The Impact of Mobile Money on Poverty - Research Brief - April 2021 - Bill ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Research Brief The Impact of Mobile Money on Poverty April 2021

DISCLAIMER This work is provided as-is, without any warranty of any kind, and for noncommercial, informational use only. Any further use may require the consent of third-party content owners. © Bill & Melinda Gates Foundation | April 2021 2

THE IMPACT OF MOBILE MONEY ON POVERTY

Mobile money accounts have spread widely

in select regions of the developing world,

particularly in Sub-Saharan Africa.

Over the past decade, evidence has emerged

citing beneficial impacts of mobile money in

developing economies on consumption, poverty, This presentation summarizes

labor outcomes, remittances, and migration. formative experimental and rigorous

non-experimental evidence from the

This has led to a surge in rigorous studies development economics literature.

focusing on the impact of mobile money on

poor and rural households who tend to be

unbanked and have nonexistent or very low

mobile money agent access.

© Bill & Melinda Gates Foundation | April 2021 3DEFINING MOBILE MONEY

“Mobile money enables mobile phone This Research Brief focuses on the individual and

household impacts of mobile money and, thus, takes

owners to deposit, transfer, and a broad definition of mobile money, focusing on the

user experience of account-to-account

withdraw funds without owning a transfers/payments enabled by mobile phones.

bank account. It is therefore distinct The studies covered leverage mobile money platforms

from mobile banking, which allows across a variety of providers and from a variety of

countries—including M-Pesa (Kenya), mKesh

access to one’s existing bank account (Mozambique), bKash (Bangladesh), and Airtel (Uganda,

Malawi, Niger).

via a mobile phone.”

Suri: 2017, Annual Review of Economics

These platforms operate under a diversity of regulatory

and licensing models for bank and non-bank led

approaches to mobile phone-based payments accounts.

Further information on regulation of mobile money

services can be found in the Inclusive Digital Financial

Services: A Reference Guide for Regulators1

1. https://docs.gatesfoundation.org/documents/InclusiveDigitalFinancialServices_ReferenceGuide.pdf

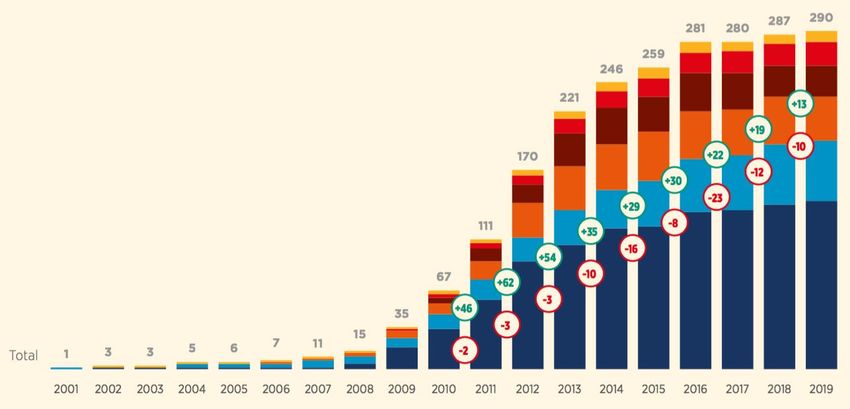

© Bill & Melinda Gates Foundation | April 2021 4EVOLUTION OF THE GLOBAL MOBILE MONEY SERVICES, 2001 TO 2019

Europe and Central Asia

Middle East and North Africa

Latin America and the Caribbean

South Asia

East Africa and Pacific

Sub-Saharan Africa

Source: GSMA State of the Industry Report on Mobile Money 2019

© Bill & Melinda Gates Foundation | April 2021 5THE RISE OF MOBILE MONEY: GLOBAL AND REGIONAL GROWTH IN 2020 Green arrows represent growth in 2020. Source: GSMA State of the Industry Report on Mobile Money 2020. © Bill & Melinda Gates Foundation | April 2021 6

THE IMPACT OF MOBILE MONEY ON POVERTY: KEY FINDINGS (1 OF 2)

Consumption, Risk Sharing, and Poverty Labor Outcomes and Investment

Mobile money had direct impacts on consumption, the ability to cope Mobile money impacted labor outcomes by allowing workers to shift into

with shocks, and extreme poverty. more productive occupations and firms to invest in fixed assets.

