City Fringe Opportunity Area Planning Framework - Consultation Draft December 2014

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

City Fringe

Opportunity Area Planning Framework

Consultation Draft December 2014

Published by Acknowledgements

Greater London Authority Project team

19 December 2014 Matt Christie (Project Manager)

City Fringe

Mark Powney (LB Hackney)

Contact Ben Johnson (LB Islington)

Gemma Hotchkiss/ Chris Horton (LB Tower Hamlets)

CityFringe@london.gov.uk David Jowsey (TfL)

Opportunity Area Planning Framework

Website Project sponsors

http://www.london.gov.uk/mayor- Martin Scholar (GLA) Consultation Draft December 2014

assembly/mayor/publications/planning

Management Group

Public consultation

Fiona Fletcher-Smith (GLA)

December 2014 John Allen (LB hackney)

Karen Sullivan (LB Islington)

Paul Beckett (City Corporation of London)

Copyright Gemma Hotchkiss/ Chris Horton LB Tower Hamlets

1. The maps in this document are

based on Ordnance Survey Material Far more people than it is possible to thank

with the permission of Ordnance individually have contributed to the production of

Survey on behalf of the Controller of this framework. They include major landowners and

Her Majesty’s Stationery Office ©. their planning, transport and design teams; local

Unauthorised reproduction infringes residents and businesses; officers at the Greater

Crown copyright and may lead to London Authority, Transport for London, The City

prosecution or civil proceedings. of London Corporation, Hackney, Islington and

Licence number LA100019726, year Tower Hamlets Councils without whom, neither the

2014. framework nor the progress that has been made so

far would have been possible.

© Crown Copyright and database

right 2014. Ordnance Survey

100032216 GLA

2. The photos in this document are

courtesy of Matt Christie unless

otherwise stated

ii iii

Foreword

Boris Johnson

Mayor of London

I am delighted to introduce the City Fringe Financial businesses and services

Opportunity Area Planning Framework which expanding from the City into the City

has been the product of some excellent joint Fringe and the high values commanded

work between the GLA, TfL and the London by residential development are creating

borough councils of Islington, Hackney and significant challenges. Rising rents, a lack of

Tower Hamlets. space and a dwindling supply of affordable

workspace are problems which, if not

The City Fringe is among London’s most

tackled, threaten the vision of Tech City being

significant areas for economic growth, whilst

the hub driving innovation and growth the

also containing some of the capitals most

UK’s digital economy.

deprived neighbourhoods. The growth of

Tech City represents a massive opportunity This document sets out the strategies that

for London to establish itself as the tech will, alongside the policies of the London

capital of Europe, whilst fuelling a growth boroughs of Islington, Hackney and Tower

engine that can drive regeneration in inner Hamlets, address these issues and allow this

East London. key part of London to fulfil its considerable

economic potential.

I look forward to receiving and reviewing your

comments.

iv v

Executive summary

A changing boundary Affordable space

The City Fringe was historically regarded as the area The key growth conditions that planning can affect in Whilst all of the issues addressed in this document are There are five objectives in order to achieve this vision:

around the north and eastern edges of the City of the City Fringe are: important, the role played by affordable employment

London’s financial district. Despite the Global Financial space and the importance this will have in future are • Ensuring there is the space for continued

Crisis, the core office market has continued to expand • Available, affordable, suitable business particularly recognised. Coworking spaces will continue business growth in City Fringe

and is now well established in these areas. As a result, to play a role, and the market has shown that provision

much of what was considered fringe in the early • stock. of some affordable space within larger developments • Striking the appropriate balance between

2000s is now considered core, whilst the City Fringe can be an attractive lure for prestigious anchor tenant. residential and commercial development

has moved north and east into areas such as Dalston, • Location and “creative vibe”. It is still likely, however, to be a role for securing

Hackney, Haggerston and Whitechapel. affordable space through mechanisms such as section • Supporting the mix of uses that makes City

• Dense, urban, collaborative environment 106 legal agreements. Local policy is recognised as Fringe special

The growth opportunity and the the most appropriate way of responding to local need

• Connectivity. and delivering such space. This document is intended • Identifying the key strategic development sites

threats to address the issue at a strategic level and provide a

• Mix of uses. suitable framework within which the policies of the

The City Fringe Opportunity Area (OA) contains • Connecting the City Fringe

London Boroughs of Islington, Hackney and Tower

significant development capacity in relatively central Hamlets can best secure affordable employment space.

areas and there is particular scope not only to support The availability of plentiful cheap business space Ensuring there is the space for

London’s critical mass of financial and business associated with the industrial legacy of the City

Fringe has been one of the most significant factors Vision continued business growth in City

services but also the diverse cluster of digital-creative

businesses in an expanding “Tech City”. The expansion in the rise of Tech City. Many of the old warehouses Fringe

of Tech City and continued business growth in the and printworks have now either been redeveloped or Tech City UK and London & Partners have

City Fringe OA are recognised by both the Mayor and refurbished and competition for leases is increasing, as complementary remits and together they address Building on the exemption from changes to Permitted

the Prime Minister as strategically important to the the core office market expands and more “traditional” nonplanning issues.The Mayor sets out in this Development rights, the City Fringe OA is broken down

economy of London and the UK. This latest draft City City businesses look to locate in the area. Furthermore document what the planning system can do to assist. into a “Core Growth Area” and a largely residential

Fringe has been re-focused to look at the key areas the increasing attractiveness of the City Fringe and the The vision is: “hinterland”. It is more important to ensure an

that planning can influence, that will maximise this arrival of Crossrail mean that higher value residential ongoing supply of employment floorspace and some

growth and continue to drive the regeneration of East can often outbid and displace lower value office and “Enabling the business cluster to continue to grow as older, affordable stock in the Core Growth Area. It

London. light industrial uses when new sites become available. a mix of large corporations, SMEs, micro businesses is, however, accepted that there is a finite supply of

