Teaching Finance Ethics Using the Case of the Subprime Mortgage Meltdown

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Teaching Finance Ethics Using the Case of the

Subprime Mortgage Meltdown

David S. Steingard, Saint Joseph’s University

George Webster, Saint Joseph’s University

ABSTRACT

The authors present the subprime mortgage crisis as a case for teaching

business ethics in finance, arguing that the crisis lends itself to rich,

focused moral analyses of accountability, responsibility, and reparations.

Following a description of the flow of the subprime mortgage process, the

authors offer detailed financial and ethical analyses of the specific

transactions between stakeholders at three levels, the primary market

level, the subprime loan (i.e., instrument) level, and the secondary market

level. Broader implications for teaching ethics in finance are also

discussed.

INTRODUCTION

One of the most important developments in the world of finance over the last

century has been the collapse of the subprime mortgage market. This includes the closing

of thousands of subprime lenders, the rapid rise in mortgage defaults, the severe

downturn in the housing and construction industries, the staggering losses that have been

taken by financial service firms, and the negative effect this problem has had on the

economy at large. We already have seen two hedge funds collapse, emergency Federal

Reserve-backed buyout of Bear Stearns, the collapse of IndyMac, a large California

savings bank, and Fed’s astonishing takeover of both Fannie Mae and Freddie Mac (the

two largest institutions in the secondary mortgage market). The subprime mortgage story

is replete with insights about economics and finance, as well as about business ethics and

the moral evaluation of market mechanisms.i

The subprime story, from a pedagogical point of view, is compelling on two

fronts. First, the subprime story allows finance professors to explicate the complex

interrelationships between stakeholders and financial instruments in a variety of markets.

Second, considerable negative impacts from the case allow for focused moral analyses of

accountability, responsibility, and reparations. Ethical problems and concerns throughout

this process provide finance instructors richness in teaching ethics not often found infinance. This case and the ethical conflicts contained in it are well suited for finance

courses in investment management and portfolio theory. Obviously, this material can be

introduced when discussing risk and return. It is clear that something in this market is

wrong when a portfolio manager can earn two percentage points more than a fixed

income instrument with the same rating as to risk. A tranche with an AAA rating cannot

pay 8% if a General Electric bond with the same rating pays 6%. This material also can

be introduced when applying time value of money to bonds. The same argument holds

relative to risk and return.

This paper traces these relationships: the process involved in creating the

subprime loan; bundling and selling them to banks and Wall Street firms; and the

creation, rating, and sale of collateralized debt instruments in slices (tranches) to ultimate

investors. Our desire, however, is to introduce this material at an introductory level in

order to cover all business majors and give them a foundation in ethical issues in finance.

Generally, only finance majors take upper level courses, so the only exposure to finance

and ethics for all other majors in business schools is usually at the sophomore level

introductory finance course.

OVERVIEW OF THE SUBPRIME LENDING MODEL

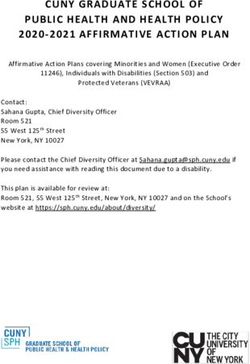

Figure 1 outlines the structure and flow of the subprime lending process.

Structure and Flow of the Subprime Lending Process

The market for mortgages is generally divided into three segments: one for those

with good or excellent credit (prime), one for those with somewhat less than good credit

(Alt-A), and one for those with poor or no credit (subprime). The “trail” begins with the

application for a mortgage with someone with poor credit through a mortgage broker.

These borrowers usually pay two or three percentage points higher than those who have

good credit. Later we will discuss “teaser” rates offered to subprime borrowers. These

rates are artificially low at first, but reset at regular intervals to higher rates.

The mortgage broker is an agent of the subprime lender and operates under a fee-

for-service arrangement with the lender. The fee is determined by the amount of the loan,

among other factors, and is earned when the loan is approved. This practice leads to what

is known as predatory lending, which will be discussed later in the paper. Mortgage

brokers handle roughly two-thirds of all subprime originations. There is no licensing

requirement or federal regulation that governs the conduct of the mortgage broker.

Page 2 of 20Subprime Mortgage Process

Home Buyers Mortgage Brokers Subprime Lenders ŅBigÓBanks

Sell bundled

Apply to É Agent for.. Debt toÉ Buy Subprime

Subprime borrower Fee for service ŅCountrywideÓ

Teaser loans Do not own loan Bundle & Sell Bundle & Resell

Lend toÉ Lend ToÉ

Sell

Subprime

& prime

Debt toÉ

Investors Bond Rating Firms Wall Street Firms

Rate repackaged

Seek high returns Rate CDO Quality (Tranche) debt (CDO) Repackage Š

CDOÕs

Buy CDOÕ

s Carved into ŅTranchesÓ for fee

Collaterized

Sell ŅTranchesÓto domestic and global investorsÉ

The subprime lender, the next institution in the process, offers a wide range of

mortgage products, including those designed for the subprime borrower. These include

no-doc loans (no income verification required) and adjustable-rate loans that do not reset

annually. An example of this is the popular 3/27 loan that resets (i.e., the interest rates

change) after an initial three-year period of a low fixed rate. Over $800 billion of

subprime mortgages were originated in 2006. Large money center banks, such as Citicorp

and UBS, routinely buy these subprime mortgages, providing a source of funding to

subprime lenders, such as Countrywide Mortgage. The subprime lenders then issue new

mortgages with this cash.

The money center banks, in turn, bundle this debt and sell to financial firms, such

as Merrill Lynch and Bear Stearns. Bundling the debt comprises combining many small

subprime mortgages into a single instrument backed by the underlying mortgages. The

aforementioned financial firms then package these securities into new securities called

mortgage backed securities (MBSes) and collaterized debt obligations (CDOs). Nearly

$2.4 trillion of these securities were issued in 2006. When a financial firm creates either a

CDO or an MBS it is necessary to assess the risk so the security can be priced and sold.

Bond rating companies, such as Moody’s and Standard & Poor’s, perform this function

for fees and provide to the issuing firm an estimate of the quality of the debt. The role of

Page 3 of 20these firms is the subject of another ethical dilemma, which will be discussed later. The

rating companies provide advice on how to slice the debt instrument into pieces, or

tranches, so as to maximize the rating of each tranche.

