TransAlta Corporation Submission to Alberta's Climate Change Advisory Panel - October 1, 2015

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

TransAlta Corporation

Submission to

Alberta’s Climate Change

Advisory Panel

October 1, 2015

October 1, 2015 Dr. Andrew Leach Chair, Alberta Climate Change Advisory Panel (submitted electronically) Dear Dr. Leach: TransAlta Submission to the Climate Change Advisory Panel I am pleased to provide you and Panel Members with TransAlta’s submission to the Alberta Climate Change Advisory Panel. A clear and robust climate change policy for Alberta is both possible and necessary, and it should carefully balance environmental objectives with economic considerations. TransAlta strongly supports a proposal, created jointly with ATCO and Maxim, to dial down production and GHG emissions from coal fired generation. The proposal as described in the attached submission achieves immediate and sustainable GHG reductions, protects jobs, keeps power price impacts to a minimum, maintains system reliability, and avoids stranded investments. In addition, it also supports a smooth yet accelerated transition to renewable energy supply, by providing firm supporting capacity from reduced but available coal generation, and providing a mechanism for new renewable resources to enter the market in a competitive manner We refer to this proposal as “Dial Down (Coal) – Dial Up (Renewables).” The concept was presented to the Panel on September 15th. In comparison to other policies that have been proposed, it is substantially less costly in total and more efficient in terms of costs per tonne reduced. Our attached submission also provides substantial analysis of various greenhouse gas and renewables policy options and their effects on Alberta’s electricity sector. We have collaborated with London Economics International to contribute experiential assessments of various policy alternatives in other jurisdictions and to conduct modeling of some of those alternatives within the Alberta market context. We trust you will find that work useful. The work with London Economics continues. While not available for this submission, we intend to subsequently provide the Government with detailed macro-economic modeling of the socio- economic impacts of various GHG policies, including jobs, taxes and GDP effects. Finally, we provide commissioned independent work through the University of Alberta on air quality in the Edmonton airshed, with particular attention to the contribution of coal-fired generation. This work was done in response to continued unsubstantiated claims that coal-fired

generation was a major contributor to Edmonton’s air quality events, and a rationale for the

need to accelerate the retirement of coal units. You will see that the research shows minimal

airshed impacts from operation of coal-fired generation to the west. Clearly the Edmonton

airshed should not be an important determinant in the Panel’s climate change-related

considerations.

We intend to continue our analytical work beyond the timeframes for the Panel submission, and

will be providing the Government with additional information as it becomes available, with the

objective of supporting good policy decisions.

We wish you and the Panel well in your upcoming deliberations.

Yours truly,

TRANSALTA CORPORATION

Original signed by

Dawn Farrell

President and CEO

Enclosure

(attached electronically)

Page 2

Contents

EXECUTIVE SUMMARY ........................................................................................................... 3

DIAL DOWN DIAL UP SOLUTION ........................................................................................... 9

Coal Dial Down ................................................................................................................. 9

Renewables Dial Up ........................................................................................................ 11

Modeling Results ............................................................................................................. 12

GHG Reductions ...................................................................................... 12

Price Impacts ............................................................................................ 13

Cost of GHG Reductions ......................................................................... 14

Remaining Market Sustainability Questions ................................................................... 16

INVESTMENT COSTS & REQUIRED RENEWABLE INCENTIVES ................................... 17

INDEPENDENT ANALYSIS OF POLICY OPTIONS.............................................................. 19

Summary of Analytical Work .......................................................................................... 19

Policy Guidance from Case Studies in Other Jurisdictions ............................................. 20

Modeling of Various GHG policy Options ...................................................................... 33

Early Retirement of Coal in Other Jurisdictions .............................................................. 50

Review of Energy Efficiency Policies ............................................................................. 56

Review of Pembina Report “Power to Change” .............................................................. 68

Macro-Economic Analysis – Work in Progress............................................................... 77

AIR QUALITY CONSIDERATIONS ........................................................................................ 80

APPENDICES ............................................................................................................................. 83

Appendix 1 - Centralia Experience .................................................................................. 83

Appendix 2 - Detailed Report on Policy Case Studies .................................................... 83

Appendix 3 - Detailed Review of the Pembina Report “Power to Change” ................... 83

Appendix 4 – Detailed Presentation of Edmonton Air Quality Study ............................. 83

Appendix 5 – London Economics Corporate Resume ..................................................... 83

1

Executive Summary

1) Overview:

The enclosed report contains three major components:

A proposal for a smart policy solution to reduce greenhouse gas emissions and grow

renewable generation, referred to as dial down coal and dial up renewables

A review of alternative policy options, including lessons from case studies in other

jurisdictions and detailed modeling of their emission and cost impacts

A recent study of air quality in the Edmonton region as a science-based indicator of

minimal impacts of coal-fired generation to that airshed

2) A Proposed GHG framework for electricity

The Alberta Government has stated two principal objectives relevant to the electricity sector and

related to the Panel’s work – those being the reduction of the Province’s greenhouse gas

emissions and the growth of renewable energy within the Alberta fuel mix. TransAlta, ATCO

and Maxim propose a policy framework that would dial down greenhouse gas emissions from

Alberta coal units in a planned and cost-effective manner. Further, the dial down of coal would

be coupled with a dial up of renewable energy build.

Under this proposal, coal-fired generators would implement a 20% reduction in output

immediately, resulting in physical GHG reductions of 8-10 Mt’s per year from coal. In

return, SGER obligations are considered met for coal generators.

The dial down coal – dial up renewables proposal minimizes the cost associated with reducing

GHG emissions from the power sector, provides a mechanism to ensure renewables investment,

and ensures an orderly transition for the industry.

The proposed dial down – dial up policy has the following characteristics:

• Immediately implementable

• Delivers the least cost per tonne of GHG reduced

• Maintains system support for renewable build without a rush to new gas generation

• Protects consumers from price shocks

• Self-funding through physical SGER compliance rather than financial compliance

• Protects jobs and mitigates economic impacts of low carbon transition

• Adjustable by government

• Compatible with the Alberta market design

The dial down coal – dial up renewables proposal has been modeled and compared to other

modeled policy options, summarized in the table on the next page:

3

Dial Down – Accelerated

Cap & Trade RPS

Dial Up Shutdown

GHG reductions

(cum. 2016 – 2030) 95 Mt 127 Mt 61 Mt 111 Mt

(net of replacem’t*)

Cost per tonne reduced $72/t $278/t $186/t $206/t

Air quality co-benefits Early reductions Uncertain Later reductions Uncertain

Renewables by 2030 Large ~25% 20% 10% - 15% Large ~35%

Modest gas and Larger than dial Early gas Large gas req’mts to

Gas replacement

delayed down replacement backstop renewables

Customer impacts** $75B $103B $79B $91B

Small increases Short term gains,

Effects on jobs Uncertain High impacts

relative to BAU Mid Term Losses

Mid Term need to

Market design change Small, Mid term

None incent back stop Market Failure

req’mts review required

capacity

Some Transmission Some Transmission

Small Transm’n Large Transmission

Transmission impacts costs for costs for

impacts Build Costs

renewables renewables

Costs will force RPS allocations will

Stranded capital None coal out – strands Strands capital force coal out –

capital strands capital

Policy impacts Creates gov’t debt,

Investment climate Breaks regulatory

Smooth transition existing investment changes market,

impacts compact

viability winners & losers

*Cumulative GHG reductions assume greater natural gas % replacement early, more renewables % later

**Customer impacts can be compared against a business-as-usual cost forecast of $68B over the same period.

Includes energy, transmission and all out-of-market costs.