Over time this could contribute to the weakening and and start-ups and become the innovation hub driving older stock and that affordable employment floorspace

The City Fringe is increasingly the home of new and dissipation of the digital-creative cluster. This would growth in London and the UK’s the digital economy, must come forward in new developments especially

emerging sectors of the economy with particular be detrimental to London’s wider knowledge economy while delivering housing and other supporting uses where there will be demolition of existing affordable

clustering and accommodation requirements. This and the ambition to create a world leading digital- such as retail and leisure. ” workspace. Developers should engage potential end-

hasn’t happened randomly, and there are particular creative business hub based around Tech City. The users using the London Open Workspace website, at an

conditions that have encouraged clustering in the City parallel growth in other sectors fuelled by the presence early stage to inform design and provide assurance that

Fringe, as they have in other places such as New York, of new residents, workers and visitors with relatively the space will be managed post construction and not

San Francisco and Berlin. Some of these conditions high incomes is also subsequently threatened. converted to another use.

are related to planning, whereas others (such as those

associated with wider economic structural changes and

cycles) are not.

vi vii

Striking the appropriate balance

between residential and commercial

development

The stock of employment floorspace, and the future go beyond the minimum standards of cycle parking

pattern of demand is unlikely to be even across the provision in the London Plan. The Super Connected

City Fringe as Tech City expands. Current and future Cities programme is signposted as a way stimulating

demand mapping has been commissioned to inform demand and encouraging businesses to apply for

a map that further breaks the City Fringe OA down vouchers to improve their Broadband connectivity.

into “Inner core”, “outer core” and “hinterland” areas.

This broadly sets out the relative levels of employment The areas containing the key development

and residential use that should come forward on opportunities are identified. It is these areas where

sites in the respective parts of the OA. It is not most change will occur and into which Tech City is

prescriptive, but is intended as a starting point for pre- already expanding. These areas also face significant

application discussions and the assessment of planning urban design challenges such as severance, poor public

applications. realm, poor structure and legibility and lack of public

open space. Key Strategic Principles set out how these

Supporting the mix of uses that issues can be addressed and which sites present the

opportunity to do so. They also set out how these

makes City Fringe special areas can be better connected to one another and

become a more integrated part of the wider City

The pressure for new development should not erode Fringe.

the qualities that draw businesses and residents to

the City Fringe attractive in the first place. Ongoing

provision of the mix of supporting uses such as leisure, Implementation

retail and night-time economy needs to be managed

in a way that doesn’t compromise the character of the The plan will be delivered in partnership with the

area and ensures “critical mass” at key locations such London boroughs of Islington, Hackney and Tower

as special policy areas, CAZ frontages and the town Hamlets and the implementation chapter sets out how

centre network. Support is given to small independent this will be achieved. Mechanisms for cooperation,

traders and temporary “pop-up” uses that provide funding and monitoring and review of the plan are

vibrancy and activity as well as provide valuable considered in detail.

opportunities for new businesses.

A transport review has been undertaken by TfL, and

a Property Market Appraisal by URS, JLL and Hatton

Identifying the key strategic Real Estate was commissioned in order to provide a

development sites and Connecting supportive evidence base for the OAPF.

the City Fringe

The various transport proposals are brought together

in one integrated strategy. This provides clarity on how

the area will be increasingly well connected within

itself and with wider London, particularly as Crossrail

and Crossrail 2 develop. Levels of walking and cycling

are already high and can go even higher as more

people live and work in the OA. Developers should

viii ix

Table of contents

1. Introduction and background 4. Supporting the right mix

2 Purpose of the guidance 32 Mix of uses- lifestyle choice and informal

4 City Fringe OA networking

6 Tech City 34 Strategy 4: Supporting the mix of uses that

12 Vision and objectives makes City Fringe special

12 Strategy 1: The City Fringe as a planning 35 Strategy 5: Supporting pop-ups and temporary

boundary usesg pop-ups

and temporary uses

2. Ensuring space for business growth 5. Connecting the City Fringe

16 The mix of business in the City Fringe 38 Context

16 Analysis of the property market 40 Tackling poor public realm and connectivity

18 Types of space being used 42 Junctions and severance: A summary

19 Supply of space 44 Promoting walking and cycling

19 Demand forecasts and comparison with 47 Strategy 6: Cycle parking

supply 50 Wider connectivity

20 Strategy 2: Protecting a quantum of 52 Super connected cities

floorspace needed for growth 56 Key strategic sites and strategic design

principles

3. Striking the balance

6. Implementation

26 Viability and competition with residential

development 88 Delivering the vision in partnership

28 Strategy 3: Striking the balance between 89 Infrastructure, funding and investment sources

employment and residential 90 LIPS/ Other Transport funding

90 Crossrail complimentary measures funding

90 Prudential borrowing

90 Business rate retention

90 GLAs regeneration funds

90 GLA housing zone

90 New Homes Bonus

90 LIF

91 European Structural and Investment Funds

92 Monitoring and review

7. Glossary of terms

x xi

Introduction

1

Contents

• Purpose of the guidance

• City Fringe OA

• City Fringe OAPF

• Tech City

• Vision and objectives

• Strategy: The City Fringe as a planning

boundary

xii 1

1 Introduction

Purpose of the guidance

1.1 In March 2012 the Government published

the National Planning Policy Framework (NPPF) with

the aim of making the planning system less complex

and more accessible and to promote sustainable National Planning Policy Framework

growth. Since then the London Plan has undergone

two reviews. Given the level of consistency between

the current London Plan and the NPPF, the Mayor

considers that the London Plan can be seen as the

expression of national planning policy for London,

tailored to meet local circumstances and to respond to

the opportunities to achieve sustainable development

here.

1.2 This document does not create policy but

provides guidance that supplements the Mayor’s

London Plan and the relevant borough policies for the

City Fringe. The purpose of the OAPF is to elaborate www.communities.gov.uk Figure 1.2 The key diagram

community, opportunity, prosperity

on the development plan policies and provide guidance

on how the Mayor and boroughs wish to see the policy

implemented, thus providing developers, investors

and land owners with greater certainty in the planning

process.

