MLC's scenario insights & portfolio positioning - October 2021

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

MLC's scenario insights & portfolio positioning October 2021 Ben McCaw Al Clark Anthony Golowenko Senior Portfolio Manager Head of Investments Portfolio Manager MLC MLC MLC MLC's investment and super portfolios MLC Inflation Plus, MLC Horizon and MLC Index Plus portfolios MLC’s Managed Account Strategies MLC Premium and Value model portfolios

Contents Quarterly insights 3 The Investment Futures Framework: Scenarios, changes in return potential, and portfolio positioning 7 Return potential 9 MLC Inflation Plus portfolios 11 MLC Horizon portfolios 13 MLC Index Plus portfolios 15 MLC Managed Account Strategies 16 Appendix 1 – MLC’s market-leading investment process 18 Update for the quarter ending 30 September 2021. Important information This communication has been provided for the funds in the table below by MLC Investments Limited (ABN 30 002 641 661 AFSL 230705) as Responsible Entity for the MLC Investment Trust, NULIS Nominees (Australia) Limited (ABN 80 008 515 633, AFSL 236465) as trustee of the MLC MasterKey Fundamentals Super and Pension and MLC MasterKey Business Super products which are a part of the MLC Super Fund (ABN 70 732 426 024), and for the MLC Managed Account Strategies by MLC Asset Management Pty Ltd (ABN 44 106 427 472, AFSL 308953) in connection with its distribution of these MLC Managed Accounts Strategies, part of the IOOF group of companies (comprising IOOF Holdings Ltd ABN 49 100 103 722 and its related bodies corporate) (‘IOOF Group’). No member of the IOOF Group guarantees or otherwise accepts any liability in respect of any financial product referred to in this communication or MLCAM’s services. The capital value, payment of income, and performance of the Funds are not guaranteed. An investment in the Funds is subject to investment risk, including possible delays in repayment of capital and loss of income and principal invested. This document has been prepared for financial advisers. This document must not be distributed to ‘retail clients’ (as defined in the Corporations Act 2001 (Cth)) or any other persons. This information is directed to and prepared for Australian residents only. This information may constitute general advice. It has been prepared without taking account of an investor’s objectives, financial situation or needs and because of that an investor should, before acting on the advice, consider the appropriateness of the advice having regard to their personal objectives, financial situation and needs. You should obtain a Product Disclosure Statement (PDS) relating to the financial products mentioned in this communication issued by MLC Investments Limited or NULIS Nominees (Australia) Limited as trustee of the MLC Super Fund (ABN 70 732 426 024), and consider it before making any decision about whether to acquire or continue to hold these products. A copy of the PDS is available upon request by phoning the MLC call centre on 132 652 or on our website at mlc.com.au. MLC Managed Accounts Strategies are available via investment platforms. Please refer to the MLC Asset Management website www.mlcam.com.au) for a full list of platform availability. You should obtain a Product Disclosure Statement relating to the investment platform and consider it before making any decision about whether to acquire or continue to hold interests in the Model Portfolios. Past performance is not a reliable indicator of future performance. The value of an investment may rise or fall with the changes in the market. Returns are not guaranteed and actual returns may vary from any target returns described in this document. No representations are made that they will be met. Please note that all performance reported is before management fees and taxes, unless otherwise stated. Any projection or other forward-looking statement (‘Projection’) in this communication is provided for information purposes only. No representation is made as to the accuracy or reasonableness of any such Projection or that it will be met. Actual events may vary materially. MLC Investments Limited, NULIS Nominees (Australia) Limited, and MLC Asset Management Pty Ltd may use the services of any member of the IOOF Group where it makes good business sense to do so and will benefit customers. Amounts paid for these services are always negotiated on an arm’s length basis. Bloomberg Finance L.P. and its affiliates (collectively, “Bloomberg”) do not approve or endorse any information included in this material and disclaim all liability for any loss or damage of any kind arising out of the use of all or any part of this material.) The funds referred to herein are not sponsored, endorsed, or promoted by MSCI, and MSCI bears no liability with respect to any such funds. Continued at end of update. 2 | MLC's scenario insights & portfolio positioning

Quarterly insights

Highlights MLC'S active investment approach

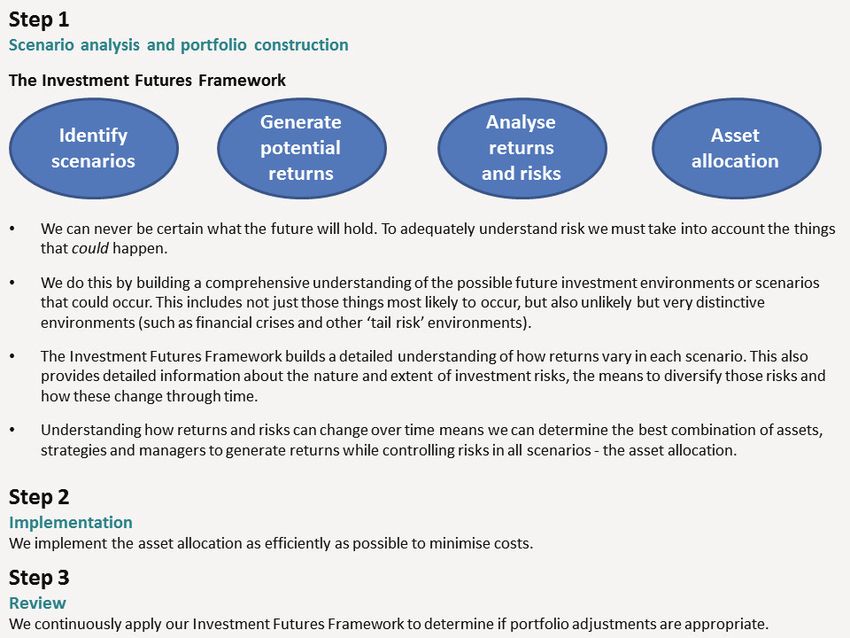

Looking closely into the composition of prevailing high share Key to MLC’s market-leading investment approach is our

market valuations it becomes clear that very low interest rates unique Investment Futures Framework.

