BIG TECH AND PAYMENTS - March / April 2019 - Payments Cards & Mobile

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

March / April 2019 COVER FEATURE BIG TECH AND PAYMENTS

SUBSCRIBE TO

Payments Cards and Mobile

the Leading Payments Industry Magazine

PCM is an award-winning magazine published every two months with a

global circulation of hard and soft copies. Readership comprises senior

executives responsible for managing all types of payment in issuers,

acquirers, retailers, telcos, schemes and networks.

Celebrating in the industry

25% OFF

Use code: PCM25Y

Call (+44) 1263 711800

PAYMENTS INDUSTRY INTELLIGENCE

www.paymentscardsandmobile.com/subscribe/ Payments CARDS & MOBILE

PAYMENTS INDUSTRY INTELLIGENCE

Payments CARDS & MOBILE

March / April 2019

Volume 11, Issue 2

Merchant Payments Ecosystem has passed, Production Team

Seamless Middle East is coming and we have Alexander Rolfe

Editor-in-chief and publisher

already had the first Money 2020 show of the year. Tel (+44) 1263 711 800

alex@paymentscm.com

Anyone miss anything?

James Wood

The payments industry is on fire right now. At PCM, we re here to keep you in touch with Editor

james@paymentscm.com

all areas of this industry, curating the best news and information for you to digest at

your leisure. This is no easy task at the moment, given the speed at which the industry is Wendy Sanders

moving and the sheer weight of market information coming to us on a daily basis. Head of Business Development

Tel (+44) 1263 711 801

wendy@paymentscm.com

Academically, I have always found it interesting how industries and markets ebb and

flow. I have lived through a slow period in the payments industry but we are very much Gemma Rolfe

General Manager

full-on at the moment. Tel (+44) 1263 711 800

gemma@paymentscm.com

So, what can we serve up for you to digest in this issue We begin by taking a close

Gemma Haywood

look at Big Tech. The GAFA (Google, Apple, Facebook, Amazon) group of companies Subscriptions and General

have long been touted as candidates to enter banking and payments, causing Tel (+44) 1263 711 800

significant disruption in doing so. In this issue we consider what those companies gemma@paymentscm.com

have in playand, more importantly, what impact their presence could have on the Adam Unsworth

payments market. Head of Design & Digital

Tel (+44) 7932905744

adam@paymentscm.com

Next up we look at retail POS estates. Successive waves of Point-of-Sale (POS)

terminals are sunsetting , leading to significant upgrade or replacement costs for Printing

retailers. Meanwhile, non-POS methods of payment are proliferating, adding to the Micropress Printers

complexity retailers face. But is a completely new infrastructure really the answer

Finally, feature-wise, we consider national payments infrastructures. Growing Editorial Advisory Board

numbers of countries are rebuilding their infrastructures, including the UK, Australia, John Berns

India, Canada and Singapore. PCM looks at what s gone right and wrong, the pitfalls Managing Partner, Accourt

and expected benefits, and the role of the private sector in these changes.

Sylvie Boucheron-Saunier

SVP Financial Institutions, North America

& Europe, ACI

Chris Harris

VP Sales Performance & Global Accounts

at Ingenico Group

Alexander Rolfe,

Siobhan Moore

AlexRolfe Partner, Global Head Cards and

Payments at Locke Lord LLP

Fiona Wilkinson

Editor-in-chief and publisher, PCM Board Member

Payments Cards & Mobile

All rights reserved. No part of the publication may be reproduced or transmitted in any form without the

publisher’s prior consent. While every care is taken to provide accurate information, the publisher cannot

accept liability for errors or omissions, no matter how caused. Payments Cards and Mobile

The Stable, Hall Yard, Kelling

© PaymentsCM LLP 2019 Holt, NR25 7EW, United Kingdom

Payment Cards and Mobile™ is owned and published by PaymentsCM LLP ISSN 1759-829X +44 1263 711800 / paymentscm.com

contents

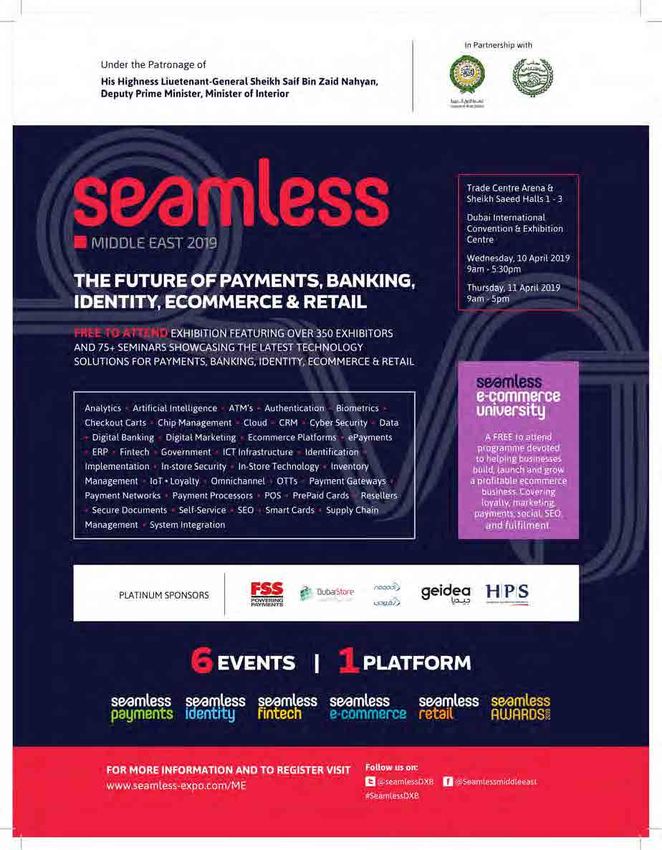

06 - 07 PAYMENTS NEWS 26-27 ISSUING & ACQUIRING 28-29 MOBILE PAYMENTS

NEWS IN BRIEF EC SETS SIGHTS ON TIPS CHALLENGING SEPA PROXY LOOKUP: PAN-EUROPEAN P2P

All the latest news from the past 60 days. VISA AND MASTERCARD PAYMENTS

The European Commission (EC) is The SEPA Proxy Lookup (SPL) service, a new

08 - 11 CARD NOTES considering implementing new regulations service that creates secure interoperability

to support and accelerate the adoption of between existing mobile P2P payments

REPORTS IDENTIFY OPEN BANKING the TARGET Instant Payments Settlement services, has launched. The SPL service is

OPPORTUNITIES System (TIPS) in an effort to challenge the ready to be used, and the first provider has

New surveys from PwC and Cardlytics have dominance of card companies and tech already integrated the service into its mobile

identified opportunities and risks in Open giants in Europe. payment solution.

Banking, with estimated revenue of £7.2bn up

for grabs over the next three years. COMMERCIAL VIRTUAL CARD PAYMENTS PAYPAL CEO: PAYMENTS MARKET TO HIT

TO EXCEED $1 TRILLION BY 2022 $100 TRILLION

STRONG AUTHENTICATION ON THE RISE A new report has found that the annual value Dan Schulman, the CEO of PayPal, has gone

New analysis from the FIDO Alliance and of virtual cards (temporary card numbers only on record with CNBC and said that the digital

Javelin Research has shown that strong available for a single transaction or limited payments industry may become a $100 trillion

authentication, which uses multiple- time) used by businesses will grow 90 percent market as the financial technology sector

factor, multiple-method authentication to over the next four years; exceeding $1 trillion continues to grow rapidly.

verify identity, is rising around the world in by 2022.

response to increasingly sophisticated fraud GLOBAL MOBILE WALLET USAGE MAPPED

attacks and growing regulatory demands. CASHLESS SOCIETY? US BANS Forecasts predict that by 2022, just 17 percent

‘CASHLESS’ STORES of global payments will be made by cash.

KEY CHARACTERISTICS OF GREAT FRAUD In highlighting ust how difficult it will be for Meanwhile, digital and mobile wallet usage will

MANAGEMENT society to go completely cashless, this week continue to rise, accounting for 28 percent of

A new report from Visa subsidiary has seen the UK report on how it cannot all point of sale transactions in just three

CyberSource, based on responses from allow its cash infrastructure to fail. years’ time.

2,800 fraud management specialists around

the world, has revealed the characteristics CARD NETWORKS PREPARE TO RAISE 31 CONTACTLESS

that make for great fraud management in SCHEME AND INTERCHANGE FEES

payments companies – while noting that Visa and MasterCard are reported to be planning APPLE PAY ADOPTION CONTINUES TO RISE

fewer than one in five firms actually adopt increases in interchange fees as well as fees In the December 2018 earnings call for Apple,

this approach. that card networks charge financial institutions analysts were given several incremental

for processing card payments for merchants. data points on the usage of Apple Pay. It

COVER STORY P14-16

BIG TECH AND PAYMENTS

4 payments cards & mobile magazine - march / april 2019 www.paymentscm.com

contents

may seem like an insignificant piece of the cryptocurrency this month. It marked an SOCIETE GENERALE SELECTS HPS FOR

ecosystem, as it only represents a fraction unprecedented move for a major US bank. PROCESSING IN AFRICA

of a percent of overall revenue, but it serves Société Générale, one of Europe’s largest

as a great example of what you can build CURVE CONSIDER LEGAL ACTION AGAINST banks with operations across the world, has

with integrated hardware/software and a AMERICAN EXPRESS selected HPS to improve payment processing

reputation of protecting user privacy. Curve says it is considering legal action activities for its ten African subsidiaries.

against American Express after the card

SHIPMENTS OF NFC POS TERMINALS TO network blocked its customers from using 38 CONFERENCES

REACH 112 MILLION BY 2022 Curve’s services this week.

According to new research from Berg RBI DIGITAL BANKING CONFERENCE EU

Insight, the market for NFC POS terminals YOYO LAUNCHES OMNI-CHANNEL 1-3 April, London

continued to show strong momentum in 2018 PAYMENTS AND LOYALTY PLATFORM retailbankinginnovation.fintecnet.com

with annual shipments reaching an estimated RETAILERS

24.7 million units worldwide. Yoyo says it has combined its in-store digital INTERNET RETAILING EXPO

payments and loyalty experience with a 3-4 April, NEC Birmingham

33 E-COMMERCE unique e-commerce solution, enabling www.internetretailingexpo.com

retailers to deliver integrated and rewarding

HOW WILL BREXIT AFFECT E-COMMERCE? omni-channel buying experience for SELF-SERVICE BANKING ASIA

Brexit brings a wave of uncertainty and customers, in-store or online. 3-4 April, Bangkok

change to the UK business landscape. Since https://www.rbrlondon.com/conferences/

the day the UK voted to leave the EU, it’s 37 CONTRACTS ssba/

been a whirlwind. But what will the payments

landscape look like leading up to, and after BARCLAYCARD AND UNIONPAY IFINTEC

Brexit? What kind of impact will it have on PARTNERSHIP IN UK 9-10 April, Istanbul

e-commerce, especially smaller sellers just Barclaycard, which processes nearly half of www.ifintec.com

starting up? With thousands of startups the UK’s credit and debit card transactions,

launching each year, will the looming shadow has announced a new card acceptance SEAMLESS MIDDLE EAST

of Brexit threaten the livelihood of new partnership with UnionPay International, a 10-11 April, Dubai

businesses and discourage people from subsidiary of China UnionPay. www.seamless-expo.com/ME

starting out?

ANT FINANCIAL MAKES BIG STEP INTO ETA TRANSACT

35 PRODUCTS EUROPE WITH $700 MILLION DEAL 17-19 April, Las Vegas

Ant Financial has finally managed to make www.electran.org/events/etatransact/

JP MORGAN CHASE TO LAUNCH ITS OWN its mark in a significant European first. The

CRYPTOCURRENCY Chinese financial services giant has agreed CONNECT:ID

Despite CEO Jamie Dimon labelling Bitcoin to buy UK payments group WorldFirst in 29 April-1 May, Washington DC

a fraud, JP Morgan, the largest bank in a deal worth around $700 million after https://www.terrapinn.com/exhibition/

the US, has announced it has created WorldFirst was forced into a rapid fire-sale of connect-id/index.stm

and successfully tested its JPM Coin its US assets.

FEATURE P18-20 FEATURE P22-24

IS THE SUN SETTING ON NATIONAL PAYMENTS

RETAIL POS ESTATES? INFRASTRUCTURES

www.paymentscm.com payments cards & mobile magazine - march / april 2019 5

news in brief global payments news from the last 60 days

US CREDIT card debt has hit a new record of MASTERCARD IS continuing its round of ANT FINANCIAL has unveiled a new core

$870 billion as of December 2018, according acquisitions, announcing it has entered banking platform co-developed with Hoperun

to data from the Federal Reserve. Credit card into an agreement to acquire Transfast, Information Technology. The Distributed

balances rose by $26 billion from the prior an account-to-account money transfer Core Banking Platform (DCBP) aims to help

quarter. “The increase in credit card balances network which competes with Earthport – financial institutions tackle digital challenges,

is consistent with seasonal patterns but a company Mastercard had been bidding including distributed development, financial

marks the first time credit card balances for in competition with Visa. Transfast will product management and accounting

have re-touched the 2008 nominal peak,” complement Mastercard by increasing liquidation. It builds on Ant Financial's bPass

according to the report. Nearly 480 million worldwide connectivity in the account-to- (Business Platform as a Service) architecture,

credit cards are now in circulation, up by more account space, enhancing compliance established to enable third party banks to

than 100 million since hitting bottom after capabilities and offering more robust benefit from the Chinese giant s tech know-

the recession a decade ago, according to foreign exchange tools. Transfast currently how. To date, Ant Financial has installed

Bloomberg. At the end of last year, credit cards supports the Mastercard Send solution for its technology into more than 200 financial

were the fourth-largest portion of consumer business-to-business and person-to-person institutions, including 100 banks, 60 insurers,

debt in the US after mortgages, student loans payment services. On March 12, Mastercard and 40 wealth management companies

and auto debt. But the quarterly increase in also announced it would buy Toronto-based and security brokerages. DCBP is the first

credit card debt was faster than the other Ethoca for an undisclosed sum. Ethoca makes co-developed product in Ant Financial’s

categories. Overall debt in all forms reached technology that helps merchants and issuers technology portfolio.

a record $13.5 trillion. collaborate to battle digital commerce fraud,

linking ,000 merchants and 4,000 financial

institutions (FIs) globally. Mastercard also

purchased Vancouver’s NuData Security

in March 201 , and Brighterion, a firm

specialising in artificial intelligence (AI), in

July 2017.

PAYPAL HAS announced instant fund transfers

THE BANK of England is to take supervisory to user bank accounts. This service expands

action against Visa following a widespread THE CONCEPT of a cashless society has the existing money transfer system offered by

outage last year that disrupted payments suffered a number of setbacks recently, with PayPal-owned Venmo since 2017. Although

for millions of shoppers across Europe. the UK reporting that it cannot allow its cash the Venmo feature lets users instantly transfer

More than five million transactions across infrastructure to fail and India recording funds from PayPal to a Visa or Mastercard

Europe failed during Visa's 10-hour outage a significant rise in the amount of cash debit card, the new option will let users move

in June last year following a failure in its in circulation since the launch of 2008 it directly to their banks. PayPal says that the

primary data centre. In the UK, 2.4 million demonetisation initiatives designed to bring “instant” transfers will vary by bank and may

transactions failed to process properly, with digital commerce to the country. Now the US take up to 30 minutes to clear, but this is still

1.7 million credit and debit cards affected. city of Philadelphia has outlawed cashless faster than the “one to three business days”

Immediately following the incident, Visa stores. Critics of cashless stores, which only offered as standard. PayPal is charging the

Europe engaged an external party to conduct accept electronic and digital payments, say same fee for instant transfers, whether they

an independent review, with the scope agreed the practice discriminates against people be to a bank or debit card: 1 percent of the

with both the Bank and the Payment Systems without bank accounts or credit cards, or who total transaction up to a limit of $10. The new

Regulator (PSR). Despite Visa's commitment prefer to pay cash. The new law, signed by instant transfer feature is only available in

to remediation actions, the Bank of England Mayor Jim Kenney last week, takes effect on the US, although PayPal COO Bill Ready has

says it intends to direct the card giant to uly 1 and could lead to fines of up to 2,000 confirmed the company is looking to launch

fully implement the recommendations of on businesses not accepting cash. However, the feature in other countries.

the independent review. As a further action, many transactions will be exempt, including

it is also using its powers to require Visa those at parking lots and garages; businesses

Europe to appoint an independent third party, that sell goods through a membership model;

PricewaterhouseCoopers (PwC), to assess rentals that require security deposits; online,

the company's progress in implementing telephone or mail-in transactions; and goods

the recommendations. sold exclusively to employees.

6 payments cards & mobile magazine - march / april 2019 www.paymentscm.com

news in brief

FIRST DATA is to acquire Brazilian eftpos

manufacturer Software Express. Founded Network with the leading innovators in

in 1986, Software Express serves 100,000 Open Banking. Hear what’s working,

merchants in Brazil, processing more than who wants to collaborate and what is

11 billion transactions in 2018. The firm also coming next…

delivers recharge services for mobile phones,

At the Open Banking World Congress

and terminal applications for correspondent 2019 (7-8 May in London) we are

banking segments and transaction capture FIDELITY NATIONAL Information Services showcasing new propositions, emerging

networks. Combined, the two companies (FIS), the Florida-based provider of computing monetisation strategies and new revenue

streams. This is a ground level view of

expect to process more than 15 billion systems for financial institutions, agreed a what is happening in Open Banking and

transactions in Brazil. Henrique Ribeiro deal on 18 March to to take over payments what opportunities will develop for the

Filho, Software Express CEO, said: “Software processor Worldpay for $43bn including finance industry, consumers, business

and, ultimately, economies.

Express is accredited by all acquirers and debt. The deal is the largest ever in the

has a broad portfolio offering including EFT, payments industry. It is also the latest in With speakers ranging from the biggest

recharge servers for prepaid phones, front- a series of mergers as the race to build banking and tech companies to new

exciting FinTechs this is the definitive

end processor software, and correspondent global payment powerhouses accelerates. In Open Banking event in 2019 and is not to

banking software, among other services. a press release, FIS said the deal expands its be missed!

Our clients will now benefit from First Data’s capabilities by enhancing its acquiring and

global expertise and knowledge, opening payment offerings. For Worldpay, it expands

up additional possibilities for our clients, its distribution footprint and accelerates its

partners and employees.” Financial terms of entrance into new regions. Once the deal

We’ll connect you….

the deal were not disclosed. is closed, the combined company will offer • to the people you want to meet.

enterprise banking, payments, capital markets Networking is very important to you

and global eCommerce services to financial and we want to help. This event has

been carefully constructed to help

institutions and businesses around the world. you meet and engage with the right

people for you. Multiple structured

opportunities over two days, contact

us via the website and we’d be

delighted to share our plans and

discuss your needs.

THE BASEL Committee has set out • with expert discussion and demos

on an innovation stag, providing

minimum standards for banks relating to operational and strategic insights

crypto-currencies. While the crypto asset which will benefit your organisation at

market remains small relative to the global THE INDIAN e-commerce market is estimated a practical level.

• with insights into how data mobility

financial system and banks currently have to miss market growth expectations since and portability will evolve in an

very limited direct exposures, the central new FDI rules kicked in on February 1, 2019, increasingly API connected world.

banking committee believes continued slowing investment by e-commerce giants What possibilities will this offer you?

growth in crypto asset trading platforms such as Amazon. Morgan Stanley has revised

Join your peers, partners and

and new financial products has the potential its estimate for Indian e-commerce, expecting future contacts at this fantastic,

to "raise financial stability concerns and it to reach $200 billion by 2027, a year later vibrant and exciting meeting of the

increase risks faced by banks." The regulatory than initially forecast. “The new regulations world’s Open Banking community

openbankingcongress.com

body recommends that before acquiring released in December 2018 strive to ensure

exposures to crypto assets, a bank should those with FDI holdings operate as pure Want to meet up regularly?

conduct comprehensive analysis of the risks marketplaces without any equity interest We recommend Open Banking Excellence

(OBE), an open forum think tank that

and establish a robust risk management or control on seller entities or mandatory

meets monthly for those in the industry

framework appropriate to the size of its exclusivity clauses. We believe these to contribute, educate, share and

crypto asset exposures. Furthermore, a regulations will pose headwinds to growth in collaborate with what is now a global

movement to make bank data accessible.

risk assessment of crypto asset exposures the near term as some prominent companies

The goal of OBE is to create an authentic,

should be incorporated into a bank’s internal restructure their businesses, processes and collaborative channel for like mind people

capital adequacy assessment processes. The contracts to be compliant,” notes Morgan to share their stories and collectively have

a greater impact within the immediate

committee is also demanding full disclosure Stanley. However, the US bank said the overall

industry at a practical, real-world level.

of any material crypto asset exposures and market is growing as online commerce takes http://obexcellence.wpengine.com/

ongoing dialogue with supervisory authorities market share away from offline channels due

relating to actual and planned crypto to pricing attractiveness, convenience, and We’d love you to join us….

asset exposure. demand aggregation.

www.paymentscm.com payments cards & mobile magazine - march / april 2019 7

card notes GLOBAL

REPORTS IDENTIFY OPEN BANKING OPPORTUNITIES

A new survey from PwC has identified financial management and integrating lending such as slow settlement speeds for international

opportunities and risks in Open Banking, with and account platforms, PwC notes that banking transactions. A second wave will see more

estimated revenue of £7.2bn up for grabs over incumbents are at risk of falling behind to more innovative products appear which address gaps

the next three years. Meanwhile, a consumer nimble, tech-savvy challengers such as Monzo in the market, while a third wave will see

study from US company Cardlytics has found and Revolut. These firms have experienced the integration of financial services products

low levels of awareness and trust in the stratospheric growth in recent years and now with products from other industries. One live

concept of Open Banking, and aversion among have more than two million UK customers example of this is the integration of social media

consumers to the possibility of multiple layers between them. messaging and payments on one App, currently

of authentication when switching between available in China and a few other markets

products in an Open Banking environment. ENABLERS OF OPEN BANKING around the world.

The UK’s drive towards Open Banking began PROPOSITION DEVELOPMENT Whilst noting widespread benefits to the

Availability and

with a 2016 investigation into customer service standardisation of data industry and consumers, PwC argue that Open

(e.g. Standard APIs)

by the Competition and Markets Authority Banking is not without its risks. In particular,

(CMA). This investigation found that banks the report sees the possibility of failure

needed to be doing more to deliver value to protect consumer data as a factor that

for customers. The introduction of the EU’s could significantly hamper the Open Banking

Second Payments Services Directive (PSD2) in revolution, and urges regulators to be aware of

January 2018 forced major financial services this possibility. Enhanced financial exclusion is

companies to make their data freely available also a possibility as those who refuse to share

Technology Consumers' interest

for trusted competitors, and to open customer and maturity of and demand for Open their data are charged higher prices to access

data analytics Banking propositions

channels to competitors by sharing application (e.g. Machine/AI learning) (i.e. Willingness to pay for services) certain products and services.

programming interfaces, or APIs. The UK is a Source: PwC report To succeed in this new, more competitive

world leader in Open Banking, with the first set environment, PwC say companies need a

of enacted legislation and associated regulatory compelling vision of what makes them different,

UK OPEN BANKING AWARENESS

frameworks anywhere in the world. UK as well as developing fresh and creative

legislation aims to foster increased competition, propositions for the consumer. Given the short

making it possible for consumers to enjoy 26% timescales in which technologies can develop,

products from numerous providers on a single Have companies will have to consider acquisitions

heard of

platform and overcome the consumer inertia Open and partnerships as a means of getting Open

Banking

which has stifled competition in the sector. Banking products to market.

According to data from Cardlytics, 84 providers

of open banking services have signed up 74% Cluing in the Consumer

Have not heard of

since the launch of Open Banking in the UK Open Banking

last January, including 58 third-party service If there are risks and upsides from the industry

providers such as insurance companies, utilities Source: Cardlytics point of view, then the Cardlytics study shows

firms and mobile phone businesses. A further 26 that consumer awareness of Open Banking has

non-bank companies have registered to launch With specific regard to financial services, been patchy at best. The Cardlytics report states

their own current accounts, with 12 of these PwC’s report identifies three key areas in which that fully 74 percent of UK consumers have never

schemes going live as of October 2018. Access Open Banking can create value – revenue heard of open banking.

to open banking technology protocols has more generation, cost reduction, and the creation of The study shows that men over fifty living

than doubled to 4.2 million since these protocols shareholder value. Outside the financial services in London and South-East England are most

were launched by the UK government in market, however, there are also opportunities likely to be aware of Open Banking, with women

June 2018. for both non-banking companies and third party under 25 living in the North least aware. These

service providers. low levels of awareness aside, the survey also

Open Season Grouping these opportunities around the provides evidence of poor consumer trust in

headings of data standards, analytics and open both their existing financial services providers

PwC’s survey, The Future of Banking is Open, banking propositions, PwC predict a series and potential alternatives. A mere 20 percent of

says there are a number of opportunities for of progressively creative waves of innovation UK consumers said they trust their bank or other

early movers in the Open Banking market, with coming to market from outside the major high financial institution to handle their data securely

revenue opportunities of £7.2 billion across street banks. In the first wave, solutions will – a figure which drops to 13 percent for utilities

retail and corporate banking. Citing examples appear that respond to existing and known companies and as low as 4 percent for social

such as merging customer accounts, improving challenges in the financial services market, media firms.

8 payments cards & mobile magazine - march / april 2019 www.paymentscm.com

BANKS AND FINTECHS:

FINANCIAL FOES CEASE-FIRE AND TEAM-UP

Regulatory changes in the past few years payments quickly and cheaply, regardless of Soni, director of innovation and FinTech at

have led to a significant shift in banking and geography. Finastra, commented, “Real platform players are

payments. Non-bank providers can now offer Compared with traditional correspondent coming into the market from adjacencies such

payment solutions, increasing competition and banking network processes, FinTech payments as big tech companies like Google, Amazon,

raising expectations among consumers and are received in seconds rather than days, cost Facebook, Apple, Alibaba – they don’t have

businesses alike. pennies rather than pounds and take place with core banking experience but are looking at the

More agile FinTechs stepped in to fill the gap just a few taps or clicks rather than detailed world through the lens of consumers shaping

between what consumers wanted, and what paperwork, phone calls and maybe even a trip to attractive user experiences and have a real

traditional banks were able to deliver. These new a local branch. advantage.”

entrants built their solutions from the ground However, it is not entirely painless for the Financial utilities - which essentially do not

up, with consumer needs and preferences as Financial Tech businesses. Without the customer compete with the banks or the FinTechs -

the foundation, and have therefore been able history and relationship many are struggling to can underpin a financial institution s offering,

to provide solutions which better suited today’s get a real foot-hold, particularly in business providing their non-core functions such as

consumer. This improvement has led to a further payments. The 2018 FinTech Disruptors report 2 payments, F and lending. This allows financial

rise in demand across the financial board. revealed that banks and FinTechs are indeed institutions to focus on their customers and add

Trends such as this in the consumer market both keen to pair-up and deliver better solutions. value to their customer service proposition, and,

often lead to similar changes in the business Change is on the horizon, and the future looks importantly, remain competitive.

market. Consumers expect better, faster, distinctly more connected than the present.

cheaper banking solutions in their personal THE FUTURE FOR BANKS AND FINTECHS

lives and once this becomes well established, COLLABORATION – NOT COMPETITION For the third consecutive year, the 2018 FinTech

they naturally expect and demand the same level Banks understand that they must focus Disruptors report showed that creating or

of service in their business lives. their resources on managing the customer extending partnerships are the main goals of

relationship, rather than on non-core activities. banks’ intentions with FinTechs. Working in

THE EVIDENCE To remain competitive and relevant in this partnership with financial utilities, banks and

A global survey of more than 8,000 consumers market, many of these banks are already FinTechs alike will be better able to provide

in 20181 showed that 34% of all consumers, partnering with third party Financial Tech efficient and convenient solutions, helping them

and 52% of 18-34-year-olds, would consider businesses and financial utilities such as to remain competitive in the long-term. In ten

banking with a familiar tech giant such as Banking Circle, to deliver non-core banking years, banks and FinTechs will look much more

Amazon, Google, Facebook or Apple rather than services. It’s a new world of seeing each other as similar than they do today.

a traditional bank. The main reasons given were collaborators rather than competitors. Financial utilities can handle the tech side

for simplicity and convenience (42%), followed As recently as five years ago, the idea of a bank without it being a burden on resources. The

by a more personal service (23%). 2018 Banking working with external partners to deliver banking financial institution is then able to offer

Circle research showed that banks are gearing services was unfathomable to most. However, in affordable, flexible and efficient credit, payments

up to take on the FinTech challenge. today’s market, with the complexities of legacy and FX to all customer segments. This allows

With more agile FinTechs building innovative systems together with the rapidly increasing banks and FinTechs to provide the best service

customer-centric solutions the front-end of competition from FinTechs, banks are ready possible, empowering businesses to reach their

payments is being rapidly simplified. Seamless for this vision. Most have accepted that full global potential, without payments or lack of

payments, local or cross border, are making the partnerships are the only way they can remain access to credit holding them back.

world smaller and more accessible. FinTechs are competitive, as it allows them to offer the best

increasing financial inclusion, now allowing even solutions to their valuable customers, without Anders la Cour,

the smallest business and newest start-up to compromising on the relationship. Co-founder and Chief Executive Officer,

operate on a global scale, sending and receiving In the 2018 FinTech Disruptors report, Mitesh Banking Circle

1

Source: Consumer connectivity insights report, Mulesoft, June 2018: www.mulesoft.com/ty/report/connectivity-insights-consumer-experience

2

Source: 2018 Fintech Disruptors Report, MagnaCarta, December 2018: https://www.magnacartacomms.com/2018-fintech-disruptors-report

card notes GLOBAL

STRONG AUTHENTICATION ON THE RISE

New analysis from the FIDO Alliance and in authentication. Of these non-adopters, of use” following behind. Being compliant with

Javelin Research has shown that strong two-thirds believe that passwords alone are existing and future regulatory requirements

authentication, which uses multiple-factor, sufficient to authenticate their employees was the least-frequently cited factor.

multiple-method authentication to verify and customers, perhaps because they do not

identity, is rising around the world in response see the value of the data assets they hold Customer Keys are King

to increasingly sophisticated fraud attacks and where those assets do not include financially

growing regulatory demands. As companies sensitive information. Organisations which do employ strong

and consumers increasingly turn to digital Even where stronger authentication authentication methodologies are more likely

channels to communicate and do business, methodologies are deployed, many of these to be concerned about friction created for

FIDO argue that more organisations need to involve relatively easy-to-compromise factors customers in the authentication process, with

employ strong authentication techniques. such as static or dynamic security questions factors such as cryptographic keys or some

The adoption of strong authentication (e.g. mother’s maiden name, or the make biometric systems risking a cumbersome entry

methods significantly reduces the likelihood of a consumer’s first car.) Only 5 percent of process. Despite this concern, FIDO argue

of successful fraud attacks, since multiple organisations employ fully robust multiple- that the adoption of stronger authentication

fraud approaches must be successfully factor authentication methods, such as systems will allow companies to focus on

combined in order to fully impersonate the cryptographic keys. enhancing their customer experience after ID

targeted individual or organisation. Strong validation, rather than worrying about system

authentication usually combines two or Regulation Push and Pull and data security.

more factors, including passwords, off-line In support of this argument, FIDO offer

cryptographic keys, or biometric factors After the introduction of PSD2 and GDPR the examples of Google, Tradelink and Visa,

and behaviours. regulations in Europe, with Canada, Australia all of which have recently adopted strong

As digital channels become the norm, weak and US states such as California set to follow authentication methodologies. Google

authentication methods are being targeted by suit, companies have recognised the need to introduced FIDO-approved security keys for

criminals to compromise customer accounts improve their authentication methodologies. its 85,000 staff world-wide in 2018, and has

at depth. As a result, regulators are raising the Whilst 70 percent of businesses agree that not had a single security breach on its internal

bar for corporate data security – and placing regulatory pressure to change is increasing, systems since. Responding to concerns about

the onus on corporations to protect customer more than half also recognise that their current the complexity of introducing strong multi-

data at the same time. FIDO’s analysis suggests authentication systems are inadequate and factor systems, Visa has recently launched its

that companies need to focus not just on will not meet regulatory expectations in a few ID Intelligence service, allowing its customer

their customer and data security, but also on years’ time. financial institutions to select from a range of

the introduction of stronger authentication Despite this, companies are still primarily biometric verification solutions and integrate

for employees, as impersonating the ID and concerned about simplicity and cost when from a single source with a trusted provider.

passwords of employees becomes a favoured it comes to selecting an authentication FIDO recommend sunsetting one-time

method for fraudsters to gain entry to corporate technology. 32 percent of businesses passwords and giving strong authentication

IT systems. surveyed cited “ease of integration” as their in online and mobile communications urgent

The use of strong authentication main consideration when selecting a new priority, since these face the greatest risk of

methodologies has increased by 50 percent authentication system, with “cost”, and, “ease compromise by fraudsters.

since the last time this analysis was conducted

in 2017. Furthermore, the use of passwords as a

ADOPTION OF STRONG AUTHENTICATION RISES FOR

sole means of verification has decreased by 25 CUSTOMER AND ENTERPRISE USE

percent for consumer identification, with only

31 percent of global organisations now using 2018 Consumer

16% 52% 33%

password-only authentication. For enterprise Authentication

applications, 47 percent of companies still 2017 Consumer

5% 51% 44%

use password-only authentication, though this Authentication

figure represents a 20 percent decline over the 2018 Enterprise

12% 41% 47%

last 18 months. Authentication

2017 Enterprise

7% 37% 56%

Two Steps to Heaven Authentication

Strong authentication Traditional multifactor authentication Single-factor authetication

FIDO warn that nearly half of those companies

Source: Javelin Strategy & Research 2018

surveyed are not using two or more factors

10 payments cards & mobile magazine - march / april 2019 www.paymentscm.comGLOBAL card notes

KEY CHARACTERISTICS OF GREAT FRAUD MANAGEMENT

A new report from Visa subsidiary CyberSource, management processes and minimise the The sectors best-equipped to manage fraud are

based on responses from 2,800 fraud number of chargebacks. those dealing with digital goods, the foodservice

management specialists around the world, has industry and professional services firms.

revealed the characteristics that make for great Plan, Do, Review

fraud management in payments companies – Balancing the Mix

while noting that fewer than one in five firms Given the relentless growth in consumer

actually adopt this approach. With emerging expectations and increasingly sophisticated CyberSource’s survey revealed that the top

fraud such as account takeover and ID theft criminal behaviour, a “set it and forget it” anti-fraud measures favoured by “leading”

rising in importance, CyberSouce argue many approach won’t work when it comes to fraud companies were Card Verification Numbers ( 4

companies need to rethink their attitude to management, CyberSource say. Instead, percent), biometrics (53 percent) and customer

fraud management. regularly rebalancing your firm s focus between order histories (52 percent). By contrast, other

The report says the best fraud management customer acceptance, fraud detection and companies relied more heavily on 3D Secure

strategies place equal emphasis on delivering operational cost management yields the best ( DS) and Address Verification Services (AVS).

a positive experience for genuine customers, results across the board. Leading companies proved themselves to be

accurately detecting and rejecting fradulent However, it appears few firms are actually more adept at switching their reliance between

orders, and efficiently managing operational taking up this challenge, with only 18 percent different tools depending on the circumstances.

costs associated with fraud prevention. of those surveyed recognising all three pillars Other tools considered to be effective across

Companies that achieve a balance between these of CyberSource’s approach as important. North the board, but used by respondents to various

three factors see significant benefits accrue America is most advanced along this path, with degrees, include negative lists for known fraud

across their business, including chargeback rates 28 percent of companies surveyed recognising sources, two-factor phone authentication,

75 percent lower than other companies, and lower the importance of all three factors. By contrast, and mobile geo-location confirmation.

staff costs associated with fraud prevention. only 12 percent of Asian firms currently use Recent improvements to 3DS have seen the

Although less than one in five of the firms CyberSource’s recommended methodology. reputation of this tool improve significantly,

surveyed are categorised as leaders by By revenue source, those with moderate revenues with previous concerns over high levels of

CyberSource, these leading companies are from e-commerce were least likely to adopt a disruption to customer service diminishing

more likely to respond quickly to fraud attacks. balanced approach (14 percent), while small and as 3DS has refocused on challenging only

“Leader” companies in fraud management also larger firms in terms of e-commerce revenue both those transactions where a risk factor has

put their digital anti-fraud strategy at the heart regularly review their anti-fraud arrangements. been identified.

of their business, and have almost twice the

capacity to manage customer data to prevent

PRIORITISING ALL THREE BALANCING ACT REQUIREMENTS

fraud compared to other firms.

Citing the advent of “omnichannel” payments as

one reason why companies need to rethink their

North America 28%

approach to fraud management, CyberSource

argue that increasingly strict fraud management Latin America 26%

By

legislation encourages companies to err on Middle East and Africa 20%

18%

region

the side of caution, flagging genuine customer Europe 16%

transactions as fraudulent and creating negative rate all three dimensions

12% as extremely important

customer experiences. Instead of focusing solely

on fraud management, the report argues for a Small 20%

By

customer-centric approach to fraud, where the eCommerce Mid-market 14%

revenue

focus is on ensuring genuine customer orders are

Enterprise 20%

automatically accepted at the same time as fraud

is identified and prevented. Physical goods 14%

Whilst recognising that criminal behaviour is Digital goods 26%

constantly changing to adapt to developments in By

Services 21%

anti-fraud technologies, CyberSource report that vertical

Food/Restaurants 22%

fraud management controls must be constantly

fine-tuned to help maximise customer revenue Travel 16%

STATISTICALLY SIGNIFICANT

and ensure the best possible customer

experience. Through a process of continuous Source: CyberSource

review, it’s also possible to streamline fraud

www.paymentscm.com payments cards & mobile magazine - march / april 2019 11How banks (even outside of Europe!) can

get ahead in the open banking age

Stéphane Joseph, Financial Services Product Manager at FIME

Open banking is high on the agenda. For banks that fall under PSD2, the

European regulation mandating banks to open-up their back-end to third-

parties, the urgency of joining the open banking trend is clear. But that doesn’t

make open banking a purely European pursuit. Nor should PSD2’s underlying

objective – to facilitate more valuable and engaging consumer experiences –

escape the priorities of banks internationally.

In fact, from the US to the Middle East and digital transformation projects requiring and complexities of compliance without

Asia, open banking and digital transformation such extensive revisions to banks’ back- huge internal investment. Not to mention

have been making waves. Consumer demand end infrastructure need to be planned and advising how best to monetize these new APIs,

for more valuable, connected services will managed sensitively. balancing the weight of initial investment with

only rise in coming years, meaning the need the pressure to generate short-term revenues.

to deliver more valuable services, strong The rewards are high for moving quickly, but

customer authentication (SCA) and open- any break in service or data compromise could Flying solo or working together?

access APIs will soon become ubiquitous – be fatal. In short, agility must be balanced

even if not legally mandated globally. with trust. Defining a comprehensive and There are different approaches to open API

effective testing roadmap can ensure trust is development. Resource can be invested

Its unsurprising many countries are already built-in to new open API initiatives from the internally to develop a new in-house API

looking to get ahead but such transformation start. Effective planning also minimizes any tailored to your organization, or a number

projects entail significant technical unexpected delays to service launch, ensuring of API standards and external ‘hubs’ can be

complexities and strategic challenges. Banks a quality, fully functional and interoperable reviewed. These initiatives have proved popular

need to be smart to remain competitive – so service is launched on time and on budget. in recent years as a means for players to pool

how can they best prepare for success? resources and streamline the launch of open

For those facing regulatory pressures, APIs.

Build with trust to promote trust it’s important to meet all the necessary

compliance hurdles. There are several legal One example in France is STET s definition

Consumers will applaud open-access constraints to consider, so consultancy can be of an open banking API standard. Developed

accounts and new digital services, but invaluable in understanding the technicalities with support from FIME, the protocols enablebanks and application developers to ensure investing to compete is more valuable than with any digital transformation, the benefits

regulatory compliance, security and seamless collaboration with – or even acquisition of – of gaining early-mover advantage also come

interoperability – all at a considerably lower new players. with high complexities, both technically and

cost and greater efficiency. While currently strategically.

active across France, the organization plans Enabling new data and authorization requests

to extend across the continent and later, across channels to be managed securely and Partnering with leading experts such as FIME

the globe. in ‘real-time’ is another technical headache. can help take the strain of understanding the

With rising demand for stronger customer market, technical and regulatory requirements,

Another example is The Berlin Group, a pan- multi-authentication methods too, issuers as well as defining how your transformation

European harmonization initiative focussed also need to review new technologies and will maximize ROI. With so many new, sensitive

on delivering open banking with a common protocols such as biometrics, risk-based and and technical complexities to consider, a

scheme- and processor-independent standard. 3D Secure. Prioritization is key to remaining testing expert working at the centre of

Incorporating major stakeholders from across flexible, responsive and competitive. innovation can be considerably more cost-

the ecosystem, participation in these and similar effective and agile than trying to source

standards efforts can maximise resource and in-house expertise.

speed-up time to launch.

FIME is working with banks and TPPs across

FIME has actively engaged in standardization the world to define, design, deploy and

efforts across the payments industry for validate their open API strategy and digital

over twenty years and is helping banks and transformation projects. Learn more about

payment stakeholders effectively evaluate the our open banking services on www.fime.com

different initiatives. or contact FIME to find out how we can help at

sales@fime.com.

Fintech friends & tackling Stéphanie Pietri, Marketing Communications

the trends Director: “You can also meet our experts

and check out our open banking demos

We’re witnessing more than just open banking at the following industry events: Seamless

however. Driven by Fintech innovation and

Partner up! Middle East, Dubai (April 10-11): booth H61

rising consumer demands – this is an era of Trust, efficiency and agility are needed to and Money20/20 Europe, Amsterdam (June

pure digital transformation. From branchless compete in this rapidly changing and exciting 03-05): booth K115.”

banks to mobile-native services and cross- market to ensure long-term success. But as

platform integration, acquiring and issuing

banks need to create more flexible business

models to remain competitive.

For those reviewing new Fintech offerings

across payment platforms and form factors,

one important consideration may be whetherBIG TECH AND PAYMENTS by James Wood, PCM Editor A late 2017 McKinsey study warned payments firms should be more worried about “Big Tech” than fintechs as a threat to their businesses. Since then, Facebook, Apple, Google and Amazon (“FAGA”) have made further inroads into global payments. PCM Editor James Wood looks at recent developments, and asks whether Big Tech’s relentless advance may be halted by regulatory concerns and consumer reluctance. The attractions of payments for a new entrant Enter Big Tech. By end 2018, the world s five giants known as “FAGA” are most aggressively are clear: rapid revenue growth over the next ten largest brands were tech companies: Amazon, targeting the entire payments spectrum, from years, initiatives like Open Banking enhancing Apple, Google, Samsung and Facebook. virtual currencies to credit cards, intermediation competition by favouring new entrants, and They have the consumer recognition and services and P2P. stability: people will always need to pay for financial muscle to make this kind of move Facebook CEO Mark Zuckerberg made things. Against these attractions, there’s rising work. Bloomberg Markets recently weighed in headlines last month with a new strategy regulation (including five ma or pieces of US alongside McKinsey, describing the advent of including a specific intent to move into legislation since 201 ) firmly established global big tech as a nightmare scenario for US finance, payments. This announcement comes as no brands with deep pockets and, worst of all, should one of these companies succeed in surprise to those following the company: as consumer inertia. When it comes to payments, replicating WeChat’s success in the West.” of 31 December 2018, payments revenues at people trust what they know. Facebook rose 42 percent year-on-year. Four Ideally, any new entrant would have enough Facing the Future months ago, the company announced the cash and the marketing clout to take on existing launch of “Facecoin”, a so-called “stablecoin” giants such as Visa and Mastercard. They would Although Samsung, IBM and Intel have all – or crypto-currency linked to the US dollar. also be fluent in emerging payment technologies made moves into payments, with Samsung’s Facecoin allows users to transfer value person- like mobile and digital, and conversant with data mobile wallet targeting the company’s device to-person and make purchases across all of the privacy and consumer protection issues. users, there’s little doubt that the four tech company’s plaforms. 14 payments cards & mobile magazine - march / april 2019 www.paymentscm.com

big tech

Having previously purchased social media clear that Apple has watched the rise of digital debit cards in Mexico; government payments

platforms WhatsApp and Instagram, Facebook P2P payment systems like AliPay and WeChat and charity subscriptions across France, Spain

intends to create a single platform for social with interest. and Italy. If this sounds like the company has

messaging, imaging and payments across all of As with Facebook, Apple believes it can deploy no clear strategy, think again: these products

its platforms. Collectively, these platforms have huge amounts of data from other customer have two clear objectives. They deepen the

more than 1.5 billion users around the world. interactions into the stringent identity required customer’s relationship with Amazon, and allow

As a first step to realising these ambitions, by payments. The meteoric rise of digital the firm to harvest as much information as

the company has been trialling payments possible about spending habits, building up

over WhatsApp in India since January 2018. strong customer identity. Amazon is so keen

FIG 1 - APPLE SERVICES GROWTH -

Intended as a rival to PayTM, Facebook’s on customer information that they’ve enabled

INCLUDING APPLE PAY $12B

Indian social media payments service has AmazonPay, their digital wallet solution, as a

more than 1 million users. Whatever the 10 third-party proxy for other merchant websites:

platform, the huge advantage Facebook and 8 as the 1990’s advertising slogan had it, for

other tech companies have in launching digital 6 everything else – there’s AmazonPay.

payments is the capacity to identify parties to

4

any transaction through their own verification Eyes Agoogle

2

technologies, as well as behavioural data that

Q1 Q2 Q3 Q4 Q1 0

acts like a virtual biometric, confirming the As this template of data redeployment emerges,

2018 2018 2018 2018 2019

consumer is present and acting normally. As the the question of when consumers may revolt

Source: Compay filings

physical and virtual worlds continue to merge, against being treated like cabbages on a data

maintaining consumer identity on-line will be a farm rears from the mist. Such revolts are not

massive benefit. payments in China has only been made possible unfamiliar: Ireland’s competition commission

by that country’s compulsory online ID system. announced a preliminary study into Facebook

Apple Takes a Bite In using data harvested from its devices to and Google for monopolistic practices in late

confirm the identity of parties to a transaction, 2018, and 2020 US Presidential Candidate

Facebook’s competitors have not stood by Big Tech believes it can steal a march on banks Elizabeth Warren has just called for FAGA to

watching. Though many have carped that Apple and card networks still struggling with the issue be broken up into smaller companies. If cynics

Pay is less successful than other wallets, one of of online security. believe this can’t happen, they should consider

Big Tech’s distinguishing features is the capacity the break-up of Standard Oil in 1911, which gave

to lead a sustained, multi-year push into sectors Amazon: Before the Flood birth to Esso and Texaco. Standard Oil simply got

ripe for disintermediation. In January 2019, too big for anyone’s comfort.

Apple Pay announced all US Taco Bell locations If Big Tech is all about capturing customer In the payments world, Visa and Mastercard

and Target stores, some 11,000 locations, would data and translating this into the opportunity are no strangers to such accusations, with

accept its digital wallet – and also declared to pay securely, then the world’s largest online allegations of alleged anti-competitive practices

that Apple Pay now reaches 60 percent of US marketplace should be best placed to lead echoing around the globe over the last twenty

retail locations. the charge. Amazon’s move into financial years. However, these allegations are yet to

Since then, Apple has proceeded to notch services is not limited to payments: in recent dampen Big Tech’s enthusiasm for payments,

further acceptance deals in France, Australia years, the company has launched a small- least of all at Google.

and Ireland that bolster its network. As Jennifer business lending platform offering loans of Although the search giant may appear a

Bailey, Vice-President of Internet Services at up to $750,000, with more than $3 billion in blushing debutante next to more brash public

Apple Pay, put it to Time magazine late last loans to 205,000 small businesses. A suite of statements by its peers, Google’s comparatively

year: “Our aim is to replace the physical wallet personal insurance products – Amazon Protect low profile may speak to a more considered

altogether. Payments are something people do – is now available, and the firm has begun approach. Despite lagging behind Samsung and

every day … this is all about making people love establishing a physical presence to match its Apple in the US digital wallet market, with only

their iPhones.” virtual dominance. Following its well-flagged 11 percent market share, GooglePay has now

Bailey’s statement masks a more frank purchase of WholeFoods, which integrated enabled P2P payments and debit payments for

strategic intent – the need to make money for grocery payments with customer loyalty offers, GooglePay, making it a comprehensive digital

investors. Whether measured by growth rate or the company set up 25,000 “Amazon Cash” solution from physical wallet payments via tap

profit margin, Apple Pay is a growth machine, kiosks in 7/11 and CVS stores across the US. to online debit. GooglePay is now more likely to

with revenue and profitability growth, if not Amazon Cash helps the underbanked to shop be used for debit transactions than either Venmo

raw dollar numbers, now outstripping Apple’s on-line by topping up their virtual amazon or Zelle in the US, demonstrating customer

hardware and software (see Figure 1). As Apple accounts using cash. enthusiasm for this model.

Pay continues its rise, the iPhone is faltering, Amazon’s financial services offering goes In January 2019, Google announced that it

with sales down 15 percent in Q4 2018. It’s on – branded US credit cards with Citibank; would be trialling non-tap contactless payments

www.paymentscm.com payments cards & mobile magazine - march / april 2019 15You can also read