Before the Bell An Ameriprise Investment Research Group Publication Nov. 24, 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

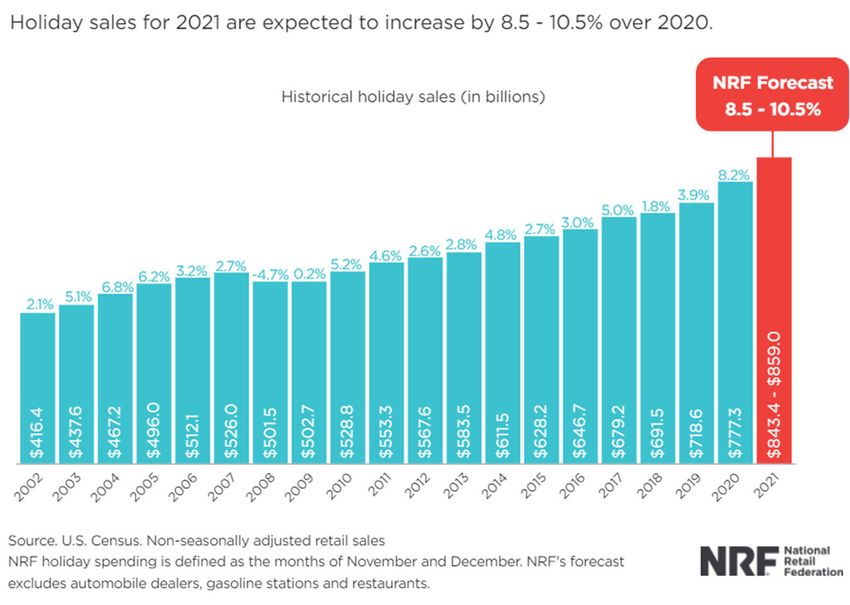

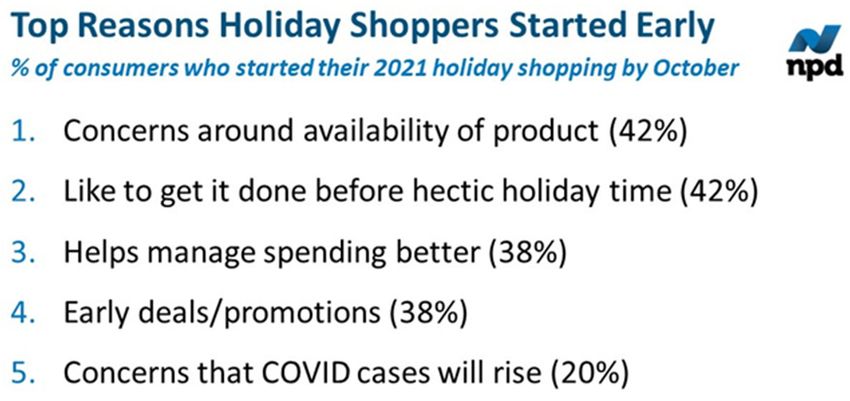

Before the Bell An Ameriprise Investment Research Group Publication Nov. 24, 2021 Starting the Day U.S. futures pointing to a lower open Asian equities finished mixed overnight European equities mostly lower on COVID fears 10-year Treasury yield flat at +1.66% Germany considering a COVID lockdown West Texas Intermediate (WTI) oil trading flat at $78.40 Market Perspectives Patrick Diedrickson, CFA, Senior Consumer Analyst In addition to comments related to overnight activity and pre-market conditions, each Wednesday, we feature commentary from members of the Ameriprise Global Asset Allocation Committee discussing investment considerations targeting their specific area of expertise. The comments are intended to provide additional insight into Committee allocation recommendations. Black Friday Versus Cyber Monday?: The holiday season is defined as the period between Thanksgiving and Christmas that comprises peak season shopping for most of the retail industry. Traditionally, the holiday season starts the day after Thanksgiving on Black Friday, and it is typically a day of large promotions by retailers with heavy discounts. Typically, Black Friday is one of the busiest shopping days of the year, and the sales performance generated on Black Friday is often considered a leading indicator for the strength of retail sales for the overall holiday season, as well as the fourth quarter. According to NPD, Black Friday has been the busiest shopping day of the year for each of the last three years. Cyber Monday is the first Monday after Thanksgiving, and it is often seen as the kickoff of the online holiday shopping season. Many online retailers use Cyber Monday to launch big promotions to drive online traffic and sales activity. Cyber Monday has been the second busiest shopping day of the year for each the last three years, according to NPD. We believe holiday season shoppers are prepared to start early in 2021 to make sure gifts are under the tree in time for Christmas. The well-publicized port disruptions are having a material impact on shipping times. According to a survey by Shopkick, 22% of consumers said they plan to start their 2021 holiday season shopping earlier than last year, with 10% expected to complete most of their shopping before Halloween and 25% before Thanksgiving. We believe mall traffic could increase materially during the 2021 holiday season because holiday season shoppers want to avoid shipping delays and ensure that gifts are under the tree in time for Christmas. According to data from Adobe, out of stock messages from online retailers have increased 172% heading into the holiday season compared to the pre-pandemic period. The apparel category has the highest out-of-stock levels currently, followed by sporting goods, baby products and electronics. The graphic at right is sourced from NPD Group. In our view, holiday season promotional activity could be less than previous years because longer shipping times have led to low inventory levels for NOTE: FOR IMPORTANT DISCLOSURES, INCLUDING POSSIBLE CONFLICTS, PLEASE SEE THE DISCLOSURE PAGES AT THE END OF THIS DOCUMENT. © 2021 Ameriprise Financial, Inc. All rights reserved.

