AXA IM ACT US Short Duration High Yield Low Carbon - AXA IM España

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Este es un documento promocional destinado únicamente a clientes profesionales

en el marco de la directiva MIFID ( 2004/39/EC) y no puede ser utilizado por

clientes minoristas. La circulación del mismo debe restringirse en consecuencia.

AXA IM Matutity 2022 →→

AXA IM ACT

→ US Short Duration

High Yield Low Carbon

Febrero 2022

• Balance de gestión MATURITY 2022 • Fechas y puntos clave • US Short Duration High Yield • US Short Duration High Yield Low Carbon • Detalles operativos • Anexos

Balance de gestión MATURITY 2022

Objetivo de inversion alcanzado en su divisa

Objetivo de Inversión anualizado Entre el 4% y el 7%

Retorno anualizado 5,29%

(antes de gastos, en USD)

• Sin embargo los inversores de las clases que tienen cobertura de divisa a Euros, la rentabilidad ha sido

menos de la mitad que el de la clase en Dólares debido al coste de cobertura EUR/USD

• El fondo no ha sufrido ningún impago de los bonos en cartera hasta la fecha

Fuente: AXA IM a cierre Diciembre 2021

2

Performance of the fund AXA IM Maturity 2022 as of the end of 2021

A USD share class evolution vs A hedged EUR

Net of fees performance of A Cap USD share class vs A Cap EUR (Hedged) since launch

125,0

A EUR (H) Cap A USD Cap

120,0

115,0

110,0

105,0

100,0

95,0

90,0

Source: AXA IM

Historical performance period 12/09/2016 to 31/12/2021. Past performance is not indicative of future results. The above information presented is

3 supplemental to the GIPS-compliant presentation included in the GIPS Disclosure Notes. No assurance can be given that the strategy will be successful

or achieve its objectives. For illustrative purposes only.

Evolución del coste de cobertura durante la vida del fondo

Historical EUR/USD Cost of Hedging (Annualized %)

3.50%

3.00%

2.50%

2.00% • 1.4% Nivel en el lanzamiento Sept 2016

1.50% • 3.5% Nivel máximo, finales 2018

1.00% • 0.7% Nivel a 31 de Dic de 2021

0.50%

0.00%

-0.50%

Dec-13

Jun-16

Dec-18

Jun-21

Dec-11

Jun-12

Dec-12

Jun-13

Jun-14

Dec-14

Jun-15

Dec-15

Dec-16

Jun-17

Dec-17

Jun-18

Jun-19

Dec-19

Jun-20

Dec-20

Dec-21

Lanzamiento de Maturity 2022

El coste de cobertura anualizado es aproximadamente la diferencia de tipos

de interés de las dos divisas en el plazo a las que se hacen las coberturas

Fuente: Bloomberg, AXA IM.Fecha de lanzamiento 12/09/2016. Solo con fines ilustrativos.

4

Evolución de la Clase de Distribución vs Capitalización (A Cubierta EUR)

Pago de Cupones de la Clase de Distribución:

Dividendo /

Fecha de Fecha de Dividendo VL Fecha de

ISIN Valor

Cálculo Pago Neto Cálculo

Liquidativo

IE00BDBVWL78 01/04/2021 01/04/2021 1.25 EUR 1,29% 96,84

IE00BDBVWL78 01/04/2020 08/04/2020 3.68 EUR 4,22% 87,28

IE00BDBVWL78 01/04/2019 08/04/2019 1.75 EUR 1,79% 97,7

IE00BDBVWL78 03/04/2018 10/04/2018 3.96 EUR 4,04% 97,95

IE00BDBVWL78 03/04/2017 10/04/2017 1.31 EUR 1,29% 101,32 1,75%

Fuente: AXA IM. Período de cálculo de la rentabilidad: 12/09/2016 to 31/12/2021. La rentabilidad pasada no es un buen indicador de la rentabilidad

5 futura. Solo con fines ilustrativos.

Fechas e información relevante

Reembolso a bid-price Maturity 2022 ✓ El fondo no se cierra, cambia

su estrategia de inversión

✓ Los ISINES permanecen los

mismos

28 de Febrero Vencimiento de Maturity 2022

✓ Idénticas comisiones de

Cartera en espera gestión y condiciones en

todas las clases

15 de Marzo Cartera plenamente invertida

✓ El fondo es traspasable en

US Short Dur.

Reembolso a mid-price materia de IRPF*

✓ Los clientes pueden

High Yield permanecer invertidos si

quieren seguir en la nueva

Low Carbon

estrategia

*A 31/12/2021

6

US Short Duration

High Yield

la leyenda

7

Nuestra estrategia US Short Duration High Yield

• Estrategia lanzada en 2001 y una de las de mayor patrimonio de AXA Investment Managers (8.000

MM de USD bajo gestión)*

• Invierte en bonos de High Yield con vencimiento esperado inferior a 3 años (Duración de la cartera

1,1*)

• Los vencimientos de los bonos más los cupones generan una renovación permanente de la cartera

(4-6% mensual aprox.)

Fuente, fecha qué es un bono HY fuente impagos. No assurance can be given that the strategy will be successful or achieve its objectives. *A 31/12/2021.

8US Short Duration High Yield

Comparación de la estrategia frente al conjunto del mercado

AXA IM US SDHY ICE BofA ML US Composite as a %

GIPS Composite High Yield Index of Index

Annualized Gross Return 5.7% 7.9% 72%

Lower volatility with consistent performance Volatility 3.7% 9.1% 41%

Beta 0.4 1.0 39%

Attractive Sharpe ratio Sharpe-ratio 1.17 0.72 162%

Upside market capture ratio 47% 100% 47%

Attractive up-market capture

Downside market capture ratio 29% 100% 29%

With low participation in down markets

Low historical default rate Defaults since strategy's inception 2 649 * 0.3%

Due to lower risk tolerance than traditional high yield

Sources: AXA Investment Managers. ICE BofA ML US High Yield index is shown for illustrative purposes only. *J.P. Morgan Default Monitor as of January 3, 2022. 1All data is from composite

inception date of September 30, 2001 through December 31, 2021. Past performance is not indicative of future results. Performance shown gross of fees is calculated before expenses,

carried

9 interest, taxation costs and other expenses the investor may incur. An investor’s return will be reduced by management fees and other expenses. Please see the Appendix for

further information about the effect of management fees. The above information presented is supplemental to the GIPS-compliant presentation included in the GIPS Disclosure Notes. No

