Annual Pensions Webinar 2021 - 18th January - 21st January - V

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Annual Pensions Webinar 2021 18th January – 21st January

Thank you for joining Contents

our Annual Pensions

Webinar 2021!

I would like to thank you for attending DC trends: consolidation, compliance and ESG 3

Baker McKenzie's Annual

Pensions Webinar 2021. The year in review - cases and determinations that

5

For those who attended, and those we have shaped the pensions landscape

missed, this brochure provides a

summary of the key takeaways The year ahead - what will 2021 hold for trustees

7

from our four sessions. and employers?

Though the pace of change looks Looking towards long term objectives: DB

set to continue for all of us as 11

consolidation and buy-out

we move into 2021, we hope that

our sessions provoked thought

and provided some clarity and

practical guidance on how to

manage some of the critical pensions

issues currently faced by employers,

trustees and pension providers. If

you have any questions, please

feel free to reach out to your usual

Baker McKenzie contact.

With very best wishes,

Jeanette

Jeanette Holland

Partner

+44 20 7919 1171

jeanette.holland

@bakermckenzie.com

DC trends: consolidation, compliance and ESG

Our first session focused on developments in defined contribution pension provision, including transfers to DC

master trusts, ESG and DC compliance issues. Here is a summary of what was discussed.

Transfers to DC Master Trusts

Employers and trustees alike are driving switches strategy. There are a number of legal aspects to

to master trusts. Potentially lower costs, and the ESG.

merit for members of regulated DC master trust

governance structures and potentially wider member Trustees' fiduciary duty to exercise their power in the

options and fund ranges - particularly when best interests of the scheme members has usually

compared with smaller DC arrangements - are often been interpreted as meaning in the members' best

key factors. financial interests, maximising the best risk-adjusted

returns for the scheme. However, there is now

The first key step is to identify the core project support for the position that profit maximisation alone

structure. A future-service only arrangement for is not enough to satisfy the fiduciary duties of a

employers is fundamentally different - in terms of trustee and that the "best interests" principle is an

legal documents (Deed of Participation and employer integral part of a broader principle that a trust power

services agreement) and due diligence (is a scheme should be exercised to promote the purpose of a

closure consultation needed first?) - from a legacy trust.

past rights transfer (with a Transfer Deed and

scheme merger due diligence of powers and fiduciary Since 1 October 2019 trustees' statements of

issues). investment principles have had to include a

statement of their policy in relation to "financially

Trustees must weigh up the relevant factors to material considerations" over the appropriate time

protect members. Once powers and process are horizon. These include but are not limited to ESG

resolved - typically a formality - trustees will want to considerations including but not limited to climate

ensure members' interests are protected. Advice change which the trustees consider financially

comparing the two arrangements is usually core to material. Trustees also have to include in the SIP a

this. Trustees may also need to assess (and policy statement on extent to which non-financial

potentially mitigate for) (i) any valuable tax matters are taken into account.

protections that members could lose, whether

scheme-specific (e.g. lump sums or early pension Under the new Governance Regulations (which will

rights) or member-specific (e.g. registered LTA- apply once the new "single code of governance" is in

enhancements); (ii) any benefits that are not place), trustees will have to carry out and document

replicated in the master trust e.g. ancillary rights an "own-risk assessment" at least every three years.

previously enjoyed on redundancy, or rights linked to One of the types of risks that will have to be

DB benefits in a hybrid scheme (e.g. flexibility to assessed are risks related to climate change, use of

maximise tax free lump sums from DC instead of resources and the environment, social risks and risks

commuting DB - with options to transfer back to the related to the depreciation of assets due to regulatory

original scheme becoming common). assessment.

ESG Aspects Climate change reporting provisions have been

included in the Pension Schemes Bill. The proposal

ESG, (environmental, social and corporate will affect only large schemes at the outset (assets of

governance) considerations have ever-growing more than £5 billion), as well as all authorised master

importance in the Pensions world. Policy makers trusts and authorised collective money purchase

believe the buying power of pension fund investment schemes. From October this year such schemes will

can be put to good use if trustees properly take have to have in place governance and metrics for

account of ESG factors. It's not just about saving the assessing and managing climate risks and

planet. There is a broad range of issues that fall opportunities from 1 October 2021 and then publish

under each aspect of ESG, and different kinds of disclosures in line with TCFD recommendations and

risks arise in each area. The challenge is to take report the greenhouse gas emissions of their

account of these risks in determining investment portfolio.

