Q1 2022 INVESTOR UPDATE - May 12, 2022 - NorthWest Healthcare Properties

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Q1 2022

INVESTOR UPDATE

May 12, 2022

DISCLAIMER

This presentation provides a summary description of Northwest Healthcare Properties Real Estate Investment Trust (“NWH” or the “REIT”). This presentation should be read in conjunction with

and is qualified in its entirety by reference to the REIT’s most recently filed financial statements, management’s discussion and analysis, management information circular and annual information

form (the “AIF”).

This presentation contains forward-looking statements. These statements generally can be identified by the use of words such as “expect”, “anticipate”, “believe”, “foresee”, “could”, “estimate”,

“goal”, “intend”, “plan”, “seek”, “strive”, “will”, “may”, “would”, “might”, “potential”, “should”, “stabilized”, “contracted”, “guidance”, “normalized”, or “run rate” or variations of such words and

phrases. Examples of such statements in this presentation may include statements concerning: (i) the REIT’s financial position and future performance, including normalized and target financial

metrics, forecasted liquidity and potential deleveraging transactions; (ii) joint venture conditional capital commitments and negotiations, potential acquisitions, dispositions and other transactions,

including a potential UK joint venture, and transactions involving Aspen and Australian Unity; (iii) the REIT’s development pipeline and associated future value creation, (iv) the REIT’s property

portfolio, cash flow and growth prospects, liquidity, un-deployed capital, leverage ratios, future financings and asset management fees, (v) the REIT’s intention and ability to distribute available

cash to security holders, (vi) the industry in which the REIT operates and trends related thereto, and (vii) the REIT’s strategic and governance initiatives.

Such forward-looking information reflects current beliefs of the REIT and is based on information currently available to the REIT. Other unknown or unpredictable factors could also have material

adverse effects on future results, performance or achievements of the REIT. Forward-looking information involves significant risks and uncertainties, should not be read as a guarantee of future

performance or results and will not necessarily be an accurate indication of whether or not, or the times at which, or by which, such performance or results will be achieved, and readers are

cautioned not to place undue reliance on such forward-looking statements. The forward-looking statements contained in this presentation are based on numerous assumptions which may prove

incorrect and which could cause actual results or events to differ materially from the forward-looking statements. Although these forward-looking statements are based upon what the REIT

believes are reasonable assumptions, the REIT cannot assure investors that actual results will be consistent with this forward-looking information. Such assumptions include, but are not limited to,

the assumptions set forth in this presentation, as well as assumptions relating to (i) completion of anticipated acquisitions, dispositions, development, joint venture, deleveraging and other

transactions (some of which remain subject to completing documentation) on terms disclosed; (ii) the REIT’s properties continuing to perform as they have recently, (iii) the REIT successfully

integrating past and future acquisitions, including the realization of synergies in connection therewith; (iv) various general economic and market factors, including exchange rates remaining

constant, local real estate conditions remaining strong, interest rates remaining at current levels, the impacts of COVID-19 on the REIT’s business ameliorating or remaining stable; and (vii) the

availability of equity and debt financing to the REIT. These forward-looking statements may be affected by risks and uncertainties in the business of the REIT and market conditions, including that

the assumptions upon which the forward-looking statements in this presentation may be incorrect in whole or in part, as well as the various risks described in the AIF.

These forward-looking statements reflect the REIT’s expectations only as of the date of this presentation. The REIT disclaims any obligation to update or revise any forward-looking statements,

whether as a result of new information, future events or otherwise, except as required by law.

Certain information concerning Vital Trust contained in this presentation has been taken from, or is based upon, publicly available documents and records on file with regulatory bodies. Although

the REIT has no knowledge that would indicate that any of such information is untrue or incomplete, the REIT was not involved in the preparation of any such publicly available documents and

neither the REIT, nor any of their officers or trustees, assumes any responsibility for the accuracy or completeness of such information or the failure by Vital Trust to disclose events which may

have occurred or may affect the completeness or accuracy of such information but which are unknown to the REIT.

Funds from operations (“FFO”), adjusted funds from operations (“AFFO”), net operating income (“NOI”), same property NOI (“SPNOI”), and net asset value (“NAV”) are not measures recognized

under International Financial Reporting Standards (“IFRS”) and do not have standardized meanings prescribed by IFRS. FFO, AFFO, NOI, SPNOI, and NAV are supplemental measures of a real estate

investment trust’s performance and the REIT believes that FFO, AFFO, NOI, SNOI and NAV are relevant measures of its ability to earn and distribute cash returns to unitholders. The IFRS

measurement most directly comparable to FFO, AFFO, NOI and SPNOI is net income. The IFRS measurement most directly comparable to NAV is net equity. An explanation and reconciliation of

Non-IFRS measures is presented in the REIT’s management’s discussion and analysis of financial condition and results of operations of the REIT for the period ended March 31, 2022 as filed on

SEDAR.