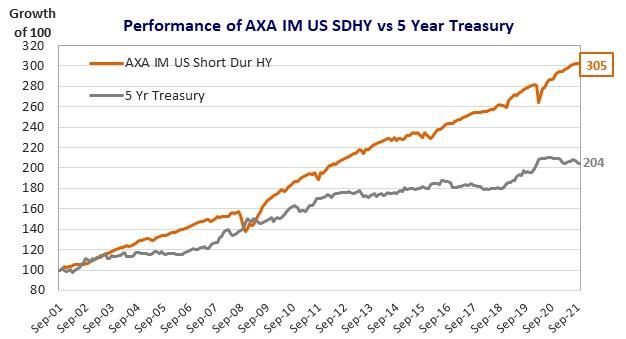

assurance can be given that the strategy will be successful or achieve its objectives.Risk-Return Profile – US Short Duration High Yield Strategy

Gross return and risk comparison since inception

US Fixed Income: Return and Risk Comparison

12% (September 30, 2001 – December 31, 2021)

10% 1 3 5 Since

Annualized Returns

AXA IM US HY Core Year Year Year Incept*

Composite AXA IM US SDHY GIPS

ICE BofA ML 3.80 5.54 4.45 5.65

8% Composite

US HY

Annualized Return

ICE BofA ML US HY Index 5.36 8.57 6.10 7.87

AXA IM US

SDHY Composite

6% ICE BofA ML

US Corporate 1 3 5 Since

Annualized Volatility

ICE BofA ML US IG Year Year Year Incept *

US Treasury

Broad (Aggregate) Index CS AXA IM US SDHY GIPS

4% 10 Year 1.23 4.57 3.64 3.73

Leveraged Composite

ICE BofA ML US Loan

Corporate 1-3 Yr US Treasury ICE BofA ML US HY Index 2.60 9.27 7.48 9.09

5 Year

2%

US Treasury

2 Year

0%

0% 2% 4% 6% 8% 10% 12%

Annualized Volatility

Performance Returns 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

AXA IM US SDHY Composite 6.3 10.4 7.7 4.0 7.4 5.0 (7.7) 22.6 9.1 4.5 7.9 5.5 1.5 1.2 6.4 4.0 1.7 8.5 4.4 3.8

ICE BofA ML US HY Index (1.9) 28.2 10.9 2.7 11.8 2.2 (26.4) 57.5 15.2 4.4 15.6 7.4 2.5 (4.6) 17.5 7.5 (2.3) 14.4 6.2 5.4

Sources: AXA Investment Managers, ICE BofA Merrill Lynch. As of December 31, 2021. *Composite Inception Date: September 30, 2001. ICE BofA Merrill Lynch US High Yield Index is shown

for illustrative purposes only. Performance shown gross of fees is calculated before expenses, carried interest, taxation costs and other expenses the investor may incur. An investor’s

return will be reduced by management fees and other expenses. Please see the Appendix for further information about the effect of management fees. Past performance is not indicative

of future results. The above information presented is supplemental to the GIPS-compliant presentation included in the GIPS Disclosure Notes. No assurance can be given that the strategy

10successful or achieve its objectives. ICE BofA ML High Yield index is shown for illustrative purposes only.

will beHistorical Default & Significant Losses

Active management of US high yield has substantially minimized default risk

AXA IM US Short Duration High Yield Strategy vs. US High Yield Broad Market

Total since

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

2002

Num ber of Defaults

1 87 61 29 21 18 11 42 70 21 21 20 21 17 29 50 23 25 27 48 8 649

US High Yield Broad Market

2 -- -- -- -- -- -- -- 1 -- 1 -- -- -- -- -- -- -- -- -- -- 2

AXA IM US SDHY Strategy

Significant Losses

Bonds sold at loss > 30% -- -- -- -- -- -- 1 8 -- -- -- -- 1 1 5 -- -- -- 2 -- 18

Bonds sold at loss 20-30% -- -- 1 -- -- -- 2 4 -- -- 1 -- 2 1 1 -- -- -- -- -- 12

120

3

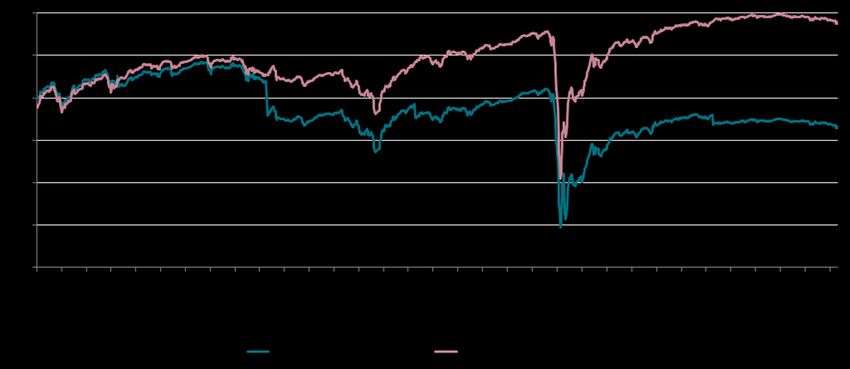

Historical Price - ICE BofA ML US High Yield Index

110

100

90

Price

80

70

60

50

Sources: 1J.P. Morgan Default Monitor as of January 3, 2022, 2AXA IM US SDHY Representative Portfolio stream (data prior to March 2004 is based on legacy portfolios managed in the same

investment strategy), 3ICE BofA Merrill Lynch, data from January 1, 2002 to December 31, 2021. ICE BofA ML US High Yield index is shown for illustrative purposes only. The representative

accounts

11 shown have been selected because they utilize an investment setup that is typical for accounts in the relevant strategy and/or on the basis that they had adequate assets under

management to effectuate a fair comparison. Please refer to the appendix for additional information. All significant loss calculations include coupon payments received during the holding

period. Past performance is not indicative of future results. For illustrative purposes only.US Short Duration High Yield

A Picture is Worth a Thousand Words

Sharpe

Since inception * Returns Volatility

Ratio

AXA IM US SDHY GIPS Composite 5.65% 3.73% 1.17

Sources: AXA Investment Managers, ICE BofA ML, Credit Suisse. As of December 31, 2021. ICE BofA ML

and Credit Suisse Indices shown for illustrative purposes only. *Composite inception date: September 30,

2001. Past performance is not indicative of future results. Performance shown gross of fees is calculated CS Levera ged Loa n Index 4.76% 6.43% 0.54

before expenses, carried interest, taxation costs and other expenses the investor may incur. An investor’s

return will be reduced by management fees and other expenses. Please see Appendix for further

information about the effect of management fees. The above information presented is supplemental to

the GIPS-compliant presentation included in the GIPS Disclosure Notes. No assurance can be given that 5 Yea r Trea s ury 3.58% 4.10% 0.55

the strategy will be successful or achieve its objectives.

