Catastrophe Risk Tolerance Study - Public disclosures by sector Year-end 2020 - Thought Leadership

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Catastrophe Risk Tolerance Study Public disclosures by sector Year-end 2020 1 Proprietary & Confidential Proprietary & Confidential

Contents Section 1 Overview and Key Findings Section 2 Analysis of Disclosure Data Section 3 Risk Tolerance Metrics Disclosure Section 4 Risk Tolerance Summary 2 Proprietary & Confidential

Section 1:

Overview and Key Findings

3 Proprietary & Confidential

Proprietary & Confidential2010 - 2020 Catastrophe Insured Losses

▪ Insured losses from natural disasters in 2020 reached USD100 billion and were significantly lower than

the record USD157 billion in 2017 but still the 4th highest of the decade

▪ Severe Convective Storm was the costliest peril (USD44 billion), driven by historic U.S. losses; tropical

cyclone (USD27 billion) & wildfire (USD14 billion) had active, but non-record years for the industry

4 Proprietary & ConfidentialCatastrophe Risk Tolerance Study Overview

Composition Disclosure

▪ Includes 88 unique re(insurers) on a global basis that report catastrophe 100% Primary Source Secondary Source

loss information in their financial disclosures 7%

15% 12% 6% 7%

75% 14% 13%

▪ Percentage reporting has been relatively flat over the last few years;

most companies provide catastrophe disclosures on a consistent basis 50%

▪ 85% of the industry disclosed some type of information relating to 73% 76% 77% 78%

69% 68% 69%

catastrophe risk tolerance, which is slightly higher than that of the year- 25%

end 2019 disclosure; the percentage of "primary" source disclosures

increased slightly to 78% 0%

2014 2015 2016 2017 2018 2019 2020

Data Sources 2019 2020 2019 (%) 2020 (%)

Primary 70 69 77% 78%

10K Reports 43 42 47% 48%

Annual Reports 25 25 27% 28%

Investor / Analyst Presentations 2 2 2% 2%

Secondary 6 6 7% 7%

A.M. Best Reports 6 6 7% 7%

Not Disclosed 15 13 16% 15%

Totals 91 88 100% 100%

Note: The following companies were part of the 2019 study but are not included in the 2020 study due to M&A activity: Sirius International Insurance Group Ltd,

Navigators Group, Inc, Third Point Reinsurance Ltd and Protective Insurance corp. The following companies were added to the 2 020 study: Sirius Point. Population

excludes (re)insurers from Medical Professional Liability, Life & Health, Financial / Mortgage Guaranty and Title sectors

5 Proprietary & ConfidentialKey Findings of Catastrophe Risk Tolerance Study

▪ Approximately 85% of companies disclosed risk tolerance or related information, of which 39% of the disclosures were

through PML figures (Net):

Undetermined /

Disclosure Type Percentage Disclosed as Target Disclosed as Actual Not Disclosed Count

PML Figure (Net) 39% 9 25 0 34

As Part of Reinsurance Discussion 39% 0 34 0 34

Other Disclosure Type 8% 1 3 3 7

Undetermined / Not Disclosed 15% 0 0 13 13

Totals 100% 10 62 16 88

▪ Disclosures varied by sector. More than 50% of the disclosures made by Commercial Lines and Reinsurance companies

were through net PML, while reinsurance structure was the most common form of disclosure for Personal and Specialty

Lines

▪ Aon’s post-Katrina risk tolerance study indicates that a catastrophe event can range from 3 – 6% of equity for primary

companies and 12 – 19% of equity for reinsurers before impacting stock price by more than 10%

‒ The average 100yr PML risk tolerance disclosure for primary and reinsurance companies is in-line with Aon’s post-

Katrina study and falls in line with 2017 Harvey, Irma & Maria (HIM) results

6 Proprietary & Confidential2020 “View of Risk” Poll Results

How does your firm obtain analysis on What catastrophe model results form When w as the last time your company

catastrophe exposure? “management view ” of risk? re-evaluated its model selection &

assumptions in determining

Developed in-house “management view ” of cat risk?

model AIR only

License a catastrophe RMS only Within the last 2 years

model

Blend

License multiple models 3 to 5 years ago

Customized

Broker or other advisor Other More than 5 years ago

0% 20% 40% 60% 0% 20% 40% 60% 0% 20% 40% 60%

What probable maximum loss (PML) Other than PML analysis, w hat analysis What “model miss” factors concern you

return period does your company target is used to determine catastrophe the most about your firm’s catastrophe

to protect to w hen determining reinsurance limit? exposure?

catastrophe reinsurance limit?

Climate change

Deterministic events

100 to 150 year Hazard & vulnerability

assumptions

150 to 200 year Exposure Regulatory

accumulations intervention

200 to 250 year

Recast of historical Social inflation

Above 250 year event

0% 20% 40% 60%

0% 20% 40% 60% 0% 20% 40% 60%

7 Proprietary & ConfidentialEvent Studies: Katrina and Harvey, Irma & Maria (HIM)

Typical CRO / CFO risk tolerance questions

▪ What proportion of one year’s earnings can be lost in a single event without an adverse stock price reaction?

▪ What proportion of GAAP equity?

Post-event share price decline best predicted by reported Katrina losses alone, rather than Katrina, Rita and Wilma losses combined

▪ Indicates a greater sensitivity to a single large loss rather than an aggregation of events

▪ (Re)insurers losing less than 10% of shareholder value had Katrina losses in the following ranges, which are consistent with recent PML public

disclosures

Katrina - Cat Loss as % of * HIM - Cat Loss as % of *

Prospective Prospective

Sector Equity Consensus Earnings Equity Consensus Earnings

Primary Insurers 3% to 6% 21% to 34% 3% to 6% 24% to 44%

Reinsurers 12% to 19% 107% to 110% 7.5% to 10% 64% to 81%

HIM observations:

▪ Six primary insurers had more than a 10% drop in stock price, all of which had more than a 6% hit to equity from HIM

– 21 publicly traded insurers traded down more than 10% at some point

– For primary insurers with less than 10% drop in shareholder value, there is an average total cat loss to equity of 3%

▪ Five reinsurers had a loss of more than 10% to shareholder value, with an average total cat loss to equity of 10%

– 11 reinsurers traded down more than 10% at some point

– Reinsurers that did not lose more than 10% of shareholder value had an average total cat loss to equity of 6%

* Show n on a net post-tax basis

8 Proprietary & ConfidentialCatastrophe Risk Tolerance Disclosure Trend Analysis:

Sample Composite PML Target Ranges Post-Tax Detail

Post-Tax Net PML as a Percent of Equity: Primary Insurers

1 in 100yr 1 in 250yr

Count Median Max Count Median Max

2020 12 5% 20% 15 6% 20%

2019 12 6% 18% 16 9% 36%

2018 13 7% 22% 16 10% 32%

Post-Tax Net PML as a Percent of Equity: Reinsurers

1 in 100yr 1 in 250yr

Count Median Max Count Median Max

2020 4 7% 8% 7 10% 20%

2019 5 8% 16% 8 11% 23%

2018 5 8% 15% 8 12% 21%

Note: The composite for 2020 consists of 33 companies across all sectors where definitive (100YR, 200YR or 250YR) PML targets or actuals were disclosed.

There were 35 companies in the 2019 composite, 36 companies in the 2018 composite, 33 companies in the 2017 composite, and 32 companies in the 2016

composite. Where companies reported an actual instead of a target, we assumed the actual was their target. Due to a limited d ataset, results should be used for

informational purposes only. An assumed effective 21% tax rate for insurers and 15% for reinsurers was used by Aon as needed for level setting since some

firms disclosed pre-tax and others post-tax.

