CAPITAL ONE SECURITIES 15TH ANNUAL ENERGY CONFERENCE - December 2020

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

CAPITAL ONE SECURITIES 15TH ANNUAL ENERGY CONFERENCE December 2020

Forward-Looking Statements

This presentation contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 ("Securities Act"), Section 21E of the Securities Exchange Act of 1934 ("Exchange Act") and the United States

("U.S.") Private Securities Litigation Reform Act of 1995 regarding our business, financial condition, results of operations and prospects. All statements other than statements of historical fact included in and incorporated by

reference into this presentation are "forward-looking statements." Words such as expect, anticipate, intend, plan, believe, seek, estimate, schedule and similar expressions or variations of such words are intended to identify

forward-looking statements herein. Forward-looking statements include, among other things, statements regarding future: production, costs and cash flows; drilling locations, zones and growth opportunities; commodity prices

and differentials; capital expenditures and projects, including the number of rigs employed; cash flows from operations relative to future capital investments; our currently suspended stock repurchase program; financial ratios

and compliance with covenants in our revolving credit facility and other debt instruments; impacts of certain accounting and tax changes; timing and adequacy of infrastructure projects of our midstream providers and the related

impact on our midstream capacity and related curtailments; impacts of Colorado political matters; ability to meet our volume commitments to midstream providers; ongoing compliance with our consent decree; and our ability to

repay our 2021 Convertible Notes.

The above statements are not the exclusive means of identifying forward-looking statements herein. Although forward-looking statements contained in this release reflect our good faith judgment, such statements can only be

based on facts and factors currently known to us. Forward-looking statements are always subject to risks and uncertainties, and become subject to greater levels of risk and uncertainty as they address matters further into the

future. Throughout this presentation or accompanying materials, we may use the term “projection” or similar terms or expressions, or indicate that we have “modeled” certain future scenarios. We typically use these terms to

indicate our current thoughts on possible outcomes relating to our business or our industry in periods beyond the current fiscal year. Because such statements relate to events or conditions further in the future, they are subject

to increased levels of uncertainty.

Further, we urge you to carefully review and consider the cautionary statements and disclosures, specifically those under the heading "Risk Factors," made in our Quarterly Report on Form 10-Q, our Annual Report on Form 10-K

for the year ended December 31, 2019 filed with the U.S. Securities and Exchange Commission ("SEC") on February 26, 2020 (the "2019 Form 10-K"), our Quarterly Report on Form 10-Q for the quarter ended March 31, 2020 filed

with the SEC on May 8, 2020 (the "First Quarter 2020 Form 10-Q"), our Quarterly Report on Form 10-Q for the quarter ended June 30, 2020 filed with the SEC on August 6, 2020 (the "Second Quarter 2020 Form 10-Q") and our

other filings with the SEC for further information on risks and uncertainties that could affect our business, financial condition, results of operations and prospects, which are incorporated by this reference as though fully set forth

herein. We caution you not to place undue reliance on the forward-looking statements, which speak only as of the date of this presentation. We undertake no obligation to update any forward-looking statements in order to

reflect any event or circumstance occurring after the date of this presentation or currently unknown facts or conditions or the occurrence of unanticipated events. All forward-looking statements are qualified in their entirety

by this cautionary statement.

