MAAGT replaces the FANG companies - Weekly Letter: 8 February 2023 Carlsquare Anders Elgemyr and Bertil Nilsson www.carlsquare.com

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Weekly Letter: MAAGT replaces the FANG companies 8 February 2023 Carlsquare Anders Elgemyr and Bertil Nilsson www.carlsquare.com

MAAGT replaces the FANG companies

• If you look at correlations in the stock market, the five

companies behind the acronym MAAGT drive the

market - Apple, Microsoft, Amazon, Google, and Tesla.

These five stocks should be on every trading desk

because they show where money is going. This has

been true in the past two years' bull and bear markets.

• The big battle between Microsoft and Google on the AI

scene is exciting. Which company will win?

• The Q4 earnings season has improved slightly, but

technical reasons, with an eye on the Fed and inflation,

are driving the market. There is still some room to the

upside, but stay close to the exit door.

We are often asked why we always start with the S&P 500. It

is because it is the best proxy for global and leading stock

markets. The S&P 500 is also the proxy for the US equity

markets. It represents about 80% to 85% of the US equity

market. From a global perspective, the US means more than

half of the global stock market cap, according to S&P, which

calculates the index.

We studied the stocks in the S&P 500 to identify the leaders

in the S&P 500.

We have all heard about the FANG stocks leading the market

- Facebook, Amazon, Netflix and Google. You missed Apple,

so that has been added.

FANG is now also breaking up weekly, which is highly

interesting to the overall market.

1

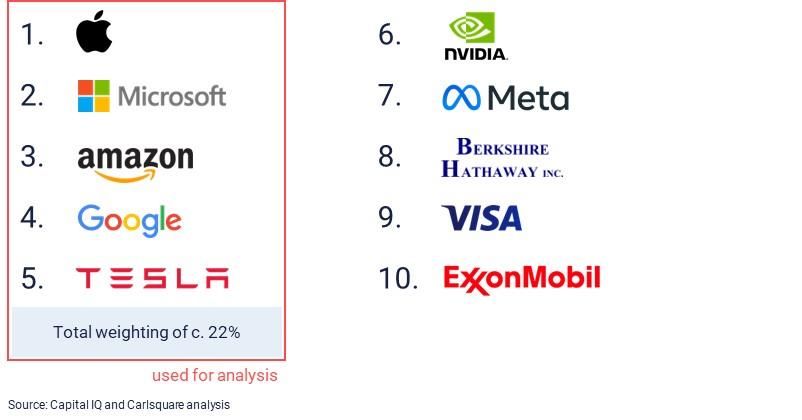

MAAGT replaces the FANG companies Carlsquare has studied the stocks in the S&P 500 index to identify the leaders in the index. We replicated the S&P 500 for each share and calculated absolute daily returns based on their weighting in the index. This allowed us to see the daily impact of each share on the overall movement of the S&P 500. Our analysis shows that it is no longer the FANG stocks that are leading the pack. It is the following stocks: Apple, Microsoft, Amazon, Google, and Tesla are the leaders. Combined, we can call them the MAAGT (as in mighty). Note that almost all the top stocks are tech stocks. Of the top seven, only Tesla is not a pure tech stock, although there is a case to be made for that too. 2

MAAGT replaces the FANG companies In the 2021 rally, these GAAMT stocks led the market and boosted the overall S&P 500 index by 9.3%. What goes up must come down. When the stock market crashed in 2022, these five GAAMT stocks dragged the S&P 500 down by 9.1%. To understand the actual trend in the market, you need to know where the generals are going. Follow the MAAGT! 3

MAAGT replaces the FANG companies Apple is, of course, the most important stock. It is back in positive territory after testing well below the MA200. There was another battle between Microsoft and Google over artificial intelligence in the tech sector after Microsoft launched Chat GPT, and Google responded with its Bard service. 4

MAAGT replaces the FANG companies We will watch this chart closely over the coming months. Either the stock market will decide which companies will succeed in the artificial intelligence market, or both will be premiered, as was the case when mobile phones lifted Ericsson and Nokia in the 90s. It will also be interesting to see which other companies, like Apple, will enter the scene. Stay tuned. The S&P 500 has broken above the falling trend line, and the bulls are in charge. The closest resistance and magnet is the gap from August last year and then the symmetry calculation. Eyes are on next week's inflation report. It will be calculated with a new methodology, but it is not the numbers that are important; it is the market’s reaction that counts. This time the inflation report falls on Valentine's Day (don't forget the flowers). But it is also at the end of the reporting season, which often produces a softening market sentiment. Next week will be very important for the market. We are still waiting for one more leg down before we have a more extended bull market. But we are not in the driver's seat, so stay humble and nimble! 5

MAAGT replaces the FANG companies

Q4 2022 Earnings season

After another busy week of reporting, 50% of S&P500

companies have reported their Q4 results. The number of

better-than-expected earnings reports improved slightly to

70% from 69% last week. The number of better-than-

expected revenue reports has increased from 60% to 61%.

