FIXED INCOME PRESENTATION - FIRST 6 MONTHS 2022 As of April 30, 2022

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

FIXED INCOME PRESENTATION FIRST 6 MONTHS 2022 As of April 30, 2022

FORWARD-LOOKING STATEMENTS AND NON-GAAP FINANCIAL MEASURES

Caution Regarding Forward-Looking Statements

Certain statements made in this document are forward-looking statements. In addition, representatives of the Bank may make forward-looking statements orally to analysts, investors, the media and

others. All such statements are made in accordance with applicable securities legislation in Canada and the United States. Forward-looking statements in this document may include, but are not

limited to, statements with respect to the economy—particularly the Canadian and U.S. economies—market changes, the Bank’s objectives, outlook and priorities for fiscal year 2022 and beyond, the

strategies or actions that will be taken to achieve them, expectations for the Bank’s financial condition, the regulatory environment in which it operates, the potential impacts of—and the Bank’s

response to—the COVID-19 pandemic, and certain risks it faces. These forward-looking statements are typically identified by verbs or words such as “outlook”, “believe”, “foresee”, “forecast”,

“anticipate”, “estimate”, “project”, “expect”, “intend” and “plan”, in their future or conditional forms, notably verbs such as “will”, “may”, “should”, “could” or “would” as well as similar terms and

expressions. Such forward-looking statements are made for the purpose of assisting the holders of the Bank’s securities in understanding the Bank’s financial position and results of operations as at

and for the periods ended on the dates presented, as well as the Bank’s vision, strategic objectives, and financial performance targets, and may not be appropriate for other purposes. These forward-

looking statements are based on our current expectations, estimates, and intentions and are subject to inherent risks and uncertainties, many of which are beyond the Bank’s control. Assumptions

about the performance of the Canadian and U.S. economies in 2022, including in the context of the COVID-19 pandemic, and how that will affect the Bank’s business are among the main factors

considered in setting the Bank’s strategic priorities and objectives including provisions for credit losses. In determining its expectations for economic conditions, both broadly and in the financial

services sector in particular, the Bank primarily considers historical economic data provided by the governments of Canada, the United States and certain other countries in which the Bank conducts

business, as well as their agencies.

Our statements with respect to the economy, market changes, the Bank’s objectives, outlook and priorities for fiscal year 2022 and beyond, are based on a number of assumptions and are subject to

a number of factors—many of which are beyond the Bank’s control and the effects of which can be difficult to predict—including, among others, the general economic environment and financial

market conditions in Canada, the United States, and other countries where the Bank operates; exchange rate and interest rate fluctuations; inflation; higher funding costs and greater market volatility;

changes made to fiscal, monetary and other public policies; changes made to regulations that affect the Bank’s business; geopolitical and sociopolitical uncertainty; the transition to a low-carbon

economy and the Bank’s ability to satisfy stakeholder expectations on environmental and social issues; significant changes in consumer behaviour; the housing situation, real estate market, and

household indebtedness in Canada; the Bank’s ability to achieve its long-term strategies and key short-term priorities; the timely development and launch of new products and services; the Bank’s

ability to recruit and retain key personnel; technological innovation and heightened competition from established companies and from competitors offering non-traditional services; changes in the

performance and creditworthiness of the Bank’s clients and counterparties; the Bank’s exposure to significant regulatory matters or litigation; changes made to the accounting policies used by the

Bank to report financial information, including the uncertainty inherent to assumptions and critical accounting estimates; changes to tax legislation in the countries where the Bank operates, i.e.,

primarily Canada and the United States; changes made to capital and liquidity guidelines as well as to the presentation and interpretation thereof; changes to the credit ratings assigned to the Bank;

potential disruption to key suppliers of goods and services to the Bank; potential disruptions to the Bank’s information technology systems, including evolving cyberattack risk as well as identity theft

and theft of personal information; and possible impacts of major events affecting the local and global economies, including international conflicts, natural disasters, and public health crises such as

the COVID-19 pandemic. There is a strong possibility that the Bank’s express or implied predictions, forecasts, projections, expectations or conclusions will not prove to be accurate, that its

assumptions may not be confirmed and that its vision, strategic objectives and financial performance targets will not be achieved. The Bank recommends that readers not place undue reliance on

forward-looking statements, as a number of factors, including the impacts of the COVID-19 pandemic, could cause actual results to differ significantly from the expectations, estimates or intentions

expressed in these forward-looking statements. These risk factors include credit risk, market risk, liquidity and funding risk, operational risk, regulatory compliance risk, reputation risk, strategic risk,

environmental and social risk, and certain emerging risks or risks deemed significant, all of which are described in greater detail in the Risk Management section beginning on page 69 of the 2021

Annual Report. The foregoing list of risk factors is not exhaustive. Additional information about these risk factors is provided in the Risk Management section and in the COVID-19 Pandemic section

of the 2021 Annual Report and in the Risk Management section of the Report to Shareholders for the Second Quarter of 2022. Investors and others who rely on the Bank’s forward-looking

statements should carefully consider the above factors as well as the uncertainties they represent and the risk they entail. Except as required by law, the Bank does not undertake to update any

forward-looking statements, whether written or oral, that may be made from time to time, by it or on its behalf. We caution investors that such forward-looking statements are not guarantees of future

performance and that actual events or results may differ materially from these statements due to a number of factors.

Non-GAAP and Other Financial Measures

The quantitative information in this document has been prepared in accordance with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board

(IASB), unless otherwise indicated, and should be read in conjunction with the Bank’s 2021 Annual Report and the Bank’s Report to Shareholders for the Second Quarter of 2022. The Bank uses a

number of financial measures when assessing its results and measuring overall performance. Some of these financial measures are not calculated in accordance with GAAP, which are based on

IFRS. Presenting non-GAAP financial measures helps readers to better understand how management analyzes results, shows the impacts of specified items on the results of the reported periods,

and allows readers to assess results without the specified items if they consider such items not to be reflective of the underlying performance of the Bank’s operations. The Bank cautions readers that

it uses non-GAAP and other financial measures that do not have standardized meanings under GAAP and therefore may not be comparable to similar measures used by other financial institutions.

For additional information relating to the non-GAAP and other financial measures presented in this document and an explanation of their composition, refer to pages 18-21 and 123-126 of the

Management’s Discussion & Analysis in the Bank’s 2021 Annual Report and to pages 4-6 and 45-48 of the Report to Shareholders for the Second Quarter of 2022, which are available at

nbc.ca/investorrelations or at sedar.com. Such explanation is incorporated by reference hereto.

2

Note: National Bank fiscal year ends October 31.

OVERVIEW NATIONAL BANK OF CANADA

YTD 2022 – STRONG START TO THE YEAR

Revenues ($MM; YoY) ▪ Strong start to the year across all segments

Reported: $4,905; +10%

- Adjusted Revenues up 10% YoY

(1)

Adjusted : $5,021; +10%

- Adjusted PTPP up 12% YoY(2)

PTPP(2) ($MM; YoY) - Positive operating leverage

Reported: $2,335; +12%

(1)

Adjusted : $2,451; +12%

▪ Industry-leading ROE of 21.2%

PCL ($MM)

Reported: $1

▪ Solid CET1 ratio of 12.9%(4) while generating strong organic growth

Adjusted: $1

Diluted EPS

▪ PCL level reflecting continued strong portfolio performance

Reported: $5.19

Adjusted: $5.19

ROE(3)

Reported: 21.2%

Adjusted(5): 21.2%

(1) On a taxable equivalent basis, which is a non-GAAP financial measure. See slide 2.

