Situation Analysis Australian Dairy - May 2019

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Australian Dairy Plan

Australian Dairy

Situation Analysis

May 2019

1

Australian Dairy Plan Disclaimer Whilst all reasonable efforts have been taken to ensure the accuracy of Australian Dairy Situation Analysis Report, use of the information contained herein is at one’s own risk. To the fullest extent permitted by Australian law, Dairy Australia disclaims all liability for any losses, costs, damages and the like sustained or incurred as a result of the use of or reliance upon the information contained herein, including, without limitation, liability stemming from reliance upon any part which may contain inadvertent errors, whether typographical or otherwise, or omissions of any kind. © Dairy Australia Limited 2019. All rights reserved. ISBN 978-1-925347-43-2 (Digital)

Introduction

1

Australian Dairy Plan Context By the early-2000s favourable seasonal conditions and productivity growth supported by strong uptake of new technology and improved farm practices has driven more than a decade of strong growth. Investment was strong and confidence was generally high. Milk production was above 11 billion litres and Australian exports were 16 per cent of world trade volumes, placing Australia as the third largest dairy exporter. 2 Australian Dairy Situation Analysis

Key external factors Key internal factors

However, the past 20 years have • Australia has the most variable • Farm profitability is essential

presented new challenges for the climate on Earth and is now for milk production growth and

Australian dairy industry: notably drier in dairy regions. supply chain efficiency, but flatter

• Despite significant progress, the production curves, while suiting

• Increased market and climate

international trade environment manufacturer supply needs,

volatility has made the operating

remains distorted and many have increased production costs

environment more complex for all

of our competitors continue to on farm.

parts of the industry.

benefit from significant levels of • Yet farm profitability varies

• Recent drought events have government support. significantly across regions and

widely impacted dairy regions,

• Australian dairy markets are many farms are not achieving a

driving farm exits higher

open to supply from international sustainable return on investment.

in general, but particularly

competitors and imports

in the Murray region and • The collapse of the Murray

are increasing. Currency

northern states. Goulburn Cooperative following

exchange rates have changed

a recent market down turn has

• Productivity growth has slowed, considerably, which influences

shaken farmers’ confidence and

increasing the difficulty of our competitive positioning.

trust in their processors, driving a

managing conditions in which • Expectations of dairy customers, reduction in supplier loyalty.

input costs have increased faster retailers and food manufacturers

than milk prices. related to animal welfare and the • Confidence in traditional industry

environment are growing. The dairy advocacy structures has been

• Despite growth in some years,

industry is responding with greater challenged and new ways of

the overall milk production

transparency, goal setting, and supporting the Australian dairy

volume has declined to levels not

consumer engagement. industry have emerged.

seen since the mid-1990s.

• Competition for inputs such as • Industry is well served in RD&E

• Many manufacturers are short of

irrigation water are rising, and the capability, providing innovations

milk, resulting in higher costs as

availability of labour (from entry to lift overall performance,

plants are underutilised.

level to Farm Manager level) is however uptake more broadly

• There is a growing milk shortfall limited and can often difficult in the industry could be

in traditionally ‘domestic to retain. significantly improved.

market’ focused regions (NSW/ • Growing regulation creates • The rising complexity of dairy

QLD) which is being filled by additional restrictions and costs farming is highlighting areas

traditionally ‘export market’ to the industry (e.g. Labelling – where increased skill levels are

regions (VIC). Country of Origin, Health Star required and our ability to attract

• The Australian share of global Rating; proposed mandatory and retain capable people is

trade in dairy products is now six Dairy Code of Conduct). critical to ongoing success.

per cent and we are the world’s

• This rising complexity is

fourth largest exporter, leading

stimulating change in farming

some to question our relevance

systems and structures,

on the global market.

but sometimes this change

This Industry Situation Analysis compromises profitability and

draws on a broad range of cost competitiveness.

knowledge, history and experience

• Highly profitable farms with

to combine commentary and

different production systems

considerations on range of topics.

in different regions shared

This material is intended to

the common characteristic

be a conversation-starter for

of business operators with

consultation forums online, and also

excellent technical, people

those scheduled in dairy regions as

and business skills.

part of the Australian Dairy Plan.

3

Australian Dairy Plan

Consequential impacts A better future

• Limitations on our ability to meet The ability of the industry to adapt

the growth needs of customers and adjust to the changing conditions

has impacted the industry’s has been testament to its resilience

reputation as a relevant and over many decades. There are still

reliable supplier. many positive factors that point

toward a better future:

• Critical mass of farmers and milk

supply volumes in some regions • Strong domestic and international

is now a concern for processors growth in demand for dairy and

with milk transportation current price forecasts are positive.

costs increasing.

• Customers are discerning and are

• Reduced farm numbers is prepared to pay a premium for

affecting service providers in the quality dairy Australian products.

dairy regions as their customer

• We have many efficient farmers

base is diminishing.

who have been successfully

• Confidence amongst normally operating under some of the lowest

resilient industry participants levels of Government support

is impacted, and the tone of across the OECD.

reporting on the dairy industry

• We have world-class RD&E

tends to now focus more on

infrastructure and support in

challenges rather than strengths

delivering important innovations.

and opportunities.

• The trading environment for

• Collaboration is reduced as

Australian dairy has improved

manufacturers compete to secure

through completion of Free Trade

milk supply in a shrinking milk

Agreements and the removal of

pool and environment where

export subsidies via the World

farmer loyalty to one processor

Trade Organisation (WTO).

is diminished.

• We have a diverse, highly

competitive dairy manufacturing

base who are committed to

the industry.

• While markets and climate will

remain volatile, this volatility also

offers ‘upside’ potential if we utilise

the current and developing tools to

anticipate and respond volatility.

• Despite current challenges, the

prospects for the industry are bright

but the pathway toward a better

future will require concerted and

sustained collective industry action.

Despite the current challenges the

prospects for further progress in

the industry are significant but the

path to a better future will require

concerted and sustained collective

industry action.