December 2020 2

Reconciliation of Non-U.S. GAAP Financial Metrics We use "adjusted cash flows from operations," "adjusted free cash flow (deficit)," "adjusted net income (loss)" and "adjusted EBITDAX," non-U.S. GAAP financial measures, for internal management reporting, when evaluating period-to-period changes and, in some cases, in providing public guidance on possible future results. In addition, we believe these are measures of our fundamental business and can be useful to us, investors, lenders and other parties in the evaluation of our performance relative to our peers and in assessing acquisition opportunities and capital expenditure projects. These supplemental measures are not measures of financial performance under U.S. GAAP and should be considered in addition to, not as a substitute for, net income (loss) or cash flows from operations, investing or financing activities and should not be viewed as liquidity measures or indicators of cash flows reported in accordance with U.S. GAAP. The non-U.S. GAAP financial measures that we use may not be comparable to similarly titled measures reported by other companies In the future, we may disclose different non-U.S. GAAP financial measures in order to help us and our investors more meaningfully evaluate and compare our future results of operations to our previously reported results of operations. We strongly encourage investors to review our financial statements and publicly filed reports in their entirety and to not rely on any single financial measure. Adjusted cash flows from operations and adjusted free cash flow (deficit). We believe adjusted cash flows from operations can provide additional transparency into the drivers of trends in our operating cash flows, such as production, realized sales prices and operating costs, as it disregards the timing of settlement of operating assets and liabilities. We believe adjusted free cash flow (deficit) provides additional information that may be useful in an investor analysis of our ability to generate cash from operating activities from our existing oil and gas asset base to fund exploration and development activities and to return capital to stockholders in the period in which the related transactions occurred. We exclude from this measure cash receipts and expenditures related to acquisitions and divestitures of oil and gas properties and capital expenditures for other properties and equipment, which are not reflective of the cash generated or used by ongoing activities on our existing producing properties and, in the case of acquisitions and divestitures, may be evaluated separately in terms of their impact on our performance and liquidity. Adjusted free cash flow is a supplemental measure of liquidity and should not be viewed as a substitute for cash flows from operations because it excludes certain required cash expenditures. For example, we may have mandatory debt service requirements or other non-discretionary expenditures which are not deducted from the adjusted free cash flow measure. We are unable to present a reconciliation of forward-looking adjusted cash flow because components of the calculation, including fluctuations in working capital accounts, are inherently unpredictable. Moreover, estimating the most directly comparable GAAP measure with the required precision necessary to provide a meaningful reconciliation is extremely difficult and could not be accomplished without unreasonable effort. We believe that forward- looking estimates of adjusted cash flow are important to investors because they assist in the analysis of our ability to generate cash from our operations. Adjusted net income (loss). We believe that adjusted net income (loss) provides additional transparency into operating trends, such as production, realized sales prices, operating costs and net settlements on commodity derivative contracts, because it disregards changes in our net income (loss) from mark-to-market adjustments resulting from net changes in the fair value of our unsettled commodity derivative contracts, and these changes are not directly reflective of our operating performance. Adjusted EBITDAX. We believe that adjusted EBITDAX provides additional transparency into operating trends because it reflects the financial performance of our assets without regard to financing methods, capital structure, accounting methods or historical cost basis. In addition, because adjusted EBITDAX excludes certain non-cash expenses, we believe it is not a measure of income, but rather a measure of our liquidity and ability to generate sufficient cash for exploration, development and acquisitions and to service our debt obligations. Beginning in the third quarter of 2019, we included a reconciling item for gains or losses on the sale of properties and equipment when calculating adjusted EBITDAX, thereby no longer including such gains or losses in our reported adjusted EBITDAX. We believe this methodology for calculating adjusted EBITDAX will enable greater comparability to our peers, as well as consistent treatment of adjustments for impairment and gains or losses on the sale of properties and equipment. For comparability, all prior periods presented have been conformed to the aforementioned methodology. December 2020 3

PDC Strategy Focused on Significant Value-Creation

Focus on Execution

Sustainable Adjusted Wattenberg Field

FCF(1) Generation Top Priorities in

161,000 Boe/d(2)

Demand Destruction

Through-the-Cycle World Delaware Basin

31,500 Boe/d(2)

Balance Sheet Strength

Committed to Corporate

Social Responsibility PDC Market Snapshot(3)

Nasdaq Symbol PDCE

Market Cap $1.7 billion

Modest Growth

On hold in Net Debt $1.7 billion

Demand Destruction Enterprise Value $3.4 billion

World

Consistent Returns Shares Outstanding 100 million

of Capital to Shareholders Total Liquidity ~$1.4 billion

(1) Adjusted FCF defined as net cash from operating activities, before changes in working capital, less oil & gas capital investments. See appendix for reconciliation.

December 2020 (2) Production = 3Q20; (3) Market cap, Enterprise Value, liquidity and shares outstanding as of 11/30/20. 4Third Quarter Results Emphasize Valuation Disconnect

3rd Quarter Highlights

Permit Update

• ~$280 million of net cash from operating activities

− Generated ~$225 million of adjusted free cash flow (FCF)(1) • 32 additional permits approved in September & October

− 3Q20 FCF represents ~15% of current market cap(2)

• Expect ~475 combined DUCs & approved permits at YE20

• ~$35 million capital investments • Anticipate more approved permits prior to year-end

− Operated one DJ drilling rig and resumed DJ completions in September

• Anticipate Mission Change rulemaking related to siting

requirements to be finalized in late November and effective

mid-January

• Paid down ~$215 million of debt in 3Q and additional

~$70 million in Oct.

