2023 Global Outlook - Recoveries and opportunities

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

2023 Global Outlook

Recoveries and opportunities

T I M H AY E S , C M T, C H I E F G L O B A L I N V E S T M E N T S T R A T E G I S T

A Special Report by J O E K A L I S H , C H I E F G LO B A L M A C R O S T R AT E G I S T

ALEJANDRA GRINDAL , CHIEF ECONOMIST

Ned Davis Research M A R K P H I L L I P S , E U R O P E A N E Q U I T Y S T R AT E G I S TSPECIAL REPORT GLOBAL OUTLOOK

DECEMBER 14, 2022 email us

NDR 2023 Global Outlook

Special Report Executive summary

Entering 2022, we anticipated “a it is likely to stay higher for longer. continuing recovery in gold.

year of reversals,” with rising equity

Table of Contents

volatility and double-digit weak- Yield curve steepening can be We are watching for better

1 Executive Summary ness. We expect 2023 to include expected. And with interest rate Technology stock performance to

recoveries and present opportuni- volatility subsiding, MBS and support global breadth and U.S.

2 Global Allocation

ties, with most central banks long-term corporate spreads relative strength. While a risk for

7 Global Fixed Income ending their tightening cycles. should narrow, leading to outper- Europe is that too much good

formance. EM bonds should also news has been discounted too

9 Global Economy

The increased probability of a be supported. And EM equities are early, a choppy uptrend is likely for

13 Europe severe global recession adds an likely to recover as EM currencies European equities. Cyclical sectors

element of risk to the outlook. And strengthen and the U.S. dollar should outperform defensive

while inflation has peaked globally, weakens, consistent with a sectors.

Toplines for NDR’s 2022 Global Outlook

Global Allocation

• Cyclical bull market potential supported by pessimism extreme, rally confirmation and Global Balanced Account Model.

• Continuation of secular bull makes it likely that cyclical bear has ended.

• Watching for improved Tech sector performance to support U.S. relative strength, emerging markets to benefit from

dollar weakness, and continuing dollar downtrend, gold uptrend.

Global Fixed Income

Strategists

• Except for Japan, tightening cycles to end in the first half of 2023.

Tim Hayes, CMT, • We see opportunities building in bonds, spread product, and cash. Once again, bonds should provide an effective

Chief Global hedge against equity risks in balanced portfolios.

Investment Strategist • Yield curves should steepen later in the year.

Global Economy

Joe Kalish,

Chief Global Macro • We estimate 2.4% real global GDP growth in 2023 and assign a 65% chance of severe global recession.

Strategist • Recession in developed economies and a Chinese reopening present offsetting risks.

• Global inflation has peaked but will stay higher for longer.

Alejandra Grindal, Europe

Chief Economist

• Bullish technical indicators suggest risk appetite could continue into the start of 2023.

• But the full impact of central bank tightening on the European economy and falling earnings could result in choppy

Mark Phillips,

markets as 2023 progresses.

European Equity

Strategist • Falling inflation and yields and an improvement in the outlook for economic growth, could pave the way to a strong

year end.

PERIODICAL | ISSUE: #SP20221214 | NDR.COM Please see important disclosures at the end of this report. DECEMBER 14, 2022 1GLOBAL OUTLOOK A L LO CAT I O N

T I M H AY E S , C M T C H I E F G LO B A L I N V E S T M E N T S T R AT E G I S T

DECEMBER 14, 2022 email us

An equity uptrend

Expect cyclical bull confirmation within ongoing secular bull

Overweight equities, marketweight bonds, underweight cash

Key Takeaways NDR Global Stock/Bond/Cash Recommendations Daily Data 2008-02-28 to 2022-12-08

Equity Line Based on NDR Global Recommendations (2022-12-08 = 224.89)

Benchmark Equity Line (55/35/10 Stocks/Bonds/Cash) (2022-12-08 = 210.17)

Clip Notes: All lines = 100 on 2008-02-28

• Cyclical bull market potential 158 158

supported by pessimism extreme, 100 100

rally confirmation and Global Recommended Equity % (2022-12-08 = 65%)

80 Maximum 80

Balanced Account Model.

60 60

• Continuation of secular bull makes it 40

Equity Benchmark Weight = 55% Minimum Source: Ned Davis Research, Inc.

40

likely that cyclical bear has ended. 50

Recommended Bond % (2022-12-08 = 35%)

50

40 40

• Watching for improved Tech sector 30 30

performance to support U.S. relative

20 20

Bond Benchmark Weight = 35% Source: Ned Davis Research, Inc.

Recommended Cash % (2022-12-08 = 0%)

strength, emerging markets to

20 20

benefit from dollar weakness, and 10 10

continuing dollar downtrend, gold 0 0

Cash Benchmark Weight = 10% Source: Ned Davis Research, Inc.

uptrend. 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Strategy vs. Benchmark Returns Strategy vs. Benchmark Returns

Allocation recommendations follow I4000 prior Full History: 2005-07-29 - 2022-12-09 Chart View: 2008-02-28 - 2022-12-08

to 2008 and I04000 from 2008-01-01 to 2009-06-04.

Equity Line Gain/Annum Equity Line Gain/Annum

A choppy uptrend is likely in 2023. And a

For more details click here.

Minimum and Maximum Equity Allocations starting from 2008-01-01. Recommendations 5.9% Recommendations 5.6%

Benchmark 5.2% Benchmark 5.2%

severe global recession would increase the Customized version of I4001A © Copyright 2022 Ned Davis Research, Inc. Further distribution prohibited without prior

permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html.

correction risk and elevate the volatility. For data vendor disclaimers refer to www.ndr.com/vendorinfo/

But our base case is that 2023 will include for the year is a conservative expectation. Global Sentiment Composite dropped below

increasing confirmation that global equities When pessimism has been excessive during 10 on September 23, as shown at the top of

have entered a cyclical bull market that the secular bull periods since 1995, the S&P the next page.

started with the October lows, reconfirming 500 has gained 32% per annum, while rising

the continuation of the secular bull market at a 13% per annum rate after entering the While those excessive fear signals have

that started in 2009. Even after the current neutral mode. A rise into that mode can be almost always been followed by rallying over

year’s decline, the ACWI is maintaining a expected as the uptrend gains strength in the subsequent three, six and 12-month

per annum gain of 10% per annum since the 2023. periods, the tendency has been especially

secular bull started. strong after a cyclical bear market has been

We have already gotten positioned for a followed by two consecutive signals. As

Reversing from sentiment better year in 2023, having increased our indicated by the highlighted sections of the

extreme global equity allocation to an overweight chart, the four second signals have been

As the strongest secular bull gains have of 65% versus the benchmark allocation followed by double-digit gains over the

tended to occur early in an advance when of 55% (above). The first hopeful sign was subsequent six months and returns of close

sentiment is still pessimistic, a 10% gain the extreme panic indicated when our DSI to 20% or more over the 12-month periods.

PERIODICAL | ISSUE: #SP20221214 | NDR.COM Please see important disclosures at the end of this report. DECEMBER 14, 2022 2GLOBAL OUTLOOK A L LO CAT I O N

3 | NED DAVIS RESEARCH

Strengthening uptrend Pessimism extremes followed by rallying

Daily Data 2002-12-31 to 2022-12-09 (Log Scale)

MSCI ACWI vs. DSI Global Sentiment Composite

We would never increase exposure based

MSCI ACWI

794 794

on sentiment alone. Broad-based trend 708 708

improvement is needed for assurance that 631 631

the lows are in place. And that’s what has 562 562

501 501

been indicated by our Rally Watch report. 447 447

After the aggregate has first risen above 398

ACWI X-Month Performance Following Initial*

398

355 DSI Global Sentiment Drops Below 10 355

50%, as it did on November 15, a rally has 316

1-Month 3-Month 6-Month 12-Month

316

2003-03-10 7.9 20.0 27.2 41.4

ensued in 81% of the cases since 1981, as 282

2008-09-17

2009-01-20

-18.8

-4.8

-21.4

5.2

-30.3

18.6

-3.8

39.7

282

shown in the chart below. The rallies have

2011-08-08 3.8 8.2 14.4 14.8

251 251

2012-06-01 5.9 8.8 12.1 27.3

224 2014-10-10 5.9 6.0 14.5 5.9 224

been followed be a median advance of 21% 200

Second 2015-08-21 -0.9 4.5 -6.1 4.9

200

signals

2016-01-15 -1.6 8.4 11.0 18.8

over the next 335 days.

