February 2022: How do you know a central banker is lying?

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Our view on global investment markets: February 2022: How do you know a central banker is lying? Keith Dicker, CFA Founder & Chief Investment Officer keithdicker@IceCapAssetManagement.com www.IceCapAssetManagement.com Twitter: @IceCapGlobal Tel: 902-492-8495 1

IMPORTANT:

An investment in any strategy, including the strategies described herein, involves a high degree of risk. There is no

guarantee that the investment objective will be achieved. Past performance of these strategies is not necessarily

indicative of future results. There is the possibility of loss and all investment involves risk including the loss of capital.

The opinions and views expressed in this publication are those of the firm and the author.

Who are the Chefs?

The moment their lips move, you know something is up. Yet, what makes Mr. Juncker one of the best out there, is that he even admits it.

For years, the oldest joke in the political world was trying to figure out exactly when a Now, what is so great about our world these

politician was lying. The punchline of course, was rather obvious - “when their lips are days is how EVERYTHING has melded together

moving”. to create something that is forcing other policy

makers to adopt their very own unique twist to

Or put another way - don’t believe a word out of a politician’s mouth. moving their lips.

To be clear, this is rather harsh - as there are many countless politicians and policy And by other policy makers, we are referring of

makers who work tireless and thankless hours doing many things most of us don’t course to the world’s central bankers.

appreciate.

In their defence, many of them just happen to

Yet, there’s a reason this joke has stood the test of time. And considering this obvious be in the wrong place at the wrong time.

point, you’d think politics 101 would have entire chapters on how to control your lips. In previous eras, central bankers were treated as rock stars.

However, many policy makers seemingly just can’t help themselves. In the 1990s, whenever US Federal Reserve Chairman Alan Greenspan would speak -

his mumbled, jumbled, googly moogly was deciphered for days on end with the

And the bigger the crisis, the faster the lips move.

conclusion that yes, Mr. Greenspan was indeed an entity from a reality far superior

Of course, there are countless stories of lips moving the wrong way - and it shouldn’t than the rest of us.

be a surprise that these lips have belonged to Liberals, Conservatives, Democrats,

Of course, years later everyone figured out his incoherent mumbles were actually not

Republicans, and every other colour and stripe out there.

the stuff of a genius wonder boy. Instead, it was the perception that he was a

The point is - one side is just as good as the other when it comes to flappin’ the old monetary genius that really mattered.

gums.

And that’s where today’s central bankers have entered the picture.

Perhaps one of the best lip movers of recent times has to be Europe’s Jean-Claude

And it has become increasingly clear, the picture they are trying to paint is one that

Juncker. His propensity to stretch the truth has become the stuff of legends.

few are buying.

3 www.IceCapAssetManagement.com

Moderately

The Central Banker The same is also true for determining how much money commercial banks should

set aside for the rainy day. Depending upon the health of the economy, central

Years ago it was quite common not to have a clue as to what a central banker was, or banks would moderately adjust the reserve requirements to ensure the overall

what they did. economy and financial system remained stable, respected and worry-free.

In fact, the fact that many were not even aware of this prestigious and academic- The key word here of course is - moderately.

based role was really a compliment to the entire central bank profession.

And that’s the whole point with central banking 101. Keep everything moving at a

In its simplest form, central banks are responsible for determining appropriate levels moderate pace. Hypnotize people to sleep as they watched the monetary paint

for interest rates, and the amount of reserve money commercial banks were required dry.

to set aside to protect the public.

Those were the days.

And what made this responsibility really special, was the independence to make

these changes regardless of what others thought or wanted them to do. And then everything started to change.

Presidents and Prime Ministers had no influence on the central bankers. In some ways, change should always be expected. After all, all domestic economies

and financial systems are already incredibly sophisticated and complicated.

Treasury Secretaries and Ministers of Finance had no influence on the central

bankers. When you begin adding global trade, product innovations and increasingly more

market participants who are all seeking to maximize profits while minimizing risk, it

CEOs of the Wall Street titans and commercial banks had no influence on the central should be no surprise that central bankers started to wakeup from their slumber.

bankers.

For many central bankers today, they are waking up to unimaginable worlds that

It really was a dream job. One, with one sole focus - do what was right. were never even dreamed of in the world of central bank academia.

When the economy was doing really well, central bankers would likely raise interest Changing interest rates to affect the economy - NO EFFECT!

rates moderately. And when the economy started to slump a bit, the central bank

would likely reduce interest rates moderately. Talking sternly and lecturing to influence market behavior - NO EFFECT!

