William Blair SICAV Class J (H JPY) - ISIN: LU1802297363

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

William Blair SICAV

Dynamic Diversified Allocation Fund

Class J (H JPY)

Quarterly Review

Q1 2022

Brian D. Singer, CFA, Partner

Thomas Clarke, Partner

ISIN: LU1802297363

FOR PROFESSIONAL INVESTORS ONLYSummary & Outlook Q1 2022

• Russia’s invasion of Ukraine and the Western financial came from long exposures to Russia and Vietnam equities and to

and economic sanctions that followed shocked equity U.S. Treasuries. Within currencies, long exposures to Brazilian real,

prices lower, although equities outside of Russia Colombian peso, and Chilean peso helped performance, while long

regained some of these losses by the end of the quarter. exposure to the Russian ruble, Swedish krona, and short exposure

The sanctions on Russia were sufficiently potent to to the Australian dollar detracted. Negative security selection was

render almost all Russian assets—and the ruble— mostly due to underperformance of the International Leaders and

untradeable in March. Emerging Markets Growth strategies.

• Before Russia’s unprovoked war, expectations for

inflation in most of the world (excluding most of Asia)

had continued to rise, and the view that inflation would

Strategy Positioning

prove transient (expressed a year ago by central banks)

looked increasingly misplaced. The market segment remains long of equities with net exposure of

• In the near term, inflation rates are therefore apt to push +35%. The segment’s largest country exposures are in U.S. and U.K.

still higher in most countries compared with prewar equities. Markets are modestly long of fixed income with a net

anticipation. The medium-term impact on global growth, exposure of +25%, with primary long exposure in U.S. Treasuries

however, is ultimately more likely to be contractionary, and emerging debt.

with implications that after inflation peaks, there may be

a greater subsequent downward impulse. Within currencies, the largest long exposures are the Brazilian real,

• Although global contagion and generalized “risk off” Japanese yen, and Singapore dollar while the largest short

behavior in other markets and currencies has been quite exposures are to the New Zealand dollar, Canadian dollar, and euro.

limited, there are some clear knock-on effects of Russia’s

entry into war with its neighbor, to which we have

responded in strategy changes.

Strategy Review and Outlook

Global equities finished the quarter down after strong performance

in 2021. In January, continuing unexpected rises in reported

Performance Summary

inflation around the world fueled worries that monetary policies

Dynamic Diversified Allocation completed the quarter with negative would result in more rapid removal of the extraordinarily

performance—both the market segment and security selection expansionary conditions that have characterized developed markets

component were negative while the currency segment was positive. for most of the past decade, and would continue to usher in rate

Within markets, long exposures to Brazil, Chile, U.K., and global hikes in emerging markets, where tightening has been the order of

energy sector equities contributed. Negative contributions primarily the day for most of the last year. This development also led to risesSummary & Outlook Q1 2022

in government bond yields, which has been an uneven trend over rate carry combined to make them high-conviction long

the last 12 months. In February, Russia’s invasion of Ukraine and opportunities within our strategy. We slightly reduced the Brazilian

the Western financial and economic sanctions that followed real exposure after some of its outperformance.

shocked equity prices lower still, although equities outside Russia

regained some of these losses by the end of the quarter. The Russia’s invasion of Ukraine, and the sanctions in response from

sanctions on Russia were sufficiently potent to render almost all Western countries, surprised the markets in their aggressiveness.

Russian assets—and the ruble—untradeable in March. Contagion to Our prior game-theoretical analysis of the geopolitical situation had

other markets, however, was quite limited, even though the underestimated the risk tolerance of Russia in seeking to advance

invasion and its aftermath will have profound effects. The U.S. dollar its objectives of greater control of Ukraine and pushing back against

was strong against its developed-currency peers. Energy prices, Ukraine’s Western-aligning aspirations. The analysis also

energy-sector stocks, and the currencies of energy-producing underappreciated the coalition power and resolve of the United

countries (not including Russia) were strong. Marketwide volatility States, Europe, and others in responding in an economic/financial

rose and experienced some upward spikes. dimension. While Russia’s military aggression appears to have had

an element of overreach, and its progress is lower than it may have

Before Russia’s unprovoked war, expectations for inflation in most expected, a rapid de-escalation may now carry with it potential

