GRAND REOPENING: NEW OPPORTUNITIES, OLD RISKS - 09 June 2021 04 A grand reopening, but a multifaceted recovery - Euler Hermes

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Photo by Artem Beliaikin on Unsplash GRAND REOPENING: NEW OPPORTUNITIES, OLD RISKS 09 June 2021 04 A grand reopening, but a multifaceted recovery 09 Markets have already celebrated, now they have to digest 13 Regional outlooks

Allianz Research

Vaccine security will shape the grand reopening. While advanced economies

delivered on immunization campaigns, vaccine hesitancy and second-

EXECUTIVE generation vaccines are first-order priorities. In the meantime, under-

vaccination in Asia and in Emerging Markets may cause desynchronized

growth paths.

SUMMARY A multifaceted recovery: high-pressure economics in the US, low-pressure eco-

nomics in Europe. We expect global GDP to grow by +5.5% in 2021, with the

US being a clear outperformer. In Europe, the return to pre-crisis levels will

take one year more compared to the US (Q1 2022) and the return to the pre-

Covid-19 growth path an extra four years – if it happens at all.

Ludovic Subran, Chief Economist

Revenge spending is happening but residual savings to amount to EUR500bn

+49 (0) 1 75 58 42 725

in Europe, and USD1trn in the US. Consumption will lead the recovery as we

ludovic.subran@allianz.com

expect pent-up demand to reach 3% of GDP in the US and the UK, and around

1.5% of GDP in Europe. However, hoarding behaviors remain for precautiona-

Alexis Garatti, Head of Economic Research ry reasons, complicating policy choices down the road.

alexis.garatti@eulerhermes.com

Inflation, what inflation? Bottlenecks in terms of supply (raw materials, trans-

Eric Barthalon, Head of Capital Markets Research portation capacity, workers) will likely keep cost inflation at a five-year high

eric.barthalon@allianz.com

until the end of 2021. Companies’ pricing power remains limited, notably in

Ana Boata, Head of Macroeconomic Research Europe. Households’ purchasing power will be under pressure as the employ-

ana.boata@eulerhermes.com ment gap (4 million jobs in the Eurozone and more than 7 million in the US)

will keep wage inflation in check. But no monetary inflation is likely as the ve-

Jordi Basco Carrera, Fixed Income Strategist

locity of money is at a record low.

jordi.basco-carrera@allianz.com

Aurélien Duthoit Sector Advisor The Faustian pact between expansionary fiscal and monetary policies is here

aurelien.duthoit@eulerhermes.com to stay. We expect central banks to be patient before hiking rates in 2023

Pablo Espinosa-Uriel, Capital Markets Research Analyst (some exceptions: Norway, New Zealand, the UK by September 2022). Total

pablo.espinosa-uriel@allianz.com global debt increased by more than USD24trn in 2020, including USD12trn of

public debt and USD12trn of private debt. Emerging Markets are more expo-

Françoise Huang, Senior Economist for APAC

sed to a sudden shift in market sentiment, which would impose a disorderly

francoise.huang@eulerhermes.com

adjustment of currencies and debt.

Patrick Krizan, Senior Economist for Fixed Income

patrick.krizan@allianz.com Political crossroads ahead for Europe but no repeat of the 2012 crisis in 2022.

In the Eurozone the Next Generation EU fund and the ECB will support the

Ano Kuhanathan, Sector Advisor and Data Scientist

ano.kuhanathan@allianz.com

recovery and keep financial stress at bay while German-French elections may

create policy surprises. Yet, watch out for heterogeneity.

Maxime Lemerle, Head of Sector and Insolvency Research

maxime.lemerle@eulerhermes.com Credit risk under control. The insolvency puzzle continues as corporate debt

Marc Livinec, Sector Advisor increased to new highs but cash on the balance sheet did, too, and liquidity

marc.livinec@eulerhermes.com support to firms will continue into 2022. European non-financial companies

will have to increase their margins by 1.5pp on average in order to make their

Selin Ozyurt, Senior Economist for France and Africa

debt sustainable.

selin.ozyurt@eulerhermes.com

Patricia Pelayo-Romero, Expert Insurance Green is the new black of industrial policy. The transition towards a cleaner

patricia.pelayo-romero@allianz.com model of growth will require the definition of a real new industrial policy, con-

Manfred Stamer, Senior Economist for Emerging Europe

sisting of generating new fiscal resources, subsidizing the transition, protecting

and the Middle East domestic producers and investing in infrastructure. Over the 2021-50 period,

manfred.stamer@eulerhermes.com annual energy sector investment has to increase by around 1% of global GDP

compared to today's levels to enable a net-zero energy transition. With

Katharina Utermöhl, Senior Economist for Europe USD1.3trn, investment in renewable electricity will need to surpass the highest

katharina.utermoehl@allianz.com level ever spent on fossil fuel supply (USD1.2trn in 2014).

Markus Zimmer, Senior Expert, ESG

markus.zimmer@allianz.com

2

09 June 2021

Political risk remains amid a new US paternalism and tactical multilateralism.

The US has launched a new wave of global and multilateral initiatives for cli-

mate change and tax policies. But such a revival in international engagement

does not necessarily mean unselective multilateralism: so far in 2021, the US

has been the most active with trade protectionist measures and China and

Germany the most targeted (in net terms). While the Asia-Pacific region could

see some acceleration in the expansion and implementation of free trade

agreements (eg. RCEP, CPTPP etc.), it is not immune to pre-existing geopoliti-

cal tensions that have worsened with the Covid-19 crisis (eg. China and the

“Quad”).

Markets’ risk-on music keeps on playing but mind endogenous financial insta-

bilities. Most asset classes are front-running the grand reopening and strong

policy support far better than expected. But the upside is limited now while

growing imbalances increase risks to the downside.

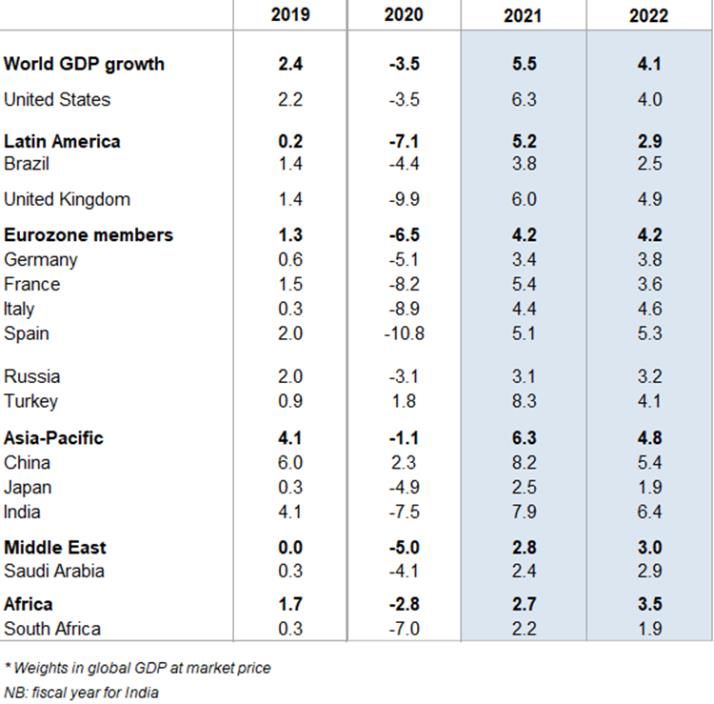

Figure 1: Real GDP growth forecasts, %

NB: Weights in gloabl GDP at market price

NB: fiscal year for India

Sources: Euler Hermes, Allianz Research

3

Allianz Research

A GRAND REOPENING,

BUT A MULTIFACETED RECOVERY

Vaccine security to shape grand reope- Multifaceted recovery. High-pressure 19 growth path an extra four years – if

ning. While advanced economies deli- economics in the US, low-pressure it happens at all.