The Australian Dairy Plan offers the

opportunity to decide on that pathway

and the actions that will follow.

4 Australian Dairy Situation Analysis

Situation analysis snapshot

The market has evolved faster Making a profit on farm has Our people and organisations

than the industry become more difficult need to adapt to succeed

The world market On farm dynamics Skills, knowledge and mindsets

• Competition: Our global • Farming systems and • Farming skill needs: Farmers

competitors have caught up and structures: The way we farm need skills in a broader range of

are now moving ahead of us in is becoming more complex in areas than was once the case.

international markets. This includes response to market, pricing and • Education and training: Farmers

a complex trade environment. climate variability. are changing the ways in which

• Relevance: While still a major global • Margins and input costs: Input they learn.

dairy exporter, our relevance on costs (water, feed, labour and

global markets is being questioned energy) have increased much Attracting and retaining people

because of our shrinking scale and faster than milk prices and • Attracting people: There is a

competitiveness. productivity gains can cover. widespread shortage of skilled

• Volatility: With the gradual removal • Farmer investment: Farmers labour at all levels in the dairy

of quotas and export subsidies have invested heavily in recent industry.

overseas, volatility in dairy markets years but are questioning their • Retaining people: Keeping skills

has increased. capacity and confidence to and knowledge in the industry,

continue investing. and encouraging farm succession

The supply chain

Risk profiles is an increasing and critical

• Processor investment: Processors challenge.

have invested heavily on the back of • Climate volatility: Australia • Promoting the industry: We can

clear opportunities for the Australian has the most variable climate do more to portray a positive

dairy industry but are now struggling in the world being 22 per cent image of dairy as an industry to be

to fill their plants. Production growth more variable than South Africa. involved in.

is required, but at the moment This variability adds to

processors are transporting milk production costs. Industry structures

to fill regional shortfalls. • Risk management: Risk • Industry structures and

• Supply chain divergence: management has become critical services: The structures and

Fierce competition has challenged to manage the peaks and troughs. services that exist to support

our capacity to collaborate. industry are under pressure to

Regional profitability

• Ownership structures: Processor adapt to changing industry needs.

ownership structures have evolved • Community sustainability and • The advocacy environment is

from the traditional cooperatives resilience: Farm consolidation changing: Expectations of how

which is also influencing processor is shifting our relationship with industry advocacy organisations

decision making. regional service providers and should operate are changing

communities. and there is a need for a trusted,

The consumer

• Export region margins being authoritative voice.

• Sales channels: Our production challenged: Milk prices are not

mix has had to adapt to changing keeping up with the rising costs of

consumer preferences and price/ production in some regions.

positioning competition from milk • Domestic region margins being

alternatives. challenged:

• Demand remains strong: Strong import competition

Consumption in Australia is robust means domestic producers are

and global dairy demand continues increasingly competing with the

to grow. international market.

• Social licence: Public expectations

are changing and consumers

are increasingly questioning the

attributes of their food.

5

Australian Dairy Plan 6 Australian Dairy Situation Analysis

Contents

Introduction 1 Our people and organisations need to adapt 61

to succeed

Key external factors 3

Skills, knowledge and mindsets 62

Key internal factors 3

Farming skill needs 62

Consequential impacts 4

Education & Training 66

A better future 4

Attracting people 67

Situation analysis snapshot 5

Attracting and retaining people 67

The market has evolved faster than the industry 9 Retaining people 68

The World Market 10 Promoting the industry 69

Competition 10 Industry Structures 70

Relevance 17 Industry structures and services 70

Volatility 19 The advocacy environment is changing 74

The supply chain 21

Processor investment 21

Supply chain divergence 24

Ownership structures 25

The consumer 26

Sales channels 26

Demand remains strong 28

Social License 30

Making a profit on-farm has become more difficult 35

On farm dynamics 36

Farming systems and structures 36

Margins and input costs 40

Farmer investment 44

Risk profiles 45

Climate volatility 45

Risk management 49

Regional Profitability 51

Community sustainability and resilience 51

Export region margins being challenged 53

Domestic region margins being challenged 56

7

Australian Dairy Plan 8 Australian Dairy Situation Analysis

Challenge 1

The market

has evolved

faster than

the industry

9Australian Dairy Plan

The World Market

Competition: Our global competitors have caught up and are now moving ahead of us in

international markets. This includes a complex trade environment.

By world standards, Australia markets and reducing the negative reforms in international trade policy.

has taken a relatively unique effect on world prices of overseas Due to the complex interactions of

approach to supporting domestic domestic support regimes and a number of subsequent internal

food production and trade. export subsidies. and external domestic market and

Many countries (like the USA, industry shocks (and overseas

In the 1990s Australian dairy

EU, Canada, Japan, Brazil and competitor reactions to policy and

significantly expanded both milk

Argentina) intervene in markets market changes) this pathway has

production and exports as the

to support domestic food not developed as expected. Some

combined effect of favourable

industry returns, address local of the drivers of this outcome are

exchange rates, world price

food affordability or boost the discussed below:

movements and improved trade

sustainability of regional food

outlooks and policy settings lifted

production. In contrast, Australia,

industry confidence and investment. The effect of the Australian

for some decades, has favoured

By the end of the decade, Australia mining boom on agriculture

an open market approach to

was supplying around 16 per cent

agricultural production and trade In the decade to 2013, the Reserve

of the measured world exports of

with government intervention Bank of Australia (RBA) estimates

dairy products.1 The two largest

focusing primarily on maintaining the mining boom increased real

local processors (MG and Fonterra)

food safety and environmental per capita household disposable

ranked in the world’s top 20 to 25

sustainability, research and income by 13 per cent3. However

firms in terms of raw milk intake

development and drought recovery. the subsequent increase in the

(although their heavy focus on

value of the Australian dollar had a

In the specific case of Australian bulk commodity sales meant that

negative impact on trade exposed

dairy, this approach resulted in the they ranked considerably lower

industries like manufacturing and

broad exposure of local industry on a revenue basis). Both firms

agriculture.

to world prices for manufactured separately accounted for five per

dairy products from 1984 (through cent of world export volumes.2 The RBA used AUS-M (an

CER with New Zealand) and the economic model of the Australian

In 2000, local industry fully

phased removal of domestic price economy) to estimate the real

expected that its share of world

support arrangements from 1985. exchange rate would have been

dairy production and trade would

Government did, however, work 44 per cent higher in 2013, relative

continue to grow based on

with industry to try and enhance the to its level in the absence of a

Australia’s relatively low production

international trading environment mining boom. In effect remaining

costs, its proximity to emerging

for Australian agriculture by largely at similar levels to where it’s

markets in Asia and expected

securing better access to major traded for the previous 20 years.