*The PMLs analyzed include those specified as all peril and all regions as well as specific peril by specific region

9 Proprietary & ConfidentialCompanies Disclosing 100yr, 200yr and 250yr net PML

PML disclosures varied by sector. The majority of Specialty Lines, Commercial lines and Reinsurance companies disclosed

250-yr net PML figures, whereas Personal lines disclosed mostly 100-yr net PML figures

Personal Commercial

25% 14% 12.1% 11.9% 11.9%

20.0%

20% 12%

8.8% 7.9%

10%

15% 11.9% 8% 5.3% 5.8% 5.8% 5.0%

6% 3.4% 3.7%

10% 6.3% 6.0% 4% 1.5% 1.5% 1.0% 2.0%

5.2% 4.8%

2%

5% 0.7% 0%

0% AIG CB CINF SIGI TRV DLG SIGI TLX AIG CB CINF FFH SIGI HIG TRV

ALL FNHC HCI KINS SAFT AV/ LN IAG AU LN

1:100 Post-Tax PML/SHE 1:250 Post-Tax PML/SHE 1:100 Post-Tax PML/SHE 1:200 Post-Tax 1:250 Post-Tax PML/SHE

PML/SHE

Reinsurance Specialty

25% 20.0% 25%

19.0% 18.2% 19.8% 19.1%

20% 16.5% 17.0%

20% 16.7%

15% 11.4%

9.2% 9.9% 9.6% 8.5% 15%

8.1% 7.9% 8.0%

10% 6.9% 6.5% 8.7%

10% 7.7%

5% 5.5%

0% 5% 2.4%

0.8% 0.8%

MUV2:GY

AXS

SCR.PA

AXS

Y

Y

WTRE

HNRI:GR

HNRI:GR

HNRI:GR

RE

SREN

RE

GLRE

PRE

0%

AFG LR E LN H SX LN AFG AC GL BEZ LN LR E LN PL MR R LI

1:1 00 P ost-Tax PML /SHE 1:2 00 P ost- 1:2 50 P ost-Tax PML /SHE

Tax

1:100 Post-Tax PML/SHE 1:200 Post-Tax PML/SHE 1:250 Post-Tax PML/SHE PML /SHE

10 Proprietary & ConfidentialClimate Change Disclosure Regimes

As part of the effort to combat climate change, corporations are starting to release yearly financial related disclosures rel ating to various

reporting regimes as an effort to provide more transparency behind risk corporations face. This year’s studies examines the n umber of

disclosures from insurance companies for the following regimes:

Task Force on Climate-related

Carbon Disclosure Project Financial Disclosures

CDP is a not-for-profit charity that runs the global disclosure system for investors, The Financial Stability Board established the TCFD to develop recommendations for

companies, cities, states and regions to manage their environmental impacts. more effective climate-related disclosures that could promote more informed

investment, credit, and insurance underwriting decisions.

By scoring companies from A to D-, The CDP guides companiesthrough disclosure

to awareness, management, and finally to leadership. In turn, enable stakeholders to understand better the concentrations of carbon-

related assets in the financial sector and the financial system’s exposures to

Scoring measures, the comprehensiveness of disclosure, awareness and climate-related risks.

management of environmental risks and best practices associated with

environmental leadership, such as setting ambitious and meaningful targets. Our disclosure recommendations are structured around four thematic areas that

represent core elements of how organizations operate:

CDP Ratings Distribution ▪ Governance

▪ Strategy

Rating 2018 2019 2020 ▪ Risk Management

A 2 3 2 ▪ Metrics and Targets

A- 2 5 11 Number of Reports Filed Featuring Companies From This Study

B 8 9 5 Disclosure Regime 2018 2019 2020

B- 1 2 0

C 13 11 7 TCFD 19 26 31

C- 0 0 0 CDP 31 31 30

D 3 0 4 Both 16 21 24

D- 1 1 1

Either 20 15 14

11 Proprietary & ConfidentialSection 2:

Analysis of Disclosure Data

12 Proprietary & Confidential

Proprietary & ConfidentialCatastrophe Risk Tolerance Disclosure Distribution by Sector

Disclosures varied by sector, with Commercial Lines and Reinsurance companies using net PML most often, while

reinsurance structure was the most common form of disclosure for Personal Lines and Specialty Lines

Commercial Lines Sector Personal Lines Sector

6% 7%

4%

Net PML

25%

Net PML

22%

Reinsurance Structure Reinsurance Structure

50%

Other Other

None None

22%

64%

Specialty Lines Sector Reinsurance Sector

26% 30% Net PML 20%

Net PML

Reinsurance Structure

Reinsurance Structure

Other

13% Other

None

67% None

44%

13 Proprietary & ConfidentialRisk Metrics Disclosures

Actual vs. Target PML Aggregate vs. Occurrence

Actual Target

12 30 Aggregate Occurrence Both

10

# Com panies

1 25

8

# Companies

2 4

3 20

6 3

4 9 15

7 14

2 4 5 3

10 15 1

0 7

Commercial Personal Specialty Reinsurance 5 8

6

0 2 3 3

Commercial Personal Specialty Reinsurance

All Peril vs. Regional Disclosure

Actual Target ▪ All carriers (Personal, Commercial, Specialty and Reinsurance)

20 lines are more inclined towards Actual PML

# Companies

15 4 ▪ All company composites predominantly report on an

10 Occurrence basis

5

13 ▪ Actual PMLs are more concentrated towards Specific Peril

5 1 Regional and All Perils Regional disclosures while Target

5 3

2

0 PMLs are featured in both Specific Peril Regional and All Peril

All Perils All Perils Specific Peril Specific Peril All Regions disclosures

Regional All Regions Regional All Regions

We Assume It as Occurrence , If PML Is Disclosed, But Not Specified as Aggregate Or Occurrence.

14 Proprietary & ConfidentialSection 3:

Risk Tolerance Disclosures

15 Proprietary & Confidential

Proprietary & ConfidentialCatastrophe Risk Tolerance - Public Disclosure

P&C Commercial Lines Sector Metric Disclosures

Aggregate/

Company Ticker 100yr 200yr 250yr Other RPs (List) Risk Quantification Metric Pre- or Post-Tax Actual/ Target Occurrence

Allianz Group XETRA:ALV Other

American International Group, Inc. NYSE:AIG ✓ ✓ Net PML Pre-Tax Actual Aggregate

Chubb Limited NYSE:CB ✓ ✓ 10yr Net PML Pre-Tax Actual Both

Cincinnati Financial Corporation NASDAQ:CINF ✓ ✓ 50yr, 500yr Net PML Post-Tax Actual Occurrence

CNA Financial Corporation NYSE:CNA Reinsurance Structure Actual Occurrence

Direct Line Insurance Group Plc LSE:DLG ✓ Net PML Pre-Tax Actual Occurrence

Fairfax Financial Holdings Limited TSX:FFH ✓ Net PML Pre-Tax Target Aggregate

Liberty Mutual Holding Company Inc. - Reinsurance Structure Actual Both

MS&AD Insurance Group Holdings, Inc. TSE:8725 Other Actual

Old Republic International Corporation NYSE:ORI None

QBE Insurance Group Limited ASX:QBE Reinsurance Structure Actual Occurrence

25yr, 50yr, 150yr,

Selective Insurance Group, Inc. NASDAQ:SIGI ✓ ✓ ✓ Net PML Post-Tax Actual Occurrence

500yr

Sompo Japan Nipponkoa Holdings, Inc. TSE:8630 Other Actual

Talanx AG XETRA:TLX ✓ Net PML Pre-Tax Actual Occurrence

The Hartford Financial Services Group, Inc. NYSE:HIG ✓ Net PML Pre-Tax Target Occurrence

Tokio Marine Holdings, Inc. TSE:8766 Other Actual

Travelers Companies, Inc. NYSE:TRV ✓ ✓ 50yr, 1000yr Net PML Post-Tax Actual Occurrence

Zurich Insurance Group Ltd. SWX:ZURN Reinsurance Structure Actual Both

16 Proprietary & ConfidentialCatastrophe Risk Tolerance - Public Disclosure

P&C Personal Lines Sector (1 of 2) Metric Disclosures

Aggregate/

Company Ticker 100yr 200yr 250yr Other RPs (List) Risk Quantification Metric Pre- or Post-Tax Actual/ Target Occurrence