− Represents nearly 10% current Enterprise Value(2)

• Continue to effectively drive down costs – LOE + G&A < $4 per Boe

− Synergies of SRC merger demonstrated through LOE of $2.11/Boe and G&A of $1.84/Boe

(1) Adjusted free cash flow (FCF) defined as net cash from operating activities, before changes in working capital, less oil & gas capital investments. See appendix for reconciliation.

December 2020 (2) Market cap and Enterprise Value as of 11/30/20 of ~$1,675 and ~$3,350, respectively. 5Resilient Balance Sheet with Strong Hedge Book

Liquidity Update

(as of September 30, 2020)

• Borrowing base and commitment level of $1.6 billion as of 10/31/20

(post-Fall redetermination in October 2020)

$2,000

• Borrowings under revolver of ~$285 million at 3Q Revolver

(Commitment Level)

− Paid down ~$215 million of debt in 3Q20

− Paid down an additional ~$70 million of debt in October

$1,500

• Liquidity of ~$1.4 billion

5.75%

Senior

$1,000 Notes

6.125% $750MM $150MM

Senior Tack-On

1.125%

Hedging Update $500 Convertible

Notes

$400MM 6.25%

(as of October 31, 2020) Notes Senior

$200MM $215MM Notes

• ~45% of 2021 crude hedged at $45.00 WA floor $100MM

• ~55% of 2021 nat. gas hedged at $2.45 WA floor $0

2020 2021 2022 2023 2024 2025 2026 2027 2028

Total Debt: ~$1.7 billion (as of 10/31/20)

December 2020 6Project Significant FCF at $35 Oil

• Capital investment range to $500 - $550 million 2020e Capital Investments

− Expect ~$110 million in 4Q (millions)

− Wattenberg – one rig and one completion crew planned

− Delaware – minimal planned activity through year-end

$1,000 - $1,100

$500 - $600

$500 - $550

• Anticipate FCF of more than $350 million(1)

2020e (February) 2020e (May) 2020e (August)

Net Oil Pricing Summary

• Full-year oil production of 64,000 – 68,000 Bbls/d and $/Bbl 2019 1Q20 2Q20 3Q20 4Q20e 2021e

total production of 175,000 – 185,000 Boe/d NYMEX Oil $57.03 $46.17 $27.85 $40.93 $35.00 $40.00

− Anticipate < 10% sequential decline in 4Q20 Deduct(2) ($3.77) ($3.86) ($9.22) ($3.44) ($3 - $4) ($2 - $4)

− Quarterly exit rates of ~175,000 Boe/d and ~60,000 Bbls/d Gross Realized (% of NYMEX) 93% 92% 67% 92% ~90% 90 – 95%

TGP ($1.24) ($1.46) ($1.87) ($3.00) ($3.00) ($2 - $4)

Realized Netback $52.01 $40.86 $16.76 $34.49 $28 - $29 $32 - $36

(1) Assumes 4Q20 pricing of $35/Bbl WTI, $2.50/Mcf NYMEX natural gas and NGL realizations of ~$10/Bbl. (2) Includes anticipated quality, roll and transport differentials, which

December 2020 vary by contract. 7Multi-Year Focus on Sustainable FCF Generation

All Numbers Approximate

2020 + 2021 Highlights Significant FCF Generation

(millions)

$350+

• Anticipate 2-year cumulative capital investments of

~$1.1 billion $300

$200

• ~$850 million of projected FCF between 2H19 and YE21

− Increase to initial SRC acquisition projections despite dramatic

decrease in pricing PDC Standalone

− Have generated FCF in 4 of the past 5 quarters $56.71/Bbl $35.00/Bbl (4Q) $40.00/Bbl