3DC Compliance Issues future. Trustees should also be aware that when

members are "mapped" from one fund to another

Planning ahead for the implementation statement. when the Trustees change their managers, this can

Trustees of DC schemes need to prepare an lead to funds which were not previously subject to the

implementation statement and publish it on a public cap becoming "default" funds, so Trustees should

website before 1 October 2021. It must set out the seek advice on any changes.

extent to which the SIP has been followed during the

scheme year, detail any review of the SIP, detail any Other upcoming issues to be aware of:

changes to the SIP and the reasons for them, and set

out details of the Trustee's voting behaviour and any Annual Benefit Statements. The DWP has

use of proxy voting services during the year. Trustees indicated it will simplify and shorten annual

will need to consider what should be included in the benefit statements, and put in place an annual

statement, and what questions they will need to ask "statement season" during which members can

their managers and advisers. expect statements from all their pension

schemes.

CMA Order compliance. At present, the Competition

Stronger "nudge" towards guidance. A DWP

and Markets Authority oversees the requirements

policy statement confirms that Trustees will in

relating to investment consultants and fiduciary

future need to provide members with a "stronger

managers. Later this year, regulations are expected

nudge" towards Pension Wise guidance before

to be finalised which will mean the Pensions

they can access Defined Contribution (DC)

Regulator will take on this role, and Trustees will then

benefits, and Trustees may need to record opt-

need to report their compliance with the requirements

outs and seek compliance statements from

to the Regulator via their annual scheme return.

members.

DC Charge Cap. The cap applies to default funds Transfer-out requirements. Changes to the

which are used for auto-enrolment, and limit member- transfer requirements are expected as part of the

borne charges to 0.75%. A recent review of the cap Pension Schemes Act 2021 once it becomes law.

by the Government has not resulted in changes to Details will follow in regulations, and Trustees

the level of the cap, but the application of "flat fees" to might need to amend their transfer processes

very small deferred pots of benefits will be limited in accordingly.

KEY CONTACTS

Arron Slocombe Chantal Thompson Caspar McConville

Partner Partner Senior Associate

+44 20 7919 1240 +44 20 7919 1959 +44 20 7919 1030

arron.slocombe chantal.thompson caspar.mcconville

@bakermckenzie.com @bakermckenzie.com @bakermckenzie.com

4The year in review - cases and determinations that

have shaped the pensions landscape

2020 was another busy year in the Courts and at the Pensions Ombudsman

Pensions Ombudsman's office. Here is a summary of

the cases that we shared with you at our seminar. The Pensions Ombudsman saw more that 20,000

new enquiries come through the door and resolved

In Court nearly 3,500 issues. Another busy year is forecast,

with complaint areas continuing to include delays,

Schrems II - Cross border data transfers. The transfer scams and ill-health cases, and also

judgment both invalidated the EU-US Privacy Shield redundancy and furlough scheme related matters - a

arrangement and raised questions over the level of sad sign of the times. Reviewing on-the-ground

data protection offered for those relying on Standard governance in these areas is key for all pensions

Contract Clauses (SCCs) when transferring data from professionals.

the European Economic Area (EEA) to a third

country. Trustees and employers of UK pension Two key determinations from last year included:

schemes should consider whether the mechanisms in

place to protect any transfers of scheme personal Mr T: CAS-38354-V5L8. Transfer delays and

data to outside of the EEA (for example to other investment loss Due to the plan administrator's

entities in the employer's corporate group) remain unreasonable delays, Mr T's transfer was not

valid. The UK will itself become a third country for completed in time to enable him to take advantage of

these purposes from the end of April (although this the fall in the stock market following the Brexit vote.