4 www.IceCapAssetManagement.com

Mountains of Debt

Changing reserve requirements to nudge commercial banks to change lending habits -

NO EFFECT!

The world certainly had changed, and now central bankers had to do something that

wasn’t in their DNA, training or culture - they had to learn on the fly and fast. After all,

the fate of humanity depended upon this group of monetary rock stars.

One thing is for sure, moderate policy changes were things old central bankers did

from the old days.

And in their defense, today’s global financial world looks nothing like the old financial

world.

And the sole attribute that is different today - the entire world has borrowed way too

much and all of this borrowing has become completely dependent upon interest rates

And recall, the primary objective of central banks is to maintain a stable financial

never increasing again - ever.

system.

This point is so important, we have to repeat it.

The irony of course is doing nothing, further increases financial stress across the

If interest rates were to rise from current levels, it will become increasingly more system, while doing something, also further increases financial stress across the

difficult for gobs of old debt to be repaid and more expensive to borrow new debt. system.

Yet, from a central banking perspective, the current global market environment This of course, has created the perfect opportunity for central bankers to start

absolutely requires central banks to raise interest rates. moving their lips.

This of course is creating quite the dilemma for central bankers. If they do nothing, Back during the 2008-09 US Housing Crisis, then-Federal Reserve Chairman Ben

then inflation will surge out of control, yet borrowing will also continue to surge out of Bernanke stunned US lawmakers by announcing “we’re literally maybe days away

control. from a complete meltdown of our financial system” (NY Times, Sep 19, 2008).

5 www.IceCapAssetManagement.com

Economic Fantasyland Called Europe

As dramatic as it sounds - and to be clear, it was a dark and stressful time for everyone We think it’s a great name, and despite numerous data points and experiences,

- if you consider the objective of the central bank at the time (stability) then this there’s absolutely no reason to change this moniker at all.

excessive warning maybe was needed to get approval to bailout the very big banks who For the European Central Bank (ECB), they have actually been a constant source

actually caused the crisis to begin with.

of material and reasons to appreciate the challenges and opportunities of central

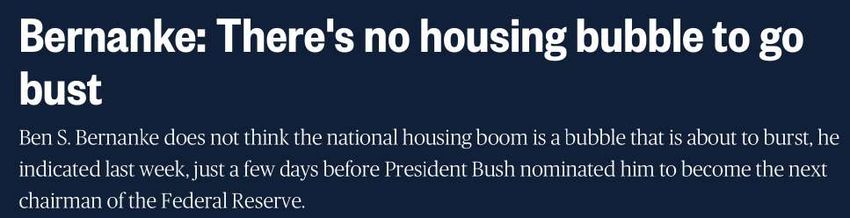

Of course, those who only follow main stream media and big box banks, will defend banking.

whatever narrative they are told. However, you should also be reminded that Ben

The challenges, of course, are many. Afterall, considering there are 19 different

Bernanke was also the central banker who proclaimed there wasn’t a housing crisis to

countries, economies, interest rates, and political agendas - a spark or two is

start with. bound to be flying at all times.

Come to think of it, the word “spark” is perhaps a disservice to all the sparks out

there in the world. Instead, a better word or phrase is perhaps “a raging financial

inferno” on the cusp of overwhelming the entire old world.

CNBC: Oct 2005

To demonstrate our skepticism towards the Europeans’ ability to achieve escape

velocity and forever leave behind their zombie banking system, unmarketable

debt and complete dependence on suppressing price discovery - consider the

following policy reactions orchestrated by the European Central Bank (ECB) since

the 2008-09 crisis:

The Americans are not the only country with central bankers that (in hindsight) have

come under suspicion of maybe not being entirely forthright with what’s really • European Financial Stability Facility (EFSF)

happening in their backyard. • European Financial Stabilisation Mechanism (EFSM)

• European Stability Mechanism (ESM)

And this is where the Europeans come into the story. • Outright Monetary Transactions (OMT)

This isn’t new, yet it bears repeating - IceCap has long referred to that part of the world • Long Term Refinancing Operation (LTRO)

as “The Economic Fantasyland called Europe”. • Long Term Refinancing Operation II (LTRO)

• Long Term Refinancing Operation III (LTRO)

6 www.IceCapAssetManagement.com

The Truth

• Tripartite Committee consisting of ECB, IMF, EC agreement (TROIKA) severe event.

