Preface: The COVID-19 Pandemic and Mineral Resources - Society of Economic Geologists

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

26 SEG DISCOVERY No 122 • JULY 2020

Preface: The COVID-19 Pandemic and Mineral Resources

Jean Cline, President, Society of Economic Geologists and

Lawrence D. Meinert, Editor, Economic Geology

Pandemics are one of the few events fallout of attempts to contain the dis- a snapshot in time that sets the stage

that are truly global and affect all of ease. Many universities and mines are for the second article, by Simon Jowitt,

humanity. Even World Wars I and closed, research and exploration bud- that offers a preliminary economic

II, as terrible and far-reaching as they gets curtailed, and most travel halted. analysis of possible effects on prices,

were, did not affect all corners of At the time of writing, no one knows stocks, and supply and demand within

the globe, and certainly not equally. how the pandemic will evolve—are we the minerals industry.

Pandemics are different, especially in past the worst of it or are there new The phrase “the new normal” has

light of modern transportation and the waves coming? been used frequently to describe the

interconnectedness of global business, Following this preface are two effects and after-effects of the COVID-19

education, and supply chains. One rapid-response articles to offer a pre- pandemic. The following two stud-

does not have to be a major partici- liminary assessment of the impact of ies are complementary and provide a

pant in the global economy or even be COVID-19 on the minerals industry framework for assessing where we are

aware of the disease at all to be affected, and all of us who are connected to today and for beginning the process

infected, or possibly killed. it. The first article, by Hitzman et al., of planning for the future. Although

Although the long-term effects of reports the results of a survey about it is likely that both articles would be

COVID-19 are not yet known, there are the pandemic’s effects on the lives, written differently a year or two from

few in the minerals sector who have education, and business of people now, they are presented here while the

not been affected, whether it be by the in the minerals industry. Although pandemic is still unfolding to provide

loss of a loved one or by the economic necessarily limited in scope, it provides the view from July 2020.

Impact of the COVID-19 Pandemic on the Minerals Sector:

A Real Time Survey

Murray Hitzman†, David Kaeter, Aileen Doran, Maeve Boland, Lingli Zhou,

David Drejing-Carroll, Subaru Tsuruoka, Sean Johnson, Siobhan Burke,

James Stratford, Aoife Brady, and Fergus McAuliffe

Irish Centre for Research in Applied Geosciences, University College Dublin, Belfield, Dublin 4, Ireland

Introduction

Abstract 45% of respondents suffered negative

effects. More often, younger respon- The COVID-19 pandemic caused by

Through the implementation of an dents (ages 18–30) reported lost jobs the novel (new) coronavirus affected

online survey, run at the end of April (14%) whereas older survey participants human activity across the planet in

2020, researchers at the Irish Centre for reported working reduced hours (21%, 2020. Early cases of COVID-19 were

Research in Applied Geosciences (iCRAG) ages 46–60). Respondents working in recorded in China in December 2019

explored the immediate effects of the mineral exploration were most affected (Huang et al., 2020) and the first cases

COVID-19 pandemic on the miner- (40% suffered negative job impacts), but outside China were confirmed in

als sector workforce. With more than the impact across base, industrial, and

1,000 respondents, the survey provides mid-January 2020 (World Health Orga-

precious metals was broadly similar for nization, 2020a). The World Health

insights into the impact of an unprece- all participants; government employees

dented global event at a crucial point in Organization (WHO) set up an Incident

were least affected but were not immune

its development. Seven weeks after the Management Support Team on January

(10% on reduced hours). The level of

World Health Organization’s declaration concern about future job security due to 1, 2020. With increasing numbers of

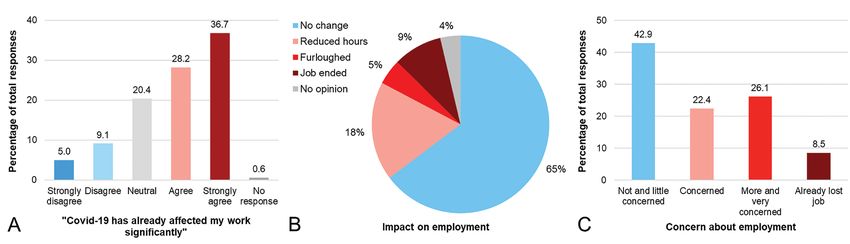

of the pandemic, 65% of survey respon- the COVID-19 crisis varied, with 35% of cases throughout the world, the WHO

dents agreed that COVID-19 had a signif- respondents being more or very con- declared the COVID-19 outbreak to be

icant impact on their work. Overall, 32% cerned or having already lost their jobs, a pandemic on March 11, 2020. Over

of respondents had experienced negative 43% had little or no concern, and 22% 10 million cases and in excess of a half

impacts on their employment, having were moderately concerned. The survey million deaths were reported world-

either lost their jobs or been furloughed/ captured the experiences and percep- wide to the end of June 2020 (Euro-

temporarily laid off, or were working tions of individual workers, providing a pean Centre for Disease Prevention and

reduced hours. perspective different from information Control, 2020; WHO, 2020b).

Geographically, the greatest impact available in corporate statements and Outbreaks of COVID-19 over-

on employment was in Africa, where official statistics. whelmed medical facilities in several

regions, leading governments through-

†

Corresponding author: e-mail, murray.hitzman@icrag-centre.org

doi:10.5382/SEGnews.2020-122.fea-01 out the world to enforce restrictions

No 122 • JULY 2020 SEG DISCOVERY 27

to prevent the spread of the illness. in other time zones to respond within (6% each), and Australia (5%). How-

Wuhan, the Chinese city of 11 mil- the May 1 deadline. ever, 13% of the responses did not list

lion people at the center of the initial A link to the online survey was a country of origin. Respondents were

outbreak, for example, entered a 76-day distributed by the authors via email to fairly evenly divided by age (Fig. 1B).

lockdown in response to the virus on their contacts in the minerals sector The largest cohort of respondents (32%)

January 23, 2020. Measures included with a request that they fill out the sur- were aged 31–45, whereas 28% were

closure of non-essential businesses, vey once and pass the link on to others older than 61 years of age, 23% were

travel restrictions, border closures, quar- in the mineral exploration, mining, and age 46–60, and 17% were 18–30 years

antines, social distancing, limits on the minerals research sectors. Information old. In relation to current employment

number of people who could congre- about the survey was sent to the eco- status, 55% reported being currently

gate, and cancellation of many in-per- nomic geology group of the Geological employed whereas 26% listed them-

son gatherings. Lockdowns to varying Society of Australia, International Asso- selves as consultants, 10% said they

degrees were put in place virtually ciation on the Genesis of Ore Deposits, were students, 5% were retired, and 4%

around the world by the end of March Irish Mining and Quarrying Society, reported being unemployed (Fig. 1C).

