COVID-19 still retreating. Industrials could break to upside in 2022. Entering "Buy November and HODL"- the other side of "Sell in May, go away"

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

This document is being provided publicly in the following form. Please subscribe to FSInsight.com

for more.

Members Area First Word COVID-19 still retreating. Industrials could break to upside in 20

First Word

COVID-19 still retreating. Industrials could break to

upside in 2022. Entering "Buy November and HODL" -

-> the other side of "Sell in May, go away"

November 1

Tom Lee, CFA

HEAD OF RESEARCH

Tickers on this report: $XHB, $IWM, $XLI, $XLF, $XLB, $RCD, $BITO, $GBTC, $BITW

Click HERE to access the FSInsight COVID-19 Daily Chartbook.

We publish on a 4-day a week schedule:

Monday

Tuesday

Wednesday

SKIP THURSDAY

Friday

Halloween 2021… way better than Halloween 2020

In most ways, Halloween is the start of the holiday season in the US. And Halloween

2021 is way better than 2020. While 2021 has many challenges and is a difficult time for

many Americans and global citizens, there has been progress. And for that, I am

thankful.

Over the weekend, COVID-19 case data tends to get spotty (many states do not report). But vaccination data continues to be encouraging: – Daily vaccinations are nearly 2X versus the same Sunday last week – The 7D trend (blue line) is hooking up sharply – More Americans are getting “boosters” and coupled with vaccine mandates = more shots in the arm I generally view this as a positive development. Israel reports zero deaths from COVID-19, and cases down 98% from recent highs Israel COVID-19 cases have fallen sharply in the past few weeks, something that is widely followed and known. The drivers for this presumably reflect the benefit of

boosters, of which ~45% of the population has received the booster shot:

– As of Sunday, Israel reported zero COVID-19 deaths

– That is the first time since July 2021

– Daily cases were only 384

– Daily cases are down 98% from their recent highs

– More importantly, it is a sign that Israel has largely vanquished the Delta surge

Source : https://twitte r.com/bnode sk/status/14 54 57 760504 74 6394 0?s=12

NYC sees daily vaccinations surge +10,000 as deadline nears

Friday was the deadline for NYC city workers to be vaccinated and as the NY Post

reported, this led to a surge in daily vaccinations across NYC. This looks more like a

“one day spike” as the deadline for city workers loomed. And it does not look like this is

a leg up in the rate of vaccination rates for NYC.

Source : https://nypost.com/2021/10/30/nyc-covid-vaccination-rate s-jump-by-10000-in-one -

day/?utm_campaign=iphone_nyp&utm_source =com.slack.slackmdm.share

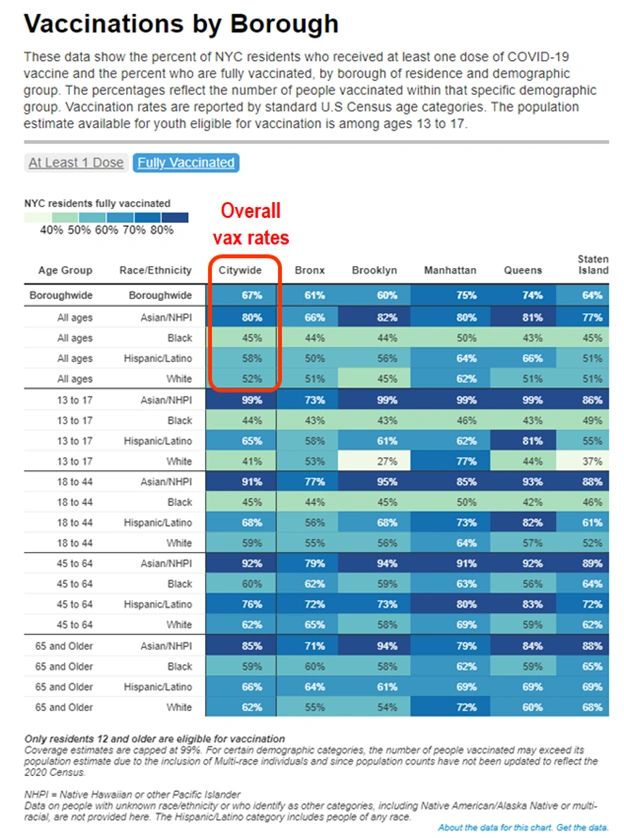

NYC fully vaccinated rate is +67%, which exceeds USA rate of 58%, mainly due to Asians