are the driver. In an unpredictable world, the Framework helps us

We believe the relatively high real interest rate environment in comprehensively assess what the future might hold. By taking

China presently provides an opportunity to harness return into account the many scenarios that could unfold – positive

potential. and negative – we gain continuing insight into return potential,

Our customised positions within the MLC Inflation Plus and future risks, and opportunities for diversification.

Horizon portfolios have been designed to achieve a targeted The information from the Framework gives us a deep

exposure to the Chinese assets that we believe will benefit most understanding of how risks and return opportunities change

from government policy settings. over time for both individual assets and total portfolios.

Inflation remains uncertain and is arguably at the behest of the We can then determine the asset allocations that will help

pandemic to a large extent. Under the most optimistic of our achieve our portfolios’ objectives with the required level of risk

control, and adjust the portfolio if necessary. We’ll generally

scenarios, we believe that inflation will remain stubbornly above

reduce exposure to assets if we believe risk is too high. We

central bank targets driven by a combination of supply and

prefer exposures with limited downside risk compared to

demand factors.

upside potential.

More information about MLC’s investment approach is available

on our website and in Appendix 1.

Insights

The devil is always in the detail. Perhaps more notable than the importance of sovereign risk on

maintenance of higher real rates in China is that standard monetary

It’s almost a truism that exposure to equity is the main driver of

policy, despite local nuances and the role of exchange rate

upside for all multi-asset investors. It’s also true, that starting

management, continues to remain effective: tighter policy rates

valuations have been a good predictor of equity returns over the

reduce demand and lower rates spur demand. Unlike peer central

ensuing decade: high starting valuations decrease the likelihood of

banks, the People’s Bank of China has not yet stepped into the realm

reasonable returns and increase the risk of loss, while low starting

of zero policy cash rates and large-scale quantitative easing, instead

valuations lift the prospect of outsized returns and limit risk. Yet,

preferring to maintain more traditional levels of monetary policy

by peeling one layer lower into the composition of the prevailing

settings.

high equity valuations, it becomes clear that very low interest rates

are the culprit. Indeed, from a relative point of view, equities are not So, if low real interest rates are the ultimate challenge for investors,

expensive relative to government bond yields, a proxy for the does the relatively high real interest rate environment in China

risk-free rate. provide an opportunity to harness return potential? We currently

think so and have expressed this view for some time through Chinese

This pattern of low core interest rates and a more or less stable equity

shares and bond positions within the MLC Inflation Plus portfolios,

risk premium (shown in Chart 1 for the US) is representative of the

and more recently in the MLC Horizon portfolios through an emerging

state of most developed markets and some more advanced emerging

market shares overweight. Importantly, these positions are

markets. Indeed, excluding the high-risk end of emerging markets,

customised to achieve a targeted exposure to the Chinese assets that

it is difficult to find any global market that has an underlying risk-free

we believe will benefit most from government policy settings.

real yield (the yield remaining after subtracting inflation) comparable

to what was a normal level prior to 2012. Table 1 shows the change Table 1: Change in 10-year real yields over 15 years

in real yields for a select group of countries/regions in the 15 years

Country/region 30/06/2021 31/10/2006

between 2006 and 2021.

China 2.2% 2.2%

What stands out to us is that China, while evolving considerably over

the last 15 years, has not witnessed any attrition in the underlying Australia -1.6% 3.0%

risk-free real rate of return as have it’s now (arguably) peer economies. US -3.0% 1.9%

A number of factors underpin the comparatively elevated level of

real rates in China, with sovereign risk an obvious key contributor. Britain -1.5% 2.9%

China’s economic progress, while very impressive, still has a eurozone -1.1% 2.2%

transitionary period ahead, raising the risk of policy error and leaving

Canada -0.8% 2.2%

investors demanding a higher risk premium to invest in what is

ostensibly a ‘command’ economy. Yet that alone cannot explain the South Korea 0.6% 2.9%

divergence between real rates in China and peer economies, given Taiwan 0.4% 1.5%

that the spread between real rates in China and other countries has

widened, while China’s economic development cycle has made strides Japan 1.2% 2.1%

forward. Source: Bloomberg, 2021.

MLC's scenario insights & portfolio positioning | 3Quarterly insights

Chart 1: US equity risk premium

US equities

Risk Free Rate and Equity Risk Premium

12%

10%

8%

6%

4%

2%

0%

Source: Bloomberg, 2021. Risk Free Rate Equity Risk Premium

The devil is in the detail The recent ructions in China’s property market are a good example

of how the system manages centralised policy and localised

At the highest level, China is an enigma. For those of us in the West, implementation. While the broad directive out of Beijing is for

it represents an unfamiliar political system, with an underlying tightening of the property sector, weak conditions in predominantly

ideology that in simplistic terms is taken as being at odds with tier-3 and tier-4 cities are being addressed by loosening of regional

capitalism. But whereas China’s political ideology clearly differs from policy. Thus, while bustling new economic hot zones such as Hainan

standard Western capitalism, it also differs from other socialist are restricting lending and inhibiting liquidity, stagnant markets

systems and is known in China as “Socialism with Chinese such as Zhuhai are relaxing liquidity and supporting prices.