2020 (Hale et al., 2020). Some govern- Irish Association for Economic Geology, Respondents were asked to iden-

ments deemed mining and mineral Ore Deposits Hub, Society for Mining, tify the sector in which they worked:

exploration to be essential businesses Metallurgy & Exploration, and student mineral exploration, mining, minerals

that could remain open. Temporary chapters of the Society of Economic research, or other. Some respondents

mine closures were especially common Geologists worldwide. These groups selected multiple sectors, leading to

in Latin America and South Africa, but shared the information with members many different combinations; there-

some operations in the United States, in various ways, including mentioning fore, we aggregated responses in order

Canada, and elsewhere also reported it online, in member mailings, podcasts, to simplify the analysis, as explained in

reduced activity (S&P Global, 2020). and webinars. iCRAG intentionally did Boland et al. (2020). Based on additional

Mineral exploration was severely not publicize the survey via social media information provided by those who

affected by travel restrictions. such as LinkedIn in order to ensure, chose “other,” we created a new cate-

To better understand the impacts to the extent possible, that it would gory of “government.” Following these

of COVID-19 on the minerals sector, remain within the minerals sector. procedures, the respondents represented

researchers at the Irish Centre for A total of 1,010 English-language 54% mineral exploration, 22% mining,

Research in Applied Geoscience (iCRAG) plus 40 Chinese responses were received 17% minerals research, 2% government,

launched a short online survey at the by the closing date. Of the 1,050 and 5% other (Fig. 1D). The other cat-

end of April 2020. The survey was responses, 1,007 contained sufficient egory included environment, educa-

designed to determine the immediate information to be included in the anal- tion, law, services, policy, engineering

effects of the pandemic on people in ysis. Data from the survey and informa- geology, petroleum, drilling, health and

the minerals sector and how the effects tion on how the data were processed are safety, information technology, corpo-

were distributed in terms of geographic available on the iCRAG website (Boland rate social responsibility, and water.

area, sector of the minerals industry, et al., 2020). For primary focus of work, respon-

and commodity. The survey asked about Choosing to distribute the survey dents were asked to choose one option

the impacts on people’s employment, through personal contacts and selected from the following: base metals,

the nature of the impact, and the level organizations and allowing respondents industrial metals, precious metals, or

of concern individuals had concerning to self-select means that the survey is not other. Where respondents provided

job security due to COVID-19 for the based on a completely random sample details under “other” the responses were

remainder of 2020 (Boland et al., 2020). and it is thus impossible to estimate the classified as “other” if they mentioned

The survey fortuitously captured data response rate. The survey was designed a commodity—responses included coal,

just before many different parts of the to be simple and rapid, with an esti- critical minerals, uranium, potash, salt,

world began to open up after a nearly mated completion time of less than three construction materials, oil and gas,

global lockdown. Thus, the results cap- minutes. In order to minimize barriers and helium. If the response indicated

ture opinion at the height of the initial to participation and to meet the require- support services such as education, soft-

response to the pandemic. ments of our ethical approval, respon- ware, drilling, they were categorized as

dents were not required to sign in and “no data” to indicate that they were not

Methodology all responses were kept anonymous; it linked to a single commodity. Follow-

is possible that some people could have ing these procedures, the respondents

An eight-question English-language responded more than once. represented 47% precious metals, 32%

survey was created in Google Forms base metals, 7% industrial minerals, 9%

in consultation with an iCRAG social other, and 5% who were classed as none

scientist, followed by an ethics review Response Demographics

listed (Fig. 1E).

at University College Dublin (Boland et Responses were received from individuals

al., 2020). Since Google is not accessible whose most recent employment spanned

in Mainland China where the pandemic 55 different countries. In terms of most Results

began, a duplicate of the question- recent employment location, the largest The pandemic had a significant impact

naire, in English, was created through a response was from those employed in on people in the minerals sector by the

Chinese survey website. The survey was North America (49% of the respondents; end of April 2020, less than six months

posted online on April 23, 2020, and Fig. 1A). The second largest response after the first cases occurred and within

was held open for responses until noon group was from Europe (14%), followed seven weeks of the declaration of a

GMT on May 2, 2020, allowing people by Asia (7%,) Africa and South America pandemic.

28 SEG DISCOVERY No 122 • JULY 2020

Impact of the COVID-19 Pandemic on the Minerals Sector: A Real Time Survey (continued)

change whereas 18% reported reduced

hours, 4% reported being furloughed,

and 9% reported having been laid off.

Four percent of participants reported

“no opinion” (Fig. 2B). The highest rate

of change in employment status was

from Africa, where 45% of respondents

reported negative employment activity,

defined as job loss, furlough, or reduced

hours (Fig. 3A). South American respon-

dents were next, with 34% reporting

negative employment activity. Europe

appeared to be the most stable, with

70% of respondents experiencing no

change in employment status followed

by Asia and North America, where 66%

of respondents reported no change in

employment status.

Currently employed (78%) and retired

(83%) individuals stated they had not

seen a change in employment due to the

COVID-19 crisis (Fig 3B). Fifty-six per-

cent of consultants indicated a change in

employment conditions, predominantly

reduced hours, due to the pandemic.

Twenty-five percent of students reported

either being either laid off or furloughed

since the start of the pandemic. Look-

ing at change in employment by age

(Fig. 3C), the youngest cohort (ages

18–30) reported the highest percentage

of lay-offs (14%) followed by the 31- to

Fig. 1. iCRAG COVID-19 Survey demographic data. A. Responses by continent. B. Responses

by age group. Four responses with no data (

No 122 • JULY 2020 SEG DISCOVERY 29

Fig. 3. iCRAG COVID-19 Survey responses on the impact of the pandemic by group. A. Impact on employment status by geographic

region. B. Impact on employment status by type of current employment. C. Impact on employment status by age. D. Impact on

employment status by employment sector. E. Impact on employment status by commodity the survey participant was involved with.

and 6% reported having been fur- industrial metals, and precious metals level of concern varied by geographic

loughed (Fig. 3D). Both mining and sectors was broadly similar (Fig. 3E). area among the respondents (Fig. 4A).

minerals research were less affected; Some 36% of African respondents were

nevertheless, 24% of respondents from Concern about job security due very concerned about job security going

the mining sector and 18% of those in to COVID-19 in 2020 forward due to the pandemic. Respon-

the minerals research sector reported Looking to the future, 26% of respon- dents from South America were next in

negative employment changes. The dents were very concerned (scoring 4 line with 33% stating strong concern.

