Colliers Radar Report 2018 - Colliers International

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Colliers Radar Report 2018

Melanie Kotschenreuther

Analyst | Research

Executive Summary

melanie.k@colliers.com

Don’t miss the opportunity

Soaring overnight visitor numbers to Hong Kong led to a

boom of new hotels in 2012 and prompted numerous

investors to convert their office properties into hotels.

Hannah Jeong However, many investors missed the optimal time to

Senior Director | Valuation and Advisory invest, as completions reached a peak just as tourism

growth started to decline. This led to a change of heart,

hannah.jeong@colliers.com with several investors ending conversions.

Given the recent recovery in tourism numbers, is it time

for this trend to be reversed? Recently, we have seen

several cases where owners have considered the

Pureanae Jang conversion of their hotel asset into other uses,

particularly to offices. This is natural given the current

Assistant Manager | Valuation and market environment of soaring office prices and rents in

Advisory core locations. However, an increasing number of

pureanae.jang@colliers.com investors are seeking advice about whether it is a good

time for hotel investments in Hong Kong. Existing hotel

owners are also interested in understanding whether

they should hold on to their assets and prepare for

another peak in tourism or exit with fast evolving

Colliers projects that the number of concepts such as co-working spaces or small office /

overnight visitors to Hong Kong will grow home (SOHO) office.

at an annual rate of 7%, reaching 36.6 Our analysis of the current tourism and hotel market

performance shows that the local market is currently

million by 2021, up from 27.9 million in experiencing a revival in fortunes. In H1 2018, Hong

2017. We expect this to be driven mostly Kong’s hotels accommodated more travellers than ever

by millennials and the emerging middle before, this is largely attributable to the influx of mainland

Chinese that are flocking back to the city. Room

class, with medium-tariff hotels in high occupancy and particularly medium-tariff hotel

demand. As a result, our analysis shows performance, especially in the New Territories, has stood

out. Current conversions from hotel to office are

that the demand for medium-tariff hotels therefore not driven by weak hotel market performance,

should outstrip supply by 21.5% in this but rather by the consistently strong office market

segment by 2021, providing investment performance in the CBD and fringe CBD locations due to

a long-term supply shortage combined with high

opportunities in this high return demand. Can hotels, in an improving tourism market,

segment. offer better returns or compete on a level playing field?

Numerous tourism initiatives from the government,

coupled with major upcoming transportation

We want to encourage developers and infrastructure, should strengthen Hong Kong’s position

investors to consider this segment as an international hub, whether for business or leisure.

carefully. This is particularly true in the medium-tariff sector, where

despite new supply, the room availability will likely not be

sufficient to accommodate the rising number of travellers

in this segment. With a shortage supply of medium tariff

hotels in the next couple of years and relatively lower

development and operating costs, we project a solid

performance that leads to good hotel investment

opportunities.

Contents

1. The revival of Hong Kong's tourism

market ............................................... 4

1.1 Hong Kong remains an attractive

destination ............................................. 4

1.2 Entering a new tourism cycle - the

potential upside of the current market .... 5

1.3 Upgrading attractions and infrastructure 7

1.4 Conclusion ............................................ 8

2. Is it still a good market for hotel

investments?.................................... 9

2.1 Busy 2017, an active year for hotel

transactions ........................................... 9

2.2 A cross-sectoral perspective ............... 10

2.3 Securing Plan B................................... 12

3. Adapting to changes in the

hospitality market .......................... 14

4. New opportunities for hotel

investments on the horizon .......... 17

4.1 An imbalanced pipeline ....................... 17

4.2 Hotel investment opportunities ............ 18

3 Are you checking in or checking out? | Colliers International | Radar Report 2018

1. The revival of We believe that Hong Kong has entered a new cycle as

records continued to be set in H1 2018. The arrival of

more than 13.8 million overnight visitors, including 9.2

Hong Kong's million from mainland China in the first six months of the

year alone, set a new record high, as highlighted in

Chart 1.

tourism market Hong Kong is still the number one choice for

Mainland tourists

1.1 Hong Kong remains an With rising spending power and relaxed visa and entry

requirements, mainland Chinese tourists are increasingly

attractive destination venturing further afield when travelling.

Strengthening tourist arrival performance Numerous international markets are benefiting from the

Hong Kong's tourism market is currently experiencing a Chinese travel boom. Despite suffering from a visitor

revival. The upturn follows a two-year decline in visitors decline in 2015 and 2016 Hong Kong has remained the

between 2015 and 2016, which was largely attributable undisputed number one choice for mainland tourists

to the decreasing number of mainland Chinese tourists, given its proximity, accessibility and reputation for

as political protests and anti-mainland sentiment shopping. In 2017, 35% of all mainland Chinese

impacted the relationship between Hong Kong and outbound tourists came to Hong Kong.2 Hong Kong was

mainland China. also the strongest performer amongst its peers regarding

overnight stays from mainland travellers as shown in

Since Q3 2016, however, overnight tourists have been

Chart 2.

flocking back to the city. Due to the mainland's strong

economic development and improved sentiment towards

Hong Kong, the trend of mainland Chinese tourist

arrivals was reversed and regained momentum in 2017,

growing 6.7% YOY. Overall, 2017 marked an all-time

record high in Hong Kong as the city accommodated

more overnight tourists than ever before, with the

majority of visitors coming for vacation and visiting

friends or family.1

Chart 1: Development of Overnight Visitor Arrivals in Hong Kong

Mainland Chinese overnight visitor growth (L) Total overnight visitor growth (L)

Total overnight visitor arrivals (R) Linear

Trend (Total overnight visitor arrivals (R))

50% 10

Overnight visitor arrivals (mil)

40% 8

30% 6

YOY growth

20% 4

10% 2

0% 0

-10% -2

-20% -4

Q4

Q3

Q4

Q3

Q1

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q1

Q2

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q1

Q2

Q4

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q2

Q3

Q1

Q2

Q1

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Source: Hong Kong Tourism Board, Colliers

1 2

Hong Kong Tourism Board China National Tourism Administration

4 Are you checking in or checking out? | Colliers International | Radar Report 2018

Chart 2: Development of Mainland Chinese Visitor Arrivals in Selected Countries/ Territories and YOY growth (2016/2017)

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 H1 2018

20,000,000 6.7%

18,000,000

Number of overnight and total

Mainland Chinese visitors

16,000,000

14,000,000

16.4%

12,000,000

12.0%

10,000,000

(48.3%) 15.4%

8,000,000

6,000,000

48.6%

12.7% 14.7%

4,000,000 7.4%

12.2%

2,000,000

0

Hong Kong* Macau* Thailand South Korea Japan Vietnam Singapore U.S. Malaysia Australia