Before the Bell - Nov. 24, 2021 | Page 2

several retailers. Typically, reduced

promotional activity could lead to higher

gross profit margin for retailers, but we

believe higher labor costs and increased

shipping costs could lead to relatively flat

gross margins this holiday season.

According to the Adobe Digital Economy

Index, U.S. consumers are estimated to

pay an average of 9% more year/year

during Cyber Week this year. Adobe

estimates 2021 overall holiday season

discounts to be approximately 5%-to-25%

compared to the historical average of

10%-to-30%. The graphic at right is

sourced from the National Retail

Federation.

According to data from Adobe, some of

the top sales performing toys for the 2021

holiday season are estimated to be The

Tamagotchi Pix, Pop Fidget, Got2Glow Fairy Finder, Baby Yoda, and Gabby’s Dollhouse. Adobe estimates other top

performing holiday season gifts could be the Nintendo Switch OLED, PlayStation 5, Xbox Series S/X, Airpods Max, smart

mugs, Instant Pot, smart water bottles, Metroid Dread, Battlefield 2042, Pokemon Brilliant Diamond & Shining Pearl, drones,

and record players.

We maintain our view that the overall fundamental outlook remains favorable for the retail industry. In our view, this could

potentially be one of the best holiday seasons in at least 10 years, and we project retail industry sales could exceed 10%

year/year growth. The Ameriprise Global Asset Allocation Committee has an Equalweight rating on the Consumer

Discretionary sector.

U.S. Pre-Market Indicators / Overnight International Market Activity

United States: Equity markets are set to open lower on Wednesday following some lower than Street projected earnings

results from retailers. The retailers primarily cited supply or supply chain issues rather than demand.

Europe: European markets are mostly lower amid fears that Germany, the largest economy in the region may join

Austria and put its economy on lockdown to stem the tide of a significant COVID outbreak . France’s CAC 40 index

was down 0.3%, and Germany’s DAX 30 was 0.6% lower, while in London the FTSE 100 gained 0.1%.

Asia-Pacific: Equities were mostly lower in Asia on Wednesday. In Japan, the Nikkei 225 closed 1.6% lower. The

Shanghai composite closed 0.1% higher. The Hang Seng Index in Hong Kong was up 0.1%. South Korea’s KOSPI

index was down 0.1%.

This space intentionally left blank.

© 2021 Ameriprise Financial, Inc. All rights reserved.

Before the Bell - Nov. 24, 2021 | Page 3

WORLD CAPITAL MARKETS

11/24/2021 As of: 8:30 AM ET

Americas % chg. % YTD Value Europe (Intra-day) % chg. %YTD Value Asia/Pacific (Last Night) % chg. %YTD Value

S&P 500 0.2% 26.5% 4,690.7 DJSTOXX 50 (Europe) -0.4% 23.2% 4,267.4 Nikkei 225 (Japan) -1.6% 8.4% 29,302.7

Dow Jones 0.5% 19.0% 35,813.8 FTSE 100 (U.K.) 0.2% 16.4% 7,277.7 Hang Seng (Hong Kong) 0.1% -7.0% 24,685.5

NASDAQ Composite -0.5% 23.2% 15,775.1 DAX Index (Germany) -0.7% 15.4% 15,825.0 Korea Kospi 100 -0.1% 4.7% 2,994.3

Russell 2000 -0.1% 18.8% 2,327.9 CAC 40 (France) -0.3% 29.4% 7,022.5 Singapore STI 0.0% 17.1% 3,227.2

Brazil Bovespa 0.0% -12.9% 103,648 FTSE MIB (Italy) 0.0% 21.2% 26,937.0 Shanghai Comp. (China) 0.1% 3.4% 3,592.7

S&P/TSX Comp. (Canada) 0.2% 26.0% 21,453.8 IBEX 35 (Spain) -0.1% 11.4% 8,810.2 Bombay Sensex (India) -0.6% 23.4% 58,341.0

Mexico IPC 1.2% 18.3% 51,116.3 MOEX Index (Russia) -0.4% 25.7% 3,944.8 S&P/ASX 200 (Australia) -0.2% 17.8% 7,399.4

Global % chg. % YTD Value Developed International % chg. %YTD Value Emerging International % chg. %YTD Value

MSCI All-Country World Idx -0.2% 18.0% 749.2 MSCI EAFE -0.7% 10.6% 2,311.1 MSCI Emerging Mkts -0.5% -0.8% 1,255.4

Note: International market returns shown on a local currency basis. The equity inde x data shown above is o n a to tal return basis, inclusive o f dividends.