2018-03-23 3.2 4.9 8.4 4.3

178 2018-12-24 9.3 15.3 19.1 28.8

178

2020-03-06 -11.2 5.2 10.6 26.2

158 158

2022-03-07 6.5 0.3 -4.7 -

141 2022-09-23 0.7 - - - 141

Model shift to equities 126

*First time DSI drops below 10 in three months Source: MSCI

Mean

Median

Percent Positive

0.5

3.2

61.5%

5.4

5.6

91.7%

7.9

11.5

75.0%

18.9

18.8

90.9%

126

Along with the bullish implications of the 100

DSI Global Sentiment Composite 2022-12-09 = 50.2

100

90 90

sentiment extreme and trend improvement, 80

70

80

70

our equity upgrade was a response to the 60

50

60

50

more favorable implications of our Global 40

30

40

30

Balanced Account Model. The model not 20

10

20

10

0 0

only includes sentiment and price-based Daily Sentiment Index (DSI) Global Sentiment Composite: Equal-weighted composite based futures trader expectations for

S&P 500, NASDAQ 100, Nikkei, FTSE 100, and Euro-Stoxx 50 (DAX and CAC 40 included prior to 2019-11-26) Source: DSI trade-futures.com

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

indicators, but also macro factors related to I4121C © Copyright 2022 NDR, Inc. Further distribution prohibited without prior permission.

All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html

earnings and economic influences. For data vendor disclaimers refer to www.ndr.com/vendorinfo/

Rally Watch signals followed by rallying Consistent with the Rally Watch report,

Maximum Rallies in Global Stocks vs. Rally Watch Indicators Daily Data 2012-12-10 to 2022-12-09

Global Stock Price Index** (2022-12-09 = 2,288.59) the internal components of the model’s

Bullish Signal on 2022-11-15**

3,162

Market Return Since Signal: -0.7%

3,162

stock/bond composite model have shifted

2,512 2,512

to equities, with the composite ending

1,995 1,995

1,585 1,585

November at 75%. And following a buy

1,259 1,259

signal from its credit spread factor, the

1,000 21.9 19.9 21.4 1,000 model’s external composite ended the

15.3 8.9 35.8

794 ** MSCI World Index price returns used prior to 1988, MSCI ACWI price returns used thereafter. Source: MSCI 794 month in its neutral mode at 43%. As a

Percentage of Bullish Rally Watch Indicators (2022-12-09 = 37.50)

result, the model’s recommended allocation

70 70

60 60 moved from an October allocation of 47%

50 50

stocks, 40% bonds and 13% cash to a

40 40

30 30 November allocation of 58% stocks, 40%

20 20

10 10

bonds and 2% cash.

0 0

Bracket = 50 Source: MSCI

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 The model’s decisive reallocation from

** Bullish Signal Expires on 2023-11-15 or

cash to stocks was the primary reason for

After a 5% Correction from the Signal Date,

Whichever Occurs First. the upgrade, with the sentiment extreme

Bullish signals (vertical dashed lines) = % Bullish

Indicators first crosses above 50.

Total Valid Cases Signal Median Median Rally Length Median Length to Rally

Cases (>3% Rally) Accuracy (%) Rally (Calendar Days) (Calendar Days)

and Rally Watch implications supporting a

Repeat signals screened for 12 months.

After screening period the % bullish must reverse above

21 17 81.0 21.4 335 8 more aggressive upgrade than the model

the bracket from below to trigger a new signal.

Shaded periods = max rallies > 3% during the 12 months following signals has called for.

(signal dates followed by corrections of 5% or more excluded)

Customized version of I55G © Copyright 2022 Ned Davis Research, Inc. Further distribution prohibited without prior

permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html.

For data vendor disclaimers refer to www.ndr.com/vendorinfo/

PERIODICAL | ISSUE: #SP20221214 | NDR.COM Please see important disclosures at the end of this report. DECEMBER 14, 2022 3GLOBAL OUTLOOK A L LO CAT I O N

4 | NED DAVIS RESEARCH

Receding rate hike fears 2022 decline consistent with cyclical bears within secular bulls

A History of Bear Markets: Dow Jones Industrial Average (1900-Present)

It was the fear of inflation and its -10

Sources:

influence on central bank policy that 1953

S&P Dow Jones Indices

2016 Ned Davis Research Calculations

drove the stock and bond downtrends this 2011 19711984

1960

1949 1980

-20 1998 1923

1957

year, culminating in the sentiment extreme. 1990

2022

19391934 1947

1982 1914

Stocks and bonds have since trended higher 1962

1966

1978 1911

-30

on the increasing evidence that inflation is 2002

2001

receding, which means that central banks 1987 1970

2020 1933

will be able to slow and eventually stop their -40

1917 1942

rate hiking initiatives. 1974

Loss %

1921 1903

1929 1907

-50 1938

Recognizing that the inflation of 2023 has 2009

been driven by supply disruptions rather -60

than a wage-price spiral, we have made

the case that the secular bear years of the -70

stagflationary 1970s, which were fueled

Cyclical Bears within Secular Bulls

by oil price shocks, are less comparable Mean for Cyclical Bears within Secular Bulls (-22.8% Loss, 198 Days)

-80 Cyclical Bears within Secular Bears

than the late 1940s, when the post-war Mean for Cyclical Bears within Secular Bears (-36.9% Loss, 371 Days)

Mean for All Bear Markets (-31.0% Loss, 299 Days)

reopening produced a short-lived inflation Current Bear Market 1932

spike driven by supply shortages, pent-up 25 50 75 100 125 150 175 200 225 250 275 300 325 350 375 400 425 450 475 500 525 550 575 600 625 650 675 700 725 750 775 800

Market Days

demand and the removal of price controls. S0202C © Copyright 2022 NDR, Inc. Further distribution prohibited without prior permission.

All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html

For data vendor disclaimers refer to www.ndr.com/vendorinfo/

Equities have usually advanced from last rate hike to first cut The earlier spike produced a cyclical bear

Data Updated Through 2022-11-22

MSCI ACWI Performance Between Fed's Last Rate Hike and First Cut

124 1989-02-24 to 1989-06-06 (4.9%) 124

market of -23% on the DJIA in 1946 and

123

122

1995-02-01 to 1995-07-06 (5.9%)

2000-05-16 to 2001-01-03 (-11.5%)

123

122

1947, within an ongoing secular bull. That

2006-06-29 to 2007-09-18 (19.2%)

120 2018-12-19 to 2019-07-31 (14.8%) 120 bear market low is therefore one of the

119 Mean (8.0%) 119

117 117 green dots in the chart above, indicating

116 116

115 115 that the cyclical bears within secular bulls

114 114

112 112 have tended to be shorter and more shallow

111 111

110 110 than the cyclical bears within secular bears

108 108

107 107 (red dots). The black dot identifies the

106

105

106

105

2022 drop of -22%, more consistent with a

104

102

104

102

secular bull than a secular bear.

