Banco Santander Chile - Institutional Presentation - December 2020

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Banco

Santander

Chile

Institutional Presentation

December 2020

1

AGENDA

MACROECONOMIC ENVIRONMENT

SOLID FINANCIAL SYSTEM WITH GROWTH POTENTIAL

SANTANDER CHILE: LEADING BANK

ADVANCES IN OUR STRATEGIC INITIATIVES

2

Macroeconomic environment

Economy based on low debt and high rating

Chile: Key economic indicators Economy is highly diversified1

GDP by economic sector, %

Population1: 19.7mm Mining

10.5%

GDP2: US$267 billion 11.5% Manufacturing

GDP per capita3 (PPP): US$23,366 3.5% Construction

5.1% 10.6%

Commerce

Exports / GDP2: 28%

5.7% Transportation

Investment / GDP2 : 20%

10.9% Services

Net public debt / GDP3: 11% 34.0% Public admin.

8.2%

JCR: AA- / Mdy: A1/ SP: A/ Fishing and agriculture

Sovereign ratings: Fch: A

Others

Low public debt High sovereign rating5

Gross public debt, % GDP3

USA

120 Australia

UK

77 Chile

63

33 China

Japan

Peru

Chile Adv. Latam EM Mexico

Economies Brazil Ba2 Ba3 Baa3 Baa2 Baa1 A3 A2 A1 Aa3 Aa2 Aa1 Aaa

3

3

1. INE 2. BCCh, 3. IMF. 4. Moodys

Macroeconomic environment

Our largest commercial partners are China and USA

Exports: US$73 billion Imports: US$60 billion

Chemicals Energy

Copper;

; 6.5 Others; 52 Capital goods 12%

13.2

Pulp and

22%

forestry;

By products

By products

6.7 2.5

Wine;

Salmon; Other

5.4 intermediary

Agro, Consumer goods

fishing; Other 38%

8.7 goods

minerals;

5 28%

South

America; Rest Asia Others

7% 4% North

Rest Asia; 10 China; 39

Japan America

12 22%

By country

By country 2%

Japan; 9

North China South Ameria

America; 28% 20%

Europe; 17

13

Europe 4

17%

1. Source: Banco Central de Chile(BCCh), December 2020

Macroeconomic environment

Evolution of the pandemic

Population under different phases of

Population vaccinated (% of total) confinement (% of total)

60 100%

One

Al dose

menos una dosis

Twodosis

Dos doses 53.5 90%

Otras

50

80% regiones

70%

40 40.7 Región metropolitana

60%

50%

30

40%

30%

20

20%

10 10%

0%

15-ago 15-oct 15-dic 15-feb 15-abr

0

ene-21 feb-21 mar-21 abr-21 may-21

Phase

Fase 11 Phase2 2

Fase Phase3 3

Fase Phase4 4 Phase

Fase Fase 5 5

Phase 1 is the strictest lockdown

5 5

Source: OWID and Santander

Macroeconomic environment

Strong economic recovery in 2021

GDP Terms of trade

YoY real growth, % 2013 = 100

124

7.5 119

3.5 111

1.1 106

103 102

98

-5.8 2016 2017 2018 2019 2020 2021 (f) 2022(f)

2019 2020 (e) 2021 (f) 2022 (f)

Inflation Central Bank Monetary Policy Rates

Annual CPI inflation, % %

3.6 1.75

3.0 3.0 3.0 1.50

0.50 0.50

2019 2020 2021 (f) 2022 (f) 2019 2020 2021 (f) 2022 (f)