Characteristics”. In our opinion, the “Chinese Characteristics” part of

the name at least in part embodies the traditional mercantilist nature Evergrande

of Chinese society and the role it plays in helping address the Evergrande is worth touching on at this point. Whereas headlines

inefficiencies embedded in traditional socialism. are suggestive of an impending calamity, our view is that China

As observers of China, we believe that a useful way to conceptualise makes no major policy decision without first carefully considering

China’s political structure and social economy is to delineate unified the consequences against the country's long-term goals and

control from fragmented implementation. China knows well from its short-term situation. That’s not to say that decision-making is

own history that the country prospers under the leadership of a without risk, but that the risk of unintended consequence is low. In

united core and stumbles upon fragmentation and erosion from this case, property developer Evergrande’s fate was most likely sealed

within. This fear of division is well evidenced by the fact that the in late 2020 when China’s regulators implemented the ‘Three Red

country, while spanning 54 degrees of longitude only has a single Lines’ policy that governs access to leverage for property developers.

time zone (Australia by way of contrast spans 30 degrees of longitude The market quickly read Three Red Lines as a risk to Evergrande,

and has a three-hour time zone gap between Perth and Sydney). But prompting a slide in the share price that began long before the

while governance is centralised, implementation of policy is delegated company grabbed headlines (Chart 2). And if the market could see

both regionally to the provinces and cross-sectionally in the economy what potentially lay in store, we believe it is highly unlikely that

to either private-like organisations (state-owned enterprises, SoE) regulators had not considered contingencies for large property

or the private sector. developers at that point.

4 | MLC's scenario insights & portfolio positioningChart 2: Evergrande’s share price

$25

$20

Evergrande share price

Hong Kong

$15

$10

$5

$0

Source: Bloomberg, 2021.

Failure of Evergrande is very unlikely to ignite contagion either Our guide to investing in China is to follow policy signals. As eluded

domestically or offshore. For now, the Chinese government will most to above, strategic policy is clearly communicated in China by the

probably prioritise the welfare of home buyers exposed to Evergrande command economy. The trick we believe is not to get lost in

through sale contracts and contractors exposed to commercial loss. cyclicality, but to focus instead on strategic priorities. Since the trade

The financial system may well incur losses, but analysts believe that war and subsequent pandemic, China’s inward focus has accelerated.

exposure of both the formal and shadow banking systems to Coined ‘dual circulation’, China has made a sharp turn toward

Evergrande debt is low enough to be absorbed without system wide development of self-sustaining domestic-led growth as a substitute

disruption. Evergrande debt represents less than 0.25% of Chinese for reliance on exports and capital formation. This has led to a series

bank loans. of policy measures that directly support small to medium-sized

enterprises (SMEs) and foster less reliance on offshore markets.

Although China is a socialist command economy it is certainly not

Policies aimed at supporting SME’s range from access to credit,

anti-enterprise. Policy well recognises that innovation requires

through to taxation and support for employees. In our view, the

optimisation of both capital and talent. So, while recent headlines in

support offered to the SME sector trumps the cyclical drag from

offshore press have focused on a crackdown against a narrow

monetary policy in the short term and, if we are right, won’t

segment of mega-rich technology fortunes, the move by SoE’s to

necessarily run countercyclical when monetary conditions change

re-align employment incentives to enable greater sharing of

(ie SME’s could coincidently benefit from both monetary and strategic

commercial interest with employees has almost gone unnoticed.

policies).

These seemingly contradictory moves are in fact serving two

purposes. The former limiting further evolution of commercial

entities that threaten centralisation, and the latter aimed at

continuation of what is becoming a rapidly competitive and

productive technology sector in China.

MLC's scenario insights & portfolio positioning | 5Quarterly insights

Portfolio implications We continue to view domestic policy in China as supportive and plan

on retaining our exposures to the CSI-500 Index. In the meantime,

Our view that Chinese SME’s represent an attractive risk-reward

our exposure remains risk controlled to the downside through the

given the prevailing high base-real rates and supportive strategic

purchase of equity put options that are more than fully funded by

policy is currently expressed in the Inflation Plus portfolios via a

the outperformance received on the swap. We also hold a small

protected derivatives exposure to small capitalisation Chinese

allocation to Chinese government bonds as a risk offset. The

companies (a total return swap on the CSI-500 equity index with a

allocation to Chinese bonds serves purposes beyond offsetting share

high level of guaranteed outperformance of greater than 10%). This

market risk, helping to diversify our currency exposure away from

position has been in place for over 18 months and has delivered very

the US dollar (USD) and providing much needed carry, particularly

close to our expectations given the continued backdrop of SME

to the risk averse conservative portfolio.

supportive policy. And, while our thesis has played out well on an

absolute return basis, the importance of being selective in our The MLC Horizon portfolios maintain an overweight to China via a

allocation to China appears even stronger. For while the CSI-500 derivative exposure to the MSCI Emerging Markets Index that

Index is up 10% year-to-date, domestic large enterprises (the CSI-300 substitutes in the CSI-300 Index for the MSCI China Index holdings.

equity index) are down 5% and the tech-heavy and more globalised This is our way of balancing tracking error and our insights that

MSCI China Index is down almost 25% (Chart 3). domestic exposure to China is preferred over entities that have more

offshore exposure.

