plans to construct a railway between Matadi and Leopoldville,

while French policymakers and investors did not take to his project to develop the route to

Brazzaville so as to turn this outpost into the main commercial hub for Central African trade—

de Brazza wanted to canalize the Kwilu River and construct a railroad to connect this waterway

to Stanley Pool.33 The French governor-general feared that Leopold’s railway would cripple

the economic future of his colony. Leopoldville would become the linchpin of Congolese trade

instead of Brazzaville. Consequently, trading firms would circumvent the French territories,

eroding the colonial tax base. To save his colony from this gloomy prospect, de Brazza linked

any possible customs agreement—a key interest of the Free State—to shared railway access to

the Upper Congo.34

In ever greater financial trouble, Leopold’s administration in Brussels vainly continued

its attempts to convince French policymakers.35 The fiscal race to the bottom ended only with

the appointment of a new minister of colonies in France.36 Contrary to his predecessor, Pièrre

Tirard did not concur with de Brazza. In his view, common tariffs would put an end to a

situation in which trading houses based their decision to use a particular trade route to the coast

on the differences between the customs policies on the left and right bank of the Congo. In

addition, Tirard believed that a tariff agreement would curb smuggling. Moreover, a customs

deal would allow the French to tax trade upstream from Stanley Pool, which would generate

© 2018 Bas De Roo and The Johns Hopkins University Pressmore customs revenue.37 In 1890, both Congos agreed to tax exports from the Upper Congo in

Brazzaville and Leopoldville, ending the fiscal race to the bottom which had deprived both

cash-strapped colonial states of a considerable amount of customs revenue.38

Negotiating Common Tariffs during the Brussels Convention (1889–92)

By 1889, people in Europe and the United States started calling for action against slavery and

liquor abuse in Africa. The measures of the Berlin Act were considered insufficient to curb the

slave and liquor trade. A new international convention was organized in Brussels to deal with

the matter. Desperately looking for additional ways to finance his colonial project, the by then

heavily indebted Leopold II used this opportunity to convince the signatories of the Berlin Act

to allow import duties in the Congo Free Trade Zone. By then his colony was on the verge of

bankruptcy and desperately sought new sources of revenue. Leopold’s argument was simple:

without import duties colonial states could not fund the fight against the slave and liquor trade.39

After long and arduous talks, the Brussels Convention allowed import duties in the Basin

Conventionnel du Congo below the maximum of 10% ad valorem. The United Kingdom,

Germany and Italy were to determine common import duties in the eastern part of the Congo

Free Trade Zone. France, Portugal and the Free State had to settle on common import tariffs in

the western part of the Basin Conventionnel du Congo.40 The two Congos negotiated common

export tariffs at the same time. The Portuguese did not play a very active role in these tariff

negotiations. Lisbon simply agreed with the temporary and final agreements between France

and the Free State without making any important demands of their own.

Contrary to the previous period, France was eager to reach a tariff agreement with

Leopold.41 The new French secretary of colonies stressed the importance of close cooperation

with the Free State: both colonies produced the same exports that were traded by the same

commercial networks and shared a long border, which was also the main waterway that

connected the coast to the Central African interior.42 However, Paris had a set of clear demands

that had to be met by Brussels. As the years went by, the financial troubles of the Free State

and its royal financier had grown. The Free State failed to collect sufficient tax revenue to

cover the considerable annual costs of discovering, occupying and administering its vast

territory.43 Desperate for more revenue, Leopold’s administration had started trading ivory on

its own accord, which meant it competed with European trading firms.44 In addition, Brussels

had increased ivory tariffs and had introduced a patent tax per kilogram of ivory, a liquor license

and a direct tax based on the amount of buildings and boats a company owned and the number

© 2018 Bas De Roo and The Johns Hopkins University Pressof people it employed.45 Paris insisted that Brussels put an end to its commercial activities and

demanded to reduce the tax burden on trading firms. Leopold had to comply with these demands

if he wanted to conclude an agreement on common import and export tariffs.46

It took more than a year of negotiating before Paris and Brussels reached a consensus.