6 6

Soruce: Banco Central de Chile and Santander Chile estimates 6

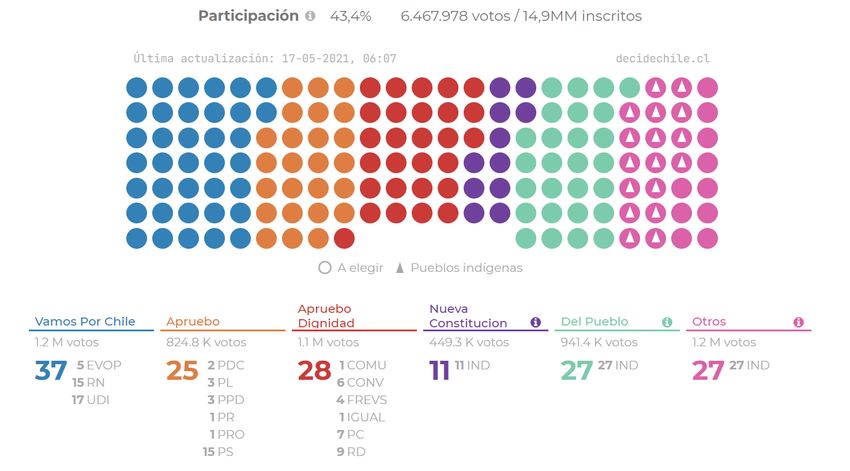

Macroeconomic environment

Composition of Constitutional Convention

Participation: 43.4% 6,467,978 votes/ 14.9 million signed up

-4.75

Political system

Social rights

Subsidiary role of the state

Autonomous bodies of the state

24% 16% 18% 7% 17% 17%

Center Center

right left Left

Traditional parties Independents

7 7

AGENDA

MACROECONOMIC ENVIRONMENT

SOLID FINANCIAL SYSTEM WITH GROWTH POTENTIAL

SANTANDER CHILE: LEADING BANK

ADVANCES IN OUR STRATEGIC INITIATIVES

8

Solid financial system

Solid financial system

87%

Of total loans

As of Dec. 2020 Ch$bn US$ bn

25 16 in Top 6

Assets 323,127 441.16 Banks in Banks in banks

financial Increased financial

Loans 189,092 252.70 system Concentration system

88%

Deposits 144,422 197.18 2009 2020 Of total loans

in Top 6

Equity 22,170 30.27 banks

Net income 1,242 1.70 Evolution of Return on Equity (%)

NIM 3.6% 34.9

Cost of credit 1.7%

NPL ratio 1.6% 21.6

16.4

Coverage ratio 218.1% 14.5

18.0 17.5

Efficiency ratio 51.4% 14.2

ROAA 0.4%

5.6

ROAE 5.6% 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Core capital 10.6%

Series1 Series2

BIS ratio 14.3%

No banking crisis in Chile since the beginning of the

1980’s thanks to prudent regulations and strong

supervisory bodies. 9

Source: CMF

Solid financial system

Financial indicators of the system 2020

Net income attr. to shareholders ROAE

Ch$bn Change YoY -53.5%

-6.3% 14.5%

-21.9% 1,179 12.8%

517 463 -21.2%

317 8.1%

-828.4%

5.4%

System System

-925 -5.7%

NIM Efficiency

4.0% 3.8%

3.4% 3.6% 533.0%

3.0%

44.6% 48.8% 51.4%

39.8%

System System

Soruce: CMF and Santander Chile estimates

10Solid financial system

Developed banking system with high growth potential

Loans to GDP (%)1

144

123

64 52 45 37

OECD Chile Brasil Colombia Peru Mexico

1 Loans to companies over GDP 2 Loans to individuals over GDP

The large corporates make up around 1% of all the The mortgage market is deep in Chile and many

companies, but have 80% of the total debt. households have long-term stable debt.

Commercial lending by type of client2 Debt households/GDP(%)3

38

93

62 48%

35%

7 17%

% number of debtors % of total debt

Chile Brasil Mexico

SME Corporates

1. Fuente: World Bank https://data.worldbank.org/indicator/FS.AST.PRVT.GD.ZS 2. Fuente: 3. Fuentes : https://tradingeconomics.com/country-list/households-

11

CMF dic 2020 debt-to-gdp?continent=america 09/2020Solid financial system

Calidad de activo estable durante distintos ciclos económicos

All financial institutions regulated by the CMF (previously the SBIF) use Chilean Bank GAAP as the accounting standard. The

main difference to other accounting standards is that under Chilean Bank GAAP, loan loss allowances are calculated based on

specific guidelines set by the local regulator, using an expected loss approach. Through the years, the local regulator has been

updating their standardized provisioning models, becoming more conservative. To date, the local regulator has announced

that it will not be adopting IFRS 9.

Total loans: Non-performing loans (NPL) and coverage (%)

2016: Standard 227%

2014: Changes to provisioning model July 2019: Standard

provisioning for mortgages (B1). provisioning model

models: Consumer Higher provisioning for SMEs (B1).

and Commercial for LTV > 90%

Economic Crisis

US and Europe 147%

136% 145%

12… 128% 130%

121% 123%

107%

89% 92%

84% Oct. 2019: Covid-19

73% Start of

social unrest

2.8% 2.9% 2.7% 2.6%

Feb 2010 Earthquake in 2.1% 2.0% 2.0% 2.0%

Maule Chile- 8.8Mw 1.8% 1.9% 1.9%

1.7%

and destructive Tsunami 1.4%

Mar-09

Mar-10

Mar-11

Mar-12

Mar-13

Mar-14

Mar-15

Mar-16

Mar-17

Mar-18

Mar-19

Mar-20

Jun-09

Jun-13

Jun-17

Jun-10

Jun-11

Jun-12

Jun-14

Jun-15

Jun-16

Jun-18

Jun-19

Jun-20

Dec-09

Dec-10

Dec-11

Dec-12

Dec-13

Dec-14

Dec-15

Dec-16

Dec-17

Dec-18

Dec-19

Dec-20

Sep-09

Sep-10

Sep-11

Sep-12

Sep-13

Sep-14

Sep-15

Sep-16

Sep-17

Sep-18

Sep-19

Sep-20

NPL (1) Coverage (2)

12

1. Loans with 90 days or more overdue. 2. Stock of provisions divided by NPLs. Source: CMFSolid financial system

Competition has been consolidating throughout the years

Total loans to clients by bank

Santander

BCI

Banco de Chile Santander’s

growth has been

Itaú Corpbanca organic

Scotiabank throughout the

years, but

recently

acquired

Santander

Consumer Chile,

Banco Ripley an autofinancing

jun-2013 jun-2014 jun-2015 jun-2016 jun-2017 jun-2018 jun-2019 jun-2020

company.