The Allstate Corporation NYSE:ALL ✓ Net PML Pre-Tax Target Aggregate

Assicurazioni Generali SpA MIL:G ✓ Other

Aviva Plc LSE:AV. ✓ Net PML Pre-Tax Target Both

AXA SA ENXTPA:CS Reinsurance Structure Actual Occurrence

Donegal Group Inc. NASDAQ:DGICA Reinsurance Structure Actual Occurrence

Echelon Financial Holdings Inc. TSX:EFH Reinsurance Structure Actual Occurrence

Erie Indemnity Company NASDAQ:ERIE Reinsurance Structure Actual Aggregate

Federated National Holding Company NASDAQ:FNHC ✓ 50 yr Net PML Pre-Tax Actual Occurrence

Hanover Insurance Group, Inc. NYSE:THG Reinsurance Structure Actual Both

HCI Group Inc. NYSE:HCI ✓ 50yr,127 yr, 260yr, 320yr Net PML Pre-Tax Actual Occurrence

Heritage Insurance Holdings, Inc. NYSE:HRTG ✓ Reinsurance Structure Actual Both

Hilltop Holdings Inc. NYSE:HTH None

Horace Mann Educators Corporation NYSE:HMN Reinsurance Structure Actual Occurrence

Insurance Australia Group Limited ASX:IAG ✓ ✓ 1000yr Net PML Pre-Tax Target Aggregate

17 Proprietary & ConfidentialCatastrophe Risk Tolerance - Public Disclosure

P&C Personal Lines Sector (2 of 2) Metric Disclosures

Aggregate/

Company Ticker 100yr 200yr 250yr Other RPs (List) Risk Quantification Metric Pre- or Post-Tax Actual/ Target Occurrence

Intact Financial Corporation TSX:IFC 500yr Reinsurance Structure Actual Aggregate

Kemper Corporation NYSE:KMPR Reinsurance Structure Actual Both

Kingstone Insurance Company NASDAQ:KINS ✓ Net PML Pre-Tax Target Occurrence

MAPFRE SA MAD:MAP None

Mercury General Corporation NYSE:MCY Reinsurance Structure Actual Occurrence

National General Holdings Corporation NASDAQ:NGHC Reinsurance Structure Actual

NI Holdings, Inc NASDAQ:NODK Reinsurance Structure Actual Occurrence

Progressive Corporation NYSE:PGR Reinsurance Structure Actual Aggregate

Royal & Sun Alliance Insurance Plc LSE: RSA ✓ Reinsurance Structure Actual Occurrence

Safety Insurance Group, Inc. NASDAQ:SAFT ✓ 135 yr Net PML Post-Tax Actual Occurrence

State Auto Financial Corporation NASDAQ:STFC Reinsurance Structure Actual Occurrence

United Insurance Holdings Corp. NASDAQ:UIHC Reinsurance Structure Actual Aggregate

Universal Insurance Holdings, Inc. NYSE:UVE ✓ Reinsurance Structure Actual Occurrence

Vienna Insurance Group AG WBAG:VIG Reinsurance Structure Actual Occurrence

18 Proprietary & ConfidentialCatastrophe Risk Tolerance - Public Disclosure

P&C Specialty Lines Sector (1 of 2) Metric Disclosures

Aggregate/

Company Ticker 100yr 200yr 250yr Other RPs (List) Risk Quantification Metric Pre- or Post-Tax Actual/ Target Occurrence

American Financial Group, Inc. NYSE:AFG ✓ ✓ 500yr Net PML Pre-Tax Actual Occurrence

Amerisafe, Inc. NASDAQ:AMSF Reinsurance Structure Actual

ARCH Capital Group, Ltd. NASDAQ:ACGL ✓ Net PML Pre-Tax Target Occurrence

Argo Group International Holdings, Ltd. NYSE:ARGO None

Assurant, Inc. NYSE:AIZ Reinsurance Structure Actual Occurrence

Beazley Plc LSE:BEZ ✓ Net PML Pre-Tax Actual Occurrence

CV Starr - None

Employers Holdings, Inc. NYSE:EIG Reinsurance Structure Actual Occurrence

First Acceptance Corporation OTCQX:FACO None

Global Indemnity Plc NASDAQ:GBLI Reinsurance Structure Actual Occurrence

Hallmark Financial Services, Inc. NASDAQ:HALL Reinsurance Structure Actual Aggregate

Hiscox Limited LSE:HSX ✓ ✓ ✓ Net PML Pre-Tax Target Occurrence

James River Group Holdings, Ltd. NASDAQ:JRVR 1000yr Net PML Pre-Tax Target

19 Proprietary & ConfidentialCatastrophe Risk Tolerance - Public Disclosure

P&C Specialty Lines Sector (2 of 2) Metric Disclosures

Aggregate/

Company Ticker 100yr 200yr 250yr Other RPs (List) Risk Quantification Metric Pre- or Post-Tax Actual/ Target Occurrence

Kingsway Financial Services Inc. NYSE:KFS None

Lancashire Holdings Limited LSE:LRE ✓ ✓ Net PML Pre-Tax Actual Occurrence

Markel Corporation NYSE:MKL None

Palomar Holdings, Inc. NASDAQ:PLMR ✓ Net PML Pre-Tax Actual Occurrence

ProSight Global, Inc. NYSE:PROS Reinsurance Structure Actual Occurrence

RLI Corp. NYSE:RLI ✓ Net PML Pre-Tax Actual Occurrence

Sampo Plc - Reinsurance Structure Actual Occurrence

State National Companies Inc. - None

Suncorp Group Limited ASX:SUN Reinsurance Structure Actual Aggregate

Topdanmark A/S CPSE:TOP Reinsurance Structure Actual Occurrence

Unico American Corporation NASDAQ:UNAM Reinsurance Structure Actual Aggregate

United Fire Group, Inc. NASDAQ:UFCS Reinsurance Structure Actual Occurrence

W. R. Berkley Corporation NYSE:WRB Reinsurance Structure Actual Occurrence

White Mountains Insurance Group, Ltd. NYSE:WTM None

20 Proprietary & ConfidentialCatastrophe Risk Tolerance - Public Disclosure

P&C Reinsurance Sector Metric Disclosures

Aggregate/

Company Ticker 100yr 200yr 250yr Other RPs (List) Risk Quantification Metric Pre- or Post-Tax Actual/ Target Occurrence

Alleghany Corporation NYSE:Y ✓ ✓ Net PML Post-Tax Actual Occurrence

AXIS Capital Holdings Limited NYSE:AXS ✓ ✓ 50yr Net PML Pre-Tax Actual Both

Berkshire Hathaway Inc. NYSE:BRK.B Other Pre-Tax Target Aggregate

China Reinsurance (Group) Corporation SEHK:1508 Other

Everest Re Group, Ltd. NYSE:RE ✓ ✓ 20yr, 50yr, 500yr, 1000yr Net PML Pre-Tax Target Occurrence

Greenlight Capital Re, Ltd. NASDAQ:GLRE ✓ Net PML Pre-Tax Actual Aggregate

Hannover Rück SE XETRA:HNR1 ✓ ✓ ✓ Net PML Pre-Tax Target Aggregate

Maiden Holdings, Ltd. NASDAQ:MHLD None

Münchener Rückversicherungs -Gesellschaft AG XETRA:MUV2 ✓ Net PML Pre-Tax Actual Occurrence

Partner Re - ✓ 500yr Net PML Pre-Tax Actual Occurrence

RenaissanceRe Holdings Ltd. NYSE:RNR None

SCOR SE ENXTPA:SCR ✓ Net PML Pre-Tax Actual Occurrence

SiriusPoint Ltd.. NYSE:SPNT None

Swiss Re Limited SWX:SREN ✓ Net PML Pre-Tax Actual Occurrence

Watford Holdings Ltd. NASDAQ:WTRE ✓ Net PML Pre-Tax Actual Occurrence

21 Proprietary & ConfidentialSection 4:

Risk Tolerance Summary

22 Proprietary & Confidential

Proprietary & ConfidentialCatastrophe Risk Tolerance - Public Disclosure

P&C Commercial Lines Sector (1 of 5)