government sector reported the least or 5 on a 5-point scale) about future These areas also had the highest rate of

change in employment though even employment due to the pandemic, 43% job loss due to the pandemic. Approx-

there 10% of respondents reported stated they had little or no concern imately 50% of respondents from Asia

reduced hours due to the COVID- about future employment, while 22% and Australia had little to no concerns

19 crisis. The impact of COVID-19 were moderately concerned, and 9% about employment in 2020 going

on employment in the base metals, had already lost their job (Fig. 2C). The forward. Even though Europe showed

30 SEG DISCOVERY No 122 • JULY 2020

Impact of the COVID-19 Pandemic on the Minerals Sector: A Real Time Survey (continued)

the least change in employment due to unemployed (32%) being the most of the 31- to 45-year-old cohort being

the pandemic, 30% of its respondents concerned, followed by consultants very concerned and a further 22% being

recorded being very concerned about (29%), then students (28%), and those concerned about job security in 2020.

employment for the rest of 2020. employed (25%); retired respondents However, younger people were not far

The survey results for job security were the least concerned. Concerns by behind, with 27% of the 18- to 30-year-

concerns in 2020 by current employ- age (Fig. 4C) indicate that those aged 31 olds reporting that they were very con-

ment status (Fig. 4B) showed the to 45 were most concerned, with 30% cerned. Older people were somewhat

Fig. 4. iCRAG COVID-19 Survey responses on concern about the impact of the pandemic. A. Concern about employment by geographic

region. B. Concern about employment by type of current employment. C. Concern about employment by age. D. Concern about

employment by employment sector. E. Concern about employment by commodity the survey participant was involved with.

No 122 • JULY 2020 SEG DISCOVERY 31

less concerned about the impact of the initial reopening of many economies. 2020, the overall number of press

pandemic on their employment for Although Wuhan entered quarantine releases began to drop in mid-February

2020, with 23% of 46- to 60-year-olds, on January 23, 2020, known cases 2020, perhaps reflecting a decrease in

and 24% of the group aged over-60 outside of China did not rise signifi- corporate activity. COVID-19 was first

reporting strong concern. cantly until March (Fig. 5A). The WHO mentioned in these mining company

Slightly over 50% of those in both announcement of the COVID-19 pan- press releases in mid-February in

the base metals and the industrial demic on March 11, 2020, was quickly connection with delayed shipments of

minerals sectors were somewhat to very followed by lockdowns worldwide as mine construction components from

concerned about job security (Fig. 4D). demonstrated by school closures (Fig. China. COVID-19 was mentioned

Those in the precious metals sector 5B). The survey at the end of April was frequently in press releases during April

fared slightly better, with 48% showing conducted just after the first peak of and May 2020. Some press releases

concern or significant concern. By sec- COVID-19 cases in the United States, provided information on mine closures

tor, those in mineral exploration were while weekly newly confirmed COVID- or suspension of activities. Several press

the most concerned about job security 19 cases were still very high in Europe, releases highlighted corporate efforts

in 2020 followed by those in mining but prior to a sharp rise in cases in to mitigate the impact of the pandemic

and in the “other” job sector category Brazil and India (Fig. 5A). on workers and local communities,

(Fig 4E). Not surprisingly, government Public interest in the pandemic, as including improved health and safety

employees had the least concern though represented by daily Google searches measures, donations of personal pro-

even in this group approximately 18% for the topic “Coronavirus” and related tective equipment, water, and food,

expressed concern or strong concern. terms (Google LCC, 2020) peaked coin- as well as providing education about

cident with the WHO announcement COVID-19. However, it proved very

Discussion and then began a slow decline through- difficult to derive a comprehensive pic-

This survey reflects the experiences of out March and April (Fig. 5C). Daily ture of the impacts of the pandemic on

a self-selected section of people in the Google searches for the topic “Unem- the minerals sector from press releases,

minerals industry at a particular point ployment” and related terms show a reflecting the selective nature of the

in time. We cannot ascertain how well nearly tenfold increase in late March information provided.

the respondents represent the total compared to the beginning of the year Perhaps the most surprising result

workforce because there are no readily (Fig. 5D), likely reflecting global con- from the survey is that while 65% of

available data on the demographics of cern about job losses as a consequence respondents felt that COVID-19 had

the global minerals sector workforce. of COVID-19 containment measures. significantly impacted their work,

There are some general indications that Search interest in the topic “Unemploy- only about a third of the respondents

the survey results are credible. The age ment” gradually decreased in April but, reported a significant change in employ-

distribution matches well with the age by the end of June, was still about five ment status. At the time of the survey

distribution of employees in the U.S. times higher than in the beginning of the globe was largely in lockdown

“metal ore mining, nonmetallic mineral the year (Fig. 5D). The decreasing inter- (Fig. 5B), people in most non-essen-

mining and quarrying, and not specified est in both “Coronavirus” and “Unem- tial sectors were working from home,

type of mining” employment catego- ployment” search topics corresponds to and some had been furloughed or laid

ries for 2019, with 49% of all survey the gradual easing of COVID-19 con- off. The fact that nearly two-thirds of

respondents being under 45 vs. 52% tainment measures around the world respondents did not report significant

reported by the Bureau of Labor Statis- after the iCRAG survey was conducted impact on their employment status

tics (2020a). The number of respondents at the end of April. As government illustrates how the mining and min-

from the United States who reported responses became less stringent globally eral exploration industry differs from

losing a job (6.6% of 303 survey (Hale et al., 2020), nationwide school many other industries and sectors of

responses) is very close to the reported closures became less common (Fig. 5B), employment. This may reflect the fact

loss of jobs in the U.S. mining (except and people began to travel more in that some countries considered mining

oil and gas) workforce between January May, as indicated by the daily number to be an essential activity, meaning that

and April 2020 of 6.8% (U.S. Bureau of routing queries for driving and pub- mines remained in operation. Some

of Labor Statistics, 2020b). Data from lic transport in the Apple Maps appli- companies quarantined workers at mine

Australia indicate that expenditure on cation (Fig. 5E; Apple Inc, 2020). The and exploration sites to enable them to

exploration on areas including existing survey was also conducted just as mine keep working without contact outside

deposits fell 16.0% and on areas of new closures were beginning to wind down the workplace. In mineral exploration

deposits by 26.1%; base metals projects and some mines that closed earlier in it appears many were transferred from

were impacted more than gold or iron the pandemic were beginning to reopen fieldwork to work on desk studies that

ore projects (Australian Bureau of Statis- (S&P Global Market Intelligence, 2020). did not entail travel, especially inter-

tics, 2020). Our survey results show that Company press releases are a key national air travel which was largely

employment in the exploration sector source of corporate information on the interrupted (Fig. 5E). Though details

was most affected but indicated less minerals sector and were examined were not requested in the survey, the

differentiation between the base and to provide additional context for our high percentage of students (25%)

precious metals sectors. survey results. Based on an analysis reporting either being laid off or fur-

The timing of the survey may of 1,234 press releases from publicly loughed since the start of the pandemic

have been fortuitous in capturing traded junior resource companies may represent loss of research project

responses at the cusp between global collated by the Junior Mining Network or internship funding and/or inability

awareness of the pandemic and the (2020) between January and mid-June to complete research due to closure of

32 SEG DISCOVERY No 122 • JULY 2020

Impact of the COVID-19 Pandemic on the Minerals Sector: A Real Time Survey (continued)

labs or restrictions on fieldwork

(Gonzales and Keane, 2020).