1.3 This Guidance is supported by a Property

Appraisal Study that looks at the business needs of

the City Fringe, possible threats and how planning

might best respond to assist growth. The framework

has also been influenced by meetings and discussions

with key public and private landowners who form the

wider stakeholder group. This has included a review of

current and consented development proposals in the

Opportunity Area (OA). DRAFT FURTHER ALTERATIONS TO

T H E LO N D O N P L A N

1.4

THE SPATIAL DEVELOPMENT STRATEGY FOR GREATER LONDON

The OAPF sits under the broad strategic DRAFT FURTHER ALTERATIONS TO THE LONDON PLAN JULY 2011

CONSOLIDATED WITH REVISED EARLY MINOR ALTERATIONS OCTOBER 2013

guidance of the London Plan and the more detailed

guidance provided in the Local Plans and Development JANUARY 2014

Management Local Plans. On publication the OAPF will

be a supplementary planning guidance (SPG) to the

policies set out in the London Plan. As such it will be

subject to formal public consultation and is therefore a

material consideration in respect of planning decisions Figure 1.1 National Planning Policy Framework and the

in the City Fringe area. Figure 1.3 Material weight of this framework

Draft Further Alterations to the London Plan

2 3

City Fringe opportunity area City Fringe OAPF

1.5 The City Fringe was historically conceived as Fringe OA are considered strategically vital- a point 1.10 In February 2008 the Draft City Fringe

being an area around the north and eastern edges recognised by the UK Government when an exemption Opportunity Area Planning Framework (CFOAPF) was

of the City of London’s financial district, covering to changes in permitted development rights was published for consultation with Hackney, Islington and

Clerkenwell, Old Street, Shoreditch, Spitalfields, granted for the area. Tower Hamlets Councils as well as the City of London

Aldgate and Whitechapel as well as outer parts of the Corporation. This, however, used the original City

City itself such as Broadgate. Over the past decade 1.9 The City Fringe also contains some of the most Fringe boundary. A joint response was received in

the core office market has expanded into these fringe deprived inner city neighbourhoods in the UK, as well October 2010.

areas, with new Grade A office developments and as more affluent neighbourhoods and developments.

replacing much of the older stock. As a result, much of 1.11 This latest draft City Fringe OAPF responds

what was considered fringe in 2003 is now considred to the joint response of October 2010 and has been

“core” by planners and the development industry. By re-focused to look at the key areas that planning can

the same token the City Fringe has moved north and influence, that will allow the Tech City digital cluster

east into areas such as Dalston, Hackney, Haggerston to continue to grow and be a driver of regeneration in

and the wider Whitechapel area. inner East London.

1.6 The City Fringe Opportunity Area (OA) is now 1.12 As the City Fringe also has a significant role

defined in the London Plan as being approximately in addressing London’s housing need, a key aim is

901 hectares of land covering parts of the London achieving a balanced, spatially nuanced approach that

boroughs of Islington, Tower Hamlets and Hackney. allows for the residential development needed without

Tech City is recognised as a significant business cluster compromising the opportunity for economic growth.

within the City Fringe but does not cover the whole Residential development should not be at the expense

of the OA. For planning purposes Tech City represents of the employment land and the commercial floorspace

the commercial core of the City Fringe - around the City Fringe needs to support growth.

Shoreditch, Old Street, Bishopsgate and Spitalfields,

extending north to Hackney Central and Dalston, and 1.13 The London Plan recognises that the City

south and east to include Aldgate and Whitechapel. Fringe is increasingly the home of new and emerging

The wider boundary covers the hinterland area, which sectors of the economy with particular clustering and

is mixed-use in many places but more residential in accommodation requirements. This document looks

nature. at the characteristics of this business ecosystem and

what it is about the City Fringe that has enabled the

1.7 The City Fringe boundary no longer includes growth of this digital cluster within it. The particular

any part of the City of London Corporation area. accommodation requirements are the subject of

As the City is an adjacent area of internationally supporting work, which has informed the strategies set

significant business activity, the relationship and the out throughout this document.

dynamic between the areas has still considered in the

formulation of this document.

1.8 The City Fringe OA contains significant

development capacity in relatively central areas and

there is particular scope not only to support London’s

critical mass of financial and business services but also

the diverse cluster of digital businesses that constitute

Tech City. Consolidation of the digital cluster and

continued business growth in the core areas of the City

4 5

Tech City Why cluster here? This emerging east-west axis broadly aligns with the • Location and “creative vibe”. The area

new Crossrail route, offering London’s knowledge is centrally located and has for decades

economy a new corridor of cross-sector collaboration, attracted small businesses and artists who

1.14 As low-skill manufacturing relocates to low

connectivity and growth. were also attracted by the availability of cheap

cost labour markets and the service and creative

space. Local Authority policies promoting

sectors become dominant in mature economies, the

1.20 The increasing attractiveness of the City nightlife, leisure and the arts (The “Young Brit

digital economy is becoming more important for

Fringe, as well as the arrival of Crossrail also mean that Art” movement started on Hoxton Square)

the UK and other western countries. Realizing the

higher value residential can potentially outbid and provided improved amenity for banking and

potential, governments are engaged in efforts to

displace lower value office and light industrial uses financial services workers from the nearby City,

intensify growth in their digital and creative clusters.

which, over time, could lead to the weakening and whose spending promoted rapid growth in the

The approach of the UK government is to support

dissipation of the cluster. This would be detrimental to arts and leisure industries.

the growth of the existing clusters and the wider

promotion of technology, creative and knowledge London’s wider knowledge economy and the ambition

intensive businesses as part of their strategy to to create a world leading digital-creative business hub • Dense, urban, collaborative environment.

rebalance the economy and strengthen the UK’s based around the current Tech City cluster. The City Fringe’s unique character, mix

competitive position internationally. of uses, transport and lively and informal

1.21 The London Plan estimates that London may networking opportunities and creative

need up to 5.2m sq.m of additional office floorspace atmosphere make it a very attractive place

1.15 Digital businesses have been setting up in 1.18 Large cities, especially long-established ones

by 2031 in order to support projected employment for the highly educated, highly mobile

London since the 1970’s but since the late 1990’s such as London create agglomeration economies-

growth. Central London is expected to need the professionals that successful digital companies

there has been significant growth focused on inner within which businesses benefit from concentrating

majority of this floorspace and the Mayor is concerned need to attract. Such conditions prevail in

east London and in particularly the City Fringe. The and co-locating in large groups. Over centuries of

that the planning process does not compromise other “urban tech clusters” like those in New

resultant digital-creative cluster has been christened trading many specialisms have clustered in distinct

employment growth. York City, San Francisco and Berlin.