vered on immunization campaigns, economics in Europe. After nearing pre-

vaccine hesitancy, and second- crisis levels of growth in Q1 2021, Global trade is set to rebound strongly

generation vaccines, are first-order fueled by the US and China, the global in 2021, but bottlenecks will lead to

priorities. However, avoiding the vacci- economy looks set for a strong me- short-term hurdles. We forecast growth

nation fatigue trap will be key for a chanical recovery in the coming quar- of +7.7% in volume terms (after -8.0% in

sustainable reopening as demand-side ters amidst a grand reopening in seve- 2020) and +15.9% in value terms (after

hurdles are now following the supply- ral advanced economies. We expect -9.9% in 2020), supported by favorable

side ones. In the meantime, under- global GDP to grow by +5.5% in 2021, base effects, a stronger-than-expected

vaccination in Asia and in Emerging with the US being a clear outperformer momentum in the first months of the

Markets may cause desynchronized and the only economy where growth year and expectations of robust ex-

growth paths. Stop-and-go govern- will exceed its pre-Covid-19 path from ports out of Asia-Pacific, as well as

ment strategies to cope with the in- the end of the year. In Europe, the re- strong imports in the US, Europe and

crease in new cases – albeit more mo- turn to pre-crisis levels will take one China.

derate than previous waves - are still year more compared to the US (Q1

likely to continue. 2022) and the return to the pre-Covid-

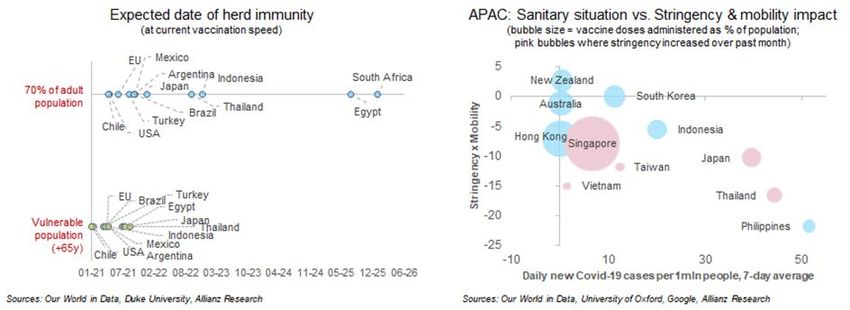

Figure 2: Covid-19 sanitary and vaccination situation

Mexico

5

European

1.5 Union

New Zealand

Japan Argentina Indonesia 0 South Korea

Indonesia

South Africa

1 -5 Hong Kong

Stringency x Mobility

Thailand

Brazil Egypt Australia Japan

Turkey -10 Thailand

0.5

Chile

United States

-15

0 Vietnam

-20

European Turkey

-0.5 Singapore Philippines

Union -25

Indonesia

Mexico

-1

Thailand -30 Taiwan

United States Egypt

Chile Argentina Japan

-35

-1.5 -10 0 10 20 30 40 50 60

01-21 Brazil 05-22 10-23 02-25 06-26

Daily new Covid-19 cases per 1mln people, 7-day average

Sources: Our World in data, Duke university, Euler Hermes, Allianz Research

4

09 June 2021

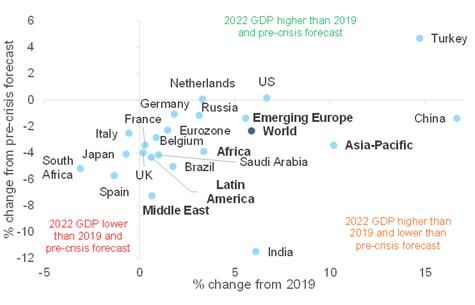

Figure 3: 2022 GDP, compared to 2019 and to pre-crisis forecast

Sources: Various, Euler Hermes, Allianz Research

Indeed, the global exports rebound has same time, global supply chains remain with the rise in input and asset prices.

until now clearly been driven by the disrupted, with suppliers’ delivery times Competition to access the workforce

Asia-Pacific region, with exports from and container prices from Asia at re- will significantly intensify with the grand

most other regions still below pre-crisis cord highs. As effects from fiscal stimuli reopening. The time needed for the

averages. However, the global supply- will start to be even more visible in the reallocation of the workforce, the lower

demand imbalance could be exacer- US as well as in the Eurozone in the incentive to work in the immediate af-

bated during the summer, given new coming months, demand for goods will termath of the reopening (relief effect)

Covid-19 outbreaks in Asia-Pacific, no- remain high (notably for building mate- and the persistence of high social trans-

tably in Taiwan, on which the world has rials and semiconductors), bringing fers could weigh on the pace of the job

become increasingly dependent in the input prices to a record high during the market’s recovery as mirrored by disap-

electronics sector. The impact of these summer. This situation is likely to prevail pointing numbers of non-farm US pay-

outbreaks on trade volume is likely to until the end of the year before de- rolls in April. In the UK, job shortages

be temporary and limited to Q2 (after mand starts normalizing and produc- have continued to intensify since the

which the epidemics in Asia-Pacific tion capacity ramps up, thanks to upco- second stage of eased restrictions in

trade hubs should be controlled), while ming business investments. The key April, notably in the transportation,

high prices due to input shortages are question will remain companies’ pricing construction and catering and hospita-

likely to remain for most of this year. power capacity, which is limited, nota- lity sectors. In the medium-run, negative

bly in Europe1. output gaps should keep wage pres-

Revenge spending is happening but sure in check as well as the employ-

residual savings to amount to Inflation, what inflation? Bottlenecks in ment gap compared to the long-term

EUR500bn in Europe, and USD1trn in terms of supply (raw materials, trans- average (4 million jobs in the Eurozone

the US. The grand reopening sets the portation capacity, workers) will likely and more than 7 million in the US). In

stage for a V-shaped recovery, but glo- keep cost inflation at a five-year high addition, companies have limited pri-

bal supply still needs to catch up. We until the end of 2021. Global inflationa- cing power, notably in Europe. Finally,

estimate pent-up consumption at 3% of ry pressures are at record high levels there is no monetary inflation as the

GDP in the US and UK in 2021, and at but the good news is that they are velocity of money is at a record low.

around 1.5% in most European coun- mainly driven by energy prices and

tries. Consumption will lead the recove- USD appreciation, which should prove

ry but hoarding behaviors remain for temporary. The cost inflation is likely to

precautionary reasons, complicating prevail until 2022, when pressures from

policy choices down the road. At the labor shortages should reduce along

1

See our recent report Pricing superpowers: Which sectors have them in the Eurozone?