Chart 3: China’s share market year-to-date performance

YTD performance

0.3

0.2

0.1

0

-0.1

-0.2

-0.3

-0.4

Source: Bloomberg, 2021. CSI-500 CSI-300 MSCI China

6 | MLC's scenario insights & portfolio positioningThe Investment Futures Framework: Scenarios, changes

in return potential, and portfolio positioning

Scenarios With this in mind, we retain our three core pandemic scenarios with

very similar probabilities to last quarter.

In managing MLC’s multi-asset portfolios using our Investment

Futures Framework, following are the short-term scenarios that we Global pandemic: Immunity drives a return to growth (reduced

have assessed as currently providing the highest potential future probability)

risks and opportunities. Rollout of vaccines and innate immunity supress COVID-19 across

the northern hemisphere winter and spring season.

As the pandemic progresses to normalisation in the developed world,

other issues have begun to compete for importance in determining Further lockdowns are avoided.

the opportunities and challenges faced by investors. Nonetheless, Government stimulus fades.

we believe that COVID-19 remains strong enough a determinant of Consumer behaviour returns to near pre-COVID profile.

near-term risk to continue anchoring our short-term scenarios Elevated inflation persists.

thinking and mapping the outcome of many critical issues into one Interest rates rise, but lag inflation.

of the three scenarios.

Global pandemic: Slow return to normality (higher probability)

Inflation remains uncertain and is arguably at the behest of the Vaccine rollout continues at a moderate pace.

pandemic to a large extent. Under the most optimistic of our three Infection rates fall slowly.

scenarios, we believe that inflation will remain stubbornly above Earnings suffer in both FY21 and FY22.

central bank targets driven by a combination of supply and demand

Consumers remain cautious.

factors. Monetary policy will react, but most likely lag the inflationary

Inflation outlook remains ambiguous.

tendency, tempering real interest rates and steepening yield curves.

By contrast, lingering risks from the pandemic, should delta continue Global pandemic: Emergence of vaccine resistance (higher

to repress activity in the developed world, will drive an ambiguous probability)

inflation environment and the debate regarding supply-side impacts A severe vaccine-resistant strain of COVID-19 emerges. Full

will persist. Yet, should the COVID-19 pandemic take a turn for the lockdowns are re-established.

worst, with the emergence of a strain that is both virulent and more Fiscal and monetary stimulus near the point of exhaustion.

resistant to vaccines than delta, the resultant shock to demand will Acceleration of populism.

most likely drive inflation expectations lower and prompt a sharp High risk of global depression.

rise in risk aversion.

Disinflation or deflation are more likely than inflation.

There is however, one critical factor that sits outside the pandemic

but remains acutely important for Australian investors. China’s

economic fortunes and bilateral relationship with the West are an Changes in return potential for asset classes

axis of uncertainty that require careful consideration. For now,

The return potential across most asset classes remained more or less

Australia’s relationship with China is precarious but it remains

unchanged from the end of the June quarter (Chart 4).

unclear how much further China can go with economic reprisals. But

while Australia draws confidence from being a choice amongst one In terms of absolute levels, the five year return potential of all asset

for adequate volumes of high-quality iron ore, uncertainty over classes remains significantly below normalised long-term

China’s property construction sector and demand for steel are a risk expectations. Indeed, for some asset classes the long-term

for both price and volumes of iron ore. Our base case is that China’s expectation now lies close to the most bullish of our 40 scenarios,

supply cuts will be met and iron ore will settle at a level somewhere particularly for fixed income sectors whose long-term expectations

below US$100 per tonne. Yet, while $100 is a far cry from the US$240 sit beyond the average of the best 10% of scenarios on a five year

per tonne that prevailed in September, it is more than adequate to basis.

support domestic income and maintain a high level of profitability

for major domestic iron ore miners. A significant drop in iron ore

volumes represents the downside case for Australia. Thus, a sharp

drop (as opposed to a step-down) in Chinese residential construction

remains the critical risk to monitor. For now, the signals remain

comfortably above the negativity embedded in community and share

market prices. Steel prices indicate that the output curbs

implemented to date are greater than the drop in demand (stronger

prices), inventory levels are dropping and infrastructure plans in

China and abroad continue to grow.

MLC's scenario insights & portfolio positioning | 7The Investment Futures Framework: Scenarios, changes in return

potential, and portfolio positioning

Chart 4: 40 scenario set (generic scenarios) potential real returns (September 2021) - 5 years, 0% tax with franking

credits, pre-fees, pre-alpha

25% Average of best 10% tail Average of worst 10% tail 25%

Probability weighted expected returns Long-term 'normal' return

20% 20%

15% 15%

Real returns (% pa)

10% 10%

Real returns (% pa)

5% 5%

0% 0%

-5% -5%

-10% -10%

-15% -15%

-20% -20%

Global Listed Infrastructure

Australian cash

All maturities diversified fixed income

Global government bonds

Australian non-government bonds

Australian shares

Global shares (unhedged)

Global Listed Property

Short maturities diversified fixed income

Global non-government bonds

Global shares (hedged)

Australian government bonds

Private Equity

Australian inflation-linked bonds (all

Australian inflation-linked bonds (short

Global high yield bonds

maturities)

maturities)

Source: MLC Asset Management Services

Limited.