(2) Pre-Tax Pre-Provision earnings (PTPP) refers to Income before provisions for credit losses and income taxes.

(3) Represents a supplementary financial measure. See slide 2.

(4) Common Equity Tier 1 (CET1) capital ratio represents a capital management measure. See slide 2.

(5) Expressed as a percentage of net income and excluding specified items when applicable. 4

TOTAL BANK – YTD 2022 RESULTS

Total Bank Summary Results – YTD 2022

($MM, TEB)

Adjusted Results

(1)

6M 22 6M 21 YoY ▪ Revenues up 10% YoY(1) and PTPP up 12%

Revenues 5,021 4,563 10% YoY(1)(2)

Non-Interest Expenses 2,570 2,379 8%

(2)

- Average loans up 12% YoY

Pre-Tax / Pre-Provisions 2,451 2,184 12%

PCL 1 86 - Average deposits up 10% YoY

Net Income 1,825 1,562 17%

Diluted EPS $5.19 $4.40 18% ▪ Positive operating leverage

Operating Leverage

(3)

2% - Expenses up 8% YoY

(3)

Efficiency Ratio 51.2% 52.1% -90 bps

Return on Equity(3) 21.2% 21.6% ▪ PCL of $1M reflecting continued strong

Reported Results 6M 22 6M 21 YoY

performance

Revenues 4,905 4,462 10%

Non-Interest Expenses 2,570 2,379 8% ▪ Diluted EPS of $5.19

(2)

Pre-Tax / Pre-Provisions 2,335 2,083 12%

PCL 1 86

Net Income 1,825 1,562 17%

Diluted EPS $5.19 $4.40 18%

(3)

Return on Equity 21.2% 21.6%

(3)

Key Metrics 6M 22 6M 21 YoY

Avg Loans & BAs - Total 187,760 167,119 12%

Avg Deposits - Total 253,069 230,684 10%

CET1 Ratio 12.9% 12.2%

(1) On a taxable equivalent basis, which is a non-GAAP financial measure. See slide 2.

(2) Pre-Tax Pre-Provision earnings (PTPP) refers to Income before provisions for credit losses and income taxes.

(3) For supplementary financial measures, non-GAAP ratios and capital management measures, see slide 2. 5

PERSONAL AND COMMERCIAL BANKING

P&C Summary Results – YTD 2022

($MM) ▪ Revenues up 9% YoY

- Strong growth on both sides of the balance sheet

6M 22 6M 21 YoY

YoY with NII up 7%

Revenues 1,920 1,763 9%

- Continued momentum in client activity with other

Personal 1,159 1,099 5%

income up 12% YoY

Commercial 761 664 15%

Non-Interest Expenses 1,057 980 8%

▪ Expense growth mostly driven by salaries and

Pre-Tax / Pre-Provisions 863 783 10%

continued IT investments

PCL 6 28

- Continued investments in digitalization to

Net Income 630 555 14%

enhance online offering

- Retaining and attracting talent, and increased

Key Metrics 6M 22 6M 21 YoY

market coverage investments

Avg Loans & Bas 136,309 121,622 12%

Personal 90,701 83,414 9%

Commercial 45,608 38,208 19%

Avg Deposits 79,503 74,263 7% P&C Net Interest Margin(1)

Personal 37,427 36,253 3%

Commercial 42,076 38,010 11%

NIM (%) 2.07% 2.15% (0.08%) 2.14% 2.09% 2.09%

2.05% 2.05%

Efficiency Ratio (%) 55.1% 55.6% -50 bps

PCL Ratio 0.01% 0.05%

Q2 21 Q3 21 Q4 21 Q1 22 Q2 22

(1) NIM is on Earning Assets. 6

WEALTH MANAGEMENT

Wealth Management Summary Results –YTD 2022

($MM) ▪ Revenues up 11% YoY

6M 22 6M 21 YoY - Strong growth in fee-based revenues mainly

Revenues 1,171 1,059 11% driven by full-service brokerage

Fee-Based 731 622 18% - NII up 12% YoY from volume growth and recent

Transaction & Others 194 217 (11%) interest rate hikes

Net Interest Income 246 220 12%

Non-Interest Expenses 701 621 13%

▪ Expenses up 13% YoY, mostly related to

Pre-Tax / Pre-Provisions 470 438 7%

variable comp.

PCL - -

Net Income 345 322 7% - Shift in revenue growth mix (from higher

transaction to higher fee-based) increases

variable costs

Key Metrics ($B) 6M 22 6M 21 YoY

Avg Loans & BAs 7.0 5.6 25% - Additional FTE to support growth

Avg Deposits 34.4 34.4 - - 6M efficiency ratio

FINANCIAL MARKETS

Financial Markets Summary Results – YTD 2022

($MM) ▪ Strong performance with revenues of $1,294M,

up 9% YoY

6M 22 6M 21 YoY

Revenues 1,294 1,185 9% - Global Markets: Continued momentum in

Structured Products

Global Markets 829 624 33%

- C&IB: Good performance against record 6M 21

C&IB 465 561 (17%)

Non-Interest Expenses 515 460 12%

▪ Expenses up 12% YoY

Pre-Tax / Pre-Provisions 779 725 7%

PCL (32) 41 - Higher compensation

Net Income 596 503 18% - Continued IT investments to support growth

opportunities

Other Metrics 6M 22 6M 21 YoY - 6M efficiency ratio

US SPECIALTY FINANCE & INTERNATIONAL

USSF&I Summary Results – YTD 2022 ABA Bank

($MM)

▪ Continued growth with revenues up 36% YoY,

ABA Bank Summary Results 6M 22 6M 21 YoY loans up 39% and deposits up 28%

Revenues 322 240 34%

Non-Interest Expenses 99 86 15% ▪ Solid credit position; well diversified portfolio

Pre-Tax / Pre-Provisions 223 154 45% - Portfolio 99% secured

PCL 9 13 - Low average LTVs: ~40%

Net Income 173 117 48% - Deferrals: represent 7.4% of portfolio; ~95%

Avg Loans & Receivables 6,772 4,888 39% deferred only principal, and upon expiry ~90%

returned to current or fully repaid

Avg Deposits 8,115 6,331 28%

Efficiency Ratio (%) 30.7% 35.8%

Number of clients ('000) 1,572 1,115 Credigy

Credigy Summary Results 6M 22 6M 21 YoY

▪ Continued strong underlying portfolio

Revenues 246 270 (9%) performance across asset classes

Non-Interest Expenses 68 73 (7%)

Pre-Tax / Pre-Provisions 178 197 (10%) ▪ Well diversified and resilient portfolio; 84% of

PCL 18 4 assets are secured

Net Income 126 148 (15%)

▪ Maintaining our disciplined investment

Avg Assets C$ 7,949 7,429 7%

approach in the current environment

Efficiency Ratio (%) 27.6% 27.0%

9

STRONG CAPITAL POSITION

CET1 Ratio(1)

▪ Strong CET1 ratio of 12.9%(2)

▪ Robust net income generation

▪ NCIB: 2M common shares repurchased in Q2

(2.5M year to date)

▪ Solid organic RWA growth, partly offset by:

- Positive impact from rating migration (17 bps), mostly

from non-retail lending portfolios and derivatives

exposure

Risk-Weighted Assets(1) ▪ Modest impact from model updates:

($MM) - Transition of a retail portfolio from the Standardized to

the AIRB Approach (favourable)

- Market Risk RWA reflects a change in the stressed VaR

period (unfavourable)

▪ Limited impact from unrealized gains and losses

from debt securities accounted for at fair value

through OCI (-3bps)

(1) Represents a capital management measure. See slide 2.

