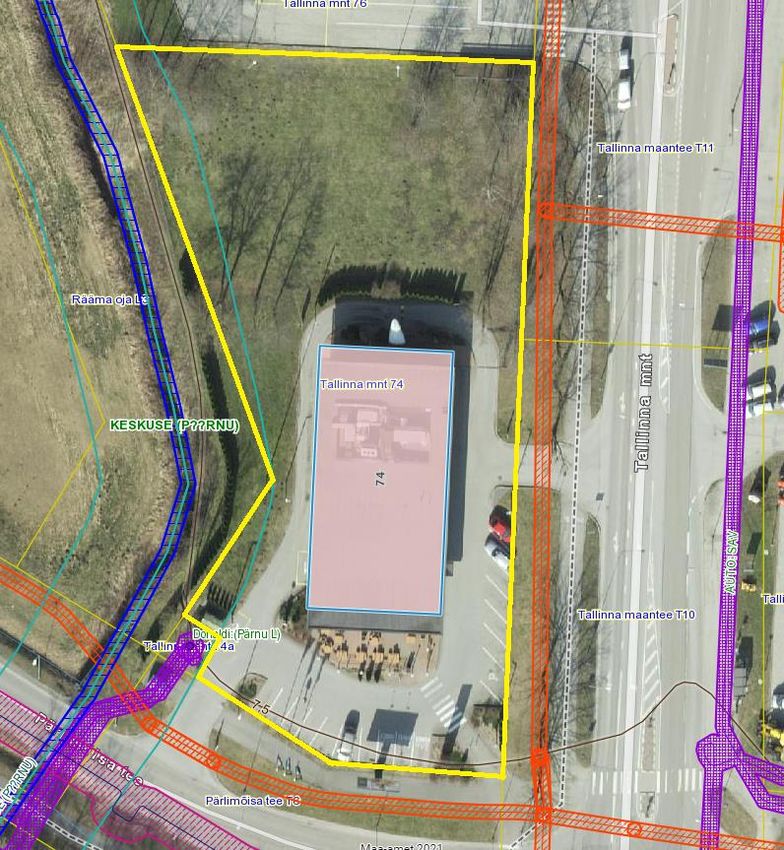

VALUATION REPORT Restaurant building - Tallinn Road 74, Pärnu County, Estonia - Hili Properties

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

VALUATION REPORT Restaurant building – Tallinn Road 74, Pärnu County, Estonia Report No 81/E/21 Date of valuation report: September 29, 2021

VALUATION REPORT No. 81/E/21

Table of Contents

Executive Summary ........................................................................................................................................... 4

Material valuation uncertainty due to Coronavirus (COVID – 19)..................................................................................... 5

Probability of changes ............................................................................................................................................................ 6

Special valuation Conditions ............................................................................................................................. 7

Customer of Valuation and Task ........................................................................................................................................... 7

Date of Inspection, valuation and Preparation of Valuation Report ................................................................................ 7

Extent of the inspection .......................................................................................................................................................... 7

Property Valuer ....................................................................................................................................................................... 7

Basis of valuation .................................................................................................................................................................... 7

Valuation for financial statements prepared under IFRS ................................................................................................... 8

Investment property – valuation under IAS 40 .................................................................................................................... 8

Valuation for secured lending purposes .............................................................................................................................. 8

Materials used ......................................................................................................................................................................... 9

Assumptions and Limitations ........................................................................................................................... 9

Material valuation uncertainty due to Coronavirus (COVID – 19)................................................................................... 10

Probability of Changes ......................................................................................................................................................... 11

Environmental matters ................................................................................................................................... 11

Conflict of interest ........................................................................................................................................... 11

Confidentiality and disclosure ........................................................................................................................ 11

Copyright ........................................................................................................................................................... 12

Compliance with Standards and Status of Valuers ...................................................................................... 12

General Description and Legal Status of the Subject Property ................................................................... 13

Identification data ................................................................................................................................................................. 13

Restrictions ............................................................................................................................................................................. 13

Encumbrances ....................................................................................................................................................................... 13

Mortgages .............................................................................................................................................................................. 14

Other restrictions .................................................................................................................................................................. 14

Access ...................................................................................................................................................................................... 15