101 101

100 100

99 99 Considering that the U.S. accounts for 61%

98 98

97 97 of the ACWI’s weight, it would be especially

95 95

94 94 influential if the Fed would end its tightening

93 93

92 92 cycle, with the markets expecting an

91 91

90 90 eventual cut. The chart at left shows that

89 89

88 88 in four of the last five cases, the ACWI has

87

86 Source: MSCI

87

86

moved higher during the period between

85 Based on periods between Federal Reserve Board's last fed funds rate increase in a tightening cycle and first rate cut in an easing cycle

03 12 21 01 10 21 30 08 19 28 09 18 27 07 16 27 06 15 26 04 15 24 02 13 22 05 14 23 03 12 23 02 11 22 31 11 20 29 10 19 30 08 17 28 06 17

85

the last hike and first cut. The exception

Jul '06 Aug '06 Sep '06 Oct '06 Nov '06 Dec '06 Jan '07 Feb '07 Mar '07 Apr '07 May '07 Jun '07 Jul '07 Aug '07 Sep '07

STH22_49A_C © Copyright 2022 NDR, Inc. Further distribution prohibited without prior permission.

All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html

followed the final hike in 2000, during the

For data vendor disclaimers refer to www.ndr.com/vendorinfo/

early stages of the secular bear.

PERIODICAL | ISSUE: #SP20221214 | NDR.COM Please see important disclosures at the end of this report. DECEMBER 14, 2022 4U.S. FOCUS EQUITIES

5 | NED DAVIS RESEARCH

Severe recession scenario Valuations have improved

MSCI ACWI Trailing and Forward Earnings Yield Daily Data 2003-06-30 to 2022-12-09

A similar failure to respond would reflect MSCI ACWI (2022-12-09 = 745.75)

the onset of a severe global recession. With 794 794

631 631

earnings estimates proving to be overly 501 501

optimistic, the disappointments would 398

316

398

316

send equities back to new lows. Instead of 251 251

200 200

considering valuations reasonable at current Source: MSCI

12-Month Trailing Earnings Yield (2022-12-09 = 5.9%)

Global

levels, seeing equities as a far better value recession

10.0 10.0

than a year ago, investors would require extremes

8.0 8.0

much better valuations, as they did

6.0 6.0

around the bottoms in 2009 and 2020. 4.0 4.0

Source: MSCI

12-Month Forward Earnings Yield (2022-12-09 = 6.7%)

12.0 12.0

10.0 10.0

8.0 8.0

6.0 6.0

4.0 Source: MSCI 4.0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

2003-06-30 to 2022-12-09 Mean Median

Trailing Earnings Yield 5.8% 5.7%

Forward Earnings Yield 7.1% 6.9%

Customized version of I182 © Copyright 2022 Ned Davis Research, Inc. Further distribution prohibited without prior

permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html.

For data vendor disclaimers refer to www.ndr.com/vendorinfo/

Tech has most weight in U.S. Otherwise in the absence of a severe

Daily Data 1994-05-31 to 2022-12-09

MSCI United States Sector Weights

Energy Materials Industrials Consumer Discretionary Consumer Staples Health Care Information Technology Communication Services Utilities Financials Real Estate

recession, with interest rate pressures

(4.6%) (2.7%) (8.5%) (10.6%) (7.4%) (15.3%) (26.4%) (7.6%) (2.9%) (11.2%) (2.7%)

100%

BEAR BULL

100%

abating, the Information Technology sector

95% 95% would be better positioned to participate in

90% 90% a global market advance, potentially leading

85% 85%

it.

80% 80%

75% 75%

70% 70%

As the sector’s weight is 26% of the MSCI

65% 65% U.S. Index, (left) better Tech performance

60% 60% would increase the chances that after

55% 55% weighing down the global benchmark with

50% 50%

its underperformance for most of the

45% 45%

year, the U.S. would outperform during a

40% 40%

35% 35%

2023 market advance. Continuing Tech

30% 30% sector breadth improvement would be an

25% 25% encouraging development for the sector and

20% 20%

in turn the relative strength prospects for

15% 15%

the U.S. index.

10% 10%

5% 5%

Source: MSCI

0% 0%

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

ICS_400C_US © Copyright 2022 NDR, Inc. Further distribution prohibited without prior permission.

All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html

For data vendor disclaimers refer to www.ndr.com/vendorinfo/

PERIODICAL | ISSUE: #SP20221214 | NDR.COM Please see important disclosures at the end of this report. DECEMBER 14, 2022 5U.S. FOCUS EQUITIES

6 | NED DAVIS RESEARCH

We are also watching for improved relative

Strengthening emerging market currencies support EM equities

Daily Data 2019-12-09 to 2022-12-09

strength in the MSCI Emerging Markets MSCI Emerging Markets vs. Equal-Weighted Emerging Market Currency Composite

Index now that the U.S. dollar is weakening 79,433

MSCI Emerging Markets (2022-12-09 = 58,968.29)

79,433

(below, top clip), helping our equal-weighted 70,795 70,795

Emerging Market Currency Composite rise 63,096 63,096

above its 50-day moving average (right). 56,234 56,234

When the composite has been above the 50,119 50,119

smoothing, the EM Index has gained more 44,668 44,668

than 20% per annum since 2000 and during

Source: MSCI

Equal-Weighted Emerging Markets Currency Index vs. USD(2022-12-09 = 63.0)

the three years shown in the chart. 50-Day Moving Average (2022-12-09 = 61.8)

72.0 72.0

70.0 70.0

The U.S. Dollar Index downtrend can be 68.0 68.0

expected to continue as long as nominal 66.0 66.0

and real U.S. bond yields continue to fall 64.0 64.0

relative to non-U.S. yields. The widening 62.0 62.0

spreads underpinned the dollar this year

60.0 Source: Ned Davis Research, Inc. 60.0

Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct

until it became clear that the Fed would be 2020 2021 2022

tightening less aggressively. MSCI EM Index Performance

Full History: 2000-03-13 to 2022-12-09

MSCI EM Index Performance

Chart View: 2019-12-09 to 2022-12-09

Equal-Weighted EM % Gain/ % of Equal-Weighted EM % Gain/ % of

Currency index based on 22 emerging market currencies Currency Index is: Annum Time Currency Index is: Annum Time

Above 50-Day MA 22.71 48.45 Above 50-Day MA 25.07 40.24

Below 50-Day MA -10.21 51.55 Below 50-Day MA -13.79 59.76

Buy/Hold = 4.50% Gain/Annum Buy/Hold = 0.13% Gain/Annum

Customized version of I2051 © Copyright 2022 Ned Davis Research, Inc. Further distribution prohibited without prior

permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html.

For data vendor disclaimers refer to www.ndr.com/vendorinfo/

As dollar weakens, gold and EM performing better Aligned with our models, we are entering

U.S. Dollar Index, Gold Futures & Emerging Markets Relative Strength Daily Data 2021-12-09 to 2022-12-09

U.S. Dollar Index (2022-12-09 = 104.93) 2023 with the bearish dollar position

50-Day Moving Average (2022-12-09 = 109.28)

200-Day Moving Average (2022-12-09 = 105.75) assumed in November. And in recognizing

110 110

the dollar’s inverse correlation with gold

105 105 (middle clip), the positive influence of

100 100 declining yields, and the recent buy signal

95 95

from the aggregate indicators in our Gold

91 Source: Bloomberg Finance L.P. 91

Gold Futures (2022-12-09 = 1,817.90) Watch report, we moved to bullish on gold

50-Day Moving Average (2022-12-09 = 1,726.72)

200-Day Moving Average (2022-12-09 = 1,802.01) last week.

1,995 1,995

1,905 1,905

While the S&P GSCI Energy Index has

1,820 1,820

1,738 1,738 continued to trend lower, the Precious

1,660 1,660 Metals Index has reversed higher, as has the

Source: Commodity Systems, Inc. (CSI) www.csidata.com

MSCI Emerging Markets/MSCI ACWI (2022-12-09 = 7,907.22) Industrial Metals Index. The metals recovery

50-Day Moving Average (2022-12-09 = 7,684.52)

200-Day Moving Average (2022-12-09 = 7,891.82) would not be likely to continue with a severe

8,710 8,710

global recession developing.

