Investor Presentation - Winter 2023 - Freehold Royalties Ltd

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Investor

Presentation

Winter 2023

freeholdroyalties.com TSX FRU Quality Assets • Sustainable Dividends

Investment Highlights

A North American energy royalty company

7.2% dividend yield Torque to commodity

current dividend coverage to $40 WTI direct returns to shareholders without

cost inflation

ESG friendly investment High margin asset class

rated top 1% among global oil producers >95% operating margin

Diversified assets Financial strength

ownership in the top North American low debt levels & strong free cash flow

basins

Winter 2023 | 2

Dividend yield based on $15.00 share price and $0.09/share monthly dividend rate. ESG rating based on Sustainalytics 2022 ESG

ranking. Operating margin reflects Q3-2022 realized price minus operating costs, ad valorem costs and interest expense.

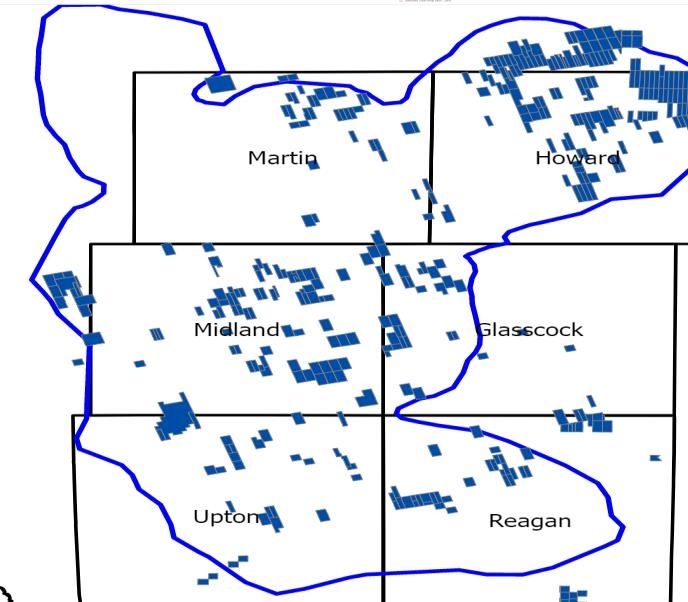

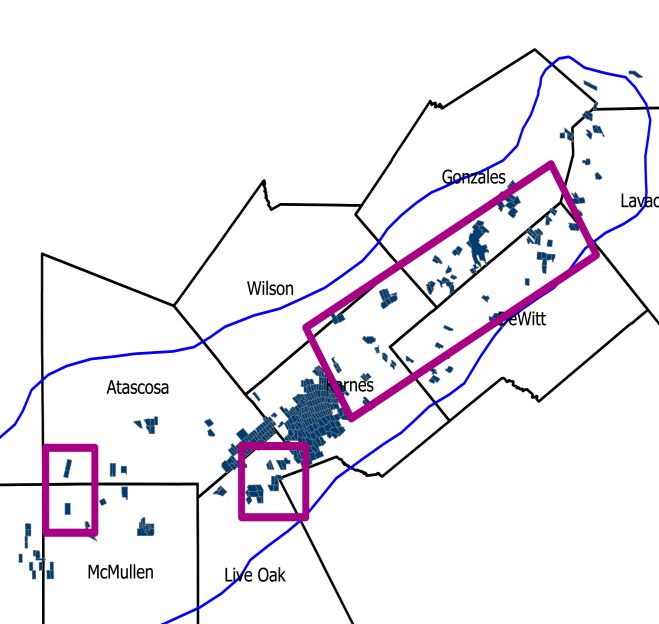

US Royalty Expansion

Adding core positions in the Permian and Eagle Ford

▪ In Q3-2022, Freehold closed transactions, adding Howard

County Eagle Ford

core positions in the Midland Permian (Howard Midland

County) and Eagle Ford for CAD$159 million Purchase price (CAD$, mm, net of estimated closing

$126 $33

adjustments)

Net Royalty Acres 4,400 2,500

▪ Transaction highlights include:

– $38 million in 2023 forecast funds from operations 2023E production (boe/d) 750 250

– Forecast average 1,000 boe/d in 2023 production 2023E funds from operations (CAD$, mm, futures

$27 $6

pricing)1

– 6,900 net royalty acres (Permian, Eagle Ford focused,

>90% mineral rights)

FRU Land

Howard County Acquisition

▪ All transactions funded through the utilization of Eagle Ford Acquisition

Freehold’s credit facility and funds from operations Basin Outlines

– Freehold continues to maintain financial flexibility with an

estimated >$100 million in undrawn credit at YE 2022

– Inclusive of the transactions, exited Q3-2022 at ~0.5x net

debt to trailing funds from operations

6 mi

1Assumes a 2023 average West Texas Intermediate price of US$74/barrel of oil and a NYMEX natural gas price of US$5.75/Mcf and an exchange rate of US$0.75 for every CDN$1.00.