The potential real returns for each asset class are shown above. The probability-weighted real returns are shown as diamonds. For comparison we’ve included long-term

‘normal’ return expectations which are set by considering a stable fair value world – these are shown by the horizontal lines. Also, as an indicator of how uncertain

these returns are, we’ve taken the bottom (and top) 10% of the scenario real returns and calculated the probability-weighted average in those ‘tail’ outcomes. These

are shown in the bars. Asset classes with wider ranges could have more extreme return outcomes than those with narrow ranges.

Portfolio positioning We believe the addition of infrastructure further broadens the drivers

of growth within the portfolios while at the same time contributing

This quarter market movements proffered many opportunities for

valuable real income in an environment where traditional sources

us to take profits and enter into additional participate and protect

of yield are anaemic at best.

strategies in the Inflation Plus portfolios. We also made a new

allocation in the MLC Horizon portfolios to global listed infrastructure Details on portfolio positioning is in the sections: MLC Inflation Plus,

implemented through a strategy that provides market exposure after Horizon, Index Plus, Premium, and Value portfolios.

deducting fees, and swapped over Inflation Plus portfolios’

infrastructure exposure which was previously implemented via

derivatives. We believe the addition of infrastructure further

broadens the drivers of growth within the portfolios while at the

same time contributing valuable real income in an environment

where traditional sources of yield are anaemic at best.

8 | MLC's scenario insights & portfolio positioningReturn potential

Charts 5 and 6 show return potential for the MLC Horizon, Inflation Consistent with their objectives, the Inflation Plus portfolios have

Plus and Index Plus portfolios, and the Managed Account Strategies responded to shrinking return potential and weakening risk

respectively, based on our generic (40) scenario set, looking forward diversifiers by continuing to pursue a ‘Participate and Protect’

from the end of September 2021. strategy – adding to appropriately priced sources of return potential

in a risk-controlled way. This reduces the return potential in strong

The stronger risk focus of the Inflation Plus portfolios is evident

scenarios but provides tighter risk control in the event of an adverse

(Chart 5).

environment.

Chart 5: 40 scenario set (generic scenarios) potential real returns (September 2021) - 5 years, 0% tax with franking

credits, pre-fees, pre-alpha

25% 25%

Average of best 10% tail Average of worst 10% tail

Probability weighted expected returns Long-term 'normal' return

20% 20%

15% 15%

Real returns (% pa)

Real returns (% pa)

10% 10%

5% 5%

0% 0%

-5% -5%

-10% -10%

-15% -15%

Index Plus Conservative Growth

Index Plus Balanced

Inflation Plus Assertive

MLC Horizon 1

MLC Horizon 2

MLC Horizon 3

MLC Horizon 4

MLC Horizon 5

MLC Horizon 6

MLC Horizon 7

Index Plus Growth

Inflation Plus Conservative

Inflation Plus Moderate

Source: MLC Asset Management Services Limited.

The probability-weighted real returns are shown above (diamonds). For comparison we’ve included long-term ‘normal’ return expectations which are set by considering

a stable fair value world - these are shown by the horizontal lines. Also, as an indicator of how uncertain these returns are, we’ve taken the bottom (and top) 10% of

the scenario real returns and calculated the probability-weighted average in those ‘tail’ outcomes. These are shown in the bars. Portfolios with wider ranges could

have more extreme return outcomes than those with narrow ranges.

MLC's scenario insights & portfolio positioning | 9Return potential

Consistent with their Horizon and Index Plus multi-asset While both the Premium and Value Model Portfolios are expected to

counterparts, the medium-term return potential of all the MLC deliver similar returns, the additional levers and active management

Managed Account Strategies remains significantly below the returns dimensions afforded by the higher cost of the Premium Model

similar asset allocations have produced in the past (Chart 6). Portfolios result in slightly more positively skewed potential

outcomes, with incrementally higher returns in the most positive

scenarios and less negative returns in the worst.

Chart 6: MLC Managed Account Strategies - 40 scenario set (generic scenarios) potential real returns (September

2021) - 5 years, 0% tax with franking credits, pre-fees, pre-alpha

20% 20%

Average of worst 10% tail Average of best 10% tail

15% 15%

Probability weighted expected returns Long-term 'normal' return

10% 10%

Real returns (% pa)

Real returns (% pa)

5% 5%

0% 0%

-5% -5%

-10% -10%

-15% -15%

-20% -20%

Value Assertive

Premium Assertive

Value Moderate

Value Aggressive

Premium Moderate

Premium Aggressive

Model Portfolio

Model Portfolio

Model Portfolio

Model Portfolio

Model Portfolio

Model Portfolio

Source: MLC Asset Management Services Limited.

The probability-weighted real returns are shown above (diamonds). For comparison we’ve included long-term ‘normal’ return expectations which are set by considering

a stable fair value world - these are shown by the horizontal lines. Also, as an indicator of how uncertain these returns are, we’ve taken the bottom (and top) 10% of

the scenario real returns and calculated the probability-weighted average in those ‘tail’ outcomes. These are shown in the bars. Portfolios with wider ranges could

have more extreme return outcomes than those with narrow ranges.