Disclosed Risk Tolerance

Actual/ 1:100 1:200 1:250 Summary Source Date

Company Ticker Target

Allianz Group XETRA :ALV N/A - - - The top three perils contributing to the natural catastrophe risk as of 31 December 2020 Allianz Group 2020 12/31/2020

were: windstorms in Europe, floods in Germany, and earthquakes in Australia. Annual Report, Risk

Management

Section, Page100

American International Group, NYSE :AIG Actual 1.9% - 7.3% For 100-year return period scenario, Occurrence Exceedance Probability (OEP) losses are American 12/31/2020

Inc. $1.31B (net of 2020 reinsurance, pretax) for US Hurricane and $0.563B for Japanese Wind. International Group

For 250-year return period scenario, Occurrence Exceedance Probability (OEP) losses are 2020 10-K Filing,

$4.901B (net of 2020 reinsurance, pretax) for World-wide all peril, $1.240B (net of 2020 Natural Catastrophe

reinsurance, pretax) for US Earthquake and $0.608B for Japanese Earthquake. Total Risk section, Page

Shareholders equity as of 12/31/2020 is $67.199bn. 178

Chubb Limited NYSE :CB Actual 6.7% - 11.1% Their modeled annual aggregate pre-tax probable maximum loss (PML), net of reinsurance, Chubb limited 2020 12/31/2020

for 100-year return period for U.S. hurricane and California earthquake at December 31, 10-K Filing,

2020, is 4.6% and 2.2% of the total shareholders' equity, respectively and for 250-year Catastrophe

return period for U.S. hurricane and California earthquake, PML is 8.3% and 2.5% of the Management

total shareholders' equity, respectively. Section, Page 119

Cincinnati Financial NASDAQ Actual 1.5% - 3.7% We use the Risk Management Solutions (RMS) and Applied Insurance Research (AIR) Cincinnati Financial 12/31/2020

Corporation :CINF models to evaluate exposures to a once-in-a-100-year and a once-in-a-250- year event to Corp 2020 10-K

help determine appropriate reinsurance coverage programs. In conjunction with these Filing, Reinsurance

activities, we also continue to evaluate information provided by our reinsurance broker. (Net Programs section,

PML for 1:50 Year, 1:100 Year, 1:250 Year and 1:500 based upon RMS is 1.3%,1.5%, Page 110

3.7% and 6.8% of total equity and based upon AIR is 1.3%, 1.5%, 2.6% and 5.1% of total

equity). Shareholders Equity as of 12/31/2020: $9.86 bn). Net losses are net of reinsurance

and income tax.

Information in red is disclosed on a post-tax basis

23 Proprietary & ConfidentialCatastrophe Risk Tolerance - Public Disclosure

P&C Commercial Lines Sector (2 of 5)

Disclosed Risk Tolerance

Actual/ 1:100 1:200 1:250 Summary Source Date

Company Ticker Target

CNA Financial Corporation NYSE Actual - - - We purchased corporate catastrophe excess-of-loss treaty reinsurance covering our U.S. states and CNA Financial 12/31/2020

:CNA territories and Canadian property exposures underwritten in our North American and European Corporation , 2020 10

companies. Exposures underwritten through Hardy are excluded. The treaty has a term of May 1, K Filing, Catastrophe

2020 to May 1, 2021 and provides coverage for the accumulation of covered losses from catastrophe and Reinsurance

occurrences above our per occurrence retention of $250 million up to $1.2 billion. Losses stemming Section, Page 23

from terrorism events are covered unless they are due to a nuclear, biological or chemical attack. All

layers of the treaty provide for one full reinstatement.(Shareholders Equity as of 12/31/2020 is

$12.707bn)

Direct Line Insurance Group Plc LSE Actual - 4.3% - Catastrophe reinsurance to protect against an accumulation of claims arising from a natural perils Direct Line Insurance 12/31/2020

:DLG event. The retained deductible is £130 million, and cover is placed annually on 1 July up to a Group Plc 2020

modelled 1-in-200-year loss event of £1,125 million.(Shareholders Equity as of 12/31/2020 is £3046.2 Annual report ,

million) Reinsurance section,

Page 32

Fairfax Financial Holdings TSX Target - - 15.0% The company’s objective is to limit its company -wide catastrophe loss exposure such that one year’s Fairfax Financial 2020 12/31/2020

Limited :FFH aggregate pre-tax net catastrophe losses would not exceed one year’s normalized net earnings Annual Report,

before income taxes. The company takes a long term view and generally considers a 15% return on Catastrophe Risk

common shareholders’ equity, adjusted to a pre-tax basis, to be representative of one year’s section, Page 113

normalized net earnings. The modeled probability of aggregate catastrophe losses in any one year

exceeding this amount is generally more than once in every 250 years.

Liberty Mutual Holding Company - Actual - - - The Company has property catastrophe reinsurance coverage for its domestic business and certain Liberty Mutual Holding 12/31/2020

Inc. specialty operations including: 1) hurricanes and earthquake reinsurance covering a substantial Company Inc. FIN

portion of $3,300 of loss in excess of $300 of retained loss in the United States, Canada and the SUPP_2020-12-31 -

Caribbean, excluding certain reinsurance exposures; 2) aggregate excess of loss programs; and 3) Page: 30

quota share reinsurance programs. These programs are structured to meet the Company’s

established tolerances under its Enterprise Risk Management Program.

24 Proprietary & ConfidentialCatastrophe Risk Tolerance - Public Disclosure

P&C Commercial Lines Sector (3 of 5)

Disclosed Risk Tolerance

Actual/ 1:100 1:200 1:250 Summary Source Date

Company Ticker Target

MS&AD Insurance Group TSE Actual - - - As of 3/31/2021, MS has catastrophe reserves of JPY 580.4 B (USD 5.32 B ) and AD has catastrophe MS&AD 2020 3/31/2021

Holdings, Inc. :8725 reserves of JPY 331B (USD 3.03 B). MS has catastrophe risk of JPY 100.6 B (USD 0.92 B) and AD Supplement Report,

has catastrophe risk of JPY 71 B (USD 651.7 M) . page 26

As of 03/31/2021, MS&AD's risk amounted to JPY2.3Tn (USD 21.10 B ) calculated as 99.5% VaR. MS&AD: FY2020

[Stockholders Equity as of 03/31/2021 is JPY 3,126.65 bn (USD 28.27 B)] Second Information

Meeting, page 12

Old Republic International Co NYSE N/A - - - No risk tolerance metrics indicated N/A N/A

:ORI

QBE Insurance Group Limited ASX: Actual - - - QBE uses reinsurance mainly for reducing volatility of capital and performance metrics. With some QBE Insurance Group 11/3/2021

QBE exceptions, QBE’s outwards reinsurance purchasing is centralized within Equator Re, the group’s 2020 AMB Report,

reinsurance captive. In line with the group's strategy to de-risk the portfolio, the group's 2019 Reinsurance Section,

structure provided higher protection from catastrophe and large losses, with material reduction in Page 10

probable maximum losses. In particular, the group reduced its retention and increased the

catastrophe protection limit. The group also maintains an aggregate cover for protection from high

occurrence of medium-sized events. Further revisions were made with the 2020 reinsurance

placement, and, At the 2021 renewal, the group increased its main catastrophe tower limit to USD 3.4

billion (2020: USD 3.3 billion), while refining areas including retention for certain non -peak peril

exposures. With the placement of the 2021 structure, QBE also announced an increased net

catastrophe allowance of USD 685 million (2020: USD 550 million), to reflect recent heightened

catastrophe experience.