These instruments include a mix of traditional bonds subprime mortgages, and

home equity loans. One quarter of the $375 billion CDO market was comprised of

subprime mortgages in 2006. Finally, investors, namely, investment companies, pension

funds, hedge funds, and some banks purchase these debt instruments because they

promise higher yields than other corporate bonds with the same rating (e.g., AAA). Fund

managers, ideally, try to improve returns without accepting additional risk. These

investors are the last link in this chain. By the time it reaches the end of the chain, the

subprime mortgage, initially issued by a subprime lender, has been sold numerous times

and repackaged once or twice and been sold as one element in a tranche. This tranche has

been given a certain quality rating that may or may not bear any relation to the debt

within the tranche.

FINANCIAL AND ETHICAL ANALYSES OF SUBPRIME LENDING

As depicted in Figure 2, the following sections provide detailed financial and

ethical discussions at three of the four levels of analysis.ii The levels we discuss are the

market level, the subprime loan level, and the secondary market level.

Subprime Lending Levels of Analysis

Figure 2

4. Economic and Political Impacts Level

3. Secondary Market Level

2. Subprime Loan Level

1. Market Level

Page 4 of 20FINANCIAL ANALYSIS AT THE MARKET LEVEL

Ethics Newsline editor Carl Hausmaniii is credited in the financial industry with

coining the phrase “perfect storm” to describe the underlying financial and ethical issues

of the current prime mortgage market crisis.iv “Subprime lending” usually means lending

to borrowers with less-than-pristine credit or to those with low income or few assets. As

with any investment, there is a relationship between risk and return. Interest rates

associated with subprime lending for residential mortgages are higher than they would be

for borrowers with good credit. Subprime loans are riskier loans, in that they are made to

borrowers unable to qualify under traditional, more stringent criteria. Subprime

borrowers are generally defined as individuals with limited incomes having FICO credit

scores below 620 in a scale that ranges from 300-850. Subprime mortgage loans have a

much higher rate of default than prime mortgages and are priced based on the risk

assumed by the lender.v

The first element of the “perfect storm” involves potential problems from

differing rates and terms for mortgages. One potential problem for a borrower is that the

standard subprime mortgage is the 2/28 mortgage and not the standard 30-year fixed rate

mortgage. The initial rate is fixed for two years and then becomes variable for 28 years.

There are annual and lifetime caps on these mortgage products, although the rates can

rise annually. A variation of this mortgage is the 3/27, which functions in exactly the

same way, except the initial rate is fixed for three years instead of two years. The initial

rates on these mortgages are usually low, called “teaser” rates, but then adjust upwards as

market interest rates rise. Also, subprime mortgages usually have prepayment penalties

associated with them. According to data from the Federal National Mortgage Association

(Fannie Mae), about 80% of subprime mortgages contain prepayment penalties.

Another element of the “perfect storm” involves the policy of the Federal Reserve

Bank. Shortly after September 11, 2001, the Federal Reserve began to lower the interest

rates on the federal funds “overnight” rate (the interest rate at which Fed-member banks

lend to each other on an overnight basis). These loans are often made so that banks can

maintain legally required reserves. The Federal Reserve Bank lowered the fed funds rate

in an effort to help prevent the economy from slipping into a recession after the

September 11th attacks. After a series of fed funds rate cuts the overnight reached a low

rate of 1% by 2003. As a result, financial institutions around the world were awash in

cash. Coupling a large new market for loans in the subprime category, along with a glut

of money, helped lead to the current situation.

The subprime mortgage crisis manifests itself through liquidity problems caused

by foreclosures in the global banking system. Foreclosures have accelerated in the United

States since late 2006, triggering a global financial crisis. The crisis began when the

housing bubble burst and high default rates on subprime and other debt instruments were

offered to high-risk borrowers with low incomes or poorer credit histories than prime

borrowers.vi Borrowers, encouraged by loan incentives and a long-term trend of rising

house prices, believed they would be able to refinance at more favorable terms or “flip”

their houses. Once house prices dropped between 2006-2007, refinancing became more

difficult. Defaults and foreclosures increased dramatically as ARMs reset at much higher

rates. During 2007 nearly 1.3 million house properties were subject to foreclosure. This

was an increase of about 805,000 from 2006, almost a 62% increase.

Page 5 of 20We posit the subprime mortgage market crisis and all its attendant problems, such

as hedge fund failures, massive write-downs of assets, and a depressed housing market

are the collective result of three distinct sets of circumstances. These sets of

circumstances resemble three legs of a stool. The “seat” of this “stool” represents the

monetary effects that have reverberated through the world economy.

One leg of this stool represents the expansionary monetary policy of the Fed’s

policy arm, the Open Market Committee (FOMC). As the technology-led economic

boom of the 1990s faded, the FOMC began to aggressively cut interest rates. Having

already cut the overnight rate in 2003 to 1%, the FOMC waited until 2005 to begin to

raise them; by 2005 it was apparent that the economy was not headed for recession.

Former Fed Chairman Alan Greenspan’s purposes in raising rates were both to maintain

positive economic growth and to prevent deflation. Greenspan’s critics argue that the

result of keeping rates so low for such a long period of time resulted in a glut of savings

globally, fueling demand for houses. The glut in the money supply resulted in low long-

term loan rates. The housing market became overheated and unsustainable.

The other criticism of the Fed is they adopted a “hands-off” approach with regard

to consumer protection laws. This resulted in lax lending standards, which, in turn,

resulted in borrowers taking out mortgages they could not afford. None of the Fed’s

measures to tighten oversight were focused on the type of adjustable-rate “teaser” loans

whose growth in 2005-2006 contributed to this crisis.

The second leg of the stool represents the influence of the capital market itself.