As his colony already experienced great difficulty in balancing its annual budget Leopold II

refused to abolish taxes or stop trading ivory in the Free State. The French government also

stuck to its guns. Paris was heavily influenced by Daumas, Béraud et Compagnie, a French

firm that had been trading Congolese exports since the 1880s. This firm fiercely lobbied and

campaigned against the fiscal policies and commercial activities of the Free State, arguing that

it was no longer possible for trading companies to export Congolese products at a profit.47 This

impasse was resolved only in 1892. Leopold II offered Médard Béraud a settlement to end the

opposition of his firm. The specifics and the exact timing of the deal are unclear but it involved

the merger between the Société Anonyme Belge and Daumas, Béraud et Compagnie, brokered

by Albert Thys, manager of the Belgian trading firm and close confidant of the king. 48 In

addition, Leopold’s diplomats managed to convince their king to reduce some of the taxes on

trading firms. Leopold did refuse to end the commercial activities of the Free State.49 Portugal

also gave its approval to the tariff agreement between the two Congos and that is how the Lisbon

Protocol was born.

On the April 8, 1892, the Free State, Angola and French Congo agreed to levy the same

export and import duties until 1902. Cash crops were taxed at a rate of 5% ad valorem and ivory

and rubber at rate of 10%. These ad valorem rates were converted to fixed tariffs based on the

prices of the respective products in colonial ports. The three colonies also implemented the

same import duties: 6% ad valorem on regular imports (naval, railway-related, agricultural or

scientific imports were exempted); 10% on salt, guns and ammunition; and 15 francs per

hectoliter of liquor with an alcohol percentage of 50%—depending on the alcohol percentage

liquor imports were taxed higher or lower than the rate of 15 francs.50 The Lisbon Protocol

marked the start of a period of cooperation between the two Congos. Common tariffs reduced

the incentives to smuggle and relocate trading posts, and ended the fiscal race to the bottom.

However, both parties had been forced to make fiscal compromises during a long and bumpy

negotiation process. The next section shows that the French Congo and the Free State had to

make new compromises every time the Lisbon Protocol had to be renegotiated. Moreover, the

© 2018 Bas De Roo and The Johns Hopkins University Pressagreement significantly limited the colonial ability to autonomously develop customs policies.

The fiscal histories of both colonies remained closely intertwined.

French Preconditions for the Renewal of the Lisbon Protocol (1892–1914)

The Lisbon Protocol had to be renewed every so often. Each time, France seized the opportunity

to make a set of demands which gave rise to new negotiations with the Free State and the

Belgian Congo. These talks were difficult at times but both parties always managed to come to

terms. Policymakers realized far too well that breaking the agreement would mean a return to

the past, when the two Congos had the choice between reducing tariffs to match those of its

neighbors—this strategy had fueled a fiscal race to the bottom—or tolerate smuggling. Either

way, customs revenue would decrease considerably.

By 1897, Paris was fed up with de Brazza’s fiscal negligence and replaced him. 51 The

French Congo launched a strategy to boost economic growth and to develop a sound fiscal

system, capable of generating sufficient income to cover colonial expenditure. Customs played

a key role in the new fiscal approach. In 1898, the French introduced many reforms to improve

the performance of the customs system, which had been the only source of revenue till then.52

France wanted to increase import duties and reform customs procedures to tax imports more

effectively. When the Lisbon Protocol was up for renewal in 1902, the Quai d’Orsay demanded

a set of changes. First of all, Paris proposed to change import duties from ad valorem taxes to

fixed tariffs. France wanted to impose fixed import tariffs because the customs department of

the French Congo depended completely on the goodwill of colonial firms to honestly declare

the value of their imports.53 Secondly, the French government wanted to increase import tariffs.

Thirdly, France suggested including Spain and Germany in the tariff union. An agreement with

Rio Muni and Cameroon would curb smuggling across the northern borders of the French

territories in Central Africa.54

Leopold’s administration refused to comply with most French demands. 55 Including

Rio Muni and Cameroon in the tariff union did not benefit the Free State. Neither colony

bordered on its territory. Moreover, additional members would complicate future

negotiations. 56 In addition, Leopold’s diplomats convinced the French Congo to drop the

proposed conversion of ad valorem to fixed import tariffs. Brussels was not yet convinced of

the need to improve the efficiency of its customs system.57 Most importantly, the Free State

was hesitant to raise import tariffs. In addition to customs, Leopold’s fiscal system was based

© 2018 Bas De Roo and The Johns Hopkins University Presson rubber exploitation by large concession companies and in-kind taxation.58 The mass violence

that characterized rubber extraction had become the subject of growing criticism in the German

and British press. Leopold’s administrators hesitated to raise the tax burden for fear of further

damaging the reputation of the Free State, which was already widely regarded as a ruthless

exploitation machine owned by a greedy, monopolistic king.59 In the end, France managed to

convince Leopold that the proposed tax raise did not exceed the maximum rate of the Brussels

Convention.60 The Lisbon Protocol was renewed in 1902 and the common import tariffs in

Angola, the French Congo and the Free State were increased from 6% to 10% ad valorem.61