• Forced austerity and bailouts of Portugal, Ireland, Italy, Greece, Spain

• Activation of FED USD Swap Lines The fact that the Europeans have enacted over 20 new (and renewed) emergency

• Asset Purchase Program (APP) response programs should be enough of a sign, that they’re screwed.

• Corporate sector purchase programme (CSPP)

• Public sector purchase programme (PSPP) Yet to be clear, despite over a decade of emergency bailout programs, the ECB has

• Asset-backed securities purchase programme (ABSPP) achieved an unintended and unwanted goal - an economy and banking system that

• Covered Bond Purchase Programme (CBPP) must be propped up on crutches and medicines 24 hours a day.

• Covered Bond Purchase Programme II (CBPP)

• Covered Bond Purchase Programme III (CBPP) They have no way out.

• Pandemic Emergency Purchase Programme (PEPP)

• Quantitative Easing (QE) And when a central banker’s back is to the wall, and they have no way out, there’s

• Zero Interest Rate Policy (ZIRP) only one thing to do - start moving those lips.

• Negative Interest Rate Policy (NIRP)

It all started in 2011 when then-ECB President Jean Claude Trichet played serious

Recall, the prime directive of central banking is to create an environment that dulls games with Greece all while telling everyone else, it wasn’t so serious at all.

everyone to sleep, making them watch the paint dry and become glossy-eyed at the

mere mention of central bank monetary policies. Next page displays a NYT article detailing both the “serious” discussions that happen

behind the curtain, and the absolute dismay by the market once the truth eventually

Considering this objective and the rather awkward situations that have dominated comes out.

the the European Union and Eurozone system, the ECB has actually done a masterful

job of making people somehow either forget, or ignore the severity of the problems. And make no mistake - the truth will always eventually come out.

Or worse still, maybe everyone has simply stopped caring. Next up as ECB President was Mario Draghi.

The irony here of course, and the fact that few have picked up on this, makes it even And to demonstrate the ironies that pulsed through Europe at that time, consider that

more absurd - an “emergency” program is itself a one-time response to a one-time the head of the ECB was an Italian, and the head of the Catholic Church was a

German.

7 www.IceCapAssetManagement.com

Draghi Was Ready

Of all the central bankers that graced our financial world, Mr. Draghi certainly ranks

up there as being perhaps the most confident that has ever stood over a

spreadsheet.

Of course years from now, this confidence might actually end up being viewed as

over-confidence.

Let us explain.

For starters, right out of the gate Mr. Draghi immediately cut interest rates. His

assessment of the Eurozone economy as being incredibly weak and on the verge of

bending the knee was correct - something had to be done.

Next up, Mr. Draghi correctly sensed what the bond market was telling everyone -

Italy (and Spain) was on the verge of plummeting through a financial blackhole and

drag the rest of the old world down with it.

And this is where Draghi created perhaps the most memorable moment in any

central bankers’ time.

He drew the line in the sand.

Analogous to the scene in Lord of Rings when Gandalf facing life or death, struck his

sword into the ground screaming “THOU SHALT NOT PASS!”, Draghi did the same.

As European Bond Markets were crumbling on July 26, 2012, Draghi did his Gandalf

impersonation by shouting he was “ready to do whatever it takes to preserve the

euro. And believe me, it will be enough”.

8 www.IceCapAssetManagement.com

Not Our Fault

This is the point where Europhiles declare “the rest is history”. And this is where central banks are choosing their words wisely.

This is nonsense of course. Whether inflation was caused by the COVID global lockdowns, or by over a decade

of free money is really irrelevant at this point in time.

All Draghi did was merely suspend the eventual day of reckoning for the Eurozone

and its mis-fitting monetary and fiscal marriage. Instead, everyone should first notice how policy makers will never accept blame for

such extreme economic and monetary reactions - “it isn’t our fault”.

Was Draghi lying at the time? Certainly no. He did everything possible to save the

Euro and the Eurozone members. Rather, shift your focus to what policy makers are now saying and how they are

saying it.

Yet, he was lying to himself.

Over a very quick 6-9 month period, central bankers have changed their tune on

And that’s the important distinction. There isn’t a person in the universe with inflation.

enough power, wisdom or connections to solve the world’s debt problem.

Inflation is seemingly no longer a short-term reaction. Nor is it a transitory phase

All Draghi did was merely slow the rate of decay. from one economic environment int the next.