10 | MLC's scenario insights & portfolio positioningMLC Inflation Plus portfolios

The key portfolio activities during the September 2021 quarter,

The MLC Inflation Plus portfolios have flexible asset allocations

including up until the time of writing, were:

with few constraints which enable us to target tight control of

Introducing a second Australian dollar (AUD)/USD risk reversal risk over each portfolio’s time horizon.

trade. The leg-down in the AUD during September provided a

second opportunity for the portfolios to use optionality to reduce We’ve replaced the exposure to global listed infrastructure. Since

exposure to the USD. The zero-premium collar protects the fund December 2020 we’ve gained exposure through derivatives which

from losses above an exchange rate of $0.76, with the cost being we’ve now replaced with a strategy that provides market exposure

loss of the covered portion of USD exposure below $0.68 cents. after deducting fees. Infrastructure fulfils a role in the portfolios,

The fall in the AUD also provided the opportunity to profitably across multiple potential scenarios:

reduce some of the portfolios’ exposure to the British pound (GBP). In scenarios where inflation moves higher (a scenario that’s

UK economic fundamentals have deteriorated recently, with increasing in probability), returns from infrastructure may be

inflation surprising to the upside. The GBP is providing little by beneficial because infrastructure assets, particularly in regulated

way of currency diversification across scenarios, so the recent sectors like utilities, deliver stable earnings growth and cash

move higher relative to the AUD provided an opportune time to flows which tend to increase as inflation rises.

reduce the portfolios’ GBP position. The long-term nature of infrastructure cash flows sees them

Rolling our protected China exposure for another 12 months using perform well in environments of falling real yields (ie yields in

the same total return swap already in place. The CSI-500 Index excess of inflation), not unlike the one that’s prevailed for much

provides the portfolios with an exposure to a high growth of the last decade.

opportunity in China that is currently receiving the benefits of The long-term characteristics of infrastructure means they tend

policy support. The swap contract pays a fixed outperformance to outperform other growth assets should economic conditions

over the underlying total return index providing a budget to build sour.

put protection that caps losses if the market falls beyond a pre More details are available at mlc.com.au

specified threshold.

Taking profits on our Japanese yen (JPY) call and rolling the strike

up and out. This position is designed to protect against a weakening

of the JPY. The portfolios’ exposure to JPY forms part of a protective

core but is vulnerable to a rise in real rates. Other parts of the

portfolio have a similar sensitivity to changes in real rates (eg gold,

inflation linked bonds, infrastructure etc) making this a pain point

for the portfolios under an adverse interest rate scenario.

Optionality over JPY is the cheapest means of offsetting this risk.

A further allocation to our mining and energy thematic basket. We

took the strong sell off in resources and energy to increase the

portfolios’ exposure to real cash flows. Prior to the sell off and in

recognition of price risk, the portfolios had made only a small

allocation to the basket. We are now close to full weight.

MLC's scenario insights & portfolio positioning | 11MLC Inflation Plus portfolios

Here is a summary of the changes to positioning of the MLC Inflation Plus portfolios over the recent quarter.

Asset class MLC Wholesale Inflation Plus portfolios change in target asset allocation over the

3 months ended 30 September 2021

Conservative Moderate Assertive

Chinese government bonds (through derivative Steady Steady Steady

strategies)

China A-shares with downside limit of -20% (through Steady Steady Steady

derivative strategies)

Emerging market shares (through derivative Steady Steady Steady

strategies)

Defensive Australian shares (including protected Steady Steady Steady

income mining and energy shares)

Global shares (through derivative strategies) Steady Steady Steady

Global listed infrastructure Steady Steady Steady

Global shares (unhedged) Steady Steady Steady

Foreign currency exposure Diversified basket Diversified basket Diversified basket

maintained maintained maintained

Gold exposure (through derivative strategies via call Steady Steady Steady

options)

Low correlation strategy Steady Steady Steady

Real return strategy Steady Steady Steady

Australian inflation-linked bonds Steady Steady Steady

Insurance-related investments Steady Steady Steady

Global high yield bonds and loans Steady Steady Steady

Global non-government bonds (short maturity) Steady Steady Steady

Global non-government bonds (all maturity) Steady Steady Steady

Australian non-government bonds (short maturity) Steady Steady No allocation

Cash Steady Steady Steady

Borrowings Not permitted Not permitted No borrowings

12 | MLC's scenario insights & portfolio positioningMLC Horizon portfolios

MLC Horizon portfolios made a new allocation to global listed

For the active management of the MLC Horizon portfolios, risk

infrastructure during the September quarter through a strategy that

is primarily benchmark-related. Strategic (benchmark) asset

provides market exposure after deducting fees. This strategy is

allocations have been designed to efficiently generate

benchmarked against the FTSE Developed Core Infrastructure 50/50 above-inflation outcomes on the basis of long-term investment

Index ($A hedged), providing the Horizon portfolios with an assumptions and taking into account that over time a broad range

economically and geographically diversified basket of infrastructure of scenarios could play out.

stocks.

Infrastructure assets are a useful addition to the portfolios at this During the quarter we also removed one of the Australian fixed

time, as they can fulfil a role across multiple potential scenarios. income managers, UBS Asset Management, from the Horizon 1

Their revenue streams are typically positively linked to inflation, portfolio. UBS’s focus on the macro economic environment was

particularly in the regulated sectors like utilities, which can provide previously complementary to our other short duration Australian

a steady source of real income in scenarios where inflation moves fixed income manager, Antares’, focus on credit. However, in recent

higher. We believe this will be beneficial for the portfolios moving years UBS hasn’t provided sufficient diversification of returns from

forward as the probability of higher inflation is increasing across our Antares. The Horizon 1 portfolio continues to have diversification

scenario set. across fixed income sectors and investment managers.