(2) Ratio takes into account the transitional relief measures granted by OSFI in the context of COVID-19 (12.8% excluding ECL transitional relief measures). For 10

additional details regarding relief measures introduced by the regulatory authorities, see page 17 of the Bank’s 2021 Annual Report to Shareholders.STRONG CAPITAL AND LIQUIDITY POSITIONS

Regulatory Capital, TLAC and Liquidity Ratios

($MM)

▪ Our capital levels remain strong

Q2 22 Q1 22 Q4 21

Capital(1)

CET1 $13,833 $13,515 $12,973 ▪ Total capital ratio of 16.2%

Tier 1 $16,481 $16,164 $15,622

Total $17,399 $17,123 $16,643 ▪ Strong liquidity ratios

Capital ratios(1)

CET1 12.9% 12.7% 12.4%

Tier 1 15.3% 15.2% 15.0%

Total 16.2% 16.1% 15.9%

Leverage 4.4% 4.4% 4.4%

(1)(2)

TLAC ratios

TLAC $29,887 $29,462 $27,492

TLAC ratio 27.8% 27.8% 26.3%

TLAC leverage ratio 8.0% 8.0% 7.8%

Liquidity Coverage Ratio(1) 145% 149% 154%

(1)

Net Stable Funding Ratio 114% 117% 117%

(1) Represent capital management measures. See slide 2.

(2) Total Loss Absorbing Capacity (TLAC). Since November 1, 2021, OSFI is requiring D-SIBs to maintain a minimum risk-based TLAC ratio of 24% (including the

domestic stability buffer) of risk-weighted assets and a minimum TLAC leverage ratio of 6.75%. 11CREDIT RISK OVERVIEW

PROVISIONS FOR CREDIT LOSSES

PCL Q2 2022

($MM) POCI Total PCL

Performing

40

173 Impaired ▪ PCL of $3M (1bp), reflecting continued strong

Total (bps)

20 portfolio performance

1 0 1

123 -10 -9 0 PCL on Impaired Loans

-20 ▪ $28M (6bps)

$5

73

$2 -40 ▪ Continued low impaired PCLs in both retail

($43) ($2) $3

and non-retail portfolios

$65 ($41) -60

$8 $2

23

$34 $28

PCL on Performing Loans

$19 $24 -80

▪ Release of $27M (-6bps)

($41) ($34) ($27) -100

-27 ($62) ($58) ▪ Retail: -$4M, reflects overall continued strong

-120 performance

($36)

($2)

($MM) -77 -140 ▪ Non-retail: -$19M, reflecting positive migration

Q2 21 Q3 21 Q4 21 Q1 22 Q2 22

and scenarios updates

▪ USSF&I: -$4M, driven by credit migration and

Personal 17 15 15 17 15 portfolio growth

Commercial 2 6 (1) 2 3

Revised FY 2022 Target Range

Wealth Management 2 - 1 0 (1)

Financial Market 39 11 2 (1) 0 ▪ Impaired PCLs : below 15 bps

USSF&I 5 2 2 6 11

PCL on impaired 65 34 19 24 28

(1)

POCI 2 (36) (2) 8 2

PCL on performing (62) (41) (58) (34) (27)

Total PCL 5 (43) (41) (2) 3

13

(1) Purchased or Originated Credit ImpairedPRUDENT PROVISIONING IN UNCERTAIN ECONOMIC ENVIRONMENT

Strong Performing ACL Coverage Total Allowances Cover 6.2X NCOs

Performing ACL / LTM PCL on Impaired Loans Total ACL / LTM Net Charge-Offs

7.8x 7.9x

6.0x 6.4x 6.6x

6.1x 6.2x

5.9x

4.8x 5.4x

4.7x

3.8x

3.3x 4.1x

2.8x 2.8x 2.8x 3.0x

1.8x 2.6x

Q1 20 Q2 20 Q3 20 Q4 20 Q1 21 Q2 21 Q3 21 Q4 21 Q1 22 Q2 22 Q1 20 Q2 20 Q3 20 Q4 20 Q1 21 Q2 21 Q3 21 Q4 21 Q1 22 Q2 22

Total Bank Total Bank

Performing ACL movement Strong Total ACL Coverage

Total ACL / Total Loans (excl. POCI and FVTPL)

Q2 22 Q1 22 Q4 21 Q1 20

Mortgages 0.21% 0.21% 0.20% 0.15%

Credit Cards 6.97% 7.75% 7.35% 7.14%

Total Retail 0.48% 0.49% 0.49% 0.53%

Total Non-Retail 0.79% 0.86% 1.04% 0.58%

Total Bank 0.61% 0.63% 0.72% 0.56%

14

Note: Performing ACL includes allowances on drawn ($678M), undrawn ($115M) and other assets ($28M)GROSS IMPAIRED LOANS AND FORMATIONS

Gross Impaired Loans(1) (GIL)

($MM)

50

▪ Gross impaired loans of 31bps ($611M),

42 a decline of 1bp QoQ and 11bps YoY

$1,000M 39

36 40

32 31

$800M $731 $699

$662

30

▪ Net formations of $45 million

$608 $611

20

$600M

- Lower formations in Personal

$470 $450 10

$406 $339 $314

$400M - Net repayments in Commercial

0

$200M

$188 $179 - Increase in ABA’s new formations

$208 $193 $192 -10

$118

following the end of moratoriums

$0M $53 $56 $64 $81 -20

Q2 21 Q3 21 Q4 21 Q1 22 Q2 22

USSF&I Retail Non-Retail GIL ratio (bps)

Net Formations(2) by Business Segment

($MM)

Q2 21 Q3 21 Q4 21 Q1 22 Q2 22

Personal (8) 10 14 20 12

Commercial (37) 7 (2) 10 (10)

Financial Markets 54 (17) (31) (10) (1)

Wealth Management 6 − 10 − 2

Credigy 6 4 2 5 5

ABA Bank 1 3 8 15 37

Total GIL Net Formations 22 7 1 40 45

(1) Under IFRS 9, impaired loans are all loans classified in stage 3 of the expected credit loss model. Impaired loans presented in

this table do not take into account purchased or originated credit-impaired loans.

(2) Formations include new accounts, disbursements, principal repayments, and exchange rate fluctuation; net of write-offs. 15LIQUIDITY AND FUNDING OVERVIEW

FUNDING STRATEGY

The main objective of the funding strategy is to support the Bank's organic growth while also enabling it

to survive potentially severe and prolonged crises and to meet its regulatory obligations and financial

targets.

The funding framework consists of 3 pillars:

1. Pursue a diversified deposit strategy to fund core banking activities through stable deposits

coming from the networks of each of the Bank’s major business segments;

2. Maintain a sound liquidity risk management through centralized expertise and management of

liquidity metrics within predefined risk appetite;

3. Maintain active access to various markets to ensure diversification of institutional funding in

terms of source, geographic location, currency, instrument and maturity, whether secured or

unsecured.

The funding strategy is implemented in accordance with the overall objectives of strengthening the

Bank's franchise among market participants and consolidating its excellent reputation.

The deposit strategy remains a priority for the Bank, which continues to prefer deposits to institutional

funding.

17DIVERSIFIED DEPOSIT STRATEGY

Pursue a diversified deposit strategy to fund core banking activities through stable deposits coming

from the networks of each of the Bank’s major business segments

NBC TOTAL DEPOSITS

250

200

Total Deposits:

1Y CAGR = 6%

150

100

Personal Deposits:

50 1Y CAGR = 5%

-

Q4 2018 Q4 2019 Q4 2020 Q4 2021 Q2 2022

Personal Business and Government

▪ Resulting from the steady execution of the Bank’s successful deposit strategy, Personal Deposits

increased to $72B, while Total Deposits stabilized to $197B as of Q2 2022.