In 1906, the Lisbon Protocol had to be renewed once more. France demanded to

increase rubber tariffs as global rubber prices were skyrocketing at the time. Paris even

considered withdrawing from the tariff union if their request was not complied with. French

policymakers were still convinced of the necessity of common tariffs in the western part of the

Congo Free Trade Zone.62 However, the French Congo was forced to considerably reform its

fiscal system. Following the example of the Free State, the French had also introduced a

concession system in their Central African territories in 1898. 63 Contrary to the initial

“successes” of rubber exploitation in the Free State, the French system was a fiscal and

economic failure. Moreover, in the French Congo coercive rubber exploitation had also resulted

in widespread abuse, which was heavily criticized by the press. As a result, France was forced

to abolish the concession system and find new sources of income.64 As in 1902, the Free State

was reluctant to comply with the French demand to increase the tariff burden. Brussels was

afraid to further antagonize international public opinion. 65 Moreover, the rubber sector

protested against the tariff increase, which reduced their profits.66 In the end, the Free State did

agree to raise rubber tariffs as the measure simply entailed adjusting the fixed export tariffs to

the price surges on the world market. The Lisbon Protocol was renewed in 1907.67 In addition,

the two Congos and Angola decided to automatically renew the Lisbon Protocol every year.68

By 1909, the enthusiasm about the Lisbon Protocol started to waver on both sides of the

Congo and Ubangi Rivers. The growing international criticism against violent rubber

exploitation and the growing unproductiveness of their concession systems forced the French

and the Belgians to radically rethink their fiscal strategies.69 Both colonies felt increasingly

constrained by the Lisbon Protocol and were tempted to back out of the agreement in order to

develop a customs system that best suited their economic and fiscal needs.70 The French were

particularly keen on withdrawing from the Lisbon Protocol. In addition, Paris feared that the

© 2018 Bas De Roo and The Johns Hopkins University Pressnew Belgian government would be less malleable than Leopold’s administration. In 1910, the

French decided to renegotiate the terms of the Lisbon Protocol one last time. Paris stipulated

three conditions: export duties on cash crops had to be abolished to boost the performance of

these sectors, imported fuels and coal had to be exempted to facilitate the development of a

railway and ad valorem import duties had to be replaced by fixed tariffs to curb rampant fraud—

by the end of the 1900s the French and Belgian Congo discovered that falsely declaring import

value to pay less ad valorem tariffs was a common practice among trading and concession

companies in the two Congos. 71 The Belgian response was positive. However, the Lisbon

Protocol was never renewed.

In 1911, France and Belgium informed Portugal of their decision not to renew the

Lisbon Protocol, thus ending twenty years of common tariffs in the western part of the Congo

Free Trade Zone.72 The French and the Belgians wanted to reform their fiscal systems, but felt

their Portuguese partner held them back. A republican coup had brought down the Portuguese

monarchy at the end of 1910. The revolt put the renewal of the Lisbon Protocol on a back

burner.73 In addition, the Angolan administration had been violating the tariff agreement by

exempting imports in the Cabinda enclave, which stimulated contraband traffic with the coastal

areas of the French and Belgian Congo.74

As the Lisbon Protocol was not renewed, the two Congos could independently reform

their tariff policies. However, both the French and the Belgians were eager to continue their

fruitful cooperation. The Belgian Congo suggested waiting until the summer of 1912 to

implement any customs reforms. France took up this offer. In the end, the tariffs of the Lisbon

Protocol unofficially remained in effect in the two Congos until 1913. That year, France decided

to collect fixed import duties instead of ad valorem tariffs and exempted all exports other than

ivory and rubber to boost the cash crop sector in its Central African territories. In addition,

tariffs on imported fuels and coal were reduced in light of the plans to develop the Congo-

Ocean railway from Brazzaville to Loango. 75 The Belgians implemented the exact same

reforms about one year later.76 One could interpret this series of reforms as a return to the past

when Brussels was compelled to adjust its customs policies to French decision-making.

However, both parties had more or less agreed on these three modifications in 1910. Even after

the Lisbon Protocol was abolished, the two Congos continued to cooperate in the field of

customs to curb contraband and prevent a new fiscal race to the bottom which would

substantially reduce customs revenue either way.