The numbers are starting to stabilise around a slightly weaker

result than a typical quarter, where around 75% of S&P500

companies tend to report better-than-expected earnings. The

market impact of this is likely to be slightly negative.

S&P 500 Q4 2022 results vs expectations

80%

70%

70%

61%

60%

50%

39%

40%

30% 27%

20%

10% 3%

0%

0%

Above In-line Below

S&P500 companies' results S&P500 companies' revenues

Source: Factset Earnings Insight.

S&P500 company’s earnings growth in Q4 2022 has

deteriorated further from minus 5.0% one week ago to 5.3%.

The S&P500 sectors that have managed to beat analysts' Q4

2022 earnings forecasts by the most significant margin are

Utilities (100% of Q4 earnings better than expected), Health

Care (83%) and Information Technology (78%). The worst

performers are Financials (64%), Materials (50%) and

Commercial Services (36%).

6MAAGT replaces the FANG companies For Q1 2023, 37 S&P500 companies have issued negative earnings guidance, while six S&P companies have issued positive earnings guidance. Analysts' earnings estimates for S&P500 companies for Q1 2023 have declined by 3% and for FY 2023 by 2.5% from 31 December 2022 to 31 January 2023. As a result, the P/E of the S&P500 index has risen from 16.7 on 31 December 2022 to 18.4 on 31 January 2023. Looking at all S&P500 large-cap earnings reports since 17 January 2023, these companies have beaten analyst estimates by an average of 4.0%, with a median of 2.5%. The share price reaction to the Q4 2022 reports has been adverse by an average of 0.3% and 1.0% after the release of the Q4 2022 reports. 7

MAAGT replaces the FANG companies We have compiled 53 Q4 2022 reports submitted by OMX companies. The percentage of reports with better-than- expected results has increased to 56%, while 75% of Q4 reports had higher-than-expected revenues. Twelve OMX companies reported order intake for which there were analyst forecasts, and of these, seven (58%) were better than expected. Looking at the strong revenue performance in Q4, the weak Swedish SEK has had an impact. But it has also boosted costs, in some cases, for companies with a high proportion of imports (such as H&M and Axfood). Inflation also partly explains the higher-than-expected revenue outcome. Sources: www.di.se, Placera, Carlsquare. In terms of profitability, some sectors, such as B2B industries, have been able to pass on price increases to customers. Others, such as consumer discretionary and consumer staples companies, have yet to do so. Another impression of the Q4 2022 reporting season for OMX companies is how fragmented the results are for the engineering industry, with good reports from, for example, Sandvik, SKF and Alleima and poor ones from, for example, Atlas Copco and Volvo. The mixed performance in Q4 2022 also applies to the Swedish construction sector, with solid results from Skanska, JM and NCC and weak results from Peab and Bonava. 8

MAAGT replaces the FANG companies We conclude with a list of upcoming Q4 2022 reports and expected earnings per share. Source: Zacks Research. 9

MAAGT replaces the FANG companies Week Ahead The company reports on Wednesday, 8 February: Handelsbanken, Kindred, Wallenstam, Elkem, Veidekke, XXL, Lundbeck, Storebrand, Maersk, Neste, Yara, Aker Solutions, Equinor, Rockwool, Vestas, CVS Health, Goodyear, Smurfit Kappa, Sappi, Societe Generale, Sumitomo Metal, Walt Disney, Voestalpine. Japan's current account balance for December will be released at 0.50 CET. Sweden's production value index, industrial orders and household consumption for December will be released at 8.00 CET via the SCB. From the US, we get wholesale inventories for December and weekly oil inventories (DOE). The company reports on Thursday, 9 February: Astra Zeneca, Volvo Cars, Coor, Sweco, Munters, Lindab, Pandox, Fastpartner, Caverion, DNO, DNB, Huhtamäki, Outokumpu, Metsä Board, Orion, Atea, GN Store Nord, TGS, Arcelor Mittal, Aurora Cannabis, Baxter, British American Tobacco, Canopy Growth, Credit Agricole, Credit Suisse, Nippon Steel, Paypal, Pepsico, Philip Morris, Siemens, S&P Global, Toyota, Unilever. On Thursday, 9th February, the US will publish its weekly initial jobless claims figures. The EU holds a summit during the day. The company reports on Friday, 10 February: Saab, Thule, Millicom, Balder, Latour, New Wave, NP3, Troax, Kemira, Sanoma, YIT, Sampo, Aker BP, Entra, Schibsted. China's January CPI will be released at 2.30 CET. The UK will release Q4 GDP and December Industrial Production at 8.00 CET. Germany will publish its January CPI at the same time. In the afternoon, the Canadian unemployment rate for January and the US Michigan index for February will be released. 10