1

TORONTO

Focused Healthcare Real Estate Investment Partner

9 Global scale, local relationships

Partner of choice for leading operators

LONDON

SÃO PAULO

9 Defensive operating fundamentals

Cure focus underpinned by government funding

PHOENIX

9 A proven track record

Annual total shareholder return of 13.1%

B E R L I N S Y D N E Y

9 Scalable platform with embedded growth

Robust acquisition and development pipeline

+70% Global Gateway City Exposure

Established Relationships with Leading Healthcare Operators

NWH AT A GLANCE CONSOLIDATED NO

NOII

DIVERSIFICATION(4)

18.1M 229 $10.3B

SQUARE FEET* PROPERTIES* TOTAL ASSETS(3)

97.0% 14.6 5.2%

OCCUPANCY* YEAR WALE* IFRS CAP RATE

$3.0B 6.4% 95%

MARKET CAP (1) DISTRIBUTION YIELD(1) PAYOUT RATIO (2)

2

*Q1 2022 PF completion of US portfolio acquisition

WHY INVEST IN HEALTHCARE REAL ESTATE

$3 Trillion ‘niche’ Excellent demand Defensive

healthcare real estate fundamentals characteristics;

market with growing indexation delivering

demand growth

• $8 Tn spent annually on global • Supportive demographic trends • Healthcare real estate has been

healthcare with growing & ageing among the top performing real

• Healthcare spending growing at populations particularly in the estate asset classes since before

4%-7% annually key 65+ demographic the global financial crisis

• Rising prevalence of chronic • Essential nature of healthcare

• Among largest global industries

conditions is driving demand makes the asset class recession

accounting for over 10% of

resilient as demonstrated during

global GDP • Wellness trends are increasing

the GFC and C-19

“consumption” of healthcare

Delivering Superior Risk Adjusted Returns

3

NORTHWEST’S FOCUS

CURE CARE

Higher Acuity Lower Acuity

NWH FOCUS

Hospital Ambulatory Care & MOB Life Sciences Skilled Assisted Living Independent

Outpatient Nursing/Aged Living

Care

Healthcare precincts drive long-

Evolution term value creations through;

¾ Higher value tenants &

retention

¾ Higher rent growth

¾ Up zoning

¾ ESG compliant

4

HIGHLIGHTS OF THE QUARTER

+2% +15%

$0.21 YoY $14.73 YoY 320 bps YoY 2.2% YoY

AFFO/Unit NAV/Unit LTV Reduction SPNOI

US MARKET ENTRY & AFFO GROWTH LEVERAGE & VALUE CREATION

$753M 5.5%

Acquisition Price Portfolio cap rate 52.1%

49.6% 49.8% 48.8%

48.5%

+90% 55%

Indexation LTV 44.3%

43.1% 43.8%

41.9% 42.5%

Q1 21 Q2 21 Q3 21 Q4 21 Q1 22

Consolidated Proportionate

$0.83 $0.84 $12.77 $14.73

Q1-21 AFFO/Unit

+2% YoY Q1-22 AFFO/Unit

+15% YoY

Q1-21 NAV/Unit Q1-22 NAV/Unit

Annualized Annualized

5

2022 STRATEGIC PRIORITIES

CORE DEFENSIVE ACCELERATING GROWTH RAPIDLY GROWING ASSET

PORTFOLIO PROFILE MANGEMENT PLATFORM

• NWH’s portfolio is highly

defensive:

• US market entry to

accelerate growth: 9 • Total management fees

+23% YoY

9 Long-WALE of ~15 9 Largest healthcare RE

years market globally; • Asset manager expected

9 Highly diversified 9 High transaction to continue rapid growth

geographically velocity; in 2022

including exposure to 9 Acquisition cap rates at

USD; ~100 bp premium to • New fund initiatives incl:

9 Inflation protection

from inflation indexed

other markets 9 $2.2B AUS JV upsize

9 $2.5Bn UK JV

9

& annual contractual • Healthcare Precinct including ~$1B seed

rent growth strategy: portfolio (2H-22)