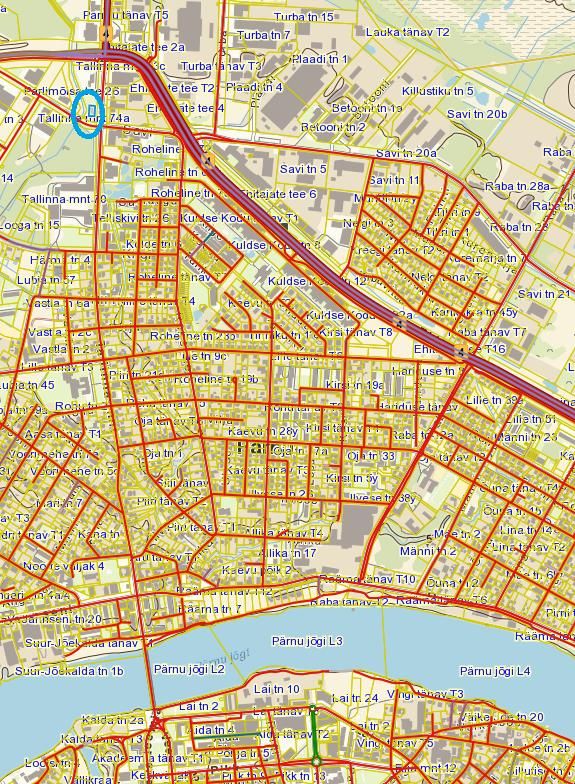

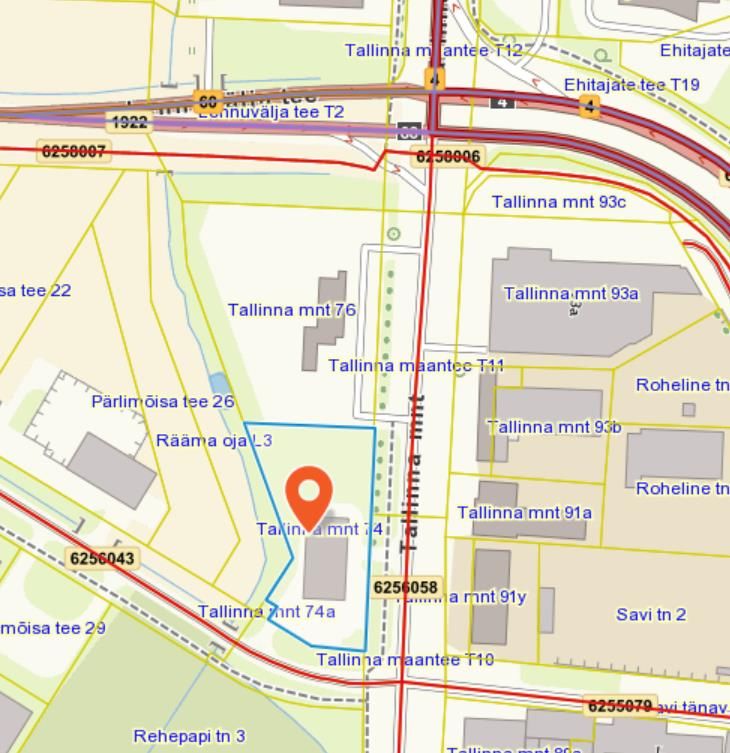

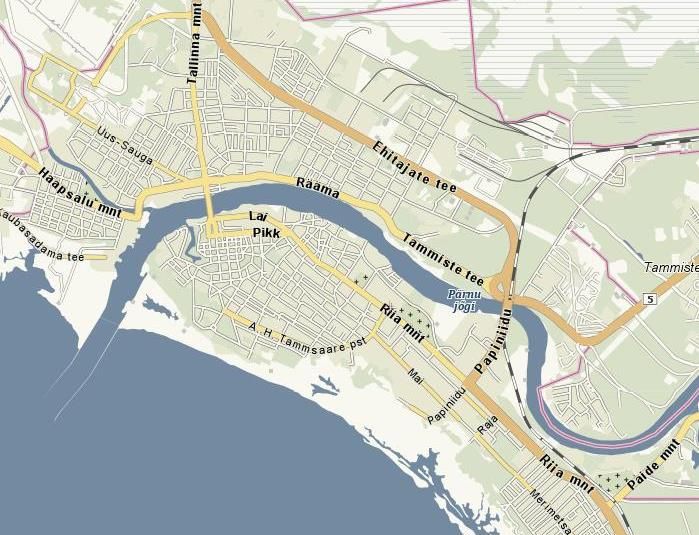

Location of the Subject Property .................................................................................................................... 16

Maps ....................................................................................................................................................................................... 16

Description of Location ........................................................................................................................................................ 18

Location main parameters macro level ................................................................................................................ 18

Location main parameters micro level ................................................................................................................. 19

Infrastructure ........................................................................................................................................................... 19

Subject Property Description .......................................................................................................................... 20

Site description ...................................................................................................................................................................... 20

Territory characteristics .......................................................................................................................................... 20

External engineering networks .............................................................................................................................. 21

Legal use / zoning / planning ................................................................................................................................. 21

Building description .............................................................................................................................................................. 23

Summary of main parameters ............................................................................................................................... 23

Detailed Description of Buildings (Structures) ..................................................................................................... 23

Highest and best use ............................................................................................................................................................. 25

Quality class ........................................................................................................................................................................... 26

Direct competitors ................................................................................................................................................................. 26

Current marketability of the property ................................................................................................................................ 26

Overview of the lease contract/s ......................................................................................................................................... 26

Basic agreement terms ........................................................................................................................................... 27

COLLIERS INTERNATIONAL ADVISORS 1

VALUATION REPORT No. 81/E/21

Market analysis ................................................................................................................................................ 29

Economic Overview ............................................................................................................................................................... 29

2018-2019 Summary ............................................................................................................................................... 29

2020-2021 .................................................................................................................................................................. 30

Forecasts ................................................................................................................................................................... 32

Estonian Real Estate Market Overview ............................................................................................................................... 34

Investment Market 1HY 2021............................................................................................................................................... 36

General Overview .................................................................................................................................................... 36