12How the strategy has performed in bear markets and rising interest rates environment vs the market

Negative Quarters in US High Yield since 2001

AXA IM US Short Duration High Yield Composite Yield % Per Unit of Duration

ICE BofA Merril l Lynch US High Yiel d Index

2%

AXA IM US Short Duration High Yield

0% AXA IM US Enhanced High Yield

2010 2015

2004 Q2 Q2 2018

AXA IM US Dynamic High Yield

2007 2014

-2% Q3 2005 2013 Q1

Q1

Q4 Q2 2014

Q4

2015

AXA IM US Core High Yield

Q3 Q4

2002 2008 ICE BofA US High Yield Index

Quarterly Performance

-4% Q3 Q1

2018 ICE BofA European Currency High Yield Index

2015

-6% Q4

Q3 ICE BofA Emerging Markets Corp Plus Index

2011

-8%

2002 Q3 ICE BofA US Mortgage Backed Sec Index

Q2

ICE BofA US Corporate Index

-10% 2008 ICE BofA 5-Year US Treasury Index

Q3

ICE BofA US Municipal Securities Index

-12%

ICE BofA 10-Year US Treasury Index

2020

-14%

Q1 ICE BofA Global Broad Mkt (Aggregate) Index

ICE BofA European Corporate Index

-16% 2008

Q4

0.0 0.5 1.0 1.5 2.0 2.5 3.0

-18%

Since 2001, the fund has had 3 quarters closing with a In a rising interest rate environment, duration is

return below 2% a risk

Source: AXA Investment Managers. As of December 31, 2021. The ICE BofA ML US High Yield Index is shown for Sources: AXA Investment Managers, ICE BofA ML, Credit Suisse. As of December 31, 2021. ICE BofA ML

illustrative purposes only. Performance shown gross of fees is calculated before expenses, carried interest, and Credit Suisse Indices shown for illustrative purposes only. *Composite inception date: September

taxation costs and other expenses the investor may incur. An investor’s return will be reduced by management 30, 2001. Past performance is not indicative of future results. Performance shown gross of fees is

fees and other expenses. Please see the Appendix for further information about the effect of management fees. calculated before expenses, carried interest, taxation costs and other expenses the investor may incur.

Past performance is not indicative of future results. The above information presented is supplemental to the An investor’s return will be reduced by management fees and other expenses. Please see Appendix for

GIPS-compliant presentation included in the GIPS Disclosure Notes. No assurance can be given that the strategy further information about the effect of management fees. The above information presented is

will13

be successful or achieve its objectives. supplemental to the GIPS-compliant presentation included in the GIPS Disclosure Notes. No assurance

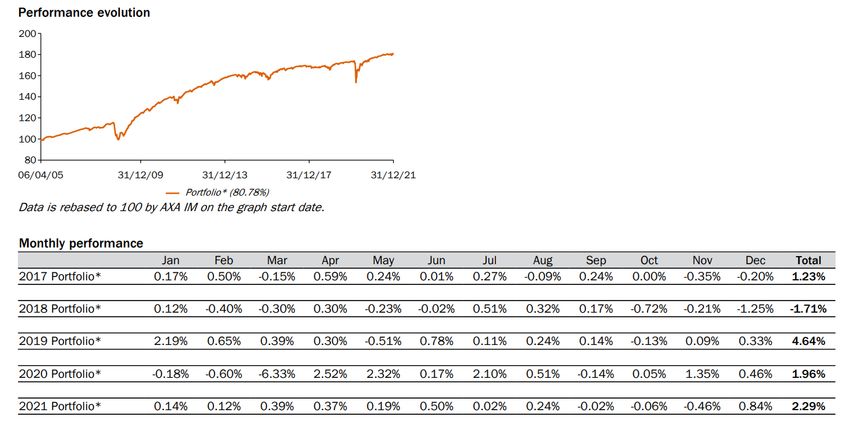

can be given that the strategy will be successful or achieve its objectives.Últimos 5 años, rentabilidad neta mensual

Clase institucional Euro Hedge

14 Fondo: AXA IM FIIS US Short Duration High Yield (Clase institucional Euro Hedge)AXA IM ACT US Short Duration High Yield Low Carbon la evolución natural

AXA IM, a global leader in responsible investing

ESG is fully integrated across our investment processes and embedded within our organisation

Expertise across

20+ years 100+ incl. 26 88% of Core eligible

of RI experience dedicated RI AUMs classified

professionals Article 8 & 9

A comprehensive &

Founding Member of

the Net Zero Asset

Innovative RI fund

Managers Initiative offering

(incl. 70 Labels funds)

PRI 2020 Leader

Group

A+

RI: Responsible Investment

16 *Source: AXA IM as of 30/09/2021. Non audited figures

Some resources are shared by the entire AXA IM Organization. There is no assurance that any particular individual will be involved in the management of the portfolio for any given

period of time, if at all. We do not guarantee the fact that staff remain employed by AXA Investment Managers and exercise or continue to exercise in AXA Investment Managers.US High Yield Low Carbon Investing

Investment process

FUNDAMENTAL CREDIT ANALYSIS + ESG ANALYSIS

Our high yield products already incorporate the following:

As a fundamental credit manager, the investments will be

largely driven by our credit risk assessment and relative ▪ ESG analysis embedded into our research process,

value analysis. including ESG engagement with portfolio companies.