>80% vax rate

The overall vaccination rate for NYC of 67% is above the USA 58%, and being 900bp above the US is generally positive. The city tracks by minority group and the table below is from the NYC website: – Vax rates for Blacks are 45% – Vax rates for Whites are 52% – Vax rates for Hispanics are 58% Thus, the overall vax rates for these ethnic groups are low and about the same for the US overall. So how is the NYC vax rate above the US? – Asian vax rate is 80% In other words, surprisingly, NYC vax rates are actually not that impressive, compared to the rest of the US.

Source : https://www1.nyc.gov/site /doh/covid/covid-19-data-vaccine s.page NYC will have a tough vax battle on its hands –> 26 FDNY firehouses close Mayor de Blasio claims 91% of city workers are now vaccinated but this does not seem to be 91% across all services. As the NY Post article below highlights, 26 FDNY firehouse companies were closed due to staff shortages. – I don’t have a view of how this resolves – But it is obvious that vaccine mandates are going to lead to staffing shortages

Source : https://nypost.com/2021/10/30/fdny-fire house s-shutte re d-ove r-vaccine -staffing-

shortage s/?utm_campaign=iphone_nyp&utm_source =com.slack.slackmdm.share

This is also happening in Los Angeles, as school workers and teachers are now out of

work. The Los Angeles Times article highlights this:

– 95% of school staff are vaccinated, so this ratio is better than NYC

Source : https://www.latime s.com/california/story/2021-10-29/the -unvaccinate d-fe w-in-l-

a-unifie d

STRATEGY: Bond markets are pricing in more aggressive Fed hikes, but this doesn’t

means stocks need to panic

There was quite a bit of heightened concern across fixed income markets last week. It

looks like bond markets believe the Fed will have to tighten early and aggressively. As

JPMorgan Fixed Income team notes, there have been mixed signals from global central

banks, so this is probably emboldening bond markets to price more aggressive tightening. – the chart from JPMorgan shows government 2-yr (short term) bond yields moved globally – the US saw a relatively more modest move But JPMorgan also notes that they believe poor market liquidity is contributing to these moves in rates. In fact, they show that the 20-yr US bond made a daily move that is sizable relative to the past 5 years. – the last time 20-yr daily move was so sharp – it was March 2021 So you can appreciate, these are sharp moves in the rates world. And that is why many macro investors have become bearish in the past week — arguing that stocks are ignoring moves in rates. The bond market smells trouble before equity markets, so this is a divergence. But there has not been sufficient divergence that would cause us to change our views on stocks.

STRATEGY: Entering “Buy November and HODL” –> the other side of “Sell in May, go away” In our view, the key story arc driving equities is the strengthening global recovery. COVID-19 trends are improving, but with vaccinations and boosters, the improvement in healthcare risk could materially accelerate in 2022. And while the plurality of citizens, even Americans, are resuming their normal lives, this is not the entirety. – the latest Pew Research poll shows 21% to 35% of Americans see COVID-19 as a major threat – the variance is not vaccinated versus vaccinated – This means somewhere between ~20% to 35% of Americans have not resumed normal activities – if even 5% of Americans/global citizens are deferring activity due to COVID-19 risks – and if these improve in 2022 – this would represent substantial incremental demand Thus, the poll data suggests there is still quite a lot of potential pent-up demand.

…Buy in November and HODL This tweet sums it up well by Steve Deppe @SJD10304. As we have said in the past, strong markets stay strong: – S&P 500 is +9.36% from May 5 to Oct 27 – Since 1950, when S&P 500 up >5% from May 5 to Oct 27 – 20 of 20 times, the index is up Oct 27 to following May 5 – Avg gain +12% and median gain +10% So, this is another study showing that equities should remain strong into YE.

