1H FY2021 Business Results

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

1H FY2021 Business Results

Sumitomo Life at a Glance Company Overview Group Overview 6 ◼ Established: May 1907 Life Insurance Insurance Outlets Key Figures1 – 1H FY2021 (as of Sep. 2021) Medicare Life Domestic Insurance ◼ Premium income: JPY 1.17tn (USD 10.5bn) ◼ Sells simple and affordable (JPY 2.41tn in FY2020) products through banks and outlets Izumi Life Designers / ◼ Core business profit2: JPY 184.0bn (USD 1.6bn) ◼ 100% subsidiary INSURANCE DESIGN / Agent Insurance Group / (JPY 357.0bn in FY2020) Small-amount and Mycommunication Short-term Insurance ◼ Total assets: JPY 42.004tn (USD 375.3bn) AIARU Small Amount ◼ Also sell other insurers’ products & Short Term Insurance ◼ Ownership: 100% / 95% / ◼ Annualized premiums from JPY 2.84tn (USD 25.4bn) ◼ Owns 99.84% of the shares 44.83% / 43% policies in force3: ◼ Solvency margin ratio: 919.6% U.S. China ◼ Embedded value4 (EEV) : JPY 4.79tn (USD 42.8bn) Symetra Financial Corp PICC Life ◼ Life insurance group ◼ Life insurance JV with ◼ Number of sales 35,314 operating businesses PICC Overseas representatives: across the U.S. ◼ Owns 10% of the ◼ 100% subsidiary since shares ◼ Insurer financial strength A+ [S&P], A1 [Moody’s], February 2016 rating5: AA- [R&I], AA- [JCR], A+ [Fitch] Vietnam Indonesia Singapore Aviva Singlife Holdings ◼ Holding company with Aviva Source: Company disclosure Baoviet Holdings PT BNI Life Singapore, one of the largest 1. Consolidated figures. USD amounts in parentheses in this presentation (except as otherwise stated) are ◼ The largest financial / ◼ JV with BNI, a domestic insurance companies, translated from JPY using USD1 = JPY111.92, as of September 30, 2021. national bank insurance group in and Singlife, an emerging 2. Core business profit of the group (see page 7 for details) ◼ Owns 39.99% Vietnam insurance company that aims to 3. Figures for individual life and individual annuity for domestic business (see page 6 for details) ◼ Owns 22.08% of the of the shares harness cutting-edge technology 4. Combined figures of Sumitomo Life’s EEV, Medicare Life’s EEV and Symetra’s EEV (see page 8 for details) shares ◼ Owns 20.74% of the shares 5. As of October 31, 2021. The rating from Fitch is unsolicited 6. As of September 30, 2021 on ownership 2

Key Highlights ◇ 1H FY2021 Results ✓ Group Annualized premiums (AP) from policies in force have shown ・・・ P.6 stable growth. AP from new policies increased from 1H FY2020 due mainly to the growing sales of protection products. ✓ Group core business profit decreased from 1H FY2020 due to ・・・ P.7 investment for long-term growth, payments related to COVID-19, and higher initial policy costs associated with the growth in new policies of Medicare Life. ✓ EEV increased from the end of the previous fiscal year due to positive ・・・ P.8 results of the insurance business such as acquiring new policies and securing earnings from policies in force, as well as an increases in stock prices, etc. ・・・ P.9 ✓ Established a strong capital base consisting mainly of contingency reserves. 3

Ⅰ. FY2021 Business Results 4

Impact of the Pandemic Payments of claims and benefits related to COVID-19 totaled approximately ¥11.2 billion, of which, approximately ¥7.1 billion was paid in 1H FY2021. Annualized premiums (AP) from new policies recovered to the level before the spread of COVID-19. Situation in Japan (Sumitomo Life (non-consolidated)) < COVID-19-related Payments > Death benefits Hospitalization benefits Extension of grace period of premium Number Amount Number Amount payment Total since the spread of COVID-19 1,109 JPY 7.3bn 30,413 JPY 3.8bn 12,350 Of which, in 1H FY2021 664 JPY 4.3bn 21,381 JPY 2.7bn 863 < Claims Paid and Benefit Payments > < Annualized Premiums from New Policies > JPY bn JPY bn 59.4 60.0 500 54.9 50.3 49.4 50.0 400 153.0 153.9 142.7 40.0 153.8 40.0 148.9 300 30.0 200 20.0 300.5 307.6 287.2 270.9 257.7 100 10.0 0 0.0 FY19 FY19 FY20 FY20 FY21 FY19 FY19 FY20 FY20 FY21 1H 2H 1H 2H 1H 1H 2H 1H 2H 1H Claims Paid Benefit Payments 5

Operating Performance Annualized premiums (AP) from policies in force have shown stable growth. AP from new policies increased from 1H FY2020 due mainly to the growing sales of protection products. Annualized Premiums from Policies in Force1 Annualized Premiums from New Policies1 (Group) (Group) JPY bn JPY bn 3,000 2,845.4 150 2,783.2 2,782.4 2,806.5 2,804.4 (USD 25.4bn) 123.4 113.1 109.8 113.6 419.7.0 419.4 462.4 462.5 505.9 (USD 1.0bn) 2,500 (USD 4.5bn) 100 97.4 51.6 43.9 51.1 53.4 50.6 (USD 0.4bn) 2,000 50 45.6 39.7 39.8 31.5 29.8 (USD 0.2bn) 26.1 26.1 28.0 1,500 1,790.4 1,779.1 1,753.9 1,740.0 1,727.5 22.6 16.9 (USD 0.2bn) (USD 15.4bn) 0 FY17 FY18 FY19 FY20 FY21 1H 1H 1H 1H 1H 1,000 Third sector Excl. third sector Overseas (Symetra) Persistency Rate2 (Non-consolidated) 500 601.8 611.9 % 573.0 583.8 590.0 100 (USD 5.4bn) 13th month 96.6 96.8 96.5 96.1 95 93.3 91.9 0 Mar 18 Mar 19 Mar 20 Mar 21 Sep 21 92.9 90 92.4 92.2 Third sector Excl. third sector Overseas (Symetra) 25th month 85 87.3 1. Figures for domestic business (Third sector + Excl. third sector) are individual life insurance and individual annuities Timing Sep 17 Sep 18 Sep 19 Sep 20 Sep 21 2. Figures are based on annualized premiums for products sold by sales representatives 6

Profit Trend Group core business profit decreased from 1H FY2020 due to investment for long-term growth, payments related to COVID-19, and higher initial policy costs associated with the growth in new policies of Medicare Life. Gain from Insurance Activities Core Business Profit1 (Group) and Interest Gain (Non-consolidated) JPY bn JPY bn 200 200 150 Gain from insurance 153.1 142.5 132.7 112.4 activities 100 137.5 (USD 1.0bn) 203.3 168.3. 184.0 100 202.6 196.5 (USD 1.6bn) 50 65.3 46.9 55.3 36.7 Of which, overseas operations 22.6 (USD 0.5bn) Interest 0 gain FY17 FY18 FY19 FY20 FY21 1H 1H 1H 1H 1H 14.5 20.1 17.6 18.2 26.3 (USD 0.2bn) 0 FY17 FY18 FY19 FY20 FY21 % (Non-consolidated) 1H 1H 1H 1H 1H 2.90 Investment yield2 2.70 2.55 2.44 2.41 2.42 2.50 2.34 1. Group core business profit is calculated by combining core business profit of Sumitomo Life and 2.30 Medicare Life, and profit before tax of Symetra, Baoviet Holdings, BNI Life, Aviva Singlife Holdings 2.10 2.03 Average and PICC Life attributable to Sumitomo Life’s equity stake in each company, with adjustments 2.10 2.30 2.17 1.94 assumed yield made to some internal transactions 1.90 2. Related to core business profit FY17 FY18 FY19 FY20 FY21 7

EEV Trend EEV increased from the end of the previous fiscal year due to positive results of the insurance business such as acquiring new policies and securing earnings from policies in force, as well as an increase in stock prices, etc. EEV (Group) EEV Growth Factors JPY bn 4,799.2 JPY bn 5,000 (USD 42.8bn) Economic 4,489.2 Income from variances new business 4,000 3,778.9 3,699.0 +57.6 3,584.1 and existing business etc. 3,000 +252.4 2,000 4,799.2 1,000 4,500 [+310.0] <Reference> Mar 21 Sep 21 0 Mar 18 Mar 19 Mar 20 Mar 21 Sep 21 30yr JGB 0.665% 0.670% 20yr JGB 0.475% 0.445% % 50bp downward parallel shift in 10yr JGB 0.090% 0.065% JPY risk-free yield curve 20.0 4,489.2 TOPIX 1954.00 2030.16 10.4 10.7 11.0 10% decline 10.0 6.4 in equity and real estate 5.2 4.9 5.3 5.4 values 4,000 0.0 Mar 18 Mar 19 Mar 20 Mar 21 1. Sensitivity for each item. Other conditions are assumed to be the same Mar 21 Sep 21 8

Capital Base Established a strong capital base consisting mainly of Internal reserves and surplus. Solvency margin ratio remains at a stable level. Trend of Capital (Non-consolidated) Solvency Margin Ratio (Consolidated) JPY bn % 2,914.1 1,000 3,000 2,765.7 (USD 26.0bn) 915.6 919.6 JPY 100.5bn 881.7 870.0 862.5 issuing of 2,508.5 US$ Subordinated600.5 External ⑥ 2,500 2,402.8 2,462.6 569.9 bond Capital 800 JPY 600.5bn JPY 70.0bn ⑤ redemption of 499.9 499.9 subordinated 499.9 bond 2,000 610.4 ④ 50.0 508.2 100.0 417.1 600 364.3 349.4 1,500 899.2 ③ Internal 787.5 883.6 reserves and 400 656.9 744.4 surplus 1,000 JPY 2,313.6bn 165.0 165.0 165.0 165.0 165.0 ② 200 500 Regulatory minimum threshold of 200% 631.6 639.0 639.0 639.0 639.0 ① 0 0 Mar 18 Mar 19 Mar 20 Mar 21 Sep 21 Mar 18 Mar 19 Mar 20 Mar 21 Sep 21 ① Reserve for fund redemption + ② Fund for price ③ Reserve for price Reserve for redemption of fluctuation allowance fluctuation foundation funds1 ④ Contingency reserve ⑤ Foundation funds ⑥ Subordinated loans / bonds 1. Figures before March 2021 are after appropriation of surplus 9

Progress of Medium-Term Business Plan (2020-2022) Targets for Results as of Items March 2023 September 2021 Number of Customers (Policies in Force)1 14.00 million policies 14.19 million policies (Sumitomo Life + Medicare Life + Business Alliance Partners) Annualized Premiums from Policies in Force JPY 2,310.0bn JPY 2,339.4bn (Sumitomo Life + Medicare Life) Of which, Third Sector JPY 610.0bn JPY 611.9bn Domestic Business Core Business Profit 3-year total FY2020 – 1H FY2021 total (Sumitomo Life + Medicare Life) JPY 901.0bn JPY 490.8bn Overseas Operation Core Business Profit 3-year total FY2020 – 1H FY2021 total (Symetra, etc.) JPY 103.0bn JPY 58.5bn 1. Number of individual life insurance and individual annuities, including products provided by our business alliance partners (Mitsui Sumitomo Insurance, NN Life, Sony Life). 10

Ⅱ. Sumitomo Life Group’s Initiatives 11

① Multi-Channel and Multi-Product Strategy ② Asset Management ③ Sustainability ④ Overseas Business Development ⑤ Capital Policy 12

Multi-Channel and Multi-Product Strategy We aim to expand the entire customer base of the Sumitomo Life group by providing products customized to the unique characteristics of each channel. Entities ✓ Arouse potential needs Channels ✓ Provide products and services based on consulting ✓ Provide new value of “Health Enhancement” 【Policies in Force:13mm1 】 (for needs including medical, nursing Business Alliance care and work disability, health Sales Reps enhancement, asset building, etc.) ✓ Expand the efficient product lineup ✓ Contribute to expense savings (NN Life) revenue through sales commissions, and diversification of revenue Customers (for business coverage, business Bancassurance- succession, retirement planning, Banks, Financial Institutions & stable asset building, etc.) Subsidiary Japan Post Group, etc. ✓ Provide simple and affordable medical insurance Insurance Outlets (Medicare Life) 2 【Policies in Force:1mm 】 ✓ Agile marketing, insurance coverage to the “niche areas” (AIARU Small Amount & Short Term Insurance) Expansion of the customer base of the Sumitomo Life group by leveraging the unique characteristics of each channel 1. As of September 30, 2021. Number of individual life insurance and individual annuities, including products provided by our business alliance partners (Mitsui Sumitomo Insurance, NN Life, Sony Life) 2. As of September 30, 2021 13

Our Main Products We develop and provide products to match customer needs, utilizing subsidiaries and business alliances. Life Insurance P&C Insurance Customer Individual Life In case of Needs Corporate a sudden Mortality Nursing Care / Medical Insurance Work Disability Insurance Savings accident Comprehensive Medical Single-Premium Insurance Protection Insurance Term Life Automobile Insurance [Yen] [Foreign Currency] Insurance (Whole Life) (Whole Life) Property Insurance Dementia Protection Cancer Protection Products Level-Premium Insurance Wellness program that could be attached [Yen] [Foreign Currency] to the above main products (Whole Life) (Whole Life) Casualty Insurance Medical Protection Income Assurance Medical Insurance (Endowment) Others Insurance (Simple and affordable) Work Disability がん保険 (Annuity) (Annuity) Protection 14

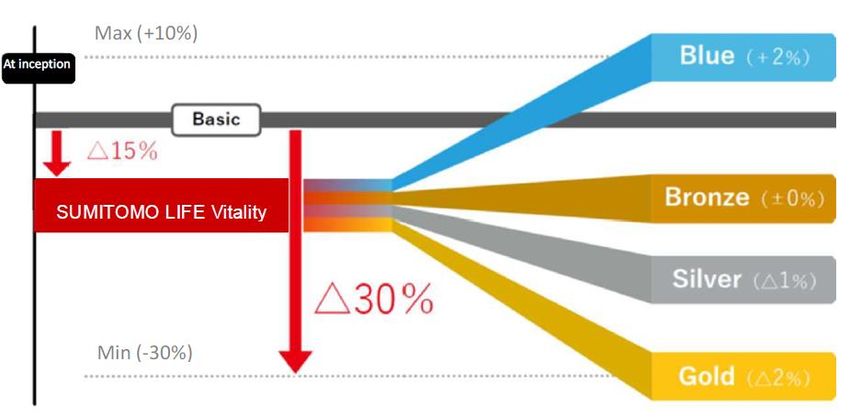

SUMITOMO LIFE Vitality Sales Sales of SUMITOMO LIFE Vitality were strong in 1H FY2021, with the number of policies sold increasing steadily. Started offering a trial version and a family plan to enable more customers to experience for themselves the attraction of the Vitality program. Overview of SUMITOMO LIFE Vitality Number of SUMITOMO LIFE Vitality policies sold ・Package product, which adds Vitality, a globally recognized ・Sales in 1H FY2021 were a record high on a semi-annual basis. health enhancement program with over 20 million members (thousand policies) across 30 countries and regions as of June 30, 2021, to a protection type product. 193 ・Sumitomo Life is the exclusive partner insurer for the Japanese 200 market for the distribution of Vitality. 127 139 ・Cumulative 820,000 contracts as of September 30, 2021. 110 116 100 68 67 Protection Type Vitality Wellness Program Products ・Contribute to reduction of risks ・Prepare for nursing, associated with illness via 0 medical and mortality mechanism that promotes FY18 FY18 FY19 FY19 FY20 FY20 FY21 risks sustained health enhancement 1H 2H 1H 2H 1H 2H 1H Efforts to let more customers experience for themselves the attraction of the Vitality program ■ Provision of a Vitality trial version ■ Launch of a family plan ・Started offering a “trial version” that allows customers to experience ・ Launched a “Family Plan” targeting Vitality members’ families, part of the Vitality Wellness Program (e.g. Active Challenge) free of with the aim of encouraging members to participate in the charge for a limited time before signing life insurance policies. The Vitality Wellness Program as a family. aim is to enable customers to experience for themselves the attraction of Vitality. I became more conscious of “family The Active Challenge system health” since the COVID-19 outbreak1 1. A weekly target 2. Points are gained 3. If the weekly target is is set automatically. through activities such as achieved, the user is I am working on health improvement walking, with the aim to guaranteed to receive together with families and friends2 achieve the target tickets that can be 1.Results of questionnaire for Vitality members: Survey of 32,316 members living with other number of points. exchanged for various household members drinks. 2.Results of questionnaire for Vitality members: Survey of 12,732 members who have Vitality members in their households 15

Contribution and Evolution of SUMITOMO LIFE Vitality SUMITOMO LIFE Vitality contributes to change in awareness, behavior, and health condition of policyholders Continuously work on the evolution of SUMITOMO LIFE Vitality in order to support policyholders to engage in health enhancing activities Contribution of SUMITOMO LIFE Vitality Evolution of SUMITOMO LIFE Vitality [Vitality members] Increase in or continuation of exercise opportunities ■Expansion of Bundled Target Products Increase in exercise opportunities after enrollment : 1 81 % 【As of Sep 30, 2021】 +9 % increase in the average number of steps after enrollment and subsequent continuation of moderate exercise2 Improvements in the results of health checks3 Blood pressure reduction of 10 mmHg or more: 44 % Blood sugar reduction of 10 mg/dl or more: 31 % LDL cholesterol reduction of 10 mg/dl or more: 39 % [Payments] ■ Expansion of reward partner companies 4 Decrease in mortality and hospitalization rates (companies) 【As of Sep 30, 2021】 17 Mortality rate Down Down 20 13 about 40% about 85% 11 Vitality members have about 40% lower mortality rate and about 10% 17 10 lower hospitalization rate. companies 0 Mar 19 Mar 20 Mar 21 Non-Vitality Vitality Blue Bronze Silver Gold Hospitalization rate Down Down about 10% about 40% ■Donation to the Japan Cancer Society using Active By Vitality member status, both Challenge mortality and hospitalization rates [Addition in June 2021] Made it possible to choose donation to the are significantly lower for gold Japan Cancer Society instead of using coffee and drink tickets members than blue members. Non-Vitality Vitality Blue Bronze Silver Gold obtained in Active Challenge (after achieving weekly exercise point 1.Questionnaire by Sumitomo Life. The number of responses: 41,666. Excluding Sumitomo Life employees. goals) 2.Analysis of the average number of steps taken by members enrolled between September 2018 and January 2019, by the end of January 2021. 3.Members who enrolled between September 2018 and January 2021, who, after enrolling, had submitted health-check results by March 2021, and who met all of the following conditions. ・Blood pressure: systolic blood pressure of 140 mmHg or more at the time of enrollment ・Blood sugar level: fasting blood sugar level of 126 mg/dl or more at the time of enrollment ・LDL cholesterol: LDL cholesterol of 140 mg/dl or more at the time of enrollment 4.Calculated based on payments made from April 2020 to March 2021 for policies issued before March 2020. The mortality rate excludes accidental deaths, and the hospitalization rate excludes accidental hospitalizations. Non-Vitality refers to policies that do not include the Vitality Wellness Program despite their eligibility. 16

Medicare Life Sales of medical whole life insurance continued to be strong from last fiscal year,1,187 1,200 and the number of policies in force increased. 1,025 Medicare 1,000 Life < Number of New Policies > < Number of Policies in Force > 800 policies) (thousand 778 (thousand policies) 715 1,187 2H 1,200 297 619 300 1H 600 1,025 1,000 191 200 171 400 800 778 124 715 100 97 200 619 600 0 0 Mar 18 Mar 19 Mar 20 Mar 21 Sep 21 400 Mar 18 Mar 19 Mar 20 Mar 21 Sep 21 Insurance Outlets, etc. of Sumitomo Life Group < Key Indicators (As of September 30, 2021) > 200 Izumi Life Designers Co., INSURANCE DESIGN EEV JPY 226.1 bn Ltd. 0 Operates insurance outlets Operates Mar 18 insurance Mar 19 outlets calledMar Mar 20 “Hoken 21 Design” Sep 21 called “Hoken Hyakka” Solvency Margin Ratio 1,349.8% Mycommunication Co., Ltd. Agent Insurance Group, Inc. Credit Operates insurance outlets Mainly sells P&C insurance AA- (R&I) under the brand of “Hoken Rating Hotline” 17

① Multi-Channel and Multi-Product Strategy ② Asset Management ③ Sustainability ④ Overseas Business Development ⑤ Capital Policy 18

Medium-Term Asset Management Policy We plan to control the total risk amount by reducing domestic interest rate risk through investment in super long-term domestic bonds in anticipation of a prolonged low interest rate environment, and enhance profitability by further expanding investment in foreign credit assets and risk assets. Medium-Term Asset Management Policy Reduction of domestic interest Enhancement of profitability Promotion of responsible rate risk through risk-taking investment Super long-term domestic GHG net-zero Foreign credit assets bonds, etc. Consideration of new Responsible investment schemes Non-traditional investments1 structure (comprehensive hedging by interest rate swaps) Foreign stocks All assets to be covered Unhedged foreign bonds Amount of thematic investment Risk Amount Risk Amount Improve profitability while controlling the total risk amount 1. Assets and investment methods other than those that are called traditional assets such as bonds and listed stocks (e.g. private equity, private debt) 19

Initiatives in 1H FY2021 Managed general account with portfolios classified into two categories: ALM Investment and Balanced Investment. Aimed to increase our investment earnings in accordance with investment objectives and to strengthen our asset management platform in order to enhance medium to long-term investment profitability. Initiatives in 1H FY2021 ALM Investment Portfolio Balanced Investment Portfolio ・Portfolio focused on yen-denominated assets (approx. JPY 26tn) ・Portfolio focused on highly liquid securities (approx. JPY 7tn) ・Objective is to contribute to sustainable growth of ・Objective is to contribute to secure payment of claims, etc. Embedded Value ・Promoted investment in foreign credit assets when ・invested in domestic, U.S., and Asian equities, paying corporate bond issuance increased, while strengthening Increased diversification of the portfolio, and selection. attention to stock price trends Investment ・Gradually increased investments in infrastructure equity Promoted ・Increased investment of unhedged foreign bonds Earnings funds and private equity funds. Considered and started Respon- (USD/Asian currencies) while taking the levels of investing in new non-traditional assets such as private sible interest rates and foreign exchange rates into debt. Invest- account ment ・Reduced domestic interest rate risk by investing in Strengthen super long-term bonds and implementing ・ Hedged risks in case of decline in stock market and -ed Risk comprehensive hedging of interest rate swaps, with the yen appreciation Control outlook of a prolonged low interest rate environment Initiatives to Strengthen Asset Management Platform Market Interest Rate and Our Investment Yield ・Started to formulate human capital strategy based on long- term asset strategy. 2.55% 2.34% 3.0% ・Promoted cross-departmental BPR1, expand work from home 2.0% by introducing remote operation system 1.0% 0.06% 0.09% ・Entrusted assets such as bank loans and US private 0.0% corporate bonds, and decided to fully outsource overseas (1.0%) corporate bond management to Symetra Investment Mar 17 Mar 18 Mar 19 Mar 20 Mar 21 Management. Investment yield (related to core business profit) JGB yield (10yrs) 1. Business Process Reengineering: Fundamental review and redesign of work content and flow, etc. 20

General Account Asset Portfolio Prudent investment policy, focusing mainly on yen-denominated interest-bearing assets Trend of General Account (GA) Assets Breakdown of GA Assets (Non-consolidated) (Non-consolidated) Figures on B/S <As of September 2021> JPY tn 34.5 34.8 (USD 311.8bn) Others 4.2% 32.2 1.7 1.4 6.2%1.6% 31.9 0.5 0.5 Real estate 1.4% 30.5 2.1 2.4 1.8 2.1 Foreign Yen-denominated 30 0.4 0.4 interest-bearing 2.0 0.5 0.5 stocks, etc. 7.3% assets 1.2 1.3 2.4 2.5 0.5 0.1 0.3 Other securities 52.1% 1.0 0.0 1.8 1.7 1.9 Domestic stocks 40.0% 9.5 9.4 Foreign-currency 8.2 8.5 denominated 7.6 foreign bonds1 27.1% 20 Monetary claims 0.5 0.4 bought 1.3% 6.2% 0.2 0.3 1.6 1.5 0.3 1.6 1.5 1.6 Yen-denominated 4.6% 1.9 2.1 foreign bonds2 2.7 2.8 2.0 Domestic bonds Loans Yen-denominated foreign bonds Monetary claims bought Loans Foreign-currency denominated foreign bonds Domestic stocks Other securities Foreign stocks, etc. 10 Unrealized Gains/Losses in GA Assets Domestic (Non-consolidated) bonds JPY bn 12.5 12.9 13.2 13.8 13.9 As of Mar 2021 As of Sep 2021 change Yen-denominated Securities 3,694.1 3,810.0 +115.9 17.2 17.6 17.3 17.9 18.1 interest-bearing Held-to-maturity debt securities 261.3 254.6 (6.7) assets Policy-reserve-matching bonds 1,597.1 1,587.7 (9.4) 0 Available-for-sale securities 1,840.9 1,972.7 +131.8 Mar 18 Mar 19 Mar 20 Mar 21 Sep 21 Domestic stocks 1,222.5 1,285.0 +62.4 Foreign securities 521.9 570.4 +48.4 1 Foreign currency-denominated foreign bonds (including those issued by residents) include currency-hedged foreign bonds 2 Yen-denominated foreign bonds include foreign currency-denominated foreign bonds with a fixed amount in Japanese yen *See page 51 for details 21

Profile of Domestic Bonds Strengthen domestic interest rate risk management based on ALM strategy Domestic Bonds by Maturity Domestic Bonds by Category (GA・non-consolidated) (GA・non-consolidated) <As of September 2021> 5 years or less Domestic Bonds Outstanding Balance: Between 5 to 10 years JPY tn More than 10 years or no fixed maturity JPY 14.56tn (USD 130.0bn) 14.4 14.5 14 13.8 13.3 1.1 1.4 13.0 1.0 0.9 18.5% 12 1.0 2.4 4.3 4.3 2.2 3.6 1.9% 10 8 79.6% 6 10.0 9.6 8.9 8.7 9.0 4 2 Policy-reserve matching bonds Held-to-maturity debt securities 0 Available-for-sale securities Mar 18 Mar 19 Mar 20 Mar 21 Sep 21 22

Asset Management Strategy for 2H FY2021 In 2H FY2021, investments will be made based on the asset management policy, while paying attention to various risks. We will increase investment in credit assets and domestic/foreign stocks without increasing the total amount of asset management risk by steadily reducing domestic interest risk, in order to enhance profitability in the low interest rate environment Asset Management Strategy for 2H FY2021 ALM Investment Portfolio Balanced Investment Portfolio ・Invest in foreign credit assets while taking ・Increase investment in domestic and foreign hedging costs into account, and consider stocks that are undervalued from a mid- to long- Increase further investment in the event of rising term perspective Investment interest rates ・Increase investment in unhedged foreign bonds, Earnings ・Increase alternative investments while taking levels of interest rates and foreign Promote ・Consider investing in high quality real estate exchange rates into account Respon- sible ・Steadily invest in super long-term bonds and Invest- new schemes while paying attention to the ・ diversify the portfolio, and make prudent ment trend of interest rate, and consider further selectioThoroughlyn taking the post-pandemic Strengthen investment in the event of rising interest rates situation into account Risk Control ・Build hedge position of stocks and foreign ・Thoroughly diversify the portfolio, and make prudent selection taking the post-pandemic exchange rates in case of decline in market situation into account ・Accelerate human resource development Strengthen ・Develop IT strategy for medium- to long-term asset management, reinforce platform Asset ・Expand entrusted assets, and promote full outsourcing of overseas corporate bond management to Symetra Management Investment Management Platform ・Research and expand alternative investments 23

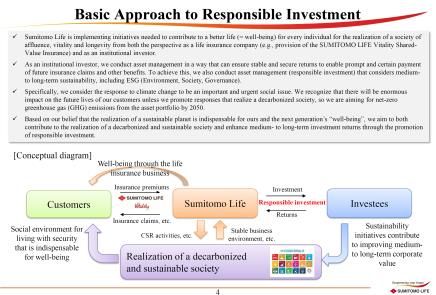

Major Initiative for Responsible Investment Accelerate decarbonization of asset portfolio in 1H. Steadily implement thematic investment. Promote ESG integration of all assets through dialogue with investees on their decarbonization initiatives in 2H. Initiative to Achieve Net Zero of Asset Portfolio NEW (2021/10) NEW (2021/8) NEW (2021/10) Net-Zero Net-Zero Asset Owner Alliance Asset Owner Alliance Measurement & Target Setting Information Commitment Action Scenario Analysis Disclosure April 2021: Announced Measure GHG emissions June 2021:Set a reduction Promote dialogue with October 2021: Release net-zero GHG emissions from the asset portfolio. target of -42% by 2030 companies with top Responsible Investment by 2050 Next challenges will be (compared to fiscal 2019) in GHG emissions to Activities Report enhancements of aspects our asset portfolio encourage (GHG emissions, etc.) such as scenario analysis decarbonization Implementation of the Thematic Investment Target amount (Fiscal 2020 - 2022) Results (1H 2020 - 2021) Thematic investment Cumulative: ¥500.0 billion Approx. ¥240.2 billion (¥94.5 billion for 1H 2021) Promote ESG Integration of All Assets 1H FY2021 2H FY2021 (planned) ✓ Clarify the process of real estate and project financing ✓ Clarify the process of entrusted assets and ✓ Start considering sovereigns securitized products, etc. 24

① Multi-Channel and Multi-Product Strategy ② Asset Management ③ Sustainability ④ Overseas Business Development ⑤ Capital Policy 25

Initiatives in FY2021 We continued to implement sustainability initiatives as in FY2020. Various reports have been newly published to report the status of our efforts to promote sustainability. Formulation of an “Action Plan Launch of new products contributing to solving for Promoting Participation by Women” social issues Set a target for female employees in managerial Launched an ESG-focused investment product that positions by the end of FY2025, with an aim to further mainly invests in Japanese stocks for corporate pensions promote the active participation of diverse talents Goal for the end of FY2025 April 2020 (Product name) Group annuity separate account “Yen-denominated stocks account E” (ESG investment) Publication of the Responsible Publication of the Sustainability Report Investment Activities Report Newly published the Sustainability Report in September Published the Responsible Investment Activities Report 2021 (comprehensive description of the approach and in October 2021 (the previous “Stewardship Activities efforts for promoting sustainability) Report” was renamed after information on ESG investment and other initiatives was added) 26

External Initiatives Participation in External Initiatives 【Environment (E) related】 【Society (S) related】 New New AOA ・An international initiative that aims to achieve the Paris Agreement's goal of Net-Zero limiting temperature rise to 1.5°C through the cooperation of asset owners. Asset Owner Under the leadership of the United Nations Environment Programme Finance Alliance Initiative (UNEP FI) and the Principles for Responsible Investment (PRI), the AOA has been active since 2019. ・Sumitomo Life joined AOA in October 2021. 27

① Multi-Channel and Multi-Product Strategy ② Asset Management ③ Sustainability ④ Overseas Business Development ⑤ Capital Policy 28

Overseas Business Expansion Stable revenue base in Japan, steady growth in the U.S. and high growth in Asia Established a business portfolio with stability and growth potential Track Record of Overseas M&A 2019 2020 Singapore Singlife completes merger 2014 Investment in Singlife1 transaction with Aviva Ltd Indonesia (Ownership: 20.74%) (“Aviva Singapore”)1 Investment in BNI Life ◼ Strengthened our ability in gathering information on (Ownership: 39.99%) Insurtech 2013 2016 2005 Vietnam US Investment in Baoviet HD Acquisition of Symetra China (Ownership: 22.08%) (Ownership: 100%) Establishment of PICC Life (Ownership: 10%) ◼ Shared PICC’s business ◼ Increased the size of overseas knowledge with Vietnam business through expanding and Indonesia into the U.S. market United States Japan Asia (China, Vietnam, Indonesia, Singapore) ~ Steady Growth / The Largest ~ Stable Revenue Base ~ ~ High Growth Market ~ Market ~ ◼ The second largest market in the world ◼ China has the largest population in the world and its ◼ The largest market in the world insurance market is still growing ◼ Less growth potential due to the trend ◼ Benefit from steady growth in the U.S. of declining population, but stable ◼ Rapid growth is expected in the future in Vietnam/Indonesia insurance market through Symetra, underwriting income resulting from our 100% subsidiary ◼ Development of Insurtech is flourishing in Singapore mortality gain is expected ◼ Benefit from growth opportunities through technical ◼ Our home market which supports our assistance including channel development, risk stable revenue base management, system development and asset management 1. Invested in Singlife in 2019. In November 2020, Singlife merged with Aviva Singapore, one of the largest domestic insurance companies. We made an additional investment to support the transaction. Following the transaction, our equity interests in Singlife were exchanged for those of Aviva Singlife Holdings Pte., Ltd, a holding company which was newly established. 29

Initiatives in the U.S. Market ① Symetra has solid business base across the U.S. Capture steady earnings resulting in improved earnings base and risk diversification. Business Development in the U.S. - Symetra (100% subsidiary) Total Revenues and Total Assets (USD mn) ◼ 100% acquisition of Symetra Financial Corporation (JPY 6,683.0bn1) 5,000 70,000 (February 2016) 58,911 60,436 60,000 55,535 4,000 ◼ Number of employees (Consolidated): Approx. 1,900 50,000 49,263 42,865 40,000 2,650 3,000 ◼ RBC Ratio (Risk Based Capital)*: 422% 2,481 2,298 2,239 (JPY 167.4bn1) 30,000 (As of December 31, 2020) 1,514 2,000 *Calculated without considering 50% of the risk profile (denominator) 20,000 1,000 ◼ Ratings: A (S&P), A1 (Moody’s), A (AM Best) 10,000 0 0 Dec 17 Dec 18 Dec 19 Dec 20 Jun 21 Total Asset(Left Axis) Total Revenue(Right Axis) Conservative Investment Policy – Asset Management Portfolio Synergy Effects <As of June 2021> Limited Product ・Leveraged Symetra’s expertise to commence Stocks Partnership Others sales in Japan of a fixed indexed annuity product, 0.2% 1.0% 1.9% Development one of Symetra’s core products ・Sharing information about the markets and certain CMLs issuers, placing orders for U.S. corporate bonds 15.6% Corporate through Symetra Bonds, etc. Asset ・Plan to expand the outsourcing of asset Management management for investment grade corporate bonds 81.4% entrusted to Symetra Investment Management, and reach an entrusted asset balance of 2 trillion yen. ◼ 52.2% for A and above (JPY 5,436.2bn1) ◼ 97.0% Above IG Total: USD 49.1bn ・Sumitomo Life and Symetra are dispatching IT personnel to a base in Silicon Valley to gather information on FinTech activities 1. USD 1 = JPY110.58 (as of June 30, 2021) 30

Initiatives in the U.S. Market ② Symetra has a balanced business portfolio, and each business line has shown stable growth even in amidst of the COVID-19 pandemic. Balanced Business Portfolio Summary P&L – Ordinary Income by Segment USD (mn) <As of June 2021> Year ended Year ended Six months ended Dec 31, 2019 Dec 31, 2020 Jun 30, 2021 1 Adjusted pre-tax income 172.3 130.4 118.1 Benefits 33.9 12.9 39.6 Individual Retirement 137.8 128.8 79.8 Life Individual Life 24.6 8.7 4.4 Retirement Other (24.0) (20.0) (5.7) 25.4% Add (deduct) the following: (549.6) (290.3) 3.5 35.0% Excluded realized gains (losses) (63.3) (37.4) 18.7 Amortization of intangible assets (87.3) (143.2) (64.5) Benefits Closed Block results (399.0) (109.7) 49.3 Income (loss) from operations before income tax (377.3) (159.9) 121.6 39.6% Total provision (benefit) for income taxes 111.8 68.4 (25.4) Net income (loss) (265.5) (91.5) 96.2 Ordinary Income from Ordinary Income from Ordinary Income from Retirement Benefits Individual Life USD (mn) USD (mn) USD (mn) 1,000 905 962 1,400 800 1,190 1,175 785 1,200 625 670 800 711 1,025 569 911 600 (JPY 55.9bn2) 1,000 513 600 (JPY 63.2bn ) 2 (JPY 40.6bn2) 505 800 571 400 367 400 600 400 200 200 200 0 0 0 Dec 17 Dec 18 Dec 19 Dec 20 Jun 21 Dec 17 Dec 18 Dec 19 Dec 20 Jun 21 Dec 17 Dec 18 Dec 19 Dec 20 Jun 21 1 Income from operations before income taxes, excluding results from closed blocks, intangible asset amortization and certain net realized gains (losses). 2. USD 1 = JPY110.58 (as of June 30, 2021) 31

Initiatives in the Asian Market Partner with local leading companies in the Chinese, Vietnamese, Indonesian and Singaporean markets. The companies we have invested in have shown stable growth and contributed to our profit. In Singapore, two life insurance subsidiaries of Aviva Singlife Holdings are scheduled to be integrated early next year. China Vietnam ◼ Establishment of PICC Life Insurance Company (November 2005) ◼ Investment in Baoviet Holdings (March 2013) PICC Life’s Total Premium Income Baoviet’s Premium Income from Life Insurance CNY bn VND bn 120 106.2 30,000 28,046 93.7 98.1 96.1 1 25,452 100 (Approx. JPY1,097.9bn ) 25,000 (Approx. JPY70.6bn1) 21,507 80 64.1 20,000 17,476 14,704 60 15,000 40 10,000 20 5,000 0 0 Dec 17 Dec 18 Dec 19 Dec 20 Jun 21 Dec 17 Dec 18 Dec 19 Dec 20 Jun 21 Indonesia Singapore ◼ Investment in BNI Life, a subsidiary of Bank Negara Indonesia ◼ Investment in Aviva Singlife Holdings2 (June 2019) (BNI) (May 2014) IDR bn BNI Life’s Total Premium Income Aviva Singapore’s Total Premium Income 5,710 5,568 SGD mn 6,000 4,754 4,600 4,000 3,791 5,000 4,000 (Approx. JPY17.3bn1) 3,000 2,503 (Approx. JPY163.7bn1) 1,978 1,992 3,000 2,254 2,000 2,000 1,000 1,000 0 0 Dec 17 Dec 18 Dec 19 Dec 20 Dec 21 Dec 18 Dec 19 Dec 20 Jun 21 Source: Company disclosure 1. CNY1 = JPY17.12, VND1 = JPY0.004802, IDR1 = JPY0.0077, SGD1 = JPY82.18 (as of June 30 2021). 2. Invested in Singlife in June 2019. Following the business combination of Singlife and Aviva Singapore, our equity interests in Singlife were exchanged for those of Aviva Singlife Holdings Pte., Ltd , a holdings company which was newly established. We made an additional investment to support the transaction. 3. Aviva Singlife’s operating results are based on the combined figures of the two life insurance subsidiaries (consolidated figure for six months ended June 30, 2021 and the simple sum of the two companies for the periods before the year ended Dec 31, 2020). 32

COVID-19 Situation in countries where we operates U.S. China Population : 0.33bn 16000 350000 Population : 1.4bn 1 14000 300000 Total Cases : 46,693,102 1 12000 Total Cases : 98,016 250000 Total Deaths1: 757,291 10000 Total Deaths1: 4,636 200000 8000 150000 6000 100000 4000 50000 2000 0 0 新規感染者数 New cases 死亡者数 Deaths 7日平均新規感染者数 7-day average of new cases 新規感染者数 New cases 死亡者数 Deaths 7日平均新規感染者数 7-day average of new cases VIetnam Indonesia Singapore 6000 20000 60000 18000 Population : 90mn Population : 0.27bn 5000 Population : 5.69mn 16000 50000 14000 Total Cases1 : 984,850 Total Cases1 : 4,248,843 4000 Total Cases1 : 224,200 12000 40000 10000 Total Deaths1: 22,686 Total Deaths1: 143,578 3000 Total Deaths1: 523 30000 8000 20000 2000 6000 4000 1000 10000 2000 0 0 0 New cases 新規感染者数 死亡者数 Deaths New cases 新規感染者数 Deaths 死亡者数 New cases 新規感染者数 死亡者数 Deaths 7日平均新規感染者数 7-day average of new cases 7日平均新規感染者数 7-day average of new cases 7日平均新規感染者数 7-day average of new cases Source: Our World in Data Note: As of 9 November 2021 33

① Multi-Channel and Multi-Product Strategy ② Asset Management ③ Sustainability ④ Overseas Business Development ⑤ Capital Policy 34

External Capital Philosophy Behind External Capital In building core capital, we focus on enhancing internal reserves and surplus, and view external capital as a complement. We will secure a sufficient capital level, considering the current solvency regulation and new economic value-based capital regulation, which we expect to be implemented in the near future. Total Balance of External Capital Total Balance of External Capital: JPY600.5bn redeemed US$ Sub. bond US$ Sub. bond USD1.34bn US$ USD920mn (JPY Sub. bond (JPY 145.44bn) Sub. bond USD1bn 100.5bn) Sub. bond (JPY Sub. loan JPY84.0bn 99.48bn) Sub. bond JPY70.0bn JPY70.0bn Sub. Loan JPY10.0bn JPY 50.0bn Sub. bond JPY30.0bn Sub. bond JPY11.0bn FY21 FY22 FY23 FY24 FY26 FY27 FY30 FY31 Note: As of Octoberl 31, 2021. The first call maturity coming year for subordinated loans / bonds 35

Capital Adequacy (Economic Value Basis) Appropriately control the balance between risks and risk buffers in consideration of future changes in circumstances such as the regulatory environment. The capital adequacy ratio as of the end of September 2021 (ESR, preliminary figure) is 217%. ESR1 Sumitomo Life’s Risk Management System (preliminary figure) Current JPY bn 215% 217% 6,000 Risk management based on the requirement by the 200% regulatory authorities 5,000 ・Solvency margin ratio, etc. 159% 150% 4,000 Risk management based on internal control 3,000 (economic value) (from FY2009) 100% ・ESR monitoring: Confirmation of the adequacy of capital, etc. ・Stress testing: Check the impact under multiple risk scenarios 2,000 50% 1,000 Future (Economic value-based solvency regulation in Japan, 2025 at the earliest) 0% 0 Risk management based on the requirement by the Mar 20 Mar 21 Sep 21 regulatory authorities Risk Buffer Risk Amount ESR (left axis) ・Details have not been confirmed Mar 20 Mar 21 Sep 21 Change Newly Issued 30yr JGB 0.420% 0.665% 0.670% +0.005% Risk management based on internal control TOPIX (Closing Price) 1,403.04 1,954.00 2,030.16 +76.16 (economic value) ① ② ②-① ・Make adjustments to internal risk management as necessary, taking into account the requirement by regulatory authorities 1. The risk amount is calculated using an internal model with a confidence level of 99.5% (holding period of 1 year). The calculation of economic value-based capital amount and risk amount uses an ultimate forward rate for setting super long-term interest rate. 36

Introduction of Economic Value-Based Capital Regulation Timeline for the Introduction of Japan’s Economic Value-Based Solvency Regulation Indicated by the Study Group 2019 2020 2021 2022 2023 2024 2025 … Pillar 1 Refinement of Tentative Develop- Domestic Solvency Study Report Study for the decision technical Finali- ment of Frame- regulation Group release formulation of tentative on the specifications and zation practical Implementation specifications specifi- development guidance of the economic work towards finalization cations value-based solvency Incorporation in the study on specifications as necessary framework (April 2025) Field testing Pillar 2 Utilizing the results of the field testing for supervisory dialogue with insurers Risk manage- Considering revision/abolition of financial accounting, risk information, etc. ment and based on economic value base super- visory Continuing & strengthening dialogue with insurers on internal control based review on economic value Pillar 3 Study on Information Developing details of the disclosure the outline of the disclosure requirements disclosure requirements Global ICS monitoring period Applicable as a Completion Economic impact Finali- standard for regulatory Frame- Review of specifications based on the reporting by IAIGs Consul- assessment of ICS tation zation intervention in each work Consideration of comparability with the Aggregation Method Comparability Ver 2.0 assessment country 1. Internationally Active Insurance Group. IAIG is selected with the following criteria by national authorities: (1) Premiums are written in at least three jurisdictions and at least 10% of the group’s gross written premium (GWP) is from outside the home jurisdiction; and (2) Total assets of not less than USD 50 billion or GWP of not less than USD 10 billion. 37

Ⅲ. Appendix 38

Domestic Life Insurance Market The life insurance market in Japan has grown by 2.1% CAGR over the last 10 years, driven primarily by the third-sector insurance. Trend of Annualized Premiums from Policies in Force1 JPY bn 30,000 27.0% 25,000 26.0% 20,000 25.0% 15,000 24.0% 10,000 23.0% 5,000 22.0% 0 21.0% FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19 FY20 Annualized premiums from policies Annualized premiums from policies Ratio of Third-sector products (Right-Axis) in force of Third-sector products in force excluding Third-sector products Survey on Life Protection (FY2019) 11% 4% 5% 6% 23% 12% 15% I am currently 30% Totally insufficient 16% making preparations 49% 38% Somewhat 69% 66% 75% I will make preparations 73% insufficient 76% 60% 46% within several years 45% 53% 43% 8% Do not know I will prepare 9% Somewhat at some point 37% sufficient 12% 29% 18% 20% Do not have intention of 20% 14% 2% Sufficient 7% 5% 6% making any preparations 7% 3% Nursing Care Medical Annuity Nursing Care Medical Annuity Do not know Feelings Regarding Sufficiency Intention to Make Future Preparations Source: The Life Insurance Association of Japan, Japan Institute of Life Insurance “Survey on Life Protection” 1 Excluding Japan Post Insurance 39

Attractive Domestic Business Model We offer broad insurance products with a focus on protection products in highly profitable individual life insurance. Even under the low-interest rate environment, we have maintained profitability mainly thanks to our stable insurance underwriting profit. Business / Product Portfolio Gain from Insurance Activities / Interest Gain (Non-consolidated) (Non-consolidated) <As of September 30, 2021> <1H FY2021> Group annuities JPY bn Business Portfolio 2.5% 200 (Policies in force) Group life 31.1% 150 Individual life 52.4% 112.4 Individual annuities 100 13.9% Product Portfolio (Individual insurance, annualized premiums from policies in force) Individual annuities Individual life 50 (Excl. third sector) (Excl. third sector) 34.5% 41.0% 65.3 0 Third sector Interest gain (Living benefit + Medical/Nursing care) Gain from insurance activities 24.5% Source: Company Disclosures 40

How Vitality Program Works A proprietary program developed by Discovery had been localized by Sumitomo Life to adapt to the local lifestyles, guidelines, etc. in Japan. A framework consists of three steps to assist program members to enjoy the program and become healthier. How Vitality Program Works Step 1 Step 2 Step 3 Know Your Health Improve Your Health Enjoy Rewards ・As a first step, complete health ・Earn points by engaging in ・Rewards provided according to check and other activities to know physical activities such as walking member’s engagement level. one’s health and earn points. a little more. ・Rewards to improve the health ・Boost motivation for sustained ・Rewards to know the health conditions. engagement. conditions. Vitality Status and Points Illustrative Premium Flex Design Blue Bronze 0pt ~ 12,000pt ~ -15% ( -1% ) -30% Silver Gold -15% 20,000pt ~ 24,000pt ~ ( -2% ) 41

Global Network of Vitality Discovery has a global network of Vitality with over 20 million members across 30 countries and regions worldwide (as of June 30, 2021). Sumitomo Life is the exclusive partner insurer for the Japanese market. Global Network of Vitality1 Established 1992 Representative Adrian Gore, Group Chief Executive Head office Sandton, Johannesburg, South Africa Stock listing Johannesburg Stock Exchange (JSE) Total assets (as of June 30, 2021) ZAR 246,694 million (JPY 1,820.6 billion)2 1 Each country and region has its own point distribution standards, status levels and other aspects of the Vitality program 2 ZAR 1 = 7.38 JPY (exchange rate as of September 30, 2021); Discovery Limited’s financial year end is June 30 42

AIARU Small Amount & Short Term Insurance Acquired AIARU Small Amount & Short Term Insurance Co., LTD as a subsidiary in August 2019, and built a flexible product development structure consisting of Sumitomo Life, Medicare Life and AIARU Small-amount and Short-term Insurance Business Deals only with the underwriting of protection-type insurance products, in small insurance amounts in short insurance terms of one year (two years for non-life insurance) within a certain business scale <Key differences between regulations on insurance companies and on small-amount and short-term insurance companies> Insurance companies Small-amount and short-term insurance companies Conditions for market License granted by Commissioner of the Registration with a local finance bureau access Financial Services Agency Annual insurance premiums receivable of no more than Business scale No limit JPY 5 billion1 Product examination Approval (notification for some products) Notification Limit on insurance amount Limit on insurance amount per insured person, depending on No limit (original rule) the insurance category (maximum of JPY 10 million) Limit on insurance term No limit One year (two years for non-life insurance) 1 Calculated by adding reinsurance recoverables and reinsurance fees to insurance premiums receivable in one business year, and then subtracting reinsurance premiums and premium refunds for policy surrender. Overview of AIARU AIARU's Strengths AIARU Small Amount & Short Term AIARU has developed many unique products, based on Company name Insurance Co., LTD.2 the concept of developing original insurance products Establishment April 1984 that meet market needs. Katsuyuki Ando, <Key products> Representative President and Representative Director Head office Nihonbashi Odenmacho, Chuo-ku, Tokyo Capital JPY 299.4 million3 2 In February 2011, Gakuso Co., Ltd. and Rise Small Amount & Short Term Insurance Co., LTD. merged to become AIARU Small Amount & Short Term Insurance Co., LTD. 3 As of September 30, 2021 43

“Well Aging Support- ASUNOEGAO” Sumitomo Life and AXA Life jointly developed a long-term care service that realizes total coordination of long-term care. The service was introduced nationwide from April 1, 2021. Business Alliance with AXA Life Key Services of ASUNOEGAO October 2018 ASUNOEGAO call center Basic agreement on a business alliance for joint development and usage of long-term care services ◇Consultation on various topics related to long-term care ◇Introduction to and information on long-term care facilities ◇Consultation on public long-term care insurance system October 2019 Introduction according to Introduced the “Well Aging Support- ASUNOEGAO” content of phone consultation service in certain areas Face-to-face Long-term care consultation about prevention / QOL April 2020 long-term care enhancement Expanded menus of “Well Aging Support- facilities support service ASUNOEGAO” Long-term care / Asset management Living-support service support service April 2021 Launched “Well Aging Support- ASUNOEGAO” nationwide 44

Effects of Symetra’s Reinsurance Transaction Effects of the reinsurance transaction to Symetra’s GAAP-based income could be expected decrease gradually Positive Impacts Overview of the Reinsurance Transaction from the Reinsurance Transaction ・Reduced exposure to long-term interest rate risk associated Economic ・Contributed to an increase of EV with the long-tail nature of the business through entering into a Value (JPY4.4 billion) reinsurance transaction in September 2018 ・Avoided future losses by reducing the risk ・The modified coinsurance structure of the transaction requires Statutory of additional cash flow testing reserve that Symetra continues to hold the associated invested assets Income expected with the assumption based on and liabilities on its balance sheet (Loss) the interest rates at the time of entrance of ・Investment returns etc. belongs to the Reinsurer on a statutory reinsurance agreement accounting basis Financial ・RBC ratio improvement ・Asset management is executed under the instruction of the Strength ・Reduced exposure of equities Reinsurer Effects of the Transaction to Symetra’s GAAP-Based Income (Loss) Accounting Impact #1: Positive impact to GAAP net income (loss) (USD mn) Six months of Symetra when interest-rates hike (negative impact at the time of Year ended Year ended ended December December interest-rates decline) June 30, 31, 2019 31, 2020 2021 Based on the GAAP accounting rules, amounts equivalent to unrealized gains of bonds in the reinsured business are booked as losses for Adjusted pre-tax income1 172.3 130.4 118.1 Symetra via FV changes of embedded derivatives in insurance liabilities. Add (deduct) the following: (549.6) (290.3) 3.5 Excluded realized gains (losses) (63.3) (37.4) 18.7 Amortization of intangible assets (87.3) (143.2) (64.5) Accounting Impact #2: Negative impact to GAAP net income (loss) Closed Block results (399.0) (109.7) 49.3 of Symetra on sale or maturity of bonds Income (loss) from operations Quarterly gains (losses) of the reinsured business are passed to the (377.3) (159.9) 121.6 before income tax Reinsurer on a statutory accounting basis and is neutral to statutory Total provision (benefit) for earnings of Symetra. However, GAAP BV of bonds held by Symetra is 111.8 68.4 (25.4) income taxes higher than statutory BV due to revaluation when Sumitomo Life Net income (loss) (265.5) (91.5) 96.2 acquired Symetra (PGAAP). 1 Income from operations before income taxes, excluding results from closed blocks, intangible asset amortization and certain net realized gains (losses). 45

Initiative to Sustainability① Our Vision We aim to contribute to the realization of a society of affluence, vitality, health and longevity through the sound operation and development of the insurance business. Extending healthy life Provision of sense of expectancy through the security through the insurance business insurance business Realization of sustainable Building mutual trust with Management structure and stable growth stakeholders that supports CSR To be an “Indispensable” Insurance Company for Society Towards a Society of Affluence, Approach to a Sustainable Society Vitality, Health and Longevity Social issue of “extending healthy life expectancy” Corporate philosophy of “contributing to the advancement of social and public welfare” Implementation of CSV Project1 Enhancing corporate value through addressing (Promote health enhancement across society and health-focused social issues in the main business (=CSV) will management through the provision of SUMITOMO LIFE Vitality) lead to the achievement of the SDGs Contribute to the achievement of the SDGs through Aim to realize a society of affluence, vitality, health and providing attractive insurance products such as longevity by creating a shared value of health SUMITOMO LIFE Vitality and solving social issues enhancement among customers, society, and the through responsible investment and social contribution Company and our employees programs 1. CSV is abbreviation of Creating Shared Value and a business concept which means achieving both resolving social challenges and increasing corporate value (including profit and competitiveness). Please see page 46 for details. 46

Initiative to Sustainability② It implements initiatives to achieve the SDGs, with a focus on contributing to a healthy and long-living society through SUMITOMO LIFE Vitality. Discuss Sustainability initiatives by the Sustainability Promotion Council CSV1 Project Sustainability Promotion Council Contribute to the realization of a healthy and long-living Promote the sharing of social and environmental society through the provision of SUMITOMO LIFE issues, such as SDGs, as well as initiatives to solve Vitality Shared-Value Insurance, promotion of health them enhancement and health-focused management Customers Board of Directors Vitality 4 1 Executive Management Committee CSV Project 3 6 Promotion Health- of health focused Sustainability Promotion Council enhancement management (Secretariat: Corporate Planning Department, Company Society 2 5 Employees Brand Communication Department) (1) Contribute to health enhancement of customers through SUMITOMO LIFE Vitality Promotion of Sustainability Initiatives (2) Convey the importance and value of health enhancement to the world (3) Contribute to a “healthy and long-living society” by enhancing health of ・ Discussion and review of initiatives to achieve the SDGs customers (4) Those who understand the importance and value of health enhancement ・ Information sharing on social and environmental issues, etc. become new customers (5) Cultivate pride and job satisfaction by contributing and being indispensable to the society (6) Positive evaluation as an entity that supports health 1. CSV is abbreviation of Creating Shared Value and a business concept which means achieving both resolving social challenges and increasing corporate value (including profit and competitiveness). 47

Initiative to Sustainability③ Promote Responsible Investment after setting Basic Principles on Responsible Investment and social issues to be focused on Basic Principles on Responsible Investment 1 The Company shall systematically consider non-financial information including ESG factors and make investment decisions based on the characteristics of each asset. 2-1 In stewardship activities, the Company shall accurately assess the conditions (including sustainability) of portfolio companies, seek to share mutual understanding with them through dialogue and exercising voting rights, encourage them to improve problems, and promote their medium- to long- term corporate value improvement and sustainable growth. 2-2 The Company shall request companies that it engages in dialogue with to appropriately disclose information on ESG issues. 2-3 The Company shall establish guidelines that clarify the criteria for exercising voting rights and other related matters, and exercise voting rights accordingly. 2-4 The Company shall perform stewardship activities in accordance with the Sumitomo Life Group Code of Conduct, the Conflict of Interest Management Policy, and the Conflict of Interest Management Regulations, while complying with laws, regulations and provisions related to the management of conflicts of interest. 3 In addition to individual dialogue, the Company shall collaborate with other institutional investors to resolve globally important ESG issues such as climate change response through participation in Japanese and overseas initiatives. The Company shall also endeavor to promote responsible investment by actively participating in various meetings held by such initiatives, etc. 4 The Company shall publicly disclose information on its efforts for responsible investment (including the disclosure items stipulated by the Stewardship Code) via its website and by other means, and regularly update the information. 5 To appropriately implement the PDCA cycle, the Company shall set up the “Responsible Investment Committee” and establish other structures as necessary, while aiming to develop human resources with necessary skills and knowledge. Social Issues to be Focused on Through Responsible Investment An urgent issue for the whole world and an important issue that could cause damage to the Climate change response asset value. We will encourage the transition to a carbon-free society through responsible investment. Health and welfare / As a life insurance company, we will address the issues of health and welfare and aging Aging population population, including COVID-19 response. We will promote the medium- to long-term corporate value improvement of portfolio companies Economic growth through dialogue and contribute to the growth of the Japanese economy as a whole, including (including diversity) regional economies. We will also address diversity, including the active participation of women, as an important issue. Development of social As an institutional investor who manages assets over the medium- to long-term, we will provide infrastructure medium- to long-term funding for the development of social infrastructure. 48

You can also read