AI, RPA, Analytics & Banks - Shawn Stewart Partner, Advisory Grant Thornton Cost Effective and Practical uses for - Western Bankers Association

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

AI, RPA, Analytics & Banks

Cost Effective and Practical uses for

Transformational Technologies in Community/Regional Banks

Shawn Stewart

Partner, Advisory

Grant Thornton

Presenting Today

Grant Thornton

Financial Services

Los Angles, California

Shawn Stewart

Partner, Advisory Shawn.Stewart@us.gt.com

Grant Thornton 310.266.6502

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 2

Agenda

Learning Objective

• Discuss trends and transformational technologies that are

positioned to impact our industry

• Identify and understand the relative market positions and state

of leading products/solutions

• Explore practical and cost effective opportunities where your

bank can utilize these advances in technology to better support

your operations and business

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 3

"Technology is anything that wasn’t

around when you were born."

- Alan Kay (Computer Scientist) -

Trends & Transformational Technologies

The Banking industry is changing…

Traditional Banks Banks of the Future

Baby boomers Millennials

Branches Mobile & Social

Face-to-face Digital

Product focus Customer centric

Common (products) Personalized (solutions)

Process driven Agile

Change averse Fast evolving customer needs and Innovative

technology capabilities are forcing banks to

Silos Collaborative

transform the way they do business

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 5

…and the Digital imperative is at the core of most of the disruption

The Four Pillars of Digital Transformation in FS The branch of the future

1. Reinvent the consumer journey

2. Leverage the power of data

3. Redefine the operating model

4. Build a digital driven organization

Digital disruption in Financial Services

Digital will

Digital is a high Most transactions are now made through On Line Banking,

fundamentally change

priority, but banking Customers go to a branch to seek for advice and expertise,

the economics and

providers are moving

competitive landscape usually in relation with a project,

at different speeds

in corporate banking

The mission, number, location, technology of the branches

86% 10%

need to evolve,

75% 80% 85% 90% 95% 100% The evolution of the branch personnel’s skillset is also a

major issue for Retail Banks,

Strongly agree Neutral Disagree or strongly disagree

Digital also leads to the disintermediation of a number of

banking activities and is challenging future revenue streams.

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 6

Data Analytics

Data analytics is the quantitative and qualitative science of

drawing insights from raw information sources.

Many of the techniques and processes of data analytics have been automated

into mechanical processes and algorithms that work over raw data for human

consumption. Data analytics techniques can reveal trends and metrics that

would otherwise be lost in the mass of information. This information can

then be used to optimize processes to increase the overall efficiency of a

business or system.

• Descriptive Analytics: What has happened over a period of time

• Predictive Analytics: What is likely to happen

• Prescriptive Analytics: What should happen (suggesting a course of action)

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 7

Robotic Process Automation (RPA)

Robotic Process Automation (RPA) – software robot that

is programmed to do basic tasks across applications

just as human workers do; performs repetitive tasks more

quickly, accurately, and consistently than a human can.

Designed to reduce the burden of repetitive, high volume

simple tasks on employees.

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 8

AI

Machine Learning (ML) &

Artificial Intelligence (AI) ML

Artificial Intelligence (AI) and Machine Learning (ML) –

computer programs that have the ability to learn and adapt

to new data without human interference; these computer

programs in more advanced AI states have the ability to

rationalize and take actions to achieve a specific goal or

outcome.

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 9

Blockchain

At its most basic level, blockchain is literally just a chain of blocks, but not in

the traditional sense… digital information (the “block”) stored in a public

database (the “chain”). Blocks on the blockchain are made up of digital pieces

of information. Specifically, they have three parts:

1. Blocks store information about transactions, say the date, time, and dollar amount of

your most recent purchase

2. Blocks store information about who is participating in transactions. Instead of using

your actual name, your purchase is recorded without any identifying information

using a unique “digital signature,” sort of like a username.

3. Blocks store information that distinguishes them from other blocks. Much like you

and I have names to distinguish us from one another, each block stores a unique

code called a “hash” that allows us to tell it apart from every other block.

Blocks are also encrypted and transactions are verified and stored in multiple locations

Source: Investopedia

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 10Blockchain

A Simplified View

Each block has a unique

hash and once entered into

the chain it also contains

the hash of the record

before it.