Fannie Mae initially purchased government insured mortgages; in the late 1960s its

charter was changed to allow it to buy conventional mortgages. The federal government’s

National Mortgage Association, Ginnie Mae, was established to buy Federal Housing

Administration (FHA) and Veterans Administration (VA) loans. Finally, the Federal

Home Loan Mortgage Corporation (Freddie Mac) was created to bring more liquidity to

the nation’s thrift institutions by buying their mortgages. These government-sponsored

enterprises (GSEs) are charged with providing liquidity to the prime mortgage market by

buying mortgages. They finance, in the main, by issuing bonds. This secondary market

now buys about two-thirds of all new mortgages issued and collectively hold over $5

trillion of total mortgages.vii The GSEs hold some of the purchased mortgages on their

own balance sheets; however, they also have begun to securitize mortgages and sell them

into the capital market. They do this by packaging these mortgages into bundles where

risks are also pooled. These securities, called collateralized mortgage obligations, or

CMOs, are sold directly to investors. The GSEs do not play as much of a role in the

subprime mortgage market as they do in the prime mortgage market.

Many subprime mortgages do not meet the standards of Fannie Mae, Ginnie Mae,

and Freddie Mac, so the GSEs do not purchase these mortgages as readily as they do

prime-mortgage loans. Many subprime loans have high loan-to-value rates (due to low

down payments by borrowers), have “piggyback loans” or otherwise do not conform to

GSE standards. In these cases, the GSEs will not purchase the loans. Due to a form of

financial engineering called securitization many mortgage lenders had sold the rights to

those payments and related credit/default risk to third-party investors via mortgage-

backed securities (MBSes) and collateralized debt obligations (CDOs). Investors holding

these securities faced significant losses as the value of the underlying mortgage assets

declined.viii

Page 6 of 20The third and final leg of our “stool” was rapid house price appreciation. As long

as houses gained in value year after year, the effects of resetting the rates paid on

adjustable rate mortgages by two to four percentage points was negligible. It was simply

a matter of selling the house every two to three years and repeating the process. Due to

factors discussed earlier like the Fed’s actions), no-documentation loans, high loan-to-

value ratios, and teaser rates, homeownership rates dramatically increased. Ownership

rates jumped from 64 to 69 percent of households from 1994-2005. The rates for blacks

jumped from 42 to 49 percent and for Hispanics from 42 to 50 percent of households.

Low and moderate income households (i.e., subprime borrowers) were at the center of

this ownership boomix. In 1994 subprime originations were $35 billion, representing 55%

of total originations; by 2005, subprime originations were $35 billion, or 20% of total

originations. Further, house prices were rising, permitting borrowers who had trouble

paying the mortgage to sell the house, pay any prepayment penalties, and walk away.

Home prices in the United States increased approximately 80%, or over 12%, per

year from 2000-2006. In certain locations, prices rose much faster than the national

average. In California, for example, house prices rose about 160% (or 20% per year) over

the same period. The housing boom benefited from lax lending standards and growth in

the non-agency secondary market.x The increase in house prices was also fueled by a big

drop in interest rates due to Fed action. Rates fell on both fixed-rate and variable-rate

mortgages from about 10% in 2000 to just over 7% in 2004; this corresponds to the

easing policy following the recession of late 2000. Finally, new mortgage products

allowed borrowers to stretch their payments to purchase homes priced higher than they

normally could afford.

Overbuilding during the boom period, increasing foreclosure rates, and

unwillingness of many homeowners to sell at reduced market prices increased the supply

of housing inventory. Volume (units) of new homes dropped by 26.7% compared to a

year earlier. By January 2008, the average house stood unsold for 9.8 months, the highest

level since 1981.xi. Further, four million homes were unsold, including 2.9 million that

were vacant.xii This excess supply exerted significant downward pressure on prices. As

prices fell, more homeowners were at risk of default. According to Standard &

Poor’s/Case-Schiller Housing Price Indices, by November 2007 average prices were off

8% from their peak in 2006.xiii.

Unfortunately, much of the mortgage lending of the past several years, as well as

investments in mortgage-backed securities and other debt instruments, was predicated on

a set of narrow assumptions. Unemployment was assumed to stay low, interest rates were

forecast to stay flat and home prices were expected to continue rising 10% annually. In

other words, the three legs of the stool were assumed to remain stable.

In fact this has not happened. First, unemployment has inched up from about

4.5% in when 2006 to 6.1% in August 2008. This has caused a shift in demand for houses

leading to the most drastic reduction in house prices in recent memory. The Standard and

Poor’s/Case-Schiller U.S. Home Price Indices has shown at least an 8% increase each

year since 2001, but recently has fallen 6% in 2007.xv They forecast another 7% decline

in 2008.xvi Moody’s forecasts an overall decline of 12.3%, nationwide, from peak 2006

2nd quarter to 2009 1st quarter.xvii Housing starts have fallen from a seasonally adjusted

annual rate of over 2.1 million in 2005 to about half that at the beginning of 2007.xviii

Page 7 of 20Other factors, in addition to the ones discussed here, have fueled this crisis. For

instance, a George Mason University professor opinedxix, “There has been plenty of talk

about ‘predatory lending’ but ‘predatory borrowing’ may have been the bigger problem.”

According to one studyxx, as much as 70% of recent early payment defaults had

fraudulent misrepresentations on their original loan applications. The study looked at

more than three million loans from 1997-2006, with a majority from 2005 and 2006.

Applications with misrepresentations were five times as likely to go into default. Many of

the frauds were simple; in some cases borrowers simply lied about their income. Other

borrowers falsified income documents by using computerized applications.xxi

Another contributor to the subprime crisis involves the construction industry.

Severe contraction in the construction industry has resulted in more layoffs; the economy

has experienced net job losses each month between February and April 2008. According

to First American Loan Performance company data, 12.5 % of subprime loans made in

2002 had foreclosed by May 2005. In 2006, 1.2 million household loans were foreclosed,

an increase of 42% from the previous year. The firm estimates another two million

foreclosures in 2007 and more than that in 2008, when 2.5 million ARMs will be reset to

higher rates.xxii

The increase in foreclosures has triggered huge losses in the financial services

industry. Since mortgages were bundled and sold to banks and other investors, the value

of those securities has fallen as well. Total write-downs by banks, brokerage firms, hedge

funds, and other institutions in the meltdown totaled almost $108 billion in 2007.xxiii

Predictions made in 2006 for 2007 and 2008 include the following: two million

foreclosures, an additional $150-200 billion in housing-related losses, $2-3 trillion loss in

household wealth due to a 10% decline in house prices, and $1 billion loss in local

property tax revenue from property devaluation.xxiv

Indeed, a perfect storm has arisen, resulting in huge losses everywhere in the

economy. Some of this has been the result of market forces; some of it has been the result

of greed on the part of many market participants. Consequently, ethical questions have

been raised in conjunction with this crisis.

