Equity Picks WM CM Equities - April 2022 - UBS

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

For UBS Marketing Purposes Only Equity Picks WM CM Equities April 2022 Report prepared by UBS Wealth Management Please see important disclaimers at the end of the document.

For UBS Marketing Purposes Only

Stock Review – Recovery as war concerns faded

• Recovery. The past month did well as markets

recovered from war concerns. S&P rose +7.9%, Stock performance over the past month

Nasdaq was up +9.5%, and HSCEI +2.8%.

% chg % chg UBS UBS +/- UBS

Stock Price

52wk Hi 1-mth Rating TP ($) (%)

• Performance. Most of our picks were up 9-15%,

THERMO FISHER 612.2 (8.9) 16.8 BUY 700.0 14.3

except for Tencent (-3.5%), which was hit by poor BOOKING HOLDINGS 2,213.2 (18.5) 16.5 BUY 2,775.0 25.4

results. Outflows from Taiwan dragged TSMC (+1%) AMAZON.COM INC 3,155.7 (16.4) 16.0 BUY 4,625.0 46.6

AIA 82.9 (21.5) 13.5 BUY 110.0 32.7

while Bank of America (+2.1%) fell over concerns

LVMH MOET HENNE 624.0 (17.7) 13.4 BUY 807.0 29.3

that an economic slowdown will hurt the banks. MASTERCARD INC-A 349.6 (12.9) 11.2 BUY 463.0 32.5

CHINA LONGYUAN-H 18.1 (10.1) 11.2 BUY 30.0 65.7

• Deletion. We are removing Thermo Fisher (done MSCI INC 510.0 (25.0) 9.4 BUY 692.0 35.7

MICROSOFT CORP 301.4 (13.8) 9.3 BUY 360.0 19.5

well, less upside) and Bank of America (CIO cuts ALPHABET INC-A 2,717.8 (10.3) 6.9 BUY 3,900.0 43.5

Financials to Neutral over slowdown fears). BANK OF AMERICA 39.4 (21.4) 2.1 BUY 64.0 62.5

TSMC 568.0 (17.7) 0.9 BUY 810.0 42.6

• Addition. In their places, we add Netflix (improving TENCENT 369.8 (40.1) (3.5) BUY 460.0 24.4

content & price hikes may spur recovery) & Applied As of 08 Apr 2022

Materials (fell over concerns of shortage).

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information, including 1

but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.

For UBS Marketing Purposes Only

Key Changes

Netflix (NFLX US) Applied Mat. (AMAT US)

Stock has fallen -47% from peak after Stock fell -16% lately over concerns that

guidance fell short amidst the broader component shortages & China lockdown

tech selldown. Expectations are low. could hurt near-term growth.

Content pipeline is improving as filming The longer-term outlook is good as each

has resumed. This could help to spur a region plans to beef up their chip supply

pick-up in new subscribers. chain for security reasons.

Recent price hikes (10-11%) should start This wil benefit wafer equipment makers

to show through while content costs such as ASML and AMAT.

may begin to moderate by 3Q22.

Stock offers >30% upside to target

There is 60% upside to target price. price.

Thermo Fisher (TMO US) Bank of America (BAC US)

Share price has rallied +17% in the past CIO downgraded Financials to Neutral as

month and is looking overbought. business sentiment & growth could be

affected by inflation concerns.

There is only +15% upside to our target

($700), hence not as compelling. Happy In the near term, rising rates will benefit

to revisit if it falls to $580. banks, but this may be negated by the

concerns of an economic slowdown.

Overall, still a great stock. Covid sales

may slow but can be offset by a pick-up Within the sector, BAC is our key pick as

in the core lab supply business. it is the most sensitive to rising rates.

M&A and buybacks can provide support It is also less dependent on IB, WM &

given strong cashflows. trading where activites are slowing.

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information, including 2

but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.

For UBS Marketing Purposes Only

Equity Picks – Valuation Table

10Y RSI Profit FCF

M/Cap % chg UBS UBS +/- UBS P/E P/E

Stock Code Ccy Price Chg 30- Margin Margin

(US$b) 52wk Hi Rating TP ($) (%) (FY22) 5Y Avg

(%) 70 (%) (%)

AIA 1299 HK HKD 82.3 127.0 (21.5) 199 59 BUY 110.0 33.7 17.8 5.7 17.3 24.1

ALPHABET INC-A GOOGL US USD 2,665.8 1,766.4 (12.0) 738 43 BUY 3,900.0 46.3 26.2 26.0 21.4 31.4

AMAZON.COM INC AMZN US USD 3,089.2 1,571.2 (18.1) 1,543 45 BUY 4,625.0 49.7 5.1 (3.1) 46.9 136.6

APPLIED MATERIAL AMAT US USD 120.0 106.0 (28.2) 907 39 NEUTRAL 160.0 33.4 26.7 20.7 14.7 17.4

BOOKING HOLDINGS BKNG US USD 2,167.4 88.6 (20.2) 197 44 BUY 2,775.0 28.0 15.7 23.0 24.5 191.4

CHINA LONGYUAN-H 916 HK HKD 17.2 26.4 (15.2) 171 60 BUY 30.0 74.6 16.1 (14.0) 15.7 11.5

LVMH MOET HENNE MC FP EUR 631.7 347.0 (16.7) 451 48 BUY 807.0 27.8 18.7 25.1 23.9 32.7

MASTERCARD INC-A MA US USD 352.3 344.3 (12.3) 719 50 BUY 463.0 31.4 44.1 48.0 34.4 41.0

MICROSOFT CORP MSFT US USD 297.0 2,226.3 (15.1) 879 46 BUY 360.0 21.2 35.5 33.4 31.4 31.8

MSCI INC MSCI US USD 506.5 41.2 (25.5) 1,319 50 BUY 692.0 36.6 38.8 45.1 44.2 47.7

NETFLIX INC NFLX US USD 355.9 158.1 (49.2) 2,396 41 BUY 575.0 61.6 16.5 (0.4) 31.4 120.4

TENCENT 700 HK HKD 358.8 439.9 (42.6) 743 44 BUY 460.0 28.2 0.7 32.2 21.7 51.2

TSMC 2330 TT TWD 560.0 500.6 (18.6) 580 39 BUY 810.0 44.6 38.0 17.4 18.3 21.7

As of 11 Apr 2022

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information, including 3

but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.

For UBS Marketing Purposes Only

Netflix – Better showing in 2H22?

Netflix plunged -40% in January as it was hit by the 11 April 2022

global tech rout, further exacerbated by the weak Netflix Inc USD BUY

guidance. Could it see a recovery in 2H22? Bloomberg NFLX US Price 355.9 Beta 1.1

• Shows are returning from the gap last year with Share Cap (m shr) 444 UBS TP 575.0 52-Hi 701.0

Free Float 98% % diff 61.6 52-Lo 329.8

hits such as Bridgerton & Stranger Things. Market Cap ($m) 158,108 Price Chg. 1-Yr 3-Yr 5-Yr

Market Cap (US$m) 158,108 Absolute (35.9) (3.2) 146.5

• Price hikes of 10-11% in 1Q22 could help to Daily Vol 3m (m shr) 8.3 Industry Movies & Entertainment

support earnings and mitigate any impact from the Daily Val 3m (US$m) 3,305 Major S/Holder CAPITAL GROUP COMPAN (13.23%)

higher churn. YE 12/2021 - USD 2020A 2021A 2022E 2023E 2024E

• Expectations low. Mgmt. guided for just 2.5m Sales ($m)

Net Profit ($m)

24,996

2,761

29,698

5,116

33,399

5,260

37,549

6,793

41,797

8,383

net adds for 1Q21. Recent data tracker suggests EPS ($) 6.26 11.55 11.33 14.44 17.49

that actual users may be doing better. EPS Growth (%) 46.9 84.5 (1.9) 27.4 21.1

P/E (x) 56.8 30.8 31.4 24.7 20.4

• Margin recovery. Margins fell sharply in 4Q21 as P/B (x) 14.2 10.0 7.9 6.3 5.0

Yield (x) 0.0 0.0 0.0 0.0 0.0

content costs spiked when filming resumed. Profits ROE (%) 29.6 38.0 27.6 27.9 28.1

may recover in 2H22 as production normalises. Net Gearing (%) 93.1 76.3 - - -

Source : Bloomberg

• Decent upside to our target price of $575.