9 Opportunity to develop 9 $765M US JV (2H-22)

core real estate at the 9 $5.0B Global

intersection of Healthcare Precinct

healthcare, education Fund (2H-22)

and life science

MATCHING THE RIGHT CAPITAL WITH ATTRACTIVE INVESTMENT OPPORTUNITIES

TO DRIVE VALUE CREATION ACROSS A RAPIDLY EXPANDING ASSET MANAGEMENT

PLATFORM

6

DEFENSIVE UNDERLYING PORTFOLIO

Operating Metrics Diversification

~97% 8 >2,000

Portfolio Occupancy Countries Tenants

Diverse tenants encompass

80% 15 yr hospitals operators,

Inflation Indexed rehabilitation clinics, life

WALE sciences and individual

Rents

STABLE practitioners

OPERATING

FUNDAMENTALS

> 80%

Tenants with One of Australia’s Leading

Government Support Hospital Operators

>$350B

One of Germany’s leading Brazil’s Leading

Stable Private Funding from Public

Rehabilitation Clinic Operators Hospital Operator

Healthcare Funding Healthcare Systems

Government Funding Strategic Relationships

7

HIGH INDEXATION

THE REIT’S z Due to the long duration of most of Northwest’s leases; rents generally escalate each year

INTERNATIONAL z Within international markets ~99% of leases are indexed minimizing the impact of the current

inflationary environment

PORTFOLIO IS

z The international portfolio is also characterized by a weighted average lease term of 17 years

CHARACTERIZED BY A and occupancy of ~99% indicating long term stability in rental income

LONG WALE OF 17 z Canadian portfolio continues to increase percentage of inflation indexed leases. With shorter

YEARS AND 99% term leases, renewal spreads are in line with inflation.

INDEXATION WHICH

MINIMIZES THE IMPACT International Portfolio Indexation Canadian Portfolio Metrics

OF THE INFLATIONARY

ENVIRONMENT 100% 99% 99% 99%

91%

$1.2B 84%

AUM MOB

91% 5 Yr

Occupancy WALE

Brazil Europe ANZ USA Total

International

Portfolio

8

UK JV POSITIONED FOR COMPLETION

KEY METRICS & HISTORY TIMELINE

• 2020: 10 hospital portfolio acquired for

27% YOY AUM GROWTH SINCE 2020 ~$620M at a weighted average cap rate

$1B+ of ~6%

$980M

• 2021: Aspen acquisition and restructuring

$620M initiatives generated $150M+ of fair value

uplift. Cheshire Hospital acquisition of

$150M resulted in a regional AUM of ~$1B

2020 2021 2022

JV GROWTH STRATEGY

£600M (~$1B) ~5% 100%

UK Portfolio value - Of rents indexed

Portfolio cap rate

Achieving critical mass to inflation £600M (~$1B) £1.5B (~$2.5B)

Current AUM 3-5 yr AUM

100% +$350M

Occupancy Net Proceeds

LEADING UK PORTFOLIO WITH GREATER LONDON CONCENTRATION

9PLANNED US JV

ILLUSTRATIVE METRICS

~$750M 27 1.2M 5.5% Fully

Portfolio Assets Sq. Ft. GLA WACR Stabilized

OPPORTUNITY HIGH QUALITY PORTFOLIO

z Opportunity to expand global asset

management platform to a dynamic US

market generating significant fees and value

creation

z Targeting partnership with institutional sponsor

which is expected to lead to future growth

opportunities while reducing equity

requirements

>95% >10 Year >90%

Occupancy WALE Indexation

10GLOBAL JV FORMATION DRIVES NAV GROWTH

Pre-2020 2020-2022 2022+

Region

Capital

Partner(s)