The survey demonstrates

that while there were significant

similarities in response to the

pandemic by individuals in the

mineral industry worldwide,

differences can be discerned

geographically. The pandemic

was severe in Europe and North

America at the end of April and

there was widespread apprecia-

tion of its potential long-term

effects, but many people were

beginning to move (Fig. 5E)

indicating a weakening of the

lockdowns. The survey results

reflect this with large majori-

ties stating that the pandemic

had affected their work to

some degree and with wide-

spread worry about the future

in terms of employment. The

very high levels of concern in

Africa and South America are

notable because at the time of

the survey the pandemic had

not led to the dramatic number

of reported cases and deaths

in these areas compared to

those then observed in Europe

and North America. However,

according to our analysis of

mining company press releases

and data collected by S&P

Global (2020), minerals sector

operations in Latin America and

South Africa were most affected

by COVID-19 containment

measures.

Most of the survey results

are what would be expected

in terms of response by age

and by employment status

with younger employees and

consultants most affected.

Results by type of employment

were predictable with those in

the mineral exploration sector

both most affected and also

most concerned, reflecting the

Fig. 5. Comparison of time series relating to the COVID-19 pandemic from January to June 2020. Vertical

lines indicate the announcement of the quarantine in Wuhan, China (23.01.2020), and declaration of the typical response to a down-

COVID-10 pandemic by the World Health Organization (11.03.2020); the shaded area highlights the time turn in the minerals industry

of the iCRAG survey (23.04.–01.05.2020). A. Weekly number of newly confirmed COVID-19 cases for a when exploration spending

selection of countries (European Centre for Disease Prevention and Control, 2020). B. Number of countries is commonly an early cau-

declaring country-wide or local school closures (UNESCO, 2020) as part of their COVID-19 containment sality followed by changes of

measures. C. Google Trends data for daily relative global interest in the topic “Coronavirus” (Google LCC,

2020). The Google Trends data for topics include Google searches in different languages and for related employment for temporary or

terms. D. Google Trends data for daily relative global interest in the topic “Unemployment” (Google LCC, contract employees.

2020). The periodicity of the data reflects variation between weekdays and weekends. E. Relative change

in driving, public transport (Apple Mobility Trends, Apple Inc, 2020) and commercial flights (Flightradar24,

2020). The daily Apple Mobility Trends data show relative change from January 13, 2020, for routing queries Conclusion

in Apple Maps. Data for driving are the daily averages for 63 countries; data for public transport are the The survey provides insights

daily averages for 27 countries. Data for daily global commercial flights show relative change from January

20, 2020. The periodicity of the data reflects variation between weekdays and weekends.

into the effects of COVID-19 on

the minerals sector workforceNo 122 • JULY 2020 SEG DISCOVERY 33

at a distinctive point in time during an Gonzales, l., and Keane, C., 2020, COVID- Stephany, F., Stoehr, N., Darius, P., Neuhäuser,

unprecedented global event. It captures 19 impacts to research activities in spring L, Teutloff, O., and Braesemann, F., 2020,

2020: American Geosciences Institute Data The CoRisk-Index: A data-mining approach

the experiences and perceptions of indi- Brief 2020-009; June 26, 2020, https://www. to identify industry-specific risk assess-

vidual workers, providing a perspective americangeosciences.org/geoscience-cur- ments related to COVID-19 in real time:

that is different from the information in rents/covid-19-impacts-research-activi- Working Paper, v. 1, March 2–30, 2020,

corporate statements and official statis- ties-spring-2020. arXiv:2003.12432v2 [econ.GN]

Google LCC, 2020, Google trends: https:// 30 Mar 2020.

tics. Surveys such as this can supplement

trends.google.com/trends/. UNESCO, 2020, School closures caused by

other approaches such as economic Hale, T., Angrist, N., Kira, B., Petherick, A., Coronavirus: https://en.unesco.org/covid19/

analyses and data-mining studies (e.g., Phillips, T., and Webster, S., 2020, Variation educationresponse.

Stephany et al., 2020) as we strive to in government responses to COVID-19, Ver- U.S. Bureau of Labor Statistics, 2020a, Labor

understand the full implications of the sion 6.0: Blavatnik School of Government force statistics from the current population

Working Paper, May 25, 2020, https://www. survey: Household data annual averages:

COVID-19 pandemic. bsg.ox.ac.uk/sites/default/files/2020-05/ 18b. Employed persons by detailed industry

BSG-WP-2020-032-v6.0.pdf. and age, 2019: https://www.bls.gov/cps/

Acknowledgments Huang, C., and 28 others, 2020, Clinical cpsaat18b.htm.

features of patients infected with 2019 U.S. Bureau of Labor Statistics, 2020b,

We wish to thank all those that took novel coronavirus in Wuhan, China: Employment, hours, and earnings from

part in the survey as well as those who Lancet, v. 395, p. 497–506, https:// the current employment statistics survey

helped spread awareness of its existence. www.thelancet.com/action/showPdf?pi (national): All employees, thousands, min-

i=S0140-6736%2820%2930183-5. ing, except oil and gas, seasonally adjusted:

Junior Mining Network, 2020, Newsroom: https://beta.bls.gov/dataViewer/view/

REFERENCES https://www.juniorminingnetwork.com/ timeseries/CES1021200001.

Apple Inc., 2020, COVID-19 mobility trends junior-miner-news.html. World Health Organization, 2020a, Time-

reports: https://www.apple.com/covid19/ S&P Global, 2020, COVID-19 mining line of WHO’s response to COVID-

mobility. impact—impact to mine sites winding 19: https://www.who.int/news-room/

Australian Bureau of Statistics, 2020, down, May 8, 2020: https://www.spglobal. detail/29-06-2020-covidtimeline.