Winter 2023 | 3

C$ unless otherwise noted

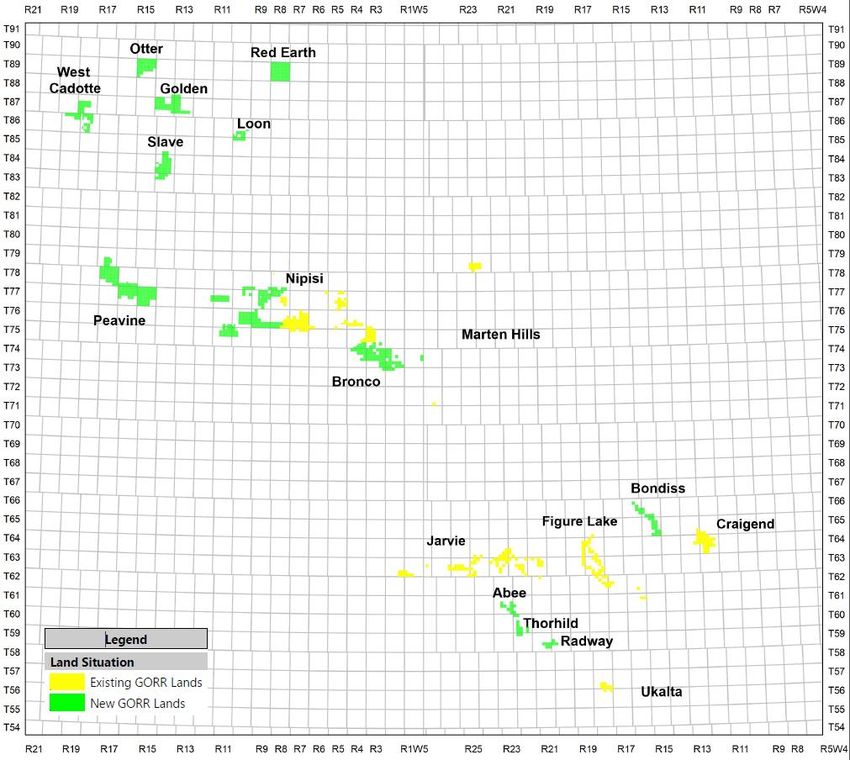

Canadian Royalty Expansion

Expanding Clearwater Land Base

▪ Freehold closed a royalty transaction prospective for

Clearwater oil

▪ Transaction adds over 300,000 gross acres to

Clearwater transaction

Freehold’s Clearwater land position, tripling Freehold’s adds acreage in the

current land position northwest section of the

▪ Expands Freehold’s acreage into new production and Play

exploration areas of the play

▪ $18.4 million transaction includes a drilling

commitment with a strategic partner with a track

record of development success

▪ We expect the development of the Clearwater to be a

key driver of Canadian organic growth for Freehold as

we enter 2023

Clearwater Production Profile

Production (boe/d)

340

300

260

220

180

140

100

Mar-21

Mar-22

Oct-21

Oct-22

Nov-21

Dec-21

Jan-21

Apr-21

Jun-21

Jul-21

Sep-21

Jan-22

Apr-22

Jun-22

Jul-22

Sep-22

Feb-21

May-21

Aug-21

Feb-22

May-22

Aug-22

Winter 2023 | 4

Source: Company Reports

Inflation Hedge

Performance Through All Commodity Cycles

▪ Freehold is not exposed to capital or operating costs

▪ Significant margin advantage relative to E&P producers

▪ Operating and capital cost inflation (15%-30% increase YoY) have no influence on Freehold’s cash

flow profile

▪ In an inflationary environment Freehold’s operating margin will stay flat and not compress as

an E&P’s would

Price Performance 2023 Consensus Capex Change Q1-Q3/22

110 50%

Consensus Capex Increase

100

Relative Performance

40%

90

30%

80

20%

70

10%

60

50 0%

Jun Jul Aug Sep Oct Nov Dec Jan E&P E&P E&P E&P E&P E&P E&P E&P E&P E&P

Peer Peer Peer Peer Peer Peer Peer Peer Peer Peer

Freehold WTI Canadian Energy Index

1 2 3 4 5 6 7 8 9 10

Winter 2023 | 5

Source | Company Reports, FactSet, National Bank Financial; Peer group includes PEY, TVE, PIPE, VET, POU, KEL, SDE, CPG, ARX, SGYBalanced Portfolio