of the world (excluding most of Asia) had continued to rise, and the costs to Russia and may be more difficult than before. Western

view that inflation would prove transient (expressed a year ago by sanctions, on the other hand, have surprised markets with their

central banks) looked increasingly misplaced. Developed-market power to set off a systemic financial crisis in the Russian economy

monetary authorities, who (mostly) have yet to raise interest rates that has caused the ruble to collapse and Russian assets to be

by any significant amount from their post-pandemic lows, appeared effectively canceled from the global trading system. Russia’s

increasingly behind expectations in respect of their actions to economy is likely to tip into recession as a result, accompanied by a

contain prices. The contrast in the policy interest rate stance period of significantly higher inflation. Many other nongovernment

between G7 central banks and some in the emerging world had economic agents have swiftly curtailed or exited their involvement

become quite stark, and more so than the contrast in inflation rates. with Russia, and its government has experienced sudden and severe

Somewhat unusually, this policy difference allowed currencies such political isolation from much of the world, although notably not

as the Brazilian real, Chilean peso, and Colombian peso to from China.

outperform the U.S. dollar through a period of increasing global

pessimism about inflation and rates, principally because the former Higher energy prices are an offsetting benefit to Russia, as is the

three central banks had started their monetary tightening cycle reluctance (and practical inability) of Europe, among others, to

significantly earlier and had been more aggressive. We carried cease buying oil and natural gas from the country. World prices of

positive exposure to Latin American currencies, which we food such as grain, which is also a significant export from Russia

accumulated over 2020-2021 as their prior fundamental (and Ukraine), have also increased sharply as the war will

undervaluation and their increasingly attractive relative interest undoubtedly disrupt and shrink supply capacity. Global inflationSummary & Outlook Q1 2022

pressures, as a result, have had an additional upward shock on top enduring ethical and ESG objections to including Russia as an

of what had previously already been a significant reflationary investment option for some time. Should the situation ultimately

impulse. In the near term, inflation rates are therefore apt to push change in a favorable direction, we will likely seek to position again

still higher in most countries compared with prewar anticipation. for what may be very large opportunities in Russian markets, but

The medium-term impact on global growth, however, is ultimately for now these are precluded and we are not contemplating re-

more likely to be contractionary, with implications that after establishing positions in the near term.

inflation peaks, there may be a greater subsequent downward

impulse. Weighing these influences, the U.S. Federal Reserve ended Although global contagion and generalized “risk off” behavior in

its period of ultra-low interest rates with a small increase in March, other markets and currencies has been quite limited, there are some

although it published expectations of additional increases at each of clear knock-on effects of Russia’s entry into war with its neighbor,

its scheduled rate decisions in 2022. We had notably reduced our to which we have responded in strategy changes. These include

government fixed income exposure in 2021 in advance of the first- reducing our exposure to European financial sector equities, which

quarter back-up in yields. We bought back bond exposure in 2022 at are adversely impacted by regional proximity and the nature of the

higher yields (lower prices). sanctions weaponry deployed by the Western coalition. We have

also increased our short exposure to the euro and the British pound,

Long exposure to the Russian ruble (RUB) had been a high- to the benefit of the U.S. dollar and the oil-sensitive Colombian peso.

conviction position before the invasion of Ukraine, supported by Importantly, although the negative impact of the Russia sanctions is

large fundamental undervaluation and an aggressive central bank likely greater for Europe, European leaders have nonetheless

operationally free from political influence (similar to Latin evidenced the collective political will to stand by the measures to

America). The invasion suspended the normal risks associated with which they have so far jointly agreed with the United States. We

valuation and monetary policy, and Western sanctions severely have retained our overweight exposure to energy sector equities

weakened RUB. We had cut the exposure by half pre-invasion and, even though energy prices have moved above our long-term

as our analysis shifted in line with the developing events, eliminated equilibrium expectation as a result of the war. In addition, we have

the rest on the last day of February. The central bank has been opened a thematic equity position long of a basket of names in

rendered largely impotent to defend RUB as its foreign-exchange cybersecurity, which is hedged by an equivalent sale of the

reserves have been sanctioned and, despite a dramatic policy rate information technology sector. This area had already looked

increase, trading of rubles has mostly dried up as investors attractive to us before Russia-Ukraine, but the war has likely

overwhelmingly exited or wished to exit. We had also established a increased the demand for cybersecurity spending looking ahead.