8412.0 Mineral and petroleum explo- com/marketintelligence/en/news-insights/ ——2020b, WHO coronavirus disease (Covid-

ration, Australia, Mar 2020: https:// research/covid-19-mining-impacts-impact- 19) Dashboard, June 30: https://covid19.

www.abs.gov.au/AUSSTATS/abs@.nsf/ to-mine-sites-winding-down. who.int/.

Lookup/8412.0Main+Features1Mar%20

2020?OpenDocument.

Boland, M., Hitzman, M., McAuliffe, F., Zhou, Murray Hitzman is SFI Professor in the School of Earth Sciences,

L., Doran, A., Kaeter, D., Brady, A., Burke,

S., Craig, J., Drejing-Carroll, D., Johnson, S., University College Dublin and Director of the Irish Centre for

Stratford, J., and Tsuruoka, S., 2020, COVID- Research in Applied Geosciences. He served as Associate Director

19 and the minerals sector: Survey results: for Energy and Minerals at the U.S. Geological Survey, Charles

iCRAG report, 29 p., https://www.icrag-cen- Fogarty Professor of Economic Geology at Colorado School of

tre.org/news-and-media/covid-19andthe-

Mines, policy analyst in the White House Office of Science and

mineralssector.html.

European Centre for Disease Prevention and Technology Policy and the U.S. Senate, and exploration geologist

Control, 2020, COVID-19 situation update conducting mineral exploration worldwide. Hitzman has B.A.

worldwide: https://www.ecdc.europa.eu/en/ degrees in geology and anthropology from Dartmouth College,

geographical-distribution-2019-ncov-cases. an M.S. degree in geology from University of Washington, and a

Flightradar24, 2020, Number of commercial

flights tracked byFlightradar24, per day: Ph.D. in geology from Stanford University.

https://www.flightradar24.com/data/statistics.

COVID-19 and the Global Mining Industry

Simon M. Jowitt

Department of Geoscience, University of Nevada Las Vegas, 4505 Maryland Parkway,

Las Vegas, Nevada 89154-4010, USA; simon.jowitt@unlv.edu

Abstract the effect of mitigation on the min- That includes variations in metal

The world is currently experiencing a ing industry and on metal production and commodity prices and stocks

rapid and deep economic slowdown has been minimal to date. However, during the crisis and the outlining

as a result of COVID-19 mitigation increases in metal stocks and decreases of two possible scenarios for COVID-

efforts. The depth and global nature of in metal prices suggest that the mining 19 related impacts. The first involves

this recession, which could turn into a industry will be negatively affected persistent supply-chain disruptions,

depression, suggests that this pandemic by the COVID-19 crisis, at least in the where metal supply is restricted by

will significantly affect the demand for short term. logistical or COVID-19–related mitiga-

metals and the global mining sector. This paper presents an overview tion impacts on intermediates such as

The majority of governments consider of the effects of COVID-19 mitiga- smelters and refiners. This restriction

mining to be essential, meaning that tion on the mining sector to date. of supply could cause higher metal

doi:10.5382/SEGnews.2020-122.fea-0234 SEG DISCOVERY No 122 • JULY 2020

COVID-19 and the Global Mining Industry (continued)

or effective treatment for COVID-19 industry the same way, closing opera-

prices but also could cause issues and the need to prolong mitigating tions in March 2020 (Ramaphosa, 2020)

with demand for ores and concen- measures. but later changing this to only reduce

trates that negatively affect individ- The continuing supply of metals mining capacity by 50%.

ual mining operations. More likely provided by a continuation of min- This is not to say that mining

is a second slower demand growth ing also contrasts with an apparent activities that are currently continuing

scenario in which a global decrease decrease in global metal demand as couldn’t be suspended if a second wave

in demand for metals causes further a result of the COVID-19 crisis. This of COVID-19 infection (e.g., Anderson

lowering of metal prices with asso-

potential oversupply suggests we may et al., 2020) eventuates or if outbreaks

ciated negative economic impacts

enter a period of relatively low metal develop at individual mine sites. The

on mining operations. However,

prices until either demand recovers remote nature of (most) mine sites may

further research into global metal

or some mines close as a result of the be advantageous in terms of keeping

supply chains and the impact of

prevailing economic conditions. This operations running as this physical

the COVID-19 crisis on individual

paper discusses the data underlying distance from the general population

metals is needed. Key remaining

these scenarios and highlights the may act to prevent COVID-19 out-

unknowns include the influence of

variables involved in the current situa- breaks. Mining operations that have

mitigation efforts on global metal

tion. It also outlines the impact of this gone through recent epidemics are also

supply and demand, the effect of

crisis on mining to date and areas for particularly well equipped to con-

these efforts on metal prices, and

future research to more fully determine tinue operating during this crisis. This

the geography of supply chains.

the likely effects of COVID-19 on the is exemplified by West Africa, where

global mining sector as well as possible knowledge of screening and isolation

mitigation approaches. practices developed during the Ebola

Introduction epidemic means that individual mine

The rapidly evolving and global Mining continues in most countries; sites and other businesses in this part of

COVID-19 crisis has impacted all challenges are not governmental; the world are better equipped to con-

aspects of human life, including they are logistical and related to tinue operations during the COVID-19

metal and mineral production and the outbreak itself and economics pandemic (Ihekweazu, 2020).

the industries that the mining sector Most governments have allowed mining Mining companies are also mak-

supplies. This has led to a slowdown to continue during the COVID-19 pan- ing decisions based on their own

in the global economy as a result demic, if not as per normal then with situations, including local COVID-19

of efforts to reduce the spread of somewhat limited restrictions relating outbreaks at individual operations,

COVID-19. However, the effect of the to COVID-19 mitigation (Table 1), logistical challenges, and changes

crisis on the mining industry remains despite the suspension by some compa- in metal prices and demand (both

unclear, partly because of the different nies of individual operations for their positive and negative). This undoubt-

approaches to mitigation adopted by own economic or other reasons. The edly has the potential to create clashes

various governments. Most countries continuation of mining is not directly between mining companies, interme-

consider mining essential (albeit with related to the dependency of the econ- diates, and governments if legislation

a couple of major exceptions in South omy of a given country on mining or is enacted that suspends operations