• Mobile money increased consumption expenditure by 44% when • In Northern Uganda, self-employment increased from 3% to 6% for

households experienced a flood shock in Mozambique (Batista and Vicente, individuals that lived far away from a bank branch (Weiser et al., 2019).

2020). • Women in Kenya increased self-employment by 2-3%. (Suri and Jack,

• Mobile money users in Kenya who experienced a negative shock saw no 2016)

change in their consumption level, whereas nonusers experienced a 7% • In Malawi, microentrepreneurs worked less in their primary business and

decrease in consumption (Jack and Suri, 2014). more on their farms (Aggarwal et al., 2020).

• Mobile money increased daily per capita consumption by 8% and reduced • In Bangladesh, rural households that had urban migrants were 17% less

the extreme poverty index by 42% when urban migrants remitted income likely to engage in wage labor (Lee et al., Forthcoming).

back to their household in rural Bangladesh (Lee et al., Forthcoming).

• Rural households in Mozambique reduced their agricultural investment by

• In Northern Uganda, mobile money increased food security by 45% for 28%, but saw an increase in their number of migrants, suggesting a shift

households that lived far away from bank branches (Weiser et al., 2019). from rural to urban occupations (Batista and Vicente, 2020).

• Kenyan female-headed households who lived in areas with many agents • Firms in Kenya, Tanzania, and Uganda that use mobile money saw a 16%

saw their long-run consumption grow by 8.5% (Suri and Jack, 2016). increase in the likelihood of investing in fixed assets (Islam et al., 2016).

© Bill & Melinda Gates Foundation | April 2021 7THE IMPACT OF MOBILE MONEY ON POVERTY: KEY FINDINGS (2 OF 2)

Remittances and Migration Savings

Mobile money users were more likely to send and receive remittances Mobile money does not tend to impact the level of savings*; however,

and to have additional household members migrate. there is suggestive evidence that mobile money accounts can be used

as a substitute for informal savings.

• Remittances received by Kenyan households increased their annual income

by 3-4%, following a negative shock (Jack and Suri, 2014). The biggest impact on savings seems to be for migrants and firms with

high cash turnover.

• In Mozambique, mobile money led to a 30% increase in the share of

migrants in a household. (Batista and Vicente, 2020). • Households in Bangladesh that had urban migrants and actively used

mobile money saved 296% more than nonusers (Lee et al., Forthcoming).

• In Bangladesh, mobile money increased the value of remittances by 28%

and the migration rate by 35% (Lee et al., Forthcoming). • 83% of microentrepreneurs in Malawi used mobile money accounts to save

when there were no withdrawal fees, and continued to save via mobile

• In Niger, 50% of households are willing to pay to use mobile money to send

money following the intervention once withdrawal fees increased (Aggarwal

remittances, but there is a lack of agent infrastructure to do so (Aker et al.,

et al, 2020).

2020).

*Weiser et al., 2019; Batista and Vicente, 2019; Jack and Suri, 2014

© Bill & Melinda Gates Foundation | April 2021 8RESEARCH BRIEFS:

THE IMPACT OF MOBILE MONEY

ON POVERTY

Bangladesh

4

Niger

9, 13

Sri Lanka

11

Kenya

Uganda

1, 2, 10, 12

5, 6, 10

Tanzania

7, 10

Malawi

8

Mozambique

3REPORTS SUMMARIZED

Relevance: Low High

Labor Outcomes

Consumption Remittances Migration Savings

Article Authors & Investment

Risk Sharing and Transaction Costs: Suri, Jack

1 Evidence from Kenya’s Mobile Money Revolution (2014)

The Long-Run Poverty and Gender Impacts Suri, Jack

2 of Mobile Money (2016)

Is Mobile Money Changing Africa? Batista, Vicente

3 Evidence from a Field Experiment (2020)*

Poverty and Migration in the Digital Age: Lee, Morduch, Ravindran,

4 Experimental Evidence on Mobile Banking in Bangladesh (Forthcoming) Shonchoy, Zaman

The Impact of Mobile Money on Poor Households: Wieser, Bruhn, Kinzinger,

5 Experimental Evidence from Uganda (2019)* Ruckteschler, Heitmann

Mobile Money and Risk Sharing Against Village Shocks (2018) Riley

6

Payment Mechanisms and Antipoverty Programs: Aker, Bounmijel,

7 Evidence from a Mobile Money Cash Transfer Experiment in Niger (2016) McClelland, Tierney

Cashing In (and Out): Experimental Evidence on the Effects of Mobile Money Aggarwal, Brailovskaya,