may be extended) under the Brexit deal and we await Mr T had appealed to the High Court, after the initial

the decision of the European Commission with Ombudsman decision in 2018 only compensated him

respect to what this will mean for data transfers from for distress and inconvenience. On remission, the

the EEA to the UK going forward. Ombudsman upheld Mr T's complaint. Though not

able to establish exactly what would have happened,

Palestine Solidarity Campaign - Investment on the balance of probabilities the Ombudsman held

strategy. The Supreme Court found the Secretary of that Mr. T would have invested £250,000 cash in the

State had exceeded his powers by issuing guidance FTSE 100 immediately after the leave vote and that

prohibiting investments by local government pension had he done so, he would have made a profit of

schemes that ran counter to the Government's £43,700. The Ombudsman awarded the lost profit as

foreign or defence policy. Power to direct how compensation, plus interest of 8%. This is an

administrators should approach non-financial (e.g. important decision showing the need to process

ESG) considerations did not include a power to direct transfer requests without undue delay, and how

what investments they should not make. foreseeability and measurability of loss may be

Administrators of local government pension schemes considered and determined in this context.

are quasi-trustees who should act in the best

interests of members, and the funds of the scheme

represented the employee's money, not public

money. ESG considerations should, therefore, be

subject to an overriding duty to act in member's best

financial interests and any guidance from the

Secretary of State has to be read in that context.

5Mr Y (PO-27002). Incomplete member records and a indicated retained GMP liabilities in the plan for Mr Y.

claim for deferred pension GMP benefits were No evidence was provided as to why Mr Y would

discovered for Mr Y during the plan's GMP have lost his entitlement to a deferred pension. The

reconciliation exercise. However, Mr Y's employment Deputy Ombudsman therefore concluded that on the

and pension records were no longer available and Mr balance of probabilities Mr Y was entitled to a full

Y was unable to provide evidence of his benefit deferred pension and not just the GMP element. Mr Y

entitlement. The scheme's management team were was also awarded £500 for significant distress and

therefore only prepared to provide Mr Y with a GMP, inconvenience. The determination clearly shows the

but Mr Y claimed that he was entitled to a full need for good record keeping by all parties involved

deferred pension. The Deputy Ombudsman noted with running a pension scheme and it is useful to

that she could only form her opinion based on the show where the Deputy Ombudsman considered the

evidence available and clearly NICO records burden of proof lies in such cases.

KEY CONTACTS

Danielle Klinger Hannah Moxon Sue Tye

Senior Associate Associate Of Counsel

+44 20 7919 1490 +44 20 7919 1068 +44 20 7919 1178

danielle.klinger hannah.moxon sue.tye

@bakermckenzie.com @bakermckenzie.com @bakermckenzie.com

6The year ahead - what will 2021 hold for trustees and

employers?

2021 is also shaping up to be another busy year. In receiving trustees, the judge did not address this

this session, we looked ahead at issues around GMP issue directly.

equalisation and conversion, the Pensions Schemes

What does 2021 hold? GMP equalisation should be

Bill, including DB funding requirements and

at the top of many trustees' agendas. In terms of

contingency planning for employers becoming

which method trustees are likely to select, whilst the

distressed.

two principal dual records methods, Methods C2 and

GMP Equalisation and Conversion B, are likely to be more straightforward from a legal

perspective, they may cause more of a long-term

GMP equalisation: Equalisation projects under so- administrative burden on schemes. Conversely, GMP

called "dual record" equalisation methods (such as conversion throws up more legal issues but the

Methods C2 and B) can more easily get underway in administrative burden may be lighter. A comparison

2021 as HMRC provided helpful tax guidance in 2020 of all options should be discussed with advisers.

that will enable adjustments to be made to members'

benefits without, for the most part, affecting members' Pension Schemes Bill Developments

personal tax positions.

The Pension Schemes Bill will shortly receive

GMP conversion: There are more legal issues to Royal Asset. The implementation of the various

work through on GMP conversion projects, including provisions will occur at different times, for example

which employer should consent to a conversion and the new Regulator powers provisions will take effect

benefits to be provided for contingent beneficiaries. by the Autumn following a consultation, production of

Benefit adjustments may also cause significant Regulator guidance by the Regulator, and new

annual allowance and lifetime allowance tax issues regulations.