S&P 500 Sectors % chg. % YTD Value Equity Income Indices % chg. % YTD Value Commodities

Communication Services -0.4% 22.9% 270.5 JPM Alerian MLP Index 1.6% 32.1% 183.3 Futures & Spot (Intra-day) % chg. % YTD Value

Consumer Discretionary -0.6% 27.7% 1,654.0 FTSE NAREIT Comp. TR 0.8% 32.4% 26,819.2 CRB Raw Industrials 0.4% 27.6% 651.6

Consumer Staples 0.7% 11.8% 761.2 DJ US Select Dividend 0.8% 29.4% 2,828.0 NYMEX WTI Crude (p/bbl.) -0.3% 61.4% 78.3

Energy 3.0% 57.6% 432.1 DJ Global Select Dividend 0.0% 20.6% 249.1 ICE Brent Crude (p/bbl.) -0.2% 58.6% 82.1

Financials 1.5% 38.2% 667.3 S&P Div. Aristocrats 0.3% 22.7% 4,089.2 NYMEX Nat Gas (mmBtu) -0.2% 95.3% 5.0

Health Care 0.1% 18.1% 1,541.9 Spot Gold (troy oz.) -0.1% -5.9% 1,786.8

Industrials 0.2% 21.1% 896.3 Spot Silver (troy oz.) -0.6% -10.9% 23.5

Materials 0.1% 23.7% 555.4 Bond Indices % chg. % YTD Value LME Copper (per ton) -0.3% 26.5% 9,805.0

Real Estate 1.1% 35.6% 302.7 Barclays US Agg. Bond -0.4% -2.4% 2,333.9 LME Aluminum (per ton) -0.9% 35.2% 2,668.5

Technology -0.2% 30.5% 2,965.3 Barclays HY Bond -0.4% 3.8% 2,427.2 CBOT Corn (cents p/bushel) 0.7% 34.6% 592.5

Utilities 0.1% 10.6% 343.1 CBOT Wheat (cents p/bushel) 0.1% 35.2% 868.8

Foreign Exchange (Intra-day) % chg. % YTD Value % chg. % YTD Value % chg. % YTD Value

Euro (€/$) -0.4% -8.3% 1.12 Japanese Yen ($/¥) 0.0% -10.3% 115.16 Canadian Dollar ($/C$) -0.2% 0.2% 1.27

British Pound (£/$) -0.2% -2.3% 1.34 Australian Dollar (A$/$) -0.3% -6.3% 0.72 Swiss Franc ($/CHF) -0.3% -5.4% 0.94

Data/Price Source: Bloomberg. Equity Index data is total return, inclusive of dividends, where applicable.

Global Equity Regions - Tactical Views

MSCI All-Country GAAC GAAC MSCI All-Country GAAC GAAC

World Index GAAC Tactical Recommended World Index GAAC Tactical Recommended

Weight Tactical View Overlay Weight Weight Tactical View Overlay Weight

United States 58.4% Overweight 3.0% 61.4% Latin America 0.9% Equalweight - 0.9%

Europe ex U.K. 13.2% Overweight 3.0% 16.2% Asia-Pacific ex Japan 14.2% Underweight -2.0% 12.2%

United Kingdom 3.5% Equalweight - 3.5% Japan 6.0% Underweight -3.0% 3.0%

Canada 2.8% Equalweight - 2.8% Middle East / Africa 1.0% Underweight -1.0% 0.0%

as of: September 30, 2021

Index weightings are based on the regional market capitalizations of the MSCI All-Country World Index as of 09/24/2021. The GAAC Tactical Overlay, as well as the Recommended Tactical Weights, are derived

from the Ameriprise Global Asset Allocation Committee (GAAC). Views are expressed relative to the Index and are provided to represent investment conviction in each region. Tactical Allocations are designed to

augment Index returns over a 6-12 month time horizon. Numbers may not add due to rounding.

Ameriprise Global Asset Allocation Committee (GAAC)

U.S. Equity Sector - Tactical Views

S&P 500 GAAC GAAC S&P 500 GAAC GAAC

Index GAAC Tactical Recommended Index GAAC Tactical Recommended

Weight Tactical View Overlay Weight Weight Tactical View Overlay Weight

Information Technology 28.1% Overweight 2.0% 30.1% Communication Services 11.2% Equalweight - 11.2%

Financials 11.2% Overweight 2.0% 13.2% Energy 2.6% Equalweight - 2.6%

Industrials 8.0% Overweight 2.0% 10.0% Real Estate 2.6% Equalweight - 2.6%

Health Care 13.4% Equalweight - 13.4% Materials 2.6% Equalweight - 2.6%

Consumer Discretionary 12.3% Equalweight - 12.3% Consumer Staples 5.7% Underweight -4.0% 1.7%

Utilities 2.5% Underweight -2.0% 0.4%

As of: September 30, 2021

Index weightings represent the respective market capitalization of each sector in the S&P 500 as of 09/24/2021. The GAAC Tactical Overlay, as well as Recommended Tactical Weights, is derived from the Ameriprise Global

Asset Allocation Committee (GAAC).Views are expressed relative to the Index and are provided to represent investment conviction in each region. Tactical Allocations are designed to augment Index returns over a 6-12

month time horizon. Numbers may not add due to rounding.

© 2021 Ameriprise Financial, Inc. All rights reserved.