8,318 8,318

7,943 7,943

7,586 7,586

7,244 Source: MSCI

7,244

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2022

Customized version of I210 © Copyright 2022 Ned Davis Research, Inc. Further distribution prohibited without prior

permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html.

For data vendor disclaimers refer to www.ndr.com/vendorinfo/

PERIODICAL | ISSUE: #SP20221214 | NDR.COM Please see important disclosures at the end of this report. DECEMBER 14, 2022 6GLOBAL OUTLOOK FIXED INCOME

J O S E P H F. K A L I S H , C H I E F G LO B A L M A C R O S T R AT E G I S T

DECEMBER 14, 2022 email us

A better year for fixed income!

Look for steeper curves and more opportunities

Yields should break to the downside on recession fears

Key Takeaways Yields on Key 10-Year Governments Daily Data 2017-12-11 to 2022-12-09

U.S. (2022-12-09 = 3.57%)

U.K. (2022-12-09 = 3.18%)

Germany (2022-12-09 = 1.93%)

Japan (2022-12-09 = 0.26%)

4.5 4.5

• Except for Japan, tightening

4.0 4.0

cycles to end in the first half of 3.5 3.5

2023. 3.0 3.0

2.5 2.5

• We see opportunities building 2.0 2.0

in bonds, spread product, and 1.5 1.5

cash. Once again, bonds should 1.0 1.0

provide an effective hedge 0.5 0.5

against equity risks in balanced 0.0 0.0

portfolios. -0.5 -0.5

-1.0 -1.0

Source: Bloomberg Finance L.P., Federal Reserve Board

• Yield curves should steepen later Jan

2018

Apr Jul Oct Jan

2019

Apr Jul Oct Jan

2020

Apr Jul Oct Jan

2021

Apr Jul Oct Jan

2022

Apr Jul Oct

in the year. Full History Chart History

Correlation Matrix Correlation Matrix

1992-01-02 to 2022-12-09 2017-12-08 to 2022-12-09

Assets U.S. U.K. Germany Japan Assets U.S. U.K. Germany Japan

U.S. 1.00 U.S. 1.00

U.K. 0.96 1.00 U.K. 0.88 1.00

With most developed economies expected Germany 0.95 0.98 1.00 Germany 0.87 0.97 1.00

Japan 0.86 0.93 0.90 1.00 Japan 0.47 0.69 0.73 1.00

to flirt with, or fall into, recession in B190 © Copyright 2022 Ned Davis Research, Inc. Further distribution prohibited without prior

permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html.

2023, central banks are also expected For data vendor disclaimers refer to www.ndr.com/vendorinfo/

to slow, and then end, their tightening

cycles sometime in the first half of next MBS and long-term corporate spreads to Japan remains the exception. The BOJ

year. The market expects the Fed’s terminal ease, leading to outperformance. Lower remains on hold with yield curve control

rate to be around 5.00%, while the ECB’s volatility will also be appealing for EM firmly in place through Q1. But at that

should peak below 3.00%. A 4.50% terminal bonds. point, an expected policy assessment

rate is anticipated for the Bank of England. coinciding with the end of Governor

For the first time in years, discounted Kuroda’s term could result in a policy shift

Bonds could easily rally through yield bonds will be attractive for those investors should inflation continue to run above the

support levels shown on the chart on who favor capital gains over interest BOJ’s 2% target. Core inflation excluding

evidence of recession, slowing inflation, and income. fresh food is current running at 3.6% y/y. In

shifting policy. Once again, bonds could a new regime, JGB yields would likely

provide an effective hedge for equities Cash will also earn a positive nominal rise, putting upward pressure on global

against growth and earnings concerns. return and maybe a positive real return, bond yields. Japan is already favored on a

and be a viable alternative for conservative currency-hedged basis compared to the

With most central banks on hold, rate investors. U.S. and Europe. That could stifle any Q1

volatility should subside, allowing agency bond rally.

PERIODICAL | ISSUE: #SP20221214 | NDR.COM Please see important disclosures at the end of this report. DECEMBER 14, 2022 7GLOBAL OUTLOOK FIXED INCOME

8 | NED DAVIS RESEARCH

Prepare for a steepener in 2023

Government Yield Curve for Select Countries (10-Year minus 2-Year) Daily Data 2021-12-10 to 2022-12-09

U.S. (2022-12-09 = -76.0 bps)

U.K. (2022-12-09 = -24.5 bps)

Germany (2022-12-09 = -22.7 bps)

Japan (2022-12-09 = 26.8 bps)

80 80

60 60

40 40

20 20

0 0

Except for Japan, developed market yield -20 -20

curves are inverted. With recessions likely -40 -40

and policy tightening to end, we anticipate -60 -60

that yield curves will start to produce a -80 -80

bull steepener. -100 -100

Source: Bloomberg Finance L.P., Federal Reserve Board

15 3 18 1 1 15 1 18 2 16 1 15 1 18 1 15 1 16 3 17 1 15 30

1

Jan 2022 Feb 2022 Mar 2022 Apr 2022 May 2022 Jun 2022 Jul 2022 Aug 2022 Sep 2022 Oct 2022 Nov 2022 Dec 2022

Available Term Structures: Full History Chart History

10-Year - 2 Year Correlation Matrix Correlation Matrix

10-Year - 3 Year

1992-01-02 to 2022-12-09 2021-12-13 to 2022-12-09

10-Year - 5 Year

30-Year - 2 Year Assets U.S. U.K. Germany Japan Assets U.S. U.K. Germany Japan

30-Year - 3 Year U.S. 1.00 U.S. 1.00

30-Year - 5 Year U.K. 0.69 1.00 U.K. 0.56 1.00

30-Year - 10 Year Germany 0.64 0.57 1.00

Germany 0.27 0.53 1.00

5-Year - 2 Year

5-Year - 3 Year Japan 0.00 -0.05 0.40 1.00 Japan -0.64 -0.12 -0.06 1.00

B1591 © Copyright 2022 Ned Davis Research, Inc. Further distribution prohibited without prior

permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html.

For data vendor disclaimers refer to www.ndr.com/vendorinfo/

Global credit unlikely to continue its outperformance Global credit has had a remarkable year

Major Sector Credit Performance Relative to the Global Aggregate Daily Data 2017-12-11 to 2022-12-09

Global IG Corporate Credit (USD) / Global Aggregate ex-CNY (2022-12-09 = 120.05) relative to the Global Agg, particularly

120.0 120.0

118.0 118.0

for Europe. But this had more to do with

116.0 116.0 the shorter duration of European credit

114.0 114.0

112.0 112.0

compared to the broader indexes, as credit

110.0 110.0 spreads widened modestly over the course

108.0 108.0

106.0 106.0

of the year. We’re looking for credit to

Source: Bloomberg Barclays Indices

Global HY Credit (USD) / Global Aggregate ex-CNY (2022-12-09 = 193.90) underperform in the first half of next year,

200 200

190 190

creating a better opportunity for credit

180 180 outperformance later in the year.

170 170

160 160

150 150 Although we recently closed out our local

140 140 currency Chinese bond trade, dollar-

130 Source: Bloomberg Barclays Indices 130

Emerging Markets (USD) / Global Aggregate ex-CNY (2022-12-09 = 196.57) denominated emerging market debt has a

195 195 mixed outlook. Although a declining dollar

190 190

is bullish for EM debt, falling commodity

185 185

prices and weak growth tend to result in

180 180

175 175

wider spreads. We are currently neutral and

170

Source: Bloomberg Barclays Indices

170 stuck in a trading range, but are looking to

Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct Jan Apr Jul Oct establish bullish EM positions sometime

2018 2019 2020 2021 2022

B1196C © Copyright 2022 Ned Davis Research, Inc. Further distribution prohibited without prior in 2023.

permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html.