The long-dated nature of infrastructure cash flows also sees them MLC Horizon portfolios also inherit exposures through investment

perform well in an environment of falling real rates, not unlike the in Inflation Plus, providing important real return exposure and

one that has prevailed for much of the last decade. This ‘long duration’ sources of low correlation return streams. Inflation Plus’ activity this

characteristic means infrastructure can outperform other growth quarter was focused on reducing exposure to the USD by introducing

assets should economic growth sour. This dual profile of inflation a second AUD/USD risk reversal trade after the fall in the AUD in

linkage and protected growth makes infrastructure an appealing September, the AUD fall also provided the opportunity to profitably

addition to the portfolios. reduce GBP exposure, we rolled the protected exposure to Chinese

shares, took some profits on our strategy that provides protection

The significant underperformance of infrastructure since the start against a fall in the JPY, and after a sell-off in resources and energy

of the pandemic has provided an opportunity for the Horizon stocks we took the opportunity to make a further allocation to the

portfolios to get access to this asset class at an attractive valuation mining and energy thematic basket.

level. The addition of infrastructure further broadens the drivers of

growth within the portfolios whilst at the same time contributing

valuable real income in an environment where traditional sources

of yield are anaemic at best.

The allocation to infrastructure has been funded by reducing exposure

to global shares (hedged), inflation-linked bonds and Inflation Plus.

More details are available at mlc.com.au

MLC's scenario insights & portfolio positioning | 13MLC Horizon portfolios

Here is a summary of the positioning of the MLC Horizon 4 Balanced Portfolio.

Asset class MLC Wholesale Horizon 4 Balanced Portfolio target asset allocation at

30 September 2021

Under Strategic asset allocation Over

Australian shares

•

Global shares (unhedged)

•

Global shares (hedged)

•

Global property securities

•

Global listed infrastructure

•

Cash

•

Australian bonds (short maturities)

•

Australian bonds (all maturities)

•

Australian inflation-linked bonds

•

Global bonds (short maturities)

•

Global bonds (all maturities)

•

Global non-investment grade bonds (high yield bonds and loans)

•

Real return strategies (including Inflation Plus)

•

Low correlation strategy

•

14 | MLC's scenario insights & portfolio positioningMLC Index Plus portfolios

Asset allocation positioning of the MLC Index Plus portfolios was

Risk is primarily benchmark-related for the Index Plus portfolios.

little changed in the September quarter.

Strategic (benchmark) asset allocations have been designed to

MLC Index Plus portfolios inherit exposures through investment in efficiently generate above-inflation outcomes on the basis of

the real return strategy, providing important real return exposure long-term investment assumptions and taking into account that

and sources of low correlation return streams. The real return over time a broad range of scenarios could play out.

strategy’s activity this quarter was focused on accessing reasonably

priced return sources whilst at the same time controlling for adverse The foreign currency basket was also adjusted through the addition

outcomes: of an AUD/USD derivatives strategy and a resetting of the USD/JPY

Additional growth exposure was added through the customised calls. Currency remains an important risk control mechanism in

basket of mining and energy stocks, as well as rolling the China the real return strategy, but the fall in the AUD over the quarter

shares exposure via a CSI-500 Small Cap Index swap. Both these provided the opportunity to profitably reduce some of the foreign

strategies have embedded option protection to limit losses, currency exposure.

consistent with our ‘Participate and Protect’ mantra. Here is a summary of the positioning of the MLC Index Plus Balanced

Portfolio.

Asset class MLC Wholesale Index Plus Balanced Portfolio target asset allocation at 30

September 2021

Under Strategic asset allocation Over

Australian shares

•

Global shares (unhedged)

•

Global shares (hedged)

•

Global property securities

•

Cash

•

Australian bonds (short maturities)

•

Australian bonds (all maturities)

•

Australian inflation-linked bonds

•

Global bonds (short maturities)

•

Global bonds (all maturities)

•

Real return strategies

•

MLC's scenario insights & portfolio positioning | 15MLC Managed Account Strategies

The MLC Managed Account Strategies were launched on 1 July 2020.

The MLC Managed Account Strategies are focused on providing

No major changes have been made to the portfolio asset allocations

investors with above-inflation returns through professionally

since then. We’ve positioned the portfolio for diverse and resilient

managed portfolios that are extensively diversified across asset

returns across asset classes in the following key ways: classes, specialist investment managers, and stocks.

Investing growth asset distributions to re-establish asset

allocation targets – Reinvestment of what were in some instances Inflation Plus changes – MLC Wholesale Inflation Plus portfolios’

substantial year-end distributions within global shares. While provide important real return exposure and sources of low

slightly moderated from prior levels, we retain our positioning correlation return streams. Inflation Plus’ activity this quarter was

towards a reflationary environment and are keen to benefit from focused on reducing exposure to the USD by introducing a second

the real cash flows of assets with revenues linked to inflation, most AUD/USD risk reversal trade after the fall in the AUD in September,

notably Australian and global shares. During July we took the the AUD fall also provided the opportunity to profitably reduce

opportunity to rebalance growth allocations back toward targets GBP exposure, we rolled the protected exposure to Chinese shares,

following payment of year-end distributions. took some profits on our strategy that provides protection against

Foreign currency diversification – Within global shares we a fall in the JPY, and after a sell-off in resources and energy stocks

continue to see foreign currency exposure as an important we took the opportunity to make a further allocation to the mining

diversifier (holding both hedged and unhedged global shares). and energy thematic basket. During July we took the opportunity

Active fixed income – Fixed income funds are actively managed, to rebalance the alternatives allocations back toward targets

which we believe is essential in effectively navigating a rising following payment of year-end distributions, most notably from

interest rate environment. Our fixed income duration is relatively global share managers.

short to help reduce the portfolio’s exposure to rising interest rates, Details of stock changes made since 30 September 2021 and the

and we selectively pursue investments in credit through Bentham’s rebalance in early July 2021 using income distributions, are available

funds. During July we took the opportunity to rebalance fixed in the Portfolio Activity Reports at mlcam.com.au

income allocations back toward targets following payment of

While there was a reasonable level of portfolio rebalancing activity

year-end distributions, most notably from global share managers.

over July and August for both the Premium and Value series of MLC’s

Managed Account Strategies, there were no changes in target

allocations during the quarter.