Notes: *Overnight visitor arrivals figures only for Hong Kong and Macau, YOY growth figure for 2016/2017, U.S. growth figure refers to 2015/2016

Source: Hong Kong Tourism Board, Colliers

Millennials are travel champions 1.2 Entering a new tourism cycle -

Be it spending on shopping, entertainment, or travelling, the potential upside of the current

millennials, being one of the most influential

demographic groups, are setting the tone. Millennials market

focus on ‘lifestyle’ to express their personalities and New momentum for hotel spending

place travel as part of their identities, as such, they travel

more than any previous generation.3 Making up 44% of Traveller habits, especially given the influence of

all hotel guests in Hong Kong (as of 2017), millennials millennials, are shifting more towards lifestyle

and their hotel requirements are shaping the city's experiences, and so has spending. While shopping is

accommodation landscape. still a popular pastime in Hong Kong, the emphasis on

experiences is rising, which is also reflected in hotel

Fuelling the growth of global tourism, millennial travellers spending. After a decline for four consecutive years,

from the mainland have had a significant impact on Hong spending on hotels has regained momentum in 2017.

Kong's hotel industry, accounting for almost a third of all

hotel guests in Hong Kong in 2017.4 There are 415 In 2017, overnight tourists spent on average HKD431

million and 440 million millennials in mainland China and (US54.90) per person per night, an increase of 8.6%

India respectively, making up 47% of the world’s YOY. The jump has been even bigger for tourists from

millennial population.5 Given the sheer size of this the mainland, which on average spent HKD354 (US45.1)

demographic, we expect millennials to remain a key for their hotel room per night, 16.8% more than in 2016.

driver for international traveller growth, like the baby The spending on hotel bills increased across all major

boomers before them, but perhaps with less spending short-haul submarkets.

power. Considering the fact that mainland Chinese visitors

account for on average around 67% of overall overnight

tourists (2013-2017),6 their spending power indicates the

significance of medium-tariff hotels in Hong Kong.

Medium-tariff hotel performance stands out

Consistent with higher numbers of millennial travellers,

we found that hotels in the medium-tariff segment are

faring better than those in higher categories.

3 5

Forbes.com, 8 November 2017 SCMP, 5 August 2018

4 6

Hong Kong Tourism Board Hong Kong Tourism Board

5 Are you checking in or checking out? | Colliers International | Radar Report 2018

Chart 3: Occupancy Performance by Hotel Category Chart 4: RevPAR Performance by Hotel Category

All Hotels High Tariff A Hotels High Tariff A Hotels High Tariff B Hotels

High Tariff B Hotels Medium Tariff Hotels Medium Tariff Hotels

Linear (All Hotels)

Trend

Occupancy (%) RevPAR YOY growth (%)

95% 60%

50%

90%

40%

30%

85%

20%

80% 10%

0%

75% Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2

-10%

2009 2010 2011 2012 2013 2014 2015 2016 20172018

-20%

70%

-30%

65% -40%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 H1

2018 Source: Hong Kong Tourism Board, Colliers

Source: Hong Kong Tourism Board, Colliers

Note: continued in H1 2018 as the RevPAR for medium-tariff

High Tariff A – the highest rated properties based on location,

hotels grew by 18.2% YOY in H1 2018, reaching an

facilities, staff-to-room ratio, achieved room rate and business mix. average of HKD699 (USD89) in this period, while high-

This segment mostly equates to luxury hotels tariff hotels struggled until year-end 2017 and have only

High Tariff B – the second highest, and loosely equates to five- returned to positive territory in H1 2018.

star/upper upscale hotels

Medium Tariff – can be loosely equated to midscale

tariff/midmarket or three/four-star hotels. Strong performance in the New Territories

Tourist Guesthouse – loosely equated to budget hotels and other Despite a slight slowdown in H1 2018, we also found

downmarket options including hostels and the like.

that hotels in the New Territories showed superior

Please refer to the website of the Hong Kong Tourism Board for

more detailed information

occupancy performance compared to other districts in

the past five years, outperforming against the traditional

> Occupancy of Medium Tariff hotels is the highest tourist districts including Yau Ma Tei/Mong Kok and Tsim

Having reached a low in 2015, the recovery of Hong Sha Tsui (“Yau Tsim Mong”), as illustrated in Chart 5.7

Kong's overall hotel occupancy rate has been

Chart 5: Hotel Occupancy in % by District

encouraging. In H1 2018, the average overall occupancy

rate reached 91%, an increase of 3.5 percentage points Central/ Western Wan Chai/ Causeway Bay

Eastern & Southern Hong Kong Tsim Sha Tsui

compared to the same period last year. Yau Ma Tei/ Mong Kok Other Kowloon

New Territories Islands

The gap in occupancy rate between different hotel

Occupancy (%)

categories has been narrowing. However, medium-tariff

hotels have consistently outperformed other categories 100%

over the past ten years and their occupancy reached an

average of 92.0% in H1 2018, compared to 88.5% in the 95%

same period last year as shown in Chart 3.

> Average daily room rates are on an upward trend 90%

We have witnessed a sustained trend of double-digit

85%

RevPAR growth rates at medium-tariff hotels since the

beginning of 2017, as presented in Chart 4. In Q4 2017,

80%

this hotel category reached an all-time record ADR of

HKD840 (USD107.50), fuelled by almost half a million

more overnight visitors from mainland China compared 75%

2005 2010 2011 2012 2013 2014 2015 2016 2017 H1

to the same period in 2016. The strong upward trend has 2018

Source: Hong Kong Tourism Board, Colliers

7

Hong Kong Tourism Board

6 Are you checking in or checking out? | Colliers International | Radar Report 2018

room rates. At the same time these hotels can take

1.3 Upgrading attractions and advantage of unique local neighbourhood cultures, which

infrastructure can particularly attract millennials.