18SOUND LIQUIDITY RISK MANAGEMENT

Maintain a sound liquidity risk management through centralized expertise and management of liquidity metrics within

predefined risk appetite, with 4 main principles: Efficient Risk & Reward Balance through a Risk Appetite Framework,

Decision-making processes based on clear and complete understanding of liquidity risk and liquidity risk contributors,

support to NBC’s credit ratings and liquidity position maintained above regulatory minimum requirements.

Unsecured Wholesale Funding Liquidity Coverage Ratio and Net Stable Funding Ratio

vs. Unencumbered Liquid Assets

($B) 160%

100

150%

80 140%

60 130%

120%

40

110%

20 100%

- 90%

Q4 2018 Q4 2019 Q4 2020 Q4 2021 Q2 2022

80%

NBC - Unsecured WF under 1Y NBC -Unsecured WF over 1y Q1 21 Q2 21 Q3 21 Q4 21 Q1 22 Q2 22

NBC - ULA Surplus over Unsecured WF LCR NSFR

Liquidity Approach to Wholesale Funding Regulatory Liquidity

▪ High-quality liquidity portfolio more than offsets ▪ Ongoing well-positioned LCR

reliance on Unsecured Wholesale Funding ▪ NSFR stood at 114% at end of Q2 2022

▪ Continued disciplined approach to Unsecured

Wholesale Funding

Additional information on the Bank’s liquidity position can be found in the Q22022 Report to Shareholders as well as in pp. 94-101 of the

2021 Annual Report.

19MATURITY PROFILE

Maintain active access to various markets to ensure diversification of institutional funding in terms of

source, geographic location, currency, instrument and maturity, whether secured or unsecured.

Term Funding (C$ millions) Term Funding

12,000

10,000 Covered

bonds

8,000 20% Senior

Debt

6,000

33%

4,000

2,000

-

Mortgage

< 1YR 2YR 3YR 4YR 5YR > 5 years

Securitization 47%

Senior Debt Mortgage Securitization Covered bonds

Canada (selected issuances)

Currency Principal (in millions) Tenor Product Coupon Maturity

CAD 1,000 5Y Senior Unsecured (BID) 2.237% 26-Nov

CAD 1,000 5Y Senior Unsecured (BID) 2.545% 24-Jul

CAD 750 6NC5 Senior Unsecured (BID) 1.573% 26-Aug

CAD 750 5Y Sustainable Senior Unsecured (BID) 1.534% 26-Jun

Foreign (selected issuances)

Currency Principal (in millions) Tenor Product Coupon Maturity

GBP 750 4Y Covered Bonds SONIA + 100 bps 26-May

USD 1,250 3Y Covered Bonds 2.900% 27-Apr

EUR 1,000 5Y Covered Bonds 0.125% 27-Jan

USD 750 4NC3 Sustainable Senior Unsecured (BID) 0.550% 24-Nov

USD 400 2NC1 Senior Unsecured (BID) SOFR + 30 bps 23-May

USD 500 3Y Senior Unsecured (BID) 0.750% 24-Aug

20DIVERSIFIED FUNDING PLATFORMS

Maintain active access to various markets to ensure diversification of institutional funding in terms of

source, geographic location, currency, instrument and maturity, whether secured or unsecured

Unsecured Wholesale Funding Platforms Securitization and Covered Bond Programs

▪ Benchmark C$ Senior Unsecured ▪ Canadian Mortgage Bonds

▪ US$ Senior Unsecured MTN programs ▪ Canadian Credit Card Trust II

(Structured Notes and Senior Bail-in) ▪ Legislative Global Covered Bond Program

▪ Euro MTN program (EMTN)

▪ US$ Commercial Paper programs and

Yankee CDs

▪ C$ MTN shelf

In addition to benchmark deals, we also have capacity to:

✓ act on Reverse enquiries

✓ execute Private Placements and Club Deals

✓ tailor Sustainability Bonds (ESG) and Structured Notes (incl. Formosa, Step-ups, Callables, CMS)

21TLAC RATIOS(1)

All Canadian D-SIBs are now required to maintain a TLAC risk-weighted ratio of at least 21.5%. In addition, all D-SIBs

are expected to hold buffers above the minimum TLAC Ratio, including the Domestic Stability Buffer (“DSB”, adjusted by

OSFI on June 17, 2021, to 2.50% of total RWA effective Oct. 31, 2021). Inclusive of the DSB as currently set, the D-SIBs’

supervisory target risk-based TLAC Ratio stand at 24.0% (entered in effect on Nov. 1, 2021).

All D-SIBs are also required to maintain a TLAC leverage ratio of at least 6.75%.

TLAC RWA Ratio as of Q2 2022

30.0%

27.5%

11.6%

25.0%

22.5%

▪ Q2-22 NBC TLAC RWA Ratio = 27.8%

Supervisory target risk-based TLAC, 24.00%

20.0%

2.5% 0.9%

▪ Q2-22 NBC TLAC Leverage Ratio = 8%

17.5%

15.0% 12.9% ▪ NBC exceeds both TLAC regulatory

12.5% requirements from the outset

10.0%

7.5% ▪ NBC will manage its funding activities to

5.0% bring its TLAC ratios to a desired level

2.5%

0.0%

CET1 Tier 1 Capital Tier 2 Capital Existing Bail-in

Unsecured

(1) Represents capital management measures. See slide 2. 22Environment, Social and Governance (ESG) Highlights

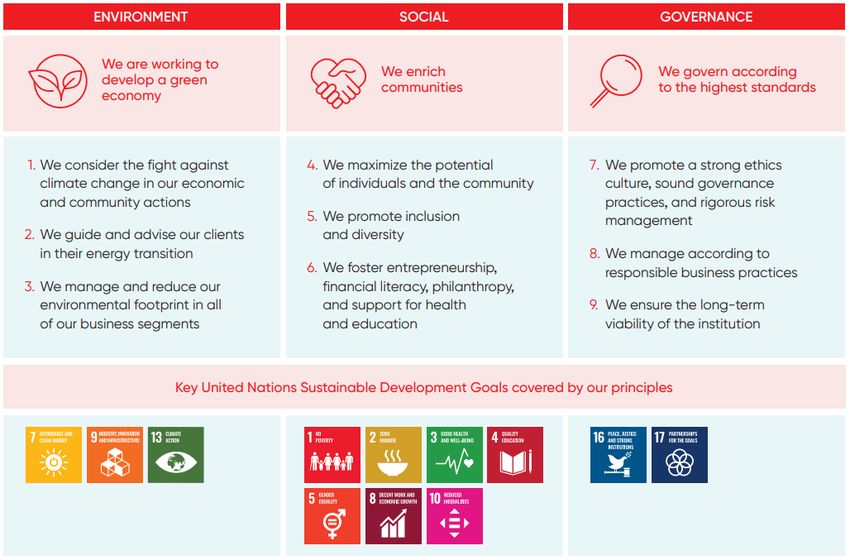

NBC ESG HIGHLIGHTS

Supporting sustainable development is an intrinsic part of our mission. Environmental, social and governance (ESG)

considerations play a key role in our business and operational decisions. At National Bank, we want to have a positive

impact in people’s lives. The nine principles approved by our Board of Directors demonstrate our commitment to building

a sustainable future while representing the best interests of stakeholders.