Our fundamental analysis is comprised of four components: ▪ AXA IM Exclusion Policy: We apply AXA IM Responsible

Investment sectorial exclusion policies, as follows:

✓ Business due diligence

✓ Controversial Weapons Policy

✓ Financial analysis ✓ Climate Risk Policy

✓ Liquidity projection ✓ Ecosystem Protection & Deforestation Policy

✓ Soft Commodities Policy

✓ Capital structure review

+

This new strategy integrates the following additional ESG

factors into the Low Carbon investment process:

Assessing

Valuing ▪ AXA IM’s ESG standards:

Risk

Understanding Risk ✓ Severe controversies

Macro ✓ Additional restrictions on white phosphorus

Economy weapons

and Markets ✓ Tobacco

✓ ESG low quality, using proprietary ESG scores

(targets scores below 1.4, on scale of 0 to 10)

Managing ▪ Carbon intensity

Risk

▪ Water intensity

The ESG data used in the investment process are based on ESG methodologies based in part on data provided by third parties, and in some cases developed in-house. They

are subjective and may change over time. Despite several initiatives, the lack of harmonized definitions can make ESG criteria heterogeneous. For example, different

investment strategies that use ESG criteria and ESG reporting are difficult to compare with each other. Strategies that incorporate ESG criteria and those that incorporate

17 sustainable development criteria may use ESG data that appear similar, but which should be distinguished because their calculation method may be different. Please refer to

definitions on slide 11 for further details regarding ESG Scores.Nuestra nueva estrategia US Short Duration High Yield Low Carbon

Misma estrategia pero donde queremos ser explícitos como inversión de impacto: Art. 9 (SFDR)

• OBJETIVO ESG DE LA CARTERA:

- EMISIONES DE CO2 Y CONSUMO DE AGUA 30% INFERIOR EN QUE EL CONJUNTO DEL MERCADO

• ¿POR QUÉ HEMOS ELEGIDO ESTE OBJETIVO?

- ES EL CRITERIO SOSTENIBLE MÁS CLARO Y CON MÁS COBERTURA EN EL MERCADO DE HIGH YIELD

- PERMITE COMPARAR ENTRE DISTINTOS SECTORES DE ACTIVIDAD

• SE EXCLUYEN LOS SUBSECTORES MAS INTENSIVOS EN CO2 Y EN AGUA AUNQUE EL GESTOR PUEDE

INCLUIR COMPAÑÍAS QUE TENGAN PLANES CREÍBLES EN LA REDUCCIÓN DE SU IMPACTO

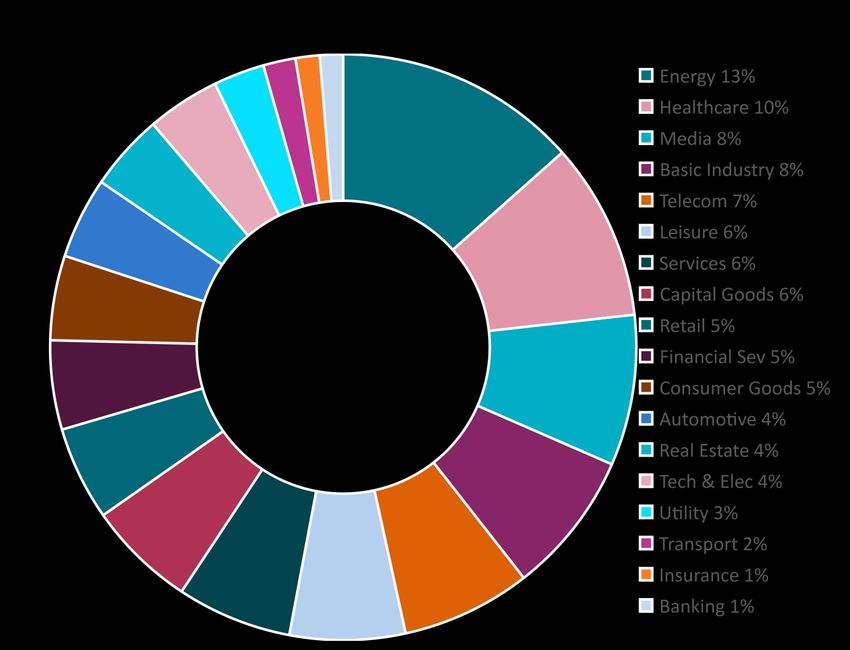

18Desglose del Mercado de HY USA por Sector de Actividad

Sub-sectores del mercado excluidos a priori del universo de inversión

Sub-Sectores Excluídos:

✓ Energy - Exploration & Production 5,7%

✓ Integrated Energy 0%

✓ Oil Refining & Marketing 0,89%

✓ Oil Field Equipment & Services 1,27%

✓ Metals/Mining 1,90%

✓ Steel Producers and Products 0,6%

✓ Electric – Dist/Trans (Utilities) 0,05%

✓ Electric – Generation (Utilities) 1,55%

✓ Electric – Integrated (Utilities) 1,12%

✓ Non-Electric Utilities 0,09%

TOTAL = 13,2%

19Desglose Sectorial del Fondo vs Mercado

20%

18%

16%

14%

12%

10%

8%

6%

4%

2%

0%

US SDHY US SDHY Low Carb. Mercado US HY *

Fuente: AXA Investment Managers. Índice: ICE BofA Merrill Lynch US High Yield Index. A 31/12/2021Portfolio Positioning

US Short Duration HY Low Carbon targeted model portfolio

Source: AXA IM, Inc., FactSet as of January 31, 2022 AXA IM US SDHY Low Carbon HY representative portfolios exclusive of cash. Benchmark is the ICE BofA ML US High Yield Index (ML

21 H0A0). The representative accounts shown have been selected because they utilize an investment setup that is typical for accounts in the relevant strategy and/or on the basis that it

has adequate assets under management to effectuate a fair comparison.ESG Facts Please refer to the appendix for additional information and for definitions of Carbon Intensity and Water Intensity Scores. Diversification does not ensure profit or protection against loss. 22

Detalles operativos

Principales participaciones disponibles

Comisión de gestión TER Min. de entrada ISIN

Banca Privada

Clase A (H) EUR cap 1,1 % 1,34 % - IE00BDBVWK61

Clase A (H) EUR dist 1,1 % 1,34 % - IE00BDBVWL78

Clase A EUR cap 1,1 % 1,31 % - IE00BDBVWJ56

Clase Limpia

Clase F (H) EUR cap 0,55 % 0,78 % - IE00BDBVWW83

Institucional

Clase I (H) EUR cap 0,50 % 0,74 % Eur 500.000 IE00BDBY8P28

Para más información acerca de las clases pueden consultar el folleto del fondo .