1

ADC – Dairy Compendium 2001, Page 54.

2

Leatherhead Food RA 1997. Key Players in the Global Dairy Industry. Report prepared by Information Group Services of Leatherhead Food RA,

November 1997.

3

https://www.rba.gov.au/publications/bulletin/2014/dec/pdf/bu-1214-3.pdf

10 Australian Dairy Situation AnalysisFigure 1: RBA Real trade weighted exchange rate without the Australian mining boom4 Trade and market policy changes

As noted above, Australia

has long embraced an open-

market approach to multilateral

trade reform. The WTO Uruguay

Round of 1995 vindicated this

approach with its commitment to

significantly cut the use of (market

damaging) export subsidies.

This gave a permanent boost to

world prices and industry sentiment.

The Uruguay Round was less

successful in generating real reform

in the areas of market access

and domestic market support.

However, it did create expectations

within major producers and traders

such as the EU and USA that they

would have to substantially adjust

their existing support policies

in future years to comply with

expected WTO rule changes.

Fluctuations in currency can be exacerbated by individual company hedging Subsequent WTO Rounds

policies and Australian farmgate returns are influenced by commodity (Millennial and Doha) have failed to

markets and individual business decisions relating to product and market mix. make further substantial progress

Independent of individual business decisions, the rapid appreciation of the AUD in these areas agricultural trade

increased competitive pressure on Australian exporters given much dairy trade policy reform (with the exception

occurs in US dollars and the AUD increased faster than the NZ dollar and Euro of the Doha Nairobi sessions of

against the US dollar; eroding Australian exporter returns. 2015 which formalised the end of

all export subsidies).

Australian dairy exporters faced more competitive pressure from 2009 to 2013

as the Australian dollar was trading comparatively higher than pre-mining boom As a result, the WTO considers the

(2002) levels, relative to competitors in New Zealand and Europe. This means in global dairy market to still be one

order to earn an equivalent local currency return, Australian exporters needed to of the most protected and distorted

sell Australian dairy product for a premium in US dollar terms in export markets. food markets. Many countries

continue to apply high tariffs on

dairy imports (see Figure 2 next

page) and to employ non-tariff

barriers – such as restrictive

customs procedures, excessive

port of entry inspections, product

testing, factory inspections or

veterinary certificate requirements –

in order to restrict trade and protect

local production. Governments also

continue to intervene in domestic

markets to distort and reduce

import trade opportunities.

Dairy Australia estimates that

Australian dairy exports attract in

excess of $200 million in direct tariff

charges each year as they enter

destination markets.

4

https://www.rba.gov.au/publications/bulletin/2014/dec/pdf/bu-1214-3.pdf

11Australian Dairy Plan Figure 2: : Average Applied MFN Tariff for All Dairy Products by Country. Source: WTO The failure of the Doha Round has led many countries to seek to gain trade advantages and protections for their local industries through a patchwork of domestic reforms and an expanding number of preferential market access agreements. Companies have also acted to advance their positions through cross-border alliances and investments in developing markets. While Australia has tried to be active in this area, its success lags that of some major competitors, leaving the local dairy industry at somewhat of a crossroads as a global market supplier. 12 Australian Dairy Situation Analysis

These include:

Europe: The EU regularly jockeys for the position of the largest dairy

exporter with New Zealand. For some time, the EU government and • Budget pressures on planned EU

dairy industry have expected that WTO reforms would force it to modify spending on direct farm payments

key tariff settings and domestic support regulations under its Common post 2020

Agricultural Policy (CAP). This has strongly influenced the EU’s approach • Moves by countries such as the

to world trade over the past decade. Netherlands to impose significant

environmental constraints on farm

production systems

An early EU response was to • The shift from price to income

expand its internal market by support, in turn, saw a gradual • General ‘greening’ measures

increasing its membership from convergence of EU domestic that could threaten the cost and

15 to 27 countries from 2004 wholesale dairy prices and efficiency of EU milk production

to 2007.5 From 1996 to 2010, the international market prices. • The impact of Brexit on Irish dairy

EU also entered into preferential This has helped sustain internal industry trade opportunities –

trade agreements with another 22 EU demand. More importantly, given that country’s significant

countries where it saw demand it has reduced the EU’s growth over the last decade.

growth opportunities for EU attractiveness as a dairy import

industries and products across market and reinforced the

North Africa, the Middle East and effectiveness of its existing tariffs

Central America. It has sustained in preventing any import trade

this push for bilateral FTAs over outside of narrowly defined tariff

the past decade – signing a rate quotas.6

further 12 agreements with various • EU expansion was also a driver of

Asian, American, African and East the removal of EU milk production

European nations since 2010. quotas in 2015. This change

In dairy, the EU is not only using saw many European farms and

these bilateral deals to gain processors, particularly those in

preferential access for EU dairy more cost-competitive grass-fed

into key import markets. It is also regions (e.g. Ireland, Denmark),

(successfully) seeking to limit gear up to expand production and

competition in these markets from exports post 2015 – an outcome

third country cheese producers that has come to fruition with both

like Australia via the enforcement EU milk supplies and exports

of EU GI regulations in each deal. growing since 2016.