8 in Malawi (2020) Robinson

Migration, Money Transfers, and Mobile Money: Aker, Prina, Welch

9 Evidence from Niger (2020)

Does Mobile Money Use Increase Firms’ Investment? Islam, Muzi, Meza

10 Evidence from Enterprise Surveys in Kenya, Uganda, and Tanzania (2018)

Can Mobile-linked Bank Accounts Bolster Savings? De Mel, McIntosh, Sheth,

11 Evidence from a Randomized Trial in Sri Lanka (2018)* and Woodruff

Transaction Networks: Jack, Ray, Suri

12 Evidence from Mobile Money in Kenya (2013)

Mobile Money, Remittances, and Household Welfare: Munyegera, Matsumoto

13 Panel Evidence from Rural Uganda (2016)

*Study is currently a well-known working paper.

© Bill & Melinda Gates Foundation | April 2021 10SUMMARY OF ONBOARDING/TRAINING INTERVENTIONS ACROSS STUDIES

Many of the studies utilize some form of training for onboarding consumers or mobile money agents. Some onboarding interventions also distribute phones

and facilitate actual money transfers to encourage learning by doing. Note that these trainings with account administration and use are often quick, inexpensive, and,

therefore, quite different from many more comprehensive financial education interventions that have been examined elsewhere and shown to have little impact.

Study Date Onboarding in Randomized Control Trials

Can Mobile-linked Bank Accounts Bolster Savings? 2018* Participants were given a mobile phone, the minimum balance to open a savings account with the

Evidence from a Randomized Trial in Sri Lanka government bank, assistance linking the savings account to the mobile phone, and training on how to

make deposits to the savings account using the mobile phone.

Poverty and Migration in the Digital Age: Experimental 2020 Participants were given a 30-45 minutes training session on how to sign up and use mobile money

Evidence on Mobile Banking in Bangladesh (bKash).The session included at least five hands-on transactions.

Is Mobile Money Changing Africa? Evidence from a Field 2020* Participants were trained to deposit money onto the mobile account, make a purchase using mobile

Experiment money, and transfer mobile money to another mobile phone. Free trial money was given to the

participant.

The Impact of Mobile Money on Poor Households: 2019* Mobile money agents were recruited and given equipment, training, and marketing materials. There

Experimental Evidence from Uganda was no direct intervention with consumers to encourage mobile money use.

Cashing In (and Out): Experimental Evidence on the Effects 2020 Participants received a mobile phone and training on how to use a mobile money account.

of Mobile Money in Malawi

Payment Mechanisms and Antipoverty Programs: Evidence 2016 Participants were given a mobile phone and training on how to exchange e-money (mobile money

from a Mobile Money Cash Transfer Experiment in Niger digital currency) for cash.

*Study is currently a well-known working paper.

© Bill & Melinda Gates Foundation | April 2021 1101 02 03 04 05 06 07 08 09 10 11 12 13

Risk Sharing and Transaction Costs

MOBILE MONEY REDUCES VULNERABILITY TO SHOCKS

Authors: Tavneet Suri and William Jack

Journal: American Economic Review, 2014

Research Design: This study Descriptive Descriptive Impact Impact Impact

surveyed households across

Mobile Money Use Mobile Money Agents Consumption and Remittances Better Leveraging of

Kenya on welfare measures,

mobile money use, and Between 2008 and 2009, Between 2008 and 2010, Risk Sharing A negative shock increases Social Networks

remittances. In addition, the the share of Kenyan M-PESA agents increased Consumption levels the likelihood that M-PESA M-PESA users reach

study surveyed the entire households who used from 4,000 to 15,000, of M-PESA users are users receive remittances deeper into their social

network of M-PESA agents in M-PESA increased from whereas bank branches unaffected by negative by 9 percentage points. network to send and

locations where households 43% to 70%. grew by 20%. shocks, whereas non-users receive remittances in the

were interviewed. In the presence of a

experience a 7% drop negative shock, remittances presence of a negative

Survey Dates: in consumption. received by M-PESA users shock.