In addition to the current positive performance of the

hotel sector, the government in Q4 2017 brought forward Government initiatives to attract more overnight

a comprehensive tourism development blueprint, which visitors

include numerous short, medium and long-term tourism New tourism products encompassing culture and

initiatives and measures. Planned to be implemented heritage, arts and ecotourism should be offered to attract

over the next five years, the measures are intended to more overnight visitors. Recently, the former Central

boost arrivals and strengthen Hong Kong's position as Police Headquarters in Central reopened as the Tai

an attractive and highly competitive tourism destination.8 Kwun Centre for Heritage and Arts. Victoria Harbour

Transportation infrastructure projects will lead to continues to serve as a focal point for tourists as new

attractions including museums and a theatre in the West

greater connectivity

Kowloon Cultural District, a redesigned Symphony of

Major infrastructure projects currently under construction Lights and a revamped Avenue of Stars will be launched.

such as the Hong Kong-Zhuhai-Macau-Bridge (HZMB), Moreover, efforts to promote large events are increasing

the Hong Kong section of the Express Rail Link (XRL), as more funding has been allocated to position local

the Shatin to Central Link and the construction of a third events such as the Wine and Dine Festival as one of the

runway at Hong Kong International Airport (HKIA) hold signature events in Asia. The proposed Kai Tak Sports

enormous potential for the local economy and the Park, scheduled to open around 2022, features a multi-

hospitality industry. Within the Greater Bay Area (GBA) purpose stadium and has the potential to attract

concept, enhanced connectivity and shortened travel additional large events. Further efforts to attract large-

times should make it more convenient for tourists and scale MICE (“meetings, incentives, conferences, and

business travellers to visit the city. Both, the HZMB9 and exhibitions”) events and cruise passenger development

the XRL10, due to be commissioned in H2 2018, should is also necessary.12

not only attract more visitors from mainland China, but

These initiatives will likely help Hong Kong remain a

should also help position Hong Kong as a gateway city

competitive travel destination internationally, amid fiercer

for travellers who would like to visit the mainland as part

competition like competitive pricing for air plane tickets

of their journey.

and relaxed visa policies.

The new infrastructure is planned to help maintain and

boost the city's competitiveness in the region and

globally. New infrastructure, together with the

development of multiple-destination travel packages in

partnership with GBA and “One Belt, One Road”

countries will probably facilitate the diversification of

source markets as well, making Hong Kong's inbound

tourism more sustainable.11

Given that the new transportation infrastructure should

provide greater accessibility within Hong Kong as

presented in Chart 6, location should be a less crucial

factor for many new hotels and will likely boost hotel

performance in decentralised districts, especially the

New Territories. Furthermore, hotels which are planned

to be in decentralised districts are well-positioned to

capture diverse demand, driven by increasingly

individualistic travellers.

Lower land prices compared to traditional tourism areas

provide investors with more flexibility, allowing for larger

room sizes, a greater variety of hotel facilities and better

8,11,12 10

Tourism Commission Commerce and Economic Commerce and www.expressraillink.hk

Economic Development Bureau (October 2017): Development

Blueprint for Hong Kong’s Tourism Industry

9

Hong Kong Economic Journal, 28 May 2018

7 Are you checking in or checking out? | Colliers International | Radar Report 2018Chart 6: Major Current Transportation Infrastructure Projects in Hong Kong

Source: expressraillink.hk, threerunwaysystem.com, hzmb.hk, mtr-shatincentrallink.hk, hyd.gov.hk,

the Government of the HKSAR press releases, Colliers

1.4 Conclusion This positive outlook holds opportunities for the hotel

investment market. With indications that Hong Kong has

Colliers believes that the availability of upgraded and

entered a new tourism cycle and is heading toward a

new tourist attractions, an increasing comfortability with

new peak of arrivals, both potential investors and hotel

wanderlust, in particular among millennials, together with

an enhanced transportation network should lead to a owners should now prepare to accommodate those

tourists.

continued upturn in overnight visitor numbers which

should strengthen Hong Kong’s position as an attractive

“

leisure and business destination.

Based on these factors, we project the number of

overnight visitors in Hong Kong to grow at an annual rate We project that the

of 7% from 27.88 million in 2017, to 36.6 million by 2021,

with the majority being visitors from the mainland.

number of overnight visitors

Moreover, the World Travel and Tourism Council has a in Hong Kong will likely

positive outlook for Hong Kong, projecting that total

inbound tourism expenditure will rise 51.2% in real prices grow at an annual rate of 7%

by 2028, reaching HKD461.9 billion (USD58.84 billion),

compared to HKD305.5 billion (USD38.92 billion) in

from 27.88 million in 2017, to

2017.13 36.6 million by 2021, with the

majority being visitors from

Mainland China.

“

13

World Travel & Tourism Council (March 2018): Economic impact

2018 Hong Kong, WTTC refers to inbound tourism expenditure as

visitor exports

8 Are you checking in or checking out? | Colliers International | Radar Report 2018compared to 2015 as the increased transactions come

2. Is it still a good from a variety of investors.

Continued interest in the hotel investment market

market for hotel We see continued interest from investors likely to enter

the local hotel market and others who would like to

remain invested.

investments? There are several owner-operators who consider now is

a good time to invest into the hotel market in Hong Kong.

One example is the international medium-tariff hotel

2.1 Busy 2017, an active year for brand Travelodge Hotels Asia. Headquartered in

Singapore, the brand recently entered the market in

hotel transactions 2017. In a franchise agreement with the local Tai Hung

Increased investment appetite for medium tariff Fai Group, the former Hotel Rainbow in Hong Kong’s

hotel assets Jordan neighbourhood was renovated and rebranded as

Travelodge Kowloon.15 The group has since expanded

Coinciding with the recovery of inbound tourism, we and opened Travelodge Central on Hollywood Road in

have seen increased investment activity, reversing the Sheung Wan. According to a 2017 comment from Mr.

downward trend of previous years. Stephen Burt, Chairman of Travelodge Hotels Asia, the

Hong Kong's hotel investment showed renewed launch of the second hotel in Hong Kong reflects the

buoyancy in 2017, with a transaction volume of group’s confidence that, despite the challenges in recent

HKD23.55 billion (USD3 billion), with 17 hotels changing years, Hong Kong will continue to be a major leisure and

ownership. Notably, demand came from both local and business destination. The hotel, formerly Butterfly on

international investors. As displayed in Chart 7, Hollywood, was acquired by Travelodge Asia's parent

investment activity has continued in H1 2018. Four company ICP and Pamfleet (a real estate private equity

hotels with a combined value of HKD3.34 billion fund) in mid-2017 and has since been renovated and

(USD425.9 million) were transacted in H1 2018, rebranded. The hotel benefits from its proximity to the

demonstrating strong market liquidity.14 Sheung Wan MTR station, numerous tourist attractions,

some of the city's largest malls, including ifc mall and

Chart 7: Hong Kong’s Hotel Investment Market The Landmark, as well as offices in the CBD.16

Hotel transaction volume Number of hotel transactions

There have also been numerous investment activities by

Investment volume Number of

(HKD million) transactions local investors. Hong Kong based investor Tang Shing-

20,000 12 bor, for instance, has been on a buying spree. Pushing

18,000 forward the expansion of the hospitality sector of family-

16,000 10

owned Stan Group, the real estate magnate has so far

14,000 8

12,000

invested around HKD10 billion (USD1.27 billion) into

10,000 6 hotels and other assets to be redeveloped into hotels.17

8,000 Focusing on increasing demand from young travellers in

6,000 4

APAC, the group has been rapidly expanding its portfolio

4,000 2

2,000

of new medium-tariff lifestyle hotel brands in Hong Kong.