ETHICAL ANALYSIS AT THE MARKET LEVEL

Identifying ethical issues at the market level of analysis is challenging. Individual

culpability for making unethical decisions does not exist at this level. Most of these

dynamics occur at a societal level. For example, a widespread belief that the housing

market would continue to grow at a 10% annual rate cannot be linked to the agency of an

individual. Similarly, a shared social belief that consumer income growth would rise to

match an increasing cost of living, namely housing costs, is not any individual’s

responsibility. Economic forecasts, perhaps tainted with some “irrational exuberance”xxv,

were perhaps overly optimistic, but not morally irresponsible. It would be difficult to

attach a moral judgment to something as amorphous as the market.

However, some moral accountability can be attributed to key players who shape

the market. Critics of Alan Greenspan suggest he was at fault for keeping interest rates

low, provoking much of the subprime crisis. Unlike many stakeholders in the subprime

story, Greenspan had direct control over decisions (e.g., mandating the interest rate) with

largely knowable impacts. Whether or not he used poor judgment in making these

decisions is a moral question of gatekeeping responsibility. Others blame the government

Page 8 of 20for an overly generous laissez-faire policy about regulating subprime market dynamics.

The government, in this case, is charged with making certain decisions affecting

regulation; again, how effectively they regulated is a moral question of gatekeeping

responsibility.

The unprecedented degree to which the government has bailed out subprime

disaster companies like Bear Stearns, IndyMac, Freddie Mac, and Fannie Mae may make

the government morally complicit in producing economic conditions from which

subprime loans spawned. This shifts the liability of the financial fallout from subprime

loans from private corporations who did not profit (but expected to) to the public. Of

course, government bailouts are based on the assumption that keeping the financial

system afloat, even if it means making handouts to profit-seeking corporations, is

necessary to maintain financial stability for the public good. Essentially, helping a few

corporations during tough times is a small price to pay for a widespread collapse of the

financial system.

It is reasonable to argue that the government basically let the market overinflate

and is responsible for its burst. That they have been so munificent in bailing out failing

financial institutions as well as in helping consumers may be an indication of fulfilling

some duty to repair what they helped break. Overall, though, attributing all of the

responsibility onto the Federal Reserve Bank or the United States Government is too

simplistic. The complexity of the economic situation preceding the subprime crisis is well

beyond the scope of what any individual stakeholder could generate of their own accord.

Also, mortgage brokers would have it in their best interests to encourage

mortgage consumers to take on riskier loans, predicated on the assumption that housing

values and real income would increase. Again, assigning moral indiscretion to individual

mortgage brokers who used the best available public information to counsel clients would

be unsubstantiated. Most of the individual actors in the subprime mortgage meltdown did

not directly contribute to artificially or illegitimately creating market performance

assumptions that led to the subprime meltdown. As we analyze their behavior at the

subprime and secondary market levels, however, we will see how many of them

inappropriately exploited the economic zealousness that fueled the subprime crisis.

Hausman’s idea of a “perfect storm”xxvi applies at this level of analysis., Societal

belief in continuous prosperity reflects, paradoxically, a healthy hope in human progress,

as well as an unfounded belief in sustained growth. A fine line exists between healthy

optimism for a better future and a greed that can rationalize away the reality of negative

downturns. Is it plausible to assign moral blame to an entire society for irresponsibly

advancing a halcyon economic outlook amidst obvious signs of trouble? No. Yet, as we

will see in subsequent sections, are specific ethical incursions by individual actors acting

within these market assumptions. Analogously, nobody in particular created the rules of

the game, but some of the players interpreted or ignored the rules in ways that harmed

others.

FINANCIAL ANALYSIS AT THE SUBPRIME LOAN LEVEL

The subprime mortgage market is organized around a broad base of mortgage

brokers and “net branches.” Regulation of these brokers is enforced at the state level and

is patchwork at best; neither licensing nor formal training is required. The trick in the

Page 9 of 20business is to outsource sales to these brokers and salesmen, as New Century financial

did. New Century maintained a network of 47,000 mortgage brokers and 222 branch

offices to grow to almost $60 billion in loans in 2006. Fremont Financial Corporation, for

their part, originated over $36 billion in loans the same year.

The potential problem for the borrower is that, unlike the standard 30-year fixed

rate mortgage, the standard subprime mortgage is the 2/28 mortgage. The initial rate is

fixed for two years and then becomes variable for twenty eight years. There are annual

and lifetime caps on these mortgage products but the rates can rise annually to the

borrower.

A variation of this mortgage is the 3/27, which functions in exactly the same way

as the 2/28, except that the initial rate is fixed for three years instead of two years. The

initial rates on these mortgages are usually low, called “teaser” rates, but then adjust

upwards as market interest rates rise. A typical mortgage is reset to five percentage points

over the London Interbank Offered Rate, which is based on the demand for and supply of

Eurodollars (dollar-denominated deposits in European banks). Subprime mortgages also

usually have prepayment penalties associated with them. According to data from the

Federal National Mortgage Association (Fannie Mae) about 80% of subprime mortgages

contain prepayment penalties.

Other popular mortgages issued in this market are the “interest-only” loans, which

allow borrowers to pay interest only for a period of time, and the “pick-a-payment,” for

which borrowers pick a monthly payment they can afford. Many times these loans result

in negative amortization, where the monthly payments are not high enough to reduce the

balance of the loan. The system is based on rewards for the broker for simply closing the

loan. The broker will not own the loan nor will he or she service it. There are incentives

in such cases to sell a loan that is either larger than the borrower needs or one that the

borrower cannot afford. Often, there was outright deception and fraud on the part of the

broker just so the loan could be originated.