For data vendor disclaimers refer to www.ndr.com/vendorinfo/

PERIODICAL | ISSUE: #SP20221214 | NDR.COM Please see important disclosures at the end of this report. DECEMBER 14, 2022 8GLOBAL OUTLOOK ECONOMICS

ALEJANDRA GRINDAL , CHIEF ECONOMIST

DECEMBER 14, 2022 email us

Severe global recession risk rising for 2023

U.S. and China present offsetting risks

We’ve been in a global slowdown since early 2022

Key Takeaways Global Recession Probability Model Monthly Data 1970-03-31 to 2023-01-31

Global Recession Probability Model (2023-01-31 = 97.00)

High Recession Risk

100 100

95 95

90 90

• We estimate 2.4% real global GDP 85 85

growth in 2023 and assign a 65% 80

75

80

75

chance of severe global recession. 70 70

65 65

60 60

55 55

50 50

• Recession in developed economies 45 45

and a Chinese reopening present 40

35

40

35

offsetting risks. 30 30

25 25

20 20

15 15

10 10

• Global inflation has peaked but will 5 5

stay higher for longer. 0

-5 Low Recession Risk Source: Ned Davis Research, Inc.

0

-5

1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Analysis Dates: 1970-03-31 - 2023-01-31

Actual:

Probability Recession No Recession

Shaded Areas Represent OECD-Defined

Model (% of Time) (% of Time)

Global Slowdown Periods

Above 70 84.24 15.76

2022 saw global growth slow markedly, Between 30 and 70 58.21 41.79

Below 30 15.20 84.80

albeit from extremely elevated levels, amid IE90 © Copyright 2022 Ned Davis Research, Inc. Further distribution prohibited without prior

permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html.

waning monetary and fiscal support, stub- For data vendor disclaimers refer to www.ndr.com/vendorinfo/

bornly high inflation eating into incomes,

and supply shocks emanating from the downside, and we assign a 65% chance global economy in 2023. Historically, global

Russia’s war in Ukraine and China’s ze- of severe global recession. growth rates under 2.5% have been asso-

ro-COVID policy. Indeed, we began to see ciated with severe global recession. Based

evidence of this slowdown in early 2022, Most of the downside risks that plagued on historical norms, the peak-to-trough

as our Global Recession Probability Model, 2022 will likely continue in 2023, but from decline in global equities we’ve seen this

which is designed to identify OECD-de- a much lower starting point. Global savings year has already priced in a moderate

fined global slowdowns, jumped into the have been depleted, while labor markets global slowdown. However, a severe global

high-risk zone in February (see chart). are starting to show signs of slowing. More- recession has not. This would suggest that

over, given the lagged impact of monetary if severe global recession develops, there

Global recession risk for 2023 policy on the economy, the indicators, will be more global equity volatility in 2023.

For most of the year, we have characterized many of which are already on the cusp of

the global slowdown as being moderate, levels associated with global recession, are Our Severe Global Recession Watch

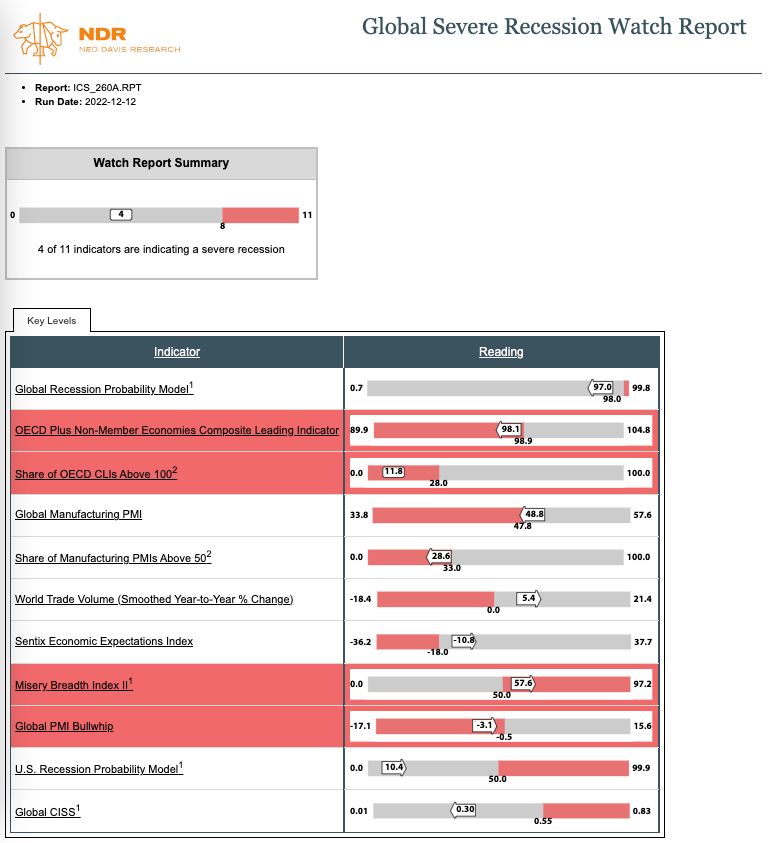

given insufficient evidence from our Severe likely to worsen in the coming months. report is showing that four out of the

Global Recession Watch report. Howev- eleven indicators are at severe recession

er, going into 2023, the risks are to the We estimate 2.4% real GDP growth in the levels. We’d like to see a firm majority

PERIODICAL | ISSUE: #SP20221214 | NDR.COM Please see important disclosures at the end of this report. DECEMBER 14, 2022 9GLOBAL OUTLOOK ECONOMICS

10 | NED DAVIS RESEARCH

before making the call. Many, including

Four out of 11 indicators are at severe recession levels

the composite PMI and PMI breadth, are

extremely close to generating negative

signals. Although the sample size is limited Source: Haver Analytics, Ned Davis Research, Inc., OECD, Main Economic Indicators

(MEI), www.oecd.org, S&P Global PMI

to just two severe recessions (GFC and

Indicators which have fallen below their key severe recession level are highlighted red.

COVID recessions), we haven’t seen more 1 A rise in this indicator indicates an increased probability of recession.

2 This indicator must be past the key recession level for three consecutive months to

than four indicators giving negative signals indicate an increased probability of recession

without imminent recession.

Global central banks have engaged in the

broadest and fastest monetary tightening

since at least the late 1990s, when our

data begins. As shown in the chart below,

since monetary policy happens with a lag,

the global economy has yet to see the

full economic impact derived from this

aggressive global tightening.

U.S. recession risk rising

Like the global economy, the risk of reces-

sion weighs on the outlook for U.S. economic

growth in 2023. We project real GDP growth

Tight global monetary policy hasn’t fully fed into the economy will end the year in a range of -0.5% to 0.5%.

Global PMI vs. Central Bank Breadth Monthly Data 1998-01-31 to 2023-11-30

Global Manufacturing PMI (Scaled Left) (2022-11-30 = 48.84) We see a 75% chance that the economy

58.0

Percent of central banks whose last rate change was a decrease (Advanced Twelve Months, Scaled Rig…(2023-11-30 = 11.8%)

100

contracts for part of 2023 and give 25%

57.0

56.0 95 odds to a soft-landing scenario. Historically,

55.0

54.0

90

severe global recessions have always been

85

53.0

80

accompanied by U.S. recession. A soft landing

52.0

51.0 75 depends on continued resilience of the labor

50.0

49.0

70

market, smooth domestic policy, and dimin-

65

48.0

47.0 60 ishing geopolitical tensions. For more details,

46.0

45.0

55 see our 2023 U.S. Outlook publication.