…

2013 2015 2015 2016 2018 2018 2018 2018 2019

Ripley Scotiabank BCI Itaú BCI buys Scotiabank BCI Falabella Santander

moves its buys acquires acquires over acquires acquires moves its acquires

credit card Cencosud’s City Corpbanca, Walmart’s BBVA TotalBank CMR credit Santander

business credit card National in becoming credit card in Florida, card Consumer

into Banco business Florida, Itaú business USA business Finance, and

Ripley USA Corpbanca into Banco autofinancing

Falabella company

13Solid financial system

BIS III requirements already published

Introducing new capital requirements Phase In

Pillar II

0% - 4%

T1 or T2

C. Cyclical Buffer

0% - 2.5%

RWA

Systemic Buffer

1% - 3.5%

RWA 10.5%

Conservation

Buffer

T2 2.5% RWA

8%

3.5% RWA T2 – 2.0% Publications

Subordinated** + RWA

AT1 – 1.5% Regulation Published

Provisions

RWA

Systemic buffer YES

CET1 CET1

AT1, Pref. Stocks and Tier II YES

4.5% RWA 4.5% RWA

Operational risk YES

Capital deductions YES

Conservation and countercyclical buffer YES

** Subordinated bonds allowed up to 50% of the CET1

Creidt risk YES

Subordinated bonds YES

Pref. Stocks and CoCos YES

In general the new local norm is aligned with BIS III, Leverage YES

however the greatest innovation are in credit risk and Pillar II YES

Market risk YES

systemic charge.

Pillar III YES

14AGENDA

MACROECONOMIC ENVIRONMENT

SOLID FINANCIAL SYSTEM WITH GROWTH POTENTIAL

SANTANDER CHILE: LEADING BANK

ADVANCES IN OUR STRATEGIC INITIATIVES

15A leading bank

Santander Chile is the nation’s leading bank

Business and Results 12M20 (US$) YoY

Gross Loans 48.3bn 5.1%

Deposits 35.3 bn 7.0%

Equity 5.1 bn 53%

Attributable profit (YTD)1 726 mn (6.3%)

Network and Customers 12M20 Market Share

Clients 3.6 mn 25.9%2

Digital Clients 1.5mn 32.0%3

Offices 358 19.0%

Market Share 12M20 Rank

Loans3 18.6% 1

Deposits3 17.4% 2

Checking accounts2 25.9% 1

Bank credit cards4 25.0% 1

1. Attributable profit to shareholders. 2. Market share of clients with checking accounts, as of Dec. 2020. Source: CMF . 4. Excludes loans and deposits of Chilean

banks held abroad as of Dec 2020 4. Average yearly market share over clients that enter a website with a passkey. Excludes Banco Estado. Source: CMF. YTD avg as

of Dec. 2020

16A leading bank

Santander Group’s first significant foreign endeavor was in Chile

1978 1982 1989-1990 1993 1996 2002 2010 2019 2020

……………………………………………………………………………………………………………..…………………………………………………….….

Banco Chilean After the Santander Santander Santander Chile suffers Santander buys The pandemic

Santander economy fails. economic crisis, acquires merges with merges with one of the 51% of hits Chile,

enters the All Banks Banco Fincard, Banco Osorno Banco largest Santander Santander is

Chilean intervened. Santander sold principal credit and la Unión, Santiago, earthquakes in Consumer the bank gives

market, Banco C part of its loan card processor becoming the reaching a the history of Chile, an auto the most help

opening a Santander buys portfolio to the in the country, largest bank in market share the world. financing to its clients,

subsidiary over Banco Central Bank. and enters the the country. of 25%. Santander was Company. through grace

mainly aimed Español Chile, Banco mass market. Loan market 100% periods and

at foreign in liquidation. Santander buys share reaches operative the FOGAPE.

trade. back all of the 12%. next working

loan portfolio day.

and changes its

name officially

to Banco

Santander Chile

17A leading bank

Ownership structure

Composition of shareholders

Minority shareholders

Acción

T Rowe Price Group Inc 3.2% EE.UU.

Local Schroders PLC 2.6% UK

15.62% A F P Provida S A 1.4% Chile

A F P Habitat S A 1.4% Chile

AFP JPMorgan Chase & Co 1.4% EE.UU.

5.29%

35.0% GOVERNMENT OF SINGAPORE*

A F P Cuprum S A

1.0% SINGAPUR

1.0% Chile

ADR

11.91% Total return local A F P Capital S A 0.9% Chile

Grupo Banchile Corredores de Bolsa S.A 0.9% Chile

Santander stock since 2015 Wells Fargo & Co 0.6% EE.UU.

67.18% B.C.I.Corredor de Bolsa S.A. 0.6% Chile

INCA Investments LLC 0.6% EE.UU.

AVIVA LIFE AND PENSIONS UK LIMITED* 0.5% UK

Harding Loevner LP 0.5% EE.UU.

Santander Group owns 67.2%. We are listed on the Santiago Stock Vanguard Group Inc/The 0.5% EE.UU.