5

Allianz Research

Figure 4: Inflation forecast

Eurozone core

6% EZ headline

US core Forecast

US headline

5% China

4%

3%

2%

1%

-1%

01/14 01/15 01/16 01/17 01/18 01/19 01/20 01/21 01/22 01/23

Sources: Refinitiv, Euler Hermes, Allianz Research

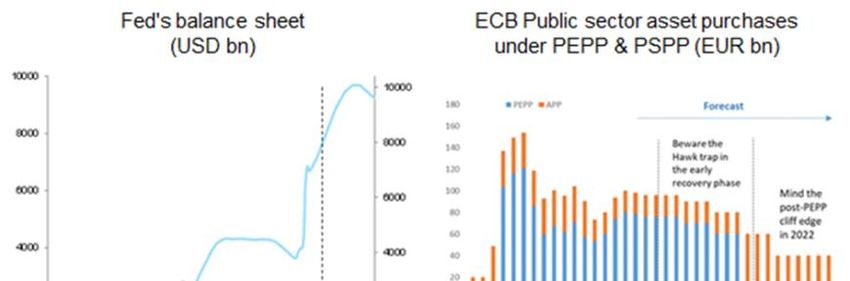

Faustian pact between expansionary ly, it should move away from pre- APP to continue for seven to 10 months

fiscal and monetary policies to stay. In committing to a quarterly purchase after March 2022. As we have learnt in

the short-term, central banks will conti- pace in an effort to make full use of the past, the ECB tends to have another

nue remaining highly accommodative PEPP’s inherent flexibility. From Sep- trick up its sleeve i.e. limits can be mo-

(with some exemptions such as Norway, tember onwards, the ECB should start ved. In that regard, the results of the

New Zealand and the UK by Septem- to give more guidance on what “life ongoing ECB strategy review expected

ber 2022). The Fed is expected to de- after PEPP” will look like. In particular, in September could come as a game-

ploy some elements of language on the focus will shift to the management changer, including by rolling over

tapering starting next year, with an of the PEPP cliff-edge when the pro- PEPP’s flexibility to APP. Some Emer-

operation twist from Q2 2022 and then grams end in March 2022. The monthly ging Markets should be an exception

a gradual reduction in securities pur- asset purchases under the APP will against rising imported inflation as pro-

chases from USD120bn per month to 0 most likely have to be lifted – at least tection of real household purchasing

in H2 2023, followed by a first rate hike for a few months – to EUR40-60bn to power will remain the focus in an envi-

in H2 2023. The ECB will continue to continue to ensure favorable financing ronment of increasing middle-income

ensure favorable financing conditions conditions. However, this could see the traps and social risk. Brazil, Romania,

during the early phase of the recovery ECB run into German debt limits: We Czechia, South Africa and Nigeria are

even as Eurozone inflation is likely to calculate that EUR40-60bn in monthly likely to hike three times by mid-2022.

overshoot at 2.5% y/y in H2 2021. Ideal- APP purchases would only allow for the

Figure 5: Fed & ECB scenarios

10000

180 PEPP APP Forecast

8000 160

140 Beware the

Hawk trap in

120 the early

6000 recovery phase Mind the

100 post-PEPP

80 cliff edge

in 2022

60

4000

40

20

2000 0

March

March

March

July

July

July

May

September

September

November

May

November

May

September

November

January

January

January

Forecast

0

03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

2020 2021 2022

Sources: Refinitiv, Euler Hermes, Allianz Research

609 June 2021

Political crossroads ahead for Europe context, there is a slim chance that the rather than a +40% surge (ceteris pari-

but no repeat of the 2012 crisis in 2022. government pushes for a softened ver- bus estimation). We expect a pragma-

Europe has learned from its crisis mis- sion of the reform that is likely to trigger tic and fine-tuned phasing-out of sup-

takes of the past, so don’t expect to see protests and social unrest again. port measures in order to manage the

any active fiscal or monetary tightening pressure on companies’ liquidity and

before H2 2022. In fact, the Next Gene- Herd policymaking: interventionism will solvability. Indeed, cash on balance

ration EU fund, next to providing a GDP still be at work in 2021. Switching from sheets increased to new highs at a glo-

boost of +1pp in 2021, will also cushion short-term to long-term policy will be bal level but so did corporate debt 3.

fiscal consolidation needs with grants gradual, and a complete withdrawal This will command European non-

not included in national deficit calcula- can take up to one year. Removing financial companies to increase their

tions. Meanwhile the ECB will look state support means a higher risk of operating margins to keep their debt

through the temporary inflation policy mistakes, especially as in theory sustainable (by 1.5pp on average,

overshoot and focus on maintaining firms still hold high cash balances2, everything else being equal). In addi-

favorable financing conditions, closing which might tempt some policymakers tion, the sectorial asymmetry of the

spreads (i.e. Italian fiscal heterogeneity to withdraw assistance mechanisms shock led to wide heterogeneity across

will be managed) and boosting policy faster. The increase in cash balances of sectors in terms of revenue, profits and

room for maneuvering via the strategy non-financial companies as of April impact on balance sheets. De facto,

review as German debt limits are mo- 2021 was EUR180bn in France, credit risk ratings recorded a stronger

ving closer. Among the large EU coun- EUR169bn in the UK, EUR 95bn in Ger- hit in sectors that bore the brunt of so-

tries, Italy will stretch its national fiscal many and EUR81bn in Italy. However, cial and mobility restrictions, such as

space the most (public deficit of 11.8% this cash should finance the recovery hotels and restaurants and transporta-

and 5.8% of GDP in 2021 and 2022) (i.e. stocks and WCR) and the new in- tion, with substantial positive perfor-

and, at the same time, will receive by vestment cycle, not a deleveraging pro- mance conversely in chemicals, phar-

far the largest share from the EU Reco- cess. maceuticals, retail and agrifood. The V-

very Fund (EUR192bn, of which shaped global recovery will lead to a

EUR69bn in grants). The prospect of a Avoiding the mistakes of an early or rebalancing in credit ratings from the

lasting fiscal integration in the EU there- disorderly fiscal tightening will be key wave of deteriorations posted in 2020

fore depends on the success of the Ita- for the sustainability of the recovery. but the heterogeneity across sectors is

lian recovery plan. If the implementa- China is already engaged in reducing likely to prevail until 2023.

tion is effective, Italy could indeed re- its monetary and fiscal impulses and

gain political credibility in the eyes of other countries could be tempted to The global economy could sponta-

the "frugal" sceptics. Capital markets follow suit. However, terminating assis- neously converge toward a new

have yet been complacent with Italy’s tance mechanisms in a premature Marshall plan for a climate-friendly

aggressive fiscal policy. The 10y spread manner could, for example, be the trig- recovery. We calculate that the

over Germany has stabilized in a range ger of a new wave of insolvencies USD2.3trn infrastructure package has

of 110 to 90bp. With ECB purchases, among non-financial companies. Brin- the potential to maintain the US econo-

fiscal variables have indeed lost much ging long-term perspectives to the cor- my’s growth potential at close to +2%

of their explanatory power for spread porate sector with infrastructure pro- by 2030 instead of +1.4% without it.

movements; a dangerous spread- jects and clearly defined industrial poli- However, execution risk could pose a

widening is only likely if the “Draghi put” cies could restore confidence and libe- problem for the EU EUR750bn Recove-

expires and political risk (“Italexit”) rate excess cash in the corporate sec- ry Fund. Accompanying demand over

reappears. In this context, the general tor. In the UK, for example, the phase- the medium-term will be key in order to

elections of H1 2023 are the next deci- out of policy support measures is set to liberate excess savings not consumed

sive event. Factoring in national elec- take a full year. The furlough scheme via pent-up demand. Around 40% of the

tions in other key political heavyweights ends in September 2021 though the excess cash from households and com-