Commodity Portfolio Clearwater

Deep

Basin Mannville

~20% of

65%

Cardium

Revenue Conv Viking

Production Gas

SE

Sask

Production

60%

Volumes Revenue

38%

Natural

Gas 62% 35%

Oil &

NGL’s Production

40%

~80% of Revenue

Revenue

Permian

Eagle

Proforma 2022 Proforma 2022 Ford

Acquisitions Acquisitions Note | Circles represent share of YTD revenue,

including impact of 2022 acquisitions

Winter 2023 | 6

Source | Company Reports, Proforma 2022 forecasts assumes midpoint of FRU 2022E production guidance, US$94/bbl WTI, US$19/bbl

heavy oil differentials, US$2/bbl light oil differentials, US$6/mcf NYMEX, $5/mcf AECO.Diversity Amongst Payors

Diversified Group of Well Capitalized Producers

▪ North American royalty portfolio provides exposure to a broad group of oil and gas plays across North

America

▪ No payor represents > 15% of 12-months trailing revenue

▪ Top 10 payors represent ~ 50% of 12-month trailing revenue

Winter 2023 | 7

Source: Company ReportsBetter Pricing, Growth, Opportunity

Upstream capital drives growth Oil production growth driven by Texas

$166 9 +2.4 million bbls/d

6x investment in the US

Oil Prod (MMbbl/d)

Permian &

8 Eagle Ford

$121

US$ billions

$110 7

$88 6 6x growth

5

4 +0.4 million bbls/d

$21 $17 $22 $23

3 Oil Sands &

2 Conventional

2019 2020 2021 2022 2014 2016 2018 2020 2022E 2024E 2026E

Significantly larger M&A opportunity set Better oil and gas pricing on US assets

31

$2bn Since 2019 Nymex Natural Gas Benchmark $11/mcf

Realized Price $9/mcf

Realized Price $5/mcf

+97% on gas

$10 406 WTI Crude Oil Benchmark $119/bbl

billion deals

Realized Price $121/bbl

Realized Price $105/bbl

5x investment 13x transactions +15% on oil

Winter 2023 | 8

Source | Company Reports, Peters & Co, IHS, Canadian Association of Petroleum Producers, EIA, Enverus. Canadian

capital Spending includes oil sands spending, realized price based on Q3-2022 results released November 8th.Bigger & Better Freehold

>$500mm of US assets added over 2 years Significant FFO growth, solid balance sheet

16,000 $350

50% growth

14,000

Corporate Production (boe/d)

since Q2-2020 $300

US

12,000

$250

10,000

Funds From Operations

Canada

$ millions

8,000 $200

6,000

$150

4,000

$100

2,000

Net Debt

0 $50

2020 Q1

2020 Q2

2020 Q3

2020 Q4

2021 Q1

2021 Q2

2021 Q3

2021 Q4

2022 Q1

2022 Q2

2022 Q3

$0

2019 2020 2021 2022E

Winter 2023 | 9

Source | Company Reports, 2022E forecasts based on the midpoint of 2022E guidance released November 8, 2022 assumes midpoint of FRU

2022E production guidance, US$94/bbl WTI, US$19/bbl heavy oil differentials, US$2/bbl light oil differentials, US$6/mcf NYMEX, $5/mcf AECOFreehold Return Profile