TBD

Target

AUM($B) +$6.2B ~$5.0B ~$3.5B

Valuation* $400M $225M $125M

$625M $750M

UK + US JV

Current Valuation Target Valuation

11

* Based on implied 13x Year 1 Manager EBITDA mutlipleBALANCE SHEET OPTIMIZATION

Proforma LTV

Forecast

-320 bps

YoY 54.2%

52.1%

49.6% 49.8% 48.8%

48.5%

44.7%

47.5% 42.1%

44.3% 43.8%

43.1% 42.5%

41.9%

37.6%

35.3%

Q1 21 Q2 21 Q3 21 Q4 21 Q1 22 US Acquisition UK & US JV Series G

& Sub events Conversion*

Consolidated Proportionate

Net

Debt/EBITDA

8.5x 9.8x ~7.0x

JV formation in the UK and US

and debt optimization results in

Floating improved metrics

Rate 64% 21%

Exposure

12

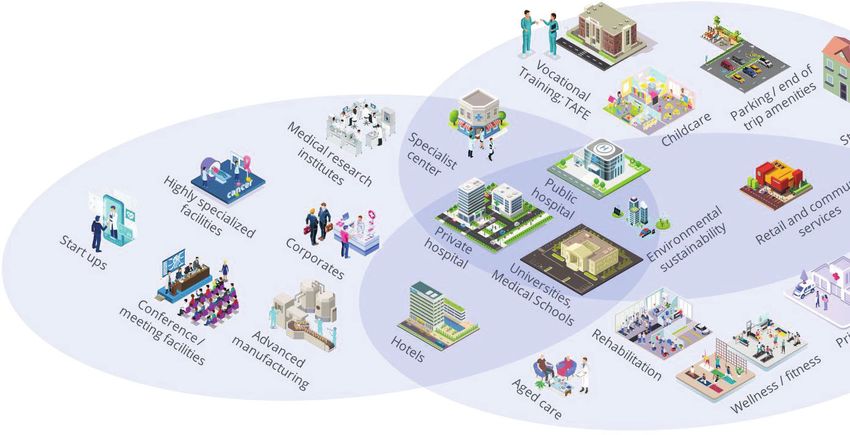

* Assumes Series G debentures are in the money and convert to equity at a strike price of $13.35GLOBAL HEALTHCARE PRECINCT STRATEGY

1 Intersection of

NORTHWEST IS healthcare,

HEALTHCARE AT THE CORE

INVESTING IN THE CORE education, and life

science

OF HEALTHCARE,

RESEARCH AND

2

KNOWLEDGE Growing PROJECT PIPELINE EXPANDING

PRECINCTS Opportunity WITH POTENTIAL VALUE OF $2.5B

3

Differentiated ATTRACTIVE RISK ADJUSTED

Return Profile RETURNS

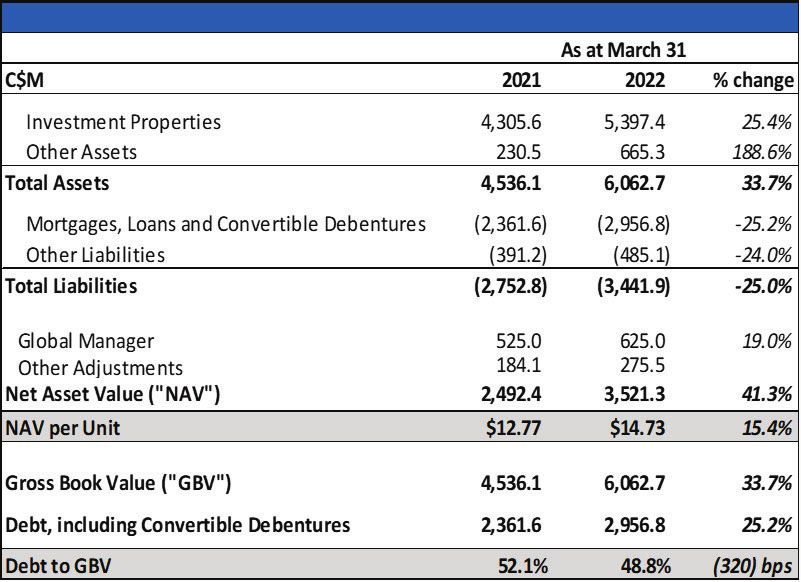

13FINANCIAL HIGHLIGHTS

14FINANCIAL DASHBOARD

Q1-21 Annualized Q1-22 Annualized

AFFO/unit (5) $0.83/unit $0.84/unit

LTV (6)/

44.3% / 52.1% 42.5% / 48.8%

Proportionate LTV

NAV (7) $12.77/unit $14.73/unit

Accretive JV Debt

Developments Deployment Repayment

15DELIVERING NAV GROWTH

15% YOY NAV/UNIT GROWTH ON PRIMARILY DRIVEN BY FAIR VALUE GAINS

$0.44 ($0.24)

$1.82 ($0.06)

$14.73

$12.77

Q1-21 NAV/Unit IPP revaluation Global Manager FX Other Q1-22 NAV/Unit

NAV growth driven by +$300M fair value gains & ~$100M valuation uplift from AUS JV expansion