The subprime mortgage crisis is an ongoing economic problem that manifests

itself through liquidity problems in the global banking system due to accelerating. The

crisis began when the housing bubble burst and high default rates on subprime and other

debt instruments that were made to high risk borrowers with low income or poorer credit

history than prime borrowers.xxvii Loan incentives and a long term trend of rising house

prices encouraged borrowers to borrow, believing that they would either be able to

refinance at more favorable terms or “flip” the house. Once house prices dropped in

2006-2007 refinancing became more difficult. Defaults and foreclosures increased

dramatically as ARMs reset at much higher rates.

ETHICAL ANALYSIS AT THE SUBPRIME LOAN LEVEL

Unlike at the market level, moral accountability will be easier to assign at the

subprime level because of specific fiduciary relationships between mortgage lenders,

consumers, and brokers. As the linchpin between consumers and lenders, mortgage

brokers are caught in a natural, two-fold conflict of interestxxix. First, they are morally

obligated to faithfully represent the true financial capacity and credit history of the

consumer to the lender. Second, they are morally obligated to communicate to consumers

the terms and conditions of a mortgage in a transparent and understandable manner. An

Page 10 of 20accurate rendition of a consumer’s ability to afford a loan is essential to the financial

well-being of the consumer and the lender. If consumers obtain loans they are incapable

of maintaining, they will jeopardize their living arrangement and credit score.

Inconsistent payments or foreclosures from consumers are detrimental to the viability of a

lending institution. Consumers are obligated to represent their ability to pay loans in an

honest manner. Although perhaps not as directly responsible as brokers, lenders are

morally obligated to sell loans that are within the means of consumers to pay off. Their

conflict of interest is usually mitigated because it is in the lenders’ best interest to have a

viable consumer; lenders do not profit when consumers inconsistently pay or are

foreclosed.

Our earlier analysis of the market assumptions undergirding the subprime

mortgage meltdown suggested that pinpointing moral culpability for a collective belief in

an overvalued market was implausible. Addressing moral failings at the transactional

level of the subprime mortgage itself, however, is considerably easier. Each of the players

in the transaction had particular duties to be truthful and transparent; both of these values

were frequently undermined. Let’s examine them in turn.

The promise of continuing economic prosperity, the lowest Fed interest rates in

its history, and the massive swell in subprime mortgages, made fulfilling the dream of

home ownership a reality for millions of Americans previously economically ostracized.

People with poorer credit, lower incomes, and minimal or no collateral suddenly had

access to subprime loans and homes they could purchase. Evaluating one’s

creditworthiness for a loan involves careful scrutiny of one’s credit history and future

income stream. Providing any loan is a risky proposition; providing it to an

inexperienced, new subprime consumer is manifold times riskier. Reports of consumers

overinflating and fabricating subprime loan applications are not incidental. Some

estimates suggest falsified information appeared as much as 50% of the time on

consumers’ loan applicationsxxx Clearly, many consumers, perhaps falsely emboldened

by the ease of capital acquisition, were not truthful on their loan applications. In good

times, consumers are more honest about their ability to be financially responsible. Yet, it

is also worth noting that consumers also have a very strong self-interest in obtaining a

loan they can manage; it is safe to assume consumers do not wittingly desire to have

monthly mortgage payment stress and possible foreclosure. Historically, many consumers

have worked diligently to represent themselves fairly so they could obtain loans within

their means. Nonetheless, falsification in applying for a subprime loan is morally wrong.

Applying the criteria of truthfulness and transparency to mortgage brokers reveals

another dimension of ethical challenge. Unlike consumers, who face consequences when

procuring an unmanageable loan, brokers are not held to account. Brokers’ commissions

are generated at the time consumers sign subprime loans; after the initiation of the loan,

the broker is out of the picture. This fundamental moral problem, called a moral

hazardxxxi in economics, absolves the broker of any financial liability for fallout from the

loan they brokered; whether the consumer successfully maintains the subprime loan or

fails miserably, there is no effect on the broker. Nevertheless, a broker is always mired in

a conflict of interest between having their consumer clients sign any loan and signing a

good loan. Although brokers have a professional responsibility to uphold the best

interests of the consumer, that it makes no difference to the broker the outcome of the

loan, the temptation to “get the deal” and not care about the consequences is endemic to

Page 11 of 20the transaction. Evidence from the subprime loan debacle suggests that many brokers

routinely turned a blind eye to consumers’ loan applications’ over inflation of income and

even encouraged consumers to falsify information. Some brokers not only ignored

falsified information, but exploited the ignorance of borrowers about the risks of

potentially harmful aspects of the loan (e.g., adjustable rates and balloon payments).

Moreover, this exploitation of consumers jeopardizes the foundation of the

relationship between brokers and lenders. Lenders rely on brokers to produce loan

applicants who are viable candidates for upholding loan agreements. Again, because of

the moral hazard associated with the role of the broker in the subprime loan transaction,

they have few compelling reasons to heavily scrutinize consumers and to produce loans

with a high probability of repayment. Certainly, the basic agent-principlexxxii relationship

between the broker, the consumer, and the lender ought to be upheld; economic

functioning depends on good-faith efforts by market participants to consider the well

being of those they are representing. Yet, the lack of real consequences for brokers

brokering bad subprime deals offers a temptation to let their self-interest prevail: Why

should brokers care about the viability of the loans they broker? Of course, their

individual reputations and the collective reputations of brokers in general have been

compromised; also, trust with consumers and lenders have been shattered in light of

myriad bad subprime loan deals.

Furthermore, the collapse of the consumer mortgage industry boom—both prime

and subprime—has left many of these brokers unemployed. Ironically, some brokers

seemingly elude the moral hazard of the transaction (i.e., the consumers and lenders in

trouble), yet the collective failure of the subprime market cycles back to them. Joint

deleterious actions by a group of stakeholders can have harsh consequences affecting a

wide variety of stakeholders, including the stakeholder group provoking the problem in

the first place.xxxiii Regardless of this temptation to eschew their basic duties, brokers who

knowingly broker subprime loans through conscious manipulation and lack of oversight

are morally at fault for their harmful actions.

While lenders are generally considered to have received the brunt end of the

subprime collapse, they also have moral responsibilities they might have not attended to

properly. How effectively did banks scrutinize loan applications stewarded by brokers

after evident data about serious problems on applications became legion? Lenders’ self-

interest in signing as many loans as possible may have attenuated protocols designed to

filter out bad loan applications, on income, credit history, and the value of the property

itself.