60% Payout Ratio

Return of ▪ Dividend of $0.09/share announced at Q3-2022 is

Capital to the highest level since 2015

Shareholders ▪ Current dividend reflects ~60% payout at US

$75/bbl WTI for 2023

2022E

Funds from Less than 1.0x Funds From Operations

Operations Balance Sheet ▪ Q3-2022 net debt to funds from operations 0.5x

Strength ▪ 2022E YE undrawn credit capacity estimated to be

$300-$320 greater than $100 million

million

Disciplined, Strategic Investment

▪ ~$375 million in acquisitions in 2021

Portfolio ▪ ~$180 million in acquisitions in 2022

Growth ▪ Freehold continues to evaluate and execute on

attractive acquisition opportunities that provide long

term shareholder value

Winter 2023 | 10

For illustrative purposes and should not be relied on as indicative of future results, 2022E forecasts based on midpoint of FRU 2022E

production guidance, US$94/bbl WTI, US$19/bbl heavy oil differentials, US$2/bbl light oil differentials, US$6/mcf NYMEX, $5/mcf AECOBalanced Returns

FRU has maintained a balance between dividend growth, portfolio growth, debt reduction

20

Dividend Change

18

Deal Announcement

16

Share Price ($/share)

14

12

10

8 Dividend increased 6 times from $0.015 to $0.09/share over last 8

6 quarters

4 Current dividend yield 7.2%

2 Executed greater than $550 million in transactions since 2021

maintaining balance sheet strength

0

Aug-21

Aug-22

May-21

May-22

Nov-21

Dec-21

Nov-22

Dec-22

Jan-21

Jan-22

Mar-21

Jun-21

Mar-22

Jun-22

Oct-21

Oct-22

Feb-21

Apr-21

Jul-21

Sep-21

Feb-22

Apr-22

Jul-22

Sep-22

Winter 2023 |11

Source | FactsetSustainable Through All Commodity Cycles

120

West Texas intermediate (US$/bbl)

100

Business planning on a long term WTI price of US$75/bbl

80

60

40

Current dividend payable down to ~US$40/bbl WTI

20

0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

WTI Crude Oil (US$/bbl) Futures Pricing

Winter 2023 |12

Source | FactsetLong History of Returns

Matching growth in dividend to growth in production and cash flow

Dividend ($/share)

$3

$2

▪ From an Initial Public Offering of

$10/share in 1996, Freehold has paid $1

out $1.9 billion in dividends to its

shareholders (~$34/share) $0

2023E

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

▪ Q3-2022 payout 47%, below the

outlined target of 60% Dividend per Share

– Increased monthly payout from $0.08 to Cumulative Revenue, FFO, & Dividends Since IPO

$0.09/share as part of Q2-2022 results $3.5

$3.0

– Sixth dividend increase over the last nine

quarters $2.5

$ billions

$2.0

▪ Providing a sustainable dividend $1.5

remains a top priority in terms of $1.0

returns for our shareholders $0.5

$0.0

Revenue Funds from Operations Dividends

Winter 2023 |13

*2023E denotes current monthly dividend annualizedWhy Own Freehold

Strong Balance Quality Long

High Margins Sustainable Sheet, Low Risk Duration Assets,

Business Multi-year Upside

▪ High operating margin ▪ Increased dividend as ▪ Q3-2022 net debt to ▪ Positioned in the top tier

provides Freehold the part of Q2-2022 results trailing funds from oil plays – Eagle Ford,

ability to pay a in tandem with the operations 0.5x Permian, Clearwater,

meaningful dividend completion of a number Viking, and Bakken

▪ In the absence of

across all commodity of accretive acquisitions

acquisitions and further ▪ Diverse operator list

cycles

▪ 2021 payout 33% dividend increases, reduces exposure risks

▪ Transformed Freehold to a expect to have >$100

▪ 2022E payout ~45% ▪ Royalty payors represent

pure play royalty company million in undrawn credit

strong suite of

with a diversified asset ▪ 2023E payout ~60% at at YE 2022

investment grade

base, deriving ~60% of US$75/bbl WTI

companies and private

revenue from Canada and

▪ ~7.2% dividend yield entities focused on

40% from the US

growth

Winter 2023 | 14

US$94/bbl WTI, US$19/bbl heavy oil differentials, US$2/bbl light oil differentials, US$5/mcf NYMEX, C$5/mcf AECO. 2022 forecasts assume midpoint of FRU 2022 production guidance. Dividend yield

assumes $15.00/share and $0.09/share monthly dividend. Payout is a Non-GAAP ratio or other specified financial measures. See “Non-GAAP Ratios and Other Financial Measures” in the Advisories.Investor Relations

tf. 888.257.1873

t. 403.221.0833

w. freeholdroyalties.com

freeholdroyalties.com TSX FRU Quality Assets • Sustainable Dividends2022 Third Quarter Results