© 2018 Bas De Roo and The Johns Hopkins University PressConclusion

Taxation represented a fundamental aspect of colonial rule in Africa. State formation, colonial

policymaking and the interaction between colonizer and colonized cannot be fully understood

without looking at taxes. This fiscal history of colonial Africa has been analyzed at different

scales: local, colonial, imperial and global. This contribution demonstrates the importance of

an additional, often neglected layer. It shows that the fiscal trajectories of the Free Congo State

and the Belgian Congo and the French Congo—neighboring colonies that belonged to different

empires—were closely connected when it comes to customs, one of the main sources of colonial

revenue in Africa aside from “Native” taxation. In the case of the two Congos, the scope to tax

imports and exports was constrained by the fear that tariff differences would stimulate

smuggling and the relocation of trading firms, which in turn would cause a considerable decline

in customs revenues. The Free State and the French Congo dealt with this issue in two ways.

Initially, the two Congos competed commercially through their customs policies. This strategy

triggered a race to the bottom that resulted in the virtual abolishment of export tariffs on both

sides of the Congo and Ubangi Rivers. This was highly problematic for both cash-strapped

colonies. In a second phase, the two regimes decided to cooperate and agreed on common

export and import tariffs. The Lisbon Protocol took away the incentives to smuggle and ended

the fiscal competition between the Free State and the French Congo. However, the negotiation

and renegotiation of these common tariffs required fiscal compromises from both parties.

Moreover, the Lisbon Protocol considerably restricted the fiscal autonomy of the Free State and

Belgian Congo and the French Congo. This is the reason why France and Belgium decided not

to renew the Protocol in 1911. The two Congos wanted to continue their cooperation in the field

of customs but felt the customs deal with Angola hindered their plans for fiscal reform. Both

colonies continued to cooperate after the Protocol. The fiscal histories of the two Congos

remained closely connected.

For correspondence: deroo.bas@gmail.com. Acknowledgements: I would like to thank the

anonymous reviewers and Geert Castryck for their helpful comments on earlier versions of

this article. The research was funded by the Collaborative Research Centre (SFB) 1199:

“Processes of Spatialization under the Global Condition”.

© 2018 Bas De Roo and The Johns Hopkins University PressNotes

1 Leigh Gardner, Taxing Colonial Africa: The political economy of British imperialism

(Oxford: Oxford University Press, 2012).

2

Ewout Frankema, “Colonial Taxation and Government Spending in British Africa, 1880–

1940: Maximizing revenue or minimizing effort?,” Explorations in Economic History 48/1

(2011): 136–49.

3

Barbara Bush and Josephine Maltby, “Taxation in West Africa: Transforming the colonial

subject into the ‘governable person’.” Critical Perspectives on Accounting 15/1 (2004): 5–34.

4

Sean Redding, Sorcery and Sovereignty. Taxation, Power, and Rebellion in South Africa,

1880–1963 (Athens: Ohio University Press, 2006).

5

Geert Castryck, “Whose History is History? Singularities and dualities of the public debate

on Belgian colonialism,” in Being a Historian: Opportunities and Responsibilities, Past and

Present, edited by Sven Mörsdorf (Pisa: CLIOHRES, 2006), 1–18; Idesbald Goddeeris,

“Colonial Streets and Statues: Postcolonial Belgium in the public space,” Postcolonial Studies

18/4 (2015): 397–409.

6

Hugues Leclercq, “Un mode de mobilisation des ressources: le système fiscal. Le cas du

Congo pendant la période coloniale,” Cahiers Economiques et Sociaux III (1965); Catherine

Coquery-Vidrovitch, Le Congo au temps des grandes compagnies concessionnaires 1898–

1930 (Paris: Mouton & Co, 1972); Ewout Frankema and Marlous van Waijenburg,

“Metropolitan Blueprints of Colonial Taxation? Lessons from fiscal capacity building in

British and French Africa, c. 1888–1940,” The Journal of African History 55/3 (2014): 371–

400.

7

This article does not deal with the concession systems of both colonies. For more

information see: Coquery-Vidrovitch, Le Congo au temps des grandes compagnies

concessionnaires 1898–1930; Aldwin Roes, “Towards a History of Mass Violence in the Etat

Indépendant du Congo, 1885–1908,” South African Historical Journal 62/4 (2010): 634–70.

8

See for example: Nancy Rose Hunt, “Noise over Camouflaged Polygamy, Colonial Morality

Taxation, and a Woman-Naming Crisis in Belgian Africa,” Journal of African History 32/3

(1991): 471–94; Christian John Makgala, “Taxation in the Tribal Areas of the Bechuanaland

Protectorate, 1899–1957,” The Journal of African History 45/2 (2004): 279–303.

9

See for example: Isaac Tarus, “Peasants, Money and Markets: A century of taxation in

Kenya and its global roots,” in Globalization and its discontents, Revisited, edited by J S

Jomo and Khoo Khay Jin (New Delhi: Tulika, 2003).