modest long position in Russian equity earlier in the year and

before the military invasion, but the geopolitical events and the Our long-term investment objective is to deliver positive investment

freezing of most Russian markets led us to unwind this exposure. returns above cash through a market cycle. We remain grounded in

There remains considerable uncertainty over when Russia may be fundamental valuation as our first stage—we strive to take only

investable again, and many institutions and corporations may have compensated risk and are unwilling to extend exposures unduly in aSummary & Outlook Q1 2022 reach-for-yield that would be dictated not by opportunities and risks but by very low real interest rates. There will be environments in which we conclude that macro markets do not provide returns and risks compatible with portfolio objectives, alongside other periods where compensation is abnormally high. During the last decade, the challenge of navigating these evolving environments has remained a significant component in the investment landscape, but we find our investment process, dialogue, and decision-making well equipped to meet this challenge in an appropriate way. We remain vigilant as we assess new and relevant information to capture future investment opportunities in a timely manner and will continue balancing the relationship between risk taken and compensation expected.

Investment Performance Q1 2022

The below table shows the performance of the William Blair SICAV – Dynamic Diversified Allocation Fund for the quarter.

Since

Periods ended 31/12/2021 Quarter 1 Year 3 Year Inception*

William Blair SICAV – Dynamic Diversified Allocation Fund

-2.85% 1.00% 2.12% 1.72%

(Class J HJPY)

JP Morgan Cash Index Japan (3M) -0.02% -0.16% -0.09% -0.07%

*Inception: 24/05/2018

The J.P. Morgan Cash Index measures the total return of a rolling investment in a notional fixed income instrument with a maturity of three months. The

deposit rates used in the calculation of the JP Morgan Cash Index are LIBOR or similar local reference rates.

Periods greater than one year are annualised. All charges and fees have been included within the performance figures. For the most current month-end

performance information, please visit our Web site at sicav.williamblair.com.

Please refer to the ‘Important Disclosures’ section at the end of this document for further information on investment risks and returns.Performance Analysis Q1 2022

The below table shows the calculated regional performance attribution of DDA SICAV by asset segment for the reporting period.

Total (%) -2.9

Equity -1.2

North America 0.3

Europe 0.4

Asia 0.0

Emerging -2.7

Other 0.8

Fixed Income -1.2

North America Rates -0.8

Europe Rates -0.2

Asia Rates 0.0

Emerging -0.1

Credit -0.1

Low Duration 0.1

Currency 1.4

North America -0.1

Europe 0.1

Asia -0.7

Emerging 2.0

Security Selection -1.7

Residual -0.2

Source: Cloud Attribution Ltd.

Past performance does not guarantee future results. Portfolio exposures based on the William Blair DDA SICAV. Past performance does not guarantee future results. Performance attribution is