23Anexos

Responsible Investment exclusions

AXA IM Sectorial Policies

Climate Risks

▪ Companies that derive 30% or more of their revenue from thermal coal

▪ Mining companies that extract more than 20 million tons of coal per year

▪ Power generation companies that have 30% or more of electricity generation capacities powered by coal

▪ Power generation companies that plan to expand coal power generation capacity by more than 300 MW.

▪ Mining companies developing new coal mining and coal industry partners developing significant new coal assets

▪ Power Generation companies with more than 10 GW of installed coal-based capacities

▪ Mining companies that derive 20% or more of their revenue from tar sands extraction

▪ Pipelines companies that derive 20% or more of their revenue from tar sands transportation.

Ecosystem Protection & Deforestation

▪ Palm oil producers which have not achieved “sustainable palm oil” production certifications, and/or have significant

unresolved land rights conflicts and/or conducting illegal logging

▪ Companies in any sector facing “high” and “severe” controversies related to “Land use and biodiversity”.

▪ Companies producing Palm Oil, Soy, Cattle and Timber that are facing “significant” “Land use and biodiversity”

controversies and that are found to have a “critical” impact on deforestation and natural ecosystems conversion.

Controversial Weapons

▪ Companies that Produce, use, store, trade, or ensure the maintenance, transport and financing of Controversial Weapons

or components specifically designed for those types of Controversial Weapons (customized components)

▪ Companies that support or provide assistance, research and technology dedicated only to those Controversial Weapons

▪ Companies that Breach the Non-proliferation Treaty for the nuclear weapons

▪ Companies that own 50% or more of an Excluded Company

Soft Commodities

AXA IM strives to not participate:

▪ in short-term instruments (such as commodity futures, ETF, based on food (“soft”) commodities, or

▪ enter into speculative transactions that may contribute to price inflation in basic agricultural or marine commodities

(such as wheat, rice, meat, soy, sugar, dairy, fish, and corn)

25

Source: AXA IM. For illustrative purposes only. AXA IM reserves the right to modify any of the procedures, process and controls described herein at its discretion.

Please see the following for further information on AXA IM exclusion policies: https://www.axa-im.com/our-policies#exclusion-policiesUS High Yield Low Carbon Investing

Carbon Intensity and Water Intensity

Lower Carbon & Water Intensity Requirements Why carbon and water intensity?

▪ Carbon intensity and water intensity scores aim at being at ▪ Better coverage of the high yield universe than many

least 30% lower than the benchmark.* other ESG KPIs.

▪ Comparable from one sector to another. These metrics

▪ High KPI scoring coverage: are objective and quantifiable and can be used to compare

✓ at least 90% of net assets will have carbon intensity scores many types of business models.

✓ at least 70% of net assets will have water intensity scores. ▪ Companies can control their direct / scope 1 emissions.

This is a meaningful metric to judge a company’s efforts

▪ Bonds without carbon intensity data can be included in the

toward decreasing their environmental impact.

portfolio, provided they make up less than 10% of the bond

holdings and they are not in the excluded sectors. ▪ The portfolio may include companies that offer :

✓ Credible plans for reducing carbon and water intensity

Definitions in the future.

• Carbon Intensity1: Amount of carbon dioxide equivalent released ✓ Products that help other businesses improve their

into the atmosphere as a result of the activities of a particular environmental footprints.

organization and first tier indirect (GHG emissions from

operations that are owned or controlled by the company & from ▪ ESG engagements can be used by the analysts to

its direct suppliers). It is expressed in CO2 tonnes per millions $ encourage companies to improve their environmental

revenue: Carbon Intensity-Scope 1 (tonnes CO2e/USD mn) + footprint

Carbon Intensity-First Tier Indirect (tonnes CO2e/USD mn).

• Water Intensity: Sum of Water Intensity-Direct Cooling (cubic

meter/USD mn) + Water Intensity-Direct Process (cubic

meter/USD mn) + Water Intensity-Purchased (cubic meter/USD

mn)

*30% is applicable as from 18 February 2022. Until 18 February 2022, 20% should be applicable instead. 1Data source: Trucost S&P. For “Carbon Intensity”, at some point in

26 2021, AXA IM may move to using (scope 1 + scope 2 emissions / revenue ($). There is a growing EU-level regulatory effort to move towards the use of carbon intensity

measures with enterprise value (EV) as a denominator rather than revenue. However, as discussed, for an asset class with such a significant proportion of private issuers, we

do not think this measure makes sense. Comparisons between private and public issuers would not be consistent.Detalle de los sectores incluídos y excluídos 27

GIPS Compliance Disclosure

US Short Duration High Yield Composite

GIPS Compliant Performance Presentation

Investm ent Strategy Objective General Inform ation

Aims to generate high current income by investing in better-quality, non- Reporting date December 31, 2021

investment grade debt of U.S. companies w ith an expected redemption

Composite Inception Date September 30, 2001

of three years or less.

Composite Creation Date September 30, 2001

Composite Currency USD

Com posite Benchm ark

The "US Short Duration High Yield" composite is not show n against a Cum ulative (%) 1 mo 3 mo 6 mo YTD

benchmark, since the strategy is an absolute return strategy and not

Composite (Gross) 1.07 0.72 1.34 3.80

managed against a benchmark.