for deferred members, for whom there may also be

The Regulator has new powers, but the big

actuarial challenges in calculating the converted

question is how it will use them. New grounds on

benefits. HMRC has yet to provide further tax

which to issue contribution notices will make it easier

guidance and a PASA working group aims to provide

some clarity in the first half of 2021. Specialist advice for the Regulator to issue these notices compared to

the current options. However, we don't necessarily

will be required.

expect a dramatic increase in the number of notices

Historic transfers: Following the November 2020 being issued - individual case circumstances and

Lloyds judgment, trustees should consider historic Regulator appetite/capacity to pursue will affect this.

transfers where the GMP was not equalised prior to

The most high profile changes are in relation to

transfer. Trustees should get advice specific to their

new criminal offences and civil penalties. The

circumstances. Broadly, for transferring trustees, a

top-up is due automatically where the original transfer potential for a prison sentence of up to 7 years will be

a strong deterrent for companies not to take action

was carried out under the cash equivalent transfer

that will be detrimental to a pension plan, as will the

value legislation. Where the transfer was carried out

under the scheme rules or was part of a bulk transfer, new £1 million civil fine. There may be more

sanctions early on as companies, trustees and

there is no automatic top-up payable, although funds

advisers digest the implications of the new powers

may have to be paid, for example, if a member

challenges this or where contractual documentation and the Regulator's approach.

requires this. Trustees need to consider proactively We expect the greatest impact of the changes will

they should pursue making top-ups; there was little be the new statement of intent. Trustees have

guidance in the judgment. The extent of proactivity sometimes been considered as an afterthought in

will be scheme-specific and will depend on various transactions, and the new statement of intent will

factors (including balancing administration costs and require companies to consult with trustees and

data availability). For receiving DB trustees, the consider the impact of a transaction on a defined

judgement confirmed that they are obliged to benefit pension plan. This is the area where there is

equalise GMPs, even in respect of pre-transfer the greatest uncertainty over how it will operate in

service, whether or not a top up is paid. For DC practice, in particular concerning at what stage in a

7transaction notifications will need to be made to signed by the Trustee chair and on which the

trustees, and how this will apply in different types of employer has been consulted on certain aspects

transactions (e.g. auction sale or public takeover). (the supplementary matters).

There are other changes in the Pension Schemes The "Statement of Strategy" must be

Bill too. Along with the Regulator powers, there are submitted to TPR periodically (the

also changes to introduce new obligations on Regulations are to prescribe how often)

schemes to consider climate change, and to give

The Statement of Strategy will also need to

greater powers to stop transfer values to prevent

scams. set out supplementary matters, including:

the extent to which the funding and

DB Funding Requirements

investment strategy is being successfully

Given the size of some Defined Benefit scheme implemented, including any remedial

liabilities, and the range of covenant support steps;

available to the schemes, it is not surprising that

main risks faced by the scheme in

scheme funding and investment remains a key area

implementing the funding and investment

of regulation through primary and secondary

strategy and intended mitigation or

legislation and through the Regulator's Code of

management of risks;

Practice.

reflections on any significant past decisions

As the last major revision of the funding requirements

taken by the trustees or managers that are

was made under the Pensions Act 2004, the time is

relevant to the funding and investment

ripe for an overhaul.

strategy (including any lessons learned that

The thrust of the new funding framework, already have affected other decisions or may do so in

anticipated in the Regulator's annual funding the future). Regulations will flesh out the

statements, is that there should be a long term detail and level of prescription and Section 10

objective for the scheme supported by a funding and Civil penalties will apply for non-compliance.

investment strategy to achieve it. Schemes are

Regulator role: Consultation on the new Code

already anticipating/debating what that long term

and the Fast Track/Bespoke approaches

objective should be. However, we await much of the

detail. The Regulator will have a key role in the new

funding regime, given the power to apply civil

More detail as regards the provisions of the

penalties and a new power under s 231 of the

Pensions Schemes Bill/Act 2021

2004 Act to direct the trustees to revise the

The primary legislation requires a funding and strategy in accordance with the Regulator's

investment strategy to be determined by the direction where there has been non-compliance.

Trustees, and where necessary, from time to

The Regulator is consulting on the new Code of

time, revised. This strategy is defined as "a

Practice to deal with the new requirements,

strategy for ensuring that pensions and other

including the approach to the long term funding

benefits under the scheme can be provided over

objective.

the long term".