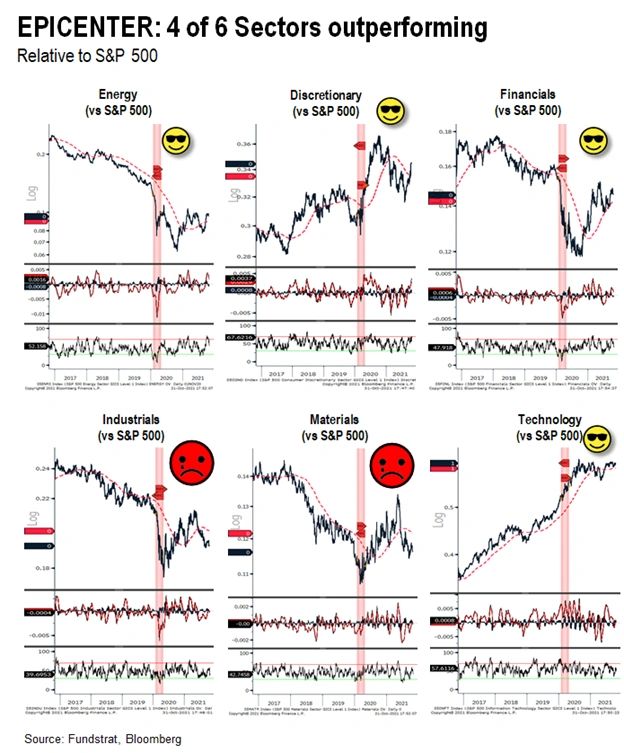

Source : https://twitte r.com/SJD10304 /status/14 54 4 786757 269094 4 1 SECTOR STRATEGY: Epicenter outperforming but laggards are Industrials and Basic Materials S&P 500 leadership in the past month has been fueled by cyclicals aka “Epicenter” stocks as evidenced below. These are stocks which are the most sensitive to improving economic conditions: – pent-up demand, both consumer and corporate

– benefit from “reflationary” pressures

– impacted by supply chain glitches –> some positive, some negative

– global GDP potentially stronger in 2022

So, if one wants to leverage the “Buy in November and HODL” and coupled with the

visibly improving COVID-19 trends (=accelerating growth), Epicenter makes sense.

Source : Bloombe rg

Why are Industrials and Materials lagging? Different reasons

Of the 6 major Epicenter sectors, however, 2 of the 6 are lagging. Take a look below:– Energy, Discretionary, Financials and Technology all showing strong relative strength (vs S&P 500) – lagging: Industrials and Basic Materials Why are these two groups lagging? In our view, there are some fundamental factors explaining their laggardship: – Basic Materials –> rising natural gas + energy costs –> margin squeeze – Cheap natural gas, a key feedstock, was a margin tailwind for Basic Materials – Now that is uncertain – Industrials –> two headwinds – first, global supply chain glitches hurt Industrials most – second, strong USD makes US Industrials less competitive – US Industrials face global competitors, and thus, FX is key – US Industrials are hit hard by supply chain glitches, the same was Consumer Staples suffer

Domestically-oriented Industrials outperforming in 2021… but doesn’t mean this is the case in 2022 There are 15 GICS 4 industries within US Industrials. We have shown these 15 groups below: – 8 of the 15 are outperforming in 2021 – Railroads, Elect. Components, Building products, Waste Services, Research + consulting, Trading cos, Construction + Engineering, Trucking – notice something? – these are mostly domestic industries The strong USD is not a headwind for these companies. Nor is the supply chain glitches