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information, including 4

but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.

For UBS Marketing Purposes Only

Netflix Inc.

1 Mgmt. guided for just 2.5m net adds in 1Q21, which is not 2 Margins plunged in 4Q21 as content costs spiked when filming

aggressive. Recent data suggests that users are holding up. resumed. Profits could recover in 2H22 as production normalises.

Netflix - User Addition QoQ (m) Netflix: Op. Margin (%)

27.4

30

25.2

20

23.5

22.1

15.8

25

20.4

18

18.7

16

16.6

20

14.4

14.3

14

10.1

12.1

12.0

11.8

12 15

9.6

10.2

8.8

8.5

8.3

9.7

10

8.4

8.2

7.5

6.8

7.0

8 10

5.2

4.6

4.4

6 4.0 5

2.7

2.5

2.2

4

2 1.6 0

0

Netflix

Source: UBS

3 Netflix raised its standard pricing from $13.99 to $15.49 in 1Q22. 4 Despite the downgrades, there is ample upside to consensus

This could help to drive ARPU higher. target price

Avg Revenue Per User ($/mth)

11.74

11.73

NETFLIX INC - Target Price (USD)

11.67

800

11.53

12.00

Netflix

700

11.13

11.06

11.02

11.50

10.95

Share Price : $368.4

10.87

10.80

600

10.75

Target Price : $509.9

11.00 500

10.27

10.14

10.50 400

300

10.00

200

9.50 100 Current Upside : 38.4% Avg Upside : 10.5%

9.00 0

1-15 1-16 1-17 1-18 1-19 1-20 1-21 1-22

Q418

Q219

Q319

Q419

Q120

Q220

Q320

Q420

Q221

Q321

Q421

Q119

Q121

Share Price Target Price Bloomberg

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information,

including but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.

For UBS Marketing Purposes Only

Applied Materials - Semi security

Applied fell 15-16% recently over concerns that the 11 April 2022

component shortages & lockdowns in China could Applied Materials Inc USD NEUTRAL

hurt demand. Stock now offers 33% upside. Bloomberg AMAT US Price 120.0 Beta 1.5

• Near-term hit. Along with other semi stocks, Share Cap (m shr) 883 UBS TP 160.0 52-Hi 167.1

Free Float 100% % diff 33.4 52-Lo 114.4

AMAT fell over concerns that lockdowns in China Market Cap ($m) 105,972 Price Chg. 1-Yr 3-Yr 5-Yr

could affect demand for smartphones & PCs. Market Cap (US$m) 105,972 Absolute (13.6) 182.5 214.0

Daily Vol 3m (m shr) 8.9 Industry Semiconductor Equipment

• Long term fine. Order book should stay strong Daily Val 3m (US$m) 1,196 Major S/Holder VANGUARD GROUP (8.28%)

as each region is planning to build their own chip YE 10/2021 - USD 2020A 2021A 2022E 2023E 2024E

making facilities to ensure national security. Sales ($m) 17,202 23,063 26,501 29,390 28,663

Net Profit ($m) 3,619 5,888 7,238 8,212 7,887

• Key leaders. Along with ASML, this will benefit EPS ($) 3.95 6.47 8.17 9.41 9.33

Applied as it is one of the leading providers of EPS Growth (%) 36.7 63.8 26.3 15.2 (0.8)

P/E (x) 30.4 18.5 14.7 12.7 12.9

wafer fabrication equipment. P/B (x) 10.4 8.7 7.9 6.7 5.5

Yield (x) 0.7 0.8 0.8 0.9 1.0

• Decent upside. P/E has fallen to 13-15x with ROE (%) 38.5 51.6 55.5 52.3 41.4

33% upside to UBS target price. Net Gearing (%) (0.3) 2.4 - - -

Source : Bloomberg

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information, including 6

but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.

For UBS Marketing Purposes Only

Applied Materials

1 Demand to stay strong as each region is planning to build their 2 This has led to a strong jump in Applied’s order book, which will

own chip-making facilities to ensure national security help to support revenue growth in 2022

APPLIED MATERIALS INC (USD) AMAT : Order Backlog ($b) AMAT

35.0 14

30.0 12

25.0 Sales Op. Income 10

20.0 8

15.0 6

4

10.0

2

5.0

0

0.0 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21

'00

'01

'02

'03

'04

'05

'06

'07

'08

'09

'10

'11

'12

'13

'14

'15

'16

'17

'18

'19

'20

'21

'22

'23

As of 11 Apr 2022

Semicon System Service Display

Source: UBS

3 Structural growth from EV, AI, IOT, metaverse and data centers 4 The recent sell-off has opened up attractive opportunities in

will help to drive future demand Applied’s share price

AMAT - Systems Sales by Industry (US$b) AMAT 200 APPLIED MATERIAL - Target Price (USD)

5.0

180

4.0 160 Share Price : $120.0

140 Target Price : $173.0

3.0 120

2.0 100

80

1.0 60

40

0.0 20 Current Upside : 44.2% Avg Upside : 20.9%

Q118

Q218

Q318

Q418

Q119

Q219

Q319

Q419

Q120

Q220

Q320

Q420

Q121

Q221

Q321

Q421

Q122

0

1-15 1-16 1-17 1-18 1-19 1-20 1-21 1-22

Foundry / Logic DRAM Flash Memory Share Price Target Price Bloomberg

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information,

including but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.

For UBS Marketing Purposes Only

Equity Picks

AIA (1299 HK) Amazon (AMZN US) Booking (BKNG US)

FY21 new business (up 20%+) is doing AWS Cloud, a major profit contributor, Booking will benefit from the recovery in

better than peers (down 20%+). continues to grow strongly. global travel as it is one of the leading

online travel platforms.

Ongoing China expansion is a key driver Rising energy prices & wages will lead to

for growth , with promising outlook in higher delivery costs but can be offset by Apart from hotels, it is expanding into

Tianjin, Shijiazhuang & Sichuan. a drop in covid-related expenses. alternative accommodation, as well as

air travel & car rental.

China’s covid lockdown is a near-term Amazon has invested heavily into capex

risk, but any HK-China border reopening over last two years & will start to reap It has also rolled out royalty programs to

will help to revive the HK business. the benefits of greater efficiencies. encourage repeat visitors.

$10b buyback will help to support the Upcoming 20-for-1 stock split (ex-date Earnings growth should stay strong due

share price. 27-May) should provide support. to the low base from the pandemic

Alphabet (GOOG US) Applied Mat. (AMAT US) Longyuan (916 HK)

Ad demand (70% sales) is doing well as Stock fell -16% lately over concerns that China’s largest wind farm operator with

Google is less affected by the IOS privacy component shortages & China lockdown new projects hitting grid parity.

changes, unlike the smaller platforms. could hurt near-term growth. Govt policies are supportive as carbon

Youtube (11% sales) continues to grow But longer-term outlook is good as each neutrality is a key goal highlighted at the

rapidly, while Cloud (8% sales) is poised region plans to beef up their chip supply 2022 NPC meetings.

to turn profitable soon. chain for security reasons. A potential repayment of long-overdue

The upcoming 20-for-1 stock split in mid This wil benefit wafer equipment makers renewable subsidies to operators could

2022 will provide support. such as ASML and AMAT. accelerate the renewable build-out.

Valuation reasonable at 22x P/E with Stock offers >30% upside to target Green electricity pricing & carbon credit

>40% upside to target price. price. trading are key catalysts for growth.

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information, including 8

but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.

For UBS Marketing Purposes Only

Equity Picks

LVMH (MC FP) Microsoft (MSFT US) Netflix (NFLX US)

Buyers of luxury good are less sensitive Earnings are highly resilient as >70% of Stock has fallen -47% from peak after

to price inflation. revenue are from software subscriptions, guidance fell short amidst the broader

where it recently raised pricing. tech selldown. Expectations are low.

Covid lockdown in China (25% sales) is

a near-term risk, but past experience has Azure, the cloud division, is now 34% of Content pipeline is improving as filming

shown the demand eventually returns. sales & continues to do well. has resumed. This could help to spur a

The recovery in global travel will help to Microsoft is sitting on $70b of near cash, pick-up in new subscribers.

rejuvenate duty-free sales. can support dividends & buybacks. Recent price hikes (10-11%) should start

P/E has fallen to 24x, which is below the P/E is at the 5-year average of 32x. Stock to show through while content costs

5-year average of 33x. There is >25% still offer >20% upside. may begin to moderate by 3Q22.

upside to target price. There is >60% upside to target price.

Mastercard (MA US) MSCI (MSCI US) Tencent (700 HK)

Mastercard benefits from the rebound in Earnings are resilient as 74% of sales are Tencent’s diverse revenue streams from

global travel & increased spending from from index subscriptions & 24% from gaming & social will help to cushion the

the economic re-opening. asset-based fees – both are recurring. weakness in advertising revenue.

Near term, a rise in marketing spent may The growing popularity of ETFs & rising Overseas expansion for gaming should

temporarily depress profits, but this can demand for new ESG & Climate indices help counter slower growth in China.

be offset by a pick-up in transactions. will help to expand the business.

Regulatory uncertainty over social media

Long term, the shift to digital payments Despite the 25% pull back, P/E is still not & payments are near-term risks.

will continue to drive growth. cheap at 44x.

Valuation is inexpensive at 23x FY22 P/E,

Stock now trades at 34x P/E (below 5yr There is >35% upside to target price. close to 10-year trough.

avg. 41x) and offer >30% upside.

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information, including 9

but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.For UBS Marketing Purposes Only

Equity Picks

TSMC (2330 TT)

Stock sold off lately over concerns that

lockdowns in China could hurt demand

for smartphones & PCs.

It was also hit by portfolio outflows out

of Taiwan due to geopolitical concerns.

TSMC now trades at 18x P/E, below its

5-year average of 21x, and offers 46%

upside to consensus target.

Overall demand for semicon is expected

to stay supported.

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information, including 10

but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.For UBS Marketing Purposes Only Company Pack WM CM Equities April 2022 Report prepared by UBS Wealth Management Please see important disclaimers at the end of the document.

For UBS Marketing Purposes Only AIA Group Limited April 2022 Report prepared by UBS Wealth Management Please see important disclaimers at the end of the document.

For UBS Marketing Purposes Only

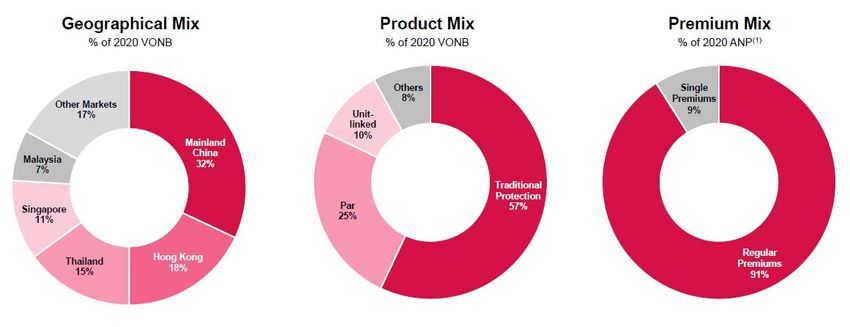

AIA Group Limited

AIA is the leading life insurance company in Asia-Pacific, with its key markets being China, HK, Symbol 1299 HK ISIN HK0000069689

Thailand, Singapore and Malaysia. Traditional protection makes up ~60% of its products mix,

Currency HKD Exchange Hong Kong

while ~90% of sales are derived from recurring premiums. AIA was spun out of AIG during

the financial crisis in 2009 and was listed on HKSE in October 2010. AIG no longer holds a Website www.aia.com.hk

stake in the company. AIA has more than 23,000 employees.

Industry Life & Health Insurance

• Low penetration. Life insurance penetration in Asia remains pretty low at just 2-4%, esp. PRICE HISTORY

in China. The industry is expected to enjoy strong growth, driven by rising income, increased

awareness for protection and favourable demographic changes. AIA GROUP LTD - Price (HKD)

120

• China is a key market and accounts for 32% of new businesses. Apart from organic growth

via expansion into more cities, AIA has struck at 15-year distribution partnership with BEA 100

and acquired a 24.99% stake in China Post Life to expand its bancassurance channels. 80

• Health ecosystem. AIA has built up an extensive health and wellness network across the 60

region, covering health monitoring and assessment, prevention, diagnostic and treatment 40

across both online and offline channels. This will help to reduce the cost of protection. 20

As of 11 Mar 2022

• Catalysts. The lockdown has impacted new businesses in 2020 but demand has rebounded 0

quickly once the lockdown eased. The re-opening of the HK-China border will also help. 10 11 12 13 14 15 16 17 18 19 20 21

AIA has diversified exposure across Asia with a focus on recurring protection products REVENUE & OPERATING PROFIT

AIA (USD)

35.0

30.0

Net Premium

25.0 Op. Income

20.0

15.0

10.0

5.0

0.0

'07 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20

AIA As of 10 Feb 2022

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information,

including but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.For UBS Marketing Purposes Only

AIA Group Limited

1 Growth potential is strong as life insurance penetration in Asia 2 China is a key revenue contributor, both directly as well as

remains relatively low, especially in China indirectly via Hong Kong

Life Insurance Penetration (%) AIA - Revenue Breakdown

45

20.0 17.5 16.8 40

16.0 35

30

12.0 25

6.7 20

8.0 6.2 6.1

15

3.6 3.3 2.7

4.0 2.3 10

1.6

5

0.0 0

'14 '15 '16 '17 '18 '19 '20

HK China Thai S'pore M'sia Others AIA

UBS

3 The lockdown has hurt new businesses in 2020 but demand 4 AIA has established a strong health & wellness ecosystem

has recovered quickly once lockdowns are eased across Asia, covering both online and offline channels

AIA - Value of New Business (US$m)

5,000

New businesses growing steadily,

4,000 though temporarily affected by

lockdowns in 2020

3,000

2,000

1,000

0

'10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20

HK China Thai S'pore M'sia Other AIA

AIA

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information,

including but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.For UBS Marketing Purposes Only Amazon.com April 2022 Report prepared by UBS Wealth Management Please see important disclaimers at the end of the document.

For UBS Marketing Purposes Only

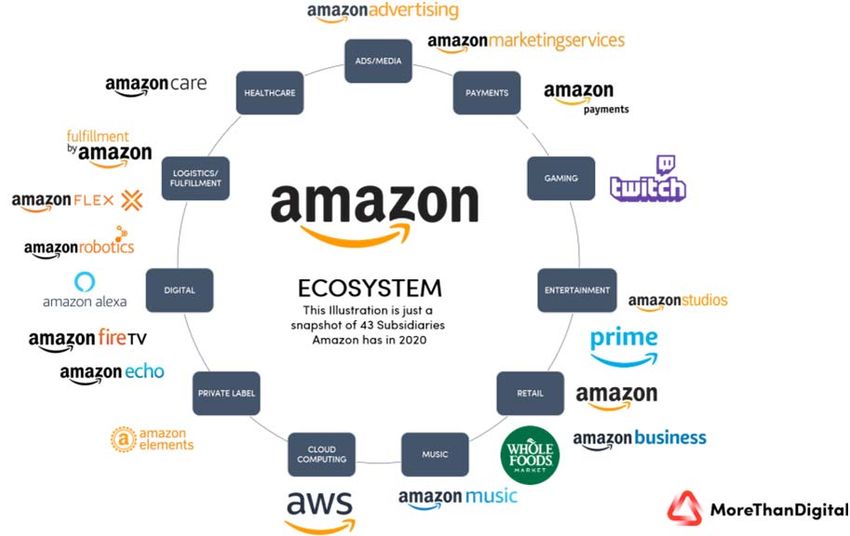

Amazon.com

Amazon is the world's largest online retailer while Amazon Web Services (AWS) is the biggest Symbol AMZN US ISIN US0231351067

cloud service provider. The company operates as both a direct seller and a platform for third- Currency USD Exchange NASDAQ

party sellers to distribute their products. To support its operations, Amazon has built a vast

global network of fulfillment centers. Jeff Bezos is the founder and executive Chairman with a Website Amazon.com

10.57% stake. Based in Washington, Amazon has about 1.3m employees. Industry Internet & Direct Marketing Retail

• Rise of e-commerce. Amazon is poised to benefit from the rapid growth of e-commerce, PRICE HISTORY

where the penetration rate is still below 25-30%. US remains its core market (60% sales).

AMAZON.COM INC - Price (USD)

• Leading cloud platform. AWS is among the leaders in cloud services globally. Cloud makes 4,000

up 12% of FY20 revenue but contributes to 60% of operating profits.

• In the Prime. Amazon has built up an extensive logistics network in the US and can do one- 3,000

day delivery in most major cities, which not many other retailers can match. It has also a big

base of 180m Prime members – where the average spending is much higher. 2,000

• Solid cash flow. Amazon generates more than US$60B of operating cash flow each year 1,000

and have been aggressively investing for future growth. There is potential to return cash once

As of 11 Mar 2022

the expansion stabilises. 0

00 02 04 06 08 10 12 14 16 18 20 22

Amazon has built a large global ecosystem which cannot be replicated easily REVENUE & OPERATING PROFIT

AMAZON.COM INC (USD)

700.0

600.0

500.0 Sales

400.0 Op. Income

300.0

200.0

100.0

0.0

'00

'01

'02

'03

'04

'05

'06

'07

'08

'09

'10

'11

'12

'13

'14

'15

'16

'17

'18

'19

'20

'21

'22

'23

As of 11 Mar 2022

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information,

including but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.For UBS Marketing Purposes Only

Amazon.com

1 E-commerce penetration in the US is still relatively low at 20-25% 2 E-commerce is big in revenue, but the profits are generated from

and has plenty of room to grow Cloud, Subscription (Prime) & Advertising (Others)

Amazon - Sales by Segment ($b)

450

Amazon

400

350

300

250

200

150

100

50

0

'14 '15 '16 '17 '18 '19 '20

Online Physical 3rd Party Subscription Cloud Others

Source: UBS Source: UBS

3 Cloud drives the bulk of profits and it will continue to grow 4 Operating cashflow has improved in recent years and is mainly

rapidly as more businesses go online spent on expanding the business

Amazon - Op. Income by Segment ($b) 150.0 AMAZON.COM INC (AMZN US) - Cashflow

25

Amazon

20 100.0

15 50.0

10

0.0

5

0 (50.0)

(5) (100.0)

2014 2015 2016 2017 2018 2019 2020

'21E

'22E

'23E

'00A

'01A

'02A

'03A

'04A

'05A

'06A

'07A

'08A

'09A

'10A

'11A

'12A

'13A

'14A

'15A

'16A

'17A

'18A

'19A

'20A

Operating Cashflow Dividend + Buyback

North America International AWS (Cloud) Investing Cashflow Other Financing Bloomberg

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information,

including but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.For UBS Marketing Purposes Only

Amazon.com

1 Cloud and Subscription continue to do well, but E-commerce sales 2 The lockdown in 2020 led to a surge in volumes, but consumers

are slower this year following the boom from last year are buying less this year as they venture back outside

Amazon - Sales by Segment ($b) Paid Units (% YoY Growth)

60 57

140

Amazon Amazon

120 50 46 47 44

100 40

32

80 30 27 28 28 27 25

24 24 23 22 22 22

60 17 15 18

20 14 15

40 10 8

10

20

0

0

Q220

Q320

Q420

Q116

Q216

Q316

Q416

Q117

Q217

Q317

Q417

Q118

Q218

Q318

Q418

Q119

Q219

Q319

Q419

Q120

Q121

Q221

Q321

Q116

Q216

Q316

Q416

Q117

Q217

Q317

Q417

Q118

Q218

Q318

Q418

Q119

Q219

Q319

Q419

Q120

Q220

Q320

Q420

Q121

Q221

Q321

Online Physical 3rd Party Subscription Cloud Others WW Paid Units (% YoY Growth)

3 Shipping costs have risen due to social distancing measures, labor 4 The higher shipping costs have affected profits for E-commerce,

tightness and supply chain disruptions but Cloud (AWS) is performing well

Shipping Cost as a % of Revenue Amazon - Op. Income by Segment ($b)

30 10

24.4

Amazon Amazon

22.9

22.7

22.4

21.9

21.4

21.3

25

20.4

8

19.9

18.9

18.0

17.0

16.8

16.6

16.2

16.1

15.7

20 6

15.2

15.0

14.9

14.3

13.2

13.2

15 4

10 2

5 0

0 (2)

Q116

Q216

Q316

Q416

Q117

Q217

Q317

Q417

Q118

Q218

Q318

Q418

Q119

Q219

Q319

Q419

Q120

Q220

Q320

Q420

Q121

Q221

Q321

Q216

Q316

Q416

Q217

Q317

Q417

Q218

Q318

Q418

Q219

Q319

Q419

Q120

Q220

Q320

Q420

Q221

Q321

Q116

Q117

Q118

Q119

Q121

Shipping Costs as a % of E-Commerce Revenue North America International AWS (Cloud)

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information,

including but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.For UBS Marketing Purposes Only Booking Holdings Inc. April 2022 Report prepared by UBS Wealth Management Please see important disclaimers at the end of the document.

For UBS Marketing Purposes Only

Booking Holdings Inc.

Booking Holdings operate six of the world's leading online travel platforms. Booking.com is Symbol BKNG US ISIN US09857L1089

the main brand with 2.4m properties across 220+ countries. It also owns Priceline (discount

Currency USD Exchange NASDAQ GS

travel), Agoda (AsiaPac travel), KAYAK (meta-search), RentalCars (car hires), and OpenTable

(dining reservations). The company generates revenue from commissions and the various fees Website www.bookingholdings.com

that it charges when a client makes a booking via its portals. It has 20,300 employees.

Industry Online Travel Agency

• Leading player. Booking.com is the clear leader among online travel agencies and has one PRICE HISTORY

of the most downloaded travel apps globally. It has a strong presence in Europe & is making

in-roads into US via Priceline and Asia via Agoda. BOOKING HOLDINGS INC - Price (USD)

3,000

• Connected trips. Apart from accommodation, it is bundling in car rental & air tickets. This

may lower overall margins but will help to drive topline growth. The company has also rolled 2,000

out a loyalty program called Genius to encourage repeat customers.

• Expansions. Besides hotels, it is adding alternative accommodations (homes & apartments), 1,000

which now make up 29% of bookings. It has also recently made acquisitions to strengthen

its presence in flight bookings and the U.S. As of 29 Mar 2022

0

• Risks. 1) competition from Google & AirBnB; 2) large hotel groups are reaching out directly 00 02 04 06 08 10 12 14 16 18 20 22

to clients via their own websites. 3) covid disruptions. 4) regulations on data transfer & tax.

Booking Holdings operate six leading online travel platforms REVENUE & OPERATING PROFIT

BOOKING HOLDINGS INC (USD)

24.0

19.0

Sales

14.0 Op. Income

9.0

4.0

(1.0) '00

'01

'02

'03

'04

'05

'06

'07

'08

'09

'10

'11

'12

'13

'14

'15

'16

'17

'18

'19

'20

'21

'22

'23

As of 29 Mar 2022

Booking.com.

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information,

including but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.For UBS Marketing Purposes Only

Booking Holdings Inc.

1 Revenue is generated from commissions & various fees that 2 Agency sales (bookings only) remain the largest contributor,

are charged when a client makes a booking on its platforms but Merchant sales (all-in services) are growing in significance

Merchant Revenue by Distribution (US$m)

34% 16.0

Agency Merchant sales come 14.0

61% from payments for 12.0

hotels, credit card

Booking 10.0

Agency sales are driven fees, commissions &

Revenue insurance etc. 8.0

by commission charged

for processing client

Breakdown

6.0

bookings on behalf of FY21 Sales from KAYAK

the partner hotels & OpenTable 4.0

Ads & Others 2.0

5% 0.0

'08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21

Booking Agency Merchant Ads & Others Booking

3 Sales were affected during the pandemic but have started to 4 Gross bookings were growing consistently until the pandemic

recover as global travel returns hit. They are expected to return to pre-covid levels by 2023.

Revenue by Distribution (US$m) Gross Bookings (US$m)

6.0 120.0

5.0 100.0

4.0

80.0

3.0

60.0

2.0

40.0

1.0

0.0 20.0

0.0

'08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21

Agency Merchant Ads & Others Booking Agency Merchant Booking

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information,

including but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.For UBS Marketing Purposes Only

Booking Holdings Inc.

1 Accommodations remain the key bookings driver, but the 2 Overall take-rate has been declining due to the expansion into

company is increasingly bundling in car rentals & flight tickets air travel and car rental where commission rates are lower

Booking Metrics Booking Take Rate (%)

1.0 30

0.9 25.5 25.1

0.8 25 22.6

20.1 19.2

0.7 20 18.5

17.3 16.8 16.6

0.6 15.8 15.6 15.7 15.6

14.3

0.5 15

0.4

0.3 10

0.2 5

0.1

0.0 0

'08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21 '08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21

Room Nights (m) Rental Car Days (m) Airline Tickets (m) Take Rate (%) Booking

3 Cashflows were affected during the pandemic but are poised 4 Covid disruptions are less of a threat now, while regulations,

to recover ahead as earnings improve competition and cyber attacks are ongoing issues.

15,000 BOOKING HOLDINGS (BKNG US) - Cashflow Competition. Large hotel groups are reaching out directly to

customers via their own websites & loyalty programs, while search

10,000

engines such as Google is another source of competition.

5,000 Travel disruptions. The pandemic has severely disrupted the

travel industry. It is unclear if the threat of covid is over.

0

Regulations. Tightening regulations over data transfer (out of

(5,000) Europe) and user privacy could affect the company’s operations

while rising global taxation may hurt its earnings.

(10,000)

Cybersecurity. As an online platform, Booking is vulnerable to

'22E

'23E

'00A

'01A

'02A

'03A

'04A

'05A

'06A

'07A

'08A

'09A

'10A

'11A

'12A

'13A

'14A

'15A

'16A

'17A

'18A

'19A

'20A

'21A

the threat of cyber attacks.

Operating Cashflow Dividend + Buyback

Investing Cashflow Other Financing

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information,

including but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.For UBS Marketing Purposes Only China Longyuan Power April 2022 Report prepared by UBS Wealth Management Please see important disclaimers at the end of the document.

For UBS Marketing Purposes Only

China Longyuan Power Group

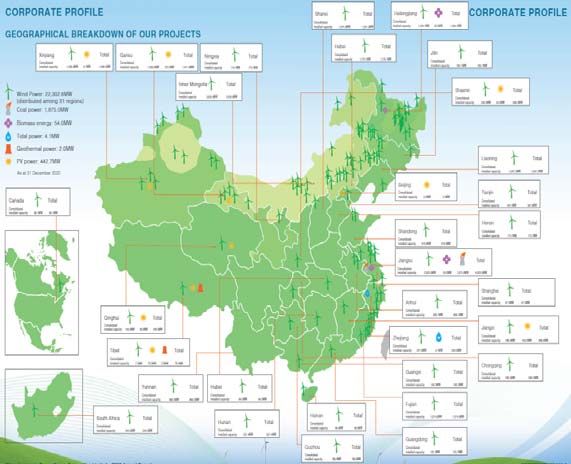

Founded in 1993, China Longyuan Power is the largest wind farm operator in China, with a Symbol 916 HK ISIN CNE100000HD4

total installed wind capacity of ~22.4GW (as of 1H21) across most of the wind-resource rich

Currency HKD Exchange Hong Kong

provinces (e.g. Inner Mongolia, Xinjiang, Gansu). It derives >98% of revenue from China, with

wind power contributing almost 100% of total profit. CHN Energy, a central SOE, owns 57% Website www.clypg.com.cn

of Longyuan. The company has ~8,000 employees.

Industry Renewable Electricity

• Beneficiary of China’s green initiatives. China’s ambition to reach “carbon neutrality” by PRICE HISTORY

2060 will pave a long runway ahead for renewables. The mix of electricity generation from

renewables is projected to double from 9% to 17% between 2020 to 2025e. CHINA LONGYUAN POWER GROUP-H - Price

25 (HKD)

• Strong expansion to drive growth. Longyuan plans to expand its capacity from 22GW to

30GW between 2020-2025e (split 30/70 between wind/solar), while there is potential for 20

asset injection of 15GW wind capacity from its parent company upon its A-share listing. 15

• Hitting grid-parity. More projects are hitting grid parity & can generate reasonable returns 10

without subsidies, thus alleviating the concern of subsidy reliance. The injection of RMB89b

by MoF into a subsidy fund will help to boost legacy subsidy repayment to Longyuan. 5

As of 11 Mar 2022

• Risks. 1) failure to collect unpaid subsidies; 2) lower utilization hours due to unpredictable 0

weather conditions; and 3) unexpected on-grid tariff cuts. 09 10 11 12 13 14 15 16 17 18 19 20 21

Longyuan’s power generation facilities are well spread across China REVENUE & OPERATING PROFIT

CHINA LONGYUAN POWER GROUP-H (CNY)

50.0

40.0

Sales

30.0 Op. Income

20.0

10.0

0.0

'06

'07

'08

'09

'10

'11

'12

'13

'14

'15

'16

'17

'18

'19

'20

'21

'22

'23

Longyuan As of 11 Mar 2022

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information,

including but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.For UBS Marketing Purposes Only

China Longyuan Power Group

1 Longyuan’s wind capacity addition target with room for 2 Over 90% of Longyuan’s installed capacity comes from wind,

upside vs China’s renewables generation mix target by 2025E where utilization rate is improving thanks to lower curtailment

BP Statistical Review of World Energy July 2021, NEA of China, Longyuan, CHN Energy NEA of China, Longyuan

3 Wind power is the key profit driver for Longyuan, accounting 4 Free cash flow will remain negative due to the aggressive

for the lion’s share of total operating profits build-out of more wind power capacities ahead

Longyuan - Operating Profit (RMB b) 40.0 CHINA LONGYUAN-H (916 HK) - Cashflow

12

30.0

10 20.0

8 10.0

6 0.0

(10.0)

4

(20.0)

2

(30.0)

0 (40.0)

'06A

'07A

'08A

'09A

'10A

'11A

'12A

'13A

'14A

'15A

'16A

'17A

'18A

'19A

'20A

'21E

'22E

'23E

(2)

'08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 Operating Cashflow Dividend + Buyback

Wind Energy Coal Energy Other Energy LongYuan Investing Cashflow Other Financing Bloomberg

Click to edit Master text styles

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information,

including but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.For UBS Marketing Purposes Only LVMH Moët Hennessy Louis Vuitton April 2022 Report prepared by UBS Wealth Management Please see important disclaimers at the end of the document.

For UBS Marketing Purposes Only

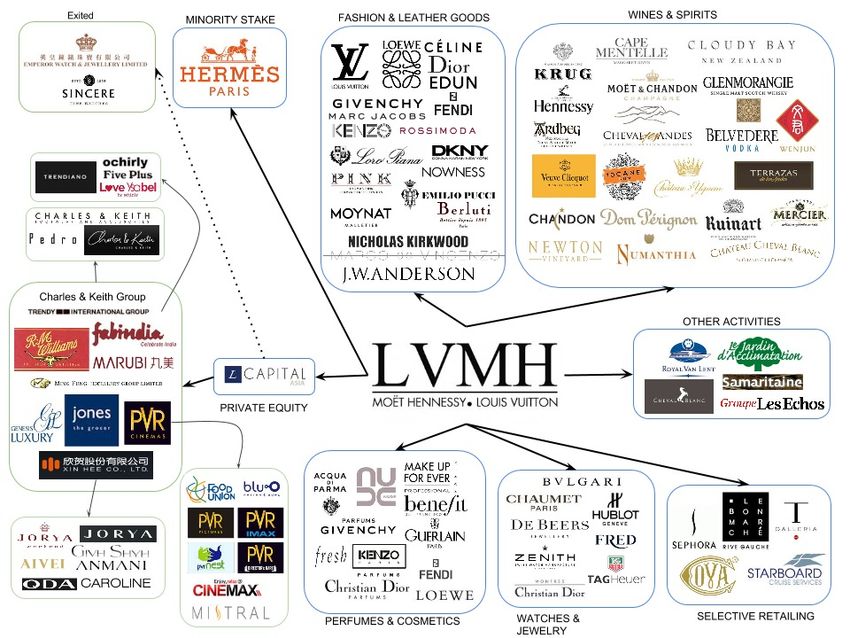

LVMH Moët Hennessy Louis Vuitton

LVMH is the world's largest luxury goods company with ~75 prestige brands spanning wines Symbol MC FP ISIN FR0000121014

and spirits (Dom Pérignon, Moët & Chandon, Veuve Clicquot, Hennessy), perfumes (Guerlain),

Currency EUR Exchange EN Paris

fashion & leather goods (Louis Vuitton, Dior, Givenchy), and watches & jewelry (TAG Heuer,

Bulgari, Tiffany). Its retail division includes Sephora, Le Bon Marché dept stores, and DFS duty- Website www.lvmh.fr

free. LVMH is collectively owned by Christian Dior & Bernard Arnault (47.5% stake). It has

Industry Apparel, Accessories & Luxury

163,000 employees.

• Secular winner. LVMH plays into several secular trends such as 1) rising consumerism across PRICE HISTORY

developed and emerging markets as wealth increases; 2) propensity for younger consumers to

buy branded goods, partly driven by the influence of social media. LVMH MOET HENNESSY LOUIS VUI - Price

800 (EUR)

• Diversified. Unlike other luxury players who depend on just 1-2 key brands, LVMH has over

75 prestige brands across several major product categories, which made it more resilient. It is 600

also well diversified across all geographies and is not over-reliant on China (~30% sales).

• Aggregator. Thanks to its immense size and extensive network of >5,400 stores, LVMH has 400

great bargaining power against retail landlords. It also has a strong track record of acquiring

small emerging brands and scaling them up profitably. 200

As of 11 Mar 2022

• Risks. 1) Bernard Arnault (72) remains an important shareholder & driving force of the group; 0

2) China makes up 30% of sales and is prone to anti-luxury or anti-Western sentiment. 00 02 04 06 08 10 12 14 16 18 20 22

LVMH owns ~75 prestige brands spanning five major product segments REVENUE & OPERATING PROFIT

LVMH MOET HENNESSY LOUIS VUI (EUR)

100.0

80.0

Sales

60.0 Op. Income

40.0

20.0

0.0

'00

'01

'02

'03

'04

'05

'06

'07

'08

'09

'10

'11

'12

'13

'14

'15

'16

'17

'18

'19

'20

'21

'22

'23

Source: eachshoes.com As of 11 Mar 2022

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information,

including but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.For UBS Marketing Purposes Only

LVMH Moët Hennessy Louis Vuitton

1 Asia (35%) and US (24%) are the two major driving forces of 2 Revenue is dominated by Fashion & Leather Goods (48%),

LVMH’s revenue growth followed by Retail (23%) - which includes Sephora & DFS

LVMH : Revenue by Region LVMH : Revenue by Category

60 60

50 50

40 40

30 30

20 20

10 10

0 0

'10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20

France Europe (ex-Fr.) US Wine & Spirits Fashion & Leather Perfumes & Cosmetics

Japan Asia Ex-Jpn Others LVMH Watches & Jewelry Selective Retailing Others LVMH

3 Main profit contributors are Fashion & Leather Goods (64% op. 4 Fashion-&-Leather Goods and Wine-&-Spirits enjoy much higher

profit), followed by Wine & Spirits (15%) margins compared to the other segments

LVMH : Profit by Category Operating Margin 2019 (%)

14

35.0 33.0

12 31.0

10 30.0

8 25.0

6 20.0 16.7

4 15.0 10.0 9.4

2 10.0

0 5.0

(2)

0.0

'10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20

Wine & Fashion & Perfumes & Watches & Selective

Wine & Spirits Fashion & Leather Goods Spirits Leather Cosmetics Jewelry Retailing

Perfumes & Cosmetics Watches & Jewelry Goods LVMH

Selective Retailing Others LVMH

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information,

including but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.For UBS Marketing Purposes Only

LVMH Moët Hennessy Louis Vuitton

1 LVMH has taken advantage of the pandemic to expand its store 2 Compared to other luxury retailers, LVMH is more geographically

networks to 5,400 this year, largely in Asia diversified and not as reliant on Chinese consumers

LVMH : Stores by Region LVMH % exposure to Chinese consumers

6,000 60

50 UBS

5,000 50

40 40

4,000 40 35 35 33 33

30 30 30

3,000 30

20

2,000

10

1,000

0

0

'11 '12 '13 '14 '15 '16 '17 '18 '19 '20 1H21

France Europe (ex-Fr) US Japan Asia RoW

3 LVMH's massive size and extensive distribution network gives it a 4 Cashflow generation is strong and has been split between paying

strategic advantange as a brand aggregator dividends and making acquistions of emerging brands

Annualised Revenue 2020 (US$b) 25.0 LVMH MOET HENNE (MC FP) - Cashflow

60 20.0

51

50 15.0

40 10.0

30 5.0

20 15 15 0.0

7 6 5 (5.0)

10 3

0 (10.0)

(15.0)

'21E

'22E

'23E

'00A

'01A

'02A

'03A

'04A

'05A

'06A

'07A

'08A

'09A

'10A

'11A

'12A

'13A

'14A

'15A

'16A

'17A

'18A

'19A

'20A

Bloomberg as of 20 Aug 2021

Operating Cashflow Dividend + Buyback

Investing Cashflow Other Financing Bloomberg

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information,

including but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.For UBS Marketing Purposes Only Mastercard Inc. April 2022 Report prepared by UBS Wealth Management Please see important disclaimers at the end of the document.

For UBS Marketing Purposes Only

Mastercard Inc.

Mastercard connects consumers, financial institutions, merchants & other partners worldwide, Symbol MA US ISIN US57636Q1040

enabling them to use electronic payments instead of cash and checks. It owns a family of well-

Currency USD Exchange NYSE

known brands, including Mastercard, Maestro and Cirrus. The company operates in over 210

countries covering >150 currencies. As of 2020, it has ~2.3b credit & debit cards in circulation. Website www.mastercard.us

It earns its revenue from processing payment transactions – it does not take credit risks.

Industry Diversified Financial Services

• Going cashless. Digital payment is rapidly displacing cash/cheques, thanks to rising internet PRICE HISTORY

access, strong growth in cross-border payments (e-commerce, travel) and rising penetration is

emerging markets. This will benefit electronic payment networks such as Mastercard. MASTERCARD INC - A - Price (USD)

500

• Strong moat. Mastercard and Visa are the two dominant card issuers globally (ex-China). It is

not easy to displace them as they have built a massive base of users, merchants and partners 400

over the years, and invested heavily into their IT infrastructure & authorization networks.

300

• Consistent growth. Sales have grown at 13% CAGR from $2.3b in 2003 to $15b in 2020.

Operating margins have held steadily above 50%, even during the pandemic. 200

• Risks. Blockchains are potential disruptors but Mastercard may include them in its solutions. 100

As of 11 Mar 2022

Other risks include pressure in interchange rates from regulations & competition.

0

06 07 08 09 10 11 12 13 14 15 16 17 18 19 20 21

Mastercard provides the network that connects consumers with banks and merchants REVENUE & OPERATING PROFIT

MASTERCARD INC - A (USD)

30.0

25.0

Sales

20.0

Op. Income

15.0

10.0

5.0

0.0

'03

'04

'05

'06

'07

'08

'09

'10

'11

'12

'13

'14

'15

'16

'17

'18

'19

'20

'21

'22

'23

Source: Company Data As of 11 Mar 2022

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information,

including but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.For UBS Marketing Purposes Only

Mastercard Inc.

1 Digital payments are replacing cash and cheque, esp. in Asia and 2 Mastercard & Visa are the two dominant card issuers globally,

EMEA where penetration rates are still low while UnionPay is popular within China

Credit card as a % of total payments

50%

44% UnionPay,

45% 30%

Mastercard,

40% 25%

35% 33%

Purchase

30%

Transactions

25% on Global

20% 18% Cards

AMEX, 2%

15% 13%

JCB, 1%

10%

Visa, 42% Discover, 1%

5%

0%

EMEA Asia LATAM North America Nilson Report

Source: McKinsey Source: Nilson Report

3 Rising contributions from Asia and emerging markets (>30% 4 Cross border fees were hit by the pandemic in 2020 but are

sales) will help to drive growth expected to recover. Other transactions have remained stable.

Mastercard: Gross Dollar Volume (US$tn) Mastercard: Gross Revenue By Fee Type ($b) Mastercard

7.0 30

6.0 25

5.0 20

4.0

15

3.0

10

2.0

1.0 5

0.0 0

'10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20

US Canada Europe LatAm AsiaPac, EMEA Mastercard

Domestic Fees Cross Border Fees Processing Fees Others

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information,

including but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.For UBS Marketing Purposes Only Microsoft Corp. April 2022 Report prepared by UBS Wealth Management Please see important disclaimers at the end of the document.

For UBS Marketing Purposes Only

Microsoft Corp.

Microsoft is the world's largest software company operating in over 190 countries. It is a leader Symbol MSFT US ISIN US5949181045

in various categories such as productivity software (Office 365), operating systems (Windows),

Currency USD Exchange NASDAQ

cloud infrastructure (Azure), gaming (Xbox) and executive search (LinkedIn). A large part of its

revenue is considered mission-critical by its clients and are based of subscriptions, thus giving it a Website www.microsoft.com

strong recurring revenue base. It has >180,000 employees.

Industry Systems Software

• Steady Growth. Thanks to the strong recurring revenue, MSFT has been able grow its sales PRICE HISTORY

steadily at 10% CAGR since 2000 from $23b to $143b, while op. margins have risen to an

MICROSOFT CORP - Price (USD)

impressive 37%. In turn this has driven strong performance in its share price. 400

• Subscriptions. Many of its core offerings such as Office are considered mission-critical and

have shifted to a subscription model. More than two-thirds of revenues are recurring. 300

• Rising Cloud. Corporations are digitizing and shifting their data to the Cloud. Azure is the 200

#2 player in Cloud globally after AWS. Cloud now makes up 34% of overall revenue.

• Strong cash flows. With minimal capex and a strong recurring revenue, cashflow is highly 100

positive. The company has over $70b of near-cash and has been allocating more towards As of 11 Mar 2022

buybacks & dividends. 0

00 02 04 06 08 10 12 14 16 18 20 22

Microsoft provides an entire suite of solutions to help companies run their businesses REVENUE & OPERATING PROFIT

MICROSOFT CORP (USD)

250.0

200.0

Sales

150.0 Op. Income

100.0

50.0

0.0

'00

'01

'02

'03

'04

'05

'06

'07

'08

'09

'10

'11

'12

'13

'14

'15

'16

'17

'18

'19

'20

'21

'22

'23

Microsoft

As of 11 Mar 2022

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information,

including but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.For UBS Marketing Purposes Only

Microsoft Corp.

1 More than 70% of revenue is recurring, driven by its software 2 Thanks to its mission critical nature, software revenue has grown

solutions for Windows, Office & Servers consistently throughout the years

Other

LinkedIn 7% 200 Microsoft - Revenue

Microsoft

6%

Enterprise Office

4% 24% 150

Search Ads

5% 100

Microsoft

Xbox Revenue

2021 50

9%

Server 0

Windows 31% '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21

14% Office Server Windows Xbox

Search Ads Enterprise LinkedIn Other

Microsoft Source: Company Data

3 Cloud has been a strong growth driver, while corporate 4 Profits have improved in recent years as the Cloud business has

digitization is another major structural trend started to achieve economies of scale

Microsoft Microsoft

Microsoft - Segmental Revenue Microsoft - Operating Profit

200 80

70

150 60

50

100 40

30

50 20

10

0 0

'14 '15 '16 '17 '18 '19 '20 '21 '14 '15 '16 '17 '18 '19 '20 '21

Personal Computing Productivity & Biz Processes Cloud Personal Computing Productivity & Biz Processes Cloud

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information,

including but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.For UBS Marketing Purposes Only

Microsoft Corp.