3) Analysis of Policy Options

TransAlta in association with London Economics International has completed a series of work

products that will contribute to thoughtful policy making.

a) Lessons from Policy Case Studies

Case studies were carried out based on first-hand experience, including:

California’s cap and trade design and experience to date

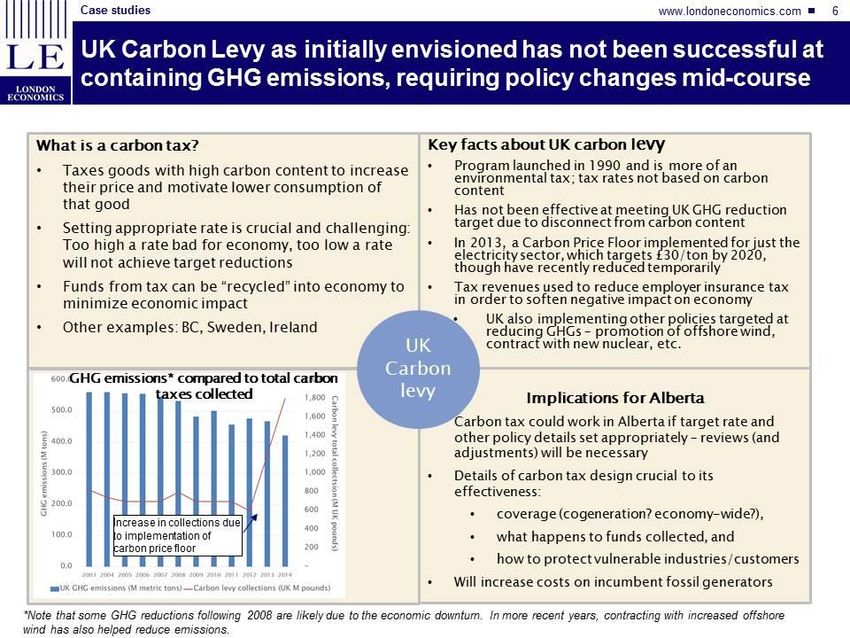

The UK’s carbon levy as an example of a carbon tax

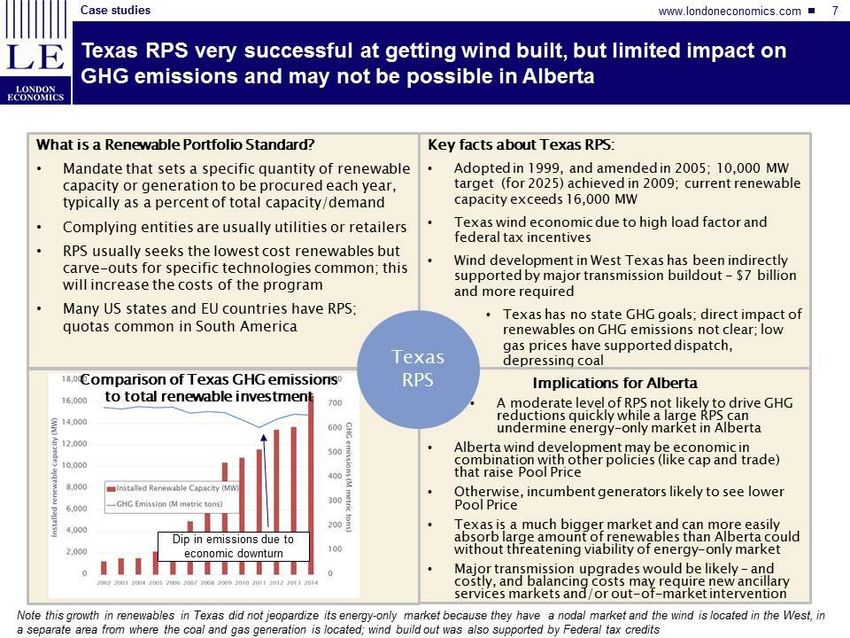

The RPS experience in Texas

Feed in tariff programs in Germany and Ontario

A large scale energy efficiency program in California

4

The report details the success factors (and sometimes failure causes) in those jurisdictions

but also comments on the challenges associated with application to the Alberta context,

especially given the uniqueness of the Alberta electricity market in terms of market design

and industrial intensity.

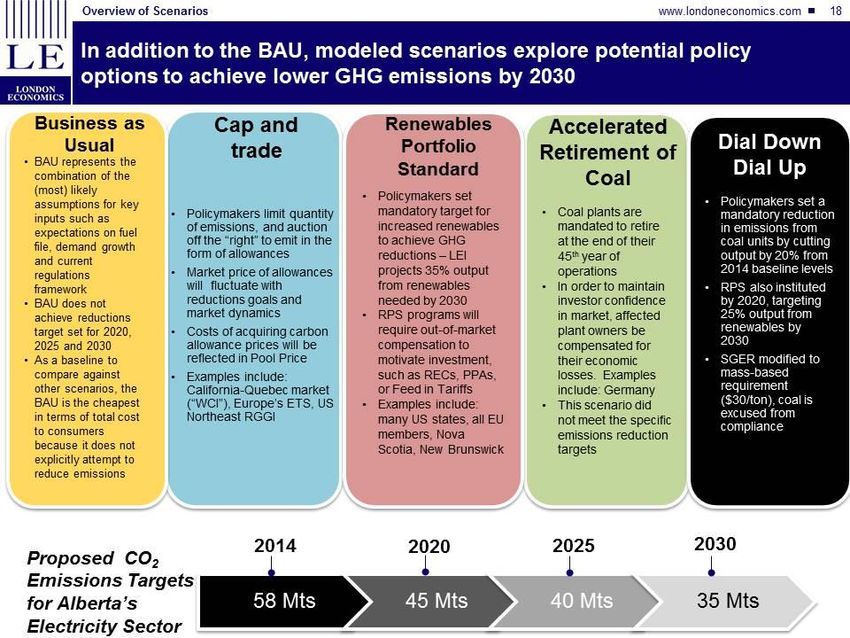

b) Modeling of GHG policies in Alberta’s electricity sector

LEI modelled the Relative performance of the Dial Down Dial Up approach against three

other policy scenarios. LEI uses a dynamic model of the Alberta electricity system. For

comparability, scenarios were created to achieve reduction of GHG emissions from sector

levels of 58 Mt/yr today to 35 Mt/yr in 2030.