“Tech City”, a name which refers to the area around parts of central London, and this is an ongoing

Old Street (or “Silicon”) Roundabout. process. Such clustering offers key advantages to

businesses. These are: 1.22 The Mayor acknowledges that London’s • Connectivity. The City Fringe has excellent

economy is changing and that it is important to ensure public transport connections to other parts

1.16 Whilst activities such as software and web

the ongoing availability of appropriate workspaces for of London and its major airports. It is also a

design and application development are important, • Attracting and retaining skilled labour

London’s changing economy. The London Plan seeks largely walkable area with permeable blocks,

Tech City is not really about creating new “tech”.

an increase in office stock where there is evidence of buildings with small floorplates and a largely

In fact TMT businesses are in a minority. Neither • Knowledge, innovation and technology

sustained demand for office-based activities, such as efficient pedestrian movement network.

is it homogeneous as there is distinctive sectoral transfer between businesses and sectors

those in the City Fringe. Although there are some issues with legibility

clustering throughout the area. Advertising, marketing,

and wayfinding, it is generally easy to travel

communications and branding agencies that have • Competition with similar firms, which

1.23 There are particular conditions that encourage between the core growth area, the hinterland

a focus on use of the internet are a key presence drives efficiency and improves global

clustering in the City Fringe. Some of these conditions areas and other areas of East and Central

throughout the City Fringe but there is a particularly competitiveness.

are related to planning, whereas others (such as those London by bicycle. Modern businesses,

high concentration of such firms to the West of

associated with wider economic structural changes particularly digital firms need a reliable

the City Fringe in Clerkenwell and St. Lukes. There 1.19 London’s knowledge economy can be seen

and cycles) are not. The key growth conditions that internet connection with decent bandwidth

is evidence of a smaller concentration of digital- to be consolidating in clusters along an east-west

planning can affect in the City Fringe are: and reliability. Central London not only has

media, advertising and marketing companies around axis running from the Olympic Park in Stratford in good broadband infrastructure, but Wi-Fi is

Spitalfields. the east and the Golden Mile and Hayes out towards

• Available, affordable, suitable business available either free or for a small fee in many

Heathrow in the west. This axis connects Tech City with places.

1.17 In October 2010 the Prime Minister David stock. The current digital-creative cluster isn’t

world class life science institutions including Queen

Cameron set out his vision for Tech City to become an the first business cluster to form in the City

Mary University, the BioEnterprise Innovation Centre, • Mix of uses. Lifestyle choice and informal

emerging technology hub of international significance, Fringe. The decline of the printing industry

Royal London Hospital, Welcome Trust, University networking. The City Fringe has many small

spreading from Old Street to the Olympic Park. The and manufacturing in particular have left

College Hospital and the new Francis Crick Institute, independent shops, bars, cafes, restaurants

“spread” was already occurring, in that similar clusters a good stock of smaller, affordable office

as well as 4 of the top 40 universities in the world. Of and street markets. This vibrant mix of land-

have formed across inner London where the right accommodation that is well suited to creative

these Imperial College, University College and King’s uses allows plentiful opportunities for informal

conditions exist. This document only addresses the industries and tech start-ups with limited

College all have major new physical expansion projects networking and initiating further collaboration.

City Fringe, which contains the original, catalytic Tech infrastructure and servicing needs.

underway and ambitions for greater collaboration with The leisure uses and night-time activities are a

City cluster. Residential pressure and rising rents mean business, industry and academia, particularly across key attractor for the area.

that the cluster is now expanding to nearby “overspill” the engineering, technology and life science sectors.

areas. Within the City Fringe the spread is generally

outwards towards Hackney, Dalston and Whitechapel.

6 7Co-working spaces The Parallel cluster

1.24 An important source of business space for not always the case. This is likely to be driven by 1.33 The digital economy is characterised by

startups and microbusinesses in the City Fringe is a combination of increased space needs and the high-wage, high-skill, labour intensive activity and

typically provided by a third party workspace provider. requirement for increased privacy, for example to has substantial multiplier effects. Whilst the Tech City

Also often referred to as “co-working spaces” or protect higher value intellectual property. This can cluster has grown, there has been parallel growth in

“hubs” provision typically has an emphasis on flexible only happen, however, if such space is available and other sectors fuelled by the presence of new residents,

occupation and collaborative working. By sharing affordable and the lack of such “grow-on” space could workers and visitors with relatively high incomes. This

services and facilities costs are kept as low as possible be a constraint on growth. growth has seen increased employment opportunities

and the relationship is usually one of membership for long-term residents of inner East London

rather than tenancy. Different levels of membership 1.29 Many co-working communities were founded highlighting the potential for tackling persistent

are tailored to needs and budget and range from hot- by entrepreneurs who understand how start-ups deprivation.

desking options to separate rooms or even a whole and small busineses work, and risk is spread across

floor. the range of membership by offering affordable Growing institutions and support

accommodation to self-employed individuals,

1.25 The multi-disciplinary, collaborative nature homeworkers, more mature microbusinesses and larger,

1.34 Several of London’s world class universities are

of these co-working spaces is likely to be important established SMEs.