The expansion of the EU’s Various public reports have

membership had several important indicated that EU company

market and policy consequences: investment in new dairy processing

• Commercially, it increased the facilities between 2012 and

size of the internal EU market for 2016 exceeded 5 billion Euros

products like dairy. (AUD $8 billion) 7.

• Politically, it forced a shift in Despite this recent growth, there

domestic support policy away are some factors that could limit the

from a more expensive system future growth in EU milk production

of maintaining high wholesale and export availability.

domestic prices (with government

purchase of market surpluses

at agreed minimum prices) to a

‘cheaper’ policy of direct income

support for local farmers.

5

Membership extended to 28 countries with the addition of Croatia in 2013.

6

Australian dairy exports to the EU have dramatically fallen over the past decade.

7

The Land – Europe leads the world in dairy processing investments – April 2016

13Australian Dairy Plan

United States: While the US has a very large dairy industry, for many

years it considered export sales as a market of last resort for surplus

local production.

This approach has changed over Based on this growth, the USA

the last decade or so. While US retains an ambition to significantly

milk production has steadily climbed increase its share of global dairy

around 2 per cent per annum, the trade over the next decade.

country has doubled dairy exports However, there are also some

(in milk equivalent terms) from restraining pressures on the

2010 to 2017. The US is now the US’s continued ability to grow its

world’s third largest contributor export presence. These include:

to dairy trade.8 This trade growth

• The high exposure of large-

reflects several factors including:

scale US farm systems to rising

• The US entering into 14 purchased feed costs, as world

preferential trade agreements in feed markets become tighter and

key target markets like Mexico, more volatile;

and Korea. In the case of Korea, • Stronger land and water-use

US dairy exports were fuelled by competition in south-western

the agreement’s rapid removal of growth regions, and barriers

tariffs under the FTA which has to new large farm and factory

seen Korea become the US’s developments from local

number two export market; communities in some regions;

• The development of large • The affordability of safety-net

scale factory operations for regulations for farm producers in

export in the Western half of more volatile markets.

the US (a number of which are

joint-venture partnerships with However, at this stage, the intensity

European export firms); of these pressures on US milk

production are well behind the

• The active physical presence of

pace of community expectations

industry organisations like the US

in competitor regions like the EU

Dairy Export Council (USDEC) in

and Australia.

major demand markets in Asia on

trade development missions;

• Significant uptake of genetically

modified herbicide tolerant and

enhanced digestibility lucerne/

alfalfa9 and increased ear

biomass and high amylose

content maize10 has improved

productivity in US agriculture.

8

IDF – The World Dairy Situation 2018, Page 8

9

https://www.ers.usda.gov/amber-waves/2017/may/genetically-modified-alfalfa-production-in-the-united-states/

10

http://www.isaaa.org/resources/publications/briefs/53/default.asp

14 Australian Dairy Situation AnalysisNew Zealand: Australia’s competitiveness with New Zealand is critical

to Australian dairy farming due to the Closer Economic Relations trade

agreement signed in 1983 which effectively treats New Zealand as the

seventh state of Australia for purposes of trade in goods and services

between the two countries.

New Zealand’s milk production have subsequently signed FTAs

has grown strongly over in the with China, New Zealand retained

past two decades (although the a clear tariff preference for its

pace of growth has slowed in products and first-mover advantage

recent years). This growth has been in the China market over much of

aided by several factors including the past decade. This allowed it

an entrenched enterprise culture, a to expand exports of products like

focus on wealth creation and dairy’s cheese to China by 30 per cent per

greater profitability compared to annum from 2012 to 2017 and to

other land uses which has seen the secure more than 50 per cent of the

significant conversion of other farm expanding Chinese import market

land into dairy production. for this product.12

While small alternate pathways As with other dairy producing

to market exist, New Zealand’s industries, there are issues that

industry development is closely may limit the future growth in

linked to the dominant position of its New Zealand milk production

major processor, Fonterra. This has and exports. These include:

allowed it to develop a consistent

• Regulatory measures imposed

export vision for the ‘industry’.

by regional councils, such as

Australia’s competition laws have

limits on stocking rates and

specifically excluded such a market

water access to address the

dominance position of one player in

environmental impact of milk

a similar way to New Zealand.

production in sensitive areas;

Fonterra has also used its control • The increased need for

over seasonal milk supplies purchased feed on larger scale

to invest heavily in some very farm units that will introduce new

large-scale export commodity costs, volatility and complexity

production plants (for milk powder to farm systems;

and cheese).11 These plants have

• Reduced land conversion

much lower per-tonne production

opportunities; and

costs than their Australian

counterparts, a factor that has • Increased production costs,

been very important in maintaining especially in South Island

New Zealand’s competitiveness in enterprises as they seek to

international markets. lift land and cow productivity.

The importance of New Zealand

dairy exports to its economy has

also meant that dairy interests given

a strong focus in that country’s

trade negotiations. The NZ–China

FTA provides a good example

of how this has benefited the New

Zealand industry. While other

countries, including Australia,

11

Fonterra’s investments from 2012–16 in this area exceeded $AUD 2 billion. Rabobank’s – Asia’s Fast Moving Cheese Markets, September 2018,

Page 6, notes that following a NZ$240 M investment, Fonterra’s Clandeboyne Mozzarella cheese plant is the largest in the Southern hemisphere

and its patented technology allows the firm to control a significant share of China’s pizza cheese trade.

12

Ibid.