Q3/2022 Q3/2021 Change

Production boe/d 14,219 11,265 26%

Funds from operations mm $80.8 $48.2 68%

Period end net debt mm $159.9 $75.3 112%

Netback per boe $69.77 $46.60 50%

Payout ratio % 47% 35% 34%

Cash costs per boe $3.62 $2.49 45%

▪ 14,219 boe/d Q3-2022 production average represents a record quarter for Freehold

▪ Volumes up 26% y/y, 6% q/q

▪ 304 gross (6.7 net) wells drilled on our royalty lands

▪ >760 gross wells drilled F9-2022

▪ Prospects targeting oil in the Viking, SE Saskatchewan, Clearwater, Permian, and Eagle Ford in addition to gas focused

drilling in Spirit River

▪ Q3-2022 payout of 47%, up from 34% during the same period last year

▪ Freehold increased its dividend 13% during the quarter, the sixth increase over the last nine quarters

▪ Period end net debt of $160 million while completing $162 million in acquisitions over the quarter

▪ Acquisitions added to Freehold’s royalty position in the Permian, Eagle Ford and Clearwater

Winter 2023 |16

Netback, cash costs, payout ratio are Non-GAAP ratios or other specified financial measures.

See “Non-GAAP Ratios and Other Financial Measures” in the advisories, C$ unless otherwise notedYTD Royalty Drilling Results

Top Canadian Drillers

Gross Wells Net Wells

Q3-2022 represented

one of Freehold’s top Teine Energy 57 5.1

quarters for activity Tamarack Valley 31 1.0

Permian Haynesville

>30 rigs running on

Freehold’s North Whitecap Resources 26 0.8

American assets Bonterra Energy 24 0.6

Crescent Point Energy 20 0.6

Clearwater Eagle Ford Total Canadian Wells 366 13.9

Top US Drillers

Deep Basin Gross Wells Net Wells

Pioneer Resources 57 0.1

Marathon Oil 50 1.0

Viking Crownquest Operating

Spirit River 30 0.1

Co.

ConocoPhillips 24 0.1

SK Bakken Total US Wells 398 2.0

Canadian Wells 366 13.9

US Wells 398 2.0

Total Wells 764 15.9

Winter 2023 | 19The Royalty Advantage

Freehold provides a lower risk/return proposition than traditional E&P’s

Environmental, Social,

Financial Strength, Low Risk Diversified Royalty Portfolio

Governance

▪ Strong operating margins, enable ▪ Diversified North American ▪ Our approach to ESG is rooted in

lower breakeven commodity portfolio with exposure to our collective desire to provide a

prices, enhancing the Permian, Eagle Ford, Viking, long-term value proposition to

sustainability of payout Clearwater, Bakken, Mississippian, our shareholders

▪ Q3-2022 corporate netback of and Cardium oil plays plus natural ▪ Royalties offer no exposure to

~$70/boe gas plays targeting the Spirit environmental pressures

▪ Ability to grow the dividend, and River, Montney and Haynesville ▪ Expect to update our ESG

generate meaningful free funds via well funded producers strategy through a sustainability

flow at in the current commodity ▪ 6.4 million royalty acres in report in late 2022

price environment Canada, 0.9 million gross drilling ▪ Freehold has strong leadership,

▪ Financial flexibility with net debt units in the U.S. an engaged and idea rich

to funds from operationsRoyalties vs. Exploration and Production Companies

Royalties provide lower costs and higher returns to shareholders

A Working Interest Barrel A Royalty Interest Barrel

Operating netback Operating netback

~ 60% of gross revenue ~ 100% of gross revenue

▪ The royalty model maintains a

material netback advantage

over traditional E&P’s

100%

▪ Able to generate free funds flow 15 %

Royalties Paid 80%

at lower commodity prices

25 %

60%

▪ Q3-2022 corporate netback Operating Costs

Operating

~$70/boe

Netback 40%

▪ Freehold maintains a >95%

operating margin enabling more

60%

Operating Netback

100% 20%

(60% of gross revenue) of gross revenue

return to shareholders

0%

Winter 2023 | 19

Payout ratio and netback are Non-GAAP ratios or other specified financial measures. Operating margin reflects Q3-2022 realized price minus operating costs, ad valorem costs and interest expense. See "Non-GAAP Ratios and