located nearby and are developing strong relationships

in stimulating the knowledge spillovers between with businesses in the area. UCL are now providing

sectors that are so important to the growth of the Tech 1.30 Co-working facilities differ from serviced support to small businesses in Tech City through

City cluster as digital, marketing, creative and other accommodation, although demand in the market allowing digital startups to test their new products

professionals sit side by side and receive ideas and for hub-type facilities has led to the lines becoming and services. Queen Mary (QMUL) are seeking to

inspiration from one another. blurred as serviced office providers add similar services establish a stronger presence and further capitalize

and try to appear more like a co-working space. Service on the business and research opportunities, such as

1.26 Co-working spaces provide a useful support office provision has a very clear landlord-tenant those promoted by the Medi-City initiative. This is a

network that often includes skills enhancement, relationship. particularly strong opportunity at Whitechapel.

mentoring and business opportunities as well as social

activities. Often the co-working space will be part 1.31 Some larger firms now recognize the social and 1.35 In addition to the growing links between

of a group of such spaces that share ownership and financial benefits they can derive through allowing part academic institutions and the digital cluster, specialist

a business model. These groups coalesce as “co- of their space to become a co-working space. Recent institutional support is being fostered within Tech City.

working communities” and some have links to the development proposals include office space aimed at In 2012 the Open Data Institute (ODI) was founded

local residential community through initiatives such accommodating co-working space to attract an anchor with help from the Technology Strategy Board to help

as free workshops, small apprenticeship schemes and tenant and balance the risk. Some models now even incubate and nurture new businesses and exploit open

community events. involve balancing the risk by also providing serviced data for economic growth. large private initiatives have

office accommodation also been announced. KPMG has stated its intention

1.27 Co-working communities in the City Fringe to open an office in Shoreditch with a dedicated

differ in size, business model, structure and space 1.32 A key variable in keeping membership costs team to support early stage technology companies,

configuration. They range from listed companies, to down within a given location is how the building was and technology firm IBM is also bringing its global

social enterprises and even charities. Space availability acquired and what the associated lease length and cost entrepreneur program to the area.

and cost will in some cases dictate the professional is. Over time they get more expensive as development

profile of the members. pressure increases and the lease is unlikely to be

extended unless tenant can afford much higher rents.

1.28 Successful businesses experiencing high At this point the building, and associated sunk costs

growth will often seek to graduate from a co-working on fit-out, are lost.

space and into their own property, although this is

8 9Emerging cluster ecosystem around technologies, invention and prototyping. Cycling and

pedestrian connection to Tech City via Regents Canal,

Tech City along which many informal networking and leisure

opportunities are now emerging.

1.36 The Prime Minister’s vision can be said to be

already happening, with clusters emerging organically 1.42 Here East, Olympic Park. Planned centre

or being created/ nurtered in various locations. The for innovation, education and enterprise in former

continued focus on regenerating East London post- broadcast centre with dedicated datacentre and

Olympics, increasing public transport delivery and the excellent digital connectivity. BT Sport, Infinity SDC

availability of development land in the nearby “Arc of and Loughborough University are already tennants,

opportunity” (the OAs of East London) significantly and TechHub and Space studios have been signed to

enhance the potential for the Tech City cluster, centred manage artist and startup facilities.

on the City Fringe OA, to become the driving force for

an enlarged technology hub of global significance that

1.43 London Bridge/ Southbank. Increasingly

is spread throughout East London.

significant levels of startup activity, partricularly in the

tech and creative industries.

1.37 Clerkenwell. A well established cluster

with a particularly high concentration of advertising,

1.44 Excel centre. Over one million square feet

marketing, communications and branding agencies

of flexible event space located close to the Siemans

Crystal and new Crossrail station. Direct link to Digital

1.38 Angel. The most significant town centre Greenwich via cable car

Figure 1.4 London’s science and tech economy, research strengths and Opportunity Areas- roughly alighned with Crossrail

in Islington Borough and a focus for the night time

economy also has a good supply of small offices. Many

1.45 Digital Greenwich. Co-located with the

small businesses have been attracted to Angel, which

O2 arena and Ravensbourne College with a quick

has grown in significance recently as a business cluster.

underground link to central London. Central hub of

the emerging Greenwich Millenium Village community,

1.39 Kings Cross. Home to Central St. Martins, which will eventually have around 10,000 homes.

Google and the Crick Institute. Tech, creative and

medical convergence with High Speed rail link to

1.46 Silvertown Quays. Mixed-use redevelopment

Mainland Europe and underground link to Heathrow

incorporating the “brand pavillion” concept, co-

locating sales, R&D and back office functions of major

1.40 Canary Wharf. Europe’s largest financial-tech tech retailers.

(Fintech) and retail start-up accelorator space situated

on levels 39 and 42 of 1 Canada Tower. Single land-

1.47 International quarter, Olympic Park. One

owner creates unparrallelled potential for Fintech and

of the UK’s largest mixed-use schemes incorporating

retail R&D. Proposals for Wood Wharf to accomodate

approximately four million square feet of office space

tech occupiers as a key part of the future business

and significant community and civic facilities.

community. New Crossrail station under construction.