Germany (base case: CDU/Green party reopening started in April. Meanwhile, panies (currently at more than 10% of

coalition) and France will keep a lid on the state-guaranteed recovery loan GDP in both the US and Europe) will

EU integration momentum until spring scheme ends in December 2021, all the morph into spending by year-end,

2022 while thereafter we expect to see discounted business rates end in March thanks to high pent-up demand. The

more evolution (investment in green & 2022, the reduced VAT rate ends in unleashing of the 60% remaining will

digital) than revolution. In France, on April 2022 and the state-guaranteed depend on the size of a positive confi-

the one hand, to avoid any social dis- mortgage loan scheme ends in Decem- dence shock that only a long-term,

content, we do not expect the govern- ber 2022. massive and coordinated fiscal plan

ment to implement any ambitious and can initiate. In the IEA projections

controversial reforms until the elections. (Figure 6), for a net-zero emission com-

An asymmetric normalization of credit

On the other hand, President Macron patible transition, investments need to

risk across sectors. Massive state inter-

will also need to reassure the electorate increase rapidly in electricity genera-

ventions helped suppress a significant

regarding pre-Covid commitments such tion, infrastructure and end-use sectors

wave of insolvencies in 2020, with the

as the pension reform that it still quali- while fossil fuel investment drops shar-

year ending with a -12% drop globally

fies as an “absolute necessity”. In this ply.

2

See our recent report European corporates: cash-rich sectors get richer 7

3

See our recent report European corporates: It could take 5 years to offload Covid-19 debt.Allianz Research

Figure 6: Projected global average annual energy investment needs for the

net-zero energy transition

Fuels

2016-20 Oil

2021-30 Natural gas

2031-40 Coal

Low-emissions fuels

2041-50

Electricity

2016-20 Fossil fuels without CCUS*

2021-30 Fossil fuels with CCUS*

Nuclear

2031-40

Renewables

2041-50 Battery storage

Infrastructure

Electricity grids

2016-20

EV** chargers

2021-30

Hydrogen infrastructure

2031-40 Direct air capture of CO₂

2041-50 CO₂ transport and storage

End-use

Renewables

2016-20 Hydrogen

2021-30 Efficiency

2031-40 Electrification

CCUS*

2041-50

0.5 1.0 1.5 2.0

Trillion USD (2019)

Source: International Energy Agency (2021), Net Zero by 2050, IEA, Paris: Net Zero by 2050

Scenario. *CCUS: Carbon capture, utilization and storage; **EV: Electric vehicle.

In particular, annual investment in elec- forefront of what we could consider as position will offer the possibility to im-

tricity generation would need to in- a new form of paternalism. Disclosure pose new norms (of trade among

crease from about USD0.5trn to can play an important role in fostering others) internationally.

USD1.6trn in 2030. The USD1.3trn of protectionism as supply chain laws

investment in renewable electricity is in coupled with ESG KPIs that, for ins- Such a revival in international engage-

the range of the highest level ever tance, include labor and human rights, ment indeed does not necessarily mean

spent on fossil fuel supply (USD1.2trn in result in diverging investment flows unselective multilateralism. Indeed,

2014). Energy infrastructure should in- away from foreign “red-flagged” activi- trade protectionist measures are still

crease from around USD290bn to ties into domestic ESG overperformers. being implemented in 2021, with the US

USD880bn in 2030 and include electri- being the most active and China and

city networks, public electric vehicle Political risk remains with a form of US Germany the most targeted (in net

(EV) charging stations, hydrogen re- paternalism and tactical multilatera- terms). Regulation affecting digital

fueling stations and import and export lism. Joe Biden’s foreign policy marks a commerce is also becoming increa-

terminals, direct air capture and CO2 revival of large-scale multilateral initia- singly apparent at the global level.

pipelines and storage facilities. In- tives such as the organization of a vir- While the Asia-Pacific region could see

vestments in end-use sectors should rise tual two-day climate summit in April some acceleration in the expansion

from USD530bn to USD1.7trn in 2030 2021 or the proposal of a global mini- and implementation of free trade

and include spending on deep retrofit- mum corporate tax rate of 15%. This agreements (e.g. RCEP, CPTPP etc.), it is

ting of buildings, transformation of in- approach, which could be compared not immune to pre-existing geopolitical

dustrial processes and the purchase of with a form of paternalism or a lea- tensions that have worsened with the

new low-emissions vehicles and more dership by the law or norms, initiates in Covid-19 crisis. Notably, China’s rela-

efficient appliances. our view a form of tactical multilatera- tions with each of the Quadrilateral

lism. In the case of the tax initiative, Security Dialogue members (the US,

Besides supporting demand, large in- there is a strong need to find new fiscal Australia, India and Japan) have

frastructure projects will define new resources. Total global debt has increa- become more tense over the past year,

industrial policies with similarities sed by more than USD24trn between with trade tensions and territorial dis-

across countries, pushing via innovation Q4 2019 and Q4 2020, including putes. While we do not expect these

and subventions towards cleaner ener- USD12trn of public debt and USD12trn issues to become economically signifi-

gy models, fostering digitization. They of private debt. USD10trn of supple- cant in the short term, they are sympto-

will not only maintain a high level of mentary debt is expected to be issued matic of a change of dynamics in the

protectionism, but also result in more in 2021. The need to find new sources geopolitical and global initiative

coordination at a global level in terms of fiscal revenues will imply not only spheres.

of tax policy, using multilateralism and raised taxes at a domestic level but

climate policy as a tactical tool of domi- also at an international level. In terms

nation by the law. The US will be at the of climate change policy, a leadership

809 June 2021

MARKETS HAVE ALREADY CELEBRATED,

NOW THEY HAVE TO DIGEST

The Fed Funds future market does not This rising uncertainty can be seen very inflation, which rose by another 10bps

expect more than a 25bps hike in the clearly when decomposing nominal to close to 2.5% for the 10-year maturi-

next two years. Investors remain thus long-term US yields into their expecta- ty, pushing real yields further into nega-

aligned with the Fed's communication tion and risk components (nominal tive territory (-25bp). But again, the

to deliberately take the risk of being term premium). Since the beginning of breakdown of risk and expectation

behind the curve. However, so far in Q2, the year, the 60bp increase of US 10y components shows that the recent rise

movements in capital markets have yields is almost entirely due to the risk is not due to a change of long-term

been much more muted and con- component (nominal term premium), expectations but to tight market condi-

trasted than in Q1, during which a clear reflecting heightened uncertainty tions (liquidity risk premium). The refla-

growth positioning took hold of all mar- about the economic and monetary tion trade is becoming increasingly

ket segments. Markets have not chal- equilibrium of the post-Covid era. Long- crowded (eg. strong inflows into TIPS

lenged the reflation trade that domi- term expectations about inflation and ETFs) while TIPS supply is withdrawn by

nated Q1, but they are now showing the real equilibrium rate have so far central bank purchases. Adjusted for

more concern about the inflation risk remained anchored. the liquidity risk premium, real yields

and the future course of monetary poli- have actually recovered to pre-crisis

cy. So while the economy is gearing up At first glance, this seems to be at odds levels, so the recovery is already fully

for the grand reopening, capital mar- with the development of break-even priced in.

kets are already one step ahead.