Other Financial Measures" in the Advisories.Safe, Lower Risk Asset Base

2019 2020 2021 F9-2022

Production (boe/d) 10,628 9,781 11,844 13,784

Acquisitions (millions) $49 $7 $377 $184

Royalty acres (millions) 6.7 6.3 6.2 6.4

U.S. gross drilling unit acres (millions) - - 0.8 0.9

Tax pools (millions) $838 $775 $1,001 -

Net debt/funds from operations 0.8x 0.9x 0.5x 0.5x

Winter 2023 | 20Strong Balance Sheet

▪ Freehold exited Q3-2022 with 5.0x

Net Debt to Funds from Operations

net debt to trailing funds from 4.5x

operations of 0.5x 4.0x

3.5x

▪ At current commodity price

levels and dividend level, 3.0x

Freehold has capacity to pay 2.5x

down debt or pursue 2.0x

acquisitions with free funds 1.5x

▪ Freehold extended its credit 1.0x

facility with an unchanged 0.5x

committed revolving 3-year 0.0x

facility at $285 million and $15

2022E

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

million operating facility

Sector Average Freehold

Winter 2023 | 21

Sector average sourced from Research estimates

Sector average reflects Canadian upstream producersIndustry Drilling vs. Freehold

▪ We have seen a strong upward momentum in 20,000 25

activity on Freehold’s royalty land along with

18,000

Gross Wells Western Canada

the broader Western Canadian Sedimentary

portfolio 16,000 20

Freehold net Wells

14,000

▪ Approximately 6% of all spending in Western

Canada has occurred on Freehold lands over 12,000 15

the past five years 10,000

8,000 10

▪ Approximately 2% of all lower 48 spending

occurred on Freehold land over the past five 6,000

years

4,000 5

▪ Freehold’s royalty portfolio has materially 2,000

outperformed the broader Western Canadian 0 0

Sedimentary Basin

2022E

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

▪ Growth in net wells reflects the quality of

Freehold’s underlying royalty portfolio Western Canadian Drilling Freehold Net Drilling

Winter 2023 | 22

Source: Canadian Association of Energy Contractors

Forecast based on Petroleum Services Association of Canada, and Freehold Q3-2022 results.Cash Costs

Freehold has shown a strong trending down in cash costs

$7.00

▪ Q3-2022 cash costs of

$6.00

$3.62/boe facilitate a

strong corporate netback

$5.00

for Freehold

Cash Costs ($/boe)

$4.00

▪ Freehold’s operating

margin >90% $3.00

▪ Changes in costs reflect $2.00

disposition of working

interest and higher $1.00

production volumes

relative to G&A and $0.00

interest charge increases Q1-20 Q2-20 Q3-20 Q4-20 Q1-21 Q2-21 Q3-21 Q4-21 Q1-22 Q2-22 Q3-22

Operating Costs ($/boe) Interest Expense ($/boe) General & Administrative ($/boe)

Winter 2023 | 23

Cash costs are equal to operating costs + interest expense + G&A costs (see non-GAAP Financial Measures)

Payout ratio and netback are Non-GAAP ratios or other specified financial measures. See "Non-GAAP Ratios and Other Financial Measures" in the Advisories.Royalty Production History

16,000

14,219 14,250

14,005 13,676

14,000 13,453

Royalty Production (boe/d)

12,000 11,137 11,265

10,618 10,946

10,139 10,311 10,149 10,315

10,000 9,605

9,150 9,096

8,000

6,000

4,000

2,000

0

2022E

Q1-19

Q2-19

Q3-19

Q4-19

Q1-20

Q2-20

Q3-20

Q4-20

Q1-21

Q2-21

Q3-21

Q4-21

Q1-22

Q2-22

Q3-22

Winter 2023 | 24

*Assumes the midpoint of 2022E production guidance.Disciplined Acquirer

Freehold will continue to look for opportunities that enhance the resiliency

and durability of our portfolio across all commodity price cycles

Cost Initial Production

Year Area ($ millions) Acquired (boe/d)