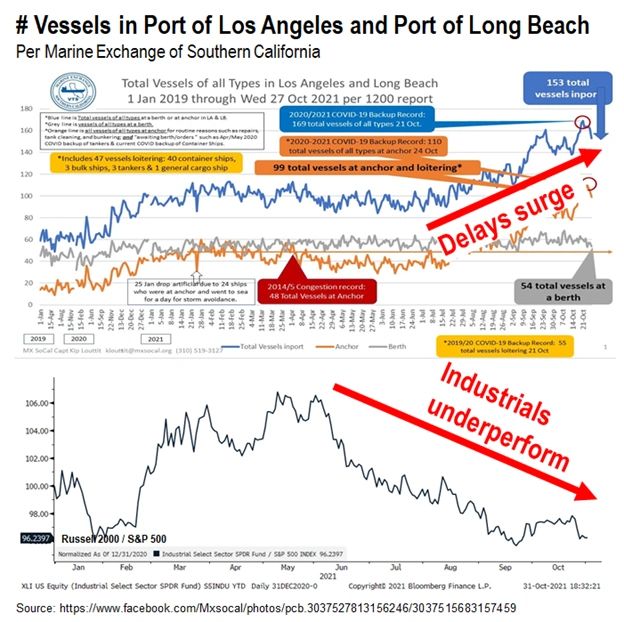

hurting them, In fact, in the case of railroads and trucking, they are able to raise prices. Back ups at LA/LB ports surely seem inversely correlated to Industrials This is purely anecdotal, but see how US Industrials began to sink as the ports became backed up? This seems to speak to a reality. Industrial companies make and deliver goods, using the global supply chain. – so naturally, they are hurt in 2021 by the glitches – conversely, as supply chain glitches ease – Shouldn’t Industrials begin to lead? – That seems intuitive to me Industrials, therefore, might be a “sleeper group” in 2022, as the supply chain glitches ease.

2022 Sales forecasts for Industrials point to acceleration –> supports Industrial outperformance in 2022 For 3Q2021, Industrials have not beaten sales forecasts as shown below on the earnings table. – Only 60% are beating on sales vs 70% for S&P 500 – The overall “surprise” percentage is a miss of -1.1% – The dual impacts of strong USD and supply chain glitches are obvious

But 2022 shows Industrials will be second fastest in sales growth vs #6 in 2021 The comparative sales growth is another reason to favor Industrials into 2022. – Industrials revs 2021 +14.2% below S&P 500 15.2% – Ranks #6 – Industrials revs 2022E +10.9% above S&P 500 +6.8% – Ranks #2 So Industrials are forecast to be the second fastest growing sector in 2022, trailing Consumer Discretionary. If you don’t think this matters, consider what was the fastest growing sector in 2021: – Energy revs growth +55% – Energy stocks YTD gains +52% – Notice something?

BOTTOM LINE: Industrials likely to break to upside in 2022 Bottom line, we think Industrials have been tricky in 2021, because of strong USD and the supply chain glitches. But we think they will show relative strength in 2022. Thus, we still recommend Industrials. Take a look below: – Industrials have been consolidating for 11 months – Similar to Small-caps, which also suffered from supply chain glitches

– Industrials recently moved above the 50D and now in positive trend That said, we still like Energy, Homebuilders, Small-caps and Bitcoin more than Industrials. SECTOR: Energy still favorite sector but also favor homebuilders + small-caps + Epicenter Into YE, our recommended strategies are: – Energy – Homebuilders (Golden 6 months) $XHB – Small-caps $IWM – Epicenter $XLI $XLF $XLB $RCD – Crypto equities $BITO $GBTC $BITW