Exchange and the NYSE Larrain Vial S.A.Corredora de Bolsa

Santander Corredores de Bolsa Limitada

0.5% Chile

0.5% Chile

BlackRock Inc 0.5% EE.UU.

Average daily volume traded NORGES BANK* 0.4% NORUEGA

Renaissance Technologies LLC 0.4% EE.UU.

(US$ millions) Standard Life Aberdeen PLC 0.4% UK

SAUDI ARABIAN MONETARY AUTHORITY* 0.4% SaudI Arabia

Bolsa de Comercio de Santiago Bolsa de V 0.4% Chile

14.6

NYSE +1,500

Contacts with investors

A F P Modelo S A

ISHARES MSCI CHILE ETF*

QSUPER*

SAS TRUSTEE CORPORATION POOLED FUND*

0.3% Chile

0.3% EE.UU.

0.3% AUSTRALIA

0.3% Australia

8.1 ISHARES CORE MSCI EMERGING MARKETS ETF* 0.3% EE.UU.

Bolsa de in the year Itau Unibanco Holding SA 0.2% Brazil

Btg Pactual Chile S.A.Corredores de Bolsa 0.2% Chile

7.3 Comercio UBS GLOBAL ASSET MANAGEMENT LIFE * 0.2% UK

Bice Inversiones Corredores de Bolsa S.A. 0.2% Chile

CALIFORNIA PUBLIC EMPLOYEES RETIREMENT

12M20 SYSTEM* 0.2% EE.UU.

18

All numbers as of Dec. 2020

*Por cuenta de terceros al 27 de noviembre, 2020A leading bank

Strong corporate governance

Related to

Santander: 4

• 7 of 11 Board members are independent

Independent

non-related to • Independent board majority in main committees: Audit

Santander: 7 Committee, ALCO and Integral Risk Committee.

Female: 3

• Integrated Annual Report: GRI and SASB compliant

Male: 8

• Local regulations also protect investors: capital and

dividend requirements, related part lending, role of the Board

Our stocks are included in:

• Compliance division: oversees application of codes of

conduct; compliant with SOX and SEC & NYSE Corporate

Chile, MILA, Emerging Governance Guidelines and ECB Basel criteria.

Markets

We are supervised by the following:

Banco Santander´s corporate governance meets the highest

international standards and ensures a sustainable management

in the long run

19A leading bank

Our team

PRESIDENT & DIRECTOR OF

COUNTRY HEAD INTERNAL AUDITING

Claudio Melandri Oscar Gomez

CEO

Miguel Mata

DIRECTOR OF RETAIL HR DIRECTOR

DIRECTOR OF RISK

BANKING M. Eugenia de

Franco Rizza la Fuente

Pedro Orellana

DIRECTOR OF DIRECTOR OF DIRECTOR OF

MIDDLE-MARKET CLIENTS &

TECH & OPERATIONS

QUALITY

Luis Araya

Ricardo Bartel Carlos Volante

DIRECTOR OF SCIB DIRECTOR OF CFO

Andrés Trautmann ADMINISTRATION Emiliano Muratore

Sergio Ávila

PRODUCTS

Cristián Peirano GENERAL COUNSEL CONTROLLER

20

Cristián Florence Guillermo SabaterA leading bank

A diversified and universal bank

% of total loans % of total net income

70% 25% 5% 0.1%

34% 34% 27% 6%

Retail Middle-market Corporate Investment Corporate activities

Banking (SCIB)

■ Loans: 70% Individuals / 30% companies

Fishing 1%

■ High diversification by sector. ALL LOANS IN CHILE. Mining 1%

Forestry 1%

Basic services 1%

Individual: focus on growing in the mid-high income segments. Transport 2%

Selective growth in lower-end segments Construction 3%

Manufacturing 4%

SMEs: focus on larger SMEs, especially with a balanced flow of Agro 4%

income (lending and non-lending products) Mortgages

36% Services 8%

Middle-market: focus on non-lending business activities. Loans

as part of an integral client relationship

Others Commerce 11%

SCIB: strong focus on non-lending activities 13%

21

Consumer 14%

Up to Dec. 2020.A leading bank

Strong results in 4Q20

Quarterly net income attributable to

shareholders Quarterly ROAE

Ch$mn

+57.2%

+74.5%

183,435 20.4%

16.8%

144,014

116,707 12.5%

105,139

84,859 9.5%

4Q19 1Q20 2Q20 3Q20 4Q20 1Q20 2Q20 3Q20 4Q20

22A leading bank

NII increases 12.5% YTD

NIM1 & Inflation Net interest income

5.0%

4.2% 4.2% 4.3% Ch$ bn 12M20 YoY QoQ

3.8% 3.7%

4.0%

Net interest income 1,594 12.5% 16.3%

3.0%

Avg. Int. earning assets 39,800 15.8% 0.1%

2.0%

1.0% 1.3% Average loans 34,436 9.7% 0.9%

0.9%

1.0%

0.3% Int. earning asset yield3 5.6% -114bp +205bp

0.0%

0.0%

Cost of funds4 1.60% -108bp +148bp

4Q19 1Q20 2Q20 3Q20 4Q20

NIM YTD 4.0% -12bp +60bp

NIM (1) UF

Improved funding mix and higher inflation drives NIMs in 4Q20

23

1. Annualized Net interest income divided by average interest earning assets. 2. MPR: Monetary Policy Rate. 3.Annualized gross interest income divided by average interest

earning assets. 4. Annualized interest expense divided by sum of average interest bearing liabilities, including non-interest bearing demand deposits.A leading bank