The scenarios modeled were:

a) a sector-wide cap and trade program,

b) an accelerated retirement of coal scenario, and

c) a sector-wide renewable portfolio standard.

The results were compared to a business-as-usual forecast assuming only the federal GHG

regulations for coal units and the recently-adjusted SGER regulations.

Comparative results are shown below.

5

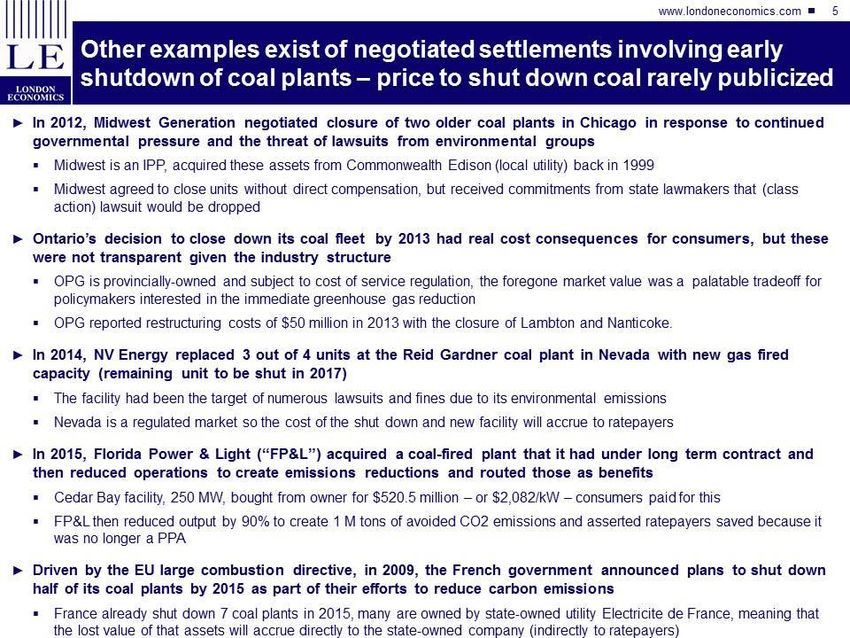

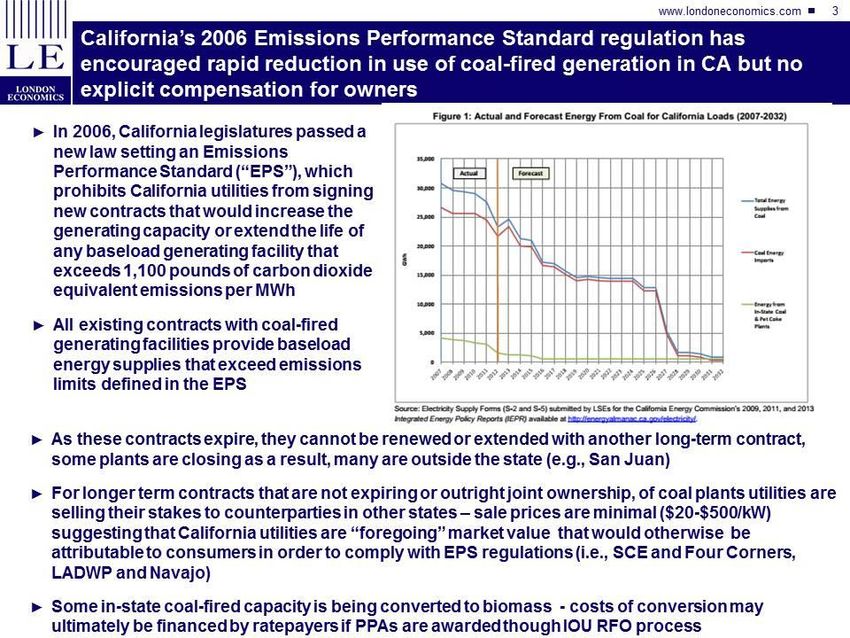

c) Examining early retirement of coal in other jurisdictions

Experiences in Germany, California and Ontario are described. These experiences are

instructive but there are also major differences compared to the Alberta situation in terms

of government ownership and market structure, and the ability to pass on costs through

rates

d) Energy efficiency programs

Alberta does not have an active history in promoting energy efficiency in the electricity

sector, in part because of the deregulated market structure and in part because of the high

industrial intensity. Examples of activities in several U.S. states are described and their

relevance to the Alberta context.