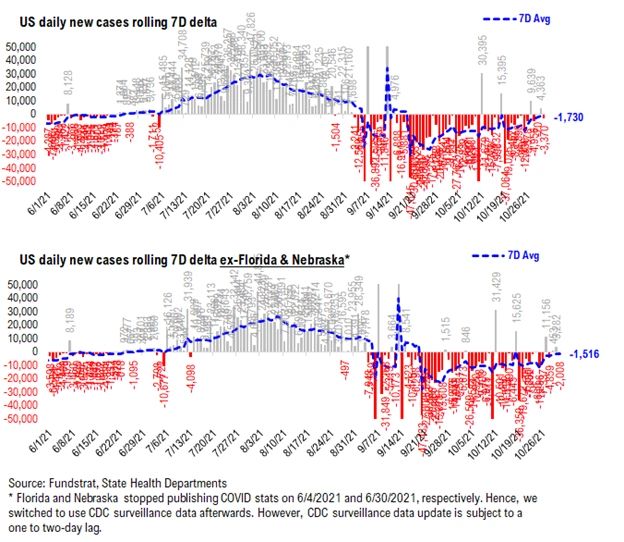

30 Granny Shot Ideas: We performed our quarterly rebalance on 10/25. Full stock list here –> Click here POINT 1: Daily COVID-19 cases 10,009, down -3,370 vs 7D ago… Current Trends — COVID-19 cases: Daily cases 10,009 vs 13,379 7D ago, down -3,370 Daily cases ex-FL&NE 10,009 vs 12,017 7D ago, down -2,008 7D positivity rate 5.0% vs 5.0% 7D ago Hospitalized patients 45,377, down -11.5% vs 7D ago Daily deaths 1,291, down -13.1% vs 7D ago *** Florida and Nebraska stopped publishing daily COVID stats updates on 6/4 and 6/30, respectively. We switched to use CDC surveillance data as the substitute. However,

since CDC surveillance data is subject to a one-to-two day lag, we added a “US ex- FL&NE” in our daily cases and 7D delta sections in order to demonstrate a more comparable COVID development. The latest COVID daily cases came in at 10,009, down -3,370 vs 7D ago. The 7D deltas over the weekend were somewhat flat, and as seen below, the speed of case rollover appears to be slowing. As booster shots are becoming more widely available, the speed of case rollover should increase once again. Rolling 7D delta in daily cases remains negative… The rolling 7D delta remains negative as cases are rolling over.

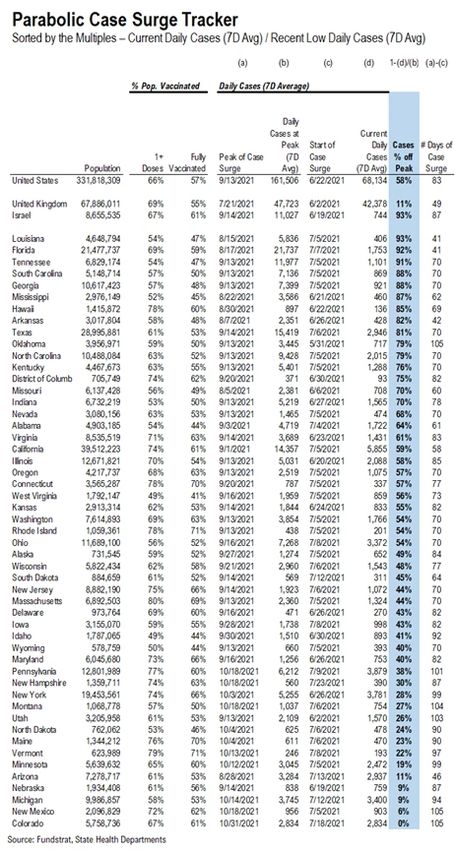

Low vaccinated states seem to have a larger increase in daily cases compared to their recent low… *** We’ve updated the “Parabolic Case Surge Tracker” to measure case % off recent peak as the more recent “delta surge” is rolling over. In the table, we’ve included both the vaccine penetration, case peak information, and the current case trend for 50 US states + DC. The table is sorted by case % off of their recent peak. – The states with higher ranks are the states that have seen a more significant decline in daily cases – We also calculated the number of days during the recent case surge – The US as a whole, UK, and Israel are also shown at the top as a reference

Hospitalizations, deaths, and positivity rates are rolling over amidst case rollover… Below we show the aggregate number of patients hospitalized due to COVID, daily mortality associated with COVID, and the daily positivity rate for COVID. – Net hospitalizations peaked below the Wave 3 peak and are currently rolling over – Daily death peaked slightly above the Wave 2 peak and are currently rolling over – As per the decline in daily cases, the positivity rate is currently rolling over