Each block can store up to

1 MB of info and several

transactions.

identical copies of the

blockchain are stored on up

to millions of computers

Facilitated by private and

public keys

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 11

Source: Financial TimesFinancial Technology (FinTech)

Historically referred to technology employed in the back-end systems of

established financial institutions (old definition)

New technology that seeks to improve and automate the delivery and use of

financial services and banking. At its core, FinTech is utilized to help companies,

business owners and consumers better manage their financial operations,

processes and lives by utilizing specialized software and algorithms that are

used on computers and mobile devices.

Can apply to any innovation in how people transact business, from the invention

of digital money to consuming financial services over your smart phone.

May also refer to industry of companies who produce innovative and disruptive

technologies for financial services.

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 12What are some of the major disruptive

technologies that we will focus on today?

• Data Analytics / Prescriptive Analytics – Mathematical or computational

analytics. Think of this as "most of what is out there now"

• Robotic Process Automation (RPA, or "Bots") – Think of them as

"macros" for your desktop with a bit more logic built in

• Machine Learning (ML) & Artificial Intelligence (AI) – The ability of

machines to create associations where none existed. Think of this as

"teaching a computer to identify patterns, after giving it some basic

instructions" (ML) so that the system can rationalize and take action (AI).

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 13What they are not (at least not yet):

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 14Example: Prescriptive analytics

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 15Example: Robotic Process Automation

Process Candidate Brief Description of Process to be Process Value/Outcomes (% Process Candidate Brief Description of Process to be Process Value/Outcomes

# (Name) Automated How Automatable (%) savings) Pri.

# (Name) Automated How Automatable (%) (% savings) Pri.

1

1

2

2

3

4 3

5 4

6 5

7 6

8

9

10

Activity 1: Fill in

7

8 Activity 2: Edit

9

11

12 these columns 10 this field

13 11

14 12

15 13

14

15

19

Activity 3:

Prepare this Table

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 16Example: Artificial Intelligence

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 17“You never change things by fighting

the existing reality. To change

something, build a new model that

makes the existing model obsolete.”

- Buckminster Fuller (Inventor & Futurist) -

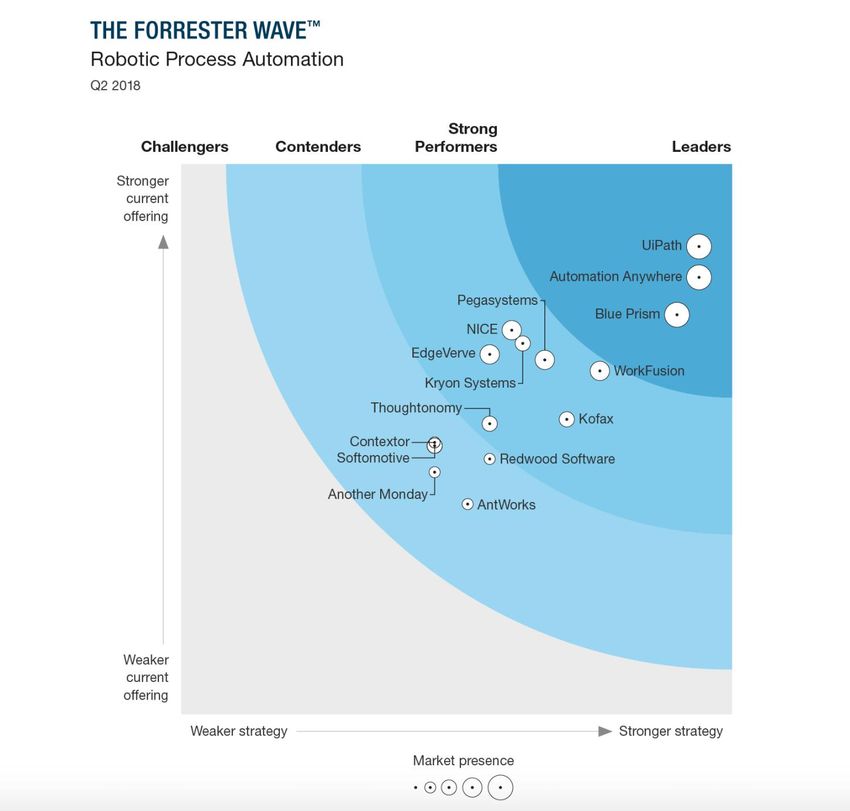

Relative Market Positions & State of

Leading Products/SolutionsDisruptive Technologies

Our Perspective

“Digitized

Start of the “serious” Cloud Infrastructure and Enterprise”

Applications

disruption window Robotic

(size = impact potential) Processing

Chatbots

Pay attention, start planning Natural Language Processing

Cyber

defense

Machine Learning

Artificial

Our discussion today Intelligence

Virtual

Blockchain Reality

"Big Data" Augmented Reality

Predictive &

Prescriptive Analytics

“Manual

Enterprise"

2017 18 19 20 21 22 23 24 2025

© 2017 Grant Thornton LLP. All rights reserved.