Composite (Net) 1.03 0.60 1.11 3.34

Since 2021 2021 2021 2021

Annualized (%) 1 year 3 year 5 year inception Quarterly (%) 1Q 2Q 3Q 4Q

Composite (Gross) 3.80 5.54 4.45 5.65 Composite (Gross) 1.03 1.39 0.62 0.72

Composite (Net) 3.34 5.09 3.98 5.16 Composite (Net) 0.91 1.28 0.51 0.60

Calendar year (%) 2021 2020 2019 2018 2017 2016 2015 2014 2013 2012

Composite (Gross) 3.80 4.38 8.50 1.69 3.98 6.38 1.23 1.51 5.46 7.87

Composite (Net) 3.34 3.93 8.06 1.22 3.48 5.88 0.77 1.03 4.96 7.35

Internal Dispersion (Std. Deviation) N/A N/A N/A N/A N/A N/A N/A N/A 0.10 0.04

As of end of period 2021 2020 2019 2018 2017 2016 2015 2014 2013 2012

Composite Assets (USD mil) 6,507 5,772 5,712 5,575 8,217 10,039 11,014 12,390 20,483 17,520

# of Portfolios in Composite 5 5 7 4 4 5 4 3 12 12

Total Strategy Assets (USD mil) 8,161 7,131 7,109 8,351 13,335 18,867 18,648 19,681 24,991 21,182

Total Firm Discr.Assets (USD mil) 250,851 208,569 191,910 223,150 177,183 182,303 215,895 225,582 196,489

Total Firm Assets (USD mil) 689,782 618,264 583,866 650,149 555,036 558,650 668,139 686,214 658,109

29

Source: AXA IM, Inc. Past results are not indicative of future performance. No assurances can be made that profits will be achieved or that substantial losses will not be incurred. Returns

assume the reinvestment of distributions. More information on the fees and expenses charged to clients of the investment adviser is available in Part II of the adviser’s Form ADV.GIPS® Performance Disclosure Notes Claim of Compliance AXA IM claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. AXA IM has been independently verified for the periods from December 31, 1999 through December 31, 2018. Verification assesses whether (1) the firm has complied with all the composite construction requirements of the GIPS standards on a firm-wide basis and (2) the firm’s policies and procedures are designed to calculate and present performance in compliance with GIPS standards. The US Core High Yield and the US Short Duration High Yield Composites have been examined since inception. GIPS verification and performance examination reports are available upon request. Select AXA IM funds under management that are included in select GIPS composites are subject from time to time to “swing” pricing. In order to ensure that AXA IM maintains its GIPS compliance standards, it has developed a comprehensive set of policies and procedures to account for such swing price impacts. As with other policies and procedures, the GIPS standards are reviewed and revised on an as needed basis. Presentation of the Firm AXA Investment Managers is a firm comprising two “sub-firms” for GIPS® purposes, each of which is defined as shown below: - AXA IM: AXA IM groups together all the fee-paying portfolios managed in a discretionary manner according to the global investment processes (active judgmental management and index management) instituted during the last quarter of 1999 following a global reorganization of AXA IM. The management centers included in this perimeter as of 31/12/2016 are AXA Investment Managers Paris, UK, Luxembourg, Deutschland, Italy, Switzerland, Hong Kong, Tokyo, Australia, AXA IM Inc. and all Fund of Hedge Funds. Following the October 2003 acquisition of the Advantus US Investment Grade team by AXA IM, AXA IM North America and the acquired team were combined within one legal entity, AXA IM Inc. AXA IM Inc. is a registered investment adviser with the Securities and Exchange Commission and has been included in the definition of AXA IM since October 1, 2003. AXA Framlington (London portfolios excluding Private Clients) is an equity manager with offices in the U.K. and has been verified for each of the years from 2001 to 2009 by PricewaterhouseCoopers London. It has been included in the definition of AXA IM since January 1, 2010. Discretionary management includes all investment management agreements for which AXA IM assumes full and entire responsibility for the performance or performance spreads. This composite presentation is made by AXA IM. - AXA Rosenberg Investment Management: AXA Rosenberg is an equity manager with offices in the U.S., U.K., Japan, Singapore and Hong Kong. Composite List and Description A complete list and description of all composites is available on request. Portfolio Valuation Portfolios are valued according to the market closing prices each day, except for certain portfolios valued in Germany, which use the closing price of the previous day, and the UK, where the price used is the 2pm price of the same day. In order to apply this valuation policy, the NAV of the day following the valuation date is used for certain portfolios. Dividends paid on securities in the portfolio are accounted for using ex-dividend date and are gross of any withholding taxes. Buy and sell transactions are taken into account using trade-date valuation after confirmation of the trade by the counterparty, except in Germany where settlement date valuation is used. Accrued interest on debt securities is recorded each time the portfolio is valued. All proceeds, including realized and unrealized gains or losses in the portfolio are included in the value of assets. There are minor exceptions to these general rules for specific types of portfolios. Some securities in portfolios of US High Yield composites are valued by reference to broker quotes. Minimum Asset Level & Total Firm Assets The minimum portfolio size for the US High Yield and US Investment Grade composites is 10,000,000 USD. If the portfolio falls below 10,000,000 USD for more than three months it is excluded from the performance calculations for the following month. For all other composites, the upper threshold is defined at 10,000,000 EUR the lower threshold at 8,000,000 EUR, with a 6-month grace period. AUM figures for the Firm include all portfolios falling within the definition of the Firm. 30

GIPS® Performance Disclosure Notes (Continued) Significant Cash Flows If the average cash balance of a portfolio is above 10% for a specific month, the entire portfolio is temporarily removed from the composite performance for that particular month. Additional information regarding the treatment of significant cash flows is available upon request. Currency Used to Express Performance Composite performance figures are presented in the currency of the composite. Performance Results / Fees Composite returns are calculated gross of fees. Gross of fees returns are calculated gross of management and custodial fees and net of all trading expenses. The management fee schedule is as follows: US Core High Yield Composite: First $50 million: 0.48%; next $50 million: 0.44%, next $50 million: 0.41%, next $50 million: 0.39%, Amount above $200 million: 0.37%. US Short Duration High Yield Composite: Flat fee: 0.45%. US Dynamic High Yield Composite: Flat fee: 0.60%. US Investment Grade Corporate Bond Composites: First $50 Million: 0.26%; next $50 million: 0.24%; next $50 million: 0.20%; next $50 million: 0.18%. Amount above $200 million: 0.17%. Benchmarks The composite may be managed against a specific benchmark as indicated on the composite page. The extent to which any given composite invests in countries or regions not included in the benchmark depends on the limits (if any) specified in the investment management contracts of the individual portfolios in the composite. In general, such investment is marginal and is typically less than 10% for any given portfolio. Compliance with Local Laws This performance presentation does not conflict with any relevant local laws in any of the AXA IM management centers included in the Firm perimeter as at 31/12/2016. Calculation Methods Composite performance is calculated on a monthly basis as follows: • The portfolios entering the performance calculation are determined according to the Minimum Asset Level described above. • Each portfolio brings its own specific start and end dates to the calculation, depending on the particular valuation dates of the portfolio. • The performance of each portfolio is calculated using the start and end dates relevant to the period in question, and using daily-weighted cash flows. • The performance of a composite is calculated as a weighted average (using each portfolio’s assets under management as at each portfolio’s specific start date for the period in question) of the performances of the portfolios. • Quarterly, annual, cumulative and since-inception returns are calculated by linking the composite monthly returns through compounded multiplication. The benchmark performance is calculated in a similar fashion, using the same portfolio-related weights and date values, and replacing the portfolio values by the composite benchmark values. The calculation of the composite benchmark return is always comparable in terms of time periods and asset-weightings to the calculation of the composite return. Dispersion Dispersion is the weighted average (using the AUM of each portfolio at the start of the period) of the tracking error between the composite and those portfolios satisfying the Minimum Asset Level test (see above) for the whole period. Composites dispersion is defined as the standard deviation of the returns of the portfolios for the period in question, taking into account the relative size of the portfolios. It is only displayed if there are at least 5 such portfolios. 31