$2.36/Mcf $2.50/Mcf $2.75/Mcf

− Project ~400 million FCF over next 5 quarters on ~$650 million

capital investment 2H19 2020e 2021e

FCF Yield(2) ~20% ~20%

FCF/EV Yield(2) ~10% ~10%

• Balance sheet strength and low absolute debt level remains

top priority FCF Margin 66% 55%

− Better positioned for incremental, sustainable return-of- FCF Sensitivity

capital initiatives

Change 4Q20 2021

− 2020 Guidance and 2021 Outlook each reflect

re-investment rate below 70% at ~$40/Bbl oil +/- $2.50/Bbl WTI < $5 MM $35 MM

+/- $0.25/MMbtu Gas < $5 MM $15 MM

+/- $1.00/Bbl NGL < $5 MM $15 MM

(1) Assumes 4Q20 pricing of $35/Bbl WTI, $2.50/Mcf NYMEX natural gas and NGL realizations of ~$10/Bbl. 2021 pricing of $40/Bbl WTI, $2.75/Mcf NYMEX natural gas and NGL

December 2020 realizations of ~$10/Bbl. (2) Market cap and Enterprise Value as of 11/30/20. Debt balance of ~$1.7 billion. 8Commitment to Corporate Social Responsibility

Published Inaugural Sustainability Report in Alignment with SASB Standards

Responsible Environmental Social Corporate

Operations Stewardship Impact Governance

52% 84% 2,285 > 50%

Year-over-year decrease in Total Recordable Reduction in methane emissions per Boe Volunteer hours by PDC employees in 2019 Office-based employees that are women

Incident Rate since 2016 Energize Our Community Day

29 260,000 90 50%

Average hours of annual health and safety Reduced truckloads per year due to Organizations across four states that Board refreshment over the past five years

training for field employees increased oil and water piping received PDC donations

December 2020 9ASSET OVERVIEW

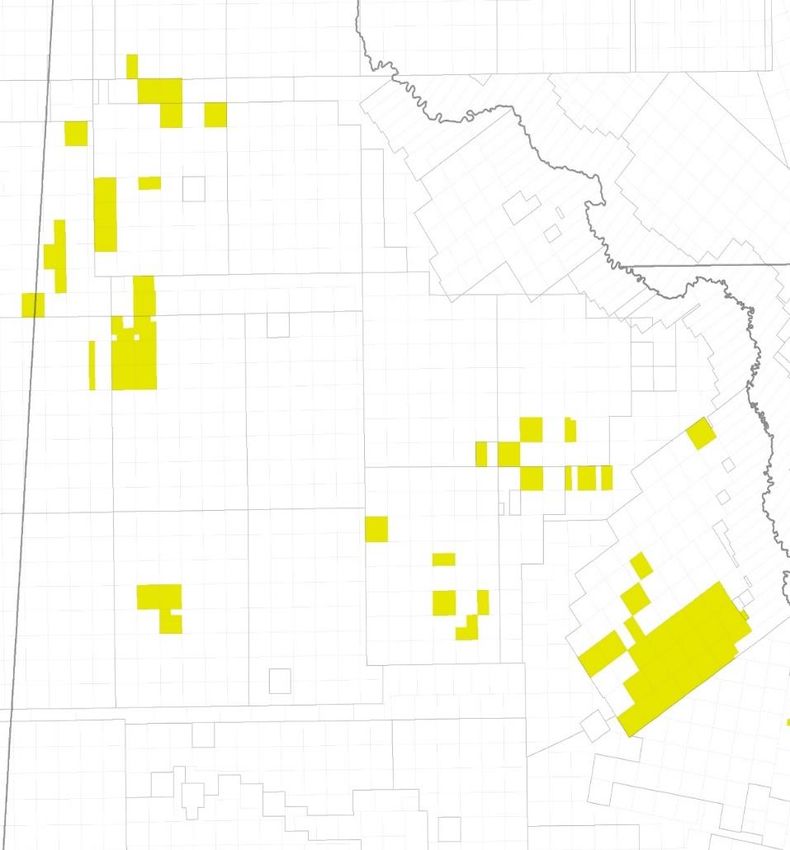

Wattenberg Overview

Key Statistics

785

YE19 PF Proved Reserves

Prairie Area

(MMBoe)

Summit Area

~161,000

3Q20 Production Kersey Area

(Boe/d)

Plains Area

33%

3Q20 Crude Oil

(Production)

~180,000 Net Acres

- Currently operating one rig and one completion crew

$1.89

3Q20 LOE/Boe

- Anticipate 1 rig and 1 full-time completion crew in 2021

December 2020 11Current Colorado Permit Process

Average ~12 Months from Permit Submittal to Approval (steps 3-4)

1. Site Selection Process – Surface Owner 3. Submit Form 2A Application – COGCC 5. PERMIT APPROVED

- Field land and surface owner agree on pad location - Submit application for approval of surface location - 2 years to commence operations

- Alternative location analysis - Does not include specific well approval

- Access roads & facility/tank locations - Includes planned # of wells on location

Best Mgmt.