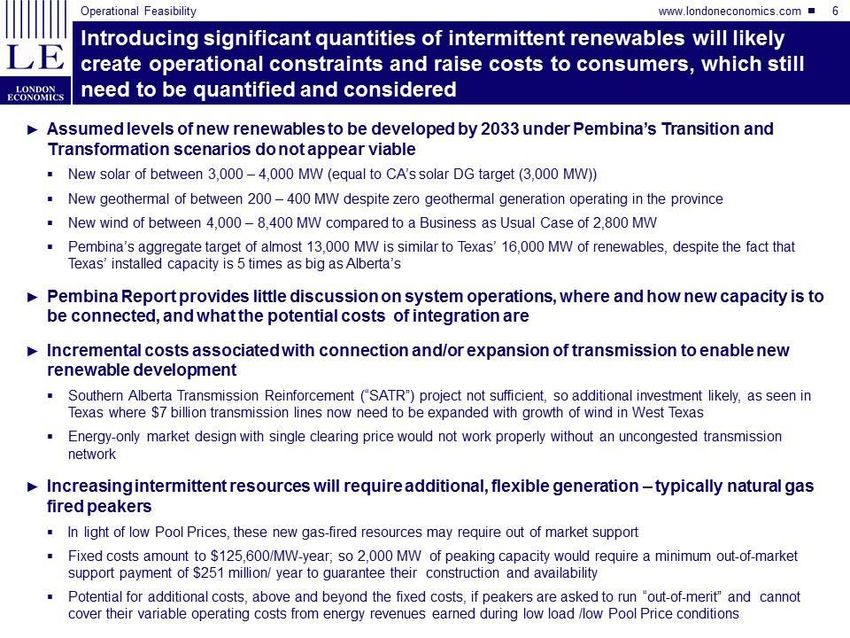

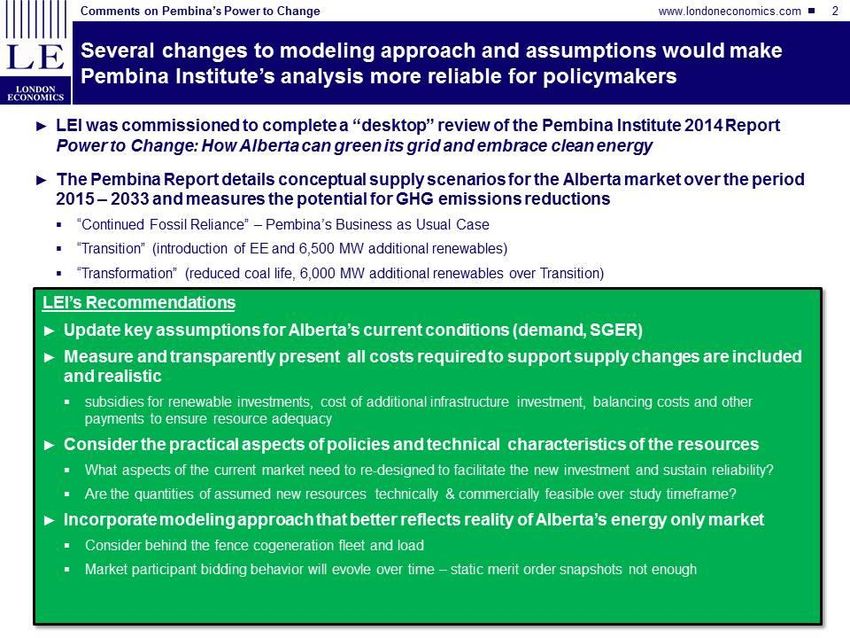

e) Review of the Pembina report “Power to Change”

The report issued by the Pembina Institute in 2014 was useful in generating discussion

about the benefits, challenges, costs and opportunities of a major transformation of the

Alberta electricity system. In order to add to this constructive conversation, a review of

the report was undertaken to identify improvements and deepen the level of discussion.

The review identified that the transformation alluded to in the report would face tougher

challenges than originally thought, and is perhaps overly optimistic about it’s potential to

both reduce emissions and grow renewable generation.

6

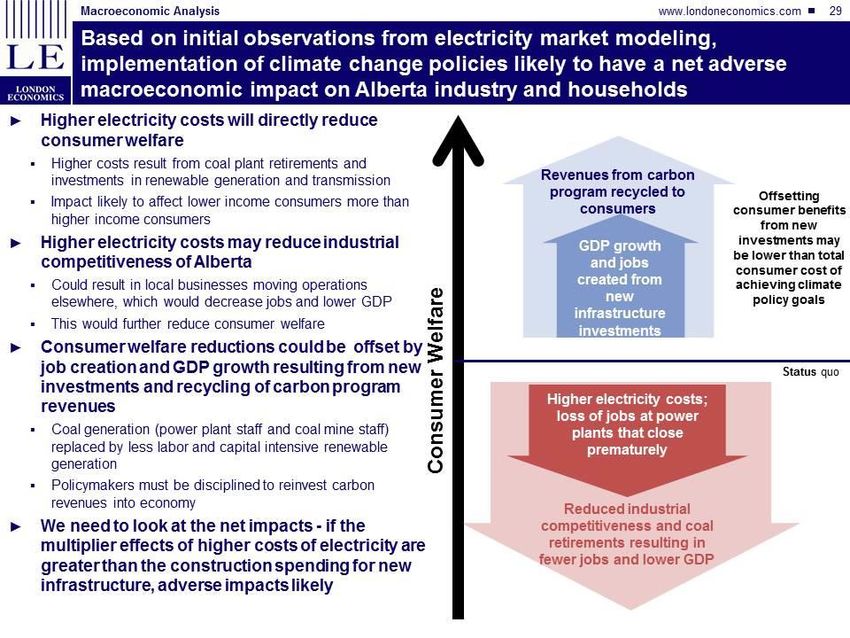

f) Macro-economic considerations

Detailed macro-economic modeling of various policy scenarios is underway and will be

provided separately to Alberta. Earlier work conducted in 2014 for TransAlta by Dr.

Robert Mansell provided the following data representative of the impacts of all coal-fired

generation in Alberta:

Alberta Coal Generation Fleet Economic Contribution

Direct, indirect and induced effects (2015 to 2020)

GDP add to the Alberta economy $10 billion

Labour income (wages) $4.4 billion

Employment 44,500 person-years

Total federal and provincial tax income $2.6 billion

4) Air quality and coal-fired generation

In the Spring of 2015, TransAlta funded research on a detailed review of data associated

with air quality in the urban Edmonton airshed. This work was in response to a series of

claims that coal-fired generation units 60 kilometers west of Edmonton were a major

contributor to air quality events being observed in Edmonton, and therefore closing those

units as quickly as possible was justified.

Based on a five-year monitoring data set and cognizant of both short range and long

range sources, the study found the following composition of PM2.5 in the Edmonton

airshed:

7

Taken in aggregate, the study found there was only a minor signal associated with

coal combustion emissions as a portion of secondary sulphate, and estimated to be

no more than 10% of the PM2.5 contribution.

Further, the study examined trends in Edmonton’s air quality and observed the

following trends:

Hourly concentrations of nitrogen dioxide (NO2), sulfur dioxide (SO2),

total hydrocarbon (THC) and carbon monoxide (CO) have steadily

decreased since 1998.

Hourly concentrations of particulate matter (PM2.5) are unchanged

since 1998.

Hourly concentrations of ozone (O3) show inconsistent change.

Chemical species present in PM2.5 unchanged or decreasing

(for organic carbon, elemental carbon, barium and lead) since

measurements began in 2007.

------------------ End Summary ------------------

8Dial Down Dial Up Solution

TransAlta, ATCO and Maxim, representing the majority of coal-fired generation in Alberta, are

proposing a policy framework that would dial down greenhouse gas emissions from Alberta coal

units in a planned and cost-effective manner. The dial down of coal would be coupled with a

dial up of renewables. Coal units would first reduce output and then begin to retire. Dial down

dial up delivers:

The most cost efficient mechanism to achieve carbon reductions in the electricity sector

Guaranteed reduction in greenhouse gas emissions from coal starting in 2016

Minimal market disruption

Job protection

Guaranteed renewables development

We believe this approach represents a balanced, pragmatic and responsible policy framework

that would achieve the optimal solution between environmental benefit and current and future

economic impacts including the impact to employment and sustainability of local communities.

Independent analysis conducted by London Economics (LEI) supports the Dial Down Dial Up

solution for reducing GHG emissions and delivering a cost effective solution for both

customers and generators.

The coal dial down component can be implemented as soon as 2016 resulting in immediate GHG

reductions. The renewables dial up component with early incentives could begin to show results

as early as 2018. Challenges such as an agency to provide contractual certainty, transmission

requirements and construction timeframes will need to be addressed over the next few years. If

the approach is taken, renewables can be commercially operational by as early as 2020.