© 2018 Bas De Roo and The Johns Hopkins University PressMichael W.C. Tuck, “‘The Rupee Disease’: Taxation, authority, and social conditions in early

colonial Uganda,” The International Journal of African Historical Studies 39/2 (2006).

10

See for example: Philip Havik, “Colonial Administration, Public Accounts and Fiscal

Extraction: Policies and revenues in Portuguese Africa (1900–1960),” African Economic

History 41/1 (2013): 159–221; Elise Huillery, “The Black Man's Burden: The cost of

colonization of French West Africa,” The Journal of Economic History 74/1 (2014): 1–38.

11

See for example: Leigh Gardner, “The Fiscal History of the Belgian Congo in Comparative

Perspective,” in Colonial Exploitation and Economic Development: The Belgian Congo and

the Netherlands Indies compared., edited by Ewout Frankema and Frans Buelens (New York:

Routledge, 2013); Frankema and van Waijenburg, “Metropolitan Blueprints of Colonial

Taxation”; Jens Andersson, “Long-term Dynamics of the State in Francophone West Africa:

Fiscal capacity pathways 1850–2010,” Economic History of Developing Regions 32/1 (2016):

37–70.

12

Leigh Gardner, Taxing Colonial Africa: The political economy of British imperialism

(Oxford: Oxford University Press, 2012).

13

People often expect numbers, tables and graphs in a contribution about taxation. This

article does not work with quantitative data. Fiscal policymaking in the two Congos—and in

colonial Africa in general—was not always based on measurable facts. In this case, decision

makers on both sides of the Congo and Ubangi Rivers assumed that tariff differences

stimulated smuggling and commercial relocation and acted accordingly. Whether this was

actually the—quantitatively verifiable—case did not matter. For annual data on taxation and

international trade in the Congo Free State, Belgian Congo and French Congo, see: Coquery-

Vidrovitch, Le Congo au temps des grandes compagnies concessionnaires 1898–1930;

Gardner, “The Fiscal History of the Belgian Congo in Comparative Perspective”; Bas De

Roo, “Taxation in the Congo Free State, an exceptional case?,” Economic History of

Developing Regions 32/2 (2017): 97–126.

14

Arthur Knoll, “Taxation in the Gold Coast Colony and in Togo: A study in early

administration,” in Britain and Germany in Africa: Imperial rivalry and colonial rule, edited

by Prosser Gifford and Alison Smith (New Haven: Yale University Press, 1967).

15

Herman Obdeijn, “The New Africa Trading Company and the Struggle for Import Duties in

the Congo Free State, 1886–1894,” African Economic History, no. 12 (1983): 195–212.

16

Droits de sortie (15–12–1885), BOEIC, 1885, pp. 40–42.

17

Protocoles et Acte Général de la Conférence de Berlin, 1884–1885 (Bremen: Übersee-

Museum, 1885).

© 2018 Bas De Roo and The Johns Hopkins University Press18

Jan Vansina, Paths in the Rainforest (Madison: University of Wisconsin University Press,

1990).

19

Samuel Henry Nelson, Colonialism in the Congo Basin 1880–1940 (Athens: Ohio

University Press, 1994).

20

Bas De Roo, “Taxation in the Congo Free State, An Exceptional Case?”

21

Archives de l’Etat Belge (AEB).Archive Hubert Droogmans (AHD).2 – l’Administrateur

Général des Finances à l’Administrateur-Général au Congo (23-7-1886).

22

AMAEB.AA.Classement Provisoire (CP).2571 – Le Gouverneur Général à

l’Administrateur Général des Finances (8-7-1887) ; AMAEB.AA.CP.2571 – l’Administrateur

Général des Finances au Gouverneur Général (22-8-1887).

23

AEB.AHD.3 – l’Administrateur Général des Finances au Gouverneur Général (29-3-1888).

AEB. Archive Edmond Van Eetvelde (AEVE).71 – Note au Roi (1888).

24

Valérie Gelade, “Les débuts de la navigation à vapeur sur le Haut-Congo (1882–1898),”

Belgisch Tijdschrift voor de Nieuwste Geschiedenis 32/3–4 (2002): 383–418; Jelmer Vos,

“The Kingdom of Kongo and Its Borderlands, 1880–1915,” (PhD diss., University of London,

2005), 120–22.

25

AEB. Archives du Palais Royal (APR). Cabinet du Roi Léopold II (CRL). Développement

Extérieur de la Belgique (DEB). Correspondances Diverses (CD).65 – Janssen au Roi (1890).