4Business Value & Analytic Maturity

Help move your institution from beginners to leaders / disruptors

Level 5

Disruptors

Level 4 - Drives new business

models

Leaders - Aggressively

Level 3 - Sophisticated data

embraces disruptive

Doers science and analytics

potential of analytics,

digital, and emerging

- Specific analytics tool team technologies

Level 2

Maturity

- Dedicated team - Streamlined data and - Disruptive

Thinkers - Integrated quality data defined analytics technologies

Level 1 - Desire to explore & do

- Regular usage of - Continuous monitoring effectively integrated

Beginners more

analytics processes into the strategy of the

- Automation for key - Automation used as a bank and driving a

- Ad-hoc analytics - Excel-based analytics

areas common solution to strategic advantage

- No dedicated team - 1- 3 member team (often

advance operations

- Disparate data wearing multiple hats)

and manage the

- No to very low insights - Low quality data

business

- Limited coverage

Undisciplined Disciplined Dynamic

Business Value © 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 20Cloud

Infrastructure

as a Service

Agility & Reduced Cost

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 21Data Integration

Tools

Efficiencies

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 22Analytics &

Business

Intelligence

Platforms

Actionable Insights

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 23Data Science &

Machine Learning

Platforms

Enhanced Capabilities

Beyond Human Cognition

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 24Robotic Process

Automation (RPA)

• Rapid & Accurate Processing

• Cost Savings

• Quality

• Ability to reassign human

resources to higher use tasks

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 25We are stuck with technology when what

we really want is just stuff that works.”

- Douglas Adams (Author) -

Explore Practical & Cost Effective OpportunitiesPrimary

StrategyValue Drivers

& Execution

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 27Primary Value Drivers

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 28Phased Approach

Explore & Define Collect, Prepare & Model & Evaluate Realize Value,

Transform Data Consume &

Use Case Ideas Generate Insights

Prioritized Use Cases

Profile Use Cases

Assess Impact

Prioritize

Evaluated Use Cases

Planned Projects

Delivered Projects

Capabilities throughout the Engagement:

• Strategy and visioning

• Analytic expertise

• Change management

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 17"Technology presumes there’s just one

right way to do things and there never is."

- Robert M. Pirsig (Writer) -

Use Cases:

Areas for SuccessData Analytics – Why it Matters

Data holds insight, but it is people—not data—who ensure that analytics

generates value for the company.

• Advances in technology are raising expectations for leadership,

creating new needs, and transforming the way we do business

• Analytics is becoming a central focus of leadership agendas

because of its potential to improve profitability, mitigate risk, and

ensure a sustainable organization

• 92% of leaders understand the value of integrating enterprise-

wide data analytics; however

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 31Accounts Payable

Accounts Payable

Analytics and Recovery

Grant Thornton can directly impact the bottom line

of our clients by recovering funds (usually in the

form of vendor credits) for erroneous payment. This

service also is one of the few that can be performed

for contingency fee with appropriate management

approvals.

We use analytics tools that risk rank vendors and

transactions related to invoices and payments. We

also identify outlier transactions for further

investigation to identify unusual, duplicate or

suspicious activity and vendors, and determine cost

recovery potential for duplicate payments. Upon

investigation and confirmation that payments may

be erroneous, we help clients recover those funds

through ongoing communications.

32

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International LtdSpend Analysis

Spending Analytics

Grant Thornton is able to help find recoveries

($$) for our client, clean up their vendor

master, provide insightful analytics, and help

our clients avoid making overpayments to

vendors.

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 33Machine Learning Use Cases

1 Fraud Detection 7 Lifetime Value Prediction

2 Risk Modeling 8 Managing Customer Data

3 Controls Automation 9 Customer Segmentation

4 Compliance Monitoring 10 Personalized Marketing

5 Internal Audit Test Automation 11 Real-time & Predictive Analytics

6 SOD & Security Monitoring 12 Recommendation engines

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 34HAVE YOU HEARD THE NEWS?