Africa and Mexico) although mitiga- the value of mining to a country (i.e., against the will of the operator. Other

tion approaches have also varied over gross domestic product, GDP), as is clashes may occur if countries with

time as COVID-19 outbreaks are man- shown in Table 1. high mining contribution index (MCI)

aged. These variations are a function There are some notable exceptions values, an indication of the mining

of the swift development of the crisis, to the continuation of mining where dependency of a country’s economy,

the relative importance of mining to the crisis has resulted in the temporary want production to continue and

different regions of the world, and closure of individual mines, the cessa- individual companies do not—as a

economic and political pressures act- tion of mining in certain regions, or result of low metal prices or other

ing on governments at all levels. The in rare cases the closure of the entire factors. One example of this is Zam-

often essential nature of mining means mining industry of a country. This most bia, where the government appeared

that the direct impact on the global likely reflects the nature of mining to be encouraging mining operations

mining sector may not be as signifi- in the countries that enacted these to remain open even where operators

cant as the impact on other economic measures, as COVID-19 mitigation were considering shutting down for

sectors, such as transportation and approaches are naturally much harder economic reasons (e.g., the Mopani

leisure travel, which have been greatly to enact in underground labor-inten- Copper Mines; Biesheuvel et al., 2020).

curtailed. However, the fact that min- sive mining situations relative to large It is also important to note that the

ing operations have remained open and more mechanized or automated dependency of a country on mining

during the COVID-19 crisis is not the open-pit environments. A complete does not just incorporate the contri-

end of the story. The economic impact shutdown occurred in Mexico, where bution of mining to that country’s

of COVID-19 may be sharp and deep the mining industry was forced to cease GDP. For example, the MCI values

but a return to economic normality operations on March 31, 2020, but was shown in Table 1 are a composite of

may not be equally as rapid (i.e., is not allowed to reopen on May 18, 2020. The four indicators that capture different

likely to be V-shaped). A slow return South African government also initially aspects of the contribution of mining

to economic normality is even more approached their underground-domi- to a country’s economy. These are the

likely given the current lack of vaccine nated and often labor-intensive mining value of mineral and metal exportsNo 122 • JULY 2020 SEG DISCOVERY 35 and how they have varied over time, institute their own travel restrictions In addition, smelters and refiners indicating whether the importance is to prevent the spread of COVID-19 that process ores and concentrates from increasing or decreasing (International (DeMarban, 2020). The pandemic may mining operations face both possible Council on Mining & Metals, 2018) of also drive companies more rapidly COVID-19 mitigation-related restric- mining as an economic activity to a towards automation of mining oper- tions as well as potential decreases in given country. The MCI values shown ations, a trend that is already well the demand for their own products. All in Table 1 also incorporate mineral established. However, the prevailing of these uncertainties relating to the production and mineral rents as a lack of certainty on the duration of the transport of ores and concentrates and percentage of GDP, providing a sense crisis and the fact it may be difficult to the operation of smelters and refiners of the value of mining to an economy accelerate beyond current uptake in the mean that although mining is likely for the former and the contribution short timescales typically associated to be able to continue, the possibility of mining-related taxes and profits to with modern epidemics and pandem- remains of a reduction in demand the economy of a country for the latter ics means it remains unclear whether as a result of logistical disruptions to (International Council on Mining & increased automation is a viable producers or the closure or lowering of Metals, 2018). The incorporation of approach to mitigation against COVID- production at smelters and refiners. these variables gives a more accurate 19. All of this suggests that although In summary, the major challenges overview of the true contribution of mining operations may be allowed facing the mining industry are not mining to an economy, rather than to continue, a wide variety of other from governments closing operations just comparing the value of mineral (non-economic) factors could mean to mitigate the spread of COVID-19. production to the overall GDP of a mines operate at lower capacity or have Instead, the logistical challenges of country; this also explains the con- to transition to care and maintenance. supplying operations with the essential trasting high MCI but low contribu- The crisis is also posing logistical workforce and transporting products tion to GDP values for some of the challenges relating to the transport such as concentrates represent more countries listed in Table 1. of supplies and the products of min- significant difficulties on the production The closure of mining operations ing such as metal concentrates. It is side of mining. This in turn suggests could also have additional negative unclear whether there has been any that metal supply may not be signifi- effects beyond the global economic major impact or interruption on the cantly affected by the direct impact slowdown in countries with economies supplying of mining operations with of COVID-19 mitigation or outbreaks that are heavily reliant on mining for key materials such as fuel, explosives, although, as discussed above, indirect the reasons discussed immediately or even the personal protective equip- impacts are certainly possible. Instead, above (Table 1). Even if mining oper- ment needed to operate. However, the it is more likely that the demand for ations can remain open, COVID-19 shipping of ores and concentrates from metals and minerals and the economics containment measures such as enforc- mines has certainly been affected. For of mining operations may be negatively ing physical distancing and reducing instance, cobalt and copper concen- affected by this crisis, as discussed in the numbers of personnel gathered in one trates produced within the Democratic following section. place might reduce metal production Republic of the Congo (DRC), a coun- capacity. International and domestic try with only limited closures of min- Changes in metal demand and travel restrictions may also impact the ing operations, are generally shipped price; metal stocks higher, metal ability of mines to continue to operate, to China for further processing via the prices lower with the exception given the significant numbers of mine South African port of Durban (e.g., of gold site employees that work on a fly-in, Luk, 2020). However, the widespread Global production and manufacturing fly-out (FIFO) basis in some coun- closures and transport restrictions in have declined as a result of economic tries (e.g., Australia). These potential South Africa are causing most ship- slowdowns caused by efforts to prevent personnel shortages could mean that ments to be diverted to Mozambique the spread of COVID-19. This led the some mines may not be able to sustain or Tanzania, resulting in a decrease in United Nations to predict that this slow- operations in the short term, especially concentrate exports as a result of cus- down would result in global GDP drop- given the lead-in time needed to move toms delays. These logistical challenges ping by at least 1% (UNDESA, 2020) a mining operation from production are present despite the South African and the International Monetary Fund to care and maintenance. This lead-in Maritime Safety Authority's stating that to predict a change in global economic time is essential to allow mines to all cargoes can be loaded and unloaded growth of –4.9% during 2020 (Inter- efficiently reopen and to prevent at South African ports. This directly national Monetary Fund, 2020). These environmental issues arising during contrasts with information from impacts are further demonstrated by a the cessation of mining activity. Mines another government agency, the Trans- decrease in U.S. industrial production in countries such as the United States, net National Ports Authority, which (indexed where 2012 = 100) from 109.1 Canada, Australia, and elsewhere that maintained that metal exports from in January 2020 to 92.6 in April 2020, a employ significant numbers of indige- Durban were banned at the time of the contraction of ~15% (Board of Gov- nous employees may also be forced to statement by the South African Mari- ernors of the Federal Reserve System, reduce operations or close, given the time Safety Authority indicating ports 2020). This decrease was coincident risk of these workers passing infections were open, creating a clearly confusing with an increase in U.S. unemployment on to often remote communities with situation (Luk, 2020). These conflicting from 3.6% in January 2020 to 14.7% limited medical infrastructure. These statements and positions are typical of in April 2020 (U.S. Bureau of Labor mitigation measures have led individ- the challenges and unknowns affecting Statistics, 2020). Although some of ual mines such as Red Dog in Alaska to all industries, not just mining. these statistics are U.S. specific, similar