26

“Ad valorem” tariffs consist of a proportional levy on the declared value of imported or

exported goods.

27

Bulletin Officiel Administratif du Gabon-Congo (BOAGC), 1887, p. 200, 201 – Décret

portant création des droits à l’exportation au sud de la colonie (22-10-1887); BOAGC, 1887,

p. 243 – Arrêté local promulguant le décret du 22 octobre 1887, portant création de droits de

sortie au Sud (28-11-1887); BOAGC, 1887, pp. 245, 246 – Décision locale. Mise en

application du décret du 22 octobre 1887, portant création de droits de sortie au Sud (29-11-

1887).

28

Bulletin Officiel de l’Etat Indépendant du Congo (BOEIC), 1888, p. 1–4 – Droits de sortie

(19-10-1887).

29

AMAEB.AA. Etat Indépendant du Congo (EIC). Affaires Etrangères (AE).326.458 –

l’Administrateur Général des Affaires Etrangères à la Légation de France en Belgique (19-10-

1888); Archives Nationales d’Outre-Mer (ANOM). Fonds Ministériels (FM). Séries

Géographiques (SG). Afrique (AFR).VI.80a – Note de Van Eetvelde (20-12-1888).

30

BOAGC, 1888, p. 21 – Arrêté local portant dégrèvement des droits d’exportation en faveur

des produits venant de Brazzaville et du Congo (10-1-1888).

© 2018 Bas De Roo and The Johns Hopkins University Press31

AMAEB.AA.EIC.AE.326.458 – l’Administrateur Général des Affaires Etrangères à la

Légation de France en Belgique (19-10-1888); ANOM.FM.SG.AFR.VI.80a – Note de Van

Eetvelde (20-12-1888).

32

ANOM.FM.SG. Gabon Congo (GCOG).VI.15a – Le Commissaire Général du Congo

français au Sous-secrétaire d’Etat au Ministère de la Marine et des Colonies de la France (10-

9-1888).

33

Catherine Coquery-Vidrovitch, “Les idées économiques de Brazza et les premières

tentatives de compagnies de colonisation au Congo Français—1885–1898,” Cahiers d'études

africaines 5/17 (1965): 57–82.

34

ANOM.FM.SG.GCOG.VI.15a – Le Commissaire Général du Congo français au Sous-

secrétaire d’Etat au Ministère de la Marine et des Colonies de la France (11-1-1889).

35

AMAEB.AA.EIC.AE.326.458 – l’Administrateur Général des Affaires Etrangères au

Gouverneur Général (28-5-1889); AMAEB.AA.EIC.AE.326.458 – l’Administrateur Général

des Affaires Etrangères à la Légation de France en Belgique (3-12-1889).

36

François Berge, “Le Sous-secrétariat et les Sous-secrétaires d’État aux Colonies : histoire

de l’émancipation de l’administration coloniale,” Revue française d’histoire d’outre-mer

47/168 (1960): 301–86.

37

ANOM.FM.SG.GCOG.VI.15e – Note du Sous-Secrétaire des Colonies de la France (1889);

ANOM.FM.SG.AFR.VI.80a – Note du Sous-Secrétaire des Colonies de la France (4-12-

1889).

38

AMAEB.AA.EIC.AE.326.458 – l’Administrateur Général des Affaires Etrangères à la

Légation de France en Belgique (21-5-1890).

AEB.APR.CRL.DEB.CD.65 – Janssen au Roi (6-1890?).

39

ANOM.FM.SG.AFR.VI.80a – Proposition relative à l’établissement d’un droit d’entrée

dans le bassin conventionnel du Congo (10-5-1890)

40

Emile Banning. L'acte général de la conférence de Bruxelles devant les chambres

françaises : réflexions d'un homme politique (Saint-Cloud: Imprimerie Belin Frères, 1891).

41

ANOM.FM.SG.AFR.VI.80a – Le Ministre des Affaires Etrangères de la France à La

Légation de France en Belgique (11-11-1890).

42

ANOM.FM.SG.AFR.VI.80a – Le Sous-Secrétaire des Colonies de la France au Ministre

des Affaires Etrangères de la France (26-3-1890).

43

Jean Stengers, “La dette publique de l'Etat Indépendant du Congo,” in La dette publique

aux 18e et 19e siècles: son développement sur le plan local, régional et national (Bruxelles:

Crédit communal de Belgique, 1980).

© 2018 Bas De Roo and The Johns Hopkins University Press44

Ruth Slade, King Leopold's Congo: Aspects of the development of race relations in the

Congo Independent State (London: Oxford University Press, 1962).