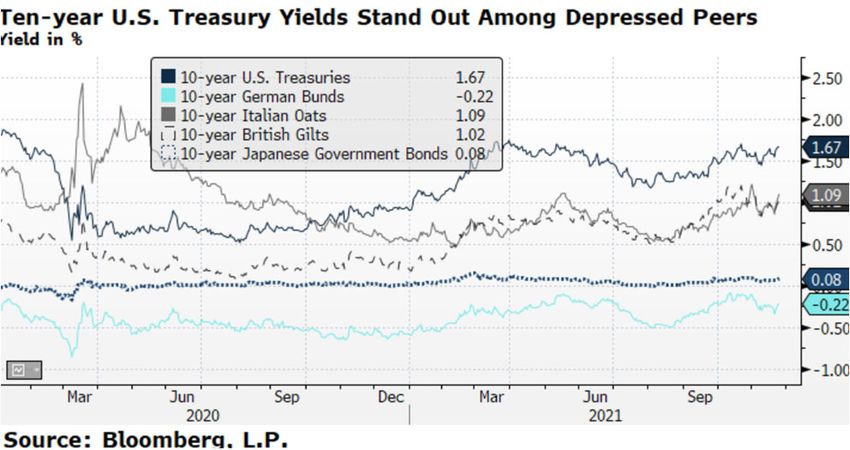

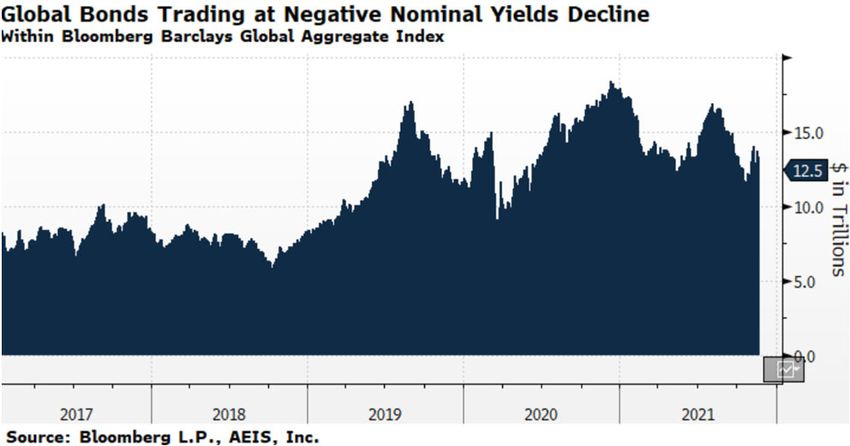

Before the Bell - Nov. 24, 2021 | Page 4 Fixed Income Perspectives Brian M. Erickson, CFA – Vice President, Fixed Income Strategy U.S. bond markets close for the Thanksgiving Holiday Thursday, and close early at 2:00 PM ET on Friday. Taking Stock of the Bond Market: Heading into the final five weeks of 2021, we reflect on where we stand today for global bond markets as context for where we may start the new year. The pace of growth, inflation and economic reopening leave nations, both developed and emerging, still firmly in a multi-speed recovery. Year to date the Bloomberg US Aggregate Index provided a -2.4% total return as the rise in Treasury yields and steepening of the Treasury curve proved too much headwind for the modest coupons hig- quality bonds offer today. Copious amounts of liquidity supported bond markets and economies as the pandemic made several trips around the world. As a result, risk assets, including US High Yield Bonds destinations for incremental funds. Bloomberg’s US High Yield Index outperformed the US Aggregate with a 3.8% total return. The JPMorgan Emerging Market Bond Index lagged with a -2.7% year-to-date total return, but stocks were the winner with the S&P 500 up 24.8% year to date as of this morning. Looking at 10-year global sovereign debt yields, we see greater dispersion than at the start of 2021, which makes sense given the unique challenges of inflation and reopening in each region. Though 10-year yields in the U.S., Britain and Italy progressed somewhat higher, yields on German and Japan debt remained anchored, leading to a still quite sizable $12.5 trillion of global debt trading at a negative yield. At the start of 2022, we see the multi-speed recovery reflected even in developed sovereign debt markets. While global monetary policy likely evolves through next year, we believe the liquidity deployed in 2020 likely takes 12 to 24 months to reabsorb, leaving risk assets poised to outperform. Economic News and Views: Russell T. Price, CFA – Chief Economist Releases for Wednesday, November 24, 2021 All times Eastern. Consensus estimates via Bloomberg Time Period Release Consensus Est. Actual Prior Revised to 8:30 AM Nov. 20 Initial Claims 260k 199k 268k 270k 8:30 AM Nov. 13 Continuing Claims 2030k 2049k 2080k 8:30 AM Q3-S Q3-Real GDP – Second Estimate +2.2% +2.1% +2.0% 8:30 AM Q3-S Q3 Personal Consumption +1.6% +1.7% +1.6% 8:30 AM OCT Advance Goods Trade Balance -$95.0B -82.9B -96.3B 8:30 AM OCT New Orders for Durable Goods (MoM) +0.2% -0.5% -0.3% 8:30 AM OCT Durables Ex. Transports (MoM) +0.5% +0.5% +0.5% 10:00 AM OCT Personal Income (MoM) +0.2% -0.3% 10:00 AM OCT Personal Spending (MoM) +1.0% +0.6% 10:00 AM OCT PCE Deflator (MoM) +0.7% +0.3% 10:00 AM OCT Core PCE Deflator (MoM) +0.4% +0.2% 10:00 AM OCT Core PCE Deflator (YoY) +4.1% +3.6% © 2021 Ameriprise Financial, Inc. All rights reserved.

Before the Bell - Nov. 24, 2021 | Page 5

10:00 AM OCT New Home Sales (annualized) 800k 800k

10:00 AM OCT New Home Sales (MoM) +0.0% +14.0%

10:00 AM Nov. F U. of M. Consumer Sentiment 67.0 66.8

Commentary:

Generally good economic data this morning. Of particular note, last week’s new claims for unemployment

insurance were their lowest since 1969, according to Bloomberg.