0 0

While international investment companies have been

Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2

focusing on core districts, some local investors, like Stan

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Group, have been leveraging local market insights and

Source: Real Capital Analytics, Colliers expertise, making use of investment opportunities in

emerging decentralised districts.

While the hotel investment volume in 2015 was jacked

“

up by a few landmark hotel transactions (including the

InterContinental Hotel and Grand Hyatt), 2017 was The majority of hotel transactions

supported by numerous medium-tariff hotel transactions. in 2017 were medium-tariff hotels, “

We believe this represents a healthier investment market

proving investors’ strong appetite in

this segment.

14 16

Real Capital Analytics, August 2018 Travelodge Hotels Asia press release, 7 August 2017

15 17

Travelodge Hotels Asia press release, 16 January 2017 Colliers interview with STAN GROUP

9 Are you checking in or checking out? | Colliers International | Radar Report 20182.2 A cross-sectoral perspective Chart 8: Gross Unit Price by Property sector

Medium-tariff hotels provide an attractive price point Grade A Office Grade B Office

Medium Tariff Hotel Industrial

Why has there been strong investment appetite on Price per sq ft (HKD) on GFA

medium-tariff hotels? 30,000

25,000

Despite the general increase in prices and compression

of yields across all property sectors over the past years, 20,000

medium-tariff hotels still represent an attractive asset

15,000

class compared to other sectors. The strong investment

appetite for medium-tariff hotels can be explained 10,000

through the fact that, with the exception of industrial

5,000

assets (flatted factories), medium-tariff hotels are

offering a lower unit price and a higher yield than Grade 0

A and Grade B office premises, amounting on average to 2010 2011 2012 2013 2014 2015 2016 2017 H1

2018

HKD18,000 (USD2,293) per sq ft in H1 2018, with a yield Source: Colliers, Rating and Valuation Department

we estimate at 3%, as shown in Chart 8 and 9. Although Source: Colliers

the price difference between Grade A office and Grade B Chart 9: Net Yield by Property Sector

offices still has a gap, the yields of the two office sectors Grade A Office Grade B Office

come down to almost the same level. However, medium- Medium Tariff Hotel Industrial

tariff hotels still provide a good buffer on the yield level in Estimated Net Yield (%)

comparison to the office sector, and have higher 6.0%

potential for capital appreciation. 5.5%

5.0%

In Chart 10, we undertook a simple hypothetical analysis 4.5%

to compare profitability between a medium-tariff hotel 4.0%

and a Grade B office in a decentralised district, by using 3.5%

Kowloon East as an example. Based on the assumption

3.0%

of an equal Gross Floor Area (GFA), we compared the

2.5%

current room rate for a medium-tariff hotel (Scenario

2.0%

One) and the Grade B office rent (Scenario Two) in

2010 2011 2012 2013 2014 2015 2016 2017 H1

Kowloon East together with their operating costs. At the 2018

gross operating profit (GOP) level, we found that the Source: Colliers, Rating and Valuation Department

Chart 10: Profitability Scenario: Medium Tariff Hotel versus Grade BSource:

OfficeColliers

in Kowloon East

Source: Colliers

10 Are you checking in or checking out? | Colliers International | Radar Report 2018medium-tariff hotel from Scenario One can generate a Due to the significant share of millennial travellers and

15% higher profit than the Grade B office in Scenario an increasing number of affluent mainland Chinese

Two. The operating expenses from GOP to net operating tourists, we forecast that the market share of occupied

income (NOI) would be different for both, with hotel room nights in medium-tariff hotels will grow from 32%

operation (as shown in Scenario One) tending to have now to nearly 40% in 2021, implying an annual growth

higher expenses, such as hotel operation management rate of about 5.5%.

fees and incentives. Even after adjusting for this factor,

the profitability of the medium-tariff hotel is superior to Based on our analysis, the demand for medium-tariff

the office example. This helps explain the increased hotels should outstrip the number of available rooms in

activity of hotel transactions in the medium-tariff segment this segment by 2021, providing opportunities for

with a focus on decentralised districts since 2017. We investment in this segment. Under these assumptions,

believe this trend should see a continuation, given the demand for hotel rooms in the medium-tariff segment will

superior performance potential. probably exceed supply by 21.5%. We expect this

outcome to boost hotel capital values over the next five

Capital appreciation potential years.

The market share of visitors staying in medium-tariff

hotels in Hong Kong has been increasing continuously

over the last seven years. In 2017, almost one third

(31.6%) of all overnight visitors chose medium-tariff

hotels for their stay in Hong Kong.18 19

Interview with STAN GROUP

STAN GROUP is a local business conglomerate lead by chairman Stan Tang. The group’s hospitality arm

has been growing rapidly in Hong Kong. In an interview with Colliers, Mr. Stan Tang and Mr. Eric Cheng,

Managing Director of Tang's Living Group, shared valuable insights into their successful investment strategy.

Leveraging rising opportunities in the New Territories

The hotel portfolio is mainly located in decentralised areas which are non-traditional tourist spots.

Hotel COZi Oasis and COZi Resort, its newest additions which are due to open soon, are both Mr. Stan Tang,

scheduled to be in the New Territories, in Kwai Chung and Tuen Mun, respectively. Chairman of STAN GROUP

Looking at the real estate mantra "location, location, location" in a new light, STAN GROUP is not fixed on prime city centre

locations. By building up a strong positioning in decentralised areas, particularly in the New Territories, the company can

capture tourists from new cross-border channels and cater to changing traveller demands such as exploring local culture,

heritage, and indulging in outdoor activities. Moreover, the New Territories hold opportunities for hotel investment, as

improved accessibility is transforming these areas into new tourism hubs that are increasingly attracting visitors.