This long term objective will be different for

The strategy must be agreed (in most cases) with

different schemes depending on the applicable

the employer.

circumstances e.g. it may mean targeting buy-

The strategy must also set out the funding level out, or "self-sufficiency" (i.e. where the scheme

to be achieved under it. The "relevant date" for no longer reliant on employer support).

achieving this funding level will be determined

The Regulator has suggested two approaches to

under Regulations - expected this year.

achieve this over time as regards actuarial

In addition, Trustees have to determine the valuations in respect of a scheme – the Fast

investments they intend to hold at that relevant Track and the Bespoke.

date.

Fast Track - the parameters for this will be

Having determined, or revised the strategy, the prescribed and where this approach is adopted

Trustees must produce a written statement of it, there will likely be less Regulator engagement.

8 Bespoke - as the name suggests - will allow insulation for member DC and DB benefits from

greater flexibilities than Fast Track but will likely employer distress or scheme termination?

involve greater Regulator engagement.

4. Identify and prioritise known issues

The Regulator's response to the first consultation is remediation - actively decide whether technical

eagerly awaited and will help set the context for the or structural issues (e.g. benefit discrepancies)

second consultation on the text of the new Code should be addressed whilst employer support is

expected later this year. available.

Protecting Schemes from Employer 5. Funding arrangements and support: holistic

Distress: Legal Aspects of Contingency review - at a proportionate level - of legal and

Planning practical support; in short, know what there is

and what needs to be done should employer

The Pensions Regulator's November 2020 distress materialise.

guidance is the latest - and clearest and most

itemised - list of expected actions of trustees for 6. Legal covenant - linked with 5, document the

up-front planning (in particular when employers are understanding of the suite of support, triggers

not in distress) to address risks that flow from and processes.

insolvency. There is no "template" policy or checklist

7. Information disclosure protocols - understand

and a core theme is "integrated" planning across

or put in place appropriate, transparent and

legal, funding, investment and covenant work

enforceable legal and practical arrangements

streams.

covering employer financial disclosures

Trustees (and employers) will want a (covenant monitoring) and a framework for

proportionate approach - and need to start the member and regulatory disclosures.

diligence somewhere. We suggest the following

8. Operations and governance - holistic

"top 10" with a legal slant to commence the due

consideration of operational continuity from

diligence (and, crucially, prioritisation) process and

administration, payroll, key personnel and a "go

lead naturally to other core areas in preparing an

to" Continuity Policy framework itself - in short,

integrated policy:

ensuring the scheme can operate independently

1. Trust Deed and Rules - core powers of the employer.

assessment and improvement where needed to

9. Data protection by design - embed this into all

ensure functionality on employer distress.

work streams.

2. Third party contracts - ensure relevant

10. Trustee knowledge and understanding -

continuation or transition powers and services

shaping the Continuity Policy; understanding

are in place (starting with core ones - others

delegated roles and "first response" actions;

might be parked until signs of employer

periodic review and refresh as with all

distress).

governance frameworks.

3. Expense reserving - can arrangements be put

in place and documented today to give greater

KEY CONTACTS

Jeanette Holland Jonathan Sharp

Partner Partner

+44 20 7919 1171 +44 20 7919 1415

jeanette.holland jonathan.sharp

@bakermckenzie.com @bakermckenzie.com

Arron Slocombe Vicky Thompson-Hill

Partner Knowledge Lawyer

+44 20 7919 1240 +44 20 7919 1913

arron.slocombe victoria.thompson-hill

@bakermckenzie.com @bakermckenzie.com

9Looking towards long term objectives:

DB consolidation and buy-out

And in our final session we looked at strategic solutions to defined benefit pension provision.

Defined Benefit Solutions: What is your endgame?

It is far from surprising that in these times of great single section for all employers and the collective

uncertainty, employers supporting, and trustees employer covenant will be pooled.

running, defined benefit pension plans are asking

themselves the important question: what steps How do the various categories differ?

should we be considering to ensure the continued This is best illustrated by the following table:

provision of benefits to plan members i.e. to ensure

that the main purpose of the pension plan can be

Key DB Master Stoneport Superfund

fulfilled? For employers, who have their businesses to

considerations trust

focus on, what is the best strategy for the

company/group to mitigate risk, limit management Continued Yes Yes No

time and reduce cost volatility? For trustees, theirs is employer

a constant quest to achieve better security for the support

plan members' benefits.