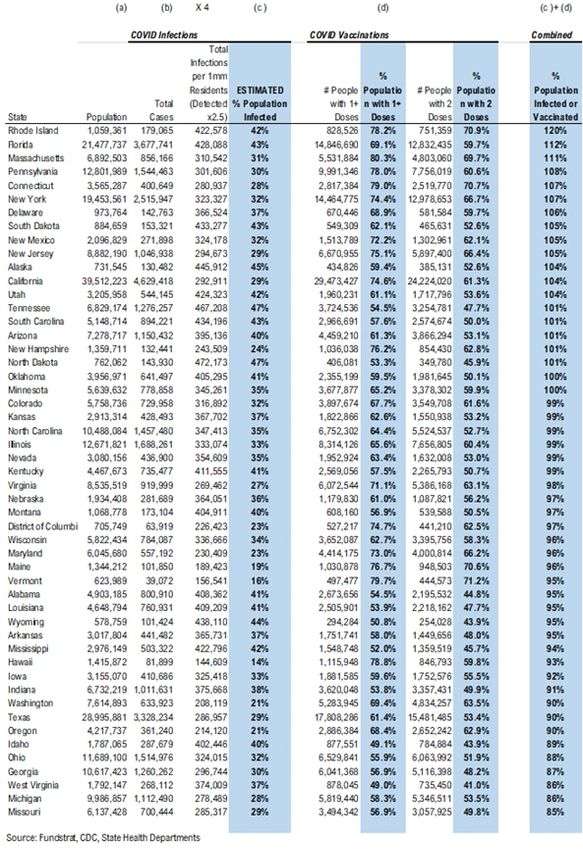

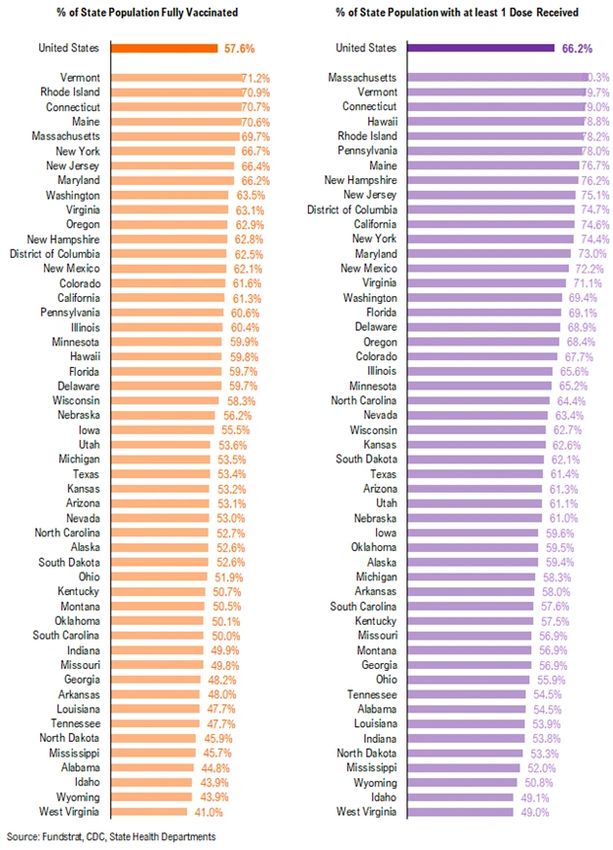

POINT 2: VACCINE: vaccination pace trending up once again… Current Trends — Vaccinations: avg 1.2 million this past week vs 0.8 million last week overall, 57.6% fully vaccinated, 66.2% 1-dose+ received Vaccination frontier update –> all states now near or above 80% combined penetration (vaccines + infections) *** We’ve updated the total detected infections multiplier from 4.0x to 2.5x. The CDC

changed the estimate multiplier because testing has become much better and more prevalent. Below we sorted the states by the combined penetration (vaccinations + infections). The assumption is that a state with higher combined penetration is likely to be closer to herd immunity, and therefore, less likely to see a parabolic surge in daily cases and deaths. Please note that this “combined penetration” metric can be over 100%, as infected people could also be vaccinated (actually recommended by CDC). – Currently, all states are near or above 80% combined penetration – Given the new multiplier. only RI, FL, MA, CT, NM, NY, NJ, IL, CA, PA, DE, SD, KY, UT, OK, ND, NH, AZ, SC, TN, and AK are now above 100% combined penetration (vaccines + infections). Again, this metric can be over 100%, as infected people could also be vaccinated. But 100% combined penetration does not mean that the entire population within each state is either infected or vaccinated

Below is a diffusion chart that shows the % of US states (based on state population) that have reached the combined penetration >60%/70%/80%/90%/100%. As you can see, all states have reached combined infection & vaccination >100% (Reminder: this metric can be over 100%, as infected people could also be vaccinated. But 100% combined penetration does not mean that the entire population within the state is either infected or vaccinated).