Figure 7: US 10y - breakdown of YtD increase Figure 8: US 10y term premium – breakdown

(different term structure models*) of YtD increase (different term structure models*)

1.0

1.0

0.6

0.6

0.2 0.2

-0.2

-0.2 ACM DKW CLR AZR

ACM DKW CLR AZR

Real term premium Inflation risk premium

Expectation Risk component

*Term structure models used: ACM (Adrian, Crump & Moench, 2013), DKW *Term structure models used: ACM (Adrian, Crump & Moench, 2013), DKW

(D'Amico, Kim & Wei, 2018), CLR (Christensen, Lopez & Rudebusch, 2010) and (D'Amico, Kim & Wei, 2018), CLR (Christensen, Lopez & Rudebusch, 2010) and

AZR (proprietary Allianz Research Model) AZR (proprietary Allianz Research Model)

Sources: Refinitiv, Euler Hermes, Allianz Research Sources: Refinitiv, Euler Hermes, Allianz Research 9Allianz Research

Figure 9: US 10y real yield – recovery fully priced in after adjusting for market frictions*

5.0

US 10y real yield

US 10y TIPS liquidity premium

4.0

US 10y liquidity adjusted real yield

3.0

2.0

1.0

0.0

-1.0

-2.0

2005 2007 2009 2011 2013 2015 2017 2019 2021

Sources: Refinitiv, Euler Hermes, Allianz Research

In our view, markets now have limited -sensitive stocks or equity sectors have ment in 2020 and Q1 2021. As of today,

upside potential. Sovereign bond mar- moved sideways or fallen. Former mar- more than 60% of the SPAC mergers

kets in the US but also the Eurozone ket darlings such as Tesla or the Ark that have been announced since the

have rebuilt a cushion against uncer- Innovation ETF now trade close to ~35% start of the year are now trading below

tainty. Their risk component of nominal below the year high. the IPO price of their SPAC.

yields is large by historical standards.

The distribution of potential outcomes Other highly speculative plays, such as As for cryptocurrencies, in early Q1

is skewed to the downside, especially in cryptocurrencies, have also taken a hit. 2021 the aggregated market cap of

the US. We see only a 14% probability Note that the correlation between Te- cryptocurrencies skyrocketed above the

for the US 10y yield to finish the year sla and Bitcoin has recently increased USD2trn mark, only to lose more than

above 2%. The rise of the US curve also (Figure 9). In the wake of the reflation USD500bn in a matter of days. It must

impacted European yields and helped trade, the gold sector (gold itself and be conceded that cryptocurrencies are

the Bund 10y to catch up to fair value (- gold mines) is on track to deliver no strangers to such sharp movements

0.25%). Improving economic momen- double-digit returns in Q2 after posting but the natural question that arises is

tum and increasing tapering rumors negative returns in Q1. where did this money go? Although the

have also contributed. We think that a answer in this “new” investment is not

switch into positive territory could be All in all, it is past midnight for risky as- straightforward, it confirms the recent

possible (18% probability), but we sets! As we showed in our last quarterly market exuberance, overtrading and

would not consider it sustainable. publication, our Kindleberger market irrationality.

cycle clock4 keeps ticking and has now

On the one hand, monetary and finan- made it past midnight. The combina- Another clear red flag that combines

cial conditions will continue to be sup- tion of extreme valuations paired with overtrading with increased moral ha-

portive, especially for risky assets. On elevated levels of overtrading has led zard is the rapid increase in money ve-

the other hand, perceived inflation risk, to large but isolated market corrections locity within financial markets. This in-

a new global sharing of the value ad- and is increasing the current market crease is relevant as it shows that the

ded, regulation and new assertive in- fragility. Among several late market recent equity rally has partly occurred

dustrial policies create the potential for cycle indicators, the rapid market cor- thanks to the market’s unconditional

financial instability. Monetary aggre- rection of “new” overtraded assets, as is trust in central banks’ unconditional put

gates show strong fluctuations as the the case for SPACs (Special Purpose protection, which has, in turn, led to a

velocity of money (the flow of Acquisition Companies) and cryptocur- rapid increase in financial money ve-

“liquidity”) is far more unstable, es- rencies, have caught the eyes of many locity. This red flag is particularly impor-

pecially in financial markets, than its market participants. tant as it is not the quantity of money

quantity (the stock of “liquidity” gene- but its circulation that causes asset

rated by QE). Risky assets are thus not SPAC IPOs have come to a halt in Q2 prices to rise or fall and historical expe-

totally in a safe spot. 2021, leading the market to substan- rience shows us that central banks do

tially correct. This comes after a subs- not control the velocity of money, es-

Credit spreads have remained close to tantial acceleration in both volumes pecially in capital markets.

the year lows, but the most interest rate and prices of this “new” financial instru-

4

See our Q1 2021 global economic outlook Race to the post Covid-19 recovery: 7 obstacles to overcome.

1009 June 2021

Figure 10: Bitcoin correlations Figure 11: # of SPAC IPOs (live & in progress)

0.6 600

FB Tesla Apple Gold

0.4 500

Rest of the World - In Progress

400

0.2 Rest of the World - Live

US - In Progress

300

US - Live

0.0

200

-0.2

100

-0.4

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 0

2015 2016 2017 2018 2019 2020 2021

Sources: Refinitiv, Euler Hermes, Allianz Research. Correlations are computed Sources: Refinitiv, Euler Hermes, Allianz Research.

using a 6M rolling correlation on daily changes

Figure 12: Cryptocurrencies vs USD (100 = 31.12.2019) Figure 13: Capital markets transactions velocity

10 5 000

3500

Velocity of US M2 in US equity market (L.H.S)

Datastream US total market index (R.H.S)

3000

Financial velocity (Turnover by value/M2) at annual rate

Bitcoin

2500

Ethereum

2000 Ripple

1 500

1500

1000

500

0

12-18 06-19 12-19 06-20 12-20 06-21 0 50

1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Sources: Refinitiv, Euler Hermes, Allianz Research. Sources: Refinitiv, Euiler Hermes, Allianz Research.