15Australian Dairy Plan

Commercial scale Fonterra is by no means unique in With Australia’s major export

and partnerships this regard. Other major firms that competitors continuing to grow,

have utilized this approach include: this situation has led some

As the above section identified,

buyers to question the ongoing

all major dairy producing countries • Saputo (Canada) which has

significance and relevance of

face issues that could limit their expanded operations into the

Australia as a supplier into the

future growth in domestic milk USA and Australia;

global dairy marketplace.

supplies, and their ability to meet • Glanbia (Ireland) which has

rising world dairy demand. major joint venture processing Industry, however, has sought to

investments in the USA; re-affirm its export commitment,

These constraints may be new

working with government to push

(and more environmentally focused) • Lactalis (France) which has

for further dairy trade liberalisation

but world dairy has faced such operations in the USA, Australia

and individually working to

constraints before. A 2002 review and Asia to underpin its global

reinforce positive consumer

by Babcock13 identified how many brand strategies;

perceptions about the quality,

of the world’s largest, and more • Yili (China) which has invested safety and integrity of Australian

successful, dairy processors had in New Zealand manufacture industry practices and products.

maintained effective company supply base, and

growth strategies in the face of To date, Australia has secured

• Nestle which has joint

limits on raw milk supply using a 14 bilateral trade agreements.

partnerships with multiple

combination of: Eleven of these are currently in

partners across a range

force – New Zealand, Singapore,

• Maximizing their manufacturing of regions.

Thailand, USA, Chile, ASEAN

efficiency (through scale

As a result, many of the world’s (AANZFTA), Malaysia, South Korea,

or technology),

major dairy players are now well Japan, and China – while a further

• Developing new markets for placed to operate across multiple three – Peru, Indonesia and Hong

their product in developing market and policy settings, and Kong – are awaiting ratification.

dairy markets; have a reduced dependence/

Australia is also a member of

• Securing access to increased focus on industry developments in

the 11 nation Comprehensive

milk supply – including through individual dairy producer countries.

and Progressive Agreement for

cross-border alliances; Consequently an Australian brand

Trans-Pacific Partnership

• Building market share and for dairy products has less capacity

(TPP-11) which entered into force

market power through their for impact in overseas markets.

in December 2018. The provides

brand portfolio. additional access rights for Australia

Many of the world’s major dairy Australia’s performance – into markets including Brunei,

firms have continued to pursue a comparison Canada, Chile, Japan, Malaysia,

these strategies over the past Mexico, Peru, New Zealand,

An irony of recent world market

decade to position themselves Singapore and Vietnam.

developments is that, while global

to meet rising dairy demand dairy demand is increasing, with Given with a range of competing

in emerging markets in Asia much of this growth being driven FTAs in place, it should be

and Africa. by markets that Australia is well recognised that the access rights

Fonterra, for example, has placed to service, local milk conferred on Australian dairy

actively pursued a strategy of production and export availability exporters by these agreements,

developing a ‘global’ farm supply have stagnated for almost 20 years. in some cases, only match those

and manufacturing footprint As noted before, a number of factors given to our competitors. So, while

(covering Europe, Asia, Oceania (drought, company collapses, they are essential for Australian

and the Americas). This allows it water availability, payment step dairy exports to remain competitive

to try and match demand growth downs in the wake of market crises in future, they do not always confer

in particular markets with its own etc.) have combined to badly affect major commercial advantages to us

multi-hub supply sources. farmer confidence, profitability and in all emerging markets.

production with a resulting decline

in regional milk pools even though

local consumption of dairy has

held firm.

13

W. D. Dobson and A Wilcox – How leading International Dairy Companies adjusted to Changes in World Markets- Babcock Institute Discussion

Paper 2002

16 Australian Dairy Situation AnalysisRelevance: While still a major global dairy exporter, our relevance on global markets is being

questioned because of our shrinking scale and competitiveness.

Global dairy markets hold significant Despite the strong brand and The two dairy commodities that

potential for the Australian historical presence Australia has have experienced the most

industry if our industry is able in international dairy markets, significant growth in international

to service market opportunities. some buyers are now questioning demand in recent decades are

These opportunities are being driven the ability of Australia to supply cheese and Whole Milk Powder

by demand growth, which in turn is future needs of dairy products. (WMP). World exports of each of

being driven by positive economic The changing production these two products have effectively

growth rates. The perception landscape in Australia is also doubled since the early 2000s to

in some markets that imported encouraging many Australian reach roughly 2.4million tonnes per

products are safer, rising incomes, dairy processors to reassess their annum in 2018. However, Australian

comparatively high birth rates and markets and reprioritise based on production and exports of these

increasing refrigerated infrastructure potential returns. products have not kept pace with

expanding opportunities for this world market growth.

As noted previously, in the late

fresh product.

1990s Australian dairy supplied Australian production of cheese

Trade data suggests global dairy around 16 per cent of measured has been relatively flat and exports

export trade volumes increased world exports of dairy products.14 have slowly dropped below 200,000

by more than 2.5 million tonnes The two largest local firms (MG tonnes per annum. As a result,

(21 per cent) between 2012 and and Fonterra) each separately Australia’s export market share

2018, while Australian dairy exports accounted for about 5 per cent has halved to less than 10 per cent.

according to the ABS increased of total world trade by volume. The limited growth in Australian

22,364 tonnes (3 per cent) over the By 2018, Australian dairy’s share cheese supplies also restricts local

same period. of (an admittedly expanded) industry’s capacity to participate

export trade has fallen to around in growing world markets for whey-

6 per cent.15 No local firm accounts based products.

for anywhere near 2 per cent of

In the case of WMP, recorded

this trade.

Australian production and exports

Figure 3: Exporter Shares – Sourced from Dairy In Focus and IFCN. have steadily fallen over the

past decade, with the result that

Australia’s share of world trade

has fallen from 13 per cent in 2000

to under 5 per cent in 2018.

Australian imports of both cheese

and WMP have risen sharply in

the past decade. In the case of

cheese this is likely to reflect local

companies maintaining export

volumes while using imported

bulk cheese to meet demand from

certain domestic sales outlets.

In the case of WMP (and imported

lactose and whey products) imports

are most probably re-exported as

recombined retail powder products.

The benefits accruing to the

local dairy industry from this

development are limited at best.

Source: Dairy Australia Source: https://ifcndairy.org

14

ADC – Dairy Compendium 2001, Page 54.