There is no internal benchmark in terms of maximum travel time to major locations when making investment decisions.

However, bustling shopping areas, popular tourist attractions, the CBD, the airport and the new cross-border facilities (HZMB)

are within 30-40 minutes travel time from Stan Group’s hotels.

Making use of existing buildings

Recent land supply by the government has been limited, and the scale and location of the released sites has not been

suitable for developing targeted products. As for finding the right assets, Mr. Tang explained that they are acquiring existing

hotel assets, such as the former Newton Place Hotel, and repurposing them rather than building new ones. Old industrial

buildings in the group’s portfolio benefited from the revitalisation scheme during 2010 and 2016, as they could be repurposed

at nil waiver fee.19

STAN GROUP successfully converted four industrial buildings into hotels. The conversion of existing buildings requires a

lower capital investment, when compared to a new development.

18 19

Hong Kong Tourism Board Note: For explanation of waiver fees, please refer to the Lands

Department, The Government of the Hong Kong SAR

11 Are you checking in or checking out? | Colliers International | Radar Report 20182.3 Securing Plan B One prominent example is the conversion of Hotel

LKF in Central. After closing its doors to hotel guests

Despite rising numbers of tourist arrivals recently, we in July 2017, it has since been refurbished for

have seen several cases, as illustrated in Chart 11, of commercial use, with 14 floors of the revamped LKF

owners considering converting hotels into offices, as well Tower now leased to the flexible workspace operator

as into other concepts. The reasons behind this include: WeWork.20

> Concentration in core locations > Operation costs

We found that many conversion/redevelopment cases For smaller-scale hotels with less than 100 rooms, gross

are in the CBD and fringe CBD districts (e.g. Central, operating costs can be as high as 50% of the overall

Wan Chai, Causeway Bay) where office rents have revenue. In contrast, gross operating costs are less than

recently outperformed the whole market due to an 10% for offices as tenants need to bear management

extremely tight supply. According to Colliers Research, fees and utility charges. Most of the confirmed

in 2017 Grade A office rents increased by 4.1% YOY in conversion cases shown in Chart 11 are smaller than

Central/Admiralty and 2.9% YOY in Wan Chai/Causeway 100 rooms; in these cases, investors faced operational

Bay. The rents have continued their growth path in 1H inefficiency, therefore triggering a conversion from hotel

2018, due to a consistent lack of new office supply, and to other uses.

strong continued demand, particularly from mainland

firms. If the rental income for office properties becomes

significantly larger than the net income from a hotel, it is

feasible to convert to office use.

Chart 11: Confirmed and Potential Hotel Conversions into Other Uses

20

Mingtiandi, 31 August 2017; hongkongbusiness.hk, 23 August 2017

* SOHO office is a combination of a small office and a home office

12 Are you checking in or checking out? | Colliers International | Radar Report 2018> Short term exit plan market when tourist arrivals recovered rapidly in Q2

2010 (B). The fast increase in tourist arrivals in Q2 2010

Reportedly the owners of Hotel Excelsior21 and Crowne

(B) resulted in a large increment of the supply of

Plaza in Causeway Bay have secured approval for a

medium-tariff hotels in Q2 2012 (b) which could be

potential office redevelopment and conversion,

interpreted as oversupply.

respectively, while the buyer of Rosedale Hotel and

Grand View Hotel has submitted a proposal for From Q4 2015 to Q2 2016 (C), overnight tourist arrival

conversion in January 2018.22 These actions might growth slowed. The conversions from hotel into other

suggest that major hotels on Hong Kong Island might uses that we are currently seeing in the market could

fade out, giving the impression that it is time to exit from potentially result in negative growth of hotel stock in

Hong Kong’s hotel market. 2019 in the medium-tariff segment. Given that inbound

tourism is recovering, investors need to carefully review

However, a conversion approval/plan does not

their strategy to avoid missing out on the upcoming

necessarily mean that the option is executed

upside of the market.

immediately. We believe that these applications are part

of a strategy to position assets for sale to capture

interest from both hotel and office buyers. 2.4 Conclusion

Therefore, we conclude that potential conversion/ The active investment market driven by prudent local

redevelopment plans should not be seen as the sole investors and international operators and owners show a

measurement to determine if the performance of the strong appetite for medium-tariff hotels in Hong Kong,

hotel market is unfavourable, nor as an indicator for the which have provided an attractive yield and price point

right time to check out. compared to the office sector in general. A comparison

of the sectoral performance in decentralised locations

Chart 12: Development of Hotel Room Supply by Hotel

Category and Overnight Tourist Arrivals (YOY, in %)

has shown that medium-tariff hotels can provide better

profit than Grade B offices.

High Tariff A Hotels High Tariff B Hotels Furthermore, based on our analysis, the demand for

Medium Tariff Hotels Total overnight tourist arrivals medium-tariff hotels should outstrip the number of

available rooms in this segment by 2021, providing

YOY Growth (%)

greater potential upside on capital value. Particularly

40% medium-tariff hotels in combination with decentralised

B

30%

locations should be able to leverage the potential of the

b upcoming new infrastructure.

20%

The recent news about more conversion and

10% redevelopment plans in the market are giving a false

impression about the right time to exit the local hotel

0%

market. We believe these conversion/redevelopment

-10% C plans are rather limited to CBD and fringe CBD

A a locations, which are driven by the extreme performance

-20% a of office rents in the area and small-scale hotels with

Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2

2008 2009 2010 2011 2012 2013 2014 2015 2016 20172018

less than 100 rooms that have a less efficient operation.

In our opinion, some approved conversion plans simply

Source: Hong Kong Tourism Board, Colliers

improve the owners’ positioning for a potential short-term

exit, while the positive outlook for the local hotel

In the past ten years, we have seen that investors investment market might not necessitate an execution in

tended to respond too quickly to market changes, the near future.

whenever there was a signal of uplift or downturn

particularly in the segment of medium-tariff hotels.

Medium-tariff hotels are relatively easy to convert to

other uses and vice versa due to their building size and

location. As illustrated in Chart 12, when overnight tourist

arrival growth in Hong Kong turned negative in Q2 2009

(A), investors rushed to convert medium-tariff hotels into

other uses, resulting in negative growth in stock (a).