2012 AB, SK and BC 60 600

2013 Numerous small acquisitions 10 30

2014 SK/MB/AB 248 1,500

2015 SK/AB/BC 410 2,100

2016 SK/AB 162 1,700

2017 SK/AB 87 420

2018 SK/AB 62 275

2019 SK/AB, US 50 410

2020 US 8 -

2021 US 377 4,400

2022 US/Canada 183 1,400

TOTAL $1,657 12,835

Winter 2023 | 252022E Guidance

Guidance August 9

2022E Annual Average

2022

Average production boe/d 13,750-14,750

Funds from operations million $300-$320

West Texas Intermediate crude oil US$/bbl $97.00

Edmonton Light Sweet crude oil Cdn$/bbl $120.00

AECO natural gas Cdn$/mcf $5.00

NYMEX natural gas US$/mmbtu $5.00

Exchange rate US$/Cdn$ 0.79

Winter 2023 | | 26

Source: Company Reports.Advisories

Forward-Looking Statements

This presentation offers our assessment of Freehold’s future plans and operations as at January 8, 2022 and contains forward-looking information including, without limitation, future dividends per share; the expectation that operating and

capital cost inflation will not influence Freehold’s cash flow profile; the expectation that DUCs will contribute to H2 2022 production and that permits will contribute to H2 2022 and H1 2023 production; the expectation that an inventory of

permits and DUCs will drive near term production additions; estimated Q3 and Q4 2022 corporate production; expectation of US$94-$97/bbl WTI, US$13-19/bbl heavy oil differentials, US$2-3/bbl light oil differentials, US$5-6/mcf NYMEX,

$5/mcf AECO; forecasts of strong growth within Freehold’s US portfolio through H2 2022; forecasted debt to trailing funds from operations ratio at year end; the expectation that Q4 2022 US production will represent approximately 35% of

corporate production and 40% of revenue; estimated 2023 funds from operations; expectation oil production in the US will continue to rise; Freehold's expectation to continue to assess optimal allocation of free funds between shareholder

returns and portfolio growth, and expectation of continuing to execute on attractive opportunities that provide long term shareholder value; the expectation that strong free funds flow continues to provide option value to return capital to

shareholders through continued evaluation of our monthly base dividend; expected year end 2022 net debt to funds from operations ratio; forecast payout for 2022; estimated 2022 guidance; that Freehold will balance portfolio investment

and dividend growth through the remainder of 2022; anticipated cumulative dividends per share in 2022 and 2023; expectation that we will continue to have a diverse set of royalty payors; the expectation we will release a sustainability

report in late 2022; expectation Freehold can maintain a >90-95% operating margin and estimated 2022 royalty production.

This forward-looking information is provided to allow readers to better understand our business and prospects and may not be suitable for other purposes. By its nature, forward-looking information is subject to numerous risks and

uncertainties, some of which are beyond our control, including: volatility in market prices for crude oil, NGL and natural gas; the impacts of the Russian-Ukraine war and associated sanctions on the global economy and commodity prices;

geopolitical instability, political instability; the continuing impact of the COVID-19 pandemic on demand and commodity prices; future capital expenditure by Freehold; future capital expenditure levels by other royalty payor; future production

levels; future exchange rates; future tax rates; future legislation; the cost of developing and expanding our assets; the impacts of inflation and supply chain shortages on the operations of our industry partners and royalty payors; our ability

and the ability of our industry partners and royalty payors to obtain equipment in a timely manner to carry out development activities; our ability to market our product successfully to current and new customers; our expectation for the

consumption of crude oil, NGLs and natural gas; our expectation for industry drilling levels on our royalty lands; the impact of competition; our ability to obtain financing on acceptable terms; our ability to add production and reserves through

our development and acquisitions activities; lack of pipeline capacity; currency fluctuations; changes in income tax laws or changes in tax laws, regulations, royalties, or incentive programs relating to the oil and gas industry; reliance on

royalty payors to drill and produce on our lands and their ability to pay their obligations; uncertainties or imprecision associated with estimating oil and gas reserves; stock market volatility; our ability to access sufficient capital from internal

and external sources; a significant or prolonged downturn in general economic conditions or industry activity; incorrect assessments of the value of acquisitions; competition for, among other things, capital, acquisitions of reserves,

undeveloped lands and skilled personnel; geological, technical, drilling, and processing problems; unanticipated litigation; and environmental risks and liabilities inherent in oil and gas operations. Risks are described in more detail in Freehold’s

annual information form for the year ended December 31, 2021 which is available under Freehold’s profile on SEDAR at www.sedar.com.