Households: Sept. 2008 – increases their annual

June 2010 consumption by about 4%.

Agents: March 2010

Households Using M-PESA Percent Growth 2008-2010 Consumption Levels After

Country: Kenya Negative Aggregate Shocks

275%

Sample: 2,017 households Non

and 7,700 agents 70% M-PESA

M-PESA

Users

Context: 70% of Kenya’s adult Users

population had adopted M- 43%

PESA Unaffected

7%

Contribution: Examines the Drop

impact of reducing the 20%

transaction costs of sending

remittances and a household’s

ability to cope with negative 2008 2009 Bank M-PESA

shocks Branches Agents

Jack, William, and Tavneet Suri. "Risk Sharing and Transactions Costs: Evidence from Kenya's mobile money revolution." American Economic Review 104, no. 1 (2014): 183-223.

© Bill & Melinda Gates Foundation | April 2021 1201 02 03 04 05 06 07 08 09 10 11 12 13

The Long-Run Poverty and Gender Impacts of Mobile Money

FEMALE-HEADED HOUSEHOLDS INCREASE FINANCIAL RESILIENCE AND

SAVINGS USING MOBILE MONEY IN KENYA

Authors: Tavneet Suri and William Jack

Journal: Science, 2016

Research Design: This study Descriptive Impact Impact Impact

uses long-term household data

Consumption Impact by the Numbers* Consumption Growth* Occupation*

to examine the impact of

changes in mobile money Kenyans consume approximately Mobile money lifted 2% of Kenyan Female-headed households The change in agent density

agent density1. US$2.50 on average each day. households out of poverty. That is, experienced an 18.5% increase in increased the share of women in

the increased availability of M- consumption due to an increase in business/ sales by 2% and

Survey Dates: 2008 – 2014

Poverty PESA agents “helped raise 194,000 agent density. decreased the share participating in

Country: Kenya households out of extreme poverty farming and secondary occupations

• Extreme Poverty: 43% of the

Sample: 1,608 households and induced 185,000 [female- by 3% and 1%, respectively.

sample live on less than US$1.25 Extreme Poverty*

headed households] to switch into

Context: 96% of Kenyan per day Increases in M-PESA agent density

business or retail as their main Savings*

households had used mobile • General Poverty: 66% of the caused the share of female-headed

occupation.” 2

money since its launch in sample live on less than US$2 households living in extreme Female-headed households

2007. increased their financial savings by

per day poverty to decrease by 21%; that is,

Contribution: Examines the from about 43% to about 34%. 22% due to the increase in agent

long-run impact of mobile

Occupations

194,000 Households density.

money, and in particular, Lifted Out of Extreme Poverty

• 25% of the sample are farmers Welfare Changes to Female Headed

differential impacts by gender. Households Due to

• 18% of the sample run a business Increases in Agent Density

*Impact results represent 185,00 Women HH Living in

the interquartile impact, i.e., Migration Extreme Poverty

Switched into Business or Retail

the difference between • 41% of households had

individuals at the 25th and at least one migrant +18.5%

75th percentiles of the agent

distribution - 21%

Increase in Agent Density Increase in

Consumption

1.Changes in agent density occurred between 2008 and 2010. 2.These results extrapolate the impacts derived from the sample to all households in Kenya. 3. Note: the study did not find impacts on migration. Citation: Suri, Tavneet, and William Jack. "The long-run poverty and

gender impacts of mobile money." Science 354, no. 6317 (2016): 1288-1292.

© Bill & Melinda Gates Foundation | April 2021 1301 02 03 04 05 06 07 08 09 10 11 12 13

Is Mobile Money Changing Africa?

MOBILE MONEY INCREASES THE ABILITY TO COPE WITH SHOCKS

IN MOZAMBIQUE

Authors: Cátia Batista and Pedro C. Vicente

Journal: Working Paper, 2020

Research Design: The Impact Impact Impact Impact

intervention introduced mobile

Consumption Labor Outcomes and Investment Rural to Urban Migration Mobile Money Transfers

money services to randomly

selected rural areas in Mobile money increases Agricultural activity decreased from Mobile money facilitates rural to Households who have access to