In addition to analyzing the obligations of consumers, brokers, and lenders, it is

worth taking a moment to examine the basic nature of the subprime loan, in and of itself,

as an ethical financial instrument. By nature, the subprime loan is endemically dangerous;

it expands the risk level for home mortgage borrowing to riskier segments of the overall

mortgage lending market. More late payments and foreclosures are expected with such a

product. On the other hand, the ability for lower-income borrowers to obtain home

ownership through a subprime loan reflects fulfillment of a basic right and need; secure,

affordable housing is a morally justifiable pursuit. Analogously, we can liken the

subprime loan to a gun. Placed in the right hands, it can serve a social good; placed in

the wrong hands it can lead to very unfavorable outcomes. As a product, then, the

subprime loan requires a great deal of care if it is to serve the noble purpose for which is

Page 12 of 20was intended. As described throughout this paper, however, the almost unregulated

context for subprime loans, coupled with serious conflicts of interest and an empty agent-

principle relationship, may construe the subprime loan product to be morally flawed.

FINANCIAL ANALYSIS OF THE SECONDARY MARKET LEVEL

At the secondary market level a fundamental change involving the large banks,

Wall Street firms, and the bond rating companies helped fuel the crisis. Fannie Mae

initially purchased government-insured mortgages, but in the late 1960s its charter was

changed to allow it to buy conventional mortgages. The government National Mortgage

Association, known as Ginnie Mae, was established to buy Federal Housing

Administration (FHA) and Veterans Administration (VA) loans. Finally the Federal

Home Loan Mortgage Corporation (Freddie Mac) was created to bring more liquidity to

the nation’s thrift institutions by buying their mortgages. All of these institutions are

referred to as government sponsored enterprises (GSEs). They are all charged with

providing liquidity to the prime mortgage market by buying mortgages. They finance, in

the main, by issuing bonds.This secondary market now buys about two thirds of all new

mortgages issued and together holds over $5 trillion of total mortgages.xxxiv The GSEs

hold some of the purchased mortgages on their own balance sheets but also have begun to

securitize mortgages and sell them into the capital market. They do this by packaging

these mortgages into bundles where risks are also pooled. These securities (collateralized

mortgage obligations or CMOs) are sold directly to investors. The GSEs do not play as

much of a role in the subprime mortgage market as they do in the prime mortgage

market. Many subprime mortgages do not meet the standards of Fannie Mae, Ginnae

Mae, and Freddie Mac so the GSE’s do not purchase these mortgages as automatically as

they do prime mortgage loans. Many subprime loans that have high loan-to-value rates,

due to low down payments by borrowers, have “piggyback loans” (essentially borrowing

the down payment), or are otherwise “nonconforming” to GSE standards. In these cases

the GSEs will not purchase the loans. Due to a form of financial engineering called

securitization many mortgage lenders had sold the rights to those payments and related

credit/default risk to third party investors via mortgage backed securities (MBSes) and

collateralized debt obligations (CDOs). Investors holding these securities faced

significant losses as the value of the underlying mortgage assets declined.xxxv

Many large financial institutions, including banks and other Wall Street financial

firms have replaced the GSEs; however, large lenders and other financial intermediaries

buy and pool subprime loans and/or merge subprime loans with prime loans into new

securities that diversify risk. These securities are sold directly to investors who can resell

to hedge funds, pension funds, and foreign investors, including banks. These instruments

are combined with other forms of debt, such as car loans or credit card debt, and sold as

collateralized debt instruments (CDOs). All that is necessary to do this is to be able to

price these instruments according to the level of risk. Enter the bond rating agencies.

In order to package and resell subprime mortgages it is necessary to evaluate the risks

associated with buying the securities.

The three rating agencies, Standard and Poor’s, Moody’s Investor Services, and

Fitch Group, Inc., began to rate the issued debt considered to be subprime. Unrated

subprime debt could not be priced and, therefore, could not be sold. The rating agencies

Page 13 of 20enabled the CMO and CDO markets to expand by virtue of their assessment of

creditworthiness of the debt being sold. Banks and other financial institutions typically

create CMOs and CDOs by bundling 100s of bonds and other securities, such as credit

card loans and car loans. These instruments also include mortgages, some of which are

subprime.

The credit rating companies help the financial institutions divide the CDOs into

tranches. Each tranche receives a separate credit rating from AAA (highest credit rating)

to unrated equity (lowest credit rating, or junk). The higher the rating on the debt, the

lower the risk and the easier it is to sell on the market. The rating agencies advise the

financial institutions on how to maximize the size of the tranche with the highest (AAA)

credit rating. In fact, they are paid by the financial institutions to do this. Charles

Calomiris, an expert on CDO finance and a professor at Columbia University comments:

“It’s important to understand that unlike in the corporate bond market, in the

securitization market, the rating agencies run the show. This is not a passive process of

rating corporate debt. This is a financial engineering business.”

Top-rated tranches receive an AAA rating. Riskier tranches receive an investment

rating down to BBB and the riskiest tranches go unrated. Unrated tranches are referred to

as equity tranches or “toxic waste.” The returns to the tranche are at a fixed spread over

LIBOR (the London Interbank Offered Rate). Changes in interest rates do not affect their

value in the same way that a change in interest rates affects a fixed-rate bond. If the

LIBOR rate rises, then the rate on the tranche also rises.

Two major problems exist in evaluating the worth of a CDO. First, CDOs are not

regulated by anyone and, second, it is difficult to find out what is in the CDO. Most are

sold in private placement (no transparent market exists) and values of these CDOs are not

made public. The entire market relies on the rating firms to assess the quality of the CDO.

What is clear is the fact that the rating agencies make enormous profits from structured

finance ratings. Fees are two to three times the fees charged to rate a corporate bond.

Finally, in this vein, the rating agencies grossly underestimated the chance of

default in subprime mortgages. At default, cash flows from debt repayment were not

enough to make full interest payments to even the highest rated tranches. As a result, the

lower-rated tranches became worthless. Even some AAA-rated tranches were worthless;

many took on losses, indicating they should not have been given an AAA rating initially.