The more aggressive the RPS goals in terms of scale and pace the more likely market design

changes will be needed to ensure the market remains cost effective sustainable and most

importantly reliable. Procurement of renewables greater than 20% creates significant risk for

market design failure.

Overall, the proposal minimizes the cost associated with reducing GHG emissions from the

power sector, provides a mechanism to ensure renewables investment, and ensures an orderly

transition for the industry.

Coal Dial Down

The coal dial down restricts energy production from coal generation by subjecting it to a fixed

production cap. This results in a guaranteed reduction of emissions from the coal generation

fleet. Further, the coal dial down maintains coal generation capacity on the system for reliability,

avoiding an immediate capital investment in new generation. Near term market price impacts

are also minimized as the capacity is still available based on economic signals.

9Key Attributes

The policy details proposed below have been developed in such a way as to exhibit the

following attributes:

Immediate implementation

Lowest Cost per tonne GHG reductions

Creates “space” for a renewable buildout while avoiding a dash to gas

Keeps electricity consumer’s bills low

Self-funding – no payment to coal generators is required

Protects jobs

Mitigates economic impacts of low carbon transition

Adjustable by government

Compatible with the Alberta market design

Description

Coal-fired generators would implement a 20% reduction in output immediately, resulting in

gross coal GHG reductions of 8-10 Mt per year. In return, SGER obligations are considered met

for coal generators. In the near term, the decrease in coal generation will be replaced with

natural gas generation, but longer term the Dial Up will offset the Dial Down with renewables.

Details

• January 2016 Implementation - convert the existing intensity-based SGER to a mass-

based approach immediately, allowing the application of a tonnage cap on coal-based

emissions. Reductions could begin as early as 2016.

• 20% Mass Based Cap for Coal - a 20% reduction from a base level of emissions

proposed. For the sake of modeling 2014 actual emissions levels from the coal fleet are

used as the baseline. The cap would be a hard cap with large financial consequences for

any exceedances.

• No Change for Gas Units - gas emission reduction burden is unchanged from the current

level at an effective price of $6/tonne of carbon.

• Flexible Compliance to a Hard Cap - generators would reduce output of coal units at their

discretion throughout the year to achieve their portion of the dial down. The total coal

capacity would be available to the system to maintain reliability and meet peak loads.

• No Payment Required for Stranded Investment - achieving the 20% reduction would be

considered as compliance with the SGER regulation, thus avoiding any additional

compliance cost. This ‘funds’ the coal dial down portion of the proposal at no direct cost

to consumers. The costs would be borne by coal generators through reduced revenues.

• Emission Reduction Credits Available Below the Cap to Further Incent Reductions -

Emissions below the cap would create fungible emission reduction instruments, tradeable

within and outside the sector. In the modeling, these instruments were valued at

$30/tonne. Coal units would receive 1 tonne of credit for every tonne of reduction below

10the cap. This incentive would increase the level of GHG reductions when electricity

market prices are low.

• 8 – 10 Mt Reduction in Gross Coal Emissions Starting in 2016 - the application of a 20%

reduction cap on coal units will produce 8 to10 Mt per year of GHG reductions initially.

This is based on actual 2014 GHG emissions from the coal fleet of about 44 Mt. As coal

units start to retire beginning in the early 2020’s, overall coal fleet reductions will decline

more. The ‘dial’ can be adjusted to meet changing targets over time.

Renewables Dial Up

Renewables Dial Up fits alongside the coal dial down as a further emission reducing strategy.

The Dial Up approach ensures renewable energy resources are developed at a greater rate than

expected under a business as usual approach. The Dial Up ensures a real and deliverable target

on renewables.

Key Attributes

The policy details proposed below have been developed in such a way as to exhibit the following

attributes:

• Mandatory renewables targets.

• Renewables investment supported by firm contracts for either energy or renewable

attributes.

• Adjustable by government.

• Competitive procurement model to minimize costs.

• Space is created for the development of renewables in a cost effective way.

• Alberta’s limited capital is used as effectively by limiting stranded investment.

Description

A mandatory target is set for renewable energy as a proportion of total provincial load. For

example, an RPS could be set at:

15% of total load in 2020.

20% of total load in 2025.

25% of total load in 2030.

With additional increases in renewables generation over time post 2030.

A 25% RPS targets would put Alberta amongst the most ambitious jurisdictions in North

America. Alberta’s current renewable generation supplies 8% of energy demand and each one

percent increase in the renewables supply is equivalent to adding a 300 MW wind farm.

11Details

A government agency such as the AESO offers long-term contracts for either renewable

energy or the environmental attributes of the renewable energy.

The contracts are offered through an auction mechanism and volumes are selected to

meet transparent renewable targets, i.e. 15% of total provincial energy in 2020.

The targets could set ‘carve outs’ for specific technologies, e.g. 1% of total provincial

energy for solar in 2020.

Incumbent renewable generation would compete for the contracts and/or sell their

environmental attributes to remain viable and ensure equal treatment of new and existing

renewables.

Double counting for environmental attributes will not be allowed: existing renewables

would only get SGER offset credits or RPS credits not both.

All Alberta Load will bear the cost of RPS, including behind the fence load. This ensures

the cost is borne fairly across all customers classes.

Modeling Results

LEI modeled the proposed Dial Down Dial Up approach as articulated and found:

1. The approach achieves 95 MT of cumulative GHG reductions between 2016 and 2030

relative to Business as Usual emissions

2. Impacts to the electricity price are moderate due to the offsetting nature of the coal Dial

Down and renewables Dial Up

3. Out of market costs are relatively minor

4. Market design will need to be revisited at higher levels of renewables to ensure market

sustainability and system reliability.

GHG Reductions

The Dial Down Dial Up scenario achieves GHG emission reductions by reducing coal output

relative to the Business as Usual (BAU) case as well as increasing renewable generation. The

total impact of the solution guarantees net GHG emission reductions of 95 Mt (inclusive of

increased gas emissions) from 2016 through 2030. The diagram below shows that the Dial

Down Dial Up scenario achieves nearly 7 Mt of net emission reductions per year on average.

Greater guaranteed reductions can be achieved by altering the relative dials, and the incentive

mechanism is also expected to result in further reductions. In addition, as natural gas will not

replace coal as the Dial Up is implemented, the reductions will be sustained over the long-term.

12Price Impacts

The Dial Down Dial Up approach results in relatively minor impacts to the market price because

the coal Dial Down and renewables Dial Up work in opposite directions. Reducing coal output

increases the power price as cheap baseload electricity is removed from the market in some

hours, but the renewables Dial Up replaces this electricity with zero marginal cost energy placing

downward pressure on market prices.

13Cost of GHG Reductions

The costs to consumers are calculated based on the total cost of the electricity market. In order

to evaluate the options relative to GHG reduction targets, the cost to consumers is evaluated

relative to the GHG reductions achieved. The result illustrated in the figure highlights that the

Hybrid option has the lowest total cost.