Consequently, they were unable to catch the optimum

21 22

Buildings Department, Monthly Digest February 2015 SCMP, 10 January 2018

13 Are you checking in or checking out? | Colliers International | Radar Report 2018also launched its flexible workspace prototype.26 The

3. Adapting to hotel has carved out an entire floor dedicated to flexible

workspaces27, setting it apart from traditional suit-and-tie

hotels.

changes in the We expect an increasing number of hotel operators and

landlords in Hong Kong to seize the opportunity of

incorporating flexible workspaces, given the relatively

hospitality market low amount of investment needed. However, we believe

that, in the short-term these spaces will likely serve as a

Evolution of concepts to stay ahead gimmick or sweetener to test the demand or boost their

reputation as a trendy hotel as the concept has yet to

of the game prove lucrative amid strong growth in demand. According

to Colliers International’s Flexible Workspace Outlook

As of June 2018, 117 out of a total of 285 hotels in Hong Report 2018, the forecasted YOY increase of flexible

Kong are medium-tariff hotels, a proportion of 41.1%.23 workspace take-up will probably reach 40% in 2018.

Given the prospects of increasing tourist numbers,

> MOJO Nomad: Continuous adaptation to meet

notably millennials, there are a number of mid-tier hotel

ever-changing needs

brands that are keen to enter the local hotel market. At

the same time, established local and international mid- The Hong Kong Government announced in October

tier to upscale hotel brands are expanding their footprints 2009 a set of revitalisation measures to facilitate the

in the city. However, competition in this price segment is redevelopment and wholesale conversion of older

rising. Hence, brands and owners of medium-tariff hotels industrial buildings. These revitalisation measures came

have been exploring creative solutions to stand out from into effect on 1 April 2010, aiming to provide more floor

the crowd and maximise their profits. space for suitable uses to meet Hong Kong’s changing

social and economic needs.

New trends spotted amongst local players

Ovolo Group, a Hong Kong-based developer which owns

> Hotel Jen: Integration of hotel and flexible

and manages a portfolio of hotels in Hong Kong and

workspaces

Australia, has been one of the key players in the market

Flexible workspace concepts are growing rapidly in by repurposing aged industrial buildings. Opened in

APAC. Initially an economical solution for start-ups and 2014, Ovolo Southside in Wong Chuk Hang, Hong

freelancers with a limited budget and a need for space to Kong’s maiden warehouse-to-hotel conversion, is an

grow their businesses, flexible workspaces have become excellent case of the transformation of old industrial

a fundamental part of the local commercial real estate space into a stunning lifestyle hotel. It is bridging the

market, according to Colliers International’s Flexible district’s old industrial roots with its future as a modern

Workspace Outlook Report 2018. Besides small and business hub.28 The redevelopment saved the owner

medium-sized enterprises, multinational corporations are about HKD60 million (USD7.7 million) on change-of-use

now taking up large number of desks for back, mid and premium and another HKD80 million (USD10.3 million)

even front office functions. We are seeing that the fast on construction, compared with a new development.29

growth of this sector is also drawing the interest of hotel Ovolo Aberdeen Harbour, a former office building in

operators and landlords who are evaluating the benefits Aberdeen completed in 1997 which was repurposed as

of incorporating flexible workspace concepts into their serviced apartments and later as a hotel, has recently

hotels.

undergone a refit between August and November 2017

Leading the trend in Asia is Shangri-La Hotels and and debuted as the Mojo Nomad brand.

Resorts, which launched a partnership between the

The brand provides “homstel living”, a combination of

flexible workspace operator theDesk and Hotel Jen, the hotel, home and hostel based on a co-living concept,

newest brand of the Shangri-La Group.24 This was targeting young professionals that are facing an

followed by the successful debut of service inside a five-

unaffordable local housing market.30

star Kerry hotel in Hung Hom by the flexible workspace

operator Kafnu in October 2017, upon the opening of the

hotel.25 A month later, in May 2017, Hotel Jen in Beijing

23 27

Hong Kong Tourism Board SCMP, 12 December 2017

24 28

theDesk press release, 25 July 2017 Ovolo Hotels press release, May 2015

25 29

Kafnu press release, 3 October 2017 SCMP, 15 July 2017

26 30

Hotel Jen press release, 9 May 2017 Ovolo Hotels press release, 21 December 2017

14 Are you checking in or checking out? | Colliers International | Radar Report 2018Learning from global players easy expansion, reduction and reconfiguration and is

thus able to adapt to changing needs.

The trend is not constrained to the local market, but

rather a global one. As the need for differentiation is > Radisson Red: Tapping into an underserved

increasing, we have seen major hotel groups, as well as segment – the four-legged furry travellers

smaller niche companies, introducing more new brands Radisson Hotel Group has also jumped on the

into the market in recent years than any time in modern bandwagon with its Radisson RED brand established in

history. Due to the rise of millennial travellers, it is not Europe since 2014, immersing itself in the underserved

surprising that most of the brands focus on limited- segment of four-legged furry travellers. Radisson RED

service hotels with tech-savvy offerings, design-heavy has a pet-friendly policy at a few of its properties in the

social spaces and budget-conscious room rates. US and Europe.34 As the market of devoted pet owners

Outside Hong Kong, the Medium Tariff brands Aloft continues to expand, the RED hotels with the pet

Hotels by Marriott International, citizenM by Artyzen programme in place has seen a high number of guests

Hospitality Group, and Radisson RED by Radisson Hotel checking in with their pets, receiving enormous positive

Group, have been rapidly gaining recognition as feedback by addressing the demand. Tapping the

innovative hotel brands among a competitive hotel growing market of international travellers with pets,

landscape that has been flooded with new hotel brands coupled with rising pet ownership in Hong Kong, this

offering similar concepts. could be another game-changer. This bold and creative

initiative reinforces the RED brand positioning as an

So how are they differentiating themselves from

evolutionary hotel that is clearly not rule-bound.

other concepts?

> Aloft Hotels: Expertise on conversion and adaptive

reuse of old buildings

One of the major players leading this trend, the Aloft

Hotels brand was first introduced into the US hotel

market in 2005. The brand has quickly gained market

shares by utilising Marriott’s expertise in producing

highly effective and cost-efficient designs for their

buildings. This concept was not only suitable for

purpose-built hotels, but also for the conversion and

adaptive reuse of residential, commercial, industrial and

even heritage buildings. Amongst a total of 138

operating hotels, 22 Aloft Hotels are conversion and

adaptive reuse projects (as of year-end 2017).31

> citizenM: Faster return on investment through

modular construction

citizenM, as a brand focusing on millennial travellers,

can leverage the benefits of off-site construction through

a modular building concept. With this construction

method, the Dutch brand has been able to accelerate

project completion times, mitigate product quality risks

and provide greater cost transparency.32 A successful

case is citizenM Bowery in New York, in Manhattan’s

Lower East Side neighbourhood, where the construction

period was reduced to one year, compared to a

traditional development taking up to three years.33

With consideration to high development costs,

construction delays, traffic congestion and limited

availability of high-potential development sites in Hong

Kong, smart construction could be a solution to these

issues. Moreover, it provides future flexibility, allowing for

31 33

Marriott International: Annual report 2017; Interview with Aloft Hotels Interview with Artyzen Hospitality Group.