24NBC ESG HIGHLIGHTS

• Board-level: ESG responsibilities integrated in the mandates of the Audit Committee, Risk Management Committee,

Human Resources Committee and Conduct Review and Corporate Governance Committee

Oversight • Executive-level: ESG committee responsible for corporate strategy regarding ESG matters includes key functional

representatives (Risk, Legal, Public Affairs, Compliance, etc.) and is chaired by CFO

• Report on Environmental, Social and Governance Advances summarizing NBC’s achievements

• SASB Report

Disclosure

• Task Force on Climate-related Disclosures (TCFD) Report

• Annual report related to the CDP Climate Change questionnaire since 2008

• The Bank has developed one of the first Canadian reference frameworks for issuing sustainable bonds.

Sustainable • As at December 31, 2021, the issues carried out since 2019 have generated more than $3.1 billion, which was used by

Finance the Bank to finance numerous projects in the field of sustainable development.

Partnerships and Coalitions

25NBC Environment Highlights

Environment Social Governance

> Set path to achieve net-zero greenhouse gas (GHG) emissions for our operating and financing activities by 2050, with interim targets.

o Established an interim target for reducing GHG emissions from our activities: -25% by the end of 2025*.

o Established an interim reduction target of 31% for financed emissions for the Canadian oil and gas producers' sub-sector by

2030*. (Since 2015, the Bank’s gross loans to O&G producers and services have decreased by 54%.)

o Joined the Partnership for Carbon Accounting Financials (PCAF)

o Joined the United Nations Net-Zero Banking Alliance (NZBA) which furthers banks' efforts to help address climate change by

aligning financing activities with net-zero emissions by 2050.

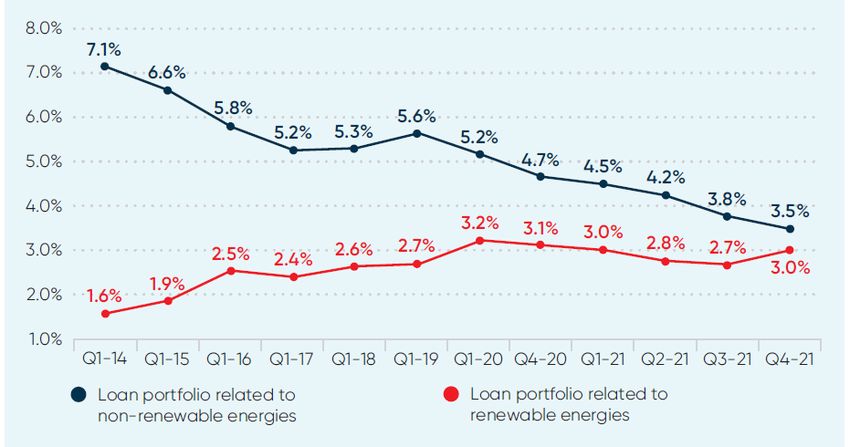

> Grow the portfolio of loans related to renewable energy at a faster pace than the portfolio of loans related to non-renewable energy.

> Committed not to finance drilling in the arctic; no new thermal coal mining and processing activities.

> Maintain carbon neutrality by offsetting our remaining annual emissions through the purchase of carbon credits, Verified Carbon

Units and carbon allowances.

* Compared to our 2019 baseline.

Operations GHG Emission (Scopes 1, 2 and 3) Financing Activities

The Bank’s actions and use of advanced inventory procedures have helped As at October 31, 2021, non-renewable energy accounted for only 3.5% of

reduce carbon emissions despite the growth in its activities. GHG emissions by the the loan portfolio’s total exposure, compared to 5.6% as at January 31,

Bank during the 2021 fiscal year represent a 30% drop in overall GHG emissions 2019. While the renewable energy proportion went from 3.0% to 3.1%

since 2019. during the same period.

Please also refer to our TCFD Report: https://www.nbc.ca/content/dam/bnc/a-propos-de-nous/responsabilite-sociale/pdf/nbc-2021-tcfd-report.pdf 26NBC Social Highlights

Environment Social Governance

Employees

> People is the key to our success. That’s why the Bank maintains an ongoing dialogue with its employees.

> Culture is a key differentiator with a focus on entrepreneurship, collaboration, agility and accountability.

> Promoting Employee Well-Being as always been a priority at the Bank. We offer flexible and innovative benefits such as

a telemedicine service, an Employee and Family Assistance Program and a childcare centre.

Clients

> Underbanked, Unbanked and Underserved Clients: The ABA acquisition has opened the door to many people who

previously had no access to banking in Cambodia. In Canada, we set up measures to give a portion of our clientele

easier access to financial services and better meet their needs.

> Financial Literacy: We make a vast range of resources and tools available to clients to allow them to carefully plan for

their financial needs, notably with the support of the Canadian Foundation for Economic Education.

> Businesses: We support a rich Entrepreneurial Ecosystem through a dozen incubators & accelerators.

Community

> The Bank supports many organizations in the areas of education, entrepreneurship, health, community outreach, arts

and culture, diversity and inclusion and the environment. Organizations are chosen according to strict guidelines that

ensure maximum fairness and community impact.

> We return tens of millions of dollars back to the community and over $15 million in donations, yearly.

> #1 Canadian bank in funding affordable housing in our home province.

> Mobilized $200M of capital for National Bank SME growth fund.

Promoting inclusion and diversity

> Publication of the 2021 Inclusion and Diversity Booklet.

> For the four year in a row, the Bank was selected for the Bloomberg Gender-Equality Index.

> The Bank participated in a number of initiatives intended to actively support women, cultural communities, the LGBTQ+

communities, persons with disabilities and Indigenous peoples.

> Partnership with the Black Professionals in Tech Network (BPTN), an organization that helps its partners attract and

recruit Black talent through pipeline building and internal culture development.

27NBC Governance Highlights

Environment Social Governance

> Publication of the ESG Report, Inclusion and Diversity Booklet and TCFD Report.

> The mandates of all the committees of the Board of Directors include ESG-related responsibilities.

> Executive variable compensation tied to achievement of our core ESG priorities.

> Succession planning for directors takes into account the Board’s diversity policy (gender, age, designated groups,

sexual orientation, ethno-cultural groups and geographic origins).

> Succession planning for all senior management positions, including the President and Chief Executive Officer.Long-

dated commitment to corporate social responsibility, based on the balance of interests of its stakeholders

(Click on images below to access full report)

28Mission of organizations we support

United Nations Environment Programme – Finance Initiative (UNEP FI) is a partnership

between United Nations Environment and the global financial sector created in the wake of the

1992 Earth Summit with a mission to promote sustainable finance. More than 250 financial

institutions, including banks, insurers, and investors, work with UN Environment to understand

today’s environmental, social and governance challenges, why they matter to finance, and how

to actively participate in addressing them.

NET-ZERO BANKING ALLIANCE – The industry-led, UN-convened Net-Zero Banking Alliance

brings together banks worldwide representing about 40% of global banking assets, which are

committed to aligning their lending and investment portfolios with net-zero emissions by 2050.

Combining near-term action with accountability, this ambitious commitment sees signatory

banks setting an intermediate target for 2030 or sooner, using robust, science-based guidelines.

The Principles provide the banking industry with a single framework that embeds sustainability at

the strategic, portfolio and transactional levels and across all business areas. The Principles

align banks with society’s goals as expressed in the Sustainable Development Goals and the

Paris Climate Agreement.

The PRI will work to achieve this sustainable global financial system by encouraging adoption of

the Principles and collaboration on their implementation; by fostering good governance, integrity

and accountability; and by addressing obstacles to a sustainable financial system that lie within

market practices, structures and regulation.

United Nations High Commissioner for Human Rights (OHCHR) launched UN Free & Equal –

an unprecedented global UN public information campaign aimed at promoting equal rights and

fair treatment of lesbian, gay, bisexual and transgender (LGBT) people.