There were a total of 1,406,214 doses administered reported on Sunday, up 80% vs. 7D ago. We are seeing the vaccination pace start to pick back up as booster shots are becoming more widely available. Also, the same catalysts remain in place: – Proof of vaccination required by many US cities and venues – Booster shots – Full FDA approval of Pfizer COVID vaccines (hopefully it could help overcome vaccine hesitancy) – Biden’s vaccination plan The daily number of vaccines administered remains the most important metric to track this progress and we will be closely watching the relevant data.

73.9% of the US has seen 1-dose penetration >60%… To better illustrate the actual footprint of the US vaccination effort, we have a time series showing the percent of the US with at least 45%/45%/50% of its residents fully vaccinated, displayed as the orange lines on the chart. Currently, 100% of US states have seen 40% of their residents fully vaccinated. However, when looking at the percentage of the US with at least 45% of its residents fully vaccinated, this figure is 97.3%. And only 81.9% of US (by state population) have seen 50% of its residents fully vaccinated. We have done similarly for residents with at least 1-dose of the vaccination, denoted by the purple lines on the chart. While 98.9% of US states have seen 1 dose penetration >50%, 90.6% of them have seen 1 dose penetration >55% and 73.9% of them have seen 1 dose penetration > 60%.

This is the state by state data below, showing information for individuals with one dose and two doses.

The ratio of vaccinations/ daily confirmed cases has been falling significantly (red line is 7D moving avg). Both the surge in daily cases and decrease in daily vaccines administered contributed to this. – the 7D moving average is about ~20 for the past few days – this means 5 vaccines dosed for every 1 confirmed case

In total, 411 million vaccine doses have been administered across the country. Specifically, 220 million Americans (67% of US population) have received at least 1 dose of the vaccine. And 191 million Americans (58% of US population) are fully vaccinated. POINT 3: Tracking the seasonality of COVID-19 In July, we noted that many states experienced similar case surges in 2021 to the ones they experienced in 2020. As such, along with the introduction of the more transmissible Delta variant, seasonality also appears to play an important role in the recent surge in daily cases, hospitalization, and deaths. Therefore, we think there might be a strong argument that COVID-19 is poised to become a seasonal virus. The possible explanations for the seasonality we observed are:

– Outdoor Temperature: increasing indoor activities in the South vs increasing outdoor activities in the northeast during the Summer – “Air Conditioning” Season: similar to “outdoor temperature”, more “AC” usage might facilitate the spread of the virus indoors If this holds true, seasonal analysis suggests that the Delta spike could roll over by following a similar pattern to 2020. We created this section within our COVID update which tracks and compare the case, hospitalization, and death trends in both 2020 and 2021 at the state level. We grouped states geographically as they tend to trend similarly. CASES It seems as if the main factor contributing to current case trends right now is outdoor temperature. During the Summer, outdoor activities are generally increased in the northern states as the weather becomes nicer. In southern states, on the other hand, it becomes too hot and indoor activities are increased. As such, northern state cases didn’t spike much during Summer 2020 while southern state cases did. Currently, northern state cases are showing a slight spike, especially when compared to Summer 2020. This could be attributed to the introduction of the more transmissible Delta variant and the lifting of restrictions combined with pent up demand for indoor activities.

HOSPITALIZATION Current hospitalizations appear to be similar or less than Summer 2020 rates in most states. This is likely due to increased vaccination rates and the vaccine’s ability to reduce the severity of the virus.

DEATHS Current death rates appear to be scattered compared to 2020 rates. This is likely due to varying vaccination rates in each state. States with higher vaccination rates seem to have lower death rates given the vaccine’s ability to reduce the severity of the virus; states with lower vaccination rates seem to have higher death rates.

Tom Lee, CFA

HEAD OF RESEARCH

Disclosures (show)You can also read