Investment Volumes ................................................................................................................................................ 36

Investment Properties ............................................................................................................................................. 37

Investment Yields ..................................................................................................................................................... 39

Trends and Forecasts .............................................................................................................................................. 39

Pärnu Retail Market 2021 .................................................................................................................................................... 40

Supply ........................................................................................................................................................................ 40

Demand ..................................................................................................................................................................... 46

Rent Rates and Vacancy .......................................................................................................................................... 47

Street Retail in Pärnu ............................................................................................................................................... 48

Tendencies in Pärnu Retail Market ........................................................................................................................ 49

Valuation ........................................................................................................................................................... 51

Methodology of the valuation Approaches ........................................................................................................................ 51

Selection of valuation approach ............................................................................................................................ 53

Process of valuation by Income method ............................................................................................................................ 53

Leasable area and current rental value ................................................................................................................ 54

Market Rent .............................................................................................................................................................. 54

Lease length.............................................................................................................................................................. 54

Market rent and rental earnings............................................................................................................................ 54

Rent to Turnover ratio Analysis ............................................................................................................................. 55

Calculation of Potential Gross Income .................................................................................................................. 56

Additional income .................................................................................................................................................... 57

Discounts .................................................................................................................................................................. 57

Vacancy ..................................................................................................................................................................... 57

Operating expenses, needed investments ........................................................................................................... 57

Indexation ................................................................................................................................................................. 59

Market / Exit Yield .................................................................................................................................................... 59

Discount Rate ........................................................................................................................................................... 61

Calculation of Market Value by Discounted Cash Flow Method ........................................................................ 63

Sensitivity analysis ................................................................................................................................................... 67

Final Conclusion ............................................................................................................................................... 68

Certification ...................................................................................................................................................... 70

Annexes ............................................................................................................................................................. 71

Annex 1 – Selection of Photos ................................................................................................................................ 71

Annex 2 – Extract from Land Register ................................................................................................................... 74

Annex 3 – Rentroll .................................................................................................................................................... 76

COLLIERS INTERNATIONAL ADVISORS 2

VALUATION REPORT No. 81/E/21 Figure 1: Contractual and potential gross income € '000" projection for next 5 years. ....................................................................................... 27 Figure 2: GDP, inflation, wages and unemployment rate, year-on-year change, 2004-2022............................................................................... 30 Figure 3: Real estate market dynamics in Estonia, 2004-2021 ................................................................................................................................ 34 Figure 4: Distribution of notarised purchase-sale transactions in Estonia by counties, 1HY 2021 ..................................................................... 35 Figure 5: Dynamics of Investment Volume in Estonia, 2010-2021 ......................................................................................................................... 36 Figure 6: Average Transaction Size by Sector in 1HY 2021 ...................................................................................................................................... 37 Figure 7: Investment Turnover by Size in 1HY 2021................................................................................................................................................. 37 Figure 8: Investment Turnover by Sector in 1HY 2021 ............................................................................................................................................ 38 Figure 9: Prime Yield Dynamics, 2008-2021 .............................................................................................................................................................. 39 Figure 10: Volume of building and occupancy permits issued for retail premises in Pärnu (sqm), 2009-2020................................................. 40 Figure 11: Total retail space in Pärnu by type........................................................................................................................................................... 41 Figure 12: Dynamics of retail space in Pärnu, 2006-2021 ....................................................................................................................................... 42 Figure 13: Pärnu retail market map ........................................................................................................................................................................... 44 Figure 14: Average turnover and visitors per sqm of GLA per month in Estonia ................................................................................................. 46 Figure 15: Street retail market in Pärnu .................................................................................................................................................................... 48 Figure 16: Contract rent versus to market rent in 5 years horizon ........................................................................................................................ 55 Figure 17: Tallinn road 74, Pärnu County, Estonia calculation model .................................................................................................................... 64 Table 1: Subject Property Structure ........................................................................................................................................................................... 13 Table 2: Encumbrances intended for Subject property ........................................................................................................................................... 13 Table 3: Tenant occupancy accordance to total Leasable area .............................................................................................................................. 27 Table 4: Rent revenues by type of premises ............................................................................................................................................................. 27 Table 5: GDP growth forecasts, 2017-2022 ............................................................................................................................................................... 31 Table 6: Inflation, unemployment rate and wages growth and forecasts, 2008-2022 ......................................................................................... 31 Table 7: GDP growth forecasts, 2017-2022 ............................................................................................................................................................... 33 Table 8: CPI forecasts, 2017-2022 .............................................................................................................................................................................. 33 Table 9: Unemployment forecasts, 2017-2022 ......................................................................................................................................................... 33 Table 10: Pärnu retail market volume ....................................................................................................................................................................... 41 Table 11: New retail developments in Pärnu in 2013-2021 .................................................................................................................................... 42 Table 12: Distribution of retail space in grocery stores by grocery chains in Pärnu, 2021 .................................................................................. 43 Table 13: Pärnu shopping centres and retail objects .............................................................................................................................................. 44 Table 14: Rent rates in Pärnu, 2020 ........................................................................................................................................................................... 48 Table 15: The summary of rental earning by type of space usage ......................................................................................................................... 54 Table 16: Comparable lease transactions with retail/service/catering space ....................................................................................................... 54 Table 17: Contract and Market rent comparison by type of premises .................................................................................................................. 55 Table 18: Indicative effort rates per business categories on gross sales............................................................................................................... 56 Table 19: Rent to turnover ratio analysis in Premier Restaurants Eesti OÜ in overall ......................................................................................... 56 Table 20: Potential gross income from leased premises......................................................................................................................................... 57 Table 21: Expected structural vacancy ...................................................................................................................................................................... 57 Table 22: Figure below summarizes estimated OPEX / CAPEX in annual bases for 1st operational year .......................................................... 58 Table 23: Indexation .................................................................................................................................................................................................... 59 Table 24: Main investment transactions in Region towns, 2014 – 2020 ................................................................................................................ 59 Table 25: Discount rate / WACC calculations ............................................................................................................................................................ 62 Table 26: Sensitivity Analysis ...................................................................................................................................................................................... 67 COLLIERS INTERNATIONAL ADVISORS 3