Covenant Employer Employer Capital

So, there is much to consider; the legal, actuarial, provided by then all buffer

investment, covenant and governance aspects must employers

all be taken into account. And the range of options in

the market and legislative framework is developing Main employer Cut Cut Pension

fast. rationale for costs/admin costs/admin fund no

joining and longer a

We took the opportunity in our seminar to look at two strengthen company

endgame solutions; the DB consolidator market and employer liability

capital backed investments. We were delighted to covenant

have be joined by Richard Jones, Chief Executive of

Stoneport Pensions and a director of Punter Southall Regulation Occupational Occupational Occupational

Solutions Limited, who provided his insights into the pensions pensions pensions

legislation legislation legislation

wider DB consolidator market and the ways in which

the different consolidator models safeguard Regulator

members' benefits. guidance

Ultimately,

DB Consolidators bespoke

What are they? legislation

There is no set definition of "DB consolidator". We

have defined it to mean any multi-employer pension

scheme which is set up to provide benefits to Why have they been developed and how is the

employees and former employees of multiple, non- market developing?

associated employers. That definition will incorporate DB consolidators are an inevitable consequence of

DB master trusts and alternative forms of the closure of DB schemes to new membership and

consolidator vehicle as well as superfunds (currently accrual. With DB schemes now being seen by many

limited to Clara and the Pension Superfund), companies as sizeable balance sheet liabilities and

An example of an alternative form of consolidator is costly to administer, there is a strong desire to cut the

the Stoneport Pension Scheme established by Punter cost of running them or to remove the liability from

Southall. This scheme is initially a segregated DB the balance sheet at a lower cost than buy-out. Each

master trust, but once there are a sufficient number of category of master trust appeals to different

employers, the scheme will be centralised into a segments of the market:

11DB master trusts typically appeal to smaller Capital-backed Solutions

schemes as they often improve governance at a

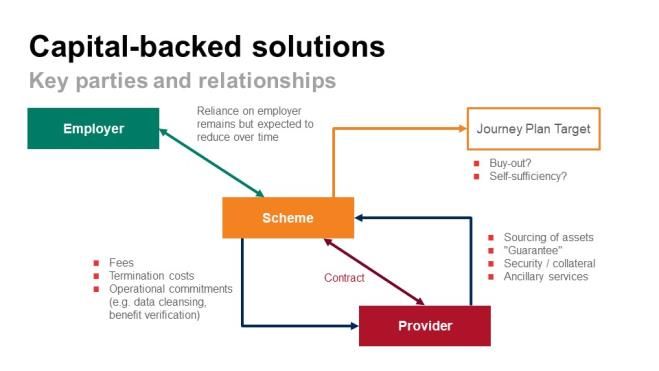

The "capital-backed solution" (also known as the

lower cost.

"capital backed journey plan") is one of the most

Stoneport is aimed at schemes with fewer than recent innovations in the DB sphere. The market in

1,000 members – it is looking for no more than 100 this area is young and still evolving. At the time of

schemes to join and will then close for business and writing only one capital-backed solution had been

become a centralised scheme. publicly announced. However, we understand that

more deals may be in the pipeline and other

Superfunds are likely to focus on larger, less mature providers may be looking to enter the market.

schemes with relatively strong employers and

potentially schemes which pass through a PPF What are they?

assessment period following employer insolvency as

Essentially, a capital-backed solution is a contractual

an alternative to securing PPF+ benefits with an

arrangement between a pension scheme and a

insurer. We may see this aspect of the market

solution provider, which puts up capital to support the

developing in the current economic conditions.

scheme's journey plan. Generally, the link between

What is the key consideration for trustees in the sponsoring employer and the scheme will remain

deciding whether to transfer to a consolidator? and the trustees will remain responsible for running

the scheme.