Costs of GHG reductions include:

1. The cost of energy at the modeled electricity price

2. The cost of transmission

3. The cost of providing real-time reliability (system balancing)

4. The cost of out of market contracts for both renewables and natural gas generation that is

required but not supported by market (in RPS case and late years in the Hybrid Case)

14The NPV of incremental costs associated with the Dial Down Dial Up scenario is $6.8B, or

roughly 10% greater than the BAU case. This represents the cost of achieving GHG emissions

reduction of 95 MT in this timeframe as compared to the BAU case, which equates to a cost of

GHG in the range of $70/tonne, as compared to costs in excess of $180/tonne in all other cases

studied (see Modeling section for the detailed results). These costs per tonne represent total

incremental costs to Alberta power consumers relative to the BAU case and measure the overall

efficiency of various carbon reduction approaches. They are not the price of carbon that would

be comparable to a given carbon tax.

The Dial Down Dial Up approach is able to create emission reductions in a low cost manner

because:

Existing capacity is maintained on the system and is used to backstop reliability

requirements as well as respond to high priced market hours.

Renewables, and wind generation in particular, are relatively cost competitive with new

natural gas generation for energy but not energy plus capacity. The Dial Down Dial Up

approach adds this renewable energy and utilizes existing capacity to the greatest extent

possible to avoid incurring immediate capital costs for new capacity.

15Remaining Market Sustainability Questions

The key concern with the Dial Down Dial Up approach is the current market design may be

inadequate over time to attract investment due to the RPS generation lowering prices. Since

renewables will be paid fixed price contracts, customers are effectively removing the market risk

of investment for these assets, but the firm (natural gas) capacity that is still needed for system

reliability will face increased risks due to potentially lower prices.

As shown in the Dial Down Dial Up case, natural gas generation required for firm capacity must

be added to the market in later years through out of market means. The potential for this

intervention could mean natural gas investment may not be added in prior years, in effect adding

a larger risk premium to generation investment in Alberta.

This issue should be further studied if the government decides to move forward with an RPS

target paid through out of market contracts. Long term sustainability must be ensured, and the

current market design may not be compatible with GHG reduction targets achieved through RPS

targets. The type of analysis that would likely be required is two-fold. First, scenario analysis

should be conducted to clarify how sensitive the wholesale market is likely to be with an RPS.

This analysis would help clarify if and when market design changes are required.

Second, a deeper analysis of both UK and German experience is important. Both markets have

added significant amounts of renewable capacity. The UK has already added market supports,

including long term contracts, to its wholesale market as a result. German policymakers are in

the process of evaluating what is required in response to sustained low wholesale power prices

that are damaging the financial viability of incumbent thermal generators. Interviews with grid

operators and policymakers in both jurisdictions would provide additional insight for Alberta as

it evaluates its options.

16Investment Costs & Required Renewable Incentives

Uncertain cash flows from electricity market increases the development costs of new gas and

wind facilities. There is a large difference in project costs based on whether the projects are

merchant or contracted.

Return Requirements for Merchant and Contracted Projects

Overall levelized costs are meaningfully impacted by:

1) the debt and equity ratio and

2) the return requirements for project

Contracted Assets Merchant Asset

Return requirements of bond and equity Debt Equity Debt Equity

holders differ depending on whether assets Ratio 75.0% 25.0% 35.0% 65.0%

are contracted or merchant. Basically, the Required Return 4.5% 12.0% 8.0% 17.5%

more contracted an asset the more debt Weighted Avg.

Cost of Capital

6.38% 14.18%

that can be used and the increased

uncertainty to revenue associated with a merchant plant leads equity and bond holders to require

greater rates of return to compensate for this risk. Numbers take from presentation CIBC

provided to the Leach Panel in September.

Gas and Wind Project Cost Implications

The return required of a merchant plant can increase the cost of a new gas fired plant by

$20/MWh.

o A contracted plant has a levelized costs of approximately $56/MWh.

o A merchant plant has levelized cost of approximately $75/MWh.

Limited operational hours lead to a much larger difference of a new wind plant levelized

costs to achieve a return requirement. Levelized is more than double for merchant wind.

o Contracted wind has a levelized cost of approximately $70/MWh.

o Merchant wind has a levelized cost of approximately $150/MWh.

17Investment Concerns Concluding Remarks

Wind and other renewables require both financial incentives and long-term contracts to ensure

renewable development and to lower development costs.

18Independent Analysis of Policy Options

Summary of Analytical Work

TransAlta, working with LEI, has undertaken analysis of multiple components of a greenhouse

gas and renewable energy strategy related to Alberta’s electricity sector. In the following

sections we have provided views from analysis and experience on the following elements:

A case study review of the policy experience in various jurisdictions related to GHG and

renewable policies

Modeling of four sector-wide policy scenarios for Alberta’s electricity sector including

o A carbon tax scenario

o An accelerated coal retirement scenario

o A pure renewable portfolio standard scenario

o The proposed dial down coal – dial up renewables scenario

An assessment of the impacts of early coal retirement

A review of energy efficiency policies in various jurisdictions

A review of the Pembina Institute’s report “Power to Change”

Further, while not available for this submission, we are about to undertake a macro-economic

analysis of the Alberta economy and the effects of various environmental and energy policies on

the economy, including jobs, community impacts and tax base.

19Policy Guidance from Case Studies in Other Jurisdictions

A detailed report of the experience in various jurisdictions with greenhouse gas and renewables

policies is provided in Appendix 2.

It is instructive to examine the experiences of other jurisdictions in implementing policies.

While underlying conditions are often somewhat different, the fundamental workings (and

failures) of environmental policies implemented in the past 5 - 10 years are important.

The following material represents a compilation of global experience with a number of

environmental and energy policy frameworks, with particular assessment of their applicability to

Alberta.