VALUATION REPORT No. 81/E/21

Executive Summary

Client Hili Properties Plc (represented as signing party to the valuation services agreement

by Premier Estates LTD SIA, (reg. No. 40003993068) 2B Satekles iela, Riga, Latvia.

Valuer Colliers International Advisors (reg. No 11330404)

Agreement with client No. 2895/VD/21, dated 26 July 2021

Owner of Property Premier Estates Eesti OÜ (Reg. no. 11740668)

Subject Property Real Property interests consists of one land plot with commercial building

(Standalone / Drive-by Fast-food restaurant) on it.

General description The Subject Property consists of a land plot with a fast-food restaurant building.

Property units 1

Address Tallinn road 74, Pärnu County, Estonia

Land book IDs Property cadastral ID Land Book file No. Ideal Parts

Tallinn road 74, Pärnu 62503:071:0001 2693505 1/1

County, Estonia

Land tenure Freehold

Type of use Current use: Fast food restaurant

Property key Total land area m2 Total net building Net leasable area, m2

parameters internal area, m2

Tallinn road 74, Pärnu 4,415 490.4 490.4

County, Estonia

Purpose of the Valuation report to be included in the Prospectus or Circular of the prospective IPO of

valuation Hili Properties plc, a company registered in the Republic of Malta (reg. No: C 57954)

Intended users of Client and related entities, prospective investors.

report

Applied valuation The Market Value is determined in accordance with the appropriate methodology as

standard applied on the local market and the national valuation standards (Estonian Valuation

Standards EVS - 875) prepared by the Estonian Association of Valuators (EKHÜ), which

based on the International Valuation Standards (IVS). The terms and valuation

methodology used in the Valuation Report corresponds the principles of Royal

Institution of Chartered Surveyors (RICS) Valuation – Professional Standards “Red

Book”.

We particularly pay - It assumes that the property is completed in accordance with the plans and

your attention to the specifications described in this report. It assumed good quality of workmanship in

following assumptions construction.

- In respect of the freehold / leasehold property, usual property owner’s fixtures such

as lifts, heating, ventilation, air conditioning have been treated as an integral part

of the premises and are included within the asset valued.

Special assumptions, - As part of the agreed scope of work the current valuation instruction is carried out

instructions, or taking into account Chapter 7 of the Capital Markets Rules of the Malta Financial

departures Services Authority.

- In accordance with Chapter 7 of the Capital Markets Rules this valuation is based

on open market value for existing use.

- Estimations are based on the tenancy schedule (contractual leased areas, rent

rates, agreement expiry terms, indexation terms, reimbursable expenses) as

provided by the Client; the information has been critically reviewed (but not

verified), adjusted where the Valuer has considered it necessary, and subsequently

all assumptions used in the calculations are confirmed by the Valuer to correspond

current market conditions and practice.

COLLIERS INTERNATIONAL ADVISORS 4

VALUATION REPORT No. 81/E/21

Inspection date August 09, 2021

Value date August 09, 2021

Date report issued September 29, 2021

Results found

Market Value EUR 1,600,000 One million six hundred thousand euros

VAT Stated value does NOT include value added tax (VAT)

Method of Valuation The Market Value estimate is estimated using the Income Approach, which is applied

through the Discounted Cash Flow method. Market approach or Sales comparison

method was considered as back-up approach for designation of market sales evidences

to secure and justify market value estimated using income method.

Notes to results Due to nature and volume of the Subject Property, the accuracy class of the Market Value

accuracy of Subject Property can be considered as average (+/- 10%).

Notes to liquidity In the context of Estonian real estate market, estimated Market Value of the Subject

Property is average (majority of the transactions are done with properties up to +/- 5

million euros). Since, the Subject Property is very well positioned contemporary

commercial building (Fast food restaurant), with several competitors in the same division

the liquidity can be considered less than average.

Notes on time of Based on recent market transactions with larger commercial properties and, as well as

exposition discussion with market participants, a sale of the subject property at the above-stated

opinion of Market Value would have required an average exposure time of 6 – 12

months. Furthermore, a marketing period of at least 6 months is currently warranted for

subject property.

Notes to results None

The Market Value valuation is based on the analysis of the information provided by the Client and available in

Estonian public registers or authorities. The contents of this Valuation Report are intended to be confidential

to the addressees and for the specific purpose stated. Consequently, and in accordance with current practice,

no responsibility is accepted to any other party in respect of the whole or any part of its contents. Before the

Valuation Certificate or Report or any part of its contents are reproduced or referred to in any document,

circular or statement or disclosed orally to a third party, our written approval as to the form and content of

such publication or disclosure must first be obtained. For avoidance of doubt, such approval is required

whether this firm is referred to by name and whether or not our Valuation Report is combined with others.

The conditions, assumptions and limiting factors listed in further sections of this report are an integral part of

the valuation report. The presented results, opinions and conclusions should be considered only in the context

of this report as a whole. Additional information, including documents and information provided to the Valuer

that is not included in this report, as well as further explanations to calculations and conclusions are available

upon request.

Material valuation uncertainty due to Coronavirus (COVID – 19)

The outbreak of the Coronavirus (COVID-19) declared by the World Health Organisation as a “global health

emergency” on the 30th of January 2020, has impacted global financial markets. In Estonia, as at the valuation

date, the quantum of transaction volumes of comparable market evidence in the specific market segment of

the valued property, upon which to base opinions of value, was inadequate. At current stage, the crisis is

regarded to have a short- to mid-term effect on the property market, subsequently within this valuation

assignment alterations (compared to pre-crisis) have been made only to those considerations and inputs that

can be supported by up-to-date market evidence. Consequently, less certainty – and a higher degree of caution

– should be attached to this valuation than would normally be the case. Given the unknown impact that COVID-

19 might have on the real estate market in the longer term, it is recommended for the terminal user of this

document to keep the valuation of this property under frequent review.

COLLIERS INTERNATIONAL ADVISORS 5

VALUATION REPORT No. 81/E/21

Probability of changes

The value of the Subject Property that is the subject of this report is established as of valuation date. Constantly

changing market situation, country mortgage politic, economic, social, political and physical conditions have

varying effects upon real property value. Even after the passage of a relatively short or mid-term period of time,

property value may change substantially and require a review based on differing market conditions.

Complier: Verifier:

Elena Kuslap Aleksander Sibul, MRICS

Valuer

Head of valuation

Certified Valuer No. 169726

Certified Valuer No. 116137

Member of the Estonian Association of Valuers

Colliers International Advisors OÜ

Colliers International Advisors OÜ

Date of valuation report: September 29, 2021

COLLIERS INTERNATIONAL ADVISORS 6

VALUATION REPORT No. 81/E/21

Special valuation Conditions

Customer of Valuation and Task

The Subject Property was valued and the valuation report was prepared on request of PREMIER ESTATES LTD

SIA, according to agreement with client No. 2895/VD/21, dated 26 July 2021.

Scope of valuation has been agreed with the Customer as following: to estimate the Market Value of the Subject

Property located at Tallinn road 74, Pärnu County, Estonia, to estimate the Market Value of the Subject Property for

to estimate the Market Value of the Client to be included in the Prospectus or Circular of the prospective IPO of Hili

Properties plc.

Date of Inspection, valuation and Preparation of Valuation Report

The Subject Property was inspected, and the pictures were taken on August 09, 2021 by Colliers International

Advisors’ Certified Valuer Elena Kuslap. The inspection was coordinated by the Landlord representative – Ms

Annika Vaarma. Photographs taken on this date are included in the Annexes.

The Market Value of the Subject Property was estimated as of August 09, 2021 based upon data and

information presented by the Customer, also considering market conjuncture conditions on the date of

valuation.

This valuation report is prepared on September 29, 2021 (date of report).

Extent of the inspection

A basic inspection was carried out. The Valuer inspected the property as a whole to be ensured that, or does it

correspond to the overall quality demands and standards. No detailed inspection (room by room) was carried

out. We rely on owners’ representative’s statements about the condition of the rooms the Valuer could or did

not inspect.

Property Valuer

The Subject Property was valued and the valuation report was prepared by Colliers International Advisors OÜ

(code of a legal entity 11330404), Certified Valuer Elena Kuslap (qualification certificate of real property valuer

No. 169726 issued by Kutsekoda SA) and by RICS Registered and certified Estonian Real Property Valuer

Aleksander Sibul, MRICS, (qualification certificate of real property valuer No. 069702 issued by Kutsekoda SA,

certificate no 116137).

Basis of valuation

We as assessing the Market Value of the property in accordance with the Estonian Valuation Standards (EVS

875-3), International Valuation Standards (IVS) and RICS Valuation Standards as follows:

“Market Value – The estimated amount for which an asset or liability should exchange on the valuation date

between a willing buyer and a willing seller in an arm’s length transaction after proper marketing and where the

parties had each acted knowledgeably, prudently and without compulsion” (RICS, IVS, EVS-875)

The Market Rent is also defined according to the manuals of the above-mentioned associations as follows:

“Market Rent – The estimated amount for which a property would be leased on the valuation date between a

willing lessor and a willing lessee on appropriate lease terms in an arm’s length transaction, after proper

marketing and where the parties had each acted knowledgeably, prudently and without compulsion” (RICS, IVS,

EVS-875)

Market value is understood as the value determined for any given asset, without accounting for costs

associated with its sale or purchase, or compensation of the cost from any applicable taxes.

The concept of Market Value presumes a price negotiated in an open and competitive market where the

participants are acting freely. The market for an asset could be an international market or a local market. The

COLLIERS INTERNATIONAL ADVISORS 7

VALUATION REPORT No. 81/E/21

market could consist of numerous buyers and sellers or could be one characterized by a limited number of

market participants. The market in which the asset is presumed exposed for sale is the one in which the asset

notionally being exchanged is normally exchanged. (IVS).

Valuation for financial statements prepared under IFRS

According to IFRS end-of-the-year market value should be estimated under IFRS in accordance with IAS 40 fair

value disclosure requirement. Valuations for financial statements prepared under International Financial

Reporting Standards (IFRS) shall be in accordance with the IVSC International Valuation Application 1 (IVA 1).

According to RICS Red Book Valuations should be reported at Market Value. Any assumptions or qualifications

made in applying Market Value should be discussed with the entity and disclosed in the report. Although under

IVA 1 the valuer will report the Market Value, the entity is required under IFRS to account for the asset at its fair

value.

Investment property – valuation under IAS 40

Investment property should be recognized as an asset when it is probable that the future economic benefits

that are associated with the property will flow to the enterprise, and the cost of the property can be reliably

measured.

Examples of investment property:

▪ Land held for long-term capital appreciation

▪ Land held for undecided future use

▪ Building leased out under an operating lease

▪ Vacant building held to be leased out under an operating lease

▪ Property that is being constructed or developed for future use as investment property

IAS permits entities to choose either:

1. Fair value model, under which an investment property is measured, after initial measurement, at fair

value with changes in fair value recognized in profit or loss; or

2. Cost model. The cost model is specified in IAS 16 and requires an investment property to be measured

after initial measurement at depreciated cost (less any accumulated impairment losses). An entity that

chooses the cost model discloses the fair value of its investment property.

The fair value of investment property is the price at which the property could be exchanged between

knowledgeable, willing parties in an arm’s length transaction.

An investment property shall be derecognized (eliminated from the balance sheet) on disposal or when the

investment property is permanently withdrawn from use and no future economic benefits are expected from

its disposal.

Gains or losses arising from the retirement or disposal of investment property shall be determined as the

difference between the net disposal proceeds and the carrying amount of the asset and shall be recognized in

profit or loss (unless IAS 17 requires otherwise on a sale and leaseback) in the period of the retirement or

disposal.

Valuation for secured lending purposes

Valuation of the property for Secured Lending Purposes is to be undertaken in accordance International

Valuation Application 2 (IVA 2).

The manner in which property would ordinarily trade in the market will determine the applicability of the

various approaches to assessing Market Value. Based upon market information, each approach is a

comparative method, and the use of more than one method may be required.

Each relevant valuation method will, if appropriately and correctly applied, lead to a similar result. All valuation

methods should be based on market observations. Construction costs and depreciation, where they apply,

should be determined by reference to an analysis of market-based estimates of costs and accumulated

COLLIERS INTERNATIONAL ADVISORS 8

VALUATION REPORT No. 81/E/21

depreciation. The use of an income method, particularly discounted cash flow techniques, will also be based

on market-determined cash flows and market-derived rates of return.

Materials used

For the completion of this report, we have used the following documents/information:

▪ Estonian Property Valuation Standards (EVS 875);

▪ International Valuation Standards (IVS);

▪ RICS Valuation Standards – Global;

▪ Estonian Land Board database www.maaamet.ee;

▪ Estonian Building Register database www.ehr.ee;

▪ Bank of Estonia database www.eestipank.info;

▪ Estonian Land Board’s transaction database;

▪ Pärnus’s planning register https://parnu-lv.maps.arcgis.com/;

▪ Data from Colliers International Advisors OÜ databases about real estate market;

▪ Extracts from the electronic Land Book, extracted on August 10, 2021;

▪ Rent roll information provided August 2021, provided by Client representative;

▪ Lease agreement dated 01 June 2010 with Premier Restaurants Eesti OÜ;

▪ Research & Forecast report by Colliers International Advisors, 2020, Economic Overview and Commercial

Market Overview;

▪ Also other information provided by the Client (or Owner), including e-mails, conversations, commentaries,

etc.;

▪ Information collected from real estate brokers, banks, property developers, managers, owners and other

sources;

▪ Data from Colliers International Advisors OÜ databases about the real estate market;

▪ Other legal, methodological and information sources.

We note that we have been granted access to copies of the rent agreements in order to verify the provided

information.

Quality of available information assessment: to large extent sufficient / reliable. Valuer has in general relied on

this information to be accurate and has generally not found any reason to believe otherwise. Our report is

therefore using this information as basis for our valuation.

Assumptions and Limitations

This Valuation Report (hereinafter referred to as Report) has been made with the following assumptions and

limiting conditions:

▪ The Conclusion is valid only in its entirety and for the purposes identified herein.

▪ The Valuer has acted independently in gathering all data, and information contained in this report is

veracious and presented without influence from third parties. The report is valid on the assumption that

the data and information presented by the Client is also veracious and all conditions of validity are fulfilled.

The Valuer is not responsible for incorrect data, which is presented to us, and for which the validity could

not be verified or was not reasonably grounded.

▪ The Valuer’s opinion on the Market Value of the Subject Property is valid only as of the date of the

valuation. The Valuer shall not be held responsible for any subsequent social, economic, legislative or

environmental changes, which may affect the value of the Subject Property appraised.

▪ We have assumed that the information and documentation supplied is correct and that our understanding

of the situation is also correct.

COLLIERS INTERNATIONAL ADVISORS 9VALUATION REPORT No. 81/E/21

▪ The Valuer has not calculated, nor measured specific areas, and has relied upon area figures provided to

us, which we assume to have been calculated in accordance with local market practice.

▪ The Valuer has not carried out structural surveys, nor have they inspected those parts of the properties,

which are covered, unexposed or inaccessible, and such parts have been assumed to be in good standing

and condition. We cannot express an opinion about or advice upon the condition of un-inspected parts,

and this report should not be taken as making any implied representation or statement about such parts.

We have considered the general condition of properties, as observed in the course of our inspection for

valuation purposes.

▪ The Valuer has made a visual inspection of the Subject Property; analysed and appraised it under the

assumption that it was not subject to factors hazardous for the existing use of the Subject Property.

▪ The Market Value of the Subject Property is determined on the assumption that the Subject Property is

free and clear of any lien, is not used to secure a debt obligation and is not under arrest. Moreover, Valuer

has also proceeded from the assumption that the Subject Property is free from third party claims or any

other encumbrances.

▪ Neither Client, nor Valuer can use this Report (or any part of it) in any manner other than how it is

stipulated by the agreement between the Client and the Valuer.

▪ The Valuer will not be responsible for losses the Client or the third party may incur, in the event of

dissemination, publication or use of this Report for purposes inconsistent with provisions of this section.

▪ The Market Value is determined on the assumption that the data presented by the Client and/or the Owner

about the Subject Property’s ownership boundaries and size is correct.

▪ In respect of the freehold / leasehold property, usual property owner’s fixtures such as lifts, heating,

ventilation, air conditioning have been treated as an integral part of the premises and are included within

the asset valued.

▪ Valuation is based on tenancy schedule provided by Client; valuation is made with assumption that

provided tenancy schedule is valid and there are no ongoing lease renegotiations on the date of valuation.

The Valuer would like to emphasize, that the Valuer is responsible only to the Client and is free from any

obligations to other parties.

Neither this, nor any other limiting conditions shall be considered as try to limit this report to use as evidence

during court or similar process. In such a case, institutions of justice have right to decide to use this report in

such way that it could, as much as it is possible, serve for sake of justice. Upon separate request, the author of

this report would stand in the court or other institution of justice in process, which is related with valuation of

this property. In such case, there shall be prior agreement for such every time estimating additional fee and

sufficient time for preparation.

This report is valid only with original signatures of the authors (incl. secured digital signatures).

Material valuation uncertainty due to Coronavirus (COVID – 19)

The outbreak of the Coronavirus (COVID-19) declared by the World Health Organisation as a “global health

emergency” on the 30th of January 2020, has impacted global financial markets. In Estonia, as at the valuation

date, the quantum of transaction volumes of comparable market evidence in the specific market segment of

the valued property, upon which to base opinions of value, was inadequate. At current stage, the crisis is

regarded to have a short- to mid-term effect on the property market, subsequently within this valuation

assignment alterations (compared to pre-crisis) have been made only to those considerations and inputs that

can be supported by up-to-date market evidence. Consequently, less certainty – and a higher degree of caution

– should be attached to this valuation than would normally be the case. Given the unknown impact that COVID-

19 might have on the real estate market in the longer term, it is recommended for the terminal user of this

document to keep the valuation of this property under frequent review.