Asset class MLC Premium Model Portfolios change in target asset allocation over the 3 months

ended 30 September 2021

Moderate Assertive Aggressive

Australian shares Steady Steady Steady

- Active, direct, all cap Steady Steady Steady

- Active, ex-20 Steady Steady Steady

- Active, small cap Zero Steady Steady

Global shares Steady Steady Steady

- Active, quant, hedged Steady Steady Steady

- Active, growth, unhedged Steady Steady Steady

- Active, value, unhedged Steady Steady Steady

- Active, emerging markets, unhedged Zero Steady Steady

Global property securities Steady Steady Steady

- Active, hedged

Alternatives and other Steady Steady Steady

- Inflation Plus Steady Steady Steady

- Active, absolute return, hedged Steady Steady Steady

Fixed income Steady Steady Steady

- Australian, active, short maturity Steady Steady Steady

- Australian, active, all maturity Steady Steady Steady

- Global, active, all maturity, hedged Steady Steady Steady

- Global, active, high yield, hedged Steady Steady Steady

Cash Steady Steady Steady

16 | MLC's scenario insights & portfolio positioningAsset class MLC Value Model Portfolios change in target asset allocation over the 3 months ended

30 September 2021

Moderate Assertive Aggressive

Australian shares Steady Steady Steady

- Passive, direct, large cap Steady Steady Steady

- Passive, all cap Steady Steady Steady

- Active, small cap Zero Steady Steady

Global shares Steady Steady Steady

- Passive, developed markets, unhedged Steady Steady Steady

- Passive, developed markets, hedged Steady Steady Steady

- Active, emerging markets, unhedged Zero Steady Steady

Global property securities Steady Steady Steady

- Passive, hedged

Alternatives and other Steady Steady Steady

- Inflation Plus

Fixed income Steady Steady Steady

- Australian, active, short maturity Steady Steady Steady

- Australian, active, all maturity Steady Steady Steady

- Global, active, all maturity, hedged Steady Steady Steady

- Global, active, high yield, hedged Steady Steady Steady

Cash Steady Steady Steady

Any portfolio change shown above is not a guarantee of a change to a client's portfolio. There may be differences between the Model Portfolio and a client's portfolio

due to the timing and transaction prices for portfolio changes, client investments and withdrawals during the period, timing of receipt of dividends and income

distributions, platform administration fees, transactional costs associated with the client's portfolio, and any portfolio exclusions required by the client.

MLC's scenario insights & portfolio positioning | 17Appendix 1 – MLC’s market-leading investment process 18 | MLC's scenario insights & portfolio positioning

Important information (continued from page 2)

MLC funds and Managed Account Strategies referenced in this communication are listed below. These funds appear on MLC’s platforms, in

addition to a number of external platforms:

MLC Investment Trust: MLC Super Fund: MLC Managed Account Strategies:

MLC Wholesale Horizon 1 Bond Portfolio MLC Horizon 1 Bond Portfolio MLC Premium Moderate Model Portfolio

MLC Wholesale Horizon 2 Income Portfolio MLC Horizon 2 Capital Stable Portfolio MLC Premium Assertive Model Portfolio

MLC Wholesale Horizon 3 Conservative Growth MLC Horizon 3 Conservative Growth Portfolio MLC Premium Aggressive Model Portfolio

Portfolio

MLC Wholesale Horizon 4 Balanced Portfolio MLC Horizon 4 Balanced Portfolio MLC Value Moderate Model Portfolio

MLC Wholesale Horizon 5 Growth Portfolio MLC Horizon 5 Growth Portfolio MLC Value Assertive Model Portfolio

MLC Wholesale Horizon 6 Share Portfolio MLC Horizon 6 Share Portfolio MLC Value Aggressive Model Portfolio

MLC Wholesale Horizon 7 Accelerated Growth MLC Horizon 7 Accelerated Growth Portfolio

Portfolio

MLC Wholesale Inflation Plus Conservative MLC Inflation Plus Conservative Portfolio

Portfolio

MLC Wholesale Inflation Plus Moderate MLC Inflation Plus Moderate Portfolio

Portfolio

MLC Wholesale Inflation Plus Assertive MLC Inflation Plus Assertive Portfolio

Portfolio

MLC Wholesale Index Plus Conservative MLC Index Plus Conservative Growth Portfolio

Growth Portfolio

MLC Wholesale Index Plus Balanced Portfolio MLC Index Plus Balanced Portfolio

MLC Wholesale Index Plus Growth Portfolio MLC Index Plus Growth Portfolio

MLC's scenario insights & portfolio positioning | 19We welcome your feedback on this document.

If you have any comments, please email us at ben.mccaw@mlc.com.au, al.clark@mlc.com.au or

anthony.golowenko@mlc.com.auYou can also read