32 34

polcommodular.com Radissonred.com

15 Are you checking in or checking out? | Colliers International | Radar Report 2018Interview with WEAVE CO-LIVING

Weave Co-Living is a Hong Kong headquartered collaborative living company founded in 2017

by Mr. Sachin Doshi. Their first project in Hong Kong, Weave on Boundary, is located in Prince Edward

and officially opened on 1st August 2018. We interviewed Mr. Doshi and his Associate, Mr. Bryan Pang,

to understand the company’s motivation to move into this emerging asset class and

create a competitive edge amid rising competition.

Mr. Sachin Doshi,

Nature of opportunity determines asset selection Founder & Chairman of

Weave Co-Living

Weave is making effective use of the number of conversion opportunities in Hong Kong,

as these are often suitable for co-living asset types. Lower investment costs as well as

shorter project completion times compared to new developments are major benefits. While building costs for new developments

range between an estimated HKD4,000 - 4,500 per sq ft (USD510 - 573), we estimate that costs for conversions are

considerably lower, ranging from approximately HKD1,500 - 2,000 (USD191 - 255). Compared to average construction times of

up to three years, Weave could complete an asset conversion within nine months, providing a positive impact on return metrics

by shortening the time from acquisition to cashflow.

Tackling the unaffordability of Hong Kong’s housing market

Weave aims to provide solutions to the two most challenging issues that Hong Kong is currently facing. Foremost, young

professionals find it difficult to find a place that is affordable, yet not too far from the city centre; and secondly, a place that

provides space to mingle and socialise. The company is redefining co-living, providing a convenient yet affordable living space

that makes it easy to meet new people and build a community. Weave has received more than 300 applications for 160 rooms -

a clear signal that the company is targeting a niche sector that has been largely underserved.

A long-term mega trend

Future demand prospects for affordable co-living concepts are looking promising. Given that 31%, 1.24 million of the overall

workforce in Hong Kong are millennials, who are well prepared to join such a living-concept that combines comfort, convenience

and community under one roof, the business model is expected to be highly sustainable without the fear of an oversupply.

16 Are you checking in or checking out? | Colliers International | Radar Report 2018hotel categories is publicly available for the upcoming

4. New hotel pipeline, we estimate that the category shares of

the upcoming hotel room supply through 2021 will be

similar.

opportunities for Chart 13: Hotel Room Supply in Hong Kong

Supply Projection Unclassified Hotel

hotel investments Medium Tariff Hotel

High Tariff A Hotel

High Tariff B Hotel

Total New Supply (YOY growth)

on the horizon Number of hotel room supply

100,000

YOY growth

20%

80,000

15%

We have reviewed the recent historical and current

performance of hotel market and investment 60,000

10%

sentiments in Hong Kong throughout the report. So, 40,000

what is next? What are the assets with potential 5%

20,000

upside? Where to invest? What are the key

considerations for hotel investments? 0 0%

4.1 An imbalanced pipeline

Since 2008, the number of hotels in Hong Kong has Source: Hong Kong Tourism Board, Colliers

almost doubled. Over the same time, the number of hotel The planned supply through 2021 in Chart 14 shows that

rooms increased from 54,804 to 79,944 as of June 2018. the Southern and Eastern districts on Hong Kong Island

Almost a third of all hotel rooms are categorised as should provide the highest number of new hotel rooms

medium-tariff. By 2021, tourists will likely have the on a district level. The new Marriott Hotel at Ocean Park,

choice between 327 hotels in Hong Kong. As shown in if developed as planned, will account for around 25% of

Chart 13, the number of hotel rooms is scheduled to those rooms.

grow to about 90,900 by 2021. 35

On a regional level, new planned supply will concentrate

Although no detailed information on the future share of in Kowloon, with Yau Tsim Mong remaining one of the

Chart 14: Upcoming Hotel Supply by District 2018-2021

Source: Hong Kong Tourism Board, Colliers

35

Hong Kong Tourism Board

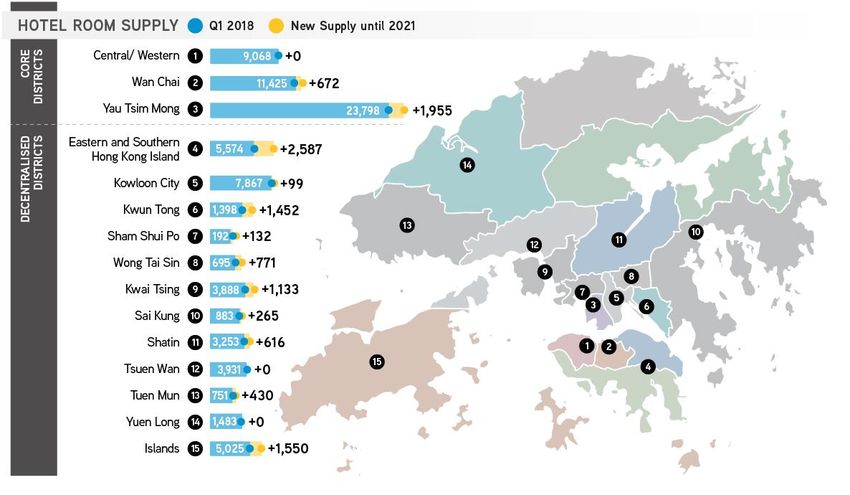

17 Are you checking in or checking out? | Colliers International | Radar Report 2018top districts for new supply. Meanwhile, new hotel supply core districts hold higher potential for hotel investment.

in decentralised districts should remain limited. We have summarised our recommendations, based on

our market findings.

By 2021, we project Kwun Tong’s Grade A office stock to

reach a net floor area of 9.7 million sq ft (901,159 sq m), Potential opportunities – medium-tariff hotels

comparable to the scheduled Grade A office stock of

Medium-tariff hotels have been bouncing back more

Wan Chai and Causeway Bay of 10.8 million sq ft

strongly from the previous downturn, showing robust

(1,003,353 sq m) combined.