15

IDF – The World Dairy Situation 2018, Page 7

17Australian Dairy Plan

These raw trade data do not, by Australia has also successfully

themselves, imply that Australia established retail and food service

has no capacity to regain position sales channels for shorter shelf life

in world dairy markets and trade. products like yogurt and milk across

As Rabobank has identified:16 Asia in recent years. This is providing

a positive platform for industry to build

• Australia has a strong reputation

outlets for more value added products

with dairy buyers in Asia and

such as cheese in the years ahead.

beyond as a reliable supplier

of technically advanced, However, perhaps the key driver

high-quality, safe products. of Australia’s future export market

• The industry continues to relevance will be its capacity to

have access to a strategic restore some level of sustained

milk pool which it can use to growth in local milk production in

deliver significant volumes of coming years. This is needed both

competitively priced products to convince buyers that Australia

to key markets in Asia. retains a capacity to meet emerging

product demand and to ensure that

• Against this, Australian dairy

local factories have sufficient

manufacturers no longer appear

throughput volumes to generate

to have any absolute production

utilisation synergies and keep

cost advantages against

processing costs competitive.

major competitors.

• So Australia remains vulnerable

to competition from alternative

exporters, with improving access

rights that operate larger scale

plants and have reliable year

round milk pools.

There has been substantial investment

in recent years to upgrade and expand

dairy manufacturing operations in

Australia and to set up a number

of greenfield powder and liquid milk

plants for export sales. While these

upgrades are important in promoting

industry competitiveness, in general

they have not been designed to match

the scale of operations now present in

many overseas operations.

16

Rabobank – Asia’s Fast Moving Cheese Markets, September 2018, Page 8

18 Australian Dairy Situation AnalysisVolatility: With the gradual removal of quotas and export subsidies overseas, volatility in

dairy markets has increased.

Unlike most of our competitors, Australian dairy farmers operate in a deregulated Compared to New Zealand, the

and open market, and have done so for almost 20 years. This does make us Australian milk price does not vary

more exposed as an industry to the global market shocks that increasingly define as much from year because of

the dairy industry. reduced exposure to international

markets (Australia exports less

Dairy commodities prices are extremely volatile, commonly perceived as one

than 40 per cent of milk production

of the most volatile of all globally traded commodities. More specifically, it

compared to New Zealand

is reported that WMP prices are more volatile than other key traded global

exporting around 95 per cent of

commodities such as sugar and oil (WMP claims to have a volatility > 60 per cent

milk production). While Australian

versus sugar at 26 per cent and crude oil at 22 per cent (Commerzbank, 2016;

farmgate prices avoided the rapid

Fonterra, 2015)).This is in no small way due to the fact that globally traded dairy

and prolonged drop New Zealand

commodities are arguably more sensitive to a variety of external impacts that can

dairy farmers experienced between

variously affect milk supply and demand.

2013 and 2015, it has spent the last

Increased levels of market and margin volatility within the industry have three years settled around levels

undermined confidence in the outlook for many farmers, who are seeking reliable not since seen since 2009. The

returns on which to build a longer term future. New Zealand milk price has since

Figure 4: Industry volatility as indicated by farm business profit

recovered in US dollar terms to be

the equivalent milk price in the USA

or EU-27 average.

In the past decade, dairy market

returns have been greatly affected

by several unexpected market

shocks. Some obvious examples of

this include:

• The step down in farm gate prices

following the Global Financial

Crisis and its impact on world

trade and pricing;

• The flow effects of Russia’s

2014 ban on cheese imports

While world dairy trade is growing, it still represents less than 10 per cent of that carried through into

global dairy production. So dairy remains a ‘thinly’ traded commodity, and significant temporary downturns

international dairy prices remain susceptible to market shocks. in international cheese prices

Figure 5: International farmgate milk price comparison (USD/100kg) and an extended fall in world

Skim Milk Powder (SMP) prices

(following a build-up of surplus

SMP stockpiles);

• More recently, the United

States has imposed higher

tariffs on a range of imported

products. Some US trading

partners, such as China,

have retaliated with their own

tariff increases (particularly

on US agricultural exports).

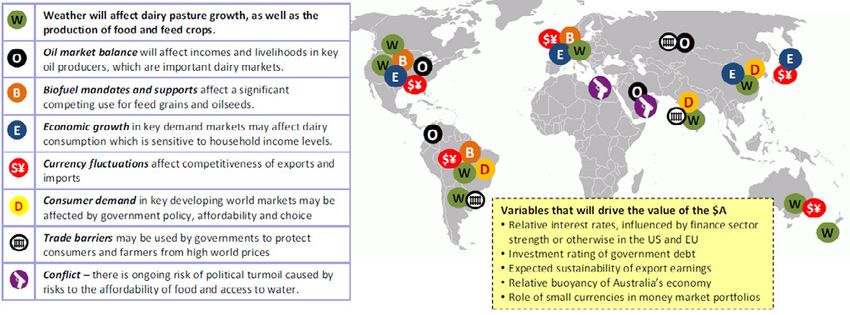

19Australian Dairy Plan While these disputes raise the farm gate milk prices. Coupled with will vary over time, affecting dairy scope for opportunistic short term increased volatility in the availability markets, competing foods and input sales for exporters like Australia, and pricing of key production inputs costs. It is imperative that Australian ultimately they raise market such as water and feed, this has dairy industry participants build uncertainty and volatility due to undermined local farmer confidence volatility into their business potentially adverse trade diversion in the long term dairy market expectations and resilience into impacts and the reduced clarity and outlook and the scope to extract their business practices. predictability of market conditions reliable returns from their milk on and opportunities. which to build a longer term future. Australian dairy farmers operate The map below is a summary of the in a deregulated and open market, variables identified in Horizon2020 leaving them quite exposed to that would drive greater volatility the product price adjustments in food and dairy markets in the induced by global market shocks next decade. The coincidence and and associated flow on impact to relative intensity of these influences Source: Horizon2020 20 Australian Dairy Situation Analysis

The supply chain

Processor investment: Processors have invested heavily on that back of clear opportunities

for the Australian dairy industry but are now struggling to fill their plants. Production growth is

required but at the moment processors are transporting milk to fill regional shortfalls.