Additionally, the rather sharp narrowing of the

October trade deficit for Goods is a good sign for

Q4 real GDP estimates.

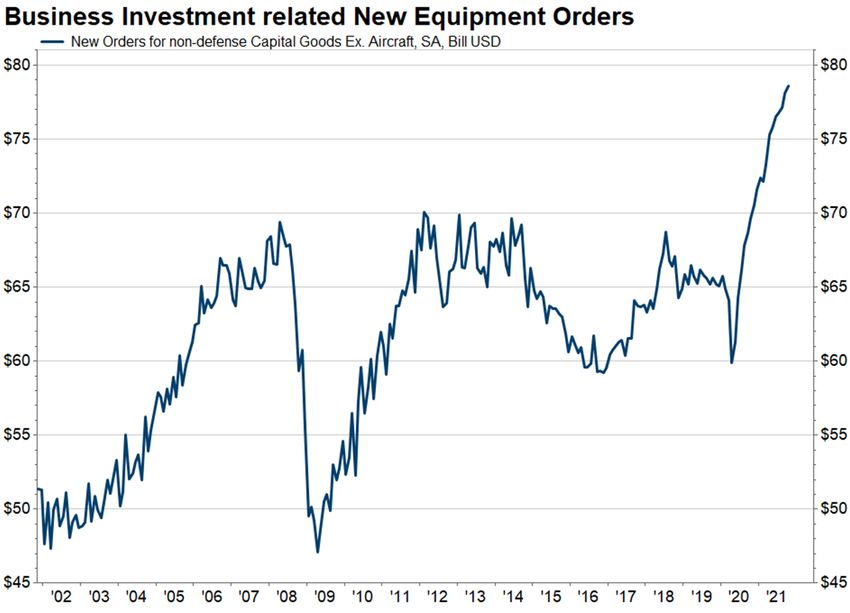

Total New Orders for Durable Goods meanwhile

were light on the top-line due to weaker orders for

civilian aircraft. The weakness is primarily

reflective of the ongoing issues at Boeing. Orders

for new vehicles and parts, meanwhile jumped

4.8% in October following two straight months of

rather material declines. The increased orders

may be an indication that auto makers are

signaling a potential near-term improvement in

production volumes (thus taking the orders). The

chart at right is sourced from FactSet and HAS

been updated to reflect today’s release.

New orders for Non-defense Capital Goods

Excluding Aircraft, the commonly used proxy for

business investment spending were up 0.6% in the month (see comments below) and growing at a 3-month

annualized pace of +8.7% through the month.

Shortages of product and labor have businesses scrambling to invest. One of the key measures offered by the

monthly Durables report is that of new orders for business equipment and machinery; specifically, “new orders for

non-defense capital goods excluding aircraft.” See chart above.

As seen in the chart, orders for such equipment have increased significantly during the COVID period as businesses

scramble to address supply shortages with added capacity. Labor shortages have also been a factor as businesses

look to improve the productivity of the workers they have.

So, are we finally at the point where machines are replacing humans more noticeably in many industries? Yes and

no, in our view. As we are all well aware, such transitions have been occurring for decades. Yet despite ever

increasing mechanization and automation, labor was already tight before the pandemic and is now even tighter as

many businesses cannot find the workers they need.

We believe there’s little doubt that mechanization and artificial intelligence will steadily increase over time.

However, such moves are necessary to expand worker productivity as to maintain economic growth above a simply

growing at the same pace as the labor force – which has slowed considerably from decades past and will continue

to slow based on demographic projections. Simply put, low unemployment CAN coexist with rising technology

utilization to boost worker productivity and economic growth, in our view.

This space intentionally left blank.

© 2021 Ameriprise Financial, Inc. All rights reserved.

Before the Bell - Nov. 24, 2021 | Page 6

Ameriprise Economic Projections

Forecast: Full-year Quarterly

Actual Actual Est. Est. Actual Actual Actual Actual Est. Est. Est.

2019 2020 2021 2022 Q4-2020 Q1-2021 Q2-2021 Q3-2021 Q4-2021 Q1-2022 Q2-2022

Real GDP (YOY) 2.3% -3.4% 5.4% 4.5% 4.5% 6.3% 6.7% 2.0% 6.0% 4.5% 5.0%

Unemployment Rate 3.5% 6.7% 4.5% 3.5% 6.7% 6.0% 5.9% 4.8% 4.3% 4.0% 3.7%

CPI (YoY) 1.8% 1.3% 6.0% 2.5% 1.3% 2.6% 5.4% 5.4% 6.9% 6.2% 4.2%

Core PCE (YoY) 1.7% 1.4% 4.1% 2.6% 1.5% 2.0% 3.6% 3.6% 4.4% 4.5% 3.1%

So urces: Histo rical data via FactSet. Estimates (Est.) via A merican Enterprise Investment Services Inc.

Yo Y = Year-o ver-year, Unemplo yment numbers are perio d ending. GDP : Gro ss Do mestic P ro duct; CP I: Co nsumer P rice Index

P CE: P erso nal Co nsumptio n Expenditures P rice Index. Co re excludes fo o d and energy.