Global Asset

Institutionalization Development

UK & US Joint Management

of Healthcare

Venture Initiatives Platform Accretion

Real Estate

Expansion

16EVOLUTION OF ASSET MANAGEMENT PLATFORM

SUCCESSFUL HISTORICAL CHART OF AUM AND OWNERSHIP

EXECUTION OF UK & US $12B

$10.3B $10.3B

100%

90%

JV WILL RESULT IN $10B

70%

$9.2B

80%

$6.5B $7.8B $5.4B

70%

LOOK-THROUGH $8B

56%

57%

60%

61% 48% 60%

OWNERSHIP $6B $3.4B $4.B

$4.1B 50%

$4.1B 40%

DECREASING TO ~48% $4B

$2.5B

30%

$1.2B

$6.2B

$5.2B $4.9B 20%

$2B $4.B $4.4B

$2.9B 10%

$B 0%

2018 2019 2020 2021 Q1 2022 PF Post UK &

US JV

Owned AUM Third Party AUM Look-through Ownership

BASE FEES CAGR OF ~29% RETURNS COMPARISON

$6,500M $100.M $100

$6,000M $5.9B $90.M Investment Direct JV

$5,500M (5% Cap Rate)

$80.M

$4.9B

$5,000M $68.7M Ownership 100% 30%

$70.M

$4,500M LTV 65% 65%

$60.M

$4,000M $47.5M Interest Rate ~3%

$3.3B $50.M ~3%

$3,500M $40.7M

$40.M NOI $5 $1.5

$3,000M $29.9M $22.4M

$30.M Fees N/A $0.4

$2,500M

$13.M Interest Expense ($1.9) ($0.6)