1.48 Westfield Stratford. New shopping centre

1.41 Hackney Wick. Many lower value creative

sited on large transport terminus as part of the

uses, some displaced from core areas of Tech City

Stratford City regeneration. Aims to set standards in

contributing to Europes largest concentration of

innovation and early uptake of retail technology.

fine artists. Many SMEs and microbusinesses and

a significant “maker community”- small-scale

manufactureres with a focus on unique applications of

Figure 1.5 Existing and Emerging science and tech economy clusters in and around the City Fringe, with Crossrail and other

recently delevered transport infrastructure

10 11The vision and objectives benefit planning can bring that will facilitate continued

growth and expansion of Tech City. The vision is:

1.49 Tech City’s role as innovation and start-up hub

for the knowledge economy in London is strategicaly “Enabling the business cluster to continue to

significant. Tech City UK and London & Partners have grow as a mix of large corporations, SMEs,

remits that specifically include assisting growth in the micro businesses and start-ups and become

sector. the innovation hub driving growth in London

and the UK’s the digital economy, while

delivering housing and other supporting uses

1.50 Tech City UK (initially Tech City Investment

such as retail and leisure. ”

Organisation) is part of UK Trade and Industry (UKTI)

and was initially set up to assist in accelerating digital

businesses in Tech City. This was later widened to a UK- 1.55 These are five objectives in order to achieve

wide remit with a focus on: this vision:

• Forging partnerships across the ecosystem that • Ensuring there is the space for continued

provide entrepreneurs with extended reach business growth in City Fringe

• Championing the digital and technology • Striking the appropriate balance between

industry in the UK and internationally residential and commercial development

• Informing policy makers at senior levels of • Supporting the mix of uses that makes

Government about the needs of the digital City Fringe special

entrepreneur

• Identifying the key strategic development

• Piloting programmes to increase the growth of sites

digital entrepreneurship

• Connecting the City Fringe

1.51 London & Partners is a not-for-profit public

private partnership, funded by the Mayor and a 1.56 Each chapter relates to one or more objectives

network of commercial partners. It was set up in and sets out the background to each issue, then sets

2011 to attract investment and visitor spend, in turn out the strategies that will deliver each objective.

creating jobs and growth, build London’s international In addition there is a chapter that sets out how the

reputation preserves its global position. document will be implemented, with additional

strategies to assist in this.

1.52 London & Partners work to attract foreign

direct investment (FDI), capital investment into Strategy 1 - The City Fringe as a

regeneration projects; and help London businesses

to win business overseas. They open up direct access

planning boundary

to expert and experienced professionals, who advise

and guide overseas companies through every aspect 1.57 The City Fringe OA is the subject of strategic

of locating and doing business in London. They also policies set out in the London Plan and the Local Plan

promote London to overseas business expanding policies of the London Boroughs of Islington, Hackney

into the UK or Europe - from start-ups to established and Tower Hamlets. This document aims to give

international companies. guidance on how these policies can be applied in order

to best deliver the agreed vision and objectives. In

order to ensure a consistent approach across the three

1.53 Tech City UK and London & Partners have

boroughs and provide a basis for the implementation

complementary remits and together they address non-

of these policies and the City Fringe OAPF an

planning issues. The Mayor sets out in this document

indicative planning boundary has been agreed. This

what the planning system can do to assist.

boundary is shown in figure 1.6 and consists of the

core growth area and the wider, largely residential

1.54 The City Fringe OAPF takes this forward and is

hinterland of the City Fringe OA. This boundary should

a growth focussed document aiming to maximize any

formally adopted in Local Plans.

Figure 1.6 The Core and Hinterland areas of the City Fringe OA

12 13Ensuring space

for continued

2

growth

Contents

• The mix of business in the City Fringe

• Analysis of the property market

• Types of space being used

• Supply of space

• Demand forecasts and comparison with

supply

• Strategy 2: Protecting a quantum of floorspace

needed for growth

14 152 Ensuring space for continued growth

The mix of businesses in the City Analysis of property market

Dalston

Fringe

2.5 In order to support and inform the preparation

2.1 The London Plan recognizes the need to process, a detailed property market appraisal has Canalside

support London’s distinctive economic clusters and been carried out. The operations, opportunities

and challenges reflected in the property market are

to protect and enhance the supply of offices where

there is evidence of sustained demand. There have considered in order to identify the main planning Hackney

been structural changes in the past decade with related issues facing the City Fringe in its role as a

small businesses becoming more important to both place of work. The property market appraisal addresses

London and the UK economies. There have also been knowledge gaps acknowledges that the City Fringe

significant changes in the way office space is used, includes a wide range of businesses at different points

with new technologies and working practices offering in their life cycle, includes multiple sub-sectors, with a

new opportunities and blurring the distinction between range of occupier and property requirements. There is

office based work and light industry. also a wide spectrum of rent levels and lease lengths

being sought. Supporting key areas of the cluster

2.2 This document notes the growth of the Tech with the right workspaces and the right locations is

City cluster and seeks to reinforce and promulgate important, but so is flexibility to allow the cluster to

the catalysts for this growth. The primary aim of the grow and develop. The findings of the property market

OAPF is therefore to create a positive environment for appraisal help inform the strategies of this document. Shoreditch

employment growth in the City Fringe.

Angel East

2.6 The basic underlying approach of the property

2.3 The knowledge intensive, business to business market appraisal was to consider the characteristics Shoreditch

(B2B) firms in the Tech City cluster are typically not of the business cluster and likely demand, and of the St’ Lukes West

limited to selling their goods and services locally but property market and likely supply. In order to allow a

over the internet, to a fast-growing global market. systematic assessment of the key issues the following

were considered:

Their success provides strong conditions locally for Spitalfields

the important business to customer (B2C) firms which

make up the “the parallel cluster” and help drive the • Types of space Whitechapel

continued attractiveness of the area.

• Supply of space

2.4 There is also evidence that larger corporations

are relocating house employees that are specifically • Demand forecasts and comparison with supply

focused on digital-media related activity in the

• Viability and competition with residential

City Fringe. This offers the potential for knowledge

spillover, innovation and recruitment due to proximity development Clerkenwell Aldgate

to other workers in the same field. The rich, innovative

mix of small businesses and entrepreneurs is an

attractor for the larger corporates. This emerging mix

of the very large and the small is therefore likely to be

a very important aspect of the ongoing development

of the cluster.