50

44.0

43.0 45

42.0

41.0

40 China’s COVID crisis

40.0

35

China’s economy presents the greatest un-

39.0 30

38.0 25

certainty to the global outlook. In response to

37.0

36.0

20 protests and unrest, the government has dra-

35.0

34.0

15

matically pared back its extremely restrictive

10

33.0

32.0 Source: Haver Analytics, S&P Global PMI

5 COVID protocols. As we wrote in our Novem-

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 ber 17 publication, a clean reopening could

see a boost of 2.0-2.5 points to real GDP

Full History

Shaded Areas Represent OECD-Defined

Global Slowdown Periods

1998-01-31 to 2022-11-30 growth, which could bring growth to over 6%.

Correlation Coefficient = 0.50

IE253 © Copyright 2022 Ned Davis Research, Inc. Further distribution prohibited without prior

permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html.

For data vendor disclaimers refer to www.ndr.com/vendorinfo/ But this goal is highly elusive. First, the easing

PERIODICAL | ISSUE: #SP20221214 | NDR.COM Please see important disclosures at the end of this report. DECEMBER 14, 2022 10U.S. FOCUS EQUITIES

11 | NED DAVIS RESEARCH

of measures must actually happen and go

An end to zero-COVID could be a boon for Chinese economy

Daily Data 2020-04-01 to 2022-12-09

COVID Indicators for China

smoothly. Given the abrupt and premature 500,000

Weekly New Cases 2022-12-09 = 233,355

500,000

450,000 450,000

nature of the reopening, there’s no guarantee. 400,000 400,000

350,000 350,000

Large swaths of the population could choose 300,000 300,000

to disengage from the economy given the 250,000

200,000

250,000

200,000

rising risk of infection and death. Also, other 150,000

100,000

150,000

100,000

elements of the economy, such as external 50,000 50,000

0 0

demand and real estate remain fragile. As a 60.0

China Markit Services PMI 2022-11-30 = 46.73

Source: Johns Hopkins University

60.0

57.5 57.5

result, we project the Chinese economy will 55.0 55.0

grow 4.25% to 4.75% in 2023. 52.5

50.0

52.5

50.0

47.5 47.5

Eurozone’s mild recession

45.0 45.0

42.5 42.5

40.0 40.0

Based on the weight of evidence presented 37.5 37.5

35.0 35.0

in our Eurozone Recession Watch report, it’s 57.5

China CFLP Services PMI 2022-11-30 = 46.70

Source: S&P Global PMI

57.5

highly likely that the economy fell into re- 55.0 55.0

cession in Q4 2022 due to the energy shock 52.5 52.5

50.0 50.0

brought by Russia’s war and tighter monetary

47.5 47.5

policy. We forecast a 0.0% to 0.5% growth rate 45.0 45.0

for the eurozone in 2023, as the recession 42.5 42.5

continues into next year. May Jul Sep Nov Jan Mar May Jul Sep Nov Jan Mar May Jul

Source: Haver Analytics

Sep Nov

2020 2021 2022

IE15254A © Copyright 2022 NDR, Inc. Further distribution prohibited without prior permission.

All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html

But given a starting point of low unem- For data vendor disclaimers refer to www.ndr.com/vendorinfo/

Eurozone likely already in recession ployment, a cushion of savings due to the

Monthly Data 2005-01-31 to 2022-11-30

Number of Indicators Past Key Recession Level in NDR Eurozone Recession Watch Report pandemic, and fiscal support to households

8.0

Number of Indicators Past Key Recession Level (2022-11-30 = 7)

8.0

to help combat the cost of higher food and

7.5 7.5 energy prices, we expect the recession to be

7.0 7.0 mild. The outlook, however, is uncertain and

6.5 6.5

is almost entirely driven by energy. Cold-

6.0 6.0

er-than-normal weather and an escalation in

5.5 5.5

5.0 5.0

geopolitical tensions could easily see energy

4.5 4.5 prices spike again, posing risks to the econo-

4.0 4.0 my and inflation.

3.5 3.5

3.0

2.5

3.0

2.5

Peak inflation behind us

2.0 2.0 The global inflation rate has likely carved

1.5 1.5 out a top due to waning demand and global

1.0 1.0 supply chain pressures and peak oil and food

0.5 0.5

prices. As shown in the top chart on Page 12,

0.0 0.0

-0.5 -0.5

global supply chain pressures have eased

Source: Ned Davis Research, Inc.

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 significantly, which should continue to put

downside pressure on inflation.

Shading indicates ECRI-defined recessions

The NDR Eurozone Recession Watch Report (ICS_260_EU.RPT) includes 8 key economic indicators.

Once a majority turn negative, a recession is more likely

IE1030 © Copyright 2022 Ned Davis Research, Inc. Further distribution prohibited without prior However, inflation is likely to stay higher for

permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html.

For data vendor disclaimers refer to www.ndr.com/vendorinfo/ longer. Continued adjustment to pandemic

PERIODICAL | ISSUE: #SP20221214 | NDR.COM Please see important disclosures at the end of this report. DECEMBER 14, 2022 11U.S. FOCUS EQUITIES

12 | NED DAVIS RESEARCH

imbalances, tight labor markets, and the Global inflation is peaking

OECD CPI vs. Global Supply Chain Pressure Index I Monthly Data 2009-01-31 to 2023-08-31

risk of further supply shocks (either geo- OECD Area CPI (Year-to-Year Change, Scaled Left)(2022-10-31 = 10.7%)

political or weather related) will likely see Global Supply Chain Pressure Index (Advanced Nine Months, Scaled Right)(2023-08-31 = 1.20)

10.5

inflation rates remain above central bank 10.0 4.0

targets through the end of 2023, indicating 9.5

9.0

3.5

pivots are unlikely in the near-term. 8.5

3.0

8.0

7.5

2.5

7.0

A quick reopening of the Chinese economy 6.5

2.0

provides upside risk to global inflation, but 6.0

5.5 1.5

likely not in the traditional consumer goods 5.0

4.5 1.0

sense. The potential upside could come 4.0

from energy prices, as consumers see an 3.5

3.0

0.5

increase in domestic mobility. 2.5 0.0

2.0

1.5 -0.5

1.0

The U.S., however, as the world’s largest 0.5 -1.0

consumer, is a much bigger player in the 0.0

-0.5

-1.5

global economy and inflation. Indeed, as -1.0

Source: Federal Reserve Bank of New York, OECD, Main Economic Indicators (MEI), www.oecd.org

-2.0

-1.5

shown in the chart at below, the U.S. CPI 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

tends to lead the rest of the world by

Full History Chart View

around six months. Although we expect U.S. 1998-06-30 to 2022-10-31 2009-01-31 to 2023-08-31

Correlation Coefficient = 0.61 Correlation Coefficient = 0.83

inflation to ease, it too is likely to remain IE770 © Copyright 2022 Ned Davis Research, Inc. Further distribution prohibited without prior

permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html.

above the Fed’s target by the end of 2023. For data vendor disclaimers refer to www.ndr.com/vendorinfo/

U.S. inflation usually leads the rest of the world The jury is still out as to whether we’re

Global ex U.S. CPI vs. U.S. CPI Monthly Data 1981-02-28 to 2023-04-30

Global ex U.S. CPI (Year-to-Year Change, Scaled Left)(2022-09-30 = 7.3%) entering a new high-inflation regime in the

21.0

U.S. CPI (Year-to-Year Change, Advanced Six Months, Scaled Right)(2023-04-30 = 7.7%)

21.0 long-term. Prior to pandemic, most devel-

20.0

19.0

20.0

19.0

oped economies were experiencing strong

18.0

17.0

18.0

17.0

disinflationary trends. Many of those

16.0 16.0 secular disinflationary factors, including

15.0 15.0

14.0 14.0 technology, demographics, and high private

13.0

12.0

13.0

12.0

debt and inequality, remain intact.