$2,000M $20.M

$25.1M $28.M

$1,500M $16.9M $10.M Total Return $3.1 $1.3

$1,000M $.M Equity Required $35 $10.5

Q1 2020 LTM Q1 2021 LTM Q1 2022 LTM

Base Fees Other Fees AUM ROE 9% 12%

17SIGNIFICANT VALUE CREATION IN GLOBAL ASSET MANAGER

Total Deployed & Available NWH

$B Status Term

~$11B OF ACTIVE Active

Capacity Committed Capacity Ownership

Australian Core

GLOBAL CAPITAL Hospital JV

Active $3.5 $3.2 $0.3 30% Perpetuity

COMMITMENTS Australian JV

Active $2.2 - $2.2 30% Perpetuity

Expansion

DRIVING SIGNIFICANT

Vital Active $2.7 $2.7 Open 27% Perpetuity

VALUE CREATION IN

European JV Active

THE REIT’S ASSET $2.8 $0.5 $2.3 30% 12 Years

MANAGER Total Commitments ~$11 $6.4 $4.8

Under

UK Healthcare Fund $2.5 $1.0 $1.5* 20%-30% +10 Years

Negotiation

Under

US Co-investment $0.8 $0.8 - 30%-50% Perpetuity

Negotiation

Global Healthcare

Preliminary $5.0 - $5.0 ~30% TBD

Precinct Fund

Under

Negotiation Total ~$20 $8.2 $11.3

$125M

$100M

$750M

$625M

$525M

Q4-21 AUS JV Expansion Q1-22 Under Negotiation Proforma

Valuation Valuation

AUM ($B) $9.0 $2.2 $11.2 $3.3 $14.5

18

* Capacity net of seed portfolioPROPORTIONATE INCOME STATEMENT

DEFENSIVE OPERATING

PERFORMANCE AND

ACCRETIVE INVESTMENT Increase driven by SPNOI

ACTIVITY COMBINED growth and investment activity

WITH MANAGEMENT Driven by increased

FEE GROWTH DRIVES deployment within global

asset manager

FINANCIAL RESULTS

10 bps

2.2% +21%

Reduction in

SPNOI Growth Base Fees

WAIR to 3.3%

19PROPORTIONATE BALANCE SHEET

~15% NAV PER UNIT

GROWTH DRIVEN BY

IMPROVED PROPERTY Includes +$300M Fair

VALUATIONS, $100M Value Gain

UPLIFT IN THE GLOBAL

MANAGER AND 320 BPS

OF DELEVERAGING

~$550M

Equity Issuance primarily

deployed towards

deleveraging

3.3% ~15% ~320 bps

WAIR NAV/Unit Growth LTV Reduction

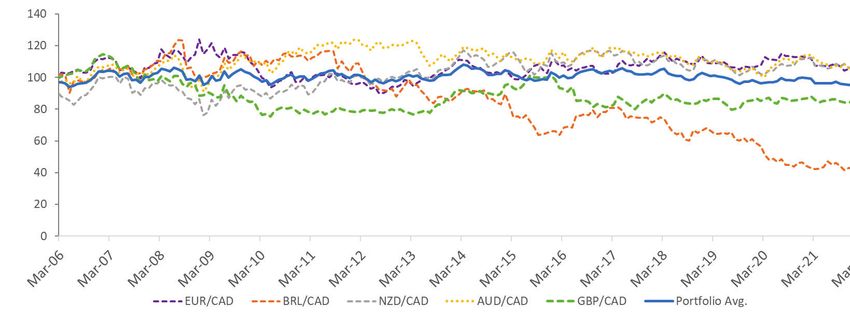

20RISK MANAGEMENT – FOREIGN EXCHANGE

OVER A 15 YEAR

PERIOD, THE REIT’S

NOI WEIGHTED

FOREIGN EXCHANGE

INDEX HAS REMAINED

RELATIVELY STABLE

RENTAL INDEXATION

ACTS AS NATURAL

CURRENCY HEDGE

PORTFOLIO SECURED

WITH LOCAL

CURRENCY DEBT

WHEREVER POSSIBLE

TO MINIMIZE FX RISK • Canada: FFX X • Europe: FX volatility • Au

Australia:

stra

st

tralililia

a: FX

appreciation due to expected due to appreciation due to

flight to stability regional conflict proximity to China’s

economic recovery

• Brazil: FX appreciation • UK: Stable FX due to

due to rising global greater certainty and • New Zealand: FX

commodity prices flight to stability within stability expected since

driven by the Europe the country is relatively

inflationary environment insulated from regional

conflicts

21GLOBAL HEALTHCARE

TRENDS

22HEALTHCARE TRENDS IMPACT ON HEALTHCARE REAL ESTATE

HEALTHCARE TRENDS are driving real estate opportunities.

Outpatient / Increased

Aging Operator Increasing

Urbanization funding

population home care consolidation asset size

needs

Limited

Positive Positive Positive Positive Positive

Hospitals impact

Outpatient / Positive Positive Positive Positive Positive Positive

Medical Office

Limited Limited

Care Positive Positive Positive Positive

impact impact

Facilities

Life Sciences Positive Positive N/A N /A Positive Positive

/ Research

23INVESTMENT ACTIVITY

24CONSOLIDATED INVESTMENT ACTIVITY

2022 TRANSACTIONS

TYPE REGION C$M

US Portfolio Acquisition Acquisition US 753

Normal Course Acquisitions Acquisition Various 125

CHESHIRE HOSPITAL UNITED KINGDOM

Total 878

2021 TRANSACTIONS

HIGHLIGHTED

TYPE REGION C$M

TRANSACTIONS

AUSTRALIA GERMANY

Netherlands MOB Acquisition NL 176

Australian Unity

M&A AUS 127

Acquisition

Cheshire Hospital Acquisition UK 153

Epworth Geelong &

Acquisition AUS 117

ELIM Hospital

NORMAL COURSE

TYPE REGION C$M

TRANSACTIONS

Normal Course Acquisitions Acquisition Various 347

Normal Course Dispositions Disposition Various 55

Total 975

25COMMITTED DEVELOPMENTS

• ~$304.1M (fully consolidated; $128.8M proportionate) of committed low risk development &

THE REIT IS expansions in Australasia, Europe, Brazil and Canada to be funded through a combination of