- Oil, gas, water & power connections Practices (BMPs) - Receive Form 2A Approval - ~6 months (move to step 4)

- Dust & sound mitigation

- Safety protocol

- Sign Surface Use Agreement (SUA)

(move to step 2)

2. Data Gathering & Local Review – Local Gov’t. 4. Submit Form 2 Application – COGCC

- Compile leaseholder & mineral owner information - Submit application for each specific well (below ground)

- Notify all BU owners within 2,000’ – include estimated drill date - Casing design

- Submit local government permit application to municipality or Weld County - Cement usage and mud weights

- Municipality = Use by Special Review (USR) - Receive Form 2 Approval - ~6 months

- Weld County = Weld Oil & Gas Location Assessment (WOGLA)

- Analysis of BMPs

- Receive ‘Local Government Approval’ to proceed with COGCC

permit application (move to step 3)

December 2020 12Current COGCC Rulemaking Update

SB-181 Rules Related to Setback and Siting Requirements Expected to be Finalized in Late November

• Current proposal of new rules viewed as extremely similar to existing Director’s Objective Criteria

− 500’ setback from Building Unit (BU)

− 2,000’ setback from School Facilities and Child Care Centers

− “Siting requirements for proposed oil & gas locations within 2,000’ of one BU or high occupancy BU” replaces “Director’s Objective Criteria”

− Oil & Gas Development Plans (OGDP) and Comprehensive Area Plans (CAP) – multiple surface location permits (Form 2A’s) with extended permit life

Must satisfy one of four criteria to obtain Surface Location Permit (Form 2A)

1. No BU’s within 2,000’ of proposed location – ~5% of PDC’s undeveloped inventory

2. Unanimous BU owner/BU tenant acknowledgment

3. Location is within a Comprehensive Area Plan (CAP)

4. COGCC Commission hearing determines equivalent protections exist at distances closer than 2,000’

− Best Management Practices – consistent with current PDC practices

− Local Government consideration – consideration of local government decision – consistent with current USR/WOGLA approval

− Alternative site analysis – consistent with current PDC site selection process

− Relation to larger development plans – consistent with PDC emphasis on long-term planning & reducing surface footprint, increased piping, etc.

− Plans to avoid, minimize and mitigate impacts on residential BU’s – consistent with current PDC noise and dust mitigation efforts

− Community Outreach – consistent with current PDC practices discussed in 2020 Sustainability Report

− Staff recommendation – COGCC staff to offer Formal Consultation Process with Municipality/Weld County

Minimal anticipated changes to individual well/below ground (Form 2) approval process

December 2020 13Attaining Colorado Permits Amidst Ongoing Rulemaking Discussions

• Project to exit 2020 with ~275 well permits (Form 2) secured through 23 approved surface location permits (Form 2A)

− 85% of approved surface locations were approved under the COGCC’s Director’s Objective Criteria

− Average proximity to nearest BU of ~800’

~130

~230

• Received approval for 32 well permits in September and October (4 surface locations)

− Each surface location contained an average ~10 Building Units (BU) within 2,000’

− Average proximity to nearest BU of ~750’

• Potential for additional approved permits prior to new rulemaking effective date ~1,470 ~1,240

Key Takeaways

Area 2020 Spuds 2020 TILs YE20 DUCs YE20 Permits • Successful track record of

Kersey 20% 25% 40% 35% attaining permits under the

Summit 60% 60% 40% 40% Director’s Objective Criteria

Plains 5% 10% 15% 10% • Expected ~475 DUCs and

Prairie 15% 5% 5% 15% approved permits at YE20

reflect ~4 years of TIL activity

Total 100 130 ~200 ~275

at current pace

December 2020 14Rural Weld County Position with Low Building Unit (BU) Density

• PDC acreage is 100% in Weld County, Colorado

PDC Inventory in Relation to Nearest BU

− ~80% in unincorporated Weld County (not within Municipal (Does Not Include DUCs)

boundaries)