Selective Insurance Group, Inc. NASDAQ:SIGI Actual 1.0% 2.0% 5.0% Our current catastrophe reinsurance program exhausts at an approximately 1 in 220 -year return Selective Insurance 12/31/2020

period, or events with 0.5% probability, based on a multi -model view of hurricane risk. 1.0% of equity Group 2020 10-K

after tax for 1:100-year event (OEP: 1%); 2% of equity after tax for 1:200-year event (OEP: 0.5%); 5% Filing, page 112

of equity after-tax for 1:250-year event (OEP: 0.4%) Shareholders Equity as of 12/31/2020: $2.74 bn

25 Proprietary & ConfidentialCatastrophe Risk Tolerance - Public Disclosure

P&C Commercial Lines Sector (4 of 5)

Disclosed Risk Tolerance

Actual/ Target 1:100 1:200 1:250 Summary Source Date

Company Ticker

Sompo Japan Nipponkoa TSE:863 Actual - - - As of 3/31/2021, SOMPO Holdings has catastrophe reserves of JPY 497.5 B (USD 4.57 B ) and Summary of Consolidated 3/31/2021

Holdings, Inc. 0 major catastrophe risk of JPY 172.37B (USD 1.57B) Financial Results for the

As of 3/31/2021, SOMPO Holdings' risk amounted to JPY 1.3 Tn (USD11.93B ) calculated as fiscal year ended March 31,

99.5% VaR. [Stockholders Equity as of 03/31/2021 is JPY 2,031.16 bn (USD18.36 B )] 2021, page 13, Highlights of

FY2020 Results _ Sompo

Holdings, Inc. - page 49

Talanx AG XETRA Actual - 15.3% - The estimates for the 200-year net loss burdens for the Group are as follows: Atlantic HU - EUR Talanx Group 2020 Annual 12/31/2020

:TLX 2,6026; US EQ - EUR 2,261M; EU WS - EUR 1,187M; Asia Pacific EQ (Japan also included) - Report, Reserving Risk -

EUR 1,596M; Central and South-American EQ - EUR 1,525; EU EQ- EUR 1,112M; EU flood- EUR Concentration risk Section,

988.(Total Shareholders Equity as of 12/31/2020 is EUR 17,125M). Page 112

The Hartford Financial Services NYSE Target - - 15.0% The estimated pre-tax loss for a 1 in 250 single event net of reinsurance is less than 15% of Hartford 2020 10-K Filing, 12/31/2020

Group, Inc. :HIG statutory surplus of the P&C operations. The estimated 250-year pre-tax probable maximum loss Natural catastrophe risk

from earthquake events is estimated to be $1.2 Billion before reinsurance and $0.6 billion net of section , Page 169

reinsurance. The estimated 250-year pre-tax probable maximum losses from hurricane events are

estimated to be $1.8 billion before reinsurance and $0.9 billion net of reinsurance. (Stockholders

Equity as of 12/31/2020 is $18,556 mn)

Tokio Marine Holdings, Inc. TSE:876 Actual - - - As of 12/31/2020, Tokio Marine Holdings, Inc. has catastrophe reserve of JPY 1023.3 Bn (USD Tokio Marine Solvency 12/31/2020

6 9.39 B ) and catastrophe risk of JPY 271.9 Bn (USD 2.49 B) margin ratio on a

The model based on 99.95% VaR is continued to be used for risk calculation. [Stockholders Equity consolidated basis as of

as of 12/31/2020 is JPY 3601.3 bn (USD 34.89 B)] December 31, 2020 , page 1

Tokio Marine Group FY2020

Results and FY2021 Profits,

page 32

26 Proprietary & ConfidentialCatastrophe Risk Tolerance - Public Disclosure

P&C Commercial Lines Sector (5 of 5)

Disclosed Risk Tolerance

Actual/ Target 1:100 1:200 1:250 Summary Source Date

Company Ticker

Travelers Companies, Inc. NYSE: Actual 5.8% - 7.9% Net, after-tax single U.S. hurricane 1:100 is 5.8% and 1:250 is 7.9% while Net, after tax Travelers 2020 10-K 12/31/2020

TRV single U.S. and Canadian EQ 1:100 is 2.7% and 1:250 is 4.1% (Total Shareholders Filing, Catastrophe

Equity as at 12/31/2020 : $29.2 bn) Modeling Section, Page

90

Zurich Insurance Group Ltd. SWX: Actual - - - N/A Zurich Financial Services 12/31/2020

ZURN 2020 Annual Report, Risk

Review Section, Page 145

27 Proprietary & ConfidentialCatastrophe Risk Tolerance - Public Disclosure

P&C Personal Lines Sector (1 of 10)

Disclosed Risk Tolerance

Actual/ 1:100 1:200 1:250 Summary Source Date

Company Ticker Target

The Allstate Corporation NYSE Target 6.6% - - Our current catastrophe reinsurance program supports our risk tolerance framework that Allstate Corp 2020 12/31/2020

:ALL targets less than a 1% likelihood of annual aggregate catastrophe losses from hurricanes and 10-K Filing, Allstate

earthquakes, net of reinsurance, exceeding $2 billion. The use of different assumptions and Protection pricing

updates to industry models and to our risk transfer program could materially change the and risk

projected loss. Growth strategies include areas where we believe diversification can be management

enhanced and an appropriate return can be earned for the risk. As a result, our modeled strategies, Page 8

exposure may increase, but in aggregate remain lower than $2 billion as noted above. In

addition, we have exposure to other severe weather events and wildfires, which impact

catastrophe losses. Shareholders Equity as of 12/31/2020 $30.217bn

Assicurazioni Generali SpA MIL:G N/A - - - Generali has centralized the program in recent years and is consistent with the group's risk Assicurazioni 12/31/2020

appetite and limits. It's primarily designed to provide protection against natural catastrophe Generali S.P.A. AM

exposures through excess of loss treaties. The group's largest exposures are to earthquakes in Best Report A.M.

Italy, followed by European windstorms. Given the program's design and Generali's mix of Best # 085124, Page

business, retention is high, with the group traditionally retaining around 95% of GWP. the group 8, Assicurazioni

using both internal and third-party models to assess its exposure. protection in each territory Generali

designed in line with the geographical footprint; however minimum coverage requirement set at S.p.A._Other

250-y return period OEP Financials_2020-12-

31_English Page 56

Aviva Plc LSE:AV. Target - - 0.9% The Group purchases a Group-wide catastrophe reinsurance programme to protect against Aviva PLC 2020 12/31/2020

catastrophe losses up to a 1 in 250 - year return period. The total Group potential retained loss Annual Report, Risk

from its most concentrated catastrophe exposure peril (Northern Europe Windstorm) is Management

approximately £150 million on a per occurrence basis and £175 million on an annual aggregate Section, Page 241

basis. Any losses above these levels are covered by the group -wide catastrophe reinsurance

programme to a level in excess of a 1 in 250- year return period. (Shareholders Equity as of

12/31/2020 is £20,560 million)

28 Proprietary & ConfidentialCatastrophe Risk Tolerance - Public Disclosure

P&C Personal Lines Sector (2 of 10)

Disclosed Risk Tolerance

Actual/ 1:100 1:200 1:250 Summary Source Date

Company Ticker Target

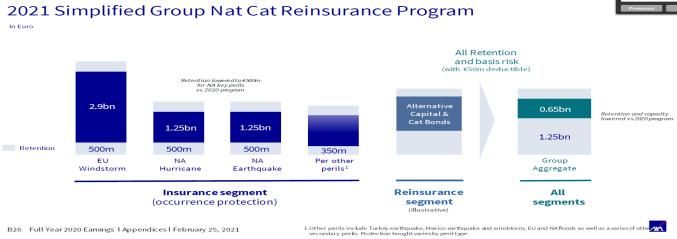

AXA SA ENXTPA:CS Actual - - - 2021 Simplified Group Nat Cat Reinsurance Program ; Retention lowered to €500m for NA AXA SA IP Full Year 12/31/2020

key perils vs 2020 program 2020 Earnings,

Page 26

Donegal Group Inc. NASDAQ:DGI Actual - - - catastrophe reinsurance, under which Donegal Mutual and our insurance subsidiaries Donegal Insurance 12/31/2020