Finally, another signal of the recent On the fundamentals side, there has cause of this, the current over-stretched

market frothiness and overtrading can been a clear global frontloading of earnings expectations leave little to no

be found in the increasing amount of “good” earnings surprises into 2021, to room for further upside potential as the

margin debt and deposits in US clea- the detriment of 2022 earnings expec- probability of experiencing at or below

ringhouses, triggered by the rapid in- tations. This pattern can be observed expectations earnings numbers far out-

crease in options trading volumes since across the globe and specifically in the paces that of experiencing upside ear-

March 2020. At this point, things start to Eurozone and Emerging Markets. Des- nings surprises. This leaves markets in a

take a systemic flavor and although we pite being a normal consequence of really fragile spot and at the mercy of

maintain that, at current levels, there is the strong Q1 earnings season, the changes in investor sentiment.

enough public and private liquidity in grand reopening may not grant

the market to absorb the increased enough positive earnings tailwinds to

trading volumes, it is an overtrading red warrant the extreme amount of frothi-

flag. ness and positive expectations. Be-

11Allianz Research

Figure 14: S&P 500 consensus EPS growth (in %)

40

2021

30

20 2022

2017

10

2023

2018

0

2015 2016

2019

-10

2020

-20

-30

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Sources: IBES, Refinitiv, Euler Hermes, Allianz Research

But what does this all mean for risky bal equity markets to finish 2021 with Because of that, we believe investment

assets? Despite the mounting evidence upper single-digit returns but to con- grade credit will remain contained

of an upcoming market clean-up/ verge towards long-term average re- close to current levels until year-end

consolidation, we remain convinced turns (~5 to 7%) in 2022. In this context, while we expect some mild widening

that policymakers are fully aware of the we still expect the Eurozone and the UK within the high-yield space due to early

situation and would backstop any sign to outperform both US and EM equities. market consolidation. For 2022, we ex-

of a full-fledged market erosion. Due to pect credit spreads to structurally widen

that, we expect the unplugging of key Similarly, and on the back of lax poli- at a 20 to 30bps rate for investment

support measures to be contained and cies, credit spreads are set to range- grade and 50 to 70bps for high yield as

extremely gradual to allow for a mild trade for the remaining of the year companies reattach to fundamentals

but structural re-convergence to funda- while allowing for some initial market and markets start repricing fundamen-

mentals. In this regard, we expect glo- clean-up within the high yield space. tal credit risk.

Figure 15: S&P 500 decomposition (in %) Figure 16: US investment grade spread decomposition (in %)

200

30

150

20

100

10 50

0

0

-50

-10

-100

M2 Money Supply 10y inflation breakeven Consumer Confidence contribution

10y real yield USD NEER S&P500 volatility contribution

-20

Budget balance Estimate

-150 FED Balance Sheet Contribution

Budget Balance Contribution

IG spread y/y

-30 -200 Estimate y/y

2003 2006 2009 2012 2015 2018 2021

-250

2018 2019 2020 2021

Sources: Refinitiv, Euler Hermes, Allianz Research. Sources: Refinitiv, Euler Hermes, Allianz Research.

1209 June 2021

REGIONAL

OUTLOOKS

In the US, fiscal policy remains at the and monetary stimuli, but also from the 2022. Embodying a form of over-

forefront of economic policy initiatives success of the vaccination campaign heating, salaries will question the Fed’s

to restore growth and create jobs post (close to 65% of the adult population assumption that the current overshoot

Covid-19. The proposal for an infras- has been vaccinated, approaching the of inflation will be temporary. The on-

tructure package, initially estimated at 70% herd immunity threshold). The going acceleration of housing prices

USD2.3trn, has been revised on the latter has allowed for a swift reopening will also contribute to challenge this

downside to USD1.7trn by Democrats of the economy, boosting the effec- assumption as it announces an accele-

to give a chance for a bi-partisan tiveness of economic policy. ration of the shelter subcomponent of

agreement in the Congress by June the CPI index. Despite all of this, we

2021. Regarding the American Families We expect US GDP growth to reach expect US CPI to broadly normalize at

Plan, the White House has reiterated its +6.3% in 2021 and +4% in 2022 compa- 2.1% in 2022 compared with 2.5% on

intention to increase public spending red to the contraction of -3.5% in 2020. average in 2021 after the dilution of

for childcare, healthcare and education However, the window of opportunity to significant basis effects. This will give

by USD1.8trn by 2030. vote in new fiscal packages could be the Fed the opportunity to wait and see

rapidly closing as mid-term elections through H2 2021 before envisaging a

Between Q1 2020 and Q1 2021, the US are to be held in November 2022. On tapering. However, stronger growth

saw USD5trn of public spending. The the back of a stronger fiscal impulse and higher inflation compared with our

multiplier effect has been impressive as now penciled in our macroeconomic previous scenario could see a new

mirrored by a strong rebound of scenario, and as a result of stronger Operation Twist announced in H1 2022

growth, which was estimated at +6.4% growth, we expect the slack of the US in order to reduce the size of MBS pur-

q/q annualized in Q1 2021, coinciding job market (8 million jobs lost during chases and augment that of Treasuries

with a level of national production al- the crisis still need to be recovered) to in the USD120bn securities purchases

ready above the pre-crisis level. This rapidly decline and produce an accele- that the Fed operates on a monthly

impressive performance obviously re- ration of salaries, which should evolve basis. Any rate hike is still expected to

sulted from the strength of both fiscal close to +3.8% y/y at the horizon of take place in H2 2023 only.

Figure 17: US public debt (as % of GDP)

170%

160%

150%

140%

130%

120%

110%

100%

19 20 21 22 23 24 25 26 27 28 29 30

Sources: Refinitiv, Euler Hermes, Allianz Research.

13Allianz Research

In China, the overall solid recovery still domestic recovery fully broad-based, sures should ease going forward

needs to broaden, which means that the third layer that needs to recover is (producer inflation to peak in the co-

gradual policy normalization remains private consumption. Labor market ming months, while consumer core in-

the baseline scenario. We maintain our indicators are encouraging, with the flation is expected at 1.3% in 2021 vs.

GDP growth forecasts at +8.2% in 2021 unemployment rate at the lowest level 0.8% in 2020), giving more room for the

(after +2.3% in 2020) and +5.4% in 2022. since 2019, but household confidence is PBOC to use liquidity tools and macro-

The post-Covid-19 recovery of the do- not yet back to normal. In such a con- prudential regulation to tighten the

mestic economy can be broken down text, policy normalization carried out in overall monetary policy stance, while

into three layers. The first layer of public a gradual and flexible manner remains directing loans to areas most in need.

and policy-driven investment our baseline scenario. Authorities aim We expect the USDCNY rate at 6.3 at

(infrastructure and real estate) was to control structural vulnerabilities (eg. year-end. We estimate that fiscal sup-

behind the quick rebound in 2020. 2021 in the real estate and financial markets) port in 2021 (4.6% of GDP) will remain

is likely to be more focused on the se- without jeopardizing the economic re- generous but lower than in 2020 (7.1%).

cond layer of private business in- covery. Short-term pressures related to The year-to-date local government

vestment in the manufacturing sector. rising input prices not transmitting to special bond issuance has already

Our proprietary credit impulse index is output prices support our expectation dropped sharply (RMB230bn in April vs.

indeed a little more resilient for the pri- that the PBOC is likely to refrain from RMB1,150bn a year ago), in line with

vate sector than overall. To make the hiking policy rates this year. These pres- slowing infrastructure investment.