Outpacing the system in NII growth and NIM evolution

Net interest income & NIM

Ch$bn, %

+3.2%

8,586

+12.5% - 4.1% 8,318

1,594 1,369

1,417 1,313

NIM 4.1% 4.0% 4.3% 3.9%

3.8% 3.6%

Santander Banco de Chile Financial system without

Santander

Dec-19 Dec-20

24

Source: CMF and Santander Chile estimatesA leading bank

Non-interest bearing demand deposits up 42.0% YoY

Total Deposits

Ch$bn

+7.0% Ch$ bnS 12M20 YoY QoQ

Demand deposits 14,561 41.4% 4.7%

-2.1%

Time deposits 10,582 (19.8%) (10.2%)

25,258 26,556 25,686 25,143 Total Deposits 25,143 7.0% (2.1%)

23,490

Mutual funds1 8,092 24.0% (2.8%)

Loans/Deposits2 100.3%

LCR3 155.4%

Dec-19 Mar-20 Jun-20 Sep-20 Dec-20

25

1. Banco Santander Chile is the exclusive broker of mutual funds managed by Santander Asset Management, a subsidiary of SAM Investment Holdings Limited. 2. (Net Loans – portion of

mortgages funded with long-term bonds) / (Time deposits + demand deposits). 3. LCR calculated following the new local Chilean modelsA leading bank

Improved funding mix & outpacing competitors

CLP Time Deposit Cost Evolution1 Demand deposits by segment

3.16%

3.00% Ch$ bn 12M20 YoY QoQ

2.92%

3.00% Individuals 5,600 53.5% 10.1%

SMEs 2,696 58.9% 7.0%

Retail 8,296 55.2% 9.1%

Middle Market 3,861 29.4% 5.9%

Corporate (SCIB) 2,117 29.0% (13.7%)

0.54%

0.50% Total 14,561 41.4% 4.7%

0.46%

0.39%

Santander Chile BCI MPR

26

1. Source: CMF. Quarterly Calculation is based on time deposit in CLP average and interest paid on time deposits in pesos.A leading bank

Retail loans lead growth in 4Q20

Total Loans Ch$ bn 12M20 YoY QoQ

Individuals1 19,363 2.8% 1.8%

Ch$bn

+5.1% Consumer 4,941 (10.8%) 0.3%

-1.4%

Mortgages 12,412 10.2% 2.5%

32,732 34,355 35,288 34,880 34,409 SMEs 4,916 20.3% 0.4%

Retail 24,279 5.9% 1.5%

Middle Market 8,136 0.5% (7.5%)

Corporate (SCIB) 1,704 2.0% (10.1%)

Total2 34,409 5.1% (1.4%)

Dec-19 Mar-20 Jun-20 Sep-20 Dec-20

FOGAPE loans disbursed each month

Ch$bn

Total disbursed up to December:

Ch$2.0 trillion

1,491

488 As of December 2020, 12.2% of

117

commercial loan book were

2Q20 3Q20 4Q20 FOGAPE loans

27

1. Includes other commercial loans to individuals. 2. Includes other non-segmented loans and interbank loansA leading bank

Record level of coverage

Total loans: Non-performing loans (NPL), coverage and cost of risk (%)

Includes Ch$126 bilioon in voluntary

Feb 2010 Earthquake in

Maule Chile- 8.8Mw

provisions and Ch$35 billion for FOGAPE 227%

and destructive Tsunami July 2019: Standard

2014: Changes to provisioning model

provisioning for SMEs (B1).

models: Consumer

Economic Crisis

and Commercial 148%

2016: Standard

US and Europe

118% provisioning model

for mortgages (B1). Covid-19

87% Higher provisioning

for LTV > 90%

71% Oct. 2019: Start of

social unrest

3.1% Sept 2015:Earthquake in

2.7% 2.8% Coquimbo, Chile – 8.3Mw

2.4% 2.6% 2.4% 2.5%

2.2% 1.9%

2.4% 1.4%

Caso La Polar 1.3%

Borronazo DICOM 1.0%

NPL (1) Costo of risk (3) System cost of risk (4) Coverage (2)

28 28

1. Loans with 90 days or more overdue. 2. Stock of provisions divided by NPLs. 3. Quarterly cost of risk= quarterly provision expenses/ average of quarterly loans 4.