Draghi and his central bank friends have all moved along, leaving the decay to a Instead through their actions, central bankers are now loudly declaring inflation is a

new, and even wiser group of monetary rock stars. problem and as a result, they are going to start raising interest rates, and reducing

other stimulus policies that were all designed to rescue the system from yesterday’s

And we’re not sure if this new group is either excited or fearful. They face war.

insurmountable odds.

The point here of course, should the world believe the words coming out of central

Global debt continues to grow exponentially. Fiscal deficits are seemingly out of bankers’ mouths?

control.

One thing is for certain, never before in anyone’s lifetime, has the world faced

And then we have the biggest challenge yet - inflation. simultaneous interest rate increases at the exact same moment when substantial

stacks of debt are dependent upon low interest rates to survive.

9 www.IceCapAssetManagement.com

Gradually, Then Suddenly

IceCap believes we have now reached a critical and important turning point. Within the monetary policy space, the US Federal Reserve has officially entered the

hawkish camp. While markets were already preparing for the American central bank

To be clear, it isn’t a turning point to be feared, instead, it is a turning point to be to begin raising rates and ending their Quantitative Easing (QE) program, markets

embraced. were not prepared to discover that the Fed was actually even more determined to

become more hawkish.

As the central banks attempt to restore interest rates to more acceptable levels at

the same time while societies brace for higher inflation, and higher debt servicing The December 2021 Fed Minutes were released in early January 2022 and surprised

costs - market disruptions should absolutely be expected. global markets by indicating US interest rates would begin to rise earlier, and faster

than markets were expecting. In addition, the FED minutes also pointed to a faster

And that’s where the opportunities lie. wind-down of their Quantitative Easing (QE) program.

Turning Points Markets do not like unexpected events. The result saw markets selling-off and

headlines including the following:

In the investment world, the really big moves are usually slow to develop. The

moves are slow at first, and some-times barely recognizable to all except those

who are looking.

For IceCap, the big moves we anticipate are certainly slow moving and fit into this

category. For this reason, many of our updates may appear as often repeating the

same themes and market movements from one period to another.

Yet, there’s a reason for these seemingly repetitive narratives – smaller pieces have

to be considered in the aggregate to more clearly see the bigger picture which

allows us to determine whether our investment thesis remains on track.

As managers, we view this event as significant as it officially signals an end (at least

And as the world progresses into the 2022, many of these smaller pieces continue for now) to 0% interest rate policies and QE in the biggest market in the world. This

to meld into larger pieces which continue pointing to a world where the probability really is a special moment that must be emphasized. We believe the resulting effect

of stress re-escalating across monetary, fiscal, economic, and geopolitical factors, is of this new policy path will ultimately lead to negative financial contagion spreading

increasing. globally across multiple markets and economies.

10 www.IceCapAssetManagement.comNot Normal

While current financial markets are still very uncertain, we should continue to be For over 12 years now, the global economy and financial markets have become

prepared for stops and starts which will eventually provide us with a longer-term picture dependent upon low rates, QE and of course fiscal deficits. This combination of

that is is a bit easier to tolerate. unorthodox fiscal and monetary policies has created a financial, economic, social,

and geopolitical marketplace where extremes have become normalized.

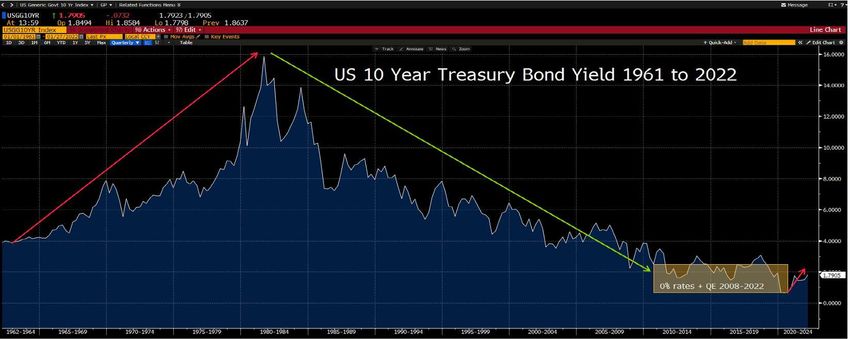

We’ve spoken before how the world has enjoyed (and likely unappreciated) the benefits

of long-term interest rates declining from highs reached in 1982 to near 0% in 2008-09. But this is not normal.