A ll Q ua rt e rly e s t im a t e s o t he r t ha n G D P a re pe rio d e nding . Last Updated: Novem ber 22, 2021

Chronological Forecast Adjustments: Russell T. Price, CFA – Chief Economist

GDP: (10/29/2021): Actual real GDP for Q3 came-in at +2.0% - moderately below our estimate of +2.4%. Reduced

business spending on automobiles (largely due to lack of availability) was the most prominent factor in the shortfall

versus our expectations, while higher than estimated import activity (which is a negative contributor to GDP) also weighed

on the results more than we anticipated.

To the positive, consumer spending was notably stronger than we expected. We were forecasting a +0.5% qtr/qtr. pace

of expansion whereas the Commerce Department report showed a strong +1.6% gain. The Commerce Department

attributed the strength to a strong return of international travel spending late in the quarter.

Overall, the slowdown in Q3 was primarily due to the Delta-variant’s negative impact on domestic consumer and business

spending. Some items, particularly automobiles, remained unavailable in the quantities desired by consumers and

businesses due to infection outbreaks elsewhere in the world.

Inflation: (10/7/2021): We hiked our inflation forecast modestly. Our headline CPI gets a boost due to rising energy

prices while our Core PCE estimate gets a boost from hotter than forecast gain in core prices during August. More

goods and services are experiencing shortages but the recent moderation in the pace of growth should help ease such

upward price pressures over the intermediate-term.

Ameriprise Global Asset Allocation Committee Targets and Views

Targets

Outlook Commentary: Anthony M. Saglimbene, Global Market Strategist

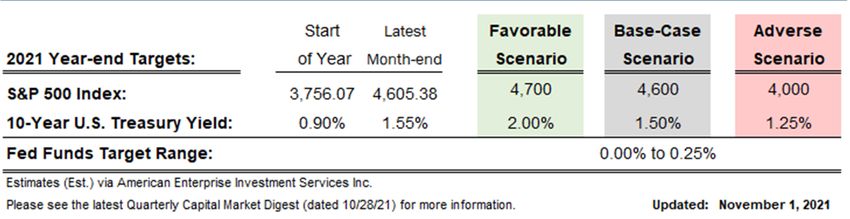

November 10: The S&P 500 could finish the year above our base and favorable targets. In our view, that's a win for investors.

We doubt investors would find much value in an S&P 500 target adjustment that attempts to predict the last several weeks

of the year after the Index has already posted such substantial gains in 2021. Thus, we are comfortable leaving our S&P 500

targets unchanged through the rest of the year and recognize the market's bias could be higher than we forecast in July (the

last time we changed our S&P 500 targets). And while the final S&P 500 level this year may fall outside our base and favorable

targets, the current messaging and direction around our targets (and the scenario forecasts found in the latest Quarterly

Capital Market Digest) should remain applicable through year-end.

© 2021 Ameriprise Financial, Inc. All rights reserved.

Before the Bell - Nov. 24, 2021 | Page 7

Recommended Weightings

Note: Our Tactical Allocations are designed to augment a Strategic portfolio over a 6-12-month time horizon. Asset Allocation and diversification

do not ensure or guarantee better performance and do not eliminate the risk of investment losses. Investors should note that rising interest

rates could have a detrimental effect on bond prices. Please consult with your financial advisor. Cash generally refers to assets, securities

and/or products low in risk and highly liquid. For asset allocation purposes, instruments can include Treasury bills, certificates of deposit, money

market funds and high-quality bonds whose maturities are less than 3 months. Outside of asset allocation purposes, cash investments can also

include illiquid cash held in a mutual fund or pledged as collateral for derivatives. You can only access this cash by redeeming the fund using it,

subject to fees or time constraints associated with redemptions.

This space intentionally left blank.

© 2021 Ameriprise Financial, Inc. All rights reserved.

Before the Bell - Nov. 24, 2021 | Page 8

The Ameriprise Investment Research Group

With Ameriprise Financial, you can benefit from our dedicated team of experienced investment research and due diligence

professionals. Our objective market insight, strategies and guidance are designed to provide you with investment strategies

and solutions to help you feel more confident about your financial future. It’s the higher level of sophistication and service

you’ve come to expect from Ameriprise.

Research and Manager Fixed income

due diligence leader research research and strategy

Lyle B. Schonberger Michael V. Jastrow, CFA Brian M. Erickson, CFA

Vice President Vice President Vice President

Business Unit Compliance Liaison Mark Phelps, CFA Jon Kyle Cartwright

Jeff Carlson, CLU, ChFC Director – Multi-asset solutions Sr Director – High yield and investment grade

Sr Manager credit

ETFs, CEFs, UITs

Kimberly K. Shores Jeffrey R. Lindell, CFA Stephen Tufo

Investment Research Coordinator Director Director – High yield and investment grade