Figure 18: China fixed asset investment by sector, 2y CAGR (%)

20%

15% First layer of

recovery that drove Second layer

10% the quick rebound of recovery to

drive 2021

5%

0%

-5%

Infrastructure (value)

-10%

Housing starts (volume), HP-filtered

-15%

Manufacturing (value)

-20%

10-2019 04-2020 10-2020 04-2021

Sources: National Bureau of Statistics of China, Euler Hermes, Allianz Research

We expect Eurozone GDP to expand by and progress on the vaccination front demand will receive some tailwind from

+4.2% in both 2021 and 2022, with a (herd immunity should be within reach the EUR750bn EU Recovery Fund (GDP

return to pre-crisis levels in Q1 2022, by late summer across the EU) will see should be lifted by +1% in 2021 assu-

almost a full year after the US. Howe- Covid-19 restrictions eased swiftly (the ming no meaningful implementation

ver, some member states, including stringency index should drop back to delay) even though we expect it to be

Spain and Italy, will only reach this Q3 2020 lows in 2021). 20% smaller than advertised due to a

milestone at the turn of 2022/23. lower loan take-up. Meanwhile conti-

In Q2 2021, the Eurozone recovery will nuous strong export demand, driven by

The third wave of Covid-19 infections be kicked off with GDP growing close to the ongoing Chinese recovery and su-

postponed the Eurozone’s economic +2% q/q, thanks to strong base effects percharged, stimulus-induced US GDP

resurrection in Q1 2021. However, we in those sectors that have been stuck in growth, will continue to boost GDP

see the economic stars aligning to set economic hibernation. Reduced econo- growth in the coming quarters as the

the stage for an unprecedented econo- mic uncertainty will in turn set the stage global recovery momentum becomes

mic rebound over the rest of 2021. We for a consumption-led catch-up growth more synchronized, even though indus-

expect the Eurozone to record some of spurt in the second half of the year tries will face lingering bottlenecks for

the strongest quarterly expansion rates (with excess savings to the tune of 1.5% the remainder of 2021 in the form of

on record (second only to Q3 2020). of GDP turbocharging the recovery). longer delivery times and component

Abruptly receding new Covid-19 cases Last but not least, Eurozone domestic shortages.

1409 June 2021

At the same time, policymakers will France (Spring 2022). Flagship fiscal whereas the ECB will continue to en-

continue to do “whatever it takes” to measures, including furlough schemes sure favorable financing conditions

safeguard the recovery and shore up (which will see the unemployment rate during the early phase of the recovery,

public support ahead of key elections in peak below 9%) and public guarantees, even as Eurozone inflation is likely to

Germany (September 2021) and will be extended until at least fall 2021, overshoot at 2.5% y/y in H2 2021.

Figure 19: Employment in millions, Eurozone vs US

165 EZ Employment

160 EZ long-term trend (1995-2019)

US employment

155 US long-term trend (1995-2019)

150

145

140

135

130

125

Q1 1995Q1 1998Q1 2001Q1 2004Q1 2007Q1 2010Q1 2013Q1 2016Q1 2019

Sources: Refinitiv, Euler Hermes, Allianz Research

In Germany, after a rather disappoin- months, including accommodation and that curbed the impact of the crisis on

ting start to 2021, the economic pros- food services. The imbalance between incomes. With the grand reopening, we

pects are now very promising. In view rapidly rising labor demand and im- expect the pent-up demand to boost

of the recent decline in new infections paired supply – Covid-19 has weighed GDP growth by around +2pp in 2021. In

and good progress on the vaccination on immigration and vocational training May, business confidence soared to a

front, the service sector is likely to have programs and, in view of poor pros- three-year high (above its historical

already started to catch up in May, ac- pects in some sectors, led to a reorien- average), while retail and services sec-

companied by the first easing of restric- tation of workers to sectors with brigh- tors have registered strong confidence

tions. In the coming months, one posi- ter prospects - can be reduced by trai- gains. This rebound in confidence in the

tive economic record after the next can ning offensives and at least temporarily services sector, unprecedented in histo-

be expected in contrast to last year's higher wages. Given the notable re- ry, finally gives us a glimpse of the end

plunge into the abyss. We expect an bound momentum, the German labor of the multi-speed recovery between

unprecedented consumption rebound market should also embark on a firm sectors. The presidential election will

(+3% in Q2/Q3), fueled by pent-up de- recovery trend. By the end of 2021, al- take place in less than a year, though

mand in a context of sharply declining most one in two people who lost their only a few candidates, including Ma-

economic uncertainty. Meanwhile, the jobs in the wake of the Covid-19 crisis rine Le Pen, have officially announced

ongoing industrial upswing – despite should find new employment. The that they will run. President Macron has

lingering rebound bottlenecks in the unemployment rate will, however, re- unofficially started his re-election cam-

form of component shortages that main elevated at 5.8% in 2021 after 6% paign on the back of easing sanitary

should hold back production momen- in 2020. restrictions. In addition to security and

tum – should fuel a capex boom. Ove- immigration, we expect the following

rall, GDP growth should come in at In France, the domestic economy will economic issues to shape campaigns:

+3.4% in 2021 and +3.8% in 2022. As a be the major driver of the post Covid- (i) boosting industrial competitiveness

result, the German economy will return 19 recovery. With the accelerating and export performance via production

to pre-crisis GDP levels already by late pace of vaccination and the progres- tax cuts and other economic incentives,

2021. However, one should be prepa- sive re-opening of all sectors, we main- (ii) achieving a green transition and

red for some economic restart difficul- tain our growth forecast at +5.4% in implementing socially acceptable envi-

ties. The abrupt reopening of the 2021 and +3.6% in 2022. French house- ronmental policies, (iii) how to support

economy is likely to lead to acute labor holds’ excess savings reached over the incomes of those in precarious con-

shortages, especially in sectors that EUR140bn in the first quarter of 2021, ditions and (iv) pension and social secu-

have been stuck in hibernation for thanks to supportive state measures rity reforms.

15Allianz Research

Figure 20: Catch-up consumption in 2021, % of GDP

3.5

3.0

2.5

2.0

1.5

1.0

0.5

0.0

Denmark

Belgium

France

Austria

Norway

Portugal

US

UK

Spain

Italy

Netherlands

Germany

Poland

Sweden

Czechia

Eurozone

Sources: Eurostat, Euler Hermes, Allianz Research

Italy is targeting the biggest fiscal sti- (focused on working capital and debt 5.8% of GDP in 2022 in addition to dis-

mulus among Eurozone peers in 2021- restructuring) towards new investment. bursements of the NGEU (around 1.2%

22. Prime Minister Draghi’s “calculated We expect real GDP to grow by +4.4% of GDP in 2022). The flipside is the pu-

risk” of accelerating the reopening at in 2021 and +4.6% in 2022. blic debt level rising to 159% of GDP,

an early stage of the vaccination cam- and likely to remain above 140% for the

paign seems to be paying off so far as The strong fiscal stimulus remains the next 15 years. But this need not be a

infection numbers continue to decline. underlying force of the recovery. Italy problem if the national recovery plan

Moreover, the summer seems to be has played the fiscal card more than (EUR248bn, of which EUR192bn by

saved for the tourism sector (13% of other Eurozone countries, with the go- NGEU) succeeds in increasing potential

GDP). Consumption will rebound as the vernment so far mobilizing EUR170bn growth (target of 0.4% to 0.6% p.a.)

economy reopens. The recent strength (10% of GDP). This year alone, the defi- while financing costs remain low.

of investment could be a signal of bor- cit has been revised twice from -7.5% to

rowing switching from crisis mode -11.8% of GDP. It is still expected at -

Figure 21: Italy’s fiscal spending plans

20

18

16

14

12

10

8

6

4

2

0

Germany France Italy Spain

Domestic recovery support (2021-23)

EU loans (2021-23)

EU grants (2021-23)