MAAGT replaces the FANG companies The company reports on Monday, 13 February: Castellum, Ratos. At 17.00 CET, we get inflation expectations from the US. The company reports on Tuesday, 14 February: Bettson, Boliden, Wihlborgs, Norsk Hydro, Orkla, Sats, Selvaag Bolig, Coca-Cola, Japan Tobacco, Thyssenkrupp. Capital Markets Day: Saab. Japan's Q4 2022 GDP and December industrial production will be submitted at 0.50 and 5.30 CET, respectively. At 8.00 CET, we will get UK unemployment (ILO) for December and the Eurozone GDP and employment for Q4 2022 at 11.00 CET. Opec also publishes its monthly oil report. From the US, we get weekly statistics from the NFIB small business index and CPI for January, weekly Redbook retail sales and oil inventories (API). 11

MAAGT replaces the FANG companies Valuation Tables, Swedish Equities Lowest P/E-ratio Highest Yield Bolag Price P/E NTM Bolag Price Yield, % Eastnine AB 126,2 2,3x Tele2 AB 92,1 21,4 Arise AB 48,6 2,8x Bonava AB 25,3 12,5 Maha Energy AB 9,1 2,8x SSAB AB 72,6 10,6 Bonava AB 25,3 3,4x Clas Ohlson AB 72,1 10,1 Tethys Oil AB 56,4 3,5x Rottneros AB 14,6 9,4 Ferronordic AB 87,0 4,6x Tethys Oil AB 56,4 9,0 Svedbergs i Dalstorp AB 26,0 4,8x Svedbergs i Dalstorp AB 26,0 8,9 Humana AB 24,5 5,2x Peab AB 58,5 8,3 Serneke Group AB 24,5 5,5x Resurs Holding AB 26,4 8,0 Bong AB 1,1 5,6x Telia Company AB 26,3 7,9 Source: S&P Capital IQ/Carlsquare Source: S&P Capital IQ/Carlsquare Lowest priced Net Asset Value Lowest priced NAV on a debt-free basis Bolag Price P/B Bolag Price EV/tB Oscar Properties Holding AB 2,1 0,1x Oscar Properties Holding AB 2,1 0,1x Eniro Group AB 0,7 0,2x Serneke Group AB 24,5 0,3x Serneke Group AB 24,5 0,3x Bonava AB 25,3 0,3x Bonava AB 25,3 0,3x Cint Group AB 22,7 0,4x Cint Group AB 22,7 0,4x Humana AB 24,5 0,4x Corem Property Group AB 11,4 0,4x Vivesto AB 0,4 0,4x BHG Group AB 16,5 0,4x K2A Knaust & Andersson Fastigheter AB 15,3 0,5x Vivesto AB 0,4 0,4x Aktiebolaget Fastator 12,9 0,5x K2A Knaust & Andersson Fastigheter AB 15,3 0,4x Concejo AB 30,7 0,5x Humana AB 24,5 0,4x Projektengagemang Sweden AB 11,6 0,5x Source: S&P Capital IQ/Carlsquare Source: S&P Capital IQ/Carlsquare Lowest priced earnings growth Top priced earnings growth Bolag Price PEG Bolag Price PEG Karnov Group AB 61,5 0,2x Hufvudstaden AB 156,5 64,7x Volvo Car AB 52,7 0,2x Sweco AB 120,5 5,9x Projektengagemang Sweden AB 11,6 0,4x Storskogen Group AB 9,6 4,5x Netel Holding AB 29,1 0,4x Garo Aktiebolag 100,5 4,4x Humana AB 24,5 0,5x K-Fast Holding AB 27,7 4,4x Ambea AB 40,4 0,5x Wallenstam AB 49,1 3,8x Better Collective A/S 179,9 0,5x Securitas AB 103,3 3,6x Truecaller AB 40,0 0,5x Nordisk Bergteknik AB 31,3 3,4x New Wave Group AB 242,4 0,5x CellaVision AB 208,0 3,4x Stillfront Group AB 18,9 0,7x Biotage AB 174,4 3,2x Source: S&P Capital IQ/Carlsquare Source: S&P Capital IQ/Carlsquare 12

MAAGT replaces the FANG companies Disclaimer: The information in this presentation is based on what the publisher Carlsquare deems to be reliable sources. However, we cannot guarantee its content. Nothing written in the presentation should be construed as a recommendation or solicitation to invest in any financial instrument, option or the like. Opinions and conclusions expressed in the presentation are intended for the recipient only. The content may not be copied, reproduced, quoted, or distributed to any other person. Carlsquare shall not be liable for any losses whatsoever caused by decisions made based on information contained in this presentation. Historical returns should not be taken as an indication of future returns. Changes in foreign currency may affect the value, price, or yield of an investment made abroad or in a foreign currency. The analysis is not directed at U.S. Persons (as that term is defined in Regulation S under the United States Securities Act and interpreted in the United States Investment Companies Act of 1940), nor may it be disseminated to such persons. The analysis is not intended for natural or legal persons where the distribution of the analysis to such persons would involve or entail a risk of violation of Swedish or foreign laws or regulations. 13

You can also read