credit

®

Jillian Willis James P. Johnson, CFA, CFP

Sr Administrative Assistant Sr Analyst

Alternatives Retirement

Strategists Justin E. Bell, CFA

Vice President – Quantitative research and

research

alternatives

Chief Market Strategist Open

Kay S. Nachampassak Vice President

David M. Joy Director

Vice President Open

Quantitative research Director

Global Market Strategist

Kurt J. Merkle, CFA, CFP®, CAIA

Anthony M. Saglimbene Sr Director

Matt Morgan

Vice President Sr Manager

Peter W. LaFontaine

Thomas Crandall, CFA, CMT, CAIA Sr Analyst

Sr Director – Asset allocation

David Hauge, CFA

Cedric Buermann Jr., CFA Analyst

Analyst – Quantitative, Asset allocation

Blake Hockert

Gaurav Sawhney Sr Associate

Research Analyst

Bishnu Dhar

Amit Tiwari, CFA Sr Research Analyst

Sr Research Associate

Parveen Vedi

Chief Economist Sr Research Associate

Russell T. Price, CFA

Vice President Darakshan Ali

Research Process Trainee

Equity Equities

Christine A. Pederson, CAIA, CIMA

research Sr Director – Growth equity, infrastructure and

REIT

Justin H. Burgin Benjamin L. Becker, CFA

Vice President Director – International and global equity

Patrick S. Diedrickson, CFA Cynthia Tupy, CFA

Director – Consumer goods and services Director – Value equity and equity income

William Foley, ASIP Open

Director – Energy and utilities Analyst – Core equity

Lori Wilking-Przekop

Sr Director – Financial services and REITs Fixed income

Steven T. Pope, CFA, CFP®

Daniel Garofalo Sr Director – Non-core fixed income

Director – Health care

Douglas D. Noah, CFA

Frederick M. Schultz Sr Analyst – Core taxable and tax-exempt fixed

Director – Industrials and materials income

Open

Director – Quantitative strategies and

international

Andrew R. Heaney, CFA

Technology and Communication Services

© 2021 Ameriprise Financial, Inc. All rights reserved.

Before the Bell - Nov. 24, 2021 | Page 9

The content in this report is authored by American written request to Ameriprise Financial, Inc., 1441 West

Enterprise Investment Services Inc. (“AEIS”) and Long Lake Road, Troy MI, 48098. Independent third party

distributed by Ameriprise Financial Services, LLC (“AFS”) research on individual companies is available to clients at

to financial advisors and clients of AFS. AEIS and AFS ameriprise.com/research-market-insights/. SEC filings

are affiliates and subsidiaries of Ameriprise Financial, Inc. may be viewed at sec.gov.

Both AEIS and AFS are member firms registered with

FINRA and are subject to the objectivity safeguards and Investors should consider the investment objectives,

disclosure requirements relating to research analysts and risks, charges and expenses of a mutual fund or

the publication and distribution of research reports. The exchange traded fund (ETF) carefully before investing.

“Important Disclosures” below relate to the AEIS research For a free prospectus, which contains this and other

analyst(s) that prepared this publication. The “Disclosures important information about the funds, please contact

of Possible Conflicts of Interest” section, where your financial advisor. The prospectus should be read

applicable, relates to the conflicts of interest of each of carefully before investing.

AEIS and AFS, their affiliates and their research analysts, Tactical asset class recommendations mentioned in this

as applicable, with respect to the subject companies report reflect The Ameriprise Global Asset Allocation

mentioned in the report. Committee’s general view of the financial markets, as of

Each of AEIS and AFS have implemented policies and the date of the report, based on then current conditions.

procedures reasonably designed to ensure that its Our tactical recommendations may differ materially from

employees involved in the preparation, content and what is presented in a customized long-term financial

distribution of research reports, including dually plan or portfolio strategy. You should view our

registered employees, do not influence the objectivity or recommendations in conjunction with a broader long-

timing of the publication of research report content. All term portfolio strategy. Not all products, services, or asset

research policies, coverage decisions, compensation, classes mentioned in this report may be available for sale

hiring and other personnel decisions with respect to at Ameriprise Financial Services, Inc. Please consult with

research analysts are made by AEIS, which is your financial advisor.

operationally independent of AFS. Diversification and Asset Allocation do not assure a

profit or protect against loss.

Important disclosures

As of September 30, 2021 Risk Factors

The views expressed regarding the company(ies) and Dividend and interest payments are not guaranteed. The

sector(s) featured in this publication reflect the personal amount of dividend payment, if any, can vary over time

views of the research analyst(s) authoring the publication. and issuers may reduce or eliminate dividends paid on

Further, no part of research analyst compensation is securities in the event of a recession or adverse event

directly or indirectly related to the specific affecting a specific industry or issuer. Should a company

recommendations or views contained in this publication. be unable to pay interest on a timely basis a default may

occur and interruption or reduction of interest and

A part of a research analyst’s compensation may be principal occur. Investments in a narrowly focused sector

based upon overall firm revenue and profitability, of which may exhibit higher volatility than investments with broader

investment banking, sales and trading, and principal objectives and is subject to market risk and economic

trading are components. No part of a research analyst’s risk.

compensation is based on a specific investment banking

transaction, nor is it based on sales, trading, or principal Income Risk: We note that dividends are declared solely

trading. A research analyst may have visited the material at the discretion of the companies’ boards of directors.

operations of one or more of the subject companies Dividend cuts or eliminations will likely negatively impact

mentioned in this research report. No payment was underlying company valuations. Published dividend yields

received for the related travel costs. are calculated before fees and taxes. Dividends paid by

foreign companies to ADR holders may be subject to a

Additional information and current research disclosures withholding tax which could adversely affect the realized

on individual companies mentioned in this research report dividend yield. In certain circumstances, investors in ADR

are available on our website at shares have the option to receive dividends in the form of

ameriprise.com/legal/disclosures in the Additional cash payments, rights shares or ADR shares. Each form

Ameriprise research disclosures section, or through of dividend payment will have different tax consequences

your Ameriprise financial advisor. You may also submit a

© 2021 Ameriprise Financial, Inc. All rights reserved.