11.0 11.0

10.0 10.0

9.0 9.0 Other influences that were disinflationary

8.0 8.0

7.0 7.0 prior to the pandemic are at risk of disinte-

6.0

5.0

6.0

5.0

grating. Globalization is one factor. Remov-

4.0 4.0 ing Russia as an energy source to the West

3.0 3.0

2.0 2.0 is an obvious change. The rise of tariffs,

1.0 1.0

0.0 0.0 protectionist policies, and onshoring may

-1.0

-2.0

-1.0

-2.0

also contribute to long-term inflation. The

-3.0

Source: Bureau of Labor Statistics, Haver Analytics

-3.0 biggest risk, however, is inflation expec-

-4.0 -4.0

1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 tations becoming unanchored. If inflation

Full History

stays higher for longer, inflation expec-

1981-02-28 to 2022-09-30

Correlation Coefficient = 0.61

tations could turn permanently higher,

IE708 © Copyright 2022 Ned Davis Research, Inc. Further distribution prohibited without prior becoming a self-fulfilling prophecy.

permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html.

For data vendor disclaimers refer to www.ndr.com/vendorinfo/

PERIODICAL | ISSUE: #SP20221214 | NDR.COM Please see important disclosures at the end of this report. DECEMBER 14, 2022 12GLOBAL OUTLOOK EQUITIES

M A R K P H I L L I P S E U R O P E A N E Q U I T Y S T R AT E G I S T

DECEMBER 14, 2022 email us

European equities

A better year, but risks remain

Technical indicators positive

Key Takeaways MSCI Europe vs. Pattern Matched Composite

30

MSCI Europe

25

MSCI Europe Pattern Matched Composite

2022-12-09

• Bullish technical indicators suggest

20

risk appetite could continue into

the start of 2023. 15

10

• But the full impact of central

5

bank tightening on the European

0

economy and falling earnings could

result in choppy markets as 2023 -5

progresses. -10

-15

• Falling inflation and yields, and an

improvement in the outlook for -20

Pattern matched composite based on 10 closest matches

to path of MSCI Europe price index in last year

economic growth, could pave the -25 according to NDR's euclidian matching algorithm

based on over 50 years of price data.

way to a strong year end. -30 Shading shows maximum loss and gain.

-35

-40

Inflation and growth shocks Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep

Source: MSCI

Oct Nov Dec

2022 2023

As this year draws to a close, many PUB_CHARTS © Copyright 2022 NDR, Inc. Further distribution prohibited without prior permission.

All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html

investors will be happy to see the back For data vendor disclaimers refer to www.ndr.com/vendorinfo/

of 2022. It is fair to say that European

economic growth and inflation have been inflation stands at 10%. The MRO rate has An inflation shock, a sharp deterioration

worse than most economists predicted at been raised to 2% and the futures market is in the outlook for economic growth, and

the end of 2021. pricing another 75 bps in rate rises by the rapidly tightening monetary policy has

first quarter of 2023. Lagarde last month provided a confluence of factors driving

At the end of 2021 the average economist stated that the bank was still in “highly down asset prices across European

surveyed in the ECB’s Survey of accommodative territory”. equities and fixed income this year. The

Professional Forecasters was predicting MSCI Europe index fell 21% from January to

eurozone growth of 4.5% and inflation at Moreover, the ECB will continue to tighten September and is down 10% year-to-date.

1.9% for 2022. And ECB president Christine even as the eurozone has most likely In inflation-adjusted terms, these numbers

Lagarde stated that the bank was very entered a recession this quarter, as the are significantly worse at 27% and 17%.

unlikely to raise interest rates in 2022, Russian invasion of Ukraine has resulted in

keeping the main refinancing operations spiralling energy and food costs on top of

(MRO) rate at 0%. the inflationary pressures which followed

the lockdowns and unprecedented fiscal

Fast forward one year, and eurozone and monetary stimulus.

PERIODICAL | ISSUE: #SP20221214 | NDR.COM Please see important disclosures at the end of this report. DECEMBER 14, 2022 13U.S. FOCUS EQUITIES

14 | NED DAVIS RESEARCH

Early signs of hope Economic nadir in sight

MSCI Europe vs. OECD Europe CLI Momentum and Acceleration Daily Data 1969-12-31 to 2022-12-09

With leading economic indicators still MSCI Europe Price Index (EUR) (2022-12-09 = 2,654.55)

deteriorating and the ECB set to tighten into 2,512 2,512

the first quarter of next year, the macro- 1,585

1,000

1,585

1,000

economic regime remains challenging for 631

398

631

398

equities as we move into 2023. 251 251

158 158

100 100

63 Source: MSCI, OECD, Main Economic Indicators (MEI), www.oecd.org 63

But since September, European equities Q/Q Point Change in Q/Q Point Change in CLI(2022-11-30 = 0.51)

have staged a strong rally, triggering several OECD Europe Composite Leading Indicator (2022-11-30 = -2.39)

Q/Q Point Change in CLI (2022-11-30 = -0.58)

bullish technical signals. The chart on Page

14 illustrates that similar recoveries have 10 10

2 2

tended to be followed by a year of robust

0 0

equity returns. Confirmation of returning risk

-2 -2

appetite has also come from other sources,

-10 -10

such as cyclical industry relative strength,

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

small-cap relative strength, and falling risk

indicators. MSCI Europe (EUR)

MSCI Europe Next Period Returns

1969-12-31 to 2022-12-09

1969-12-31 to 2022-12-09

Arrows show buy signals. % Gain/ % of

Buy signal when CLI negative and falling, Europe CLI Annum Time Buy signal 3-Months 6-Months 12-Months

Further, economic data has been surprising but rate of fall is decelerating.

Statistics apply reporting lag.

Rising + Accelerating

Rising + Decelerating

15.40 29.73

0.45 21.90

Average 3.5 6.8 15.6

Percent Positive 72.0 79.2 75.0

to the upside as economists became Falling + Accelerating -0.94 31.34

* Falling + Decelerating 13.31 17.03

Average All Periods 1.9 3.9 8.2

too pessimistic as to the outlook for EUR_CLI2 © Copyright 2022 Ned Davis Research, Inc. Further distribution prohibited without prior

permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html.

the eurozone economy, and surveys of For data vendor disclaimers refer to www.ndr.com/vendorinfo/

Market ahead of itself? economic sentiment have improved from

Daily Data 2021-09-30 to 2023-09-28

Inflation, Interest Rates and Yields Around Recessionary Bear Market Bottoms record lows.

11 Eurozone Y/Y CPI % Change (LHS) (2022-11-30 = 10.02%) Recessionary Bear Market Average (RHS)

3.25

10

Average = mean around the 7 previous

9 recessionary bear market bottoms since 1970 3.00 Leading indicators also point to an

8 1975-01-02, 1981-09-28, 1992-08-25, 2001-09-21,

7

2009-03-09, 2011-09-22, and 2020-03-18. 2.75 economic outlook that while deteriorating,

6 2.50 is doing so at a slower pace, pointing to a

5 German CPI before 1991.

4 2.25 potential upturn in leading indicators early

MSCI Europe 2022 / Bear Market Low

3 Source: MSCI, Economist Magazine, Haver Analytics in 2023 (above), in line with a growing

ECB Main Refinancing Rate (LHS) (2022-12-09 = 2.00%) Recessionary Bear Market Average (RHS)

2.5

4.25 consensus that the eurozone economy will

2.0 4.00 experience a relatively short and shallow

1.5 3.75 recession and return to growth later in 2023.

German data before 1999.

1.0

3.50

0.5

3.25 Risks remain

0.0

Source: European Central Bank, www.ecb.int

5.1

On balance, we expect 2023 to be a choppy

2.5 10-Year German Bond Yield (LHS) (2022-12-09 = 1.93%) Recessionary Bear Market Average (RHS)

2.0

5.0

4.9

year, not least because the market may be

Long-term bond yield before 1990. 4.8

1.5 4.7 discounting too much good news too early.