11 www.IceCapAssetManagement.comAlmost

And it has now become crystal clear that policy makers in both fiscal and monetary This meant that eventually global capital would ooze back into the USA, which also

roles are attempting to scale back from the extreme positioning the world has grown meant it was oozing away from other markets, and most notably emerging markets.

to accept as commonplace.

Today, the major fear and risk across global markets isn’t slowing earnings, or a new

The challenge with this transition is actually achieving it. And the challenge with covid variant, it is the potential for a rapidly strengthening US Dollar attracting capital

achieving it is convincing the world that it won’t be a challenge. away from all other markets.

Already, the US Federal Reserve’s proclamation of an end to these monetary policies This is the super-spreader-event we expect will eventually happen and believe this

has set in motion a sudden scramble to identify and secure safer environments to next phase of the monetary cycle has started.

protect capital. This has likewise led to a wave of global capital rotating from one

market to another. Which brings us to the 2022 version of the hawkish Federal Reserve.

Our expectation is for central banks to continue with tightening policies until This version is having a knock-on effect that is very different than the previous cycle -

something happens in the marketplace that forces them to stop, and then eventually it has forced other central banks to also consider raising rates and ending QE as well.

rewind these tightening moves.

So far, effectively all central banks except for the ECB (we’ll discuss them in a

As investors, we are all aware that this was tried unsuccessfully during 2017 and minute), the Bank of Japan (BOJ), and China have announced their intentions to

2018 when the Federal Reserve attempted to move away from 0% and QE policies. begin raising rates.

At the time, their strategy was to gradually raise overnight rates by 0.25% at the

While some of these central banks will use rising inflation and a recovering economy

slowest pace possible. It was so slow, it took them over 20 meetings to raise rates 8

as the reason for a sudden change in interest rate policies, the real reason is simply

times. This gradual pace of a +0.25% rate increase every second meeting was exactly

to keep pace with the Americans.

what they planned – an eventual return to 2%+ and higher rates while not rocking

the global monetary boat. Put another way, it was really the exact opposite of a This is especially true for the emerging market world. Keeping pace with the Federal

shock and awe event. Reserve will at least provide hope that foreign capital will remain in their emerging

market economies. This is the goal – keep foreign capital in your domestic economy

And it almost worked.

for as long as possible. Because, once it begins to leave, it leaves in a hurry which

The challenge back then, was that no one else (besides the Canadians) raised rates. then creates a crisis across interest rates and/or foreign exchange markets.

12 www.IceCapAssetManagement.comChina is Begging for Help

To confirm, our view and expectations, we had to look no further than China. On

January 17, 2022, Chinese President Xi Jinping spoke at the Davos World Economic

Forum. The biggest and loudest quote (from our perspective) was the following:

“If major economies slam on the brakes or take a U-turn in their monetary policies,

there would be serious negative spillovers. They would be serious negative spillovers.

They would present challenges to global economic and financial stability, and

developing countries would bear the brunt of it.”

Here we have the leader of a major economy effectively begging the Americans (and

other central banks) not to raise rates and end QE. The risk to China of course is the

immediate effect it will have on the Chinese Yuan and the Hong Kong Dollar.

As both currencies are pegged to the US Dollar and the Fed’s monetary policy, a

tightening policy in America is also an indirect tightening policy in China and Hong

Kong. And with both of these domestic economies experiencing slowing growth and

increasing credit risk (property developers), a monetary policy set to address a fast-

growing economy with little credit risk is the exact opposite of what is needed in

these markets.

To demonstrate the seriousness of this policy mismatch, note that China has actually

made the monetary situation even more strained by LOWERING interest rates.

Investors should appreciate and consider this paradox as a potential significant

fissure in the global financial system. The reason we see this as a potential crisis

opportunity is due to the combination of financial, economic and geopolitical factors

affected by this obvious awkward situation.

13 www.IceCapAssetManagement.comCanada – It’s a Bubble

To be clear, it’s awkward due to China implementing lower interest rates to protect its new policies. Instead, by raising rates in conjunction with the Americans, some of

domestic economy, yet their currency pegs to the USD is creating even more stress on these countries may actually be backing into another, much more serious risk –

FX Reserves and commercial banks. popping a domestic housing bubble.