Quarterly cost of risk for the financial system. Source: CMFA leading bank

Strong support to clients during the pandemic

COVID Solutions1 Cuota FOGAPE2

Reprogrammed

Santander

26%

23%

Rest

77%

• $9bn of loans with grace periods

• 26% of total loans received grace • #1 in FOGAPEs

periods • Ch$2 bn disbursed

• > than 300,000 digital • >35,000 clients benefited

reporgramming for personal loans

29 29

1. Reprograms are loans with grace periods between 3 and 6 months according to CMF norms for the pandemic. 2. FOGAPE: Loans under the

guaranteed fund for SMEs. Source: CMF, as of Dec. 2020A leading bank

Positive evolution of asset quality of COVID-19 Solutions

Total Covid Solutions

Ch$11,174 bn

Fogape Covid W/ payment holiday

Ch$2,076 bn (19%) Ch$9,098 Bn (81%)

Current Current

Expired Expired

Outstanding Outstanding

Ch$1,032 bn (50%) Ch$8,363 bn (92%)

Ch$1,044 bn (50%) Ch$ 735 bn (8%)

Paid Overdue Paid Overdue

Ch$1,027bn Ch$4 bn Ch$8,241bn Ch$122 bn

(99.6%) (0.4%) (99%) (1%)

(*) Contains second (*) Contains second

payment holiday for payment holiday for

three months (3+3) three months (3+3)

30

As of Dec. 31, 2020A leading bank

Cost of risk of 1.0% in 4Q20 includes Ch$50bn in additional provisions

Quarterly cost of risk1 Provision for loan losses

%

2.2% Ch$ bn 12M20 YoY QoQ

1.9%

Gross provisions

1.5% (586.0) 16.5% (32.3%)

1.2% and write-offs

1.0% Recoveries 74.9 (9.4%) (9.9%)

Provisions (511.1) 21.6% (35.8%)

Cost of risk(YTD) 1.48%

4Q19 1Q20 2Q20 3Q20 4Q20

In total we have established Ch$126 billion in additional provisions during

2019 and 2020.

31

1. Quarterly provision expense annualized divided by average interest earning assets.A leading bank

Fees rebound in 4Q20 led by card fees

Fees & financial transaction Fees

Ch$bn

Ch$ bn 12M20 YoY QoQ

-26.2% Card fees 73.3 35.3% 9.8%

Asset management 44.1 (6.9%) 0.9%

131.1 139.5 Insurance brokerage 39.8 (19.9%) 16.6%

97.3 99.1 73.1 Guarantees, cont. op. 36.3 3.5% (0.9%)

54.4 77.2 Checking accounts 34.8 (3.1%) 4.0%

22.8 37.5 4.1 Collection fees 23.2 (30.3%) 72.7%

76.7 74.4 62.3 61.6 69.0 15.8 (92.7%) 70.0%

Others

Total 267.3 (6.9%) 12.1%

4Q19 1Q20 2Q20 3Q20 4Q20

Net fee income Financial trx Financial transactions, net

Ch$ bn 12M20 YoY QoQ

Lower Non-client treasury results Client 145.2 4.4% (21.2%)

due to FX hedge of provision

Non-Client (3.6) (105.4%) 1,825.6%

expenses and liability management

Total 141.6 (31.6%) (89.2%)

32A leading bank

Efficiency at 39.8% in 2020. Cost growth under control

Operating expenses

Ch$bn

Ch$ bn 12M20 YoY QoQ

00 60.0%

-1.0% Personnel

408.7 (0.4%) (1.3%)

50 expenses

55.0%

Administrative

189 191 194 192 190 expenses

250.5 7.2% (2.3%)

00 50.0%

Depreciation 109.4 3.1% 3.3%

50 45.0%

Operational

40.6% 41.5% 768.5 2.5% (1.0%)

38.3% 38.9% 38.3% expenses1

00 40.0%

Efficiency

39.8% -23bp -326bp

50 ratio2

35.0%

Costs/assets 1.3% -36bp +6bp

0 30.0%

4Q19 1Q20 2Q20 3Q20 4Q20

Expenses Efficiency

33

1. Operational expenses exclude impairment and other operating expenses. 2. Efficiency ratio: operating expenses excluding impairment / financial margin +