This whether to transfer to a consolidator will give the

greatest likelihood of members receiving their The aim is to reach a particular target (potentially

benefits in full. Trustees must consider consolidators buy-out) with the additional capital support providing

along with all other potentially available options. scope to retain investment risk for longer – and

therefore potentially reaching the scheme's target

For a master trust, this is essentially a governance more quickly.

and cost question, as members continue to benefit

from the employer covenant. The capital support is intended to provide a measure

of protection if things going wrong (in addition to the

Similarly with Stoneport the employer covenant employer covenant) - recognising that the

remains. The key issue here is whether the pooling of arrangement will likely involve the scheme

the scheme's employer covenant with that of a maintaining a higher level of risk in its investment

number of other employers will improve members' strategy for longer. Although it will likely provide a

benefit security. measure of protection for investment, interest rate

and longevity risk (for example, the provider may

For Superfunds, the employer covenant is replaced

provide a level of "guarantee" on asset performance),

by a one-off contribution by the employer and some

there are likely to be limits to this protection. There is

external third-party capital. The main considerations

therefore a lower degree of risk transfer than in a fully

for trustees who are contemplating a superfund

insured solution (such as a buy-in) but this should be

transfer include:

reflected in the cost of the arrangement.

If benefits can be bought out now or in the

The solution may include ancillary services, including

foreseeable future, a superfund is not necessarily

fiduciary management or liability management

the best option.

exercises supported by the provider to assist the

Will joining enhance the funding level as a result scheme in reaching its target.

of the employer making an additional capital

contribution?

The level of protection provided by the interim

authorisation and supervisory regime.

Is the superfund structure suitable to the

scheme's liability profile?

For all options in the market, trustees will need to

carry out detailed due diligence, including as to

structure, terms, and likely outcome for members.

12What should trustees and employers be thinking terminated and what are the consequences (e.g.

about when looking at these solutions? any fees or penalties).

It will be important to understand the nuts and bolts of Trustee control and decision-making - the

the arrangement, what value and protection it can trustees will want to understand what this means

add and its limits. Here are some key points to think for the day-to-day running of the scheme, how

about: their governance processes may be affected and

what, if any, role the provider may have in the

Strength of the provider (counterparty risk) - if running of the scheme.

the provider has to be called on to make good on

What is the Pensions Regulator's view?

its "guarantee" how certain can the

trustees/employer be of payment. Note that the The Regulator recognises capital-backed solutions in

stringent solvency rules which apply to insurers its 2020 superfunds guidance as one of the "other

will not necessarily apply. models" available and comments that it is continuing

Limits to any protection for the scheme - to "engage with the proposers of these models to

recognising that these solutions are cheaper than understand them better and to determine whether our

insured arrangements, there will not be a guidance needs to change to reflect these

complete risk transfer to the provider. It will be developments". So there may be further guidance on

important to understand where the limits of any these arrangements.

protection lie.

In the meantime, the guidance suggests that the

Consequences of unprotected risks - what Regulator will expect many of the same principles as

happens under the arrangement if an apply for superfunds to be applied by trustees and

unprotected risk arises? It will be important to employers when assessing capital backed solutions

understand if there are any events which the (although it seems to be accepted that not all of the

arrangement cannot support and which may be a superfunds guidance will be relevant). A fundamental

termination event (e.g. employer insolvency). guiding principle, in the Regulator's view, common to

all "endgame" solutions, is whether the arrangement

Termination and its consequences - in what

is likely to result in a better outcome for members.

circumstances will the arrangement can be

KEY CONTACTS

Jeanette Holland Tom McNaughton Paul Williams

Partner Of Counsel Senior Associate

+44 20 7919 1171 +44 20 7919 1193 +27 11 911 4404

jeanette.holland tom.mcnaughton paul.williams

@bakermckenzie.com @bakermckenzie.com @bakermckenzie.com

13Baker & McKenzie LLP is a member firm of Baker & McKenzie International, a global law firm with member law firms around the world. In accordance with the common terminology used in professional service organisations, reference to a "partner" means a person who is a partner, or equivalent, in such a law firm. Similarly, reference to an "office" means an office of any such law firm. This may qualify as "Attorney Advertising" requiring notice in some jurisdictions. Prior results do not guarantee a similar outcome. © 2021 Baker & McKenzie LLP

You can also read