• Extremely rural acreage position with low BU density

increases potential to achieve unanimous consent

− ~90% of unpermitted inventory has < 20 BU’s within 2,000’

compared to ~85% of permitted inventory

BU’s within 2,000’ 0 1-10 11-20 21-35 35+

Permitted Inventory 0% 75% 10% 5% 10%

Unpermitted Inventory 5% 60% 25% 5% 5%

Key Takeaway

• Unpermitted and permitted inventory have very consistent BU

density and proximity to nearest Building Unit

*All numbers approximate and do not include surface pad optimization which has potential to further improve numbers*

December 2020 15Capital Efficiency Gains Contributing to Lower Projected Well Costs

Wattenberg Completions Efficiency(1)

(Hours per day Completing)

• Continued improvements to Wattenberg completions 85%

82%

− Recent completion activity averaging ~20 stages per day 80%

76% 77%

− Consistently improving non-productive time per day 75% 73% 74%

70%

65%

• 2020 XRL drill times more than 20% faster than 60%

early 2019 performance 1Q19 2Q19 3Q19 1Q20 3Q20

− Average spud-to-spud XRL drill times of 6 days Wattenberg Drill Times(1)

(XRL, Spud-to-Spud)

12

9

• Expect 5-10% improvement on projected well costs

from current $400/ft. (DJ) and $850/ft. (DE) estimates

Days

6

− Balancing potential per well savings with ability to D&C

more Wattenberg wells

3

0

1H19 = 7.7 days 2H19 = 7.5 days 1H20 = 6.0 days

December 2020 (1) The Company did not have any completions activity in 4Q19 or 2Q20 and did not drill any XRL wells in 3Q20 16Delaware Basin Overview

Key Statistics Loving County

120

YE19 Proved Reserves

(MMBoe)

~31,500

3Q20 Production

N. Central

(Boe/d)

39%

3Q20 Crude Oil

Reeves County

Block 4

Pecos

(Production) ~25,000 Net Acres

- No significant activity planned through year-end

$3.21

3Q20 LOE/Boe

- Anticipate 1 full-time rig and 15-20 TILs in 2021

December 2020 17Consistent, Successful Execution of Transparent Strategy

Track Record of Operational and Financial Execution Positions PDC for Sustainable Value-Creation

• Ability to generate consistent, sustainable adjusted free cash flow

− Project to generate more than $400 million FCF through 2021 with positive FCF expected in each of next 5 quarters(1)

• Focus on maintaining strong balance sheet and low cost structure

− Focus on reducing absolute debt level to ~$1.5 billion to enable sustainable shareholder friendly initiatives and continued debt pay down

• Improved DJ midstream environment

− Lower line pressures with ample capacity lead to improved well productivity

• Confident in executing Colorado development plan

− ~4 years of TIL activity secured through DUCs and approved permits with track record of successfully working with COGCC

• Resilient 5-year outlook

− FCF yield, leverage and cost structure to compete with broad market

(1) Assumes 4Q20 pricing of $35/Bbl WTI, $2.50/Mcf NYMEX natural gas and NGL realizations of ~$10/Bbl. 2021 pricing of $40/Bbl WTI, $2.75/Mcf NYMEX natural gas and NGL

December 2020 realizations of ~$10/Bbl. 18Investor Relations

Kyle Sourk, Sr. Manager Corporate Finance & Investor Relations

kyle.sourk@pdce.com

Corporate Headquarters Website

PDC Energy, Inc. www.pdce.com

1775 Sherman Street

Suite 3000

Denver, Colorado 80203

303-860-5800APPENDIX

Continued Emphasis on Cost Management

Targeting combined LOE + G&A of < $5/Boe LOE + G&A ($/Boe)

LOE G&A

$8.00 $7.51

• Merger synergies and focus on costs reflected through $6.60

$6.15

anticipated year-over-year reduction of 20+% in LOE+G&A/Boe $6.00

$4.25 ~$4.50(1)