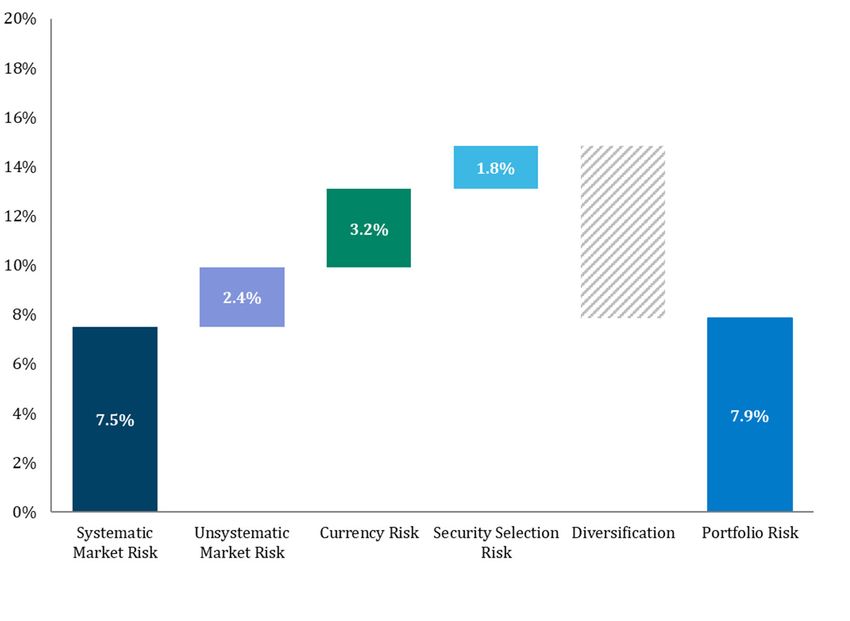

sourced from Cloud Attribution Ltd. Using the Karnosky-Singer performance attribution methodology.Forward-Looking Risk Q1 2022 The below chart shows the expected sources of investment risk* for DDA as of quarter-end. Source: William Blair. *The DAS team’s expectation of the portfolio’s volatility as viewed through the team’s proprietary Outlook risk model, in which the team’s near-term risk assumptions are quantified.

Selected Strategy Exposures Q1 2022

The table below shows select market and currency strategy exposures as of quarter end.

Equity 35.3% Active Currency

U.S. 9.1% U.S. Dollar (USD) -1.6%

Canada 0.3% Canada Dollar (CAD) -8.8%

Europe (ex-U.K.) 5.1% Other Americas 27.4%

UK 6.3% Euro (EUR) -8.8%

Asia Developed 5.2% Switzerland Franc (CHF) -4.8%

Emerging 9.3% Great Britain Pound (GBP) -3.3%

Other Europe 2.2%

Fixed Income 25.0% Australia Dollar (AUD) and New Zealand Dollar (NZD) -17.2%

U.S. Treasury & Credit1,* 9.1% Japan Yen (JPY) 8.8%

Non-U.S. Treasury & Credit1,* 6.3% China Yuan (CNY) -4.3%

Emerging 9.6% Asia (Excluding JPY and CNY) 16.1%

Other -5.8%

Cash & Other 39.7%

2

*Credit Detail Select Exposures Detail

U.S. Investment Grade Spread 8.1% Israeli Shekel (ILS) -7.4%

U.S. High Yield Spread 1.5% Brazilian Real (BRL) 9.9%

U.S. MBS Spread 0.0% Colombian Peso (COP) 8.6%

European Investment Grade Spread 3.1%

European High Yield Spread 0.0%

1

Reflected as 10-year exposures

2

Select currency exposures by largest expected contribution to portfolio risk

Market and currency strategy exposures shown above are as of quarter-end. For illustrative purposes only and not intended as investment advice. Allocations are subject to change without notice.Important Disclosures Q1 2022 GENERAL INFORMATION This is a marketing communication. Please carefully consider the investment objectives, risks, charges, and expenses of the Company. This and other important information is contained in the Company’s Prospectus and KIIDs, which you may obtain by visiting sicav.williamblair.com. Read these documents carefully before investing. Recipients of this document should be aware of the risks detailed in this paragraph. Please be advised that any return estimates or indications of past performance on this document are for information purposes only. Both past performance and yield may not be a reliable guide to future performance. The value of investments and income from them may fall as well as rise and investors may not get back the full amount invested. The value of shares and any income from them can increase or decrease. An investor may not get back the amount originally invested. Where investment is made in currencies other than the investor's base currency, the value of those investments, and any income from them, will be affected by movements in exchange rates. This effect could be unfavourable as well as favourable. Levels and bases for taxation may change. Specific securities identified and described to do not represent all of the securities purchased or sold and you should not assume that investments in the securities identified and discussed were or will be profitable. Holdings are subject to change at any time. References to specific securities and their issuers are for illustrative purposes only and are not intended and should not be interpreted as investment advice, offer or a recommendation to buy or sell any particular security or product. Any discussion of particular topics is not meant to be complete, accurate, comprehensive or up-to-date and may be subject to change. Factual information has been taken from sources we believe to be reliable, but its accuracy, completeness or interpretation cannot be guaranteed. Information and opinions expressed are those of the author and may not reflect the opinions of other investment teams within William Blair. Information is current as of the date appearing in this material only and subject to change without notice. RISKS The value of shares and any income from them can increase or decrease and an investor may not get back the amount originally invested. Where investments are made in currencies other than an investor's base currency, the value of those investments will be affected (favourably or unfavourably) by movements in exchange rates. Derivatives include the risk that the instrument is not correlated with the underlying investment to which it relates, liquidity risk, counterparty risk, and the risk that the transaction could expose the Fund to the effects of leverage, which could increase exposure to the market and magnify potential losses. The value of an investment may decline due to factors affecting securities markets generally or particular industries represented in the securities markets.