CA recovered, through a series of reinsurance agreements, 100% of an accumulation of many Group 2020 10-K

losses resulting from a single event, including natural disasters, over a set retention of Filing, Reinsurance -

$15.0 million up to aggregate losses of $185.0 million per occurrence. Unaffiliated

Reinsurer Section,

Page 27

Echelon Financial Holdings TSX:EFH Actual - - - During 2020, the Company followed the policy of underwriting and reinsuring contracts of 2020 Consolidated 12/31/2020

Inc. insurance, which limits the net exposure of the Company to a maximum amount on any one Financial

loss to $1,000 (2019 – $1,000) for auto and liability and $500 (2019- $500) for property. In Statements, Echelon

addition, the Company obtained catastrophe reinsurance which limits the loss from a series Financial Holgings,

of claims arising from a single occurrence to $1,000 (2019 – $1,000), to a maximum Underwriting Policy

coverage of $35,000 (2019 – $30,000) & Reinsurance

Ceded section,

Page 25

29 Proprietary & ConfidentialCatastrophe Risk Tolerance - Public Disclosure

P&C Personal Lines Sector (3 of 10)

Disclosed Risk Tolerance

Actual/ 1:100 1:200 1:250 Summary Source Date

Company Ticker Target

Erie Indemnity Company NASDAQ:ERIE Actual - - - For casualty risks, the maximum net retention per risk is $12.0 million, which includes underlying A.M. Best Credit 7/10/2020

and umbrella policies. Facultative reinsurance is purchased for any umbrella policy with limits in Report (4283) Page 9

excess of $12.0 million. For property risks, the maximum net retention per risk is $25.0 million.

Facultative reinsurance is purchased for any property exposure greater than $25.0 million per risk.

Effective January 1, 2020, property catastrophe reinsurance provides total coverage in four layers

of $540 million excess of $400 million retention. The first layer provides coverage of 35% of $100

million excess of $400 million retention; the second layer provides coverage of 100% of $300

million excess of $500 million; the third layer provides coverage of 60% of $300 million excess of

$800 million and the fourth layer provides coverage of 100% of $25 million excess $1.1 billion.

Federated National Holding NASDAQ:FNH Actual 15.0% - - The Company's catastrophe reinsurance program shall have a U.S. dollar maximum retention per Federated National 12/31/2020

Company C Catastrophe Event, in connection with the 1:100 and 1:50 levels no greater than 15% of the Holdings Company

Company's Consolidated Capital (Stockholders Equity as of 12/31/2020 is $158.160 mn) 2020 10-K Filing,

Reinsurance

Programs Section,

Page 77, FedNat

Holding Company -

8K - FNHC - page 50

Hanover Insurance Group, Inc. NYSE: Actual - - - The property catastrophe occurrence program provides coverage, on an occurrence basis, up to Hanover Insurance 12/31/2020

THG $1.1 billion countrywide, less a $200 million retention, with no co -participation, for all defined perils. Group 2020 10-K

For occurrences from $1.1 billion to $1.3 billion, we have coverage for 33% of losses. Additionally, Filing, page 12

there is a program feature which provides coverage in excess of $300 million in aggregate

catastrophe losses. This feature provides $75 million of coverage, subject to 24% coparticipation,

that may respond either to an event that exceeds $1.1 billion or to events in excess of $300 million

in aggregate catastrophe losses. The catastrophe losses subject to the aggregate feature are

limited only to those events that exceed $7.5 million of incurred losses per event and have a per

occurrence limit of $200 million.

30 Proprietary & ConfidentialCatastrophe Risk Tolerance - Public Disclosure

P&C Personal Lines Sector (4 of 10)

Disclosed Risk Tolerance

Actual/ 1:100 1:200 1:250 Summary Source Date

Company Ticker Target

HCI Group Inc. NYSE: Actual 8.0% - - 2020-2021 Reinsurance Program provides 1st event cover for RMS v18 Long-Term HCI Group Inc. 3/5/2021

HCI Hurricane, with Loss Amplification, excluding Storm Surge, without Secondary Uncertainty Investor

with $16M Retention, exhaustion of $1400M and limit of $1384M ($1400-$16M). They also Presentation March

have limits for different events of 1 in 320-year event ($1400M), 1 in 260-year event 2021, 2020-2021

($1240M), 1 in 100-year event ($709M). They provide 2nd event cover for Florida Hurricane Reinsurance

Catastrophe Fund (FHCF) they also have limits for different events of , 1 in 50-year event Program Section,

($418M), , 1 in 127-year event ($280M). (Stockholders Equity as of 12/31/2020 is $201.136 Page 14

mn)

Heritage Insurance Holdings, NYSE: Actual - - - The reinsurance program, which is segmented into layers of coverage, protects the Heritage Insurance 12/31/2020

Inc. HRTG Company for excess property catastrophe losses and loss adjustment expenses. The 2020- Holdings Inc. 2020

2021 reinsurance program provides first event coverage up to $1.35 billion for Heritage 10-K Filing,

P&C, first event coverage up to $965.0 million for NBIC, and first event coverage up to Products and

$690.0 million for Zephyr. Our first event retention in a 1 in 100-year event would include distribution Section,

retention for the respective insurance company as well as any retention by Osprey. The first Page 106

event maximum retention up to a 1 in 100-year event for each insurance company

subsidiary is as follows: Heritage P&C – $20.0 million; Zephyr – $20.0 million; NBIC – $13.3

million. In a 1-to-100-year event and including Osprey’s retention, the range of loss

depending upon the geographic region affected would be between an additional $22.1

million to $41.8 million above the amounts noted for the insurance company retentions. The

Company's estimated net cost for the 2020-2021 catastrophe reinsurance programs is

approximately $272.1 million.

Hilltop Holdings Inc. NYSE: N/A - - - No risk tolerance metrics indicated N/A N/A

HTH

31 Proprietary & ConfidentialCatastrophe Risk Tolerance - Public Disclosure

P&C Personal Lines Sector (5 of 10)

Disclosed Risk Tolerance

Actual/ 1:100 1:200 1:250 Summary Source Date

Company Ticker Target

Horace Mann Educators NYSE: Actual - - - The Company maintains catastrophe excess of loss reinsurance coverage. For 2020, the Horace Mann 2020 12/31/2020

Corporation HMN Company's catastrophe excess of loss coverage consisted of one contract in addition to a 10-K Filing, Property

minimal amount of coverage by the Florida Hurricane Catastrophe Fund (FHCF). The & Casualty

catastrophe excess of loss contract provided 95% coverage for catastrophe losses above a Reinsurance

retention of $25.0 million per occurrence up to $175.0 million per occurrence. This contract Section, page 11,

consisted of three layers, each of which provided for one mandatory reinstatement. The 135

layers were $25.0 million excess of $25.0 million, $40.0 million excess of $50.0 million and

$85.0 million excess of $90.0 million. Our 2021 catastrophe excess of loss reinsurance

coverage is unchanged from 2020.