Specifically, we examined:

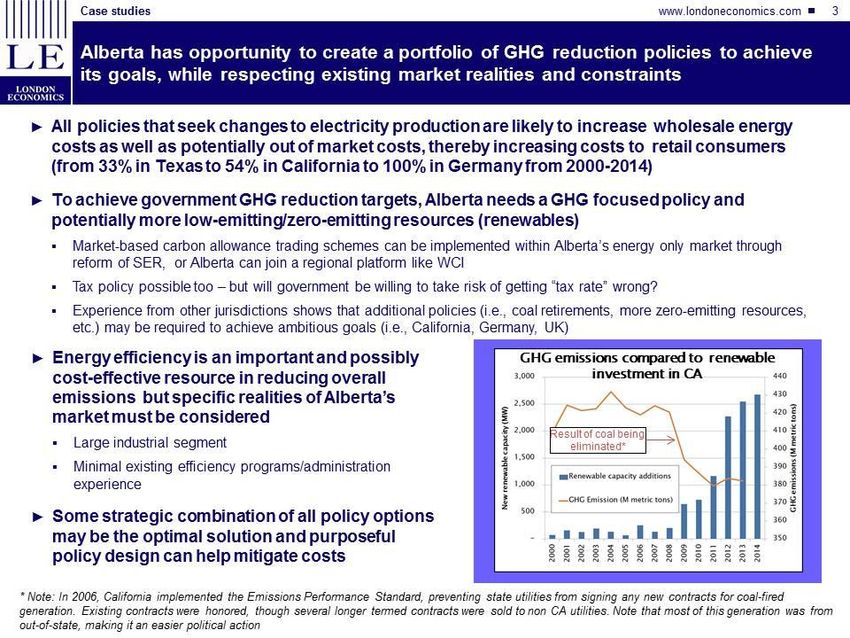

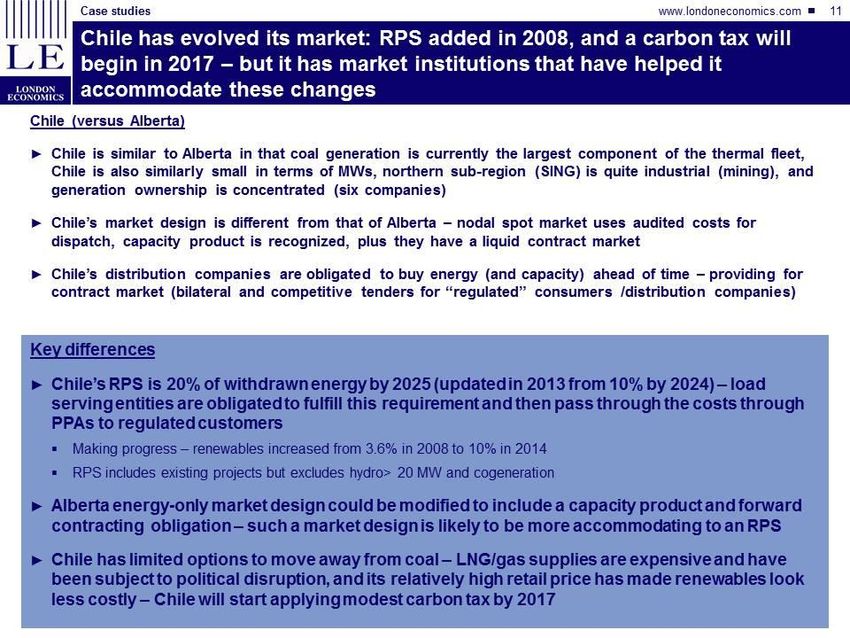

California’s cap and trade design and experience to date

The UK’s carbon levy as an example of a carbon tax

The RPS experience in Texas

Feed in tariff programs in Germany and Ontario

A large scale energy efficiency program in California

2021

22

23

24

25

26

27

28

29

30

31

32

Modeling of Various GHG policy Options

In an effort to understand the potential impacts of various greenhouse gas and renewable policies, TransAlta and LEI have modeled

four separate policy scenarios and compared those against a business-as-usual baseline, all within an Alberta context. Those scenarios

are:

A cap and trade policy framework

A policy that would accelerate the retirement of coal units from the fuel mix

A renewable portfolio standard

A Dial Down Dial Up solution

For comparability each scenario was designed in such a way as to achieve emission reductions from the entire electricity sector from a

base of 58 Mt of GHG emissions in 2015 to a target of 35 Mt in 2030.

The attached analysis describes the resulting impacts on emissions and power prices, and identifies implementation challenges should

they be implemented in Alberta. We further provide a grade assessment of each scenario in terms of their expected impacts on

consumers, government and incumbent generators.

3334

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

Early Retirement of Coal in Other Jurisdictions

One policy approach under consideration is the accelerated retirement of coal-fired generation. We believe that it’s useful to examine

the experience some jurisdictions have had with coal phase out. The attached “case studies” describe experiences in Germany,

California, Ontario, and other U.S. States.

5051

52

53

54

55

Review of Energy Efficiency Policies

Alberta has not aggressively pursued energy efficiency policies as a means of reducing energy use and thus environmental impacts

from electricity generation. There are opportunities to adopt mature approaches from other jurisdictions, cognizant that the size of

opportunity may be mitigated by the unique Alberta characteristics of Alberta’s concentrated industrial load.

The following describes several efficiency programs in the U.S. and relates their penetration rates to the Alberta context.

5657

58

59

60

61

62

63

64

65

66

67

Review of Pembina Report “Power to Change”

Detailed report is provided in Appendix 3

In 2014, the Pembina Institute issued a report on the potential for large scale transformation to the Alberta electricity system to one

with a lower emissions profile and a much greater level of renewable energy penetration. The report was useful in generating

discussion about the benefits, challenges, costs and opportunities of such an ambition.

In order to add to this constructive conversation, TransAlta and LEI undertook a review of the report in an effort to identify

improvements and deepen the level of discussion. Based on this work we also identified that the transformation alluded to in the

report would face tougher challenges than originally thought, and is perhaps overly optimistic about its potential to both reduce

emissions and grow renewable generation.

6869

70

71

72

73

74

75

76

Macro-Economic Analysis – Work in Progress

Economic Contribution of Coal-Fired Generation

In 2014 TransAlta undertook a review of the economic contribution of the coal-fired generation

sector to the Alberta economy. The work was carried out by Dr. Robert Mansell who has

authored over 100 studies on energy and regulatory issues, as well as many other studies on

regional economics.

The work was based on specific data for TransAlta’s operations. We have extrapolated that

work to reflect an approximation of the impacts of the total Alberta coal fleet by prorating based

on MW capacity. The following table provides those estimates:

Alberta Coal Generation Fleet Economic Contribution

Direct, indirect and induced effects (2015 to 2020)

GDP add to the Alberta economy $10 billion

Labour income (wages) $4.4 billion

Employment 44,500 person-years

Total federal and provincial tax income $2.6 billion

Work in Progress

TransAlta and LEI are currently undertaking a more detailed modeling of the macro-economic

impacts associated with policy scenarios. We will be using REMI’s PI+ forecasting model to

assess the Province-wide economic impacts of climate change policies in Alberta. The PI+ model

is more precise than the more conventional analysis using Input/Output multipliers from

Statistics Canada.

What is the REMI PI+ model?

For assessment of industry development and local economic implications from investment

during construction and also over the economic life of a project, LEI has leveraged the well-

known macroeconomic and policy model, PI+, developed by Regional Economic Models, Inc.

(“REMI”) based on concepts of Input-Output, Econometric, New Economic Geography, and

Computable General Equilibrium. The model has a capability to predict the complex economic

relationships between different sectors of the economy and implications of additional spending

on employment and overall economic activity in a region, including the ripple effects associated

with indirect and induced benefits, from direct spending on labor and materials and services.