Important Disclosures Q1 2022 Further specific risks may arise in relation to specific investments and you should review the risk factors very carefully before investing. Intended risk profile of the Fund may change overtime. The Fund is designed for long-term investors. The most current month-end performance information is available on sicav.williamblair.com. FUND INFORMATION The Fund is a sub-fund of William Blair SICAV, a “société d’investissement à capital variable”, incorporated under the laws of the Grand Duchy of Luxembourg having its registered office at 31, Z.A.I. Bourmicht, Bertrange, registered in the R.C.S. Luxembourg under n⁰ 98806 and approved by the Luxembourg Supervisory Authority of the Financial Sector (the “CSSF”) as an undertaking for collective investment in transferable securities (“UCITS”) in accordance with the EU directive 2009/65/EC, as amended (the “Company”). Authorization of the Company by the CSSF is not an endorsement or guarantee nor is the CSSF responsible for the contents of any marketing material or the Company’s Prospectus or applicable Key Investor Information Document (“KIID”). Authorization by the CSSF shall not constitute a warranty as to the performance of the Company, and the CSSF shall not be liable for the performance of the Company. The investments in the Fund may not be suitable for all recipients. This material is for informational purposes only, is not contractually binding, and does not contain personalized recommendations or advice and is not intended to substitute any professional advice on investment in financial products. The Company may not be registered to be marketed in or may only be marketed to certain categories of investors in your jurisdiction. For information regarding jurisdictions in which the Company is registered or passported, please contact your William Blair representative. This document should not be used or distributed in any jurisdiction, other than those in which the Fund is authorized, where authorization for distribution is required. This document has been prepared and issued by WILLIAM BLAIR INVESTMENT MANAGEMENT, LLC in its capacity as a delegate of the FUNDROCK MANAGEMENT COMPANY S.A., a "société anonyme", incorporated under the laws of the Grand Duchy of Luxembourg having its registered office at 33, rue de Gasperich, L-5826 Hesperange and registered in the R.C.S. Luxembourg under n° 104196 (the "Management Company"). The Management Company is authorised and regulated by CSSF as the management company of UCITS under the EU directive 2009/65/EC, as amended. The Management Company has been appointed as the management company of the Company and has appointed WILLIAM BLAIR INVESTMENT MANAGEMENT, LLC, the asset management business of WILLIAM BLAIR & COMPANY, LLC., having its registered office at 150 North Riverside Plaza Chicago, IL 60606, USA as the investment manager for the Fund. WILLIAM BLAIR &

Important Disclosures Q1 2022 COMPANY, L.L.C. is authorized as the global distributor of the Company and to facilitate the distribution of Shares in certain jurisdictions through financial intermediaries. The Articles of Incorporation, the Prospectus, the KIID, the Annual and Half-yearly Reports of the Fund and the Subscription Form are available free of charge in English and German from the website sicav.williamblair.com or at the registered office of the Management Company (33, rue de Gasperich, L-5826 Hesperange, Grand Duchy of Luxembourg), at the registered office of the Fund (William Blair SICAV, 31, Z.A. Bourmicht, L-8070 Bertrange, Grand Duchy of Luxembourg) or from the Swiss representative, First Independent Fund Services Limited, Klausstrasse 33, CH-8008 Zurich, and in German language at Marcard, Stein & Co., Ballindamm 36, 20095 Hamburg, Germany, and at Bank of Austria Creditanstalt AG, Am Hof 2, 1010 Vienna, Austria. Paying agent in Switzerland is NPB New Private Bank Ltd, Limmatquai 1, CH-8024 Zurich. Copyright © 2022 William Blair. "William Blair" refers to William Blair & Company, L.L.C., William Blair Investment Management, LLC, and affiliates. No part of this material may be reproduced in any form, or referred to in any other publication, without express written consent.

You can also read