The underlying competitiveness and attraction of the Australian dairy is However, reduced milk flows in

illustrated by the estimated $3 billion that processors have invested in many regions around Australia are

acquisitions and upgrades in Australian dairy assets over the last five years. straining production economics

Figure 6: Investments, acquisitions and upgrades in the Australian dairy industry of the newly constructed plants.

At the time several new plant

construction or upgrades were

budgeted for, industry confidence

and growth forecasts for

Australian milk production were

substantially stronger. The current

reduced milk production levels are

requiring processors to:

• Concentrate their fixed overhead

recovery over a smaller volume

of milk inputs and finished

product outputs

• Face increased competition for

raw milk thereby increasing the

cost of their main input.

The dynamics of the domestic

and international markets are

contributing to growing pressure

on dairy processor margins.

As Australia is an open market for

dairy, local dairy manufacturers

and processors compete for inputs

and sales both with international

suppliers in overseas markets and

with domestic competitors at home

in the Australian market.

Processors operating in traditionally

fresh product domestic markets

(typically based in Queensland,

NSW and WA) earn on average

over 70 per cent of their revenue

from fresh drinking milk. Yoghurt,

cheese, cream, other dairy

products and a relatively small

amount of UHT milk make up the

remaining revenue.

21Australian Dairy Plan

Particularly in these ‘fresh milk states’, the widespread introduction of $1/litre Since 2011/12 Queensland

milk and private label milk at retail level has had considerable negative effects hasn’t been self-sufficient with

on industry confidence and margins. respect to milk production and

consumption and has relied on milk

Evidence supplied to the ACCC Dairy Inquiry suggested that, while private label

produced in NSW to fill seasonal

contracts are profitable for some processors in isolation, many private label

gaps in production. (see figure 8

contracts are at best profit-neutral for processors and that firms may operate at

and figure 9). Reduced regional milk

a loss once overheads are fully accounted for. It is well recognised that processor

flows since 2017/18 have meant

margins are better for branded product, compared to private label equivalents.

that there is now a combined QLD

With this being the case, the discount milk policies have eroded the profitability

and NSW seasonal milk deficit, with

of the broader supply chain by reducing the market share of branded milk.

this gap having to be filled with milk

Indirectly, there has been no question about the impacts of heavy retail price shipped north from Victoria.

discounting and how it has eroded the perceived value of dairy by consumers.

Dairy farmers have felt the emotional impact as they invested their livelihood

into caring for animals and producing fresh milk in an industry that appears to

be de-valued.

Traditionally fresh milk production states (NSW, Queensland, and WA) supplied

milk to fulfil domestic demand requirements. However, reduced milk production

in these regions in recent years has created significant supply tension in the

Australian domestic market.

Figure 7: Movement of milk around Australia

As indicated in figure 7 ‘movement of milk’, there are clear supply pathways

moving milk from production surplus areas in the south eastern states, further

north to meet seasonal supply shortfalls.

Often this milk has been transported to meet domestic market supply contracts

(for retail, food service or industrial users) for fresh, short shelf life products

— which means processors have limited scope to use global suppliers to meet

their obligations.

In times of production surpluses in south eastern states this isn’t a problem as

the south eastern milk price is generally lower than that for northern and western

milk production states, suggesting freighting milk up the eastern seaboard, or

fresh manufactured product across the Nullarbor to WA is economically viable.

However, milk production dynamics within Australia are changing.

22 Australian Dairy Situation AnalysisFigure 8: : Combined NSW & QLD Fresh Milk Balance However, the 2018/19 season

has been significantly affected by

drought, reducing milk available to

fill this NSW/QLD gap and raising

significant concern amongst some

processors as to how (and at what

expense) they will fulfil contractual

supply obligations.

This shortage of milk also means

processors have needed to

buy milk off each other to fill

contractual obligations. This milk

is often procured at a price higher

than average farmgate milk prices

off the liquid milk spot market.

This is not an open and transparent

market, so farmers do not receive

pricing signals to produce more

milk on the basis of these inter-

Figure 9: Queensland Fresh Milk Balance processor purchases of milk.

The open Australian market

also allows customers to fulfil

their requirements with imported

dairy products if they are not

concerned about country of origin.

A combination of the declining milk

pool and choices to export dairy

product to some markets rather

than focus on the domestic market

has opened the door for significant

growth in dairy imports, which

have more than doubled in the

last decade.

Figure 10: Australian dairy import volumes The combination of a gradual

decline in dairy production volumes,

competition for milk at the farm

gate and significant competition

from imported dairy in Australian

domestic market is ratcheting up

the challenges faced by processors

in the Australian market.

23Australian Dairy Plan

Supply chain divergence: Fierce competition has challenged our capacity to collaborate.

The Australian dairy industry has Figure 11: Horizon 2020 working group scenarios for dairy industry future

seen a more intensely-competitive

environment between dairy

companies which are offering

different propositions and business

models through to customers.

Industry has collaborated in limited

areas where necessary but this

is far less obvious than was the

case a decade ago. The more

competitive climate has meant there

are winners and losers, and less

integration results in more exposure

to volatility.

The Horizon2020 project17

completed in 2013 identified

four potential scenarios for the

dairy industry of the future along

dimensions of; an integrated

or fragmented industry where

participants collaborated or worked

Over the last five years the industry has unfortunately drifted toward the

closely with market (integrated),

Scenario 4 (bottom left), demonstrated by declining milk production volumes,

or pursued individual interests and

limited post farmgate collaboration, a high level of competition and limited

had limited farmer ownership post

farmer ownership beyond the farmgate.

farmgate (fragmented). The second

dimension of these scenarios The significant diversity in the industry is a reflection of the many groups of

was growth or contraction in milk industry stakeholders pursuing what they’ve identified as the ‘best strategy’.

production volumes. Yet the industry could be more successful in responding to the external

environment with a coordinated approach.