While the combination of the US raising rates and China cutting rates will undoubtedly Second only to New Zealand and/or Australia, the Canadian housing bubble has grown

have an effect on capital flows, we also must recognize that aggregate government to legendary status.

spending rates are declining which will also act as a deterrent to global growth, as well

as USD flows to the emerging market economies. Official housing metrics including the below, all point to unsustainable, exponential

growth.

Using the US as an example, with the 2022 mid-term elections fast approaching, the

likelihood of additional stimulus programs being passed by Congress, or the Senate are

quite low. With most other countries also reducing their fiscal deficits relative to the

2020/21 budget years, fiscal stimulus will also act as a drag on the recovery.

Now the world has an interesting combination of rising interest rates, less QE and less

government spending, overlayed with China’s awkward monetary policy interference.

For now, however, the global investment community largely sees everything as a part

of a normal cycle.

However, as we progress through this normal cycle, it is our expectation that

increasingly more investors will recognize the really big movements have actually

begun to shift away from the low-risk markets of 2020-21, towards a new environment

of rising rates, slower growth and increasing geopolitical risks.

Yet, what makes the Canadian story even more interesting are the anecdotal stories.

As you may guess, there are some countries and economies that are reluctantly In addition to people lining up around the block to see “open houses”, it’s also quite

accepting the fact that higher interest rates are indeed on the way. Yet, this doesn’t common to see 30-40 offers being made on every house available for sale. And, like

necessarily mean they will be buffered from the effects resulting from the American’s any good “bubble”, the top is always characterized when “everyone” is talking about

the market, and everyone is afraid of missing out.

14 www.IceCapAssetManagement.comThread the Needle

The Canadians really do have quite the needle to thread.

On one hand, they have a booming economy (driven by housing and finance), and

run-away inflation, and then on the other hand they have a housing bubble built (and

encouraged/enabled) upon lower and lower interest rates. And if this wasn’t enough,

they also have to consider that the US Federal Reserve is starting on a path to raising

Which brings us back to this sudden and abrupt change to global monetary policies rates and tightening as well.

– namely rising interest rates and slowing QE.

This is a very precarious position for Canada. Inflation and growth measurements

And when applied to Canada, just consider the potential impact as demonstrated provide an extremely strong argument for them to raise rates aggressively. Yet, this

in the charts on this page. strategy would increase the probability of bursting the housing bubble, while also

increasing the debt burden for governments, corporations, and households.

15 www.IceCapAssetManagement.comEurope is up Merde Creek

Either way, it’s increasingly looking like higher rates from outside of Canada or inside Put another way, there’s no price discovery for German government bonds. The same

of Canada has the potential to create quite a stressful economic and financial is also true for French, Italian and every other EZ member. If interest rates were ever

experience. allowed to rise, it would create an eventual funding stress across all borrowers, as well

as create mark-to-market losses for those holding previously issued Eurozone debt.

Of course, the same is also true for the Eurozone. While the European Central Bank

(ECB) will absolutely begin to talk about their determination to raise interest rates and In short, the Europeans can never allow rates to rise.

end direct/indirect support to banks and sovereign states, the probability of them

actually carrying through is extremely low. Yet, the Europeans are also facing the largest surge in inflation since the Euro was

created.

The challenge faced by the ECB is that their sovereign state funding system has

become completely dependent upon the fantasies created by Quantitative Easing and

Negative Interest Rate Policies. As an example, this chart shows how nearly 50% of all

German Federal Debt has been purchased/financed by the ECB.