We will be using the 53-sector model for Alberta, Canada that has been specifically customized

for the Alberta economy. The model relies on historical data from StatsCan’s 2011 System of

National Accounts data, and is bolstered by Canada Department of Finance’s near-term (until

772021) growth forecasts, as well as, Organization for Economic Corporation and Development’s

(“OECD’s”) long-term forecasts beyond 2021.

Why the PI+ model?

The PI+ model is a very flexible and quick modeling tool that can project the implications of

various policy and structural changes in the economy. Although the PI+ model uses the same

underlying data that drives the conventional Input/Output models of national statistical agencies

(such as Statistics Canada), REMI’s dynamic model offers the ability to understand how policy

shocks or projects change the regional economy overtime. Unlike a static model that relies on a

single demographic snapshot of the labor force and capital stock as of a specific point in time in

the past, a dynamic model provides for changes in both labor force demographics and capital

stock corresponding to changes in economic labor migration and business response to the policy

shock being studied. This is particularly important for a province like Alberta where changing

economic factors, like commodity prices, can significantly influence both the types of jobs, and

business decisions pertaining to capital and operating expenditures.

The REMI PI+ model has the capability to work in tandem with POOLMod to model the

dynamic impacts of proposed climate policy changes taking into account the electricity market

impacts that LEI has produced. Outputs from LEI’s POOLMod analysis feed into the REMI PI+

model which it can then translate into GDP impacts, tax revenue considerations, and

employment trends (see Figure 1 below).

Figure 1. Using LEI’s POOLMod in tandem with REMI’s PI+ model

LEI’s forecasts of future Alberta Power Pool conditions

• Produces forecasts of energy prices, which consumers must pay

• New generation investments create downward pressure on market

prices, but there maybe offsetting “out-of-market” costs to consumers

(including associated transmission costs, investment subsidies, etc.)

• Economic (or ‘forced’) retirements of power plants may also create job

losses that need to be accounted for

REMI PI+ model

Estimates the macroeconomic impacts

Sales and income tax

Employment Economic activity

revenues

78Key inputs and assumptions

The outputs from the electricity market modeling that will be relied upon as inputs into the

REMI PI+ modeling include the following:

(1) forecast of Alberta Pool Prices under each scenario, and other non-market costs that will

impact retail costs of electricity, and

(2) new generation capacity and retirements, as well as, additional transmission investment

under each of the five scenarios.

LEI will further supplement the above metrics with assumptions on allocation of retail costs of

electricity by customer class (relying on AESO’s Long Term Outlook forecasts), composition of

O&M jobs by technology type (to reflect how plant closures and new entry will effect utility

sector employment, as well as employment of intermediary sectors (such as coal mining and

natural gas extraction). LEI will also need to develop metrics to reflect the impact of investment

on the economy (for example, the percentage of local spending from overall capital investment

and the relative breakdown of labor versus materials spending, as associated with the installation

of new power plants and transmission lines).

79Air Quality Considerations

A detailed presentation in Appendix 4

In the Spring of 2015, TransAlta funded research on a detailed review of data associated with air

quality in the urban Edmonton airshed. This work was in response to a series of claims that coal-

fired generation units 60 kilometers west of Edmonton was a major contributor to air quality

events being observed in Edmonton, and therefore closing those units as quickly as possible was

justified.

Dr. Warren Kindzierski, PhD, PEng, with the University of Alberta School of Public Health led

the study over a period of five months. Dr. Kindzierski is a recognized author and expert in air

quality and human health effects.

The results of this work are currently being captured in an academic study and report, and will

subsequently be subject to peer review. A preliminary description and results are highlighted

below and provided in more detail in Appendix 4.

The Study

The scientific objectives of study were as follows:

Understand characteristics and trends of air pollutants, including fine particulate matter

(PM2.5)

Identify sources of PM2.5 at the National Air Pollution Surveillance (NAPS) chemical

speciation monitoring site in Edmonton

Identify contribution from coal combustion sources

Investigate origins/causes of high PM2.5 levels in Edmonton during 2010

There are multiple sources (both urban and rural) that contribute to PM2.5 in Edmonton. This

study:

Examined air quality trends, and what type of sources and how much they contribute

to PM2.5 in Edmonton, including coal combustion emissions, using receptor

modeling and backward trajectory modeling

Used methods recommended by Environment Canada, US EPA and/or preferred

by research scientists across North America and Europe:

o US EPA Positive Matrix Factorization (PMF) model

o NOAA Hybrid Single Particle Lagrangian Integrated Trajectory (HYSPLIT) model

Used data from the one air monitoring station in Edmonton (McIntyre) that

collects specialized data that allows for source identification of PM2.5

Compared to earlier studies of this type for Edmonton, this study used the largest and

most current dataset – best understanding of current conditions

80Study Findings

Based on a five-year monitoring data set and cognizant of both short range and long range

sources, the study found the following composition of PM2.5 in the Edmonton airshed:

Taken in aggregate, the study found there was only a minor signal associated

with coal combustion emissions as a portion of secondary sulphate, and estimated

to be no more than 10% of the PM2.5 contribution.

Further, the study examined trends in Edmonton’s air quality and observed the

following trends:

Hourly concentrations of nitrogen dioxide (NO2), sulfur dioxide (SO2), total hydrocarbon

(THC) and carbon monoxide (CO) have steadily decreased since 1998.

Hourly concentrations of particulate matter (PM2.5) are unchanged since 1998.

Hourly concentrations of ozone (O3) show inconsistent change.

Chemical species present in PM2.5 unchanged or decreasing (for organic carbon,

elemental carbon, barium and lead) since measurements began in 2007.

These trends – which are scientifically statistically significant – do not at all

support a notion that Edmonton, at least, will have some of the poorest air

quality in Canada.

81Additionally, the study examined an annual breakdown of levels and categories of PM2.5 in

Edmonton to determine the validity of using 2010 data as an average for particulate matter

concentrations. The chart below provides an indication that 2010 was an anomalous year in

terms of PM2.5 concentrations for a variety of reasons. Using that data to compare to other

urban centers is not valid.

Overall, the study results contribute to a better understanding of the Edmonton airshed. The

future peer review of this work will provide more confidence, but it is evident that while coal

emissions may contribute a small portion to PM2.5 concentrations, it is not a major factor and

pre-emptively eliminating coal generation west of Edmonton will not resolve Edmonton air

issues.

82Appendices

Appendix 1 - Centralia Experience

Appendix 2 - Detailed Report on Policy Case Studies

Appendix 3 - Detailed Review of the Pembina Report “Power to Change”

Appendix 4 – Detailed Presentation of Edmonton Air Quality Study

Appendix 5 – London Economics Corporate Resume

83You can also read