17

https://www.dairyaustralia.com.au/about-dairy-australia/about-the-industry/horizon-2020

24 Australian Dairy Situation AnalysisOwnership structures: Processor ownership structures have evolved from the traditional

cooperatives which is also influencing processor decision making.

Processors occupy a critical position in the value chain between producers and One of the advantages multinational

consumers of dairy products and ingredients. processors offer customers is the

notion of consistent supply from

The importance of processing capacity has also been recognised in the

multiple origins. This consistency

prevalence of cooperative ownership of processing infrastructure by farmers

can be provided because of the

during the history of the Australian dairy industry. In a global context there are

internal standards and processes

still many large cooperatives in existence today, but the herd has progressively

of the organisation in all of the

thinned over the last decade. There are a number of reasons, from strategic

countries in which it operates.

missteps to improving access to capital and mitigating redemption risk.

These new ownership structures

In the context of the Australian dairy industry, the share of milk processed by

add complexity to traditional

cooperatives has gone from ‘major’ to ‘niche’ in just a few years. In the late

country of origin marketing

1990s, eight locally owned dairy firms18 (six of which were farmer-owned co-

because multinationals operate

ops) processed and sold around 85 per cent of Australia’s milk supply. The three

in multiple jurisdictions. In that

largest cooperatives controlled around 60 per cent of all milk processed.

context they are now looking to

Figure 12: Australian Dairy Manufacturing By Ownership Type, Market Orientation manage potential regional risk

that come with limiting marketing

efforts to only one country of origin.

This may mean that some firms are

more willing to contract for large

volumes of milk from other firms

than enter into open ended milk

supply arrangements with individual

farm suppliers.

Twenty years later, only one of these eight firms continues to operate

independently (and with an expanded business focus beyond dairy) and this is

no longer a cooperative. The factory operations of the other seven firms have

either been rationalised, closed or incorporated into the businesses of major

global players such as Fonterra, Lactalis, Saputo and Kirin Breweries (and, in

some cases, Bega). Essentially, Australian dairy processing has become one

of the supply hubs that major dairy players are using to meet their specific market

strategies – with these strategies largely being determined outside Australia’s

direct control.

As a result, where a cooperative might have traditionally been accountable

only to its member shareholders, the current corporate landscape has created

new dynamics which repositions the importance of Australian origin product

and means processors are accountable to shareholders and overseas

parent companies.

18

These were Murray Goulburn, Bonlac, Dairy Farmers (ACF), National Foods, Warrnambool

Cheese and Butter, Bega Cheese, Pauls (QUF) and Tatura Milk Industries.

25Australian Dairy Plan

The consumer

Sales channels: Our production mix has had to adapt to changing consumer preferences

and price/positioning competition from milk alternatives.

The Horizon2020 project identified Plant-bases now include soy, • However the industry must

an intense contest for ‘parent nuts, coconut, rice, oat, pea and positively manage how it is

brand’ trust by consumers in retail emerging sources like hemp seen by consumers keen to

food markets, which is dominated and quinoa. The products have demonstrate their care for welfare

by a core appeal to the ‘value’ also extended beyond ‘milk’ into and environmental concerns.

perception (representing ‘price ‘yoghurt’, ‘ice-cream’ and ‘cheese’. • Emerging retail channels

plus benefits’). outside of conventional grocery

Some products, particularly

It is not expected that this approach fortified soy milk and some of the and foodservice outlets offer

will change quickly due to: new pea milks, try to mimic the opportunities for real growth

core nutritional elements of milk. as lifestyles and technologies

• The entrenched desire for value influence decisions.

Others bear little nutritional

from a cautious shopping public

resemblance to the dairy products • While price discounting has

• The expansion of the Aldi and they take the name of. However, all defined the last decade of retail

Costco chains are marketed as dairy alternatives price competition, there is a

• The gradual improvement in the and attempt to mislead consumers growing view that commercial

return on investment by Coles to perceive them as such. This has capital can be gained by

been concerning for dairy industries ‘supporting the farmer’ and

Gains in grocery chains building

and government authorities around ensuring that the supply chain

consumer trust of parent brands

the world due to the significant lack is profitable. Recent fresh white

will be slow. UK retail parent brands

of perceived ‘fairness’ in the current milk supermarket developments

models started in a different place

marketing strategies being adopted have brought this consumer

to their local counterparts with a

by the alternatives. sentiment to the surface.

high-quality perception, yet have

taken 20–25 years to reach their The domestic consumer market is There are a number of strong

current levels of respect. responsible for consumption of the trends causing change in the

majority of Australia’s milk output, way consumers make their food

Australian consumers are relatively

yet grows slowly across major purchase decisions and influences

sceptical of major grocers that have

categories. But future growth is not shopping behaviour. These in turn

indistinguishable propositions.

assured, and the forces affecting have relevance for the range of

‘Gen Y’ and ‘Gen Z’ segments of the

dairy’s role are changing prospects products and usage occasions

community show less attachment

for growth are complex. A number across the dairy category.

and loyalty to ‘establishment’.

of factors have emerged that are

This implies that ‘value’ is likely re-defining the consumer market:

to remain a key plank of retailer

• There is ample scope for

propositions to shoppers, unless

growth in volume and value

there is a huge lift in consumer

as a result of shoppers trading-

sentiment and discretionary

off value, convenience, and

spending on food, which is not

indulgence priorities.

foreseen by grocers for the next

five years. • Dairy marketers have many

opportunities to capture growth

The scope for growth in unit values in an increasingly diverse market

of dairy products depends how with accelerating change due to

products can tap into the drivers the diversity of product offering

of premium, which were identified and meal and snacking occasions

during the Horizon2020 process that suit dairy.

based on feedback from retailers.

• There is widening scope to get

The last decade has seen a more more product into convenience

diverse range of products marketed purchases, where there is less

as dairy alternatives, with wide price-sensitivity.

variance as to the functional and/

or nutritional substitutability of

these products for dairy products.

26 Australian Dairy Situation AnalysisYou can also read