Mozambique. Individual and consumption expenditure in the 94% to 89% and agricultural urban migration by: mobile money and experience an

community-wide event of shocks. investment decreased by 28%. • Reducing remittance transaction aggregate flood shock are 11

demonstrations were held to percentage points more likely to

• Aggregate Flood Shock: 44% The reduction in agricultural activity costs

teach participants how to use receive a mobile money transfer

the service.

increase in consumption and investment, combined with the • Improving migration-based

expenditure than households who have access

increase in remittances and insurance possibilities

Intervention Active: July to mobile money and do not

• Household Shock: 21% increase migration, suggest an occupational Mobile money increases the share

2012 – June 2015 experience an aggregate flood

in consumption expenditure shift from rural to urban labor of migrants from exposed

Country: Mozambique shock.

activities. households by 15.8 percentage

Sample: 102 areas where points in the event of an aggregate

2,004 individuals were flood shock. Savings

surveyed Increases in Consumption Agricultural Activity

Expenditure Share of Households Mobile money does not have a

Context: The study took place significant impact on savings overall.

in a migration corridor. Aggregate Household 94%

Flood Shock Shock 89% However—households who have

Contribution: The area access to mobile money services

studied did not previously have

are 58 to 76 percentage points more

any mobile money services.

likely to save using mobile money

Themes: Examines responses compared to households in the

to aggregate and idiosyncratic +44%

unexposed group.

shocks. +21%

Exposed Group Exposed Group Unexposed Exposed

vs. Control Group vs. Control Group

For completeness, the research design also included behavioral games that were played in the field in order to illicit respondent’s marginal willingness to save and remit using mobile money.

Batista, Catia, and Pedro C. Vicente. ”Is mobile money changing rural Africa? evidence from a field experiment.” Working Paper, 2020.

© Bill & Melinda Gates Foundation | April 2021 1401 02 03 04 05 06 07 08 09 10 11 12 13

Poverty and Migration in the Digital Age

MOBILE MONEY REDUCES EXTREME POVERTY FOR FAMILIES OF

MIGRANTS IN BANGLADESH

Authors: Jean N. Lee, Jonathan Morduch, Saravana Ravindran, Abu S. Shonchoy, and Hassan Zaman

Journal: American Economic Journal: Applied Economics, Forthcoming

Research Design: The Impact Impact Impact

randomized control trial

Total Remittances: The intervention induced a Poverty: The intervention led to a 42% decline in Mobile Banking

selected migrant-household

pairs to facilitate and 26% increase in the value of total remittances the extreme poverty index of the exposed

encourage the use of a sent by urban migrants in the exposed group households that actively used bKash compared to Rural Households: Exposed rural households

Bangladesh mobile money compared to the unexposed group. the unexposed group. were 48 percentage points more likely to use

system, bKash, through a This suggests that new remittances were the bKash than the control group.

training intervention. The primary driver in the increase of total remittances

intervention taught participants Migration: The intervention led to a 7% decrease

rather than a substitution away from other means in the average household size of those exposed Urban Migrants: Urban migrants exposed to the

how to use mobile money and

of sending remittances. to the intervention and a 35% increase in the intervention were 47 percentage points more

translated the phone menus

from English to Bangla, the migration rate. likely to use bKash than the unexposed group.

local language. Consumption: Daily per capita expenditure in

Intervention Active: April households exposed to the treatment was 7.5% Labor:

2015 – June 2016 greater than households in the unexposed group.

• Exposed households that actively used bKash

Country: Bangladesh Likelihood of Using bKash

are 17% less likely to engage in wage labor.

Sample: 815 rural household- Remittances Daily Per Capita • For exposed households who actively used

urban migrant pairs Sent Expenditure bKash and engaged in self-employment, the 70% 68%

Context: The areas studied intervention led to a 42% increase in the

are rural, poor, and vulnerable number of self-employed people within the

to seasonal food insecurity household. The intervention did not

22% 21%

during the monga season. significantly induce households not engaged in

+26% self-employment to shift into self-employment.

Contribution: Examines the +7.5%

impact of mobile money as a

Unexposed Exposed Unexposed Exposed

facilitating mechanism

between rural-urban migration Exposed Group Exposed Group Rural Households Urban Migrants

pairs. vs. Control Group vs. Control Group

Lee, Jean N., Jonathan Morduch, Saravana Ravindran, Abu S. Shonchoy, and Hassan Zaman. ”Poverty and migration in the digital age: Experimental evidence on mobile banking in Bangladesh.” American Economic Journal: Applied Economics, Forthcoming.