4.6

1.0 4.5 In the past, inflation, interest rates and

4.4

0.5 4.3 yields have tended to fall before a sustained

4.2

0.0 4.1

4.0

recovery in equities has gotten underway

-0.5 Source: Bloomberg Finance L.P., International Monetary Fund, International Financial Statistics

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct

3.9

(left). And while there are some signs that

2022 2023

SP20221214B_C © Copyright 2022 NDR, Inc. Further distribution prohibited without prior permission.

All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html

yields and inflation have peaked, never

For data vendor disclaimers refer to www.ndr.com/vendorinfo/

has a European recessionary bear market

PERIODICAL | ISSUE: #SP20221214 | NDR.COM Please see important disclosures at the end of this report. DECEMBER 14, 2022 14U.S. FOCUS EQUITIES

15 | NED DAVIS RESEARCH

bottomed before the central bank has market in the second half of 2023. stocks since the sector became excessively

finished raising rates. oversold in May. European consumer

Sectors confidence has improved from record lows,

As Chief Economist Alejandra Grindal notes, Our broad market outlook also informs our and with disinflation likely in 2023 this could

Europe could easily see energy prices spike allocation to equity sectors. In line with provide a further tailwind.

again, posing risks to both the economy our broad market indicators, our sector

and inflation, pressuring the ECB to keep indicators point to a moderate tactical tilt A reopening of the Chinese economy during

monetary policy tight. toward Cyclical over Defensive sectors. 2023 could also provide a positive boost to

the sector which derives a high percentage

Secondly, analysis of past recessions shows However, given the intermediate term risks of sales from Asia and Asian tourism.

earnings on average fall around 20% per we would caution against becoming overly

annum for nearly two years (below). With aggressive in allocating to Cyclical sectors. Among the Defensive sectors, we prefer the

analysts forecasting 3% earnings growth for Therefore, a more nuanced approach will Consumer Staples and Health Care sectors,

the MSCI Europe index over the next year, make sense in 2023. due to a history of higher profitability

a potential fall in earnings is a major risk to and stronger returns on invested capital.

European equities. We still see value and positive underlying Conversely, we would underweight the

trends in the Energy and Materials sectors Communication Services sector, which has

Therefore, equities could be volatile until we with our commodity-based indicators seen a long-term decline in relative earnings

see clear evidence that interest rates have supportive. due to competition, regulation, and high

peaked, and that inflation and yields are capex requirements.

falling. Potentially this could occur later in We also see potential for further

the year and pave the way to a strong equity outperformance by Consumer Discretionary

Earnings risk

MSCI Europe Earnings Decline Around Recessions Monthly Data 1969-12-31 to 2023-11-30 (Log Scale)

Interested in

126 MSCI Europe Trailing 12-Month Earnings per Share (EUR) 126

100

EPS after 2022-11-30 based on forecast earnings.

Shading from September 2022 to March 2023 based on forecast.

100 customizing these

79 79

63

50

63

50

insights?

40 40

32 32

25 25

20

16

20

16

Learn more

13

10

Dark shading represents CEPR-defined recessions.

Light shading from March to December 2001 represents period

when both Germany and Italy were in recession.

13

10

about our

Custom Research

and eurozone real economic growth was near zero.

8 8

6 6

4

Source: MSCI

4

Solutions

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

MSCI Europe Earnings Declines Around Recessions

Recession Earnings Total Decline Annualized

Recession End Earnings Peak # Months

Start Trough (%) Decline (%)

1974-09-30 1975-03-31 1974-11-29 1976-04-30 17.0 -37.2 -28.0

1980-03-31 1982-09-30 1981-01-30 1982-01-29 12.0 -29.3 -29.4

1992-03-31 1993-09-30 1990-07-31 1993-05-31 34.0 -39.7 -16.4

2001-03-31 2001-12-31 2001-05-31 2003-05-30 24.0 -47.4 -27.5

2008-03-31 2009-06-30 2008-01-31 2009-12-31 23.0 -50.9 -31.0

2011-09-30 2013-03-31 2011-11-30 2013-12-31 25.0 -14.4 -7.2

2019-12-31 2020-06-30 2019-04-30 2021-04-30 24.0 -35.5 -19.7

www.ndr.com/custom-

Average 22.7 -36.4 -22.7

SP20221214C_C © Copyright 2022 NDR, Inc. Further distribution prohibited without prior permission.

All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html

research-solutions

For data vendor disclaimers refer to www.ndr.com/vendorinfo/

PERIODICAL | ISSUE: #SP20221214 | NDR.COM Please see important disclosures at the end of this report. DECEMBER 14, 2022 15SPECIAL REPORT GLOBAL OUTLOOK

NDR HOUSE VIEWS (Updated December 9 , 2022)

For global asset allocation, NDR recommends an overweight Economic Summary December 12, 2022

allocation to stocks, marketweight allocation to bonds, and an

Near term activity: Accelerating Neutral Decelerating

underweight allocation to cash. Our overweight equity

allocation is in response to improving model readings and a

shift in Fed rate hike expectations.

Global Economy U.S. Economy U.S. Inflation

(2.9%) (1.5%-2.0%) (4.0%-4.5%)

Economic gauges reflect changes in near-term economic activity. Numbers in parenthesis

Equity Allocation refer to NDR 2022 forecasts.

U.S. | We are neutral on stocks on an absolute basis and

Global Asset Allocation

relative to bonds and cash. Macro and earnings concerns are Overweight Marketweight Underweight

offset by extreme pessimism and technical improvements. We Stocks (65%)

favor small-caps over large-caps and Value over Growth. Bonds (35%)

Cash (0%)

INTERNATIONAL | We are overweight Europe ex. U.K. and Benchmark: Stocks (55%), Bonds (35%), Cash (10%)

marketweight on all other regions.

Equities — Regional Relative Allocation

Europe ex. U.K. (14%)

U.S. (61%) | Emerging Markets (11%) | Japan (5%) | U.K. (4%) |

Macro Pacific ex. Japan (2%) | Canada (3%)

ECONOMY | The global economy is in a sustained slowdown

Benchmark – U.S. (61.5%), Europe ex. U.K. (12%), Emerging Markets (11.2%), Japan (5.4%),

due to waning monetary and fiscal support, stubbornly high U.K. (3.8%), Pacific ex. Japan (3%), Canada (3.1%)

inflation, and rising geopolitical risk. While the slowdown

Global Bond Allocation

remains moderate, the risk of severe recession increases in

Europe (28%)

2023. Global inflation pressures are easing but will remain U.S. (55%) | Japan (14%)

historically elevated in the foreseeable future. U.K. (3%)

Benchmark: U.S. (55%), Europe (26%), Japan (14%), U.K. (5%)

FIXED INCOME | We raised our bond exposure to 100% of

U.S. Allocation

benchmark duration and are neutral on the yield curve. We Small-Cap | Value

are overweight Treasurys and MBS and underweight high Stocks (55%) | Bonds (35%) | Cash (10%) | Mid-Cap

yield, ABS and TIPS. We are marketweight everything else. Large-Cap | Growth

Benchmark: Stocks (55%), Bonds (35%), Cash (10%)

GOLD | We are currently bullish. The majority of our Gold Sectors

Health Care (17%) | Energy (5%) | Materials (4%)

Watch report indicators are now bullish and gold stands to

Consumer Discretionary (8%)

benefit from seasonality and declining bond yields. Benchmark: Technology (27.4%), Health Care (13.8%), Financials (10.7%), Communication

Services (9.3%), Consumer Discretionary (12.1%), Consumer Staples (7.0%), Industrials

(7.9%), Energy (4.0%), Utilities (2.7%), Real Estate (2.7%), Materials (2.5%)

DOLLAR | We are bearish due to worsening momentum and

model readings. U.S. Bonds — 100% of Benchmark Duration

PERIODICAL | ISSUE: #SP20221214 | NDR.COM Please see important disclosures at the end of this report. DECEMBER 14, 2022 16You can also read