National discretionary emergency support (2020-21)*

Sources: PNRR, EU Comission, Euler Hermes, Allianz Research

1609 June 2021

Figure 22: Italy’s potential GDP growth

110

108

106

104

102

100

98

96

94

92

2000 2005 2010 2015 2020 2025 2030

real GDP Potential GDP

Sources: : PNRR, Euler Hermes, Allianz Research

In Spain, mobility has improved over allocation constraints, while Spain has Plan could boost productivity and inno-

the first half of the year and will conti- already requested EUR69.5bn in grants vation to bridge the productivity and

nue to boost growth in the short-term. from the Resilience and Recovery growth gap between Spain and the EU-

The grand reopening and relaxation of Funds (RRF) but will not be able to sup- 8. In addition, we see the unemploy-

restrictions in Europe will prove to be port companies with them. The percen- ment rate remaining high in 2021

good news for the service-heavy econo- tage of companies subjected to great (15.9%) as emergency pandemic mea-

my. GDP growth in the first quarter pro- financial pressure has increased very sures are phased out, and starting to

ved more resilient than expected (-0.5% significantly (27pp) between 2019 and improve in 2022, with an average of

q/q) and with the return to normalcy we 2020 to 40%. Having more flexibility on 14.8%. We do not expect economic acti-

expect GDP to grow by +5.1% in 2021 spending would boost vulnerable com- vity to return to pre-pandemic levels in

and +5.3% in 2022, helped by the tou- panies so being able to negotiate the the next two years as political risks and

rism sector. In addition, upside risks use of the RRF would be monumental stimulus implementation hurdles could

come from the fiscal stimulus planned for Spanish companies that are strug- delay the recovery.

within the 2021 budget. This latter has gling financially. In the past, there have

already allocated EUR26bn of the been institutional hurdles to implemen-

NGEU grants. The NGEU funds have ting public spending. The Spain 2050

Figure 23: Public sector efficiency by country vs expenditure executed in

2014-20

0.8

Expenditure executed in 2014-2020 relative to

Netherlands

the European structure funds assigned

0.7

0.6 France

0.5 Portugal

0.4 Italy

Spain

0.3

0.0 0.5 1.0 1.5 2.0

Public sector efficiency indicator

Sources: : IMF Fiscal Monitor, Euler Hermes, Allianz Research

17Allianz Research

In the UK, the grand reopening will al- Credit conditions during the recovery In the medium-run, Brexit will continue

low pent-up demand equivalent to at phase may be tighter and excessive to have a negative impact on trade

least 3% of GDP to materialize in 2021 levels of corporate debt could limit flows with the EU. In Q1 2021, the im-

and push GDP up by +6%, one of the companies’ ability to borrow once state pact on imports from the EU fell by

highest European growth rates. The -support schemes are phased out. more than -20% against monthly flows

rapid pace of vaccination allowed the in 2019 while imports from outside the

economy to reopen, with mobility data Bottlenecks to the recovery are more EU remained in positive territory despite

improving and economic data strongly and more visible and probably exacer- the increased supply-chain disruption.

recovering since April, notably within bated by Brexit, particularly in the form Hence, the increase in import prices

the sectors that faced heavy restrictions of labor shortages in transport, cons- from the EU of about +5% due to non-

during lockdowns. We expect compa- truction and sectors such as tourism tariff barriers after Brexit is not so far

nies to invest actively in 2021 (+11.8% and catering and hospitality. Hence, from the tariff barriers for imports from

followed by +8.9%), supported by ex- pressures on wages are rising and we China, i.e. 6.5% excluding exchange

cess cash (GBP122bn or more than 5% expect overall growth to accelerate up rate effects. The question of the trade

of GDP). The hyper-amortization to +2.9% on average in 2022. In 2022, rotation remains high if trade hurdles

scheme until end-2023 should support we expect GDP growth to slow down to are not resolved, notably when the UK

business investment and sectors such as +4.9% as fiscal assistance mechanisms will also implement border controls on

manufacturing, transportation, food will fully end and the UK will be one of imports from the EU from October on-

and accommodation stand among the first countries to start fiscal and mo- wards. In addition, the end of the transi-

those most willing to use the tax break netary consolidation: in total, GBP30bn tion period for EU derivative products

in view of their higher share of total (1.3% of GDP) through a rise in personal clearance in the UK in mid-2022 could

assets accounted for by the plants and income tax in 2022, followed by the rise bring more downside risks to the sector,

vehicles to which the scheme applies. In in corporate tax to 23% in 2023. The given the tough negotiations on

the short run, a demand catch-up and Bank of England is also expected to "equivalence".

the reduction in spare capacities will raise the key interest rate as soon as

drive a business investment recovery. September 2022 (+15bp), embarking

However, it could take up to four years on an early, but timid monetary norma-

to return to long-term growth trends5 : lization cycle.

Figure 24: Planned end-dates for state support in the UK

Sources: UK government, Euler Hermes, Allianz Research

5

See our recent report Investment is back: harder, better, faster, stronger?

1809 June 2021

Bidirectional pressures on central from Covid-19 require a specific type of India, other countries previously cha-

banks in Emerging Markets. The first policy support, while fighting inflation racterized by low levels of contagion

quarter of 2021 saw the reemergence needs a different one. The events are now experiencing outbreaks and

of the concept of a Taper Tantrum6. As around the Turkish central bank or the new lockdown measures.

inflation figures are released, the political instability wave in Latin Ameri-

prophecies are coming closer to fulfill- ca are some examples. Taking the above-mentioned factors

ment. Central banks either have under- into account, the following months

taken rate hikes or are planning to (or These pressures have affected the could unveil Eastern EU countries as

even both). In some countries, market sovereign debt markets (Figure 26), some of the top performers of the

expectations exceed central bank tar- particularly in some of the TUCKANS7, grand reopening. For sovereign bonds,

gets for 2021. Furthermore, they also but also in Latin America as a region some of these countries may look like

exceed the long-term inflation expecta- and in Russia. an investment opportunity, with still

tions from our models. decent coupons, a relatively more opti-

Up until now and with exceptions, Asia mistic perspective than their other EM

The situation puts policymakers in a appears to be the region less influen- counterparts and bond prices not as

difficult tessitura: the idiosyncratic struc- ced by this hazard. However, the sani- crowded as in Asia.

tural problems and the severe damage tary situation may modify this: Besides

Figure 25: Proxy to EM breakeven inflation estimations. Figure 26: Largest increases (decreases) in LC Sovereign bonds yields.

Year to date.

Nigeria

Turkey (5Y)

Turkey

Colombia

South Africa (10Y) Brazil

Russia

Mexico

Brazil (10Y) Chile

Peru

Current B/Even 10Y 1Y

Philippines

Mexico (10Y) LT estimation

Hungary

+/-1 std. dev.

…

CB Target

Chile (10Y) India

Morocco

0% 3% 6% 9% 12% 15% 18% China

Croatia

-200 0 200 400 600 800

Sources: Refinitiv, BofA, Euler Hermes, Allianz Research; Inflation Target for Sources: Refinitiv, BofA, Euler Hermes, Allianz Research. When the 10Y or 1Y

the Central Bank of Turkey has been revised to 12.2% to adjust to reality, the are not references, the nearest maturity is taken into account.

aim is conversion to 5% in 2023.

6

See our recent report Taper Tantrum in 2021-22: Beware of the TUCKANS

7

Acronym used to designate the group made by Turkey, Ukraine, Chile, Kenya, Argentina, Nigeria and South Africa. Some of these countries, especially Argentina and Ukraine, do not

appear in Figure 24 as the point on 31.12.2020 was already high.

19You can also read