29Mission of organizations we support

The FSB Task Force on Climate-related Financial Disclosures (TCFD) will develop voluntary,

consistent climate-related financial risk disclosures for use by companies in providing information

to investors, lenders, insurers, and other stakeholders. The Task Force will consider the physical,

liability and transition risks associated with climate change and what constitutes effective financial

disclosures across industries. The work and recommendations of the Task Force will help

companies understand what financial markets want from disclosure in order to measure and

respond to climate change risks, and encourage firms to align their disclosures with investors’

needs

Carbon Disclosure Project want to see a thriving economy that works for people and planet in the

long term. To do this we focus investors, companies and cities on taking urgent action to build a

truly sustainable economy by measuring and understanding their environmental impact. To

achieve this, CDP, formerly the Carbon Disclosure Project, runs the global disclosure system that

enables companies, cities, states and regions to measure and manage their environmental

impacts.

The Sustainable Development Goals are the blueprint to achieve a better and more sustainable

future for all. They address the global challenges we face, including those related to poverty,

inequality, climate, environmental degradation, prosperity, and peace and justice.

Responsible investment (RI) refers to the incorporation of environmental, social and governance

factors (ESG) into the selection and management of investments.

PCAF is a global partnership of financial institutions that work together to develop and implement a

harmonized approach to assess and disclose the greenhouse gas (GHG) emissions associated

with their loans and investments.

30Sustainability Bond Framework

NBC SUSTAINABILITY BOND FRAMEWORK

November 2020, NBC revised its Sustainability Bond Framework and obtained Second Party Opinion from VigeoEiris:

https://www.nbc.ca/content/dam/bnc/a-propos-de-nous/relations-investisseurs/fonds-propres-et-dette/2020/nbc-sustainability-bond-framework-2020.pdf

https://www.nbc.ca/content/dam/bnc/a-propos-de-nous/relations-investisseurs/fonds-propres-et-dette/2020/nbc-sustainability-bond-second-opinion-2020.pdf

May 2022, NBC published its 2021 Sustainability Bond Report:

https://www.nbc.ca/content/dam/bnc/a-propos-de-nous/relations-investisseurs/fonds-propres-et-dette/2022/na-sustainability-bond-report-2021.pdf

In line with the ICMA Green Bond Principles and Social Bond Principles, NBC’s Sustainability Bonds will be allocated to financing of

projects and organizations that credibly contribute to the environmental objectives or seek to achieve positive socioeconomic

outcomes for target populations. Therefore, these are likely to contribute to United Nations’ Sustainable Development Goals (listed

below), by having a focus on:

Renewable Energy / Sustainable Buildings / Low-Carbon Transportation / Affordable Housing /

Access to Basic and Essential Services / Loans to Small and Medium-sized enterprises (SMEs)*

NBC completed various sustainability bond issuances, including the first international issuance of USD Sustainability Bonds by a

North American bank, as well as Sustainable Structured Bonds issued via tailored private placements (selected issuances):

NACN USD 750,000,000 3Y 2.15% Senior Notes Due October 2022

NACN EUR 40,000,000 12y CMS1010 Senior Notes Due February 2031

NACN EUR 40,000,000 15y Steepener Senior Notes Due May 2034

NACN USD 750,000,000 4NC3 0.550% Senior Notes Due November 2024

NACN CAD 750,000,000 5Y 1.534% Senior Notes Due June 2026

NACN AUD 12,000,000 15Y Callable Zero-Coupon Sustainable Notes Due October 2036

NACN USD 100,000,000 5Y Callable Sustainable Notes Due November 2026

* The “Loans to Small and Medium-sized enterprises (SMEs)” category was added to the Bank’s Framework in 2020. 32NBC SUSTAINABILITY BOND FRAMEWORK

For the purpose of issuing Sustainability Bonds, NBC has developed its framework, which addresses the four core

components of the ICMA Sustainability Bond Guidelines and its recommendations on the use of external reviews

and impact reporting:

1. Use of proceeds

2. Project selection and evaluation process

3. Management of proceeds

4. Reporting

As per the ICMA Sustainability Bond Guidelines: “Sustainability Bonds are bonds where the proceeds will be

exclusively applied to finance or re-finance a combination of both Green and Social Projects.

Sustainability Bonds are aligned with the four core components of both the GBP [Green Bond Principles or “GBP”] and

the SBP [Social Bond Principles or “SBP”] with the former being especially relevant to underlying Green Projects and the

latter to underlying Social Projects.

It is understood that certain Social Projects may also have environmental co-benefits, and that certain Green Projects

may have social co-benefits. The classification of a use of proceeds bond as a Green Bond, Social Bond, or

Sustainability Bond should be determined by the issuer based on its primary objectives for the underlying projects.”

https://www.icmagroup.org/green-social-and-sustainability-bonds/sustainability-bond-guidelines-sbg/

33NBC SUSTAINABILITY BOND FRAMEWORK

Project selection Management of

Use of proceeds

and evaluation

Social

proceeds

Reporting

Governance

Eligible Categories Eligibility Criteria

Eligible types of renewable energy:

o Wind, Solar, Geothermal with direct emissions < 100gCO2/kWh, Tidal

o Hydropower: small scale hydro (NBC SUSTAINABILITY BOND FRAMEWORK

Project selection Management of

Use of proceeds

and evaluation

Social Reporting

Governance

proceeds

Project Selection and Evaluation Process Management of Proceeds

✓ NBC’s business unit officers are responsible for ✓ NBC has established a Sustainability Bond Register, for

identifying and assessing potential eligible projects and the purpose of recording the Eligible Businesses and Projects

businesses and allocation of the proceeds from Sustainability Bonds to

Eligible Businesses and Projects

✓ Eligible projects / businesses selected by the business

lines are reviewed by ESG program officers ✓ The Sustainability Bond Register contains relevant

information to identify each Sustainability Bond and the

✓ The ESG program officers screen existing and future Eligible Businesses and Projects relating to it

projects and programs that align with NBC’s

sustainable development objectives ✓ The proceeds of the Sustainability Bonds issued by NBC are

being deposited in the general funding accounts of NBC. An

✓ NBC has established a Sustainability Bond amount equal to the proceeds are to be earmarked for

Committee responsible for the ultimate review and allocation in the Sustainability Bond Register in accordance

selection of the loans and investments that will qualify with its Sustainability Bond Framework

as Eligible Businesses and Projects, to which the net

proceeds of a Sustainability Bond issuance will be ✓ A dedicated team maintains and updates the Sustainability

allocated Bond Register

✓ It is NBC’s intention to maintain an aggregate amount of

assets relating to Eligible Businesses and Projects at least

equal to the aggregate proceeds of all NBC Sustainability

Bonds that are concurrently outstanding

✓ The Bank aims to fully allocate proceeds within a period of

18 months

35NBC SUSTAINABILITY BOND FRAMEWORK

Project selection Management of

Use of proceeds Social

proceeds

Reporting

Governance

and evaluation

NBC has published a Sustainability Bond report on its website:

✓ Within 1 year of the issuance of the Sustainability Bonds; and

✓ Will update its Sustainability Bond report annually, until complete allocation, and thereafter, as necessary in case

of new developments

The NBC Sustainability Bond Report will contain (at least) the following:

✓ Confirmation that the use of proceeds of the Sustainability Bond complies with the NBC Sustainability Bond

Framework

✓ The amount of proceeds allocated to each Eligible Category

✓ For each Eligible Category, one or more examples of Eligible Businesses and Projects financed, in whole or in

part, by the proceeds obtained from the Sustainability Bond, including their general details (brief description,

location, stage — construction or operation)