Insurance Australia Group ASX: Target - - 7.7% The ReMS outlines IAG's reinsurance principles, including the requirement that Insurance Australia 6/30/2020

Limited IAG reinsurance retention for catastrophe must not exceed 4% of gross earned premium. IAG Group 2020 Annual

purchases catastrophe reinsurance protection to at least the greater of a 1-in-250 - year Report, Reinsurance

return period for earthquake loss calculated on a whole-of-portfolio basis for Australia; and risk section, Page

a 1-in-1000 - year return period for earthquake loss calculated on a whole-of-portfolio basis 76

for New Zealand. This is a more conservative view than APRA’s prescribed minimum

approach of 1-in-200-year return period loss calculated on a whole-of-portfolio, all perils

basis. a Group catastrophe reinsurance protection that runs to a calendar year and

operates on an excess of loss basis, with IAG retaining the first $250 million ($169 million

post-quota share) of each loss. It covers all territories in which IAG operates. The limit of

catastrophe cover purchased effective 1 January 2020 was $9.75 billion placed to 67.5%

(i.e., net of the whole-of account quota share). Should a loss event occur that is greater

than $10 billion, (Shareholders Equity as of 6/30/2020 is AUD 6,354million)

32 Proprietary & ConfidentialCatastrophe Risk Tolerance - Public Disclosure

P&C Personal Lines Sector (6 of 10)

Disclosed Risk Tolerance

Actual/ 1:100 1:200 1:250 Summary Source Date

Company Ticker Target

Intact Financial Corporation TSX: Actual - - - For multi-risk events and catastrophes, the Company retains participations averaging 10.2% as at Intact Financial corp 12/31/2020

IFC December 31, 2020 (5.5% as at December 31, 2019) on reinsurance layers between the retention 2020 Annual Report,

and coverage limit. The coverage limit prudently exceeds the Company's risk assessment of an Reinsurance section,

earthquake in Western Canada at a 1-in-500-year return period. Effective January 1, 2021, the Page 167,66

Company maintained its coverage limits but increased the retention to $150 million and retains

participations averaging 9.2% on

reinsurance layers between the retention and coverage limit. The coverage limits are well in

excess of the regulatory requirements with respect to the earthquake risk. As at December 31,

2020, we retain participations averaging 10.2% on reinsurance layers between the retention and

coverage limit. Effective January 1, 2021, we maintained our coverage limit of $5.3 billion for multi-

risk events and catastrophes but increased the retention from $100 million to $150 million. For

2021, we retain participations averaging 9.2% on reinsurance layers between the retention and

coverage limit.

Kemper Corporation NYSE:KMPR Actual - - - Coverage for the property and casualty group's catastrophe reinsurance program is provided by Kemper P&C Group 1/28/2021

three multi-year excess of loss reinsurance contracts, one annual excess of loss reinsurance AM Best Report #914,

contract, and an annual aggregate excess property catastrophe reinsurance contract. In total, the Reinsurance Section -

excess of loss insurance contracts cover 95% of $225.0M in excess of $50.0M in various layers. Page 8, 2020 10-K

The aggregate property catastrophe reinsurance contract provides coverage for accumulated Filing - Page 15

property catastrophe losses of $50.0M in excess of $60.0M on losses arising out of one or more of

the following perils from storms or storm systems that are not named storms: (1) windstorm, (2)

hail, (3) tornado, and (4) fire, including ensuing collapse and water damage. The first multi -year

excess of loss reinsurance contract provides coverage over the three-year period of January 1,

2019 through December 31, 2021 (the “2019 Reinsurance Contract”). The 2019 Reinsurance

Contract provides coverage in two layers, which together provide coverage for losses on individual

catastrophes of $200 million in excess of $50 million. Under the 2019 Reinsurance Contract, the

percentage of coverage is 31.66% for each year in the three-year period, and participation of each

reinsurer remains the same over the entire three-year period. Accordingly, the 2019 Reinsurance

Contract provides coverage for 31.66% of losses on individual catastrophes of $200 million in

excess of $50 million in 2021.

33 Proprietary & ConfidentialCatastrophe Risk Tolerance - Public Disclosure

P&C Personal Lines Sector (7 of 10)

Disclosed Risk Tolerance

Actual/ 1:100 1:200 1:250 Summary Source Date

Company Ticker Target

Kingstone Insurance Company NASDAQ:KINS Target 6.1% - - In 2020, we purchased catastrophe reinsurance to provide coverage of up to $485,000,000 for losses Kingstone Insurances 12/31/2020

associated with a single event. One of the most commonly used catastrophe forecasting models 2020 10-K filing,

prepared for us indicates that the catastrophe reinsurance treaties provide coverage in excess of our Reinsurance Section,

estimated probable maximum loss associated with a single more than one -in-130- year storm event. Page 13,19,4,5

The direct retention for any single catastrophe event is $10,000,000. For the period December 15,

2019, through December 30, 2020, losses on personal lines policies were subject to the 25% quota

share treaty, which resulted in a net retention by us of $5,625,000 of exposure per catastrophe

occurrence. Effective July 1, 2020, we have reinstatement premium protection on the first

$70,000,000 layer of catastrophe coverage in excess of $10.000,000. This protects us from having to

pay an additional premium to reinstate catastrophe coverage for an event up to this level. Effective

July 1, 2020, KICO decreased the top limit of its catastrophe reinsurance coverage from

$610,000,000 to $485,000,000, which, at the time, equated to more than a 1 -in-130- year storm event

according to the primary industry catastrophe model that we follow. (Stockholders Equity as of

12/31/2020 is $92.8mn)

MAPFRE SA MAD: N/A - - - No risk tolerance metrics indicated N/A N/A

MAP

Mercury General Corporation NYSE: Actual - - - The Company is party to a Catastrophe Reinsurance Treaty ("Treaty") covering a wide range of perils Mercury 2020 10-K 12/31/2020

MCY that is effective through June 30, 2021. For the 12 months ending June 30, 2021, the Treaty provides Filing, Reinsurance

$717 million of coverage on a per occurrence basis after covered catastrophe losses exceed the $40 Section Page 18

million Company retention limit. The Treaty specifically excludes coverage for any Florida business

and for California earthquake losses on fixed property policies, such as homeowners, but does cover

losses from fires following an earthquake. In addition, the Treaty excludes losses from wildfires on

89.5% of certain coverage layers of the Treaty. For the 12 months ended June 30, 2020, the Treaty

provided $600 million of coverage on a per occurrence basis after covered catastrophe losses

exceeded the $40 million Company retention limit. The Treaty specifically excluded coverage for any

Florida business and for California earthquake losses on fixed property policies such as homeowners

but did cover losses from fires following an earthquake.

34 Proprietary & ConfidentialCatastrophe Risk Tolerance - Public Disclosure

P&C Personal Lines Sector (8 of 10)

Disclosed Risk Tolerance

Actual/ 1:100 1:200 1:250 Summary Source Date

Company Ticker Target

National General Holdings NASDAQ Actual - - - Effective May 1, 2020, with additional purchases made at June 1, 2020, and July 1, 2020, the National General 12/31/2020

Corporation :NGHC Company renewed its property catastrophe excess of loss program, protecting the Company against Holdings Corp 10K,

catastrophic events and other large losses. The program provides coverage up to $650,000 with one Page 205 Catastrophe

reinstatement and attaches at $70,000 for the first event and $50,000 for the second event. The Reinsurance

Company purchased additional first event coverage for named wind that attaches at $50,000. Effective

October 1, 2020, the Company’s casualty program provides $35,000 in coverage in excess of a $5,000

retention. Effective July 1, 2020, the Reciprocal Exchanges’ property catastrophe excess of loss

program provided coverage up to $475,000 with a $20,000 retention, and one reinstatement. Effective

July 17, 2020, the Company purchased an additional $125,000 of top layer coverage.

NI Holdings, Inc NASDAQ Actual - - - As a group, during the year ended December 31, 2020, the Company retained the first $10,000 of NI Holdings, Inc 10K, 12/31/2020

:NODK weather-related losses from catastrophic events and had reinsurance under various reinsurance Reinsurance Section -

agreements up to $97,000 in excess of its $10,000 retained risk. As a group, during the year ended Page 123

December 31, 2019, the Company retained the first $10,000 of weather-related losses from

catastrophic events and had reinsurance under various reinsurance agreements up to $74,600 in

excess of its $10,000 retained risk. For 2021, the catastrophe retention amount remains at $10,000

while the overall catastrophic reinsurance program limit increased to $117,000 in excess of the $10,000

retention.