45

BOEIC, 1890, p. 113–14 – Impositions directes et personnelles (16-7-1890).

46

AEB.APR.CRL.DEB.CD.65 – Le Ministre des Affaires Etrangères de la France à la

Légation de Belgique en France (13-12-1890).

47

ANOM.FM.SG.AFR.VI.94a –Daumas-Béraud et Compagnie au Sous-Secrétaire des

Colonies de la France (28-1-1891); Médard Béraud. Les intérêts du commerce français au

Congo belge considérés dans leurs rapports avec la convention franco-congolaise du 9

février 1891 (Paris: Imprimerie Chaix, 1891); Nationaal Archief van Nederland (NA).

Buitenlandse Zaken (BZ).A.215 – Adresse de Daumas et Cie à MM. les Sénateurs et MM. les

Députés (25-4-1891).

48

Musée Royal de l’Afrique Central (MRAC). Papiers Albert Thys (PAT).1. Cahier 30. Lettre

n° 40 – Le Roi à Thys (25-4-1891); AEB. Compagnie du Congo pour le Commerce et

l’Industrie (CCCI).483 – Comité permanent. Procés-verbaux des réunions (24–3-1892).

AMAEB.AA. Ministère des Colonies (MC). Statuts (ST) – Statuts du société Daumas-Béraud

et Compagnie (1887–1892); Emile Banning. Mémoires, politiques et diplomatiques :

Comment fut fondé le Congo Belge (Paris-Bruxelles: La Renaissance du livre, 1927), 280–85,

338.

49

AEB.APR.CRL.DEB.CD.106 – Thys au Roi (6-6-1891).

AEB.APR.CRL.DEB.CD.65 – Janssen au Roi (6-1890?).

50

BOEIC, 1892, pp. 111, 112 – Protocol signé à Lisbonne, le 8 avril 1892, entre les

gouvernements de l’Etat Indépendant du Congo, de la France et du Portugal, et réglant les

tarifs des droits d’entrée et de sortie dans la zone occidentale du bassin conventionnel du

Congo (8-4-1892).

51

Catherine Coquery-Vidrovitch, “French Congo and Gabon,” in The Cambridge History of

Africa, edited by J.D. Fage and Roland Oliver (Cambridge: Cambridge University Press,

1985).

52

See: BOACF, 1898; Catherine Coquery-Vidrovitch, Le Congo au temps des grandes

compagnies concessionnaires 1898–1930 (Paris: Ed. de l'Ecole des hautes études en sciences

sociales, 2001).

53

AMAEB.AA.EIC.AE.326.459 – La Légation de France en Belgique au Secrétaire Général

des Affaires Etrangères (4–8-1896).

54

Archives Diplomatiques de la France (AD). Correspondance Politique et Commerciale

(CPC). Afrique Equatorial (AE).1 – Le Ministre des Affaires Etrangères de la France au

© 2018 Bas De Roo and The Johns Hopkins University PressMinistre des Colonies de la France (12-12-1901); AD.CPC.AE.1 – Le Ministre des Colonies

de la France au Ministre des Affaires Etrangères de la France (30-12-1901).

55

AD.CPC.AE.1 – La Légation de France en Belgique au Ministre des Affaires Etrangères de

la France (3-2-1902); AD.CPC.AE.1 – Le Ministre des Colonies de la France au Ministre des

Affaires Etrangères de la France (21-2-1902); AMAEB.AA.CP.617.3 – Le Secrétaire d’Etat à

la Légation de France en Belgique (15-3-1902); AD.CPC.AE.1 – La Légation de France en

Belgique au Ministre des Affaires Etrangères de la France (16-3-1902).

56

AD.CPC.AE.1 – La Légation de France en Belgique au Ministre des Affaires Etrangères de

la France (3-2-1902); AD.CPC.AE.1 – Le Ministre des Colonies de la France au Ministre des

Affaires Etrangères de la France (21-2-1902); AMAEB.AA.CP.617.3 – Note sur la lettre de la

Légation de France en Belgique (1902).

57

AMAEB.AA.EIC.AE.326.459 – Examen de la note de la Légation de France en Belgique

(4-8-1896); AMAEB.AA.EIC.AE.326.459 – La Légation de France en Belgique au Secrétaire

d’Etat (08–02–1897); AD.CPC.AE.1 – La Légation de France en Belgique au Ministre des

Affaires Etrangères de la France (26-3-1902).

58

Leclercq, “Un mode de mobilisation des ressources.”

59

AD.CPC.AE.1 – La Légation de France en Belgique au Ministre des Affaires Etrangères de

la France (26-3-1902); AMAEB.AA.CP.617.3 – Roi Leopold II au Ministre des Affaires

Etrangères de la France (26-6-1902).