0 0.25 0.5 1 1.5 2

Kilometers

¯

Figure 2.1 City Fringe boundary divided into sub-market areas

16 17Types of space being used Supply of space Demand forecasts and comparison

with supply

2.7 There are five broad typologies of commercial 2.8 The City Fringe is clearly a place in transition.

space in the City Fringe, which are useful in High demand for housing in central areas has seen 2.11 Demand forecasting looked at short, medium

considering the differing occupiers and their needs. employment land being converted to residential use and long-term demand in low, medium and high

These are: in areas like Aldgate. Although there remains strong growth scenarios. The potential net additional demand

demand for office space in the core growth area between 2013 and 2023 was forecast at between

• Artist’s studios. Typically under 93 sqm (1,000 • Start-up and other SME space. Also up to around Shoreditch, new development is constrained to around 288,000sqm and 385,000 sqm. Strength of

sqft). per unit but usually grouped together as 372 sqm, this covers the smallest individual the north by large areas of social housing and to the demand can be broken into three categories and this is

a collection of unit in larger buildings centrally business units that are no co-working spaces south by new office development in the City. The more shown on the “demand map” in Chapter 3. Projected

managed. Artist studios laid the foundations or artist studios. peripheral areas of the City Fringe have subsequently demand exceeds supply in the short term across the

for the creative, and then digital-creative become increasingly important sources of small space City Fringe, indicating a supply-constrained market and

cluster when vacant buildings in the area were • Grow-on space. This is space occupied by for start-ups- especially around Whitechapel. Demand highlighting the important role planning can have.

initially colonized in the 1970s and 80s. More growing businesses who have typically for smaller space is increasing but the availability of

recently there has been a generally movement graduated from smaller space and is between space, including new build, is skewed towards larger 2.12 Over the medium and long term there is

away from the core growth areas into the 372 and 2,787 sqm (4,000 and 30,000 sqft). floorplates. Large floorplate city office users have potential to meet much of the projected demand

hinterland and beyond. Hackney Wick, There is a relatively scattered provision of expanded south and east into Aldgate, Shoreditch west through intensification of under developed sites and

between the City Fringe and the Olympic Park this, housed in a diverse range of spaces and and Spitalfields.This mismatch between supply and through comprehensive redevelopment of Local Plan

has a particularly high concentration of artist’s locations across City Fringe. demand means that office rents are rising rapidly and sites. Analysis of the permissions granted so far on

studios now. there is a short-term shortage of supply particularly in Local Plan sites, however, found that sites designated

• Corporate office space. This is for the largest the core growth area. for employment use have been granted permissions

• Co-working space. Typically up to 372 sqm occupiers of office space and is space over for other uses, predominantly residential. This may

(4,000 sqft) and an important source of space 2,787 sqm (30,000 sqft). These offices are 2.9 The supply pipeline is constrained in the short mean that the potential for Local Plan to meet future

for start-ups and microbusinesses. Initially a usually large floorplate flexible space offering term (to around 2016) but there are some large office demand for employment floorspace in the City Fringe

small cluster concentrated on Shoreditch, this Grade A quality offices. The expansion of the buildings scheduled for completion over the medium is overestimated.

is now moving outwards on an east-west axis City has brought more of these uses into parts term. Development activity was suppressed by the

and will continue to grow with high demand of the City Fringe. 2007 global financial crisis but interest has now picked

for affordable space up strongly indicating a step-change in demand from

past trends. The total amount of floorspace (all uses)

scheduled for completion in the City Fringe between

2013 and 2018 is almost ten times higher than the

five-year historical average.

2.10 The majority of the potential future supply of

new B Class employment floorspace is located within

sites designated in Local Plans by the boroughs.

Although this would seem to provide scope for

growth of the office stock over the medium to long

term, many planning permissions come forward with

lower levels of employment use than outlined in

policy. Furthermore once a planning permission is

secured, the site often becomes the subject of revised

planning applications which seek to reduce levels

of employment floorspace. Should the incidence of

this practice increase then the levels of employment

floorspace actually built may be significantly lower

than in the currently assumed pipeline.

18 19Strategy 2: Protecting a quantum of workspace needed to facilitate

growth

A. PD Exemption B. Core growth and residential C. affordable space at the core of D. Provision of employment

hinterland Tech City floorspace in new development

2.13 The mayor has assessed that as of April 2013,

new permitted development rights would likely have

(including mixed-use development)

2.14 The core growth areas of the City Fringe are 2.15 Much of the growth associated with the

led to the unplanned loss of significant employment where there will need to be a continued supply of (B digital-creative cluster occurred because of the 2.16 The Mayor supports proposals for new B Class

floorpace in the core growth areas of the City Fringe Class in the Use Classes Order) employment floorspace. availability of affordable, second hand office or light employment space, including the redevelopment of

(Tech City), causing significant harm to future business This is not to say that demand and the appropriate industrial stock in the City Fringe. A continued increase existing low value workspace outside of those already

growth in the area. An exemption has therefore been level of supply will be even throughout the core areas, in demand for secondary office space is highly likely identified in Canalside, Shoreditch and Spitalfields.

granted in recognition that it could otherwise have or that provision of employment space is inappropriate and it is beneficial to the future growth prospects of For sites in the core growth areas the applicant

been to the detriment of a nationally significant area in the largely residential hinterland. Further work has Tech City to protect some of this space in the most in should seek to incorporate an equivalent amount of

of economic activity. It should be noted that this already been undertaken and specific detail given with demand but vulnerable areas. These are areas where affordable workspace that is flexible and/or suitable

exemption also covers the Central Activities Zone, Isle regard to Site Allocations- shown on the map. The residential demand is high but there is a relatively large for occupation by micro and small enterprises.