© Bill & Melinda Gates Foundation | April 2021 1501 02 03 04 05 06 07 08 09 10 11 12 13

The Impact of Mobile Money on Poor Households

MOBILE MONEY INCREASES FOOD SECURITY IN RURAL UGANDA

Authors: Christine Wieser, Miriam Bruhn, Johannes Kinzinger, Christian Ruckteschler, and Soren Heitmann

Journal: World Bank Policy Research Working Paper, 2019

Intervention: The intervention Impact Impact Impact Impact Impact

rolled-out mobile money

Food Insecurity Labor Outcomes Impact by the No’s Usage Remittances

agents to randomly selected

areas in rural Northern Mobile money reduced the Mobile money stimulated In total, 8,576 households Mobile money agents Mobile money decreased

Uganda. share of households with the non-farm self- live in the exposed increased mobile money the costs of remittance

food insecurity. employment rate. communities. These usage. transactions.

Intervention Active: 2016 –

2017 This effect is likely due to This effect is likely due to impacts suggest that within

increased remittance households using their these communities:

Country: Uganda

transfers or the income increased peer-to-peer The rollout of 121 agents

Sample: 658 areas where generated from non-farm transfer receipts and cost provided self-employment

4,541 households were self-employment. savings from remittance to 257 households and

surveyed transfers to invest in self- improved food security for

Context: The regions studied -25%

employment. 1,345 households1.

are rural, poor areas that have

very few existing mobile + 121 Agents +33%

62.9%

money agents, low access to

47.2%

financial services through bank

16.8%

branches, and low remittance

receipts. Decrease in remittance

12.6% transaction costs equal

Contribution: Examines the +88%

Self Employment to saving 10%

impact of rolling out mobile + 257 Households of daily consumption

money to rural areas with low 6.4%

remittance activity (15%) and 3.4%

that are very far from banks.

Improved Food Security

Previous studies examined

country-wide samples with + 1,345 Households

Unexposed Exposed Unexposed Exposed Unexposed Exposed

remittance rates ranging from Areas Areas Areas Areas Areas Areas

40-65%.

1. These results extrapolate the impacts derived from the sample to all households living in the exposed areas. Wieser, Christina, Miriam Bruhn, Johannes Kinzinger, Christian Ruckteschler, and Soren Heitmann. ”The impact of mobile money on poor rural households: Experimental

evidence from Uganda.” The World Bank, 2019.

© Bill & Melinda Gates Foundation | April 2021 1601 02 03 04 05 06 07 08 09 10 11 12 13

Mobile Money Remittances, and Household Welfare

MOBILE MONEY INCREASES REMITTANCES TO RURAL HOUSEHOLDS

WITH MIGRANT WORKERS IN UGANDA

Authors: Ggombe Kasim Munyegera and Tomoya Matsumoto

Journal: World Development, 2016

Research Design: This paper Descriptive Impact Impact Impact Impact

studies the impact of mobile

Mobile money adoption Remittances Remittances Consumption Distance from Agent

money on welfare in rural

Uganda in the absence of increased from 1% in Comparing adopter Households located 1km

shocks. 2009 to 38% in 2012. households that have a away from a mobile money

Mobile money adoption

Survey Dates: 2009 - 2012 increases the probability of migrant worker to adopter agent consume less and

Remittance Receipts receiving remittances by 7 households that do not, the are 2 percentage points

Country: Uganda

percentage points. results show that less likely to receive

Sample: 846 Households households with a migrant remittances.

Contribution: One of the first worker:

papers to study the impact of Mobile money adopters • Increase their likelihood

mobile money on rural 78% receive 36% more in of receiving remittances

household welfare in the remittances than non- by 11 percentage points

65% Mobile money

absence of shocks. adopters, or approximately • Increase their total value adopters increase

US$61. of remittances by 42%. household per capita

50% 50% consumption by 13%

Other evidence suggests compared to non-

that prior to the introduction adopters.

of mobile money there was

no significant relationship

between having a migrant

worker and remittances;

thus, the results above

provide evidence in support

2009 2012 2009 2012 of the impact of mobile

Mobile Money Non- money.

Adopters Adopters

Citation: Munyegera, Ggombe Kasim, and Tