AGRICULTURAL LANDS & WATER - F R COLORADO'S FUTURE - Colorado Food Systems ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Updated June 10th, 2021 – Adopted June 24th, 2021

CONSERVING

AGRICULTURAL LANDS

F R COLORADO’S FUTURE

& WATER

PURPOSE

Colorado’s agricultural lands are incredibly and financial sustainability

diverse, including rangelands, croplands (including farm product pricing, input

(irrigated and non-irrigated), pasturelands, costs, market access, etc.), training

and woodlands.1 Agricultural lands of all types programs supporting new and beginning

and water are necessary for most farming and farmers, educational programs facilitating

ranching today and will be essential into the farm transitions/succession, value chain

foreseeable future. Across Colorado, however, infrastructure development initiatives, and

agricultural lands and water are under threat on-farm natural resource conservation

from development, as well as from economic, programs like Environmental Quality

regulatory, and environmental pressures. Incentives Program (EQIP), which invested

Colorado has prepared for many of these $156M on over 3,500 projects across 1.8M

challenges with multiple agricultural land and acres of Colorado from 2014-2017.4 We

water conservation tools, but current tools also acknowledge the essential role that

fall short of addressing the scale of the threat. private land owners play in conserving on-

This Issue Brief outlines threats to Colorado’s farm natural resources and in keeping land

agricultural land, reviews Colorado’s tools for in agriculture. Additional tools are likely

agricultural land protection and conservation, needed to adequately compensate private

identifies limitations to those tools, and landowners for the full public value they

recommends next steps for the State of create and steward, and still more additional

Colorado. This Issue Brief builds on two tools are likely needed to help producers

previous COFSAC Issue Briefs: Preparing for capture the full value of their production

Food Security in an Age of Limited Natural practices and product attributes. We expect

Resources Part I: Water (2015)2 and Preparing future Issue Briefs to explore one or more of

for Food Security in an Age of Limited Natural these in detail.

Resources Part II: Land Use (2015).3

In this Issue Brief, we have excluded a detailed

exploration of several closely related issues,

including strengthening agricultural viability

1|

TABLE OF CONTENTS

PURPOSE....................................................................................................................................................................... 1

TABLE OF CONTENTS ................................................................................................................................................ 2

COLORADO’S AGRIGULTURAL LANDS ARE THREATENED ................................................................................4

CURRENT AGRICULTURAL LAND AND WATER PRESERVATIONS TOOLS IN COLORADO ........................... 7

A. FEDERALLY-LED PROGRAMS......................................................................................................................... 7

FEDERAL PUBLIC LAND GRAZING LEASES AND PERMITS......................................................................... 7

FEDERAL INCENTIVES FOR PRIVATE LANDS ................................................................................................ 8

Agricultural Conservation Easement Program ........................................................................................... 8

Conservation Reserve Program (CRP).......................................................................................................... 9

FEDERAL INCENTIVES FOR KEEPING LAND IN AGRICULTURE THROUGH TRANSITIONS................ 10

USDA FSA Beginning Farmer Loans ............................................................................................................ 10

Federal Estate Taxes....................................................................................................................................... 10

B. STATE-LED PROGRAMS................................................................................................................................. 11

COLORADO LAND BOARD’S AGRICULTURAL LEASES...............................................................................11

STATE INCENTIVES FOR PRIVATE LANDS.....................................................................................................11

Colorado’s Purchase of Agricultural Conservation Easement (PACE) Programs............................... 12

Great Outdoors Colorado............................................................................................................................ 12

Colorado Conservation Easement Tax Credit.......................................................................................... 13

Agricultural Use Property Tax Assessment Rate....................................................................................... 14

STATE INCENTIVES FOR KEEPING LAND IN AGRICULTURE THROUGH TRANSITIONS..................... 15

Colorado Agricultural Development Authority........................................................................................ 15

Colorado’s Beginning Farmer Loan Program and Aggie Bonds............................................................ 16

Beginning Farmer Farm & Equipment Lease Income Tax Deduction Pilot .........................................17

2|

TABLE OF CONTENTS CONTINUED...

C. COUNTY AND MUNICIPAL SUPPORT ........................................................................................................ 18

OPEN SPACE AGRICULTURAL LEASES.......................................................................................................... 18

COUNTY TRANSFER OF DEVELOPMENT RIGHTS PROGRAMS .............................................................. 18

AGRICULTURAL LAND USE PLANNING........................................................................................................ 19

LIMITATIONS OF CURRENT TOOLS....................................................................................................................... 19

A. FINANCIAL LIMITATIONS.............................................................................................................................. 19

B. DATA LIMITATIONS......................................................................................................................................... 21

C. COMPREHENSIVE PLAN LIMITATIONS......................................................................................................22

D. AGRICULTURAL LAND OWNERSHIP AND SUCCESSION LIMITATIONS...............................................22

SUMMARY OF RECOMMENDATIONS ...................................................................................................................23

3|COLORADO’S AGRICULTURAL LANDS ARE

THREATENED KEY THREATS TO AGRICULTURAL LANDS AND

WATER IN COLORADO

COLORADO IS LOSING 15,660 ACRES OF

AGRICULTURAL LAND PER YEAR Colorado is losing 15,660 acres of agricultural

land per year

Colorado currently has 39,534,800 acres of public

and private agricultural lands, of which 62% is The rate & location of agricultural land

rangeland, 20% is cropland, 4% is pastureland, preservation is outpaced by the rate & location

and 9% is woodland.5 Between 2001 and 2016, of is loss

234,900 acres (or, about 15,660 acres per year) were

converted from agricultural uses into residential or The rate of agricultural water preservation is

moderate to high-density commercial/industrial also outpaced by the rate of its loss

use.6 Most of this development is occurring in the Over the last 5 years, public support for

rapidly developing Front Range urban corridor, maintaining land and water in agricultural

which also contains some of the best remaining production has declined

farmland in Colorado. Of the converted farmlands,

48% was considered by the American Farmland Trust Irrigated agricultural land costs 4-6 times more

(AFT) to be Colorado’s best land, which AFT defines than other agricultural land and its value is

as land with high productivity, ability to support increasing 40% faster

production of a wide range of crops, and ability to

adapt to extreme weather.7 Of remaining highly Young and beginning farmers are struggling to

productive farmland, a significant portion resides in find affordable land to start/expand operations

the Eastern Plains region which is facing increasing Farmers, especially young and beginning, are

vulnerability to extreme weather, drought, declining less likely to own their land

groundwater supplies, and development pressure.

One in three Colorado farmers is over 65 and

RATE & LOCATION OF AGRICULTURAL LAND the state’s average farmer age is higher than

CONSERVATION UNABLE TO KEEP UP WITH RATE the national average

AND LOCATION OF LOSS

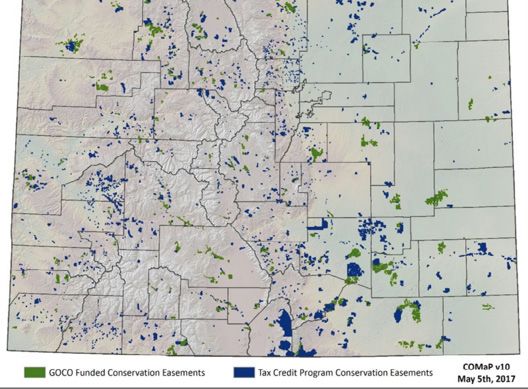

While voluntary incentive-based easements are

not the sole, nor universally acceptable form Grouse.10 However, GOCO support for agricultural

of conservation, a 2017 analysis based on the land conservation is subject to the priorities of the

Colorado Ownership, Management and Protection GOCO Board, which shift over time. Additionally,

Database (COMaP)8 documented that Colorado had conservation organizations and government entities

roughly 2.5 million acres held under conservation have directly purchased agricultural lands for

easements.9 An estimated 2.1 million of those conservation, which may remove opportunities for

acres have been conserved using state funding future private market transactions. For example,

(approximately $280 million from GOCO and $772 federal ownership of Colorado land increased 1.1%,

million from the Colorado Conservation Easement or 261,700 acres, from 1997 to 2017.11

Tax Credit program since 1995); this land includes

1.5 million acres of crucial habitat, 300,000 acres of Aggregate data on these fee simple ownership

prime farmland, 270,000 acres of elk winter range, efforts is not currently available, but taken

4,100 miles of stream, creek, or river frontage, together, it appears conservation

and private lands critical for the Gunnison Sage- efforts have not kept pace with

4|development pressures. The net loss in agricultural speculation laws and to report recommended

land noted above and the locations of protected changes to the Water Resources Review Committee

lands does not always target regions with the by August 15, 2021.14

highest rates of urban development. For example,

current COMaP data shows limited agricultural land OVER THE LAST 5 YEARS, PUBLIC SUPPORT

conservation activity in the Northern Front Range, FOR MAINTAINING LAND AND WATER IN

which is perhaps the most rapidly developing urban AGRICULTURAL PRODUCTION HAS DECLINED

corridor in Colorado12. In the 2016 public attitudes survey about agriculture

RATE OF AGRICULTURAL WATER CONSERVATION in Colorado, 94.8% of respondents indicated

ALSO UNABLE TO KEEP UP WITH RATE OF LOSS that maintaining land and water in agricultural

production was somewhat or very important.15

Working lands conservation strategies in Colorado However, this level of support was down from the

often require ensuring that agricultural water stays previous 5 years, during which as much as 97.6%

with and on the land; this is essential, as these of respondents indicated the same opinion.16 In

irrigated agricultural lands (1) are often the most 2016, the most prevalent “very important” reasons

productive working farms and ranches and (2) for conservation cited by respondents were “Open

provide critical ecosystems for wildlife, as well as raw Spaces/Wildlife Habitat” (62%) and “Food and Fiber

commodities. Water is essential for these functions. Production” (55%). Again such support for all “very

The Technical Update to the Colorado Water Plan important” reasons for conservation had dropped

projects that approximately 450,000 acres of between 2011 and 2016 - “Heritage” remained the

irrigated agriculture could come out of production lowest reason for supporting conservation across all

between now and 2050 due to various water- categories and dropped the most (41%). Supporting

resource management issues including urbanization, conservation for “Jobs” dropped by 35% and for

groundwater sustainability, and planned ag-to-urban “Food and Fiber Production” dropped by 33%.17

water transfers which traditionally involve separating

land and water rights, also known as “buy and dry”.13 IRRIGATED AGRICULTURAL LAND COSTS 4-6 TIMES

The amount of irrigated agriculture anticipated to MORE THAN OTHER AGRICULTURAL LAND AND IS

come out of production due to water-resource INCREASING IN VALUE 40% FASTER

drivers could substantially increase, depending on: According to the USDA Land Values report, the cost

i) decisions by municipalities to continue pursuing of agricultural land in Colorado ranged from a low

traditional water acquisitions, ii) climate change of $845/acre for pasture land, to $1,370/acre of

impacts that may decrease water supply while non-irrigated cropland, to a high of $5,300/acre of

increasing demands, iii) impediments to water irrigated cropland in 2020.18 Additionally, while the

storage projects, iv) curtailing new supplies of water value of pasture land and non-irrigated cropland

that are currently lost to other states, and v) other has increased by about $11/acre per year over the

factors, such as interstate water requirements. With past five years (1.3% annually), the value of irrigated

these water-resource challenges in mind, policy and cropland has increased about 10 times more (e.g.,

programming recommendations will need to reflect $103/acre per year, or 1.9% annually).19 Colorado

the challenges and opportunities of both agricultural data reflects a similar agricultural land trend that is

land and water conservation. The state has already seen across the Kansas City/Tenth Federal Reserve

begun addressing questions around speculative District service area, which includes Colorado,

water and land purchases; Colorado’s Senate Bill Kansas, Nebraska, Oklahoma, Wyoming, the

20-048 established an Anti-Speculation Law Work northern half of New Mexico, and the western third

Group to explore ways to strengthen current anti- of Missouri).20 Importantly, however, land values vary

5|substantially across regions in Colorado. land values, FARMERS ARE LESS LIKELY TO OWN THEIR LAND,

especially in the Front Range and other pockets like ESPECIALLY YOUNG, BEGINNING, AND DIVERSE

Grand Junction, have exceeded these averages and FARMERS

rates of growth.

Nationally, nearly 40% of U.S. farmland is rented or

YOUNG, BEGINNING, AND EXPANDING FARMERS leased.26 Since 1964, the percentage of leased farm

ARE STRUGGLING TO FIND AFFORDABLE LAND TO land has increased slightly (with a peak in the farm

START/EXPAND OPERATIONS crisis of the 1980s and early 1990s).27 Based on 2014

Tenure, Ownership, and Transition of Agricultural

Of Colorado’s 69,032 producers about 31% (e.g., Land (TOTAL) survey data, young farmers under the

21,157) are beginning farmers and about 8% (e.g., age of 35 are most likely to fully-lease their land

5,427) are under 35.21 A 2017 national survey from (about 26% of operators).28 Non-white farmers

the National Young Farmer Coalition found that: are also substantially less likely to own farmland.

“land access was the number one challenge faced In 2012–2014, across the U.S., white people

by young and beginning farmers and ranchers. owned 98% and operated 94% of all farmland.29

Importantly, in this survey, 39% of respondents who Unfortunately, updated national data have not been

are current farmers cited land access as a significant published since 2014 and Colorado specific data

challenge, with 17% calling it the most significant is not available due to USDA ARMS30 protocols

challenge they face. Both first-generation and intended to protect producers’ privacy. While land

multigenerational farmers cited land access as their ownership can be an important tool for long-term

top challenge.”22 stability, stewardship, and wealth building, it is

Young and beginning farmers and ranchers most important to note that leasing land - particularly

often start and grow their business operations for young and beginning farmers- can enable them

through Direct to Consumer (DTC) marketing like to be more nimble and more quickly pivot their

Community Supported Agriculture (CSAs) and production and/or business models.

farmers markets.23 Research suggests that DTC ONE IN THREE COLORADO FARMERS IS OVER 65

marketing, however, is most effective for farms AND THE STATE’S AVERAGE AGE OF FARMER IS

within 25 miles of their customers24 - a considerably HIGHER THAN THE NATIONAL AVERAGE

shorter distance than previously assumed.25 Given

land prices and development pressures near urban According to Colorado’s state demographer, one in

and other population centers, young and beginning three producers were over 65.31 In the most recent

direct market farmers often face additional barriers data available, the average farmer in Colorado was

to accessing land closer to their markets. 57.6 years old, slightly above the national average

age of the American farmer: 57.5. Importantly,

Additionally, young, beginning, and expanding succession between farm owners appears to be

farmers seeking to expand their operations often happening faster in Colorado than in other states, as

seek larger parcels of land further from population nationally the average age of the American farmer

centers. These lands are also important targets for increased 1.2 years from 2012 to 2017, whereas

conservation in order to support the wide diversity the average age of farmers in Colorado actually

of scales, production attributes, and aspirations of decreased 1.3 years from 2012 to 2017. Regional

current and future farmers and ranchers. Colorado variation on the age of farmers likely exists in

specific information about land access needs for Colorado, but data are not currently available.

young, beginning, and expanding farmers, however,

is not currently available from state, university, or Despite what appears to be an increased frequency

nonprofit partners. in farm succession in Colorado, information about

6|familial and non-familial farm succession/transitions “to represent the fair market value of grazing to

specific to Colorado, including data on prevalence, the livestock owner”.36 Over the past 20 years, the

frequency, geography, cause, and/or “success rates” fee has ranged from $1.35 to $2.11 per animal unit

is not currently available from state, university, or month (AUM), but has been $1.35/AUM from 2019

nonprofit partners. The Colorado Department of through 2021.37 Fees are also shared with state and

Agriculture is, however, currently “gathering data local governments, though Colorado only received

specific to Colorado this year as part of [their] $79,107 from BLM FY2019 leases.38

outreach and education.”32

The NSF39 in 2016 (the most recent data available

CURRENT AGRICULTURAL LAND AND online) supported 633 permittees in Colorado and

WATER PRESERVATION TOOLS IN authorized 809,861 head months (HMs). In 2019

(as most recently documented), the BLM supported

COLORADO 1,278 unique users and authorized 269,564 animal

Agricultural land and water conservation in Colorado unit months (AUMs). The BLM data does suggest

is supported by important programs led by the a slight decline in unique users (-0.54%) and a

federal, state, and local governments. potentially substantial decline in authorized AUMs

(-11.72%) compared to the prior year, but more

A. FEDERALLY-LED PROGRAMS research is needed to explore these trends over

time. To note, animal unit months (AUMs) and head

The federal government primarily supports months (HMs) are treated as equivalent measures for

agricultural land and water conservation through determining fees; these indicators reflect land use

offering grazing leases on public lands, financially by one cow and calf, one horse, five sheep, or five

supporting agricultural conservation easements, goats over one month. Allocations of AUMs/HMs are

providing beginning farmers loan programs, and based on rangeland conditions and can decline due

structuring estate taxes to avoid unintentionally to drought pressure.

forcing the sale and division of agricultural property

to meet estate tax requirements. There are, however, multiple limitations to the

efficacy of federal grazing permits and leases in

FEDERAL PUBLIC LAND GRAZING LEASES AND meeting the state’s agricultural land conservation

PERMITS needs. Federal public land grazing leases and

The total land area of the state of Colorado is over permits are limited to rangelands that support

66 million acres and 36% is owned by the federal animal agriculture and, thus, do not apply to

government.33 Specifically, about 22% of Colorado rangelands for cropping or other mixed production

land is part of the National Forest System and an practices. This limitation exists partially because

additional 13% is administered by the Bureau of Land most public leases prohibit, or substantially limit,

Management.34 See Table 1 for more detail. any on-site infrastructure development (e.g.,

irrigation systems, fixed foundation sheds, etc.).

Both the National Forest System (NFS) and Bureau Public lease termination can also be politically and

of Land Management (BLM) administer agricultural administratively complex, and there can be a lot of

lease programs important to agriculture in Colorado. uncertainty and logistical barriers for farmers and

For example, BLM reports that grazing on its ranchers when moving between consecutive lease

lands created $142M in economic contributions agreements.

and 2,077 jobs in FY 2018.35 Grazing permits and

leases generally cover a 10-year period and are There are concerns that, in general, land

typically renewable. Grazing fees are set annually leases are not conducive to best

practices for long-term agricultural

7|land conservation (i.e. leases may facilitate An agricultural conservation easement (ACE) is an

temporary thinking that can motivate tenants elective, legally recorded deed restriction placed on a

to maximize shorter-term economic benefits property that prohibits practices that would damage

and utilize more ecologically harmful farming or interfere with the agricultural use of the land, such

practices).40 However, federal agricultural land as commercial or residential development45. As the

leases actually stipulate conservation agricultural easement is a restriction on the deed of the property,

practices as part of each lease41. For example, each the easement remains in effect even when the land

10-year grazing lease includes a resource-based changes ownership.46 ACEs can be controversial as

management plan that is developed in accordance they are permanent for both current and subsequent

with a National Environmental Policy Act (NEPA) owners, which can reduce the full market value of

assessment (conducted every 10 years) and that a specific property. However, the lower costs of

establishes lease criteria while taking into account conserved agricultural land can be helpful in keeping

other surrounding land uses. The resource-based the cost of farmland more affordable for young,

management plan is implemented through annual beginning, and expanding farmers.

operating instructions which further dictates

In order to compensate the landowners for selling

amount of use, season of use, management

certain development rights on their land, ACE

practices, etc. along with providing considerations

programs seek to pay landowners based on the

of other species, riparian, invasives, fire, etc. These

difference between the land’s current “highest and

grazing leases are extremely valuable assets that

best use,” which is often residential or commercial

banks loan against. Additional fees, fines, or loss

development, and the value of the land after the ACE

of lease may occur if the lease agreements are not

and the restricted development rights are in place.

followed.

The landowner can sell or donate an easement to the

FEDERAL INCENTIVES FOR PRIVATE LANDS easement holder, or a combination of the two (e.g., a

“bargain sale”).47

The federal government also seeks to support

private landowners in conserving the quality, Agricultural conservation easements aim to ensure

viability, and use of agricultural lands. Two land is primarily devoted to active, agricultural

important tools used in Colorado are the Federal production and is not subject to development

Agricultural Conservation Easement Program pressures.48 ACEs are also specifically written to

(ACEP) and the Federal Conservation Reserve allow agriculture uses and farm structures, but to

Program (CRP). limit other types of on-site construction and physical

development.

Agricultural Conservation Easement Program

Ironically, the more valuable agricultural production

The Agricultural Conservation Easement is on a parcel, the lower the potential conservation

Program - Agricultural Land Easement (ACEP- easement compensation, ceteris paribus, as

ALE) program is administered by the National agricultural value (value in use) approaches the real

Resources Conservation Service (NRCS) of the U.S. estate (best and highest use) value. This limits the

Department of Agriculture.42 Under the ACEP-ALE, efficacy of ACEs in conserving the highest value

NRCS may contribute up to 50% of the fair market agricultural lands. This issue underscores a core

value of an agricultural conservation easement43 limitation of ACEs as a tool - easement programs

or may contribute up to 75% of the fair market are focused on reducing development, not explicitly

value for easements where grasslands of particular on conserving agriculture. Certainly revenues

ecological importance will be protected.44 from the sale of a conservation easement

may be important for farmers and

8|ranchers as income or as a means to defer capital equal in the application process.57 The Natural

gains taxation. The proceeds may also allow retiring Resources Conservation Services prioritizes land that

farmers/ranchers to fund his/her retirement which already protects agricultural uses and implements

may indirectly benefit the successor(s). But, overall, conservation practices for ACE selection over those

these outcomes are not the primary motivation of lands that don’t already do so.58 Land must also

easement policies and programs and this lack of be large enough and characteristically suitable

alignment leaves gaps that may need to be filled by for commercial agriculture to be considered for

new tools that are specifically focused on conserving selection.

agriculture itself.

Additionally, landowners report discomfort with

While providing immediate liquidity for the the perpetual nature of ACEs, as well as reluctance

landowners, ACEs can be controversial because the for any perceived external management of their

purchase of an ACE can trigger federal and state land.59 Skepticism of government influence and

capital gains taxes, which diminish the immediate unfamiliarity with conservation organizations

cash opportunity. Some landowners, however, also appears to discourage landowners’ ACE

are able to defer capital gains taxes by using the participation.60

proceeds to acquire additional land (using a like-kind

1031 exchange49). Conservation Reserve Program (CRP)

Between 2009 and 2017, approximately 122 parcels The Conservation Reserve Program (CRP) is

of land in Colorado were enrolled in a federal administered by the Farm Service Agency (FSA) of

agricultural conservation easement program.50 the U.S. Department of Agriculture. Under CRP,

Across this time, easement payment facilitated the FSA provides farmers and ranchers with annual

changes in agricultural practices by 32% of rental payments and cost-share assistance, in

participants.51 Such changes included improved exchange for removing environmentally sensitive

irrigation, increased acreage, and adjusted crop lands from agricultural production and planting

mix and rotation.52 Researchers also found that environmentally restorative species. CRP helps to

easement participation was correlated with conserve land and natural resources, but, as it takes

increased crop yields and facilitated the addition land out of production, it does not directly support

of outdoor recreation to agricultural operations.53 food production. Contracts under the Conservation

A press release about a recent study by Colorado Reserve Program are voluntary and last 10-15 years.

State University54 highlighted that “if $88.9 million Primarily, the CRP aims to improve water quality,

in federal ACEP payments (the estimated current prevent soil erosion, and reduce loss of wildlife

need for active conservation projects in Colorado) habitat through incentivizing farmer collaboration.

were secured, this funding would generate up to 20.8 million acres are currently enrolled in the

$195 million in economic activity and create more Conservation Reserve Program and the maximum

than 1,200 jobs in Colorado”.55 The research also acreage that can be enrolled is 25 million. However,

estimated that up to 80% of the resulting economic the CRP acreage enrollment cap will rise to 27

activity would directly benefit rural communities, million acres in 2023.61 Overall, CRP participation

further highlighting the essential role of the state has shrunk substantially to 9.7 million hectares (24

in helping to attract and capture federal dollars to million acres) in 2017 down from its high of 14.9

benefit Colorado communities.56 million hectares (36.8 million acres) in 2007.62

While rangeland, cropland, pastureland, grassland, While CRP may help farmers improve their

and nonindustrial private forest land can be eligible conservation practices and generate sustainable

for ACE programs, not all land is considered revenues on their lands, CRP is not a permanent

9|solution for agricultural land and water conservation. Over the past 4 years in Colorado, USDA FSA

Research on CRP has also found limited effects Beginning Farmers Loans have helped 361 beginning

on rural economies63 and that its payments may farmers acquire farm/range land and assets worth

not adequately capture the program’s ecological more than $95.5M73. See Table 2

benefits.64

There are also some critical limitations to the FSA

FEDERAL INCENTIVES FOR KEEPING LAND IN Beginning Farmer Loan program including limiting

AGRICULTURE THROUGH TRANSITIONS eligibility for who can qualify as a “new farmer” to

those who have not (1) owned a ranch or farm bigger

As noted above, transitions between agricultural land than 30% of the average U.S. farm, according to

owners represent a critical risk to agricultural land the current Census for Agriculture, and (2) have not

conservation in Colorado. The federal government operated a ranch or farm for more than a decade.74

primarily supports agricultural land transitions by (1) Applicants must also be heavily involved in the

underwriting Beginning Farmer Loans to help new operation.75 Additionally, loan value limits can create

farmers and ranchers access agricultural land and barriers to accessing affordable land when supply

(2) crafting estate tax rules to ensure heirs are not is limited and competition is increasing from well-

unintentionally forced to sell all or part of the family financed, non-tenant investors.

farm to meet inheritance tax obligations.

Federal Estate Taxes

USDA FSA Beginning Farmer Loans

Enacted in 1916, the federal estate tax76 is a tax

The U.S. Department of Agriculture’s (USDA) Farm on property (e.g. stock, real estate, cash, etc.)

Service Agency (FSA) makes and guarantees loans transferred from deceased persons to their heirs.77,78

to beginning farmers.65 Beginning farmer loans aim The tax is applied to the full value of the estate and a

to make it more financially possible for new farmers credit is applied to the tax liability, and it is currently

to start building new farms, especially as such new $11.7 million for individuals and $23.4 million for

farmers are not yet eligible for commercial loans.66 married couples.79 Between 2000 to 2020, the

Beginning farmer loans can be disbursed as a micro highest marginal estate and gift tax dropped from

loan or be specifically intended to facilitate farm 55% to 40%.80

ownership or operation.67 The FSA also provides

down payment loans to help new farmers purchase High exemption levels, estate and succession

a farm and to help transfer farmland from a retiring planning tools, and transfers of asset ownership

farmer to the next generation of farmers.68 before death ensure that the estate tax impacts

less than 1% of estates across the U.S.81 In 2020,

The USDA also extends Farm Ownership Loans to approximately only 0.6% of farm estates were

help farmers (1) expand an existing farm, (2) buy required to file an estate tax return, with only

a new farm, (3) cover closing costs, (4) integrate 0.16% of estates that filed accruing any estate tax

water & soil conservation and protection measures, liabilities.82 From that 0.16%, approximately $130.2

and (5) improve farm structures and build new farm million was collected in federal estate tax liabilities in

buildings.69 In 2020, farmers could access financial 2020.83

assistance through microloans or direct loans of up

to $600,000 (this number is adjusted annually).70 In Over time, the estate tax has been further adjusted

2020, the Farm Service Agency also guaranteed up to minimize its economic burden on farmers and to

to $1,776,000 in farm ownership loans through a encourage the transfer of farms from one generation

commercial lender.71 Farmers have up to 40 years to to the next. For example, provisions

repay for both of these loan options.72 encourage farmers and landowners

10 |to donate easements or other restrictions for estate 1876 to manage lands that the federal government

tax savings.84 Similarly, parts of the Internal Revenue provided to the state in public trust.92 The CLB is the

code allow agricultural real estate to be valued at second largest landowner in Colorado, owning 2.8

farm-use value, rather than its fair-market value. million surface acres.93

There are, however, restrictions and limitations to

valuing agricultural land at farm-use value. Lastly, The CLB owns, manages, sells, and leases publicly-

the estate tax also encourages agricultural land to owned land primarily to raise funds for Colorado

be passed down across generations by omitting farm public schools94 with two focal areas: (1) creating

real-estate value appreciation.85 consistent and satisfactory income over time,

and (2) providing reliable stewardship of the state

Some remain concerned, however, that estate taxes trust property.95 Lease payments have raised $1.7

may unintentionally encourage some farmers to billion since 200896 and the Colorado Land Board

sell their land and may also discourage farmers is entirely self-funded by its own revenue.97 Most

and ranchers from investing in the growth of their of the Land Board’s revenue is disbursed to the

agricultural businesses.86,87 so as to minimize tax Colorado Department of Education’s Building

liabilities and shore up reserves to cover anticipated Excellent Schools Program (BEST)98 though a portion

estate tax expenses.88,89 of its revenue is also invested in the Colorado

Department of Education’s annual operating

Additionally, the Internal Revenue codes that budget.99

pertain to estate and gift taxes may be changed

in the coming months. The Biden administration While not primarily focused on agricultural land

and some Congressional leaders are proposing (1) conservation, the CLB leases 98% of its 2.8 million

discontinuing portability, (2) calculating capital gains acres for agriculture via a combination of grazing,

taxes at the time of asset transfer, (3) lowering the irrigated farming, and dry land crop production

federal estate tax exemption level from $11.7 million leases.100 The Colorado Land Board also leases land

to $3.5 million, and (4) eliminating the step-up in for a variety of other uses, including commercial real

basis on death and the transfer of basis in the case of estate, mining, recreation, agriculture, ecosystem

gifts.90,91 However, it remains unknown when these services, renewable energy, oil and gas, rights-of-

proposals will be signed into law, as well as when way, water, tower sites.101 These multiple types of

they might take effect. leases, combined with the CLB’s prioritization of

revenue creation, sometimes render agricultural

B. STATE-LED PROGRAMS land conservation unrealistic or incompatible with

The state government primarily supports agricultural competing land uses.

land and water conservation through offering Importantly, and unlike federal lands, some

agricultural leases on public lands, financially state agricultural leases allow cropping or other

supporting agricultural conservation easements, mixed production practices, in addition to animal

administering beginning farmers loan programs, agriculture. Additionally, the CLB promotes

and structuring property taxes to reduce recurring conservation practices by explicitly requiring

expenses on agricultural lands. that lessees adhere to “strict land stewardship

COLORADO LAND BOARD’S AGRICULTURAL LEASES guidelines.”

In accordance with the U.S. Congress’ Northwest STATE INCENTIVES FOR PRIVATE LANDS

Ordinance of 1785, the Colorado Land Board (CLB) Similar to the federal government, the

was established by the Colorado Constitution in state also seeks to support private

11 |landowners in conserving the quality, viability and water conservation initiatives through several

and use of agricultural lands through the direct grant programs. CWCB targets funding for land

Purchase of Agricultural Conservation Easement conservation projects with significant water resource

Program (PACE) programs. The state also offers co-benefits such as the conservation of riparian and

the Colorado Conservation Easement Tax Credit wetland areas and protecting irrigated agricultural

program to incentive conservation when the full lands from water resource development. Through

purchase amount of an easement is not available the CWCB Alternative Transfer Method Grant

and seeks to reduce recurring property tax expenses Program, CWCB has also supported the coupling

for agricultural lands through a reduced agricultural of conservation easements with temporary water

assessment rate. leasing arrangements that keep water in agriculture

while also allowing water to be leased or shared for

Colorado’s Purchase of Agricultural Conservation other uses.

Easement (PACE) Programs

Colorado is one of 30 states with a Purchase

of Agricultural Conservation Easement (PACE)

Program.102 Nationwide, PACE programs help pay

landowners for keeping their land in agriculture.

PACE programs work by purchasing the

development rights from land owners (which is why

they are sometimes called Purchase of Development

Rights, or PDR, programs) using a tool called an

agricultural conservation easement (ACEs). ACEs are

described in detail above. Colorado has one of the

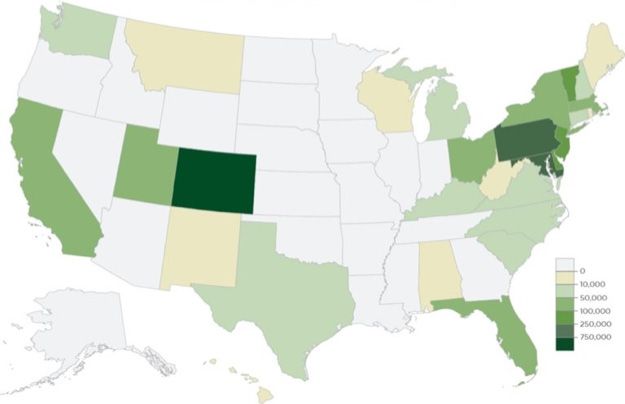

most successful PACE programs in the nation, with

over 872,167 acres protected as of January 2020103

and state investments in ACEs have conserved

almost 300,000 acres of prime farmland.104 Image 1: Acres of Farmland Protected by State, as of January 2020 -

Source: American Farmland Trust, November 2020105

Colorado’s PACE programs are primarily funded by

Great Outdoors Colorado (described in detail in the

following section), but the Colorado Department of Great Outdoors Colorado

Natural Resources (DNR) and Colorado Parks and Colorado’s Purchase of Agricultural Conservation

Wildlife (CPW) also provide some direct funding Easement (PACE) Program is funded in large part

for the purchase of specific types of ACEs. CPW, by Great Outdoors Colorado. Created through a

for example, manages the statewide Colorado Colorado Constitutional amendment in 1992, the

Wildlife Habitat Program (CWHP), which offers Great Outdoors Colorado (GOCO) Program is a

opportunities for private landowners to voluntarily trust fund (housed in the Treasury of the State of

protect important wildlife habitat, and provide Colorado106) and is completely funded by redirected

wildlife-related recreational access to the public. lottery proceeds107.

CWHP is an incentive-based, voluntary program that The Great Outdoors Colorado Program aims

accomplishes strategic wildlife conservation and to conserve, protect, enhance and manage the

public access goals using conservation easements, state’s park, trail, wildlife, river, and open space

and in some cases, fee title purchases. The Colorado resources108 and, over the past 29 years, has

Water Conservation Board (CWCB), as part of the committed more than $1.3 billion

DNR, also provides financial support for private land to over 5,300 projects in all of

12 |Colorado’s 64 counties.109 Counties, municipalities, on available dollars and the wide range of eligible

Title 32 special districts with parks and recreation grantees, there is significant competition for GOCO

authority, Colorado Parks and Wildlife, and political funds. Additionally, GOCO requires a minimum

subdivisions of the state are eligible to receive 50% match for its easement program, which in

GOCO funds.110 These entities can also obtain effect requires that all other sources of support will

GOCO funding on behalf of foundations, nonprofits consistently match or exceed GOCOs contributions.

that are not land conservation organizations, school GOCO priorities have shifted over time, but more

districts, business owners, private landowners, and research is needed to understand how agricultural

community groups and volunteers.111 land conservation has trended in terms of deal

volume and incremental conserved acres/dollars in

To date, GOCO has helped partners across the state recent years.

protect 1.2 million acres of open space112 and added

66,200 acres to the State Parks system.113 Since Colorado Conservation Easement Tax Credit

2015, GOCO also invested $44.5 million in 11 large-

scale projects that conserved 130,063 acres of land, In addition to the outright purchase of agricultural

which included both working cattle ranches and conservation easements (ACEs), 14 states, including

agricultural lands.114 Colorado, offer tax incentives for conserved land.116

These tax incentives are particularly critical when

PACE programs are not able to pay for the full value

of the ACE as they help landowners recapture the full

value of their land.

In Colorado, the program aiming to financially

incentivize the enrollment of land into conservation

easements is called the Colorado Conservation

Easement Tax Credit.117 First established in 1995,

the Colorado Conservation Easement Tax Credit

program facilitates the enrollment of private lands

into ACEs through the buying and selling of income

tax credit certificates.118 The Conservation Easement

Oversight Commission and the Director of the

Division of Conservation (housed within the Colorado

Department of Regulatory Agencies) verifies the

tax credit certificate applications, ensures the

conservation easement donations meet qualification

Image 2: Acres Conserved by GOCO and the Conservation Easement Tax appraisal requirements, and fulfils the Internal

Credit Program - Source: INVESTING IN COLORADO: Colorado’s Return

on Investments in Conservation Easements: Conservation Easement Tax Revenue Code’s 170(h) stipulations for a qualified

Credit Program and Great Outdoors Colorado115 conservation easement donation.119 Despite such a

rigorous screening system, the Colorado Department

of Revenue may still reject a tax credit claim due to

GOCO is constitutionally required to allocate its tax compliance concerns.120

funds equitably across multiple priorities: wildlife,

local governments, open space, and outdoor Currently, tax credit certificates reimburse

recreation, as well as youth outdoors engagement, landowners for 75% of the first $100,000 of donated

which further reduces the priority of using funds land value and 50% of the remaining donated

for agricultural land conservation. Given limitations value, up to a maximum of $5 million

13 |per conservation easement donation.121 Credits $220 million in back taxes from landowners.129

greater than $1.5 million are disbursed in increments Additionally, confusion about how certain business

of up to $1.5 million per year in future years.122 entities may claim the credit130 and other nuances,

Landowners can sell such tax credit certificates to any led to instances in which Colorado taxpayers

Colorado taxpayer at a discount through a Tax Credit received a federal income tax deduction for a

Connection entity.123 Buyers then use the tax credit conservation easement donation, but were denied

certificate to save money on their own income tax state income tax credit for the same donation.131

liabilities.124 Pending Colorado legislation may shift Lastly, when landowners abandon conservation

some of these program parameters; one such bill is easements, there are limited guidelines related to the

HB21-1233, which has been passed by the legislature outcomes of the state tax credits.132

but awaits Governor Polis’ signature.125

SB20-135 introduced a series of solutions created by

Since its inception, the Colorado Conservation the conservation easement working group convened

Easement Tax Credit program has helped Colorado in accordance with HB19-1264, but was postponed

conserve over 1.2 million acres, including 102,943 indefinitely once the legislature reconvened after

acres for agriculture.126 See Table 3. the COVID-19 outbreak.133 SB21-033, which again

sought to implement the conservation easement

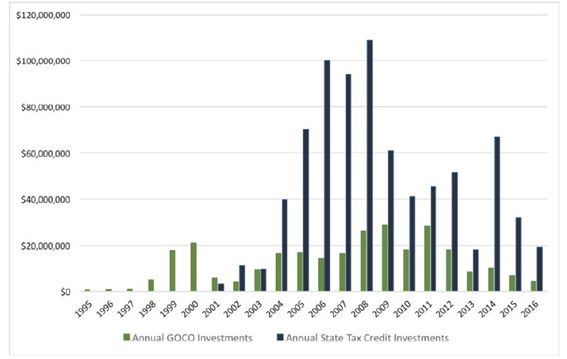

Overall, as shown in Image 3, the value of tax working group’s recommendations, failed to get to

credit investments has far exceeded that of GOCO a vote on the House floor of the Colorado General

investments. Assembly.134

Agricultural Use Property Tax Assessment Rate

Perhaps an often overlooked tool in maintaining

the economic viability of agriculture is reducing

recurring property taxes for agricultural use.

Property taxes and assessment rates are designed

to promote optimal use of land resources and to

equitably distribute the land tax burden across

all property owners.135 Property tax assessments

assume that the property is used in its best and

highest use.136 Property tax revenue funds stay

within its respective county, funding county and

municipal governments, special districts, public

schools, junior colleges.137 No portion of property

Image 3: Colorado’s Investments in Conservation Easements through taxes are diverted to fund state services.138

GOCO and the Conservation Easement Tax Credit Program, 1995-2016 -

Source: INVESTING IN COLORADO: Colorado’s Return on Investments in

Conservation Easements: Conservation Easement Tax Credit Program and Agricultural land has a significantly lower tax burden

Great Outdoors Colorado127 than residential or commercial properties,139 as

both residential and commercial property are valued

However, the Colorado Conservation Easement Tax according to the market.140 Agricultural land is taxed

Credit program has not been without controversy. according to its earning or productive capacity,141

Between 2000 and 2013, calculations of the Colorado and is capitalized at the statutory rate of 13%.142

Conservation Easement Tax Credit were challenged128 The earning capacity of agricultural land is

and led to that state seeking approximately evaluated by multiplying the 10-year

14 |average price of the grazing or commodity rate agricultural land conservation could be similarly

by the yield correlated with the property’s soil unappealing for farmers.154

classification. That figure is then multiplied with

the landlord’s typical crop share to produce the In the past, researchers have characterized various

landlord’s gross income.143 Next, the 10-year state approaches to the income capitalization

average of the landlord’s typical expenses are methods as inconsistent, not transparent,

subtracted from the landlord’s net-income to arrive excessively complex and ad hoc.155 Researchers

at the landlord’s net income.144 This net income also recommend that capitalization computation

is capitalized by the statutory 13% to produce the methods should account for default risk, liquidity

valuation of the land’s actual value.145 Such actual constraints, inflation and maturity risk.156

value is multiplied by the agricultural assessment STATE INCENTIVES FOR KEEPING LAND IN

rate (currently 29%) to obtain the land’s assessed AGRICULTURE THROUGH TRANSITIONS

value.146

The state of Colorado also helps to keep farming

Residential property on agricultural land is assessed economically viable by smoothing the transitions

by its market value and according to a separate, between owners of agricultural land. The state

residential assessment rate.147 Agricultural government primarily supports these agricultural

structures utilized for agricultural production land transitions through a beginning farmer loan

are valued typically according to cost, and the fund administered by the Colorado Agricultural

actual value of the structures is multiplied by the Development Authority (CADA).

statutory 29% assessment rate.148 Agricultural

equipment used primarily to create profit from Colorado Agricultural Development Authority

food production, as well as livestock, supplies, and

agricultural & livestock products, are exempt from The Colorado Agricultural Development Authority

taxation.149 (CADA) was statutorily established in 1981 as

an independent state entity.157 Its creation was

A three-year process is required to determine if also enabled through Title 26 of the U.S. Federal

a plot of land statutorily qualifies as agricultural Statute.158 CADA is governed by seven board

land.150 members: one appointed by the Governor, three

by the Speaker of the House, and three appointed

Agricultural tax assessment rates are designed by the President of the State Senate.159 The

to reduce property tax burden for ranchers Commissioner of Agriculture also serves on the

and farmers, so as to facilitate the economic Board as a non-voting member.160

viability of agriculture.151 Additionally, agricultural

assessment rates are also intended to protect the Currently CADA oversees the state’s beginning

environmental benefits of agriculture and also to farmer loan program (explored in more detail

discourage commercial, residential or industrial below). Historically, CADA also administered the

development of agricultural land.152 states value added development grants161 and a

3-year pilot of the state’s farm lease income tax

While farming produces a number of ecological deduction program (also, explored in more detail

benefits beyond crop commodities (e.g., below), but both of those programs are currently

wildlife habitat, amenity value, etc.), monetarily idle due to a lack of resources.

incorporating these benefits would be difficult

and would raise the assessed value and minimize

the property tax preference placed on agricultural

land.153 Incorporating the economic benefits of

15 |Colorado’s Beginning Farmer Loan Program and

Aggie Bonds

Colorado’s General Assembly established the

Colorado’s Beginning Farmer Loan Program, Colorado Housing and Finance Authority in

administered by The Colorado Agricultural 1973, to address the shortage of affordable

Development Authority (CADA), is a federal-state housing in the state. In 1982, CHFA’s mission

partnership enabled by the federal Aggie Bond Loan expanded to include loans to businesses.

Program which began in 1980.162 Colorado is one Today, CHFA serves a dual mission, 1) increase

of approximately 16 states that use this tax-exempt, the availability of affordable, decent and

beginning farmer agricultural development bond accessible housing for lower- and moderate-

program.163 income Coloradans, and 2) strengthen

the state’s economy by providing financial

Importantly Aggie Bond programs fall under the assistance to businesses.

broader umbrella of federal Public Activity Bonds

(PABs) and are subject to the federal government’s

tax-exempt Private Activity Bond Cap authorization

With its allocation of PABs, the Colorado Agriculture

for each state each year.164 For example, in 2020,

Development Authority issues tax-exempt bonds

the State of Colorado was authorized $604,667,000

to private investors and then uses bond proceeds

(equal to $105 per resident).165 The state uses

to assist first time ranchers and farmers with the

revenue from the sale of these bonds to support

purchase of equipment, land, and other capital

a range of investments including infrastructure,

expenditures.171 Since these bonds are tax-exempt,

affordable housing and economic development

their interest rates are typically up to 2% below

projects. In addition, Colorado law requires that

commercial farm rate.172

up to 50% of the annual PAB authorization goes

to local authorities—counties and cities—with a Beginning farmer loans created using Aggie Bonds

minimum population of 19,048 residents.166 This are, however, subject to substantial restrictions

population requirement immediately excludes 80% from the federal government, the state authority,

of Colorado’s rural counties as only 11 out of 53 and each specific lender.

rural counties qualified for direct PAB allocation

authorizations in 2020.167 Counties that receive Federal rules, under the guidelines established

PAB authorization allocations have the choice by the Agricultural Bond Improvement Act,173

of: 1) using their bond authorization on qualified approved in 2005, limit the maximum funds each

programs, 2) assigning their authorization to applicant is eligible to receive, indexed to the

another local issuer, 3) assigning their volume cap rate of inflation, which in 2020 established the

to the Colorado Housing and Finance Authority loan ceiling at $552,500. Additionally, the Internal

(CHFA), or 4) doing nothing, at which point the cap Revenue Code (IRC) has established a $62,500 cap

will revert back to the Colorado Department of on the amount allowed for use on used equipment

Local Affairs (DOLA) to be included in the statewide purchases. Federal requirements also stipulate

balance for future allocation.168 At this time, that a “first-time farmer” (and also, a “first-time-

counties are not able to assign their excess volume rancher”) is defined as any individual who has not

cap to CADA.169 at any time had direct or indirect ownership of, and

material participation in, “substantial farmland,”

Per state law, the remaining 50% of the total PAB and who has not received more than $250,000

allocation is further divided, with 48% going to the in tax-exempt financing, including any proposed

Colorado Housing and Finance Authority (CHFA), financing. In this case “substantial farmland” means

and 2% going to the CADA.170 any parcel of land unless: it is smaller than 30%

16 |of the median size of a farm in the county where Colorado’s Beginning Farmer Loan Program

it is located, and the value of the land does not reflects these findings, with 6 loans for $1,040,000

exceed $125,000. Importantly, first time farmers disbursed to beginning farmers and ranchers in

and ranchers can combine funding from Colorado’s 2020176 and 27 loans awarded over the past three

Beginning Farmer Loan Program with the U.S. years (2017 – 2019) for an additional $7.5MM

Department of Agriculture’s (USDA) Aggie Bond dispersed to qualified applicants (an average of

program, operated by the Farm Service Agency. $260,000 per loan). As of December 31, 2020, 390

However, under the current Internal Revenue Code, loans for a total of $62,151,909.34 have been made

section 147(c)(2), first-time farmer bonds cannot to individual borrowers over the full life of the

be aggregated under a single ownership in order to program.177

purchase large blocks of land.

Personal communications with CADA confirmed

State rules, under the Colorado Agricultural that maps of loan locations were not available, nor

Development Authority, further restrict who can was information by county or by producer type.178

receive beginning farmer loan support. However, CADA reported that “the vast majority of

bonds were to assist farmers in eastern Colorado, as

Also, these bonds are dispersed through a three- unfortunately the cost of land along the front range

way transaction between the borrower, lender and in western Colorado often prohibits farmland

and CADA,174 where the lender provides all of purchases by first time farmers.”179

the capital and bears all of the associated risk.175

Accordingly, the beginning farmer loan program Beginning Farmer Farm & Equipment Lease Income

requires that borrowers: (1) independently qualify Tax Deduction Pilot

with a lender; (2) be a resident of Colorado; and

(3) actively involved with agricultural production While no longer active, the Colorado Agricultural

on the land they seek to buy. Since the liability for Development Authority (CADA) also administered

this federally insured program rests entirely with Colorado’s Beginning Farmer Farm Lease Income

the lender, banks or others that take part in this Tax Deduction pilot program. Colorado Beginning

program must assess a borrower’s credit history Farmer Tax Deduction was designed to encourage

and ability to meet down payment requirements. private land owners to lease agricultural land and

For new producers entering into farming and other assets to new farmers and ranchers using a

ranching, an income and credit review can create personal and corporate state income tax deduction.

one of many potential barriers to entry. As established by HB16-1194,180 taxpayers that

rented an agricultural asset (e.g. livestock, land,

Overall these restrictions contribute to the crops, farm equipment, grain storage, or irrigation

successes attributed to Aggie Bond programs. equipment) to a beginning farmer or rancher for at

According to a whitepaper published in the Journal least three years qualified for the 20% deduction.181

of Agricultural and Applied Economics (JAAE),

“the proportion of beginning farmers who are full The program was a pilot that provided tax

land owners is 2.5% higher in counties of states deductions beginning in the years after 2017 and

with Aggie Bond programs than in those without, before 2020.182 While more than one deduction

and on average, beginning farmers operated certificate could be offered to a qualified taxpayer,

143.3 more acres in the program counties... .” The the related possible deductions were limited to

authors of the JAAE study further state, “We find no more than $25,000 per taxpayer, per year.183

limited evidence that the program may have led to Additionally, the taxpayer was required to lease

a greater Proportion of Full Land Ownership and to a beginning farmer or rancher who: (1) resided

greater Acres Operated... .” in Colorado; (2) farmed or ranched full-time; (3)

17 |You can also read