You are cautioned that the assumptions used in the preparation of such information, although considered reasonable at the time of preparation, may prove to be imprecise and, as such, undue reliance should not be placed on forward looking

information. We can give no assurance that any of the events anticipated will transpire or occur, or if any of them do, what benefits we will derive from them. The forward-looking information contained herein is expressly qualified by this

cautionary statement. To the extent any guidance or forward-looking statements herein constitute a financial outlook, they are included herein to provide readers with an understanding of management's plans and assumptions for budgeting

purposes and readers are cautioned that the information may not be appropriate for other purposes. Our policy for updating forward-looking statements is to update our key operating assumptions quarterly and, except as required by law, we

do not undertake to update any other forward-looking statements.

You are further cautioned that the preparation of financial statements in accordance with International Financial Reporting Standards requires management to make certain judgments and estimates that affect the reported amounts of assets,

liabilities, revenues, and expenses. These estimates may change, having either a positive or negative effect on net income, as further information becomes available and as the economic environment changes.

Winter 2023 |27Advisories continued

Production

All production disclosed herein is considered net production for the purposes of National Instrument 51-101 – Standards of Disclosure for Oil and Gas Activities, which includes Freehold's working interest (operating and non-operating) share after

deduction of royalty obligations, plus our royalty interests. Since Freehold has minimal working interest production, net production is substantially equivalent to Freehold's royalty interest production. In the second quarter of 2022, Freehold's net

production of 13,453 boe/d consisted of 5,378 bbls/d of light oil, 1,239 bbls/d of heavy oil, 1,613 bbls/d of natural gas liquids and 31,336 mcf/d of natural gas. For the full year of 2021, Freehold's net production of 11,884 boe/d consisted of

4,342 bbls/d of light oil, 1,184 bbls/d of heavy oil, 1,217 bbls/d of natural gas liquids and 30,608 mcf/d of natural gas.

Conversion of Natural Gas to Barrels of Oil Equivalent (BOE)

The 6:1 boe ratio is based on an energy equivalency conversion method primarily applicable at the burner tip. It does not represent a value equivalency and is not based on either energy content or current prices. While the boe ratio is useful for

comparative measures, it does not accurately reflect individual product values and might be misleading, particularly if used insolation. As well, given the value ratio, based on the current price of crude oil to natural gas, is significantly different

from the 6:1 energy equivalency ratio, using a 6:1 conversion ratio may be misleading as an indication of value.

Winter 2023 |28Advisories continued

Non-GAAP Financial Measures

Within this presentation, references are made to terms commonly used as key performance indicators in the oil and gas industry. We believe that netback, payout ratio and cash costs are useful supplemental measures for management and

investors to analyze operating performance, financial leverage, and liquidity, and we use these terms to facilitate the understanding and comparability of our results of operations and financial position. However, these terms do not have any

standardized meanings prescribed by generally accepted accounting principles ("GAAP") and therefore may not be comparable with the calculations of similar measures for other entities.

Netback, which is calculated on a boe basis as average realized price less production and ad valoreum taxes, operating expenses, general and administrative and cash interest charges, represents the per unit cash flow amount allowing the

Company to benchmark how changes in commodity pricing, net of production and ad valoreum taxes, and our cash-based cost structure compare against prior periods.

Payout ratios are often used for dividend paying companies in the oil and gas industry to identify dividend levels in relation to funds from operations that are also used to finance debt repayments and/or acquisition opportunities. Payout ratio

is calculated as dividends paid as a percentage of funds from operations.

Cash costs, which is also calculated on a boe basis, is comprised of recurring cash based costs, excluding taxes, reported on the statements of operations. For Freehold, cash costs are identified as operating expense, general and

administrative expense and cash-based interest and financing charges and share-based pay outs. Cash costs allow Freehold to benchmark how changes in its manageable cash-based cost structure compare against prior periods.

For further information related to these non-GAAP terms, including details of how these ratios are calculated, see our most recent management's discussion and analysis, which is available on SEDAR at www.sedar.com and is incorporated

herein.

This presentation also contains the capital management measures of working capital, net debt, capitalization and net debt to funds from operations as defined in Note 11 to the condensed consolidated financial statements as at and for the

three months ended June 30, 2022.

Winter 2023 |29Investor Relations

tf. 888.257.1873

t. 403.221.0833

w. freeholdroyalties.com

freeholdroyalties.com TSX FRU Quality Assets • Sustainable DividendsYou can also read