RevPAR growth rates since Q3 2016. In our opinion, the

Kwun Tong district is scheduled to double the number of performance of this segment, coupled with the supply

its current hotel room supply by 2021, the district’s shortage of medium-tariff hotels in the next couple of

absolute number of hotel rooms is planned to still be less years, provides good investment opportunities.

than 25% of Wan Chai’s hotel room supply. We believe

Numerous government initiatives, major transportation

the emergence of Kwun Tong as a new business hub

infrastructure, together with a high number of budget

should create demand for hotels. Therefore, the district

conscious millennial travellers, supports the need for

holds potential for hotel investments. Moreover, Tuen

medium priced hotels. The changing requirements of

Mun and Yuen Long in the New Territories, particularly

millennials and their desire for lifestyle entertainment are

targeting mainland Chinese travellers, will likely face a

shaping several industries, including the hotel sector.

shortage of hotel room supply, given the scale of the

Therefore, owners and potential investors should put an

planned and upcoming transportation infrastructure as

emphasis on offering an experience, such as smart

illustrated in Chart 15.

applications of technology, superior and value add

services or special themes to build a competitive edge.

Potential Government land supply (tender) for

hotels

Potential locations – New transportation hubs

Between fiscal years 2013 and 2018, only five parcels of

Apart from shopping – one of Hong Kong’s top activities,

government land were granted for hotel or commercial/

visitors are becoming highly interested in the cultural

hotel mixed-use, including the Murray Building site in

heritage, outdoor activities, and entertainment.

Mid-Levels Central. In the current fiscal year 2018-2019,

Therefore, tourists have been increasingly drawn to

three mixed-use sites with hotel components, all of which

alternative districts outside of established tourism spots.

are located in the Kai Tak area, are scheduled to come

Hong Kong's transportation infrastructure is efficient and

to the market by public tender. 36 New government land

commuting to tourist attractions does not deter visitors,

supply for hotel use has been limited in recent years and

particularly younger ones, from staying in alternative

highly concentrated in the Kai Tak development area.

districts. Moreover, we found prices for the same

Thus, with the exception of Kai Tak, we do not expect

medium-tariff hotels to be around 20% lower in the New

sizable land for decent-sized hotel development to be

Territories compared to Central/Western districts. New

available in the coming years.

interest, together with lower hotel prices have led to

more visitors choosing decentralised districts – a

4.2 Hotel investment opportunities development which Stan Group has clearly picked up on.

Based on our analysis we conclude that the local hotel As shown in Chart 15, we have listed five hot spots

investment market and its prospects provide numerous which we recommend investors pay attention to:

opportunities for new investors to enter the market as

(1) Tuen Mun area,

well as existing owners to hold on to their investment.

(2) Tung Chung area,

Given that Hong Kong's tourism industry has likely

(3) West Kowloon Cultural District area,

entered a new growth cycle, we see few reasons for

(4) Kwun Tong area and

owners of existing hotel assets to exit the market.

(5) Island East area.

Rather, owners should strategically improve their

positioning to be ready for the rising number of inbound The above selections should benefit from the future

tourists. As for the reverse strategy of converting hotel infrastructure developments, new town development and

assets into office use, we believe this does not represent commercial hub expansions. At the same time, we

a trend for the entire market. Given the supply deficit in believe that these hot spots will lack hotel rooms to

the CBD and fringe CBD areas, the conversion to office support demand arising from this new development.

can allow short-term profit maximisation. However, non-

36

Lands Department, The Government of the Hong Kong SAR

18 Are you checking in or checking out? | Colliers International | Radar Report 2018Chart 15: Potential Hot Spots for Hotel Investments

New Town Developments

in Tuen Mun

Kwun Tong (CBD2)

West Kowloon Cultural

District/Express Rail Link

Tung Chung/HZMB/Third Runway

Island East Commercial

Hub Expansion

R O AD / B R I D GE L AN D R E C L AM A TI O N R A I L W AY

Source: Hong Kong Tourism Board, Colliers

19 Are you checking in or checking out? | Colliers International | Radar Report 2018Valuation and Advisory Services:

413 offices in Vincent Cheung

Deputy Managing Director | Hong Kong

+852 2822 0527

69 countries on Vincent.cheung @colliers.com

6 continents Hannah Jeong

Senior Director | Hong Kong

+852 2822 0589

United States: 145 Hannah.jeong @colliers.com

Canada: 28

Latin America: 23

Research Services:

Asia Pacific: 86

Andrew Haskins

EMEA: 131 Executive Director | Asia

+852 2822 0511

Andew.haskins @colliers.com

$2.7

billion in Daniel Shih

annual revenue Senior Director | Hong Kong

+852 2822 0654

2 Daniel.shih @colliers.com

billion square feet

under management

Colliers International | Hong Kong

15,400 Suite 5701, 57F, Central Plaza

professionals 18 Harbour Road | Wanchai | Hong Kong

and staff +852 2828 9888

About Colliers International Group Inc.

Colliers International Group Inc. (NASDAQ & TSX: CIGI) is an industry-leading real estate services

company with a global brand operating in 69 countries and a workforce of more than 12,000 skilled

professionals serving clients in the world’s most important markets. Colliers is the fastest-growing

publicly listed global real estate services company, with 2017 corporate revenues of $2.3 billion ($2.7

billion including affiliates). With an enterprising culture and significant employee ownership and

control, Colliers professionals provide a full range of services to real estate occupiers, owners and

investors worldwide. Services include strategic advice and execution for property sales, leasing and

finance; global corporate solutions; property, facility and project management; workplace solutions;

appraisal, valuation and tax consulting; customized research; and thought leadership consulting.

Colliers professionals think differently, share great ideas and offer thoughtful and innovative advice

that help clients accelerate their success. Colliers has been ranked among the top 100 global

outsourcing firms by the International Association of Outsourcing Professionals for 13 consecutive

years, more than any other real estate services firm. Colliers has also been ranked the number one

property manager in the world by Commercial Property Executive for two years in a row.

For the latest news from Colliers, visit Colliers.com or follow us on Twitter: @Colliers and LinkedIn.

Copyright © 2018 Colliers International.

The information contained herein has been obtained from sources deemed reliable. While every reasonable effort has been

made to ensure its accuracy, we cannot guarantee it. No responsibility is assumed for any inaccuracies. Readers are

encouraged to consult their professional advisors prior to acting on any of the material contained in this report.You can also read