existing resources and property financing

LEVERAGING ITS

$232.7M ($64.1M proportionate) of Australasian hospital and MOB expansions

SIGNIFICANT $18.5M ($11.9M proportionate) of European developments

EXPERTISE AND $28.9M of Brazilian hospital expansions

$24.0M of Canadian MOB development

EXPERIENCE WITHIN

THE INDUSTRY TO

Anticipated

Cost to Pre-Leased

DELIVER AN Country (8) Projects Est. Completion Project Cost Project

Complete Occupancy

Yield

ADDITIONAL $304M

OF VALUE 11

Q2 2022 to

232.7 184.5 74% 6.1%

Q4 2024

ENHANCING

PROJECTS TO ITS

2 Q2 2022 18.5 3.2 90% 5.2%

PORTFOLIO

THE REIT’S 2

Q2 2022 to

28.9 28.9 100% 7.5%

Q4 2022

DEVELOPMENT

PIPELINE OF $2B

1 Q3 2022 24.0 5.1 62% 7.1%

DRIVES FUTURE

GROWTH

16 304.1 221.7 76% 6.3%

Note: represents post-quarter close development metrics

26PORTFOLIO OVERVIEW

27ASSET MIX BY REGION AND SEGMENT

ON A PROPORTIONATE PROPORTIONATE NOI DIVERSIFICATION

BASIS HOSPITALS Q1 2022 Q1 2022

Life

ACCOUNT FOR 60% OF Australasia

Canada Hospital and Sciences

25% 2%

26% Healthcare

NET OPERATING 27%

Facilities 2%

Q1 2021 27% Q1 2021

INCOME 60%

61%

REGIONS ASSET MIX

INCREASING FOCUS 37%

38%

17% MOB

18%

ON HEALTHCARE 29% Brazil

31%

INFRASTRUCTURE,

Europe

INCLUDING

ACUTE/POST ACUTE Detailed Segment Breakdown

HOSPITALS AND

AUS NZ BRL CAD GER NL UK

RELATED BUILDINGS IN

EACH OF ITS MARKETS Acute hospitals

Post-acute hospitals

MOBs

Aged care

LLife Sciences

High Priority Low Priority

28STRATEGIC RELATIONSHIPS AND TENANT DIVERSIFCATION

STRATEGIC RELATIONSHIPS ALLOWING FOR BEST-

TOP 10 TENANTS BY GROSS RENT(9)

IN-CLASS PERFORMANCE

TENANT REGION % GROSS RENT • Alberta Health Services (6

Locations): Largest provincial

1

healthcare provider to 4.3 M

Healthscope

He

e Limited 13.9% Albertans

2

Rede

Re

e D’or 8.0%

3

Epworth

Ep

p Foundation 5.9%

4

Aurora Healthcare

A

Au 4.8% • Median (5 Transactions): Germany’s

largest private provider of

5

rehabilitation services

Nuffield Health

N

Nu 4.7%

6

HealtheCare

He

e 3.5%

7

Circle

C i Health Group 2.3%

• Epworth Foundation (7 transactions):

8 The largest not-for profit hospital

Evolution

Ev

v Group 1.9% operator in the Australian state of

Victoria

9

Median Kliniken

M 1.5%

10

Spire

SSp

p Healthcare 1.2%

• Rede D’Or (7 transactions):

Top 10 Tenants 47.7% Brazil’s leading hospital

operator

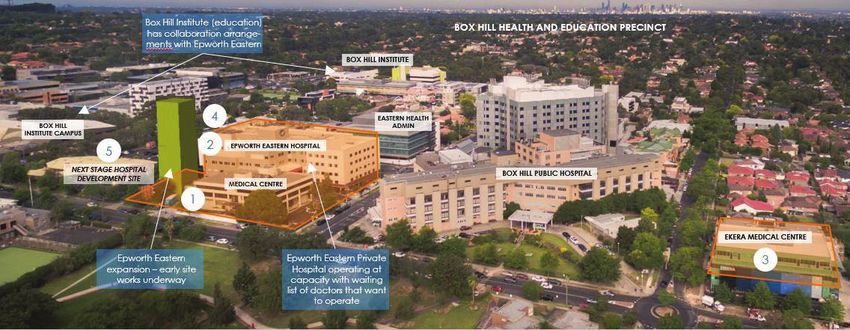

29CASE STUDY – EPWORTH EASTERN HOSPITAL, MELBOURNE

NON-FOR-PROFIT PRIVATE

HEALTHCARE GROUP THAT

RAISES FUNDS TO

PURCHASE ADVANCED

MEDICAL EQUIPMENT,

NorthWest has supported Epworth over 15+ years with expansion opportunities, advice and capital. Developments

FUND RESEARCH AND have added to the quality & value of assets, driving operational benefits & efficiencies that attract practitioners.

PROVIDE BEST POSSIBLE 2003-05 2014-17 2017-21

CARE TO PATIENTS Private hospital

Public and private hospitals Eastern Private Hospital

development leads to

EPWORTH EASTERN IS A drive health precinct announces major expansion

formation of precinct

LEADING HOSPITAL WITH

223 BEDS AND STATE OF • Development of Epworth Eastern • Acquisition of Ekera Medical Centre • $125m expansion of Epworth

Hospital (private) increases NorthWest assets in Eastern Hospital

THE ART EQUIPMENT AND • Establishes operator relationship precinct • Construction is in progress and

with Victoria’s largest not-for-profit • Strategic acquisition of adjacent site remains on target for late 2021

TECHNOLOGY private healthcare group for private hospital expansion completion.