36

Table 1. Summary of the Mitigation Approaches to COVID-19 and Their Impacts on the Mining Industry in Selected Countries Listed by Value of Metallic Mineral and Coal Production

Metallic mineral

and coal produc-

tion value 2016 Production Business Mining Country-wide or

Country (in billions of 2018 MCI value as % operations allowed to state/province-

or state USD) score of GDP Major metals produced restricted? continue? wide mitigation? Notes

China 626.3 53.1 5.6 Antimony, arsenic, bauxite, coal, cobalt, copper, Yes Yes State/province Some reduction of production in significantly

diamonds, gold, iron ore, lead, lithium, man- affected provinces

ganese, molybdenum, nickel, REE, silver, tin,

titanium, vanadium, zinc

Australia 123.1 69.8 10.2 Bauxite, coal, cobalt, copper, diamonds, gold, Yes Yes State/province Internal travel restrictions restricting some FIFO

iron ore, lead, lithium, manganese, nickel, operations

REE, silver, tin, titanium, zinc

Russian 91.5 77.9 7.1 Antimony, arsenic, bauxite, coal, cobalt, copper, Yes Yes Country

Federation diamonds, gold, iron ore, lead, molybdenum,

nickel, platinum group elements (PGE), rare

earth elements (REE), silver, tin, tungsten,

vanadium, zinc

United States 89.7 41 0.5 Bauxite, coal, cobalt, copper, gold, iron ore, lead, Yes Yes State/province although

lithium, molybdenum, nickel, PGE, REE, Silver, mineworkers are

Titanium, Zinc deemed essential

COVID-19 and the Global Mining Industry (continued)

India 77.0 56.9 3.4 Bauxite, coal, chromium, iron ore, lead, Yes Yes Country Mines allowed to remain open but downstream

manganese, REE, titanium, zinc facilities suspending or lessening operations

South Africa 48.9 65.1 16.5 Coal, chromium, cobalt, diamonds, gold, iron ore, Yes Yes Country Initial countrywide closure of mining industry

manganese, PGE, titanium, vanadium followed by change to allow mining at 50%

capacity

Indonesia 47.5 58.8 5.1 Coal, Copper, Gold, Nickel, Tin Yes Yes Country

Canada 39.4 55.1 2.6 Bauxite, cobalt, diamonds, gold, iron ore, lithium, Yes Yes State/province Designation of mining as an essential business

molybdenum, nickel, PGE, titanium, zinc varies from province to province; some mining

operations closed as a precaution

Brazil 36.6 55.3 2.0 Bauxite, diamonds, gold, iron ore, lithium, Yes Yes Country

manganese, nickel, REE, tin, titanium, vanadium

Chile 33.5 69.1 13.4 Copper, iron ore, lithium, molybdenum, silver Yes Yes Country Mining companies requested to reduce

workforce

Mexico 28.9 53.2 2.7 Antimony, copper, gold, iron ore, lead, Yes No Country Mining industry closed March 31, allowed to

SEG DISCOVERY

manganese, molybdenum, silver, zinc reopen May 18

Peru 27.1 80.1 14.1 Copper, gold, iron ore, lead, molybdenum, Yes Partially Country Mine operators given partial exemption from

silver, tin, zinc closure orders, allowing necessary opera-

tions to proceed; 75% of mining workforce

evacuated

Kazakhstan 18.6 76.7 13.6 Antimony, coal, chromium, copper, gold, iron Yes Yes State/Province

ore, lead, manganese, zinc

Turkey 17.2 67.5 2.0 Antimony, chromium, lead, molybdenum Yes Yes State/Province

Germany 15.8 36.5 0.5 Coal Yes Yes Country

Poland 14.6 49.1 3.1 Coal, silver Yes Yes Country

Colombia 10.1 72 3.6 Coal, copper, gold, iron ore, nickel, PGE, silver Yes Yes Country Mining allowed to continue with restrictions

Ukraine 9.9 61.4 10.6 Iron ore, manganese, titanium Yes Yes Country

Finland 8.5 57.3 3.6 Chromium Yes Yes Country

DRC 7.9 96.4 2.2 Cobalt, copper Yes Yes State/province Limited shutdowns of operations have taken

place in some provinces, e.g., 48-hour closures

in Haut Katanga

Mongolia 6.0 84.9 53.6 Molybdenum, tungsten Yes Yes Country

Ghana 5.5 90.9 12.8 Gold, manganese Yes Yes Country

Botswana 5.0 86.1 31.8 Coal, cobalt, copper, diamonds, gold, nickel, Yes Yes Country

PGE, silver

Uzbekistan 4.4 89.1 6.6 Gold, molybdenum Yes Yes State/province

Zambia 4.4 78.4 21.1 Cobalt, copper, gold, manganese, silver Yes Yes Country Import duties on metal concentrates and export

duties on metals suspended, and government

encouraging some mines to remain open

Madagascar 4.2 87.1 41.6 Cobalt, REE, titanium Yes Yes Country Curfews have restricted activities at certain

mines, causing closures

No 122 • JULY 2020Table 1 (Cont.)

Metallic mineral

and coal produc-

tion value 2016 Production Business Mining Country-wide or

Country (in billions of 2018 MCI value as % operations allowed to state/province-

or state USD) score of GDP Major metals produced restricted? continue? wide mitigation? Notes

Bolivia 2.9 84.5 8.5 Arsenic, lead, silver, tin, tungsten, zinc Yes Yes Country Curfews have restricted activities at certain

mines, causing closures

No 122 • JULY 2020

Zimbabwe 2.8 84.2 16.8 Chromite, cobalt, diamonds, gold, lithium, nickel, Yes Yes Country

PGE

Kyrgyz 2.5 93.3 36.3 Antimony, copper, gold, silver Yes Yes Country Government supporting the continued opening

Republic of some mining operations

Senegal 2.5 84.4 16.9 Gold, lead, silver, titanium Yes Yes Country

Sudan 2.5 79.9 2.6 Chromite, gold, iron ore, manganese, silver, zinc Yes Yes Country

Mali 1.9 93.2 13.6 Coal, gold, silver Yes Yes Country

Guinea 1.8 94.3 19.0 Bauxite, diamonds Yes Yes Country

Burkina Faso 1.8 93.4 15.2 Gold, lead, manganese, silver, zinc Yes Yes Country

Tajikistan 1.7 84.9 24.9 Antimony No No N/A No officially reported COVID-19 cases