ETHICAL ANALYSIS AT THE SECONDARY MARKET LEVEL

As we have seen in the preceding section, subprime loan failures have grim

consequences for consumers and lenders, while brokers generally escape unscathed.

Effects at the subprime loan transactions level have exponentially compounded effects at

the secondary market level.

If troubled subprime loans were contained between consumers, brokers, and

lenders, then the crisis would be significantly mitigated. Bad subprime loans would be

less prevalent if lenders actually kept the loans they provided to subprime applicants.

That is, lenders who maintain ownership of loans would work diligently to insure that

consumers and brokers are honest and produce loans on which the lenders can profit.

This is a natural check-and-balance structured upon lenders’ self-interests; however,

Page 14 of 20during the subprime crisis, lenders misrepresented these loans to private financial

institutions who, in turn, bundled them into MBSes and CDOs for investors.

Revisiting our analysis of the moral hazard at the subprime loan level, we see that

lenders at the secondary market level also have no incentive to insure the quality of the

subprime loans they provide to consumers. Often, these loans do not remain in the

lenders’ possession until the point when consumers have difficulty in repayment due to

personally adverse economic circumstances (e.g., job loss), adjustable rates resetting, or

simply the fact the loans were not calibrated within consumers’ means in the first place.

While the subprime loan is passed on to the private financial institutions, this

“hot potato” does not stop scalding there. Bundles of the loans into MBSes and CDOs

ultimately land in the hands of a wide variety of private investors, corporations, and

public institutions, domestically and globally. Again, the moral hazard and agent-

principle concepts apply here. Private institutions have a fiduciary responsibility to sell

their investors investments transparent in their construction and to estimate risk as

honestly as possible. The complexity and newness of these consolidated investment

vehicles make it difficult for financial institutions to accurately portray the investment.

Are they ethically responsible for selling investments that ended up performing so

miserably? Is it reasonable to expect sellers of MBSes and CDOs to warn investors of the

potential pitfalls of such a volatile product? It could be that overall societal enthusiasm

for boom times helped assuage any doubts that subprime loans might have fatal flaws;

nobody really knew how noxious these investments could be because all stakeholders

were blissfully, but dangerously, trapped in a bubble about to burst.

In spite of this rationalization, there are at least two stakeholder situations at the

secondary market level where we can assign moral culpability. First, several cases have

occurred where private financial institutions both encouraged investors (their clients) to

invest in subprime backed securities, taking a considerable loss, while simultaneously

divesting these loans from their own institutional portfolios at an enormous profit. There

is a clear conflict of interest here; knowingly directing your clients to invest in a product

that you have abandoned because it is faltering is not morally justifiable. Second, the role

of the ratings agencies in the process of the validating the worthiness of these

consolidated subprime investments is morally suspect. Ideally, rating agencies are

impartial judges of an investment’s value and risk. Arguably, rating agencies violated

their core duty to assure the public trust by not thoroughly investigating the convoluted

nature of the consolidated subprime investments. Unlike with bonds, stocks, companies,

and other more straightforward evaluations, accurately estimating the viability of

consolidated subprime investments is practically impossible. They are just too complex to

understand enough to advance a reasonable adjudication of their worth.

Adding to this complexity was a unique conflict of interest on the part of

organizations like Moody’s regarding excessive fees demanded of private financial

institutions for evaluating subprime investments. These fees, which could be three times

the normal rate for evaluating securities, definitely influenced unsubstantiated favorable

ratings for some MBSes and CDOs; self-interest prevailed over realistic valuations.

The fact that private financial institutions had knowledge of failing subprime-

based investments, and sold them to investors anyway, makes them morally responsible

for the harm done to those investors. Rationalizations offered by ratings agencies about

following a reasonable set of assumptions in evaluating subprime-based securities are

Page 15 of 20ethically unsound. Given they were dealing with a new type of security, ratings agencies

should have been extra cautious, altering conventional ratings methodologies

accordingly. For example, ratings agencies presumed the previous ten years of 10%

annual growth would continue unabated. It can be argued that this presumption

conveniently undermined a conservative and prudent forecast, especially for an untested

and inherently risky product. Likewise, disregarding the possibility that income may not

actually keep up with housing market growth is dubious. In both of these instances,

ratings agencies may have consciously focused on too narrow of historical assumptions;

they may have only marshaled that evidence that inflated the value of subprime-backed

securities. Ratings agencies have a critical gatekeeping obligation to present untainted,

truthful financial evaluations to society. Ethical justifications by ratings agencies that

their methodologies were conceived on sound assumptions are morally suspect. Ratings

agencies who eschewed their duties to provide accurate evaluations for investors are

morally responsible for a good part of the damage related to the subprime mortgage

meltdown.

Aside from the particular instances noted above, where private institutions and

ratings agencies violated their obligation to be truthful to investors, the bulk of the

tragedy surrounding the subprime mortgage meltdown is not attributable to individual

actors. As we discussed in the earlier market level analysis section, much of the frenzy

for consolidated investments based on subprime loans was legitimately motivated by

broader, promising economic conditions and forecasts. In a sense, then, the subprime

crisis is really a failing of society—functionally, by business and government at the

institutional level—to detect the inevitable economic collapse based on the faltering

subprime mortgage loan instrument. All of the stakeholders played an important part in

contributing to the crash, but no stakeholder in particular can be held entirely responsible.

PROGNOSTICATION ABOUT THE FUTURE OF THE SUBPRIME MORTGAGE

MELTDOWN

As we move into the fourth quarter of 2008 the evidence on the root causes of the

subprime crisis suggests there is more pain to come. To date, we have witnessed nine

bank failures, a forced fire sale of Bear Stearns at $10 per share, the collapse of two

hedge funds, Freddie Mac and Fannie Mae government takeovers, and trouble that

extends to the thrift industry. The financial service industry has written off over $300

billion since 2006 and no one is certain of how much more will be written off; no one is

certain how much the debt is worth. Savings and loan banks, combined wrote off $8.8

billion in the fourth quarter of 2007 and over $46 billion for the first half of 2008. The

Federal Deposit Insurance Fund has lost $8 billion (or over 15%) in one year. Over 100

banks are on the FDIC’s watch list. of banks it considers to be in some financial distress.