✓ The balance of unallocated proceeds

✓ Impact reporting items, as described in the potential indicators table detailed in the Framework

✓ NBC’s third Sustainability Bond Report was published in May 2022:

https://www.nbc.ca/content/dam/bnc/a-propos-de-nous/relations-investisseurs/fonds-propres-et-dette/2022/na-sustainability-bond-report-2021.pdf

36NBC SUSTAINABILITY BOND FRAMEWORK

On November 2020, Vigeo Eiris issued a Second Party Opinion on the Bank’s Framework (excerpts only):

Framework Link: https://www.nbc.ca/content/dam/bnc/a-propos-de-nous/relations-investisseurs/fonds-propres-et-dette/2020/nbc-sustainability-bond-framework-2020.pdf

SPO Link: https://www.nbc.ca/content/dam/bnc/a-propos-de-nous/relations-investisseurs/fonds-propres-et-dette/2020/nbc-sustainability-bond-second-opinion-2020.pdf

37APPENDIX

APPENDIX 1 │ TOTAL LOAN PORTFOLIO OVERVIEW

Loan Distribution by Borrower Category

($B)

▪ Secured lending accounts for 95%

As at of Retail loans

April 30, 2022 % of Total

Retail

▪ Indirect auto loans represent 1.7% of total

Secured - Mortgage & HELOC 91.9 47%

loans ($3.3B)

Secured - Other (1) 11.9 6%

Unsecured 3.9 2%

▪ Limited exposure to unsecured retail and

Credit Cards 2.0 1%

cards (3% of total loans)

Total Retail 109.7 56%

▪ Non-Retail portfolio is well-diversified

Non-Retail

Real Estate and Construction RE 20.0 10%

Agriculture 7.7 4%

Retail & Wholesale trade 6.3 3%

Other Services 6.2 3%

Manufacturing 6.1 3%

Utilities 6.0 3%

Finance and Insurance 5.9 3%

Oil & Gas and Pipeline 3.9 2%

Oil & Gas 1.4 1%

Pipeline & Other 2.4 1%

(2)

Other 22.8 13%

Total Non-Retail 84.9 44%

Purchased or Originated Credit-Impaired 0.3 0%

Total Gross Loans and Acceptances 194.9 100%

(1) Includes indirect lending and other lending secured by assets other than real estate.

(2) Includes Mining, Transportation, Professional Services, Construction Non-Real Estate, Communication, Government and Education & Health Care. 39APPENDIX 2 │ REGIONAL DISTRIBUTION OF CANADIAN LOANS

Prudent Positioning

(As at April 30, 2022)

Within the Canadian loan portfolio:

Maritimes(2) ▪ Limited exposure to unsecured consumer

Oil and loans (3.0%)

Quebec Ontario Regions(1) BC/MB Territories Total

Retail ▪ Modest exposure to unsecured consumer

Secured

Mortgage & HELOC

26.7% 14.0% 4.2% 3.3% 1.0% 49.2% loans outside Quebec (0.6%)

Secured

Other

2.5% 1.4% 0.5% 0.6% 0.3% 5.3% ▪ RESL exposure predominantly in Quebec

Unsecured

2.4% 0.3% 0.1% 0.1% 0.1% 3.0%

and Credit Cards

Total Retail 31.6% 15.7% 4.8% 4.0% 1.4% 57.5%

Non-Retail

Commercial 19.1% 4.9% 1.7% 2.1% 0.7% 28.5%

Corporate Banking

3.8% 6.0% 2.5% 1.3% 0.4% 14.0%

and Other(3)

Total Non-Retail 22.9% 10.9% 4.2% 3.4% 1.1% 42.5%

Total 54.5% 26.6% 9.0% 7.4% 2.5% 100.0%

(1) Oil regions include Alberta, Saskatchewan and Newfoundland.

(2) Maritimes include New Brunswick, Nova Scotia and P.E.I.

(3) Includes Corporate, Other FM and Government portfolios. 40APPENDIX 3 │ RETAIL MORTGAGE AND HELOC PORTFOLIO

Canadian Distribution by Province

(As at April 30, 2022) ▪ Insured mortgages account for 30% of the

total RESL portfolio

54%

▪ Distribution across product and geography

remained stable

▪ Uninsured mortgages and HELOC in GTA and

74% Uninsured & HELOC GVA represent 12% and 3% of the total

28% Insured portfolio and have an average LTV(1) of 45%

for both segments

74% ▪ Uninsured mortgages and HELOC for condos

represents 9% of the total portfolio and have

7%

6% an average LTV(1) of 55%

26% 32% 5%

26% 69% 46%

68% 31% 54%

QC ON AB BC Other Provinces Canadian Distribution by Mortgage Type

52% 46% 66% 45% 50%

Average LTV - Uninsured and HELOC(1)

HELOC

Canadian Uninsured and HELOC Portfolio $28.1B(2)

Insured

$26.1B

/ 33% / 30%

$86.2B

HELOC Uninsured

Average LTV(1) 48% 53%

Average Credit Bureau Score 792 782

90+ Days Past Due (bps) 5 12 Uninsured

$32.0B / 37%

(1) LTV are based on authorized limit for HELOCs and outstanding amount for Uninsured Mortgages.

They are updated using Teranet-National Bank sub-indices by area and property type

(2) Of which $19.1B are amortizing HELOC 41APPENDIX 4 │ COMMERCIAL REAL ESTATE PORTFOLIO

(As at April 30, 2022)

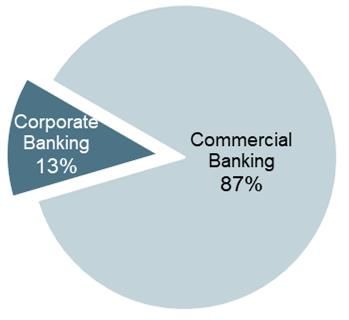

Total CRE Portfolio Commercial Banking share Total CRE Portfolio of $15.8B

$15.8B (8.1% of total loans) $13.7B (7.0% of total loans)

▪ Corporate Banking accounts for 13% of portfolio,

primarily public REITs, well diversified across

sectors

▪ Commercial Banking accounts for 87% of portfolio

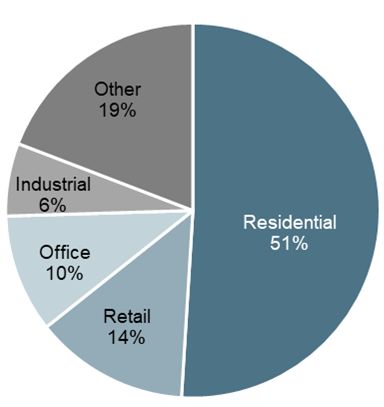

Drill down on Commercial Banking CRE:

Residential (3.6% of total loans – up $0.5B)

▪ Insured loans accounted for all of the growth QoQ

▪ Insured portfolio now represents 55%

▪ LTV on uninsured ~60%

Retail (0.9% of total loans – stable)

Geographic Distribution (Commercial Banking CRE) ▪ Share of portfolio reduced by 8% YoY

▪ Portfolio LTV ~56%

▪ ~50% of leases with essential services tenants

Office (0.7% of total loans – stable)

▪ Share of portfolio reduced by 2% YoY

64%

▪ Portfolio LTV ~59%

▪ Long term leases (over 6 years)