Representative Portfolios and Indices used Gross Performance: Performance shown gross of fees is calculated before the deduction of applicable management fees and other expenses. An investor’s actual return will be reduced by management fees and other expenses the investor may incur. Further information on the firm’s fees may be found in its Form ADV Part 2 (for US investors) or provided upon request. The collection of management fees produces a compounding effect on the total rate of return net of management fees. [As an example, the effect of management fees on the total value of an investor’s portfolio assuming a) quarterly fee assessment, b) $1,000,000 investment, c) portfolio return of 8% a year, and d) 1.00% annual investment management fee would be $10,416 in the first year, and cumulatively $59,816 over five years and $143,430 over ten years.] Net Performance: Performance shown net of fees is calculated after the deduction of management fees and other applicable expenses. The risk information provided herein is not sufficient to support an investment decision, and is qualified in its entirety by the more complete disclosures, risk factors and other terms available upon request from AXA Investment Managers. Representative Accounts: Such accounts have been selected based on objective, non-performance based criteria, including, but not limited to the size and the overall duration of the management of the account, the type of investment strategies and the asset selection procedures in place. Therefore, the results portrayed relate only to such accounts and are not indicative of the future performance of such accounts or other accounts, products and/or services described herein. In addition, these results may be similar to the applicable GIPS composite results, but they are not identical and are not being presented as such. Account performance will vary based upon the inception date of the account, restrictions on the account, along with other factors, and may not equal the performance of the representative accounts presented herein. The performance results for representative accounts are gross of all fees and do reflect the reinvestment of dividends or other earnings. The examples of securities provided for each representative account presentation are for illustrative purposes only and are intended to reflect the typical securities, sectors, and/or geographies that could be deployed by the strategy to generate the target returns. These examples do not represent all of the securities purchased, sold or recommended for the client’s accounts, and should not be considered a buy/sell recommendation. An investor’s actual experience may vary. The ICE BofA ML US High Yield Index is composed of high-yield corporate bonds and other distressed securities. Taxable and tax-exempt US municipal, DRD eligible and defaulted securities are excluded from the Index. Indices are rebalanced monthly by market capitalization. The BofA Merrill Lynch High Yield Index is an unmanaged index consisting of U.S. dollar denominated bonds that are rated BB1/BB+ or lower, but not currently in default. No assurance can be given that the strategy/fund will be successful or that investors will not lose some or all of their capital. The ICE BofA ML US Corporate Master Index is composed investment grade corporate bonds. Taxable and tax-exempt US municipal, DRD eligible and defaulted securities are excluded from the Index. Indices are rebalanced monthly by market capitalization. The ICE BofA ML 1-3 Year US corporate Index is composed of investment grade corporate bonds including securities with a remaining term to final maturity of less than 3 years. Taxable and tax-exempt US municipal, DRD eligible and defaulted securities are excluded from the Index. Indices are rebalanced monthly by market capitalization. The Bloomberg Barclays Capital US Corporate Credit – Intermediate Index is composed dollar-denominated investment grade debt from U.S. and non-U.S. industrial, utility, and financial institutions issuers of intermediate maturities (1-10 years). Subordinated issues, securities with normal call and put provisions and sinking funds, medium-term notes (if they are publicly underwritten), 144A securities with registration rights, and global issues that are SEC-registered are included. Structured notes with embedded swaps or other special features, as well as private placements, floating-rate securities, and Eurobonds are excluded from the U.S. Corporate Index. The Bloomberg Barclays Capital US Corporate Credit Index is composed of dollar-denominated investment grade debt from U.S. and non-U.S. industrial, utility, and financial institutions issuers. Subordinated issues, securities with normal call and put provisions and sinking funds, medium-term notes (if they are publicly underwritten), 144A securities with registration rights, and global issues that are SEC-registered are included. Structured notes with embedded swaps or other special features, as well as private placements, floating-rate securities, and Eurobonds are excluded from the U.S. Corporate Index. An index is unmanaged and is not available for direct investment. 32

Disclaimer

Not for Retail distribution: this document is intended exclusively for Professional, Institutional, Qualified or Wholesale Investors / Clients, as defined by applicable

local laws and regulation. Circulation must be restricted accordingly.

This document is being provided for informational purposes only. The information contained herein is confidential and is intended solely for the person to which it has

been delivered. It may not be reproduced or transmitted, in whole or in part, by any means, to third parties without the prior consent of the AXA Investment Managers,

Inc. (the “Adviser”). This communication does not constitute on the part of AXA Investment Managers a solicitation or investment, legal or tax advice. Due to its

simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts

made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time

of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the

accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material

does not contain sufficient information to support an investment decision.

Past performance is not a guide to current or future performance, and any performance or return data displayed does not take into account commissions and costs

incurred when issuing or redeeming units. References to league tables and awards are not an indicator of future performance or places in league tables or awards and

should not be construed as an endorsement of any AXA IM company or their products or services. Please refer to the websites of the sponsors/issuers for information

regarding the criteria on which the awards/ratings are based. The value of investments, and the income from them, can fall as well as rise and investors may not get back

the amount originally invested. Exchange-rate fluctuations may also affect the value of their investment. Due to this and the initial charge that is usually made, an

investment is not usually suitable as a short term holding.