60

AD.CPC.AE.1 – La Légation de France en Belgique au Ministre des Affaires Etrangères de

la France (20-4-1902); AD.CPC.AE.1 – La Légation de France en Belgique au Ministre des

Affaires Etrangères de la France (26-4-1902); AD.CPC.AE.1 – La Légation de France en

Belgique au Ministre des Affaires Etrangères de la France (2-5-1902).

61

BOEIC, 1902, pp. 135, 136 – Droits d’entrée (28-6-1902).

62

AD.CPC.AE.3 – Le Ministre des Affaires Etrangères de la France au Ministre des Colonies

de la France (1-3-1907); AD.CPC.AE.3 – Le Ministre des Affaires Etrangères de la France au

Ministre des Colonies de la France (28-3-1907).

63

Coquery-Vidrovitch, Le Congo au temps des grandes compagnies concessionnaires 1898–

1930; Daniël Vangroenweghe, “The ‘Leopold II’ concession system exported to French

Congo with as example the Mpoko Company,” Belgisch Tijdschrift voor de Nieuwste

Geschiedenis 36/3–4 (2006): 323–72.

64

Catherine Coquery-Vidrovitch, Le rapport Brazza. Mission d'enquête du Congo: rapport et

documents (1905–1907) (Neuvy-en-Champagne: Le passager clandestin, 2014).

© 2018 Bas De Roo and The Johns Hopkins University Press65

AMAEB.AA.CP.617.3 – Le Secrétaire Général des Finances au Secrétaire Général des

Affaires Etrangères (10-4-1907); AD.CPC.AE.3 – La Légation de France en Belgique au

Ministre des Affaires Etrangères de la France (20-4-1907); AMAEB.AA.CP.617.3 – Le Vice-

Gouverneur Général au Secrétaire d’Etat (18-9-1907).

66

AMAEB.AA.CP.617.3 – Président du Chambre de Commerce de Boma au Vice-

Gouverneur Général (31-8-1907).

67

BOEIC, 1907, pp. 384, 385 – Droits de sortie (2-7-1907).

68

AD.CPC.AE.3 – La Légation de France en Belgique au Ministre des Affaires Etrangères de

la France (19-6-1906).

69

Robert Harms, “The End of Red Rubber: A reassessment,” The Journal of African History

16/1 (1975): 73–88.

70

AD.CPC.AE.3 – Le Ministre des Colonies de la France au Ministre des Affaires Etrangères

de la France (13-3-1911).

71

AD.CPC.AE.3 – Note de la Direction des affaires politiques et commerciales du Ministère

des Affaires Etrangères de la France (30-8-1909); AMAEB.AA.CP.543.20.1-I.B1 - Rapport

sur le service des douanes de la colonie par le Directeur des Finances a.i. Périer (18-9-1912).

72

AD.CPC.AE.3 – Le Ministre des Affaires Etrangères de la France au Ministre des Affaires

Etrangères (22-3-1911); AD.CPC.AE.3 – La Légation de France en Belgique au Ministre des

Affaires Etrangères de la France (26-3-1911).

73

AD.CPC.AE.3 – La Légation de France en Belgique au Ministre des Affaires Etrangères de

la France (16-1-1911); AD.CPC.AE.3 – Le Ministre des Colonies de la France au Ministre

des Affaires Etrangères de la France (13-3-1911).

74

AMAEB.AA.CP.617.3 – Le Secrétaire Général des Affaires Etrangères au Secrétaire

Général des Finances (21-9-1907).

75

Journal Officiel de l’Afrique Equatoriale Française (JOAEF), 1912, pp. 547–49 – Arrêté

promulguant le décret du 11 octobre 1912, fixant les droits d’entrée à percevoir en A.E.F., à

l’exception des territoires du Gabon, soumis à la loi du 11 janvier 1892, et les droits de sortie

à percevoir dans le l’ensemble des territoires de l’AEF (21-11-1912).

76

Bulletin Officiel du Congo Belge (BOCB), 1913, p. 1023, 1024 – Droits d’entrée sur la

houille, etc. – modifications (11-12-1913); BOCB, 1914, pp. 315–24 – Tarif des douanes. –

Conversion de droits “ad valorem” en droits spécifiques équivalents (2-3-1914); BOCB, 1914,

pp. 774, 775 – Droits de sortie sur les arachides, l’huile de palme, les noix palmistes, le

sésame et le café – suppression (3-4-1914).

© 2018 Bas De Roo and The Johns Hopkins University PressYou can also read