15%

7% 8% 6%

42

QC ON BC Other Provinces ABAPPENDIX 5 │ OIL & GAS AND PIPELINES SECTOR

O&G Producers and Services Exposure

Gross Loans in $MM and % of Total Loans

▪ O&G producers and services exposure

significantly reduced

$3,956

- 64% reduction in outstanding loans: down

from $4B in Q1/15 to $1.4B in Q2/22

(stable QoQ)

- Reduction as a % of total loans: down from

3.7% in Q1/15 to 0.7% in Q2/22

3.7%

$1,438 - Canadian focused strategy, minimal direct

US exposure

0.7%

▪ Overall O&G and Pipeline portfolio

refocused from mid-cap to large cap

Q1 15 Q2 22

- Producers share declined from 82% in

O&G and Pipeline sector Q1/15 to 32% in Q2/22

Total Gross Loans of $3.9B as at April 30, 2022 - 62% of the portfolio is Investment Grade

4% 7% (as of Q2/22)

5% IG: 100%

5% IG: 13%

9%

▪ Very modest indirect exposure to

IG: 76% unsecured retail loans in the oil regions

56%

(~0.1% of total loans)

82%

IG: 35%

32%

Q1 15 Q2 22

Producers Midstream Services Refinery & Integrated

43APPENDIX 6 │ NBC CREDIT RATINGS

Long-Term Non

Covered Counterparty

Short-term Bail-inable Senior Debt(2) Outlook

Credit Rating Bonds risk(3)

Senior Debt(1)

Agency

S&P A-1 A BBB+ Stable ---- ----

Moody’s P-1 Aa3 A3 Stable Aaa Aa3

DBRS R-1 (high) AA AA (low) Stable AAA ----

Fitch F1+ AA- A+ Stable AAA AA-

▪ Strong short-term ratings

▪ Solid Deposit / Non Bail-inable Senior Debt ratings

▪ “A” Long-Term Senior Bail-in Debt ratings, Indices composite A* and A-**

(1) Includes Senior Debt issued prior to Sept. 23, 2018 and Senior Debt issued on or after Sept. 23, 2018 which is excluded from the Bank Recapitalization (Bail-in) Regime.

(2) Subject to conversion under the Bank Recapitalization (Bail-in) Regime.

(3) Moody's terminology is Counterparty Risk Rating (CRR) while Fitch's terminology is Derivative Counterparty Rating (DCR).

* FTSE Russell (as of Year End 2021)

** Bloomberg Index (as of Year End 2021)

44APPENDIX 7 │ LEGISLATIVE COVERED BOND PROGRAMME

Programme size ▪ CAD$ 20,000,000,000

Outstanding benchmark covered bonds ▪ €750M 0.0% 09/23; €750M 0.750% 03/25; €750M 0.250% 07/23;

€750M 0.375% 01/24; $US1B 2.05% 06/22; €500M 0.01% 03/28;

€750M 0.01% 09/26; €1B 0.125% 01/27; $US1.25B 2.900% 04/27;

and £750M SONIA+100 05/26.

Ratings ▪ Aaa / AAA / AAA by Moody’s, Fitch and DBRS

Asset percentage minimum and maximum ▪ 80-93%

Currency ▪ Any

Guarantor ▪ NBC Covered Bond (Legislative) Guarantor L.P.

Listing ▪ London, U.K.

Law ▪ Canadian Legislative Framework (National Housing Act)

LTV ▪ 80% Maximum

Collateral pool eligibility ▪ Canadian uninsured residential mortgage loans

Tenor ▪ Any Allowed

Coupon ▪ Fixed / Float

Bullet Type ▪ Soft Bullet

45APPENDIX 8 │ OTHER

Other Segment Summary Results – YTD 2022

($MM)

▪ Lower non-interest expenses YoY:

(1)

Adjusted Results 6M 22 6M 21 - Lower variable compensation

Revenues 66 45

- Lower pension plan expense

Non-Interest Expenses 129 158

Pre-Tax / Pre-Provisions(2) (63) (113)

PCL - -

Pre-Tax Income (63) (113)

Net Income (46) (83)

Reported Results 6M 22 6M 21

Revenues (50) (56)

Non-Interest Expenses 129 158

(2)

Pre-Tax / Pre-Provisions (179) (214)

PCL - -

Pre-Tax Income (179) (214)

Net Income (46) (83)

(1) On a taxable equivalent basis, which is a non-GAAP measure. See slides 2 and 47.

(2) Pre-Tax Pre-Provision earnings (PTPP) refers to Income before provisions for credit losses and income taxes. 46APPENDIX 9 │ RECONCILIATION OF NON-GAAP FINANCIAL MEASURES

($MM, except EPS)

Q2 22 Q1 22

Non- Non- Non- Non-

Total Net Diluted Total Net Diluted

Interest PTPP(2) controlling Interest PTPP(2) controlling

Revenues Income EPS Revenues Income EPS

Expenses interest Expenses interest

Adjusted Results(1) 2,491 1,293 1,198 893 (1) 2.55 $ 2,530 1,277 1,255 932 - 2.65 $

Taxable equivalent (52) - (52) - - - (64) - (64) - - -

Total impact (52) - (52) - - - (64) - (64) - - -

Reported Results 2,439 1,293 1,146 893 (1) 2.55 $ 2,466 1,277 1,191 932 - 2.65 $

Q2 21

Non- Non-

Total Net Diluted

Interest PTPP(2) controlling

Revenues Income EPS

Expenses interest

Adjusted Results(1) 2,282 1,199 1,083 801 - 2.25 $

Taxable equivalent (44) - (44)

Total impact (44) - (44)

Reported Results 2,238 1,199 1,039 801 - 2.25 $

(1) On a taxable equivalent basis and excluding specified items, which are non-GAAP financial measures. See slide 2.

(2) Pre-Tax Pre-Provision earnings (PTPP) refers to Income before provisions for credit losses and income taxes. 47DISCLAIMER

This document has been prepared solely for informational purpose and is not an offer to sell or a solicitation of an offer to

buy any security of the Bank or to participate in any trading strategy. Any such offer, if and when made, will be made only

by the Bank in and on the basis of, an offering circular or a final prospectus and any pricing supplement, final terms or

prospectus supplement thereto (collectively the “Offering Documents”), containing final terms describing such security and

the offering, and distributed in accordance with applicable securities laws.

Any decision by a prospective investor to purchase the Bank’s securities must be based solely on information included in

the Offering Documents relating to such securities and on such investor’s own independent evaluation, review and

investigation of the Bank, the securities and the terms of the offering, including the merits and risks of an investment in

such securities.

The information herein may contain general, summary discussions of certain tax, regulatory, accounting and/or legal issues. Any such

discussion is necessarily generic and may not be applicable to, or complete for, any particular recipient’s specific facts and

circumstances. The Bank is not offering and does not purport to offer tax, regulatory, accounting or legal advice and this information

should not be relied upon as such. Prior to making an investment in the Bank’s securities, you should determine, in consultation with

your own legal, tax, regulatory and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and

accounting characteristics and consequences, of the investment.

No representation or warranty is given with respect to the accuracy or completeness of the information herein, or that any future offer

of securities, instruments or transactions will conform to the terms hereof. The Bank and its affiliates disclaim any and all liability

relating to this information. The information included in this document is current only as of its date and may have changed since such

date. Nothing in this document is, or may be relied upon as, a representation or promise by the Bank and its affiliates as to the past or

the future.

48QUESTIONS? Mr. Jean Dagenais, Senior Vice-President, Finance Jean.Dagenais@nbc.ca Mr. Jean-Sébastien Gagné, Treasurer JeanSebastien.Gagne@nbc.ca Additional information can be found via these web links: https://www.nbc.ca/investor-relations.html https://www.nbc.ca/capital-debt-information.html

You can also read