Information concerning portfolio holdings and sector allocation is subject to change and, unless otherwise noted herein, is representative of the portfolio for the

investment strategy described herein at a fixed point in time. The performance information shown herein reflects the performance of a composite of accounts that does

not necessarily reflect the performance that any particular account investing in the same or similar securities may have had during the period. Actual portfolios may differ

as a result of client-imposed investment restrictions, the timing of client investments and market, economic and individual company considerations. The holdings shown

herein should not be considered a recommendation or solicitation to buy or sell any particular security, do not represent all of the securities purchased, sold or

recommended for any particular advisory client, and in the aggregate may represent only a small percentage of an account’s portfolio holdings.

Investing involves risk and past performance does not guarantee future results. Fixed income securities are subject to interest rate risk, credit risk, prepayment risk

and market risk. High yield and investment grade securities are subject to a greater risk of capital loss, credit risk, and default risk and liquidity risk. Investors in

offshore vehicles advised or sub-advised, in whole or in part, by the Adviser employing the investment strategy described herein may be subject to currency exchange

risk. There is no guarantee that the objectives of the investment strategy described herein will be achieved.

The Adviser is not a tax or legal advisor. Prospective investors should consult their tax and/or legal advisors before making tax-related and/or legal-related investment

decisions.

AXA INVESTMENT MANAGERS PARIS, a company incorporated under the laws of France, having its registered office located at Tour Majunga – La Défense 9 – 6, place de

la Pyramide – 92800 Puteaux, registered with the Nanterre Trade and Companies Register under number 353 534 506, a Portfolio Management Company, holder of AMF

approval no. GP 92-08, issued on 7 April 1992.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Sf Ref-23389

33This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities. It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date. All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited. Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent. Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries. © AXA Investment Managers 2021. All rights reserved 34

Disclaimer Este documento ha sido preparado con carácter meramente informativo y no constituye una oferta en un folleto en particular o una invitación para cerrar un trato, comprar o vender ningún instrumento financiero o participar en ninguna estrategia de negociación, incluyendo la prestación de servicios de inversión o análisis financiero. Este documento ha sido preparado por AXA INVESTMENT MANAGERS PARIS S.A Sucursal en España. A pesar de los esfuerzos dedicados a la revisión del contenido de este documento, no se garantiza de manera implícita o explícita que la información aquí contenida sea exacta y completa. Dicha información podrá ser modificada y/o actualizada sin previo aviso. Ni AXA INVESTMENT MANAGERS PARIS S.A., sus sucursales, filiales y asimiladas, ni ninguna otra compañía o unidad perteneciente al Grupo AXA, y ninguno de sus directores o empleados podrán ser considerados responsables directos o indirectos de la información aquí contenida. Usted asume el riesgo de la utilización de la información incluida en este documento. La información incluida en este documento se pone a disposición exclusiva del destinatario para su uso interno, quedando terminantemente prohibida cualquier distribución o reproducción, parcial o completa por cualquier medio de este material sin el consentimiento previo por escrito de AXA INVESTMENT MANAGERS PARIS S.A. La información aquí contenida está dirigida únicamente a clientes profesionales tal como se establece en las definiciones de los artículos 205 y 207 del texto refundido de la Ley del Mercado de Valores que se aprueba por el Real Decreto Legislativo 4/2015, de 23 de octubre. La información aquí contenida tiene carácter publicitario y se refiere a los sub-fondos de AXA World Funds (la Sociedad), una institución de inversión colectiva inscrita en la Comisión Nacional del Mercado de Valores (CNMV) con el número 239 (www.cnmv.es), donde puede consultarse la lista actualizada de entidades comercializadoras en España de la Sociedad (los distribuidores españoles). La información aquí contenida tiene carácter publicitario y se refiere a los de AXA IM Fixed Income Investment Strategies (la Sociedad), una institución de inversión colectiva inscrita en la Comisión Nacional del Mercado de Valores (CNMV) con el número 867 (www.cnmv.es), donde puede consultarse la lista actualizada de entidades comercializadoras en España de la Sociedad (los distribuidores españoles). La información aquí contenida tiene carácter publicitario y se refiere a los sub-fondos de AXA Rosenberg Equity Alpha Trust (la Sociedad), una institución de inversión colectiva inscrita en la Comisión Nacional del Mercado de Valores (CNMV) con el número 867 (www.cnmv.es), donde puede consultarse la lista actualizada de entidades comercializadoras en España de la Sociedad (los distribuidores españoles). Este documento contiene breve información sobre el Sub-fondo y no detalla todos los posibles riesgos u otros aspectos importantes relativos a su potencial inversión. Las decisiones de inversión se realizarán sobre la base de la lectura y entendimiento de la información contenida en el último folleto de la Compañía, datos fundamentales para el inversor (DFI) y los últimos informes económicos anuales y semestrales. Los Distribuidores españoles facilitarán a cada inversor, con carácter previo a la suscripción de las acciones del Sub-fondo, una copia traducida al español del DFI y el último informe económico. Asimismo, una copia de la memoria de comercialización, siguiendo el modelo establecido por la CNMV, estará disponible a través de los Distribuidores españoles. La documentación obligatoria oficial estaré disponible a través de los Distribuidores españoles, en versión impresa o digital, y también disponible consultando www.axa-im.es donde se podrá obtener información sobre los valores liquidativos de las clases de acciones disponibles en España. Se recomienda obtener más información y recibir asesoramiento profesional antes de llevar a cabo una decisión de inversión. Tenga en cuenta que el valor de una inversión puede fluctuar al alza o a la baja y que rendimientos pasados no garantizan rendimientos futuros. AXA Investment Managers Paris, S.A., Sucursal en España, con Código de Identificación Fiscal W0024065E, inscrita en el Registro Mercantil de Madrid, Tomo 41006, Libro 0, Folio 1, Sección 8, Hoja M-727252, con domicilio Paseo de la Castellana 93, 6ª planta e inscrita en la Comisión Nacional del Mercado de Valores con número de registro oficial 38 como una Sociedad gestora del espacio económico europeo con sucursal en España. 35

You can also read