1 Cloud continues to grow strongly while operating margins have 2 Group margins have improved from 30% to 40% as the Cloud

improved from greater economies of scale business started to contribute

Microsoft

Microsoft - Commercial Cloud Microsoft - Operating Margin (%)

25

45 41.6

38.6 38.8 37.0

20 40

34.4 34.1

32.0

35 29.5 30.1 31.8

15 30

23.7

25

10 19.4

20

5 15

10

0 5

Q117

Q217

Q317

Q417

Q118

Q218

Q318

Q418

Q119

Q219

Q319

Q419

Q120

Q220

Q320

Q420

Q121

Q221

Q321

Q421

Q122

Q222

0

'10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20 '21

Commercial Cloud Revenue Commercial Cloud Gross Profit

Microsoft

Source: UBS Source: Company Data

3 Microsoft continues to generate strong cashflow, which is used 4 The maturity of the enterprise software space, and Microsoft’s

for dividends, buybacks, and acquisitions dominance, may restrict its future growth potential

150.0 MICROSOFT CORP (MSFT US) - Cashflow High valuation. Due to its resilient nature, Microsoft still trades at

a relatively high P/E of 30-33x. This may come under pressure as

100.0 rate rises.

50.0 Slowing growth. Unlike other emerging industries, the enterprise

software space is more matured, hence it will be more difficult for

0.0 Microsoft to sustain high growth, esp. given its sheer size.

(50.0) Cyber-threats. As a software company, Microsoft is vulnerable to

cyber-attacks, which may affect the performance and reliability of

(100.0) its services.

'00A

'01A

'02A

'03A

'04A

'05A

'06A

'07A

'08A

'09A

'10A

'11A

'12A

'13A

'14A

'15A

'16A

'17A

'18A

'19A

'20A

'21A

'22E

'23E

Geopolitics. Some regions may wish to reduce its dependence on

Operating Cashflow Dividend + Buyback US-based software to avoid potential sanction risks.

Investing Cashflow Other Financing Bloomberg

Source: Company Data

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information,

including but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.For UBS Marketing Purposes Only MSCI Inc. April 2022 Report prepared by UBS Wealth Management Please see important disclaimers at the end of the document.

For UBS Marketing Purposes Only

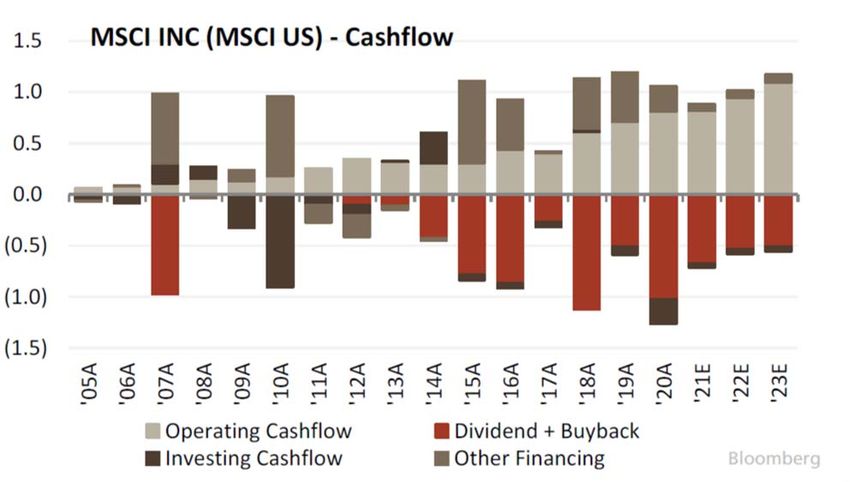

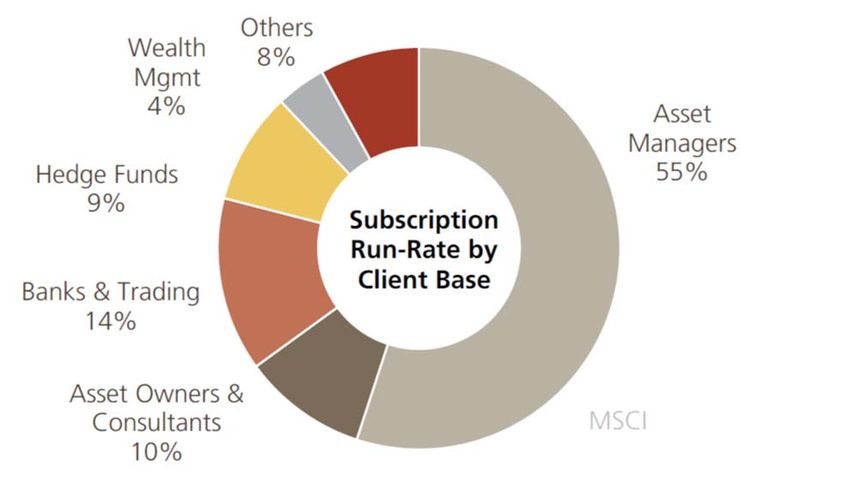

MSCI Inc.

MSCI produces indices and risk-return portfolio analytics for investment institutions. The firm Symbol MSCI US ISIN US55354G1004

manages >246,000 financial indices used by large asset management firms. It has over 4,500

Currency USD Exchange NASDAQ GS

clients across >95 countries. US makes up 47% of sales, followed by EMEA (37%) & AsiaPac

(16%). About 75% of sales comes from subscription services, while 25% is from asset-based Website www.msci.com

fees. About 97% of revenue is recurring. It has >4,200 employees.

Industry Financial Exchanges & Data

• Highly resilient. Earnings have held up well over time as 74% of revenue is supported by PRICE HISTORY

recurring subscriptions, while 24% comes from asset-based fees – which is also recurring.

Since 2010, sales have grown at 10% CAGR while op. profits grew at 16% CAGR. MSCI INC - Price (USD)

800

• Exceedingly profitable. Op. margins are high at 50% while net margins are 35%. The

business generates ample cashflow. Since it is not capital intensive, most of the surplus cash 600

are used for buybacks & dividends.

• Growth drivers. The core index business is growing at low-double digits due to the rising 400

popularity of ETFs, thematic and factor investing, while ESG & Climate offer new expansion

200

opportunities. MSCI is also branching into Fixed Income, Private Markets and alternatives.

As of 11 Mar 2022

• Risks. 1) rising rates could put pressure on high valuations, 2) challenging financial markets 0

could dampen growth of new subscriptions; 3) regulatory changes; 4) cyber-threats. 07 08 09 10 11 12 13 14 15 16 17 18 19 20 21

MSCI provides >4,500 financial institutions with index services & portfolio solutions REVENUE & OPERATING PROFIT

MSCI INC (USD)

3.0

2.5

Sales

2.0

Op. Income

1.5

1.0

0.5

MSCI Inc. 0.0

'05

'06

'07

'08

'09

'10

'11

'12

'13

'14

'15

'16

'17

'18

'19

'20

'21

'22

'23

As of 11 Mar 2022

Please see important disclaimers and disclosures at the end of the document. All information has been sourced from publicly available information,

including but not limited to, company websites and financial reports, analyst reports, news articles and information service providers.You can also read