Profits at FDIC-insured banks fell by 86% during the second quarter of 2008.xxxvi Over

the next year the financial services industry will continue to experience its most severe

crisis in 30 years; already almost six quarters of earnings have been wiped out.xxxvii

At the housing industry level, as of May, 2008 there were 4.5 million homes on

the market. This represents an 11-month supply.xxxviii Total real estate assets lost $435

billion in value and financial assets lost $1.3 trillion.xxxix

Page 16 of 20The loss is just as severe on a personal level. Moody’s forecasts home prices to

fall by 12.3% by first quarter of 2009 from 2006. Housing starts have been halved from

the level in 2007. In 2008, 2.5 million adjustable rate mortgages will reset to higher rates

because mortgage rates have risen to over 6.255 for 30-year fixed.xl Analysts’

predictions include for two million foreclosures in 2008-2009 and a loss in household

wealth of between $2-3 trillion due to a 10% decline in house prices. Estimates of

property tax losses are about $1 billion.xli

INSIGHTS ABOUT TEACHING ETHICS IN FINANCE

Analysis of the subprime mortgage meltdown in this paper offers many insights

for finance professors who desire to integrate more ethics into their pedagogy. In addition

to a specific analysis of the particular subprime case study, there are a number of useful,

more general conclusions about the healthy functioning of markets and the fundamental

ethical preconditions necessary for them. These can be integrated and applied in any

teaching related to markets, economics, and finance:

1. Transparency: Misinformation leads to misinformed choices and harmful

consequences. Of course, how much information to disclose, ignore, or obfuscate,

even fabricate, and to whom are weighty moral questions. At the very least,

however, stakeholders have a right to know information that could have material

impacts on the consequences of their decisions.

2. The rights of capital: Making a profit and maintaining competitive advantage is

always constrained by a basic moral duty to be trustworthy and not manipulate

others for personal gain.xliv An absence of deception is necessary to establish trust.

Free-market systems are, in essence, not totally free; they depend upon a solid

moral foundation to function properly.

3. Fiduciary responsibility and gatekeeping: All stakeholders in a market situation

have obligations to limit their self-interest by considering moral impacts of their

actions on others. Certain stakeholders, as we have seen with brokers and ratings

agencies in the subprime case, have additional duties to be accountable to specific

parties (agent-principle relationship) and society at large (gatekeeping).

4. Risk and return: All economic decisions involve calculations of risk and return.

As illuminated in the subprime case, there are degrees of moral responsibility

associated with both distributing (selling) and receiving (purchasing) risk.

Determining a standard of reasonableness is a critical skill of moral adjudication

as it relates to risk and return. Potential for a moral hazard ought to be related to

risk-and-return calculations, although frequently is not.

In addition to moral learnings explicated throughout the case, we have provided

some basic definitions of ethical concepts in the endnotes for the paper. All of these can

be employed by finance professors to enhance pedagogical discussions of ethics related

to finance. We hope finance professors will continue to evolve in their pedagogy the

financial and ethical analyses presented here.

Page 17 of 20Endnotes

i

“Moral” and “ethical” are used interchangeably throughout the paper.

ii

We do not include explication of the fourth level of analysis or the systemic

nature of the levels due to space considerations of this manuscript.

iii

http://www.globalethics.org/newsline/2007/08/27/subprime-lending-subpar-

ethics-and-the-perfect-storm/

iv

Shiller, Robert J. (2008). The Subprime Solution: How Today's Global

Financial Crisis Happened and What to Do about It.

v

http://en.wikipedia.org/wiki/Subprime.

vi

Subprime Mortgage Crisis, episode 0629007, Bill Moyers Journal, PBS,

6/29/07.

vii

Tabulated from Home Mortgage Disclosure Act (HMDA) data 2005.

viii

Ibid, Bill Moyer’s Journal.

ix

Source: U.S. Census Bureau data.

x

Data From Moody’s: economy.com.

xi

The Boston Consulting Group, “Investment banking and Capital Markets

Report,” 11/07.

xii

Census Bureau Reports on Residential Vacancies and Home Onwership,

U.S. Census Bureau, 10/26/07.

xiii

America’s Economy, 2008.

xv

Data from Standard and Poor’s, 2007.

xvi

Ibid.

xvii

Moody’s Economy.com.

xviii

Source: Commerce Department.

xix

January 13, 2008 column in the New York Times.

xx

BasePoint Analytics.

xxi

New York Times.com.

Page 18 of 20xxii

Bureau of labor Statistics, 2007.

xxiii

Data from: http://services.Inquirer.Net, article id = 101568.

xxiv

Source; David Gaffon, WSJ.com.

xxv

Shiller, Robert J. (2005). Irrational Exuberance.

xxvi

http://www.globalethics.org/newsline/2007/08/27/subprime-lending-subpar-

ethics-and-the-perfect-storm/

xxvii

Bill Moyer’s Journal, episode 06292007, PBS, 6/29/07.

xxix

A “conflict of interest” is defined as a: “…situation in which one’s ethical or

legal duties as an employee or professional conflict with one’s personal

interests. Even the appearance of a conflict of interest can undermine the

integrity or trust that must often be presupposed in business situations.”

Source: DesJardins, Joseph. (2008). An Introduction to Business Ethics

(Third Edition).

xxx

Wall Street Journal, 2007.

xxxi

A “moral hazard” is defined as: “One of two main sorts of market failures

often associated with the provision of insurance. Moral hazard means that

people with insurance may take greater risks than they would do without it

because they know they are protected, so the insurer may get more claims

than it bargained for.” While this definition specifically applies to insurance,

the analogy to the sales of financial instruments, considering risk and return,

is similar. Source: The Economist.com

.

xxxii

The “agent-principal relationship” is defined as: “A U.S. common law

concept that understands employees as agents of employers (the “principal”).

Agents are hired to perform certain tasks and have duties to always act in the

best interests of their employer. These “fiduciary duties” include loyalty,

obedience, and confidentiality. Source: DesJardins, Joseph. (2008). An

Introduction to Business Ethics (Third Edition).

xxxiii

In an ironic turn of events, some unemployed brokers have turned to

counseling financially troubled mortgage holders.

xxxiv

Tabulated from Home Mortgage Disclosure Act (HMDA) data 2005.

Page 19 of 20You can also read