COLLIERS INTERNATIONAL ADVISORS 10VALUATION REPORT No. 81/E/21 Probability of Changes The value of the Subject Property that is the subject of this report is established as of valuation date. The continuously changing economic, social, political and physical conditions may affect the value of the real estate to a differing degree. Even after a relatively short period of time, the value of the property may change materially; this may require conducting a new valuation considering the effective market conditions. Environmental matters The valuation is on the basis that the property is not affected by proposals for road widening or Compulsory Purchase. We have in our investigations did not find any evidence of any plans. The Valuer has assumed that the property has been erected in accordance with valid planning permissions and are being occupied and used without any breach of that. We have not had access to detailed planning of the Municipality but have assumed, that property has been approved by local authorities and are used in accordance with existing legislation and planning. The Valuer has neither carried out a structural survey of the property, nor tested any services or other plant or machinery. We are therefore unable to give any opinion on the condition of the structure and services. However, our valuation takes into account any information supplied to us and any defects noted during our inspection. Otherwise, our valuation is on the basis that there are no latent defects, wants of repair or other matters which would materially affect our valuation. The Valuer has not investigated the presence or absence of High Alumina Cement, Calcium Chloride, Asbestos and other deleterious materials. In the absence of information to the contrary, our valuation is on the basis that no hazardous or suspect materials and techniques have been used in the construction of the property. The Valuer has not investigated ground conditions/stability and, unless advised to the contrary, our valuation is on the basis that all buildings have been constructed, having appropriate regard to existing ground conditions. The Valuer has not carried out any investigations or tests, nor been supplied with any information from you or from any relevant expert that determines the presence or otherwise of pollution or contaminative substances in the subject or any other land (including any ground water). Accordingly, our valuation has been prepared on the basis that there are no such matters that would materially affect our valuation. In the event it emerges after the valuation that there are pollutants or sources of pollution on the valuation object or in its neighbourhood or that the valuation object has been used in such a manner that can bring about pollution, then it may reduce the value given in the valuation report. Should this basis be unacceptable to you or should you wish to verify that this basis is correct, you should have appropriate investigations made and refer the results to us so that we can review our valuation. Conflict of interest Hereby Valuers declare that they, nor Colliers International as legal entities, do not have any conflict of interest while performing valuation of the subject property, and benefit from the valuation process only through receiving a fixed pre-agreed fee from the Client. Fee received by the Valuer for valuation procedure is not related to the valuation results. Confidentiality and disclosure Before this Valuation Report, or any part of thereof, is reproduced or referred to, in any document, circular or statement, and before its contents, or any part thereof, are disclosed orally or otherwise to a third party, the Valuer’s written approval as to the form and context of such publication or disclosure must first be obtained. Such publication or disclosure will not be permitted unless, where relevant, it incorporates the Assumptions referred to herein. For the avoidance of doubt, such approval is required whether or not Colliers International have been referred to by name. COLLIERS INTERNATIONAL ADVISORS 11

VALUATION REPORT No. 81/E/21 The Valuers understand that it shall be entitled to disclose the Valuation Report to such of its directors, officers, employees, financial institutions who are directly concerned with such information and whose knowledge of disclosed information it deems necessary. Copyright The authors reserve all copyrights. The possession of this report or its copy does not give the right to duplicate and distribute this report or any part hereof in any way whatsoever, publicize its content or the content of any of its parts, quote this report or make any references to it without the previous written consent of the authors to the specific publication, quotation or reference. Compliance with Standards and Status of Valuers This report has been prepared by Certified Valuer Elena Kuslap (qualification certificate of real property valuer No. 169726 issued by Kutsekoda SA) and Aleksander Sibul, RICS Registered and certified Estonian Valuer (certificate no 116137) as defined in Estonian Valuation Standards (EVS-875) and Royal Institution of Chartered Surveyors (RICS) as Chartered Surveyor (Membership No. 1301782). Valuer confirms that is in a position to provide an objective and unbiased valuation and is competent to undertake the subject valuation assignment; Valuer confirms that has sufficient current local, national and international (as appropriate) knowledge of the particular market and the skills and understanding to undertake subject valuation competently. The Market Value is determined in accordance with the Estonian Valuation Standards (EVS-875), International Valuation Standards (IVS) and RICS Valuation Standards. Colliers International Advisors OÜ is acting as External Valuer. External Valuer is defined in the Standards as “A Valuer that, together with any associates, has no material links with the client, an agent acting on behalf of the client, or the subject of the assignment.”. COLLIERS INTERNATIONAL ADVISORS 12

VALUATION REPORT No. 81/E/21

General Description and Legal Status of the Subject Property

Identification data1

Real Property interests consists of land site and one commercial (drive-by fast-food restaurant) building on it.

Table 1: Subject Property Structure

Address Tallinn road 74, Pärnu County, Estonia

Property cadastral ID 62503:071:0001

Land Book file No. 2693505

Ideal Parts 1/1

Cadastral unit area 4,415 m2

Zoning 75% Commercial land, 25% Industrial land

Owner of Property Premier Estates Eesti OÜ (Reg. No 11740668)

Basis of ownership Entered to the Land Register on the 26th of February 2010

# of land units 1

# of buildings 1

Reg. ID of building (s) 120591916

Name of Property -

Tenancy The Object is covered with a lease contract, single tenant. The parties of the lease

contract are associated companies – franchisee of a global enterprise, with the

term of 20 years, concluded on the 1st of June 2010 between related parties

Premier Estates Eesti OÜ and Premier Restaurants Eesti AS. According to the lease

contract the rent for the premises is 100,000 € per annum or 8,333.33 € in a month,

indexed every 5 years period. As of the Valuation date the rent for the premises is

9166.33 € in a month.

According to the assignment set by the Client, we have considered the valid lease

contract in estimating the Object’s Investment Value. The weighted average signed

leases maturity is 8.8 years.

Restrictions

Registered restrictions in the 2nd part of the respective Land Book folios and/or according to data presented by

Estonian Land Board (www.maaamet.ee). Valuer is not aware of any restrictions for the property, except of

those which are described below.

Encumbrances

Registered encumbrances in the 3rd part of the respective Land Book folios

Table 2: Encumbrances intended for Subject property

Valuer is not aware of any other encumbrances.

No. Description Influence on assessed Value

1 There are no valid legal encumbrances as of date of valuation. Does not have negative effect on

Subject Property’s Market Value.

1 The data is based on the extract from the land register as of 10th of August 2021.

COLLIERS INTERNATIONAL ADVISORS 13You can also read