16 www.IceCapAssetManagement.comECB Has Created an Extraordinary Opportunity

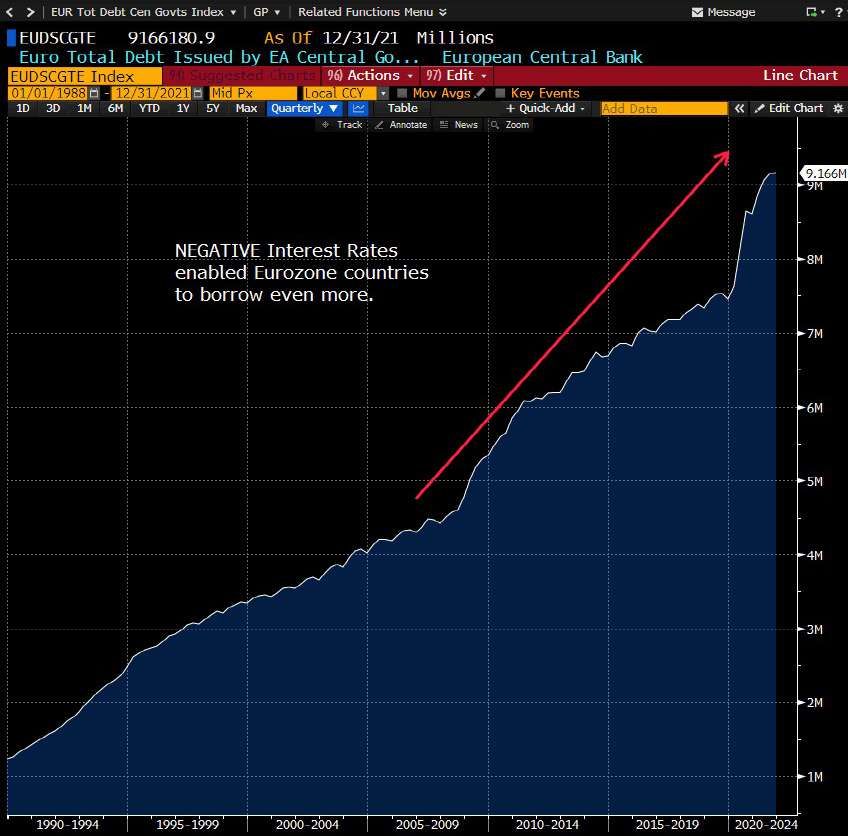

ECB lowered rates to 0% and then Yet, all it did was enable Eurozone

NEGATIVE% to save the Eurozone. countries to borrow excessively.

Rising interest rates and ending

QE increases the probability of a

debt crisis in Eurozone.

17 www.IceCapAssetManagement.comMarkets Don’t Care

And to make things even more challenging for the Europeans, they are now, for the Surprisingly, many investors want super charged returns, with no risk. From our

first time in the history of the ECB, faced with a global market driven by a hawkish US experience, this is kinda unrealistic. Yet, it happens all the time.

Federal Reserve and slowing global growth.

Which brings us to current markets conditions.

One thing is clear, the probability of the Eurozone experiencing escalating stress has

increased dramatically, which means the probability of the European Central Bank As we write, the good ‘ole days of 2020-2021 are over. Instead of everyone making

stretching the truth has also increased dramatically. money hand over fist, markets are now showing people how to lose money hand

over fist.

The Stock Market

In fact, stock, bond and crypto markets have all shifted from making many people

We love financial markets. And we also love the psychology behind financial markets. richer than they think, to making many people poorer than they really are.

And just like clockwork, whenever financial markets (and especially stock markets) And that’s the point behind market psychology - it can really mess with you.

enjoy a moment of joy, investors everywhere scramble to join the fun.

Of course, timing the top and bottom of every market is impossible. Instead,

The professional observation with this moment is, how so many investors become investors need to first swipe away their subjectivity. Never invest in something

accustomed to this new wonderful moment, that they inconveniently forget that what because you “like” it. As well, you should never, not invest in something because you

goes up, can also come down. “don’t” like it.

Or, as we like to say sometimes - there she was, gone. This may hurt some people’s feelings, but we all need to hear this every now and

then.

Put another way - all those easy money gains can disappear in a moments notice.

Markets don’t care about what your subjective likes or dislikes.

In short, and we do know it sounds both obvious and absurd, yet here it is - most

investors in general, are always chasing their tails. Instead, in its simplest form markets move up and down solely due to more/less

people buying rather than selling.

When markets are doing well, they expect all the upside. And when markets are not

doing well, they expect none of the downside. Yes, it really is all about capital moving from one market to another. Or away from

one market and seeking safety in another.

18 www.IceCapAssetManagement.comDon’t Chase Your Tail

It just so happens; we are now experiencing a market where the world’s major Final Thoughts

central bank - the US Federal Reserve - is telling everyone (rather loudly) that they

The world should really prepare for central banks, and especially the US Federal

are pulling the plug on all those nice and warm, fuzzy feelings everyone experienced

Reserve to begin to aggressively raise interest rates.

when the very same US Federal Reserve told them to go out and party hard.

It’s going to happen and it’s going to have dramatic effects across all financial

Our primary models for assessing the downside risk in equity models are both markets, especially emerging markets as well as high yield bonds.

suggesting the possibility of further downside in equities remains high.

The sad fact about this rather obvious increase in risk is that the majority of the

This isn’t a surprise to IceCap, and we’ve been positioned and waiting patiently for world’s most conservative investors unknowingly have significant allocations to bond

this opportunity. funds which are directly invested in these high risk markets.