AI adoption is exploding…

By 2020: – 85% of CIOs will be piloting AI programs through a To realize business value, AI technologies must be deployed

combination of buy, build and outsource efforts.1 to deliver specific, measureable business outcomes for

– AI technologies will be virtually pervasive in almost targeted use cases.1

every new software product and service.1

By 2021: – The term AI will no longer be considered a

AI will enable you to reduce costs. But its greater impact will

be in answering questions such as, "How do I change the

differentiator in market tech provider solutions.1

nature of the customer experience?" or "How can I initiate

– The dominant source of AI business value will

AI-driven insights to alter all levels of decision-making?"1

be new revenue.1

By 2022: – 40% of customer-facing employees and AI and the CEO: Why Every Company Must Become an AI Company3

government workers will consult an AI-powered

virtual agent every day for decision-making or

process-related support.1

Today: – Tech Giants Are Paying Huge Salaries for Scarce AI Talent:

Nearly all big tech companies have an AI project, and they are willing

to pay experts millions of dollars to help get it done.2

1 Gartner | 2 The New York Times | 3 Forbes Article

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 35Compliance Confidence

Recent reports underscore the opportunity for innovation and analytics within the compliance function

Only

27% of Legal and Compliance executives are confident in

their programs’ ability to manage risk

Top risk areas for legal and compliance executives: By 2020, 85% of CIOs will be piloting artificial

intelligence (AI) programs

Legal and compliance leaders can act to help the organization make smart

decisions by:

• Evaluating controls in newly automated areas to ensure risks are

appropriately managed

• Creating experiences to ensure that legal and compliance staff are exposed

to AI and automation

• Tracking developing regulations that impact emerging technologies.

• Updating existing legal and compliance risk assessments and sensing

mechanisms

• Coordinating with other assurance functions to gauge the adequacy of policies,

communication, and training, and make ongoing improvements

Source: Gartner, Legal and Compliance Hot Spots Report (2018) Source: Gartner Data & Analytics Summit press release (February, 2018)

© 2017 Grant Thornton LLP. All rights reserved.

2Fraud Monitoring

Fraud Monitoring

We help organizations prepare fraud risk analytics to support SAS 99

fraud testing and compliance. This is a shift to a risk-based audit

planning and testing approach, and fraud risk analytics is an essential

component. We use fraud risk analytics to identify:

>> Transactions with risk characteristics present related to financial

reporting fraud, restatement and material weakness in controls

>> Journal entries with descriptions that match potential fraud

keywords - and client or industry specific keywords

>> High risk account pairings and account combinations with a

material impact on financials

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 37The Core Compliance Problem: Compliance is

too expensive and provides little business value

Wasted Time

For every hour an auditor spends, the client spends 8 to 12 hours for

that same audit

High Overhead

SOX adds up to 15% overhead to finance and IT staff for those

companies that wish to be compliant

Poor Value

Clients perceive very little value in testing, yet it still consumes more

than 50% of an auditors time

Lack of Staff Career Trajectory

Our staff quickly realize that testing performed is not valued and that

newer technologies can address this work more efficiently

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 38Changing the nature of risk management

from risk mitigation to value protection

Time savings of 95%+ per control

With Manual Assessment With Automatic Monitoring

8 hours per control Automated control monitoring using advanceMachine Learning

Use Case

Banks are obliged to collect, analyze, and store massive

amounts of data. But rather than viewing this as just a

compliance exercise, machine learning and data science tools

can transform this into a possibility to learn more about their

clients to drive new revenue opportunities.

Nowadays, digital banking is becoming more popular and widely

used. This creates terabytes of customer data, thus the first step

of data scientists team is to isolate truly relevant data. After that,

Managing being armed with information about customer behaviors,

customer interactions, and preferences, data specialists with the help of

data accurate machine learning models can unlock new revenue

opportunities for banks by isolating and processing only this most

relevant clients’ information to improve business decision-

making.

Source; ActiveWizards

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 40Machine Learning

Use Case

The key to success in marketing is to make a

customized offer that suits the particular client’s needs

and preferences. Data analytics enables personalized

marketing that offers the right product to the right

person at the right time on the right device. Data mining

is widely used for target selection to identify the

potential customers for a new product.