Dominican 1.7 78.3 2.4 Bauxite, copper, gold, nickel, silver Yes Yes Country

Republic

Sierra Leone 1.2 92.6 34.4 Diamonds, titanium Yes Yes Country

Mauritania 1.2 78.6 24.7 Copper, gold, iron ore Yes Yes Country Mauritania reported to be COVID-19 free

on 21st April

Suriname 1.0 96.4 33.0 Bauxite, gold Yes Yes Country

Namibia 1.0 87.6 8.8 Arsenic, copper, diamonds, gold, lead, silver, zinc Yes No Country Mining operations suspended

Guyana 0.9 80.4 27.8 Bauxite, gold Yes Yes Country

Armenia 0.7 84.9 7.0 Molybdenum Yes Yes Country

Liberia 0.3 92.1 14.3 Diamond, gold, iron ore Yes Yes Country

Countries shown are the top 20 countries by 2016 production value of metallic minerals and coal and the 25 countries with the highest 2018 Mining Contribution Index values (MCI; data from International

Council on Mining & Metals, 2018, for which increasing MCI values are indicative of the increasing dependency of a given country on mining and mineral production); major metals are identified using the

USGS production statistics (U.S. Geological Survey, 2020) and italics indicate high MCI countries with production of the indicated commodities that are nationally but not internationally important; also given

are production values as a percentage (%) of the total GDP to indicate the relative importance of mining and metal production to an individual country’s economy; COVID-19–related closures and cessations of

business are current at the time of submission but the rapidity of developments means that this information may change on a daily or weekly basis; note that business restrictions can mean full or partial shut-

SEG DISCOVERY

downs, curfews, distancing restrictions, and more; the rapid variations in these restrictions mean that tracking individual efforts to determine specific restrictions on a province/state or country basis is difficult

and is beyond the remit of this paper; also note that even if mining is generally allowed to continue, individual mines may still close as a result of COVID-19 cases, logistical issues, or the deleterious effect of

COVID-19 mitigation approaches on production and the economics of a given mine (e.g. curfews)

prices down.

trates during the January-February

(Table 2), independent of whether

Most metal prices shown in Figure

2020. This trend probably reflects a

1 have generally similar trends and

the precious metals Au and Pd; Fig.

the signing of the Coronavirus Aid,

positively correlate with each other

Act by the U.S. federal government.

likelihood of demand stimulated by

decrease in demand for these metals

closure of the South African mining

copper, nickel, and zinc (Fig. 2). The

(Davy, 2020), although this decrease

2020 COVID-19 slowdown in China

restrictions related to the temporary

This was the case for copper concen-

any specific changes on a commodi-

as a result of the COVID-19 crisis, as

This global economic slowdown and

the majority of metal prices (barring

1A) have been uniformly affected by

have steadily increased since January

and oil confirms this. Figure 1 shows

started to decrease around March 10,

they are base (e.g., Cu, Ni; Fig. 1B) or

this crisis with changes reflecting the

tion (Table 2) of metal price changes.

was also influenced by the increasing

The recent price history for metals

metals given the continuation of pro-

started to decline before this (but not

data (i.e., metals available for sale) for

commodities. These data suggest that

with the onset of possible production

stocks of all three of these base metals

2020, to between 10 and 20% of early

Crude oil between January 2 and May

manufactured goods will undoubtedly

18, 2020. The majority of metal prices

of the response of the metal market to

the resulting decrease in production of

COVID-19 is reflected by the temporal

January 2020 prices, whereas oil prices

Relief, and Economic Security (CARES)

have a negative impact on the demand

of decreased demand without a change

industry (Ramaphosa, 2020). This rally

duction, which in turn will drive metal

minor or bulk (e.g., Co, Sn, Al; Fig. 1C)

in supply is consistent with metal stock

the potential to create an oversupply in

discussed below). Metal prices then ral-

global economic slowdown rather than

ty-by-commodity basis. The uniformity

for metals. This decrease in demand has

lied around March 23, 2020, coincident

without a significant decrease in supply.

prices for a number of metals and Brent

The change in metal prices as a result

impacts are occurring around the world.

consistency (Fig. 1) and positive correla-

3738 SEG DISCOVERY No 122 • JULY 2020

COVID-19 and the Global Mining Industry (continued)

in demand was earlier than the

A major decrease in copper (and

other metal) prices in March

2020 (Fig. 1). This suggests that

although the effects of mitigation

in China influenced metal stocks

during very early 2020, the slump

in most metal prices evident in

Figure 1 was more related to later

decreases in demand for these

commodities caused by COVID-19

mitigation in Europe and North

America (Fig. 2).

Not all metals have been neg-

atively affected by the COVID-19

crisis. Gold and palladium are

the only metals in Figure 1 with

prices in April and May 2020

above their respective prices on

January 2, 2020. Increases in gold

B and palladium price (Fig. 1) may

reflect two factors that poten-

tially overprint or enhance the

existing pre-COVID-19 trend of

increasing prices for these met-

als. These are (1) the temporary

shutdown of mining in South

Africa, an important producer of

both metals, and (2) increased

demand for these precious metals

as safe investment havens. The

fact that platinum has not had a

price increase similar to that of

palladium may reflect a lack of

confidence in future demand that

primarily relates to a decrease in

the use of platinum in catalytic

converters (e.g., Mudd et al.,

2018). The generally negative

C correlation between gold prices

and the majority of the other

commodities shown in Figure 1

and Table 2 also suggests that gold

is once again being considered a

safe haven during economically

turbulent times.

Oil prices have also declined

more significantly than metal

prices during the COVID-19 crisis,

reflecting two factors. The first

of these is a decline in demand

resulting from COVID-19–related

economic slowdowns (i.e., the

same as metal prices). The second

is that oil prices have also been

negatively affected by a decision

taken by Saudi Arabia and Russia

to not cut back on oil produc-

Fig. 1. Recent changes in precious (A), base (B), and bulk (aluminum) and minor (tin and cobalt; C) metals tion, thus creating excess supply.

and Brent Crude oil prices indexed to January 2, 2020, compared to select COVID-19–related events. Similar controversies may develop

Base metal price data are from the London Metal Exchange, palladium and platinum data are from John- with metals if stocks continue to

son Matthey, and gold and Brent Crude oil prices are from the Federal Reserve Bank of St. Louis, USA. accumulate (e.g., Fig. 2) as a result

Dashed line indicates metal and oil values as of January 2, 2020.

of production continuing to beYou can also read