And that’s the way one should view all markets - opportunities to buy and People should understand that central banks really are between a rock and a hard

opportunities to sell. One should never view any market as buy all the time, or place.

another as one to sell or avoid all the time.

Inflation is absolutely surging around the world. And these price increases are no

At this time, IceCap continues to hold modest allocations to equity markets. Should where close to the “official” price increases reported to us by governments. While

equities decline further from here as our models suggest, other allocations in our our governments are telling us price increases are between +4% to +7%, our pocket

portfolio will provide comfort and offsets. As well, as soon as our models and books are paying +20% and higher for many things.

perspectives guide us towards a change in trend, we’ll be ready for that shift as well. And whenever anything goes wrong in the world, people want someone to blame.

And one thing we know for certain, just as the opportunity to shift back towards Unfortunately for central bankers, everyone including the man on the street,

equities is established, most other investors are usually doing the opposite. politicians, main stream media and social media are all pointing their fingers at the

central bankers.

Our suggestion - don’t chase your tail.

Whether central bankers are directly and fully responsible for today’s surging

inflation is entirely irrelevant. It doesn’t matter. Central Bankers have been tried in

the social court of public opinion and they’ve been found guilty of causing inflation.

19 www.IceCapAssetManagement.comThe Loonie Hour

And the sentence is going to be higher rates.

Just to be clear - higher rates will not resolve the inflation problem. Instead, re-

opening the global economy and supply chains, and removing mobility restrictions

will absolutely start to help get inflation under control.

We ask you not to interpret this as IceCap showing sympathy for central bankers or

anyone else. Instead, the importance is understanding which way policy makers are

moving is what will guide you towards preserving your capital, and maybe even

taking advantage of these shifts as they occur.

Announcement

We are pleased to share IceCap has collaborated to launch a weekly podcast called

”The Loonie Hour”.

The Loonie Hour is a Canadian-based, global financial podcast covering newsworthy

events across the world and how they will impact Canadians. We are building a

community that will help Canadians better understand the really big shifts that are

occurring around the world and how it will affect you, in Canada. We invite you to

listen and watch, and provide us with your thoughts, feedback and ideas.

The “Loonie Hour” is hosted by real estate analyst, Steve Saretsky, and joined by

Richard Dias, Founder of Acorn Macro Consulting and Keith Dicker, Founder of IceCap

Asset Management Limited.

The weekly podcast can be enjoyed on Spotify, Apple Podcast, YouTube.

20 www.IceCapAssetManagement.comOur Strategy

Currencies If you appreciate IceCap’s market views and perspectives, we invite you to become a

Our long-term expectation for a strengthening USD remains on track. Our client.

expectation of a wind-down in extraordinary global monetary and fiscal stimulus is

now happening, which increases the probability of market strains which leads to a We also encourage our readers to share our IceCap Global Outlook with those who

strong USD. Emerging market currencies have potential for severe crises. they think may find it of interest.

Fixed Income

IceCap’s cautions towards the bond market are now playing out. Opportunities will

eventually develop - yet, for now we remain very concerned about emerging market Keith Dicker, CFA

debt and high yield bond markets. keithdicker@IceCapAssetManagement.com

www.IceCapAssetManagement.com

Commodities Twitter: @IceCapGlobal

IceCap portfolios added allocations to agricultural commodities. Colder climates and Tel: 902-492-8495

rising farming costs increases the probability for success in this sector.

Equities

IceCap’s decision not to chase equity markets last year is now proving correct. We

anticipate having the opportunity to increase allocations at lower risk levels than Keith Dicker, CFA founded IceCap Asset Management Limited in 2010 and is the Chief

what was offered in 2021. Investment Officer. He has over 25 years of investment experience, covering multi

asset class strategies including equities, fixed income, commodities & currencies.

Volatility

No change to our views on volatility. The potential for surges, spikes and collapse in Keith earned the Chartered Financial Analyst (CFA) designation in 1998 and is a

several volatility markets is providing our portfolios with opportunities that occur member of the Chartered Financial Analysts Institute. He has been recognized by the

infrequently. We like these markets. CFA Institute, RealVision, MacroVoices, Reuters, Bloomberg, BNN and the Globe &

Mail for his views on global macro investment strategies. He is a frequent speaker on

the challenges and opportunities facing investors today and is available to present to

groups of any size.You can also read