fees+ financial transactions and net other operating incomeA leading bank

Core capital at 10.7%

Core capital and BIS ratio Dividend per stock

Ch$ per stock

15.4% 75%

12.9% 60%

4.7% 75% 70% 60%

2.7% 60%

2.25

10.1% 10.7% 1.79 1.75 1.88 1.76 1.65

Dec-19 Dec-20 2016 2017 2018 2019 2020 2021

Tier 1 Tier 2

In August, CMF published the new treatment of FOGAPE guarantees. Instead of

computing as Tier II, now it is included in Tier I and RWA reduced from 100% to

10%

34 34A leading bank

Among banks with best international rating

Risk rating, Moody’s scale

UOB

OCBC

DBS

ANZ

Westpac

SAN Chile

Banco de Chile

Estado

RBC

BCI

HSBC Moody’s (negative) A1

SAN

Wells Fargo

JCR (stable) A+

BofA Standard & Poor’s (negative) A-

JP Morgan

Goldman Sachs

ItauCorpbanca

Citibank

Deutsche Bank

Credit Suisse

Bradesco

Ba3 Ba2 Ba1 Baa3 Baa2 Baa1 A3 A2 A1 Aa3 Aa2 Aa1

35

Source: Moody’s via BloombergAGENDA

MACROECONOMIC ENVIRONMENT

SOLID FINANCIAL SYSTEM WITH GROWTH POTENTIAL

SANTANDER CHILE: LEADING BANK

ADVANCES IN OUR STRATEGIC INITIATIVES

36Advances in our strategic objectives

Strategic priorities

Declaration

Our Our vision

We want to be the best bank for our customers, leading in

purpose Be the best Bank

digital excellence and experience, gaining their loyalty

Help people acting responsibly

and gaining the Clients

and

businesses to loyalty of our

prosper clients, We want to be the best large company to work in Chile,

shareholders, attracting and developing talent, always committed to our

people and SPF culture

Employees

communities

We want to be the most profitable and sustainable bank,

with solid capital levels, attractive dividends and strong risk

Our way management

of doing Shareholders

things

Simple, We want to be recognized as a responsible bank that

Personal, contributes to the community

Fair

Community

We want everything we do to have a seal of excellence in execution

Excellence

37

in executionAdvances in our strategic objectives

Clients

Maintain a high level of consumer Transform the Bank into a platform

satisfaction, increase the productivity of all allowing clients to use the bank as a

channels, and be more efficient and channel or as a software provider to

profitable. develop business.

Give access to digital

CHANGE THE BANK

Reactive loan growth in economy

RUN THE BANK

mass segment, rewarding

positive financial behavior Increase SME access to

banks and to the digital

economy

More efficient and digital

branches

First insurtech in Chile,

platform to compare and

Become more sustainable purchase insurance

through eco-friendly

initiatives (i.e. Carbon

footprint compensation) Allows international

transfers instantaneously

and securely

Higher client fidelity

through the accumulation Comparison platform for

of miles and benefits autoinsurance

38Advances in our strategic objectives

Clients

Life: strong growth and quick monetization

Life

Digital product for unbanked population

that seeks to be part of Bank, receiving

merits for positive financial behavior

(through credit and savings)

New Life clients each year Life: Evolution of total gross revenues1

349,866 2020: Ch$43bn

104,885 2019: Ch$20 bn

32,567

481

2017 2018 2019 2020

2018: Ch$7 bn

+480,000

Total Life clients

39 39

1. Net interest income plus feesAdvances in our strategic objectives

Clients

Superdigital opening record new accounts monthly

Superdigital

Prepaid digital product for the unbanked

population seeking a low-cost bank

account

16%

Market share of

New Superdigital clients each year balance in prepaid

card market as of

111,543 Dec. 2020

18,301

With one of the

147

highest average

2018 2019 2020 balances in the

market

+129,000

Total SD clients

40 40Advances in our strategic objectives

Clients

Insuretech platforms driving insurance brokerage fee rebound

An online platform that compares An online platform that compares

insurance between different providers in insurance between different providers in

a quick and transparent way. a quick and transparent way.

20K -14%

NPS NPS Cheaper insurance

Visits on a 86 95 than the industry

monthly basis Jun-20 Dec-20

High range vehicles and +52%

75% Currently sell life

insurance (Apr 2020)

hybrids/electric cars

One of the few in the

Growth of insurance

policies in 2020

Are not Santander market to offer insurance

and sports insurance

clients of these vehicles

(Oct 2020)

+9,000

Insurance companies participating: Insurance policies

sold in November

alone, a record

month

41 41Advances in our strategic objectives

Clients

Opening 3x more checking accounts than the rest of banks

combined

Current account openings through 12M201

324,821

103,915 3x1

Advantage in checking

account opening1

Rest of banks

Current account market share Santander Chile1

25.9%

21.7%

Dec-19 Dec-20

42 42

1. Source: CMF, with latest available informationAdvances in our strategic objectives

Clients

Strength of digital channels has been a key force in 2020

+24% Net Promoter Score (NPS)2

Increase digital 51

47

clients compared

previous year 39 41 48

45

42

+33% 39 38

34 36

Increase in sales through 33

Mar-20 Jun-20 Sep-20 Dec-20

digital channels compared Santander Comp 1 Comp 2

to previous year

As of December 2020, Santander received:

Market share of digital clients1

Net score 66

Accesibility to Digital Channels

32% 34%

22% 20% Total Loyal Clients3

16% 14%

7% 6% 4% 3% 764,407

704,090 764,407

704,090

Santander BCI Banco de Scotiabank Itau

Chile dic-19 dic-20

sep-19 sep-20 Dec-19 Dec-20

43

1. Source: CMF as of last available information. Last 12 months yearly average. Based on clients who access there account with a password. Excludes Banco Estado. 2. Source: Study by Activa for Santander with a scope of 60,000 surveys to our own clients and over 1,200 surveys to each

competitor’s clients. Measures the Net Global Satisfaction and Net Promoter Score in three main aspects: service quality, product quality, and brand image. % of clients that value with grade 6 and 7 subtracted by clients that value with grade 1 through 4. Audited by an external provider.

For the 6 month moving average ended December 2020 3. Customers with 4 products plus a minimum profitability level and a minimum usage indicator, all differentiated by segment. SME + Middle-market cross-selling differentiated by client size using a point system that depends on

number of products, usage of products and income net of risk.Advances in our strategic objectives

Clients

Lanzamiento oficial de Getnet

Acquiring network that uses the four-part model to

operate, offering a payments solution to businesses

Pays instantaneously

Clients will be able to receive money

from their sales in a Santander account

up to five times in one day, including

holidays.