• Public and private hospital co- • Public hospital major expansion • Epworth Eastern Hospital at

location further attracts specialists • Council designated ‘Education and capacity for 3 years

• Begins to drive early stage precinct Health precinct’ – targeted as a • New 30-year lease term over entire

formation high growth area with increased expanded hospital

density

30INVESTMENT OPPORTUNITY

31NORTHWEST OVERVIEW

GLOBAL HEALTHCARE REAL ESTATE INVESTMENT PARTNER

Global Dynamic

Capital Capital

Relationships Allocation

Accretive Strategic

Acquisition

Opportunities

NWH.UN Operator

Partnerships

Regional LISTED Brownfield

Operating Development

Platforms

TSE Opportunities

Healthcare Long Term

Precincts in Indexed

Urban Locations Leases

32ENVIRONMENTAL, SOCIAL AND GOVERANCE

NWH is committed to creating a more sustainable future through the implementation of a

comprehensive ESG program underscored by four key pillars resulting in key 2022 commitments:

Inclusive Company Thriving Partners Strong Communities Healthy Planet

Building for our current Preparing lasting Investing in the Deepening our

team members as well as tenant spaces for health communities we serve contribution to a

our future employees and healing healthy planet

• Establish a globally • Formalize a global survey • Pledge a contribution of • Achieve Net-Zero GHG

consistent employee for all tenants with an $5M in support of emissions by 2050. Over

experience with an ambition to achieve top academic research about the next 12 to 24 months,

ambition to achieve top quartile performance on the impacts of the we will round out our

quartile NPS tenant NPS pandemic on health baseline on emissions

performance systems across the world and establish a science-

• Define a three-year

based 2030 interim

• For every open senior schedule to complete air • Launch an employee

reduction target

leadership position and quality and wellness volunteer program

for as many other open reviews for 100% providing two days per • Conduct energy audits

positions as possible, landlord-controlled year of paid time off to across 100% of landlord-

with a goal of 90%, properties further support the controlled properties,

Consider at least one communities NWH serves helping to further inform

• Collaborate with tenants

woman or one minority energy reduction and

on sustainable

in the slate of conservation actions

construction guidelines

candidates

for renovations and • Submit to GRESB

• Deploy targeted developments evaluation

sustainability training

33INVESTOR FACTSHEET

Ticker NWH.UN

Listed Exchange TSX

Distribution Payable Monthly

40% Other Income/

Distribution Type 46% Return on Capital/

14% Capital Gain

Unit Price (May 12, 2021) $12.53

Market Capitalization ~$3.0B

Distribution Yield 6.4%

52-Week Trading Range $12.35-$14.42

Volume Weighted Avg. Price (VWAP) (20-day) $13.57

Average Daily Volume (90-days) ~917,000

NAV/Unit (Q1 2022)(7) $14.73

34NOTES

1. Based on NWH.UN’s closing unit price of $12.53/unit as of May 12, 2022.

2. Based on the REIT’s distribution policy of $0.80/unit per annum and Q1-2021 annualized AFFO/Unit of $0.84

3. Based on total assets under management of NWH pro-formal completion of the US portfolio acquisition, Vital Trust on a fully

consolidated basis including post-quarter acquisitions. NWH owns a 27.5% interest in Vital Trust.

4. The pie chart fully reflects consolidated NOI and includes i) post- quarter acquisitions ii) 100% of NOI from Vital Trust and iii) 100% of the

NOI from the REIT’s institutional JVs including the Healthscope portfolio and European JV.

5. AFFO/unit is based on annualized Reported AFFO/unit and adjusted for acquisitions, and financings as presented in the REIT’s –Q1 2022

MD&A PART III.

6. LTV includes convertible debentures and is shown on a fully consolidated basis (Vital Trust at 100%) and includes the HSO portfolio

accounted for using the equity method.

7. NAV is based on unitholder’s equity plus add-backs as set out in Part XII in the REIT’s Q1 2022 MD&A.

8. Presented on a fully consolidated basis. Assuming projects are 100% debt funded at the existing region’s financing costs and is for

indicative purposes only.

9. Gross rent on a fully consolidated basis.

35NON-IFRS MEASURES

Non-IFRS measures defined in Q4 2021 MD&A

1. FFO

2. AFFO

3. FFO per Unit

4. AFFO per Unit

5. AFFO Payout Ratio

6. EBITDA

7. Adjusted EBITDA

8. Investment Properties on a proportionate basis

9. Proportionate Management Fees

10. Interest Coverage

11. Cash Flows from Operation Activities Attributable to Unitholders

12. Distributions

13. Net Asset Value (“NAV”)

14. Constant Currency Same Property NOI (”Same Property NOI”/“SPNOI”)

36CONTACT INFORMATION

NORTHWEST HEALTHCARE PROPERTIES REIT

Paul Dalla Lana, Chairman & CEO

pdl@nwhreit.com

416-366-2000 Ext. 1001

Shailen Chande, CFO

shailen.chande@nwhreit.com

416-366-2000 Ext. 1002

37You can also read