$3.78 $3.27

$4.00

$2.05

• Anticipated LOE of $160 - $165 million $2.00 $3.26

$2.82 $2.88 $2.45

$0.00

2017 2018 2019 2020e

• G&A expected between $135 - $140 million

− Includes ~$25 million of stock-based comp

− Includes ~$10 million of SRC transition-related expense LOE + G&A ($/Boe)

− Excludes ~$20 million of SRC deal costs

LOE G&A

$6.00 $5.44(1)

• Anticipate TGP of $1.00 - $1.15/Boe

$4.13 ~$4.20

$4.00 $2.50 $3.95

$2.05 $1.84

$1.70

• Production taxes of 5% – 6% of sales

$2.00

$2.94 $2.50

$2.08 $2.11

$0.00

1Q20 2Q20 3Q20 4Q20e

(1) Excludes ~$20 million of SRC deal costs in 1Q20

December 2020 21Detailed Hedge Positions

Hedges as of October 31, 2020

December 2020 22Modified 2020 STI Compensation Metrics

PDC Board of Directors modified 2020 executive STI quantitative metrics in May 2020 in response to demand destruction

• Reduced target payout and maximum payout percentages

• Maintain current weightings:

− 75% quantitative / 25% qualitative

• Added Leverage Ratio to emphasize importance of balance sheet strength in low commodity price environment

• Removed production to better align with industry demands and account for unknown curtailment period

• G&A + LOE metric now measured in millions instead of per Boe to further de-emphasize production

2020 Proxy 2020 Revised (May)

− EHS − EHS

− Free cash flow margin − Free cash flow (absolute millions)

15%

12.5% − G&A + LOE per Boe each

− G&A + LOE (absolute millions)

each − CROCI − CROCI

− Production − Leverage Ratio (New)

− Capital efficiency/F&D − Production (No weighting)

− F&D (No weighting)

December 2020 23Adjusted Free Cash Flow & Adjusted Earnings Reconciliations

Cash Flows from Operations to Adjusted Cash Flows from Operations and Adjusted Free Cash Flow (Deficit)

Three Months Ended Nine Months Ended

September 30, September 30,

2020 2019 2020 2019

Cash flows from operations to adjusted cash flows from

operations and adjusted free cash flow (deficit):

Net cash from operating activities $ 280.1 $ 233.5 $ 649.3 $ 651.0

Changes in assets and liabilities (18.7) (31.1) 3.5 (49.1)

Adjusted cash flows from operations 261.4 202.4 652.8 601.9

Capital expenditures for development of crude oil and natural

gas properties (57.6) (237.8) (445.5) (755.8)

Change in accounts payable related to capital expenditures for 24.2 74.2 31.4 32.9

oil and gas development activities

Adjusted free cash flow (deficit) $ 228.0 $ 38.8 $ 238.7 $ (121.0)

Net Loss to Adjusted Net Income (Loss) and Adjusted Earnings Per Share, Diluted

Three Months Ended Nine Months Ended

September 30, September 30,

2020 2019 2020 2019

Net income (loss) to adjusted net income (loss):

Net income (loss) $ (30.8) $ 15.9 $ (717.6) $ (35.7)

Loss (gain) on commodity derivative instruments 68.1 (54.9) (245.9) 87.9

Net settlements on commodity derivative instruments 66.9 1.8 227.5 (19.8)

Tax effect of above adjustments (1) — 12.7 — (16.3)

Adjusted net income (loss) $ 104.2 $ (24.5) $ (736.0) $ 16.1

Earnings per share, diluted $ (0.31) $ 0.25 $ (7.34) $ (0.55)

Loss (gain) on commodity derivative instruments 0.68 (0.87) (2.52) 1.35

Net settlements on commodity derivative instruments 0.67 0.03 2.33 (0.30)

Tax effect of above adjustments (1) — 0.20 — (0.25)

Adjusted earnings per share, diluted $ 1.04 $ (0.39) $ (7.53) $ 0.25

Weighted-average diluted shares outstanding 100.2 62.5 97.8 64.9

December 2020 (1) Due to the full valuation allowance recorded against our net deferred tax assets, there is no tax effect for the three or nine months ended September 30, 2020. 24Reconciliation Non-U.S. GAAP Metrics

Adjusted EBITDAX

Three Months Ended Nine Months Ended

September 30, September 30,

2020 2019 2020 2019

Net income (loss) to adjusted EBITDAX:

Net income (loss) $ (30.8) $ 15.9 $ (717.6) $ (35.7)

Loss (gain) on commodity derivative instruments 68.1 (54.9) (245.9) 87.9

Net settlements on commodity derivative instruments 66.9 1.8 227.5 (19.8)

Non-cash stock-based compensation 5.4 5.9 17.4 18.1

Interest expense, net 21.0 17.8 67.0 53.7

Income tax expense (benefit) 0.2 10.7 (3.5) (4.2)

Impairment of properties and equipment 1.2 0.2 882.3 37.0

Exploration, geologic and geophysical expense 0.2 0.2 1.0 3.5

Depreciation, depletion and amortization 144.5 171.8 470.2 491.8

Accretion of asset retirement obligations 2.4 1.4 7.4 4.5

Loss (gain) on sale of properties and equipment (0.3) 43.9 (0.6) 9.6

Adjusted EBITDAX $ 278.8 $ 214.7 $ 705.2 $ 646.4

Cash from operating activities to adjusted EBITDAX:

Net cash from operating activities $ 280.1 $ 233.5 $ 649.3 $ 651.0

Interest expense, net 21.0 17.8 67.0 53.7

Amortization of debt discount and issuance costs (3.6) (3.4) (12.5) (10.1)

Exploration, geologic and geophysical expense 0.2 0.2 1.0 3.5

Other (0.2) (2.3) (3.1) (2.6)

Changes in assets and liabilities (18.7) (31.1) 3.5 (49.1)

Adjusted EBITDAX $ 278.8 $ 214.7 $ 705.2 $ 646.4

December 2020 25Reconciliation of Non-U.S. GAAP Metrics

Beginning in 3Q19, the Company modified its adjusted EBITDAX reconciliation to exclude (Gain) loss on sale of properties and equipment

Net income (loss) to adjusted EBITDAX (in millions): 3Q19 4Q19 1Q20 2Q20 3Q20

Net income (loss) $ 15.9 $ (21.0) $ (465.0) $ (221.8) $ (30.8)

(Gain) loss on commodity derivative instruments (54.9) 74.9 (434.7) 120.8 68.1

Net settlements on commodity derivative instruments 1.8 2.2 45.8 114.8 66.9

Non-cash stock-based compensation 5.9 5.7 5.7 6.4 5.4

Interest expense, net 17.8 17.4 24.2 21.8 21.0

Income tax expense (benefit) 10.7 0.9 (7.7) 4.1 0.2

Impairment of properties and equipment 0.2 1.5 881.1 - 1.2

Exploration, geologic and geophysical expense 0.2 0.6 0.1 0.7 0.2

Depreciation, depletion and amortization 171.8 152.4 176.2 149.5 144.5

Accretion of asset retirement obligations 1.4 1.6 2.6 2.4 2.4

(Gain) loss on sale of properties and equipment 43.9 0.1 (0.2) (0.2) (0.3)

Adjusted EBITDAX $ 214.7 $ 236.3 $ 228.1 $ 198.5 $ 278.8

December 2020 26Definitions

Adjusted FCF – Free Cash Flow (cash flows from operations before changes in EUR – Estimated Ultimate Recovery

working capital, less capital investments)

FCF Margin – Adjusted free cash flow divided by capital investments

AMI – Area of Mutual Interest

Gross Margin – Oil, gas and NGL sales less LOE, TGP and prod. tax, as a % of oil, gas

Bbl – Barrel and NGL sales

Boe – Barrel of oil equivalent Leverage Ratio – as defined in our revolving credit facility agreement; similar to

Debt to EBITDAX

BU – Building Unit

LOE – Lease operating expenses

Btu – British thermal unit

MM – Million

CAGR – Compound Annual Growth Rate

MMcf – Million cubic feet

CFPS – Cash flow per share

RoR – Rate of Return

COGCC – Colorado Oil & Gas Commission

SRL/MRL/XRL – Standard-, Mid- and Extended-reach lateral

CWC – Completed well cost

SWD – Salt-water disposal

D&C – Drilling and Completions

TGP – Transportation, gathering and processing

EBITDAX – Earnings before interest, taxes, depreciation, amortization and

exploration TIL – Turn-in-line

December 2020 27You can also read