Different plans for different clients

There will be fixed or mobile POS, all with

a SIM card incorporated. Rebates for

integrated plans with Santander, and

insurance for “Protected Billing”. +14,000 +16,700

Clients POS sold

No more “Credit or debit?”

Cardholders will no longer need to answer

what type of card as the POS will 65% 15%

automatically detect it, making the Auto-installed Expected market

shopping experience more seamless. share in the next

three years

Accepts all cards, with

following brands:

44

Figures as of April 2021Advances in our strategic objectives

Clients

Work Café: An open environment for everyone

Its digital format fits perfectly for the Workcafé Community helps entrepeneurs

continue to grow:

post COVID-19 world.

Marketplace for

local entrepeneurs

Support through e-

learning, employment

offers, among others

Tools to help create website, digitize

sales systems, among others

Network of volunteers

to advise in several

subjects

• Open to anyone

• Free wifi

• Meeting rooms for free. Reserved online Presentations from experts and other

45 45

entrepeneurs sharing their knowledgeAdvances in our strategic objectives

Strong commitment to our employees Employees

54%

Female 14.5%

11.9%

46% 11.9% 11.3%

Male

8.2%

Ch$880,488 monthly

10,470 (US$14,675 yearly)

2016 2017 2018 2019 2020

Total employees Total rotation Minimum wage in Santander (vs

Ch$326,500 monthly or US$5,442 yearly)

Top 3 in Great Place to Work

Ranking GPTW

92

86 87

Top 1

Recognized firms with the best condidition

2018 2019 2020 to develop its collaborators personally and

We were recognized as being one of the best places to work profesionally

in the country in the category of institutions of over 1,000

employees

46 46Advances in our strategic objectives

Stock return versus local stock index Shareholders

Total return 2020

From December 31, 2015; %

35.03

13.50

Santander Chile IPSA

47

Source: Santiago Stock Exchange and BloombergAdvances in our strategic objectives

COVID-19 Solutions

• Financial Support: FOGAPE loans, reprogramming plan

• Virtual channels prioritized

• Digital products: Santander Life, Superdigital

Clients • Sanitary prevention in branches

• Health and work safety

• Teleworking implementation

Employees • Adaptation of corporate buildings

• Family and work life conciliation

• Remote shareholder’s meeting

• Santander Digital Talk 2020

Shareholders

• Corporate volunteering

• Social Support during the pandemci: estoslosuperamosjuntos.cl, etc.

Society • Innovation, entrepeneurship and employment: Work Café Community

• Strengthening of remote accesses and secure

• Generation of new products: Klare, Getnet

• Development of digital solutions to replace in-person processes

Technology • Digitalization of almost 100% of processes with suppliers

and

suppliers 48Advances in our strategic objectives

Reducing our impact on the environment

Carbon footprint Electricity consumption Paper consumption

(th. of tCO2eq) (th. of MWh) (th. tons)

18 16 29 28 1.5

1.3

11

24 0.7

2018 2019 2020 2018 2019 2020 2018 2019 2020

Target 2018-2021 Target 2018-2021 Target 2018-2021

-5% -7% -15%

Water consumption E-Waste

(th. m3) (th. tons)

149 148

103 103

32 23

2018 2019 2020 2018 2019 2020

49

Coverage 52% 87% 84%Advances in our strategic objectives

Santander Verde: our new products to help clients become greener

Carbon footprint Green Green Green

compensation Mutual Fund Mortgage Loan Benefits

Up to December 2020: First fund in Chile to allow Discounts with brands

• Alliance with real

2,543 tons of CO2 were clients to invest in that are eco-friendly

estate projects with

compensated through the companies in different using you Santander card.

LEED certificate for

purchase of carbon credits geographical regions with

sustainable

First milestone of a strong focus on Incentivizes recycling and

construction.

Contribution to Fundación sustainability reusable materials

• Clients are able to buy

Llampangui for a project in • Aimed at long term

these properties at a

Parque El Durazno in investors with an

preferential rate as

Coquimbo, Chile. Now aggressive risk profile

well as contributing to

contributing to Huilo Huilo • Investment

the compensate the

Foundation completely through

carbon footprint.

digital channels

Certified Carbon Credits

Supports the development

of renewable energy,

70% 30%

At least is invested in less water

conservation, reforestation consumption

Santander GO Global

Chilean environmental Equity ESG, a diversified

projects portfolio of around 90 12%

Contributes to non-profit positions managed by less energy

organization who seek to consumption

Boston Partners (Robeco)

conserve protected

50

ecosystems in Chile.Advances in our strategic objectives

We are highly ranked in various ESG indexes

S&P IPSA ESG

Included in Chile, Among retail Included in Included in S&P

MILA, and banks: Emerging Latam IPSA ESG index,

Emerging Markets and Emerging with the third

#1 #8 Global greatest weight

in the index

Among of 270 in

banks in world

Chile

51

51Thank You.

Our purpose is to help people

and business prosper.

Our culture is based on believing

that everything we do should be:

52You can also read