Personalized Data scientists utilize the behavioral, demographic, and

marketing historical purchase data to build a model that predicts

the probability of a customer’s response to a promotion

or an offer. This helps banks make efficient,

personalized outreach and improve relationships with

customers.

Source; ActiveWizards

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 41Robotic Process Automation Use Cases

1 Data Replication 6 Customer Service

2 KYC / BSA / AML 7 IT Services

3 Lending 8 Contract Management

4 Payments 9 Compliance

5 Account Closure 10 User Access

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 42Data Replication

Auto Lending Mortgage Origination

Mobile Banking

Core Banking Mortgage Servicing

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 43Robotic Process Automation

Use Case

The pre-RPA implementation commercial lending process is 75 percent

manual, performed by a commercial loan processor in the back office—

each of these steps can be performed by a bot:

• Receive the final commercial loan onboarding package from

Underwriting and other supporting documents from the loan officer via

email

• Open the loan processing system to ensure all the information from the

loan officer and underwriting is in the loan processing system and

complete

• Reconcile, copy, and paste all the missing data from the loan officer’s

Lending email into the loan processing system

• Copy and paste all missing data from underwriting into the loan

processing system

• Prepare the loan file for closing by checking the Secretary of State

website for confirmation of loan applicant business status.

• Sends a standard template email to loan operations for loan booking

once all the paperwork is in good order

The above process takes 45 minutes per loan for a person to complete

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 44Robotic Process Automation

Use Case

Banks receive several requests to close the accounts on a

monthly basis. Sometimes, the accounts can also be closed if

the client does not furnish the proofs required for operating

the account. Considering the high volume of data handled by

the bank every month and the checklist they need to adhere

to, the scope for human error also increases.

With RPA, banks can send automated reminders to the

customers asking them to furnish the required proofs. It can

Account also process the account closure requests in the queue based

Closure on set rules in a short duration with 100% accuracy. RPA is

programmed to cover exceptional scenarios as well such as

closing an account due to failure in KYC compliance. So, this

makes it easier for the bank to focus on other functions that

are less monotonous and require more human intelligence.

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 45Navigating New Technologies

Examples of fintech solutions in place today

• BNY Mellon - Streamline trade settlement procedures – including clearing trades, conducting research on orders and resolving

discrepancies (e.g., reconciling trades) - Normally, human staff take between 5 and 10 minutes to reconcile a failed trade. In comparison,

a bot can perform the same procedure in “a quarter of a second"

• SunTrust has implemented Pega Robotic Desktop Automation in payment operations areas such as Consumer Bank Cards, Wires, and

ACH. Among the results delivered by robotics, the bank noted that average transaction speed improved 3.8x, average training time

improved 4x and the average error rate was reduced by 65 percent

• Deutsche Bank – "We are modernizing our IT and pursuing the digitalization of our business. Today, our private clients can open an

account online in a matter of minutes – and not seven days as before…We have launched robo-advisers (WISE) in the asset

management business and in the Private & Commercial Bank (ROBIN). WISE and ROBIN use algorithms to compile a suitable

portfolio for our clients. In our other businesses, too, we are utilizing robotics and artificial intelligence to automate what were previously

manual processes – this will minimize errors and lower costs.” Annual Report 2017

• Increase speed to process auto loans by validating customer data on government websites, such as the DMV or tax sites

• Reduced time to process consumer loans by eliminating the need to copy and paste data from one banking system to another

• Increase speed and accuracy of new bank account opening requests – eliminate data transfer errors from new account opening

request emails to core banking systems

• Customer service – bots can resolve lower priority inquiries and free up human customer service personnel to handle more complex

inquiries

• Credit card processing – bots are used to gather customer documents, perform credit checks and background checks, and make a

credit decisions based upon set parameters

• KYC process – bots are used to collect customer data, validate it, and perform screening

• Many banks also use chat bots to respond to customer inquiries

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 46Risks & Rewards

The speed and consistency of FinTech are great benefits if

working properly, but the risk exposure if not working properly

can spread across or multiply within the Bank extremely quickly.

Examples include:

• Faulty algorithm

• Incorrect and/or incomplete data accessed

• Process is hacked

• Business and/or economic conditions change but the

technology does not changes with them

© 2017 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd 47Thank-you

You can also read