of Dogs and Royal Docks Enterprise Zone. Figure 2.2 broad levels of employment floorspace expected from concentration of secondary office stock close to the Developers are encouraged to look at existing models

shows the extent of the City Fringe area covered by development in the different areas is explored in more core growth area. These areas are (See map) Canalside, of workspace that are designed to house a range

the exemption. detail in Chapter 3. Shoreditch East and Spitalfields. of business sizes from startups to anchor tenant,

therefore balancing the risk to the landlord. Applicants

are required to submit a detailed explanation of how

the workspace is to be managed post-construction

and, where appropriate, evidence of agreement to

lease the workspace to a Workspace Provider. This

should include confirmation from the Workspace

Provider of willingness to manage the shell and core, to

an agreed specification, on concessionary lease terms

which will allow the space to be let to end users at

economic rents. Applicants should engage Workspace

providers at the earliest opportunity in the evolution

of proposals and actively involve them in the pre-

application process in order to address issues of design

and management early and satisfy the local authority

that floorspace will be useable and viable for use by

micro and small enterprises. A map and accompanying

list of workspace providers is kept up-to-date on the

GLA website at:

• https://www.london.gov.uk/priorities/

business-economy/for-business/business-

support/london-workspaces

2.17 Where an end-user has not been identified,

employment floorspace should be well designed, high

quality and incorporate a range of unit sizes and types

that are flexible, with good natural light, suitable

for sub-division and configuration for new uses and

activities. This should include units for occupation

by small or independent commercial enterprises and

consideration should be given to providing “grow-on”

space, between 372 and 2,787 sqm (4,000 and 30,000

sqft).

20 21Figure 2.2 Area exempted from changes to Permitted Development April 2013 Figure 2.3 Map of core and hinterland areas, area where secondary office space is desireable and with Site Allocations

22 233

Striking the

balance

Contents

• Viability and competition with residential

development

• Strategy 3: Striking the balance between

employment and residential

24 253 Striking the balance

Viability and competition with

residential development

3.1 The difference in value between commercial much of it- including the new areas into which it is

and residential land use in the City Fringe has expanding, is not. Further reviews of the London Plan

put considerable pressure on commercial space- will consider the scope for extending the CAZ.

particularly at the affordable end of the spectrum.

Residential development can present potential issues 3.4 Demand for residential space is strong and

with servicing and late operation in established this is likely to continue. This strong demand is

employment areas and with residential land typically driven by some of the same factors as the rise of the

being subject to long leaseholds such areas are unlikely digital-creative cluster and the past decade has seen a

to revert to commercial regardless of future economic significant increase in the numbers of affluent young

conditions. The City Corporation have, for many years, households moving to inner east London. The market

used planning policy to tightly control land-use and for new build in inner London is also partly driven by

ensure that the City continues to operate as a hugely demand from buy to let, overseas investors and buyers

succesful business location. often agreeing to purchase units well in advance

of completion. The annualized rate of house price

3.2 The London Plan encourages mixed-use increase in the City Fringe is around 2% higher than

development, recognising that London’s economic the London average and residential prices are markedly

growth depends heavily on an efficient labour market, higher than the capitalised values achieved on recent

which in turn requires adequate housing provision office transactions.

that could also sustain other uses nearby. Local and

strategic mixed-use polices aimed at reprovision of 3.5 Even allowing for factors such as extraordinary

lost commercial space in the City Fringe area have, costs associated with changing the built fabric, the

however, had limited success. Issues encountered market outlook and landlord aspirations, it is expected

include commercial space which fails to respond that where possible the redevelopment of employment

adequately to demand and therefore is not marketable. land for residential use will remain an issue over the

This can then be unoccupied and become vulnerable short and long term in all but the prime office market.

to conversion to residential at a later date. Discussion

around viability and marketability may be failing to 3.6 Canalside appears to be a location where

take into account the changing and cyclical nature redevelopment of prime office stock into residential is

of office provision in the City Fringe. The risk is that viable. For less valuable secondary office stock the area

poorly designed workspace and short-term focused is wider and includes Shoreditch as well as Canalside,

marketing assessments threaten to limit space available where residential values are highest. This is a concern

for expansion of economic activities. as the secondary rent offices are the most attractive to

the start-ups and SMEs that form a key element of the

3.3 In recognition that mixed-use housing and business ecosystem of Tech City and the City Fringe.

commercial redevelopment can sometimes compromise These areas are also where demand for office space is

broader economic objectives, such as sustaining key outstripping supply.

clusters of business activity, the London Plan provides

for exceptions to its on-site mixed-use policy. These

exceptions currently apply when a case can be made

in the CAZ or the Northern Isle of Dogs and they still

result in the provision of extra housing off-site instead

of on-site. While some of Tech City is within the CAZ,

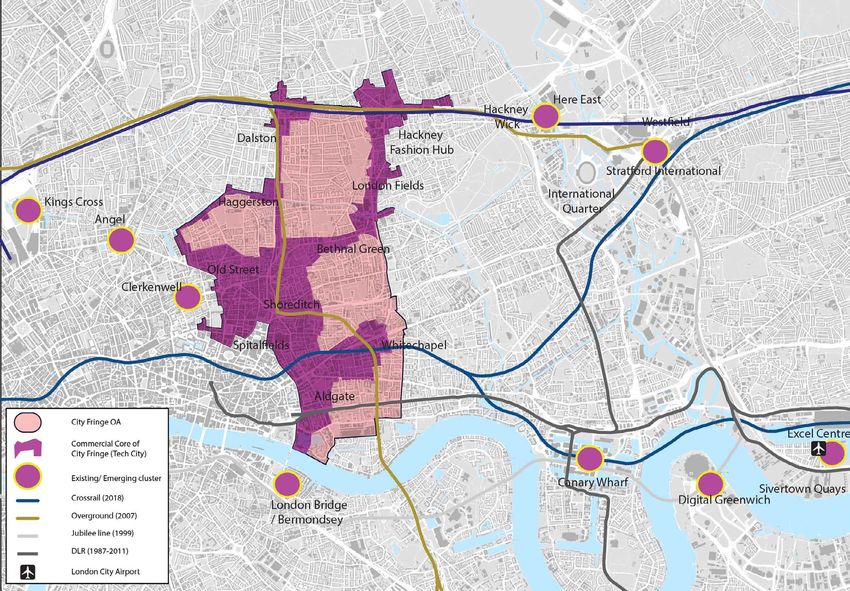

26 27You can also read