Progressive Corporation NYSE Actual - - - On January 1, 2021, we entered into a new aggregate excess of loss program with three layers. The Progressive 12/31/2020

:PGR first layer has a retention threshold of $475 million and provides $75 million of coverage for catastrophe Corporation, 2020 10

losses and ALAE, except those from named storms (both hurricanes and tropical storms). The second K, Commitments and

layer has a retention threshold of $550 million and provides $50 million of coverage on losses and Contingencies section,

ALAE from both named and non-named storms. The third layer has a retention threshold of $600 page 9, 10

million and provides $100 million of coverage, which includes $95 million under the catastrophe bond,

on losses and ALAE from both named and non-named storms to the extent losses are in excess of the

coverages provided under the first two layers. Each layer is subject to a per occurrence $2 million

deductible before each loss could be considered for aggregate retention, and each event is subject to a

$98 million coverage cap. we have several multiple-layer property catastrophe reinsurance contracts

with various reinsurers with terms ranging from one to three years; the minimum commitment under

these agreements at December 31, 2020, was $191.1 million.

35 Proprietary & ConfidentialCatastrophe Risk Tolerance - Public Disclosure

P&C Personal Lines Sector (9 of 10)

Disclosed Risk Tolerance

Actual/ 1:100 1:200 1:250 Summary Source Date

Company Ticker Target

Royal & Sun Alliance Insurance Plc LSE: Actual - - - Our catastrophe reinsurance covers flood, windstorms, hurricanes, wildfires and other severe weather RSA Group 2020,Key 12/31/2020

RSA events, with special provisions providing additional protection for prolonged or greater frequency events. risks and mitigants

Our reinsurance program is designed to cover at least 1-in-200-yea r events and is optimized to mitigate the section, page 37,

impact of extreme weather. Our main Catastrophe retentions remain at £75m for the UK and Europe Earnings Release, Page

combined, £50m for Europe excluding the UK and $75m for Canada. 28

Safety Insurance Group, Inc. NASDAQ:SAFT Actual 20.0% - - For 2021, we have purchased the same four layers of excess catastrophe reinsurance providing $615,000 Safety Insurance Group 12/31/2020

of coverage for property losses in excess of $50,000 up to a maximum of $665,000. Our reinsurers’ co- 2020 10-K Filing,

participation is 50.0% of $50,000 for the 1st layer, 80.0% of $50,000 for the 2nd layer, 80.0% of $250,000 Reinsurance Section,

for the 3rd layer and 80% of $265,000 for the 4th layer. As a result of the changes to the models, our Page 29

catastrophe reinsurance in 2021 protects us in the event of a “135-year storm.” The FAIR Plan’s exposure to

catastrophe losses increased and as a result, the FAIR Plan decided to buy reinsurance to reduce their

exposure to catastrophe losses. On July 1, 2020, the FAIR Plan purchased $1,800,000 of catastrophe

reinsurance for property losses with retention of $100,000. A comprehensive catastrophe reinsurance

program reduces the net after-tax probable maximum loss (PML) expected to arise from a 100-year

hurricane event to approximately 20% of reported policyholders' surplus at year-end 2020.

State Auto Financial Corporation NASDAQ:STFC Actual - - - Property Catastrophe Treaty Members of the State Auto Group maintain a property catastrophe excess of State Auto Financial 12/31/2020

loss reinsurance agreement, covering property catastrophe related events affecting at least two risks. This Corp. 2020 10-K Filing,

property catastrophe reinsurance agreement renewed as of July 1, 2020. Under this reinsurance Reinsurance

agreement, we retain the first $90.0 million of catastrophe loss, each occurrence, with a 5.0% co- Arrangements Section,

participation on the next $180.0 million of covered loss, each occurrence which is broken down into two page 87

layers of $70.0 million and $110.0 million. The reinsurers are responsible for 95.0% of the catastrophe

losses excess of $90.0 million up to $270.0 million, each occurrence. The State Auto Group is responsible

for catastrophe losses above $270.0 million. There is also an automatic reinstatement of the limit, for 100%

of the deposit premium. Property Per Risk Treaty As of April 1, 2020, the State Auto Group renewed the

property per risk excess of loss reinsurance agreement for a 15-month term. Under this reinsurance

agreement, the State Auto Group retains the first $4.0 million of covered loss, with a 19.5% co-participation

on the next $6.0 million of covered loss and a 14.0% co-participation on covered loss between $10.0 million

and $20.0 million. The reinsurers are responsible for 80.5% of the loss excess of the $4.0 million retention

up to $10.0 million and 86.0% of the loss excess of $10 million up to $20.0 million.

36 Proprietary & ConfidentialCatastrophe Risk Tolerance - Public Disclosure

P&C Personal Lines Sector (10 of 10)

Disclosed Risk Tolerance

Actual/ 1:100 1:200 1:250 Summary Source Date

Company Ticker Target

United Insurance Holdings Corp. NASDAQ:UIHC Actual - - - Our program includes excess of loss, aggregate excess of loss and quota share treaties. Our excess of loss United Insurance 12/31/2020

treaty, in effect from June 1, 2020 through May 31, 2021, provides coverage for catastrophe losses from named Holdings Corp 2020 10-

or numbered windstorms and earthquakes up to an exhaustion point of approximately $3,300,000,000. In K Filing, Reinsurance

addition to this treaty, we had an aggregate excess of loss treaty, effective January 1, 2020, which provided section, Page 134

coverage for all catastrophe perils other than hurricanes, tropical storms, tropical depressions and earthquakes.

We ceded $30,000,000 of catastrophe losses under this treaty for the year ended December 31, 2020. In

addition, we had an all other perils excess of loss treaty, effective January 1, 2020, which provided coverage for

all catastrophe perils other than hurricanes, tropical storms, tropical depressions, and earthquakes up to an

exhaustion point of approximately $110,000,000. The quota share agreements effective June 1, 2020 through

May 31, 2021, provide coverage for all catastrophe perils and attritional losses incurred by our insurance

subsidiaries UPC and FSIC, and were extended to cover ACIC effective December 31, 2020 through May 31,

2022 with an additional 8% coverage for UPC and FSIC. For all catastrophe perils, the quota share agreement

provides ground-up protection effectively reducing our retention for catastrophe losses. Finally, effective

December 31, 2020, we entered into a quota share reinsurance agreement with Homeowners Choice Property

and Casualty Insurance Company, Inc (HCP). Under the terms of this agreement, HCP will provide 69.5%

quota share reinsurance on in-force, new and renewal policies in Connecticut, Massachusetts, New Jersey,

and Rhode Island effective December 31, 2020, until June 1, 2021.

Universal Insurance Holdings, Inc. NYSE: Actual - - - Our 2020-2021 reinsurance program meets and provides reinsurance in excess of the FLOIR’s requirements, Universal Insurance 12/31/2020

UVE which are based on, among other things, the probable maximum loss that we would incur from an individual Holdings 2020 10-K

catastrophic event estimated to occur once in every 100 years, based on our portfolio of insured risks and a Filing, UPICC's

series of stress test catastrophe loss scenarios based on past historical events. UPCIC retains $43 million for Reinsurance Program,

First event All States and $15 million for First event Non-Florida retention. All States first event tower expanded Page 11,46

to $3.36 with no co-participation in any of the layers, no limitations on loss adjustment expenses and no

accelerated deposit premiums. Assuming a first event completely exhausts the $3.36 billion tower, the second

event exhaustion point would be $1.343 billion. (Stockholders Equity as of 12/31/2020 is $449.262 mn)

Vienna Insurance Group AG WBAG: Actual - - - It is Group-wide policy that no more than EUR 50 million for the first two natural disaster events and EUR 20 VIG 2020 Annual Report, 12/31/2020

VIG million for each additional event can be placed at risk on a PML (probable maximum loss) basis. The maximum Reinsurance Section,

Group-wide retention per individual loss is less than EUR 15 million. Page 127

37 Proprietary & ConfidentialYou can also read