Before the Bell - Nov. 24, 2021 | Page

and therefore generate a different yield. In some company’s equity and that trade similarly to domestic

instances, ADR holders are eligible to reclaim a portion of equities, and are either listed on an exchange or over-

the withholding tax. the- counter. As with any equity investment, ADRs are

subject to market and company specific risks. ADRs will

International investing involves increased risk and also be subjected to foreign market risks. These risks

volatility due to political and economic instability, currency include possible losses due to foreign currency

fluctuations, and differences in financial reporting and translation, geopolitical instability, and deviations in the

accounting standards and oversight. Risks are market value of an ADR compared to that of the

particularly significant in emerging markets. underlying common shares in its primary market. ADRs

Market Risk: Model portfolios and markets in general may suffer from a lack of investor protection and

could sustain significant volatility due to several factors. recourse. In the event of a liquidation of the underlying

As we have seen recently, both economic and company, the holders of its ADRs are not guaranteed of

geopolitical issues could have a material impact on this being able to enforce their right of claim and therefore

model portfolio and the equity market as a whole. they may lose their entire investment. Investors of ADRs

may also take on risks associated with the parties

Sector Risk: The Ameriprise Global Asset Allocation involved with the sponsoring Bank.

Committee and managers of this model portfolio can elect

to overweight or underweight (or completely avoid) Alternative investments cover a broad range of strategies

certain economic sectors. This could lead to substantial and structures designed to be low or non-correlated to

underperformance versus a more diversified or balanced traditional equity and fixed-income markets with a long-

weighting. term expectation of illiquidity. Alternative investments

involve substantial risks and are more volatile than

Security Recommendation Risk: The research team traditional investments, making them more suitable for

may not be successful in selecting securities that investors with an above-average tolerance for risk.

collectively perform better than the benchmark. When

viewing return comparisons investors should keep in There are risks associated with fixed-income

mind the following information. Our model portfolio investments, including bond funds, such as credit risk,

generally maintains less than 50 securities, whereas interest rate risk, and prepayment and extension risk. In

benchmark indices contain several times that amount. general, bond prices rise when interest rates fall and vice

The benchmark index is market capitalization weighted, versa. This effect is usually more pronounced for longer-

providing greater weight to the larger company term securities.

movements, whereas our model portfolio is designed to Growth securities, at times, may not perform as well as

be equally dollar weighted. Furthermore, the model value securities or the stock market in general and may

portfolio may deviate significantly, at times, from the be out of favor with investors.

sector allocation of the benchmark due to our

interpretation of economic conditions and market factors International investing involves increased risk and

as well as our security selection process. volatility due to political and economic instability, currency

fluctuations, and differences in financial reporting and

The benchmark index returns are taken from Bloomberg accounting standards and oversight. Risks are enhanced

Financial Markets and reflect dividends reinvested. for emerging market issuers.

Additionally, there is no fee or cost assumption in the

index comparison return. Interest payments on inflation-protected securities may

be more volatile than interest payments on ordinary

Product Risk Disclosures bonds. In periods of deflation, these securities may

Corporate Bonds are debt instruments issued by a provide no income.

private corporation. Non-Investment grade securities,

commonly known as “high-yield” or “junk” bonds, are Index definitions

historically subject to greater risk of default, including the An index is a statistical composite that is not managed. It

loss of principal and interest, than higher-rated bonds, is not possible to invest directly in an index.

which may result in greater price volatility than

experienced with a higher-rated issue. Definitions of individual indices mentioned in this report

are available on our website at

American Depository Receipts (ADR) are securities ameriprise.com/legal/disclosures/ in the Additional

issued by a U.S. bank that typically represent a foreign

© 2021 Ameriprise Financial, Inc. All rights reserved.Before the Bell - Nov. 24, 2021 | Page Ameriprise research disclosures section, or through Ameriprise Financial Services, LLC. Member FINRA and your Ameriprise financial advisor. SIPC. Disclosures of potential conflicts of interest One or more members of the research team who prepared this research report may have a financial interest in securities mentioned in this research report through investments in a discretionary separately managed account program. Disclaimer section Except for the historical information contained herein, certain matters in this report are forward-looking statements or projections that are dependent upon certain risks and uncertainties, including but not limited to, such factors and considerations as general market volatility, global economic and geopolitical impacts, fiscal and monetary policy, liquidity, the level of interest rates, historical sector performance relationships as they relate to the business and economic cycle, consumer preferences, foreign currency exchange rates, litigation risk, competitive positioning, the ability to successfully integrate acquisitions, the ability to develop and commercialize new products and services, legislative risks, the pricing environment for products and services, and compliance with various local, state, and federal health care laws. See latest third-party research reports and updates for risks pertaining to a particular security. This summary is based upon financial information and statistical data obtained from sources deemed reliable, but in no way is warranted by Ameriprise Financial, Inc. as to accuracy or completeness. This is not a solicitation by Ameriprise Financial Services, LLC of any order to buy or sell securities. This summary is based exclusively on an analysis of general current market conditions, rather than the appropriateness of a specific proposed securities transaction. We will not advise you as to any change in figures or our views. Past performance is not a guarantee of future results. Investment products are not federally or FDIC- insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value. Third-party companies mentioned are not affiliated with Ameriprise Financial Services, LLC. Ameriprise Financial, Inc. and its affiliates do not offer tax or legal advice. Consumers should consult with their tax advisor or attorney regarding their specific situation. © 2021 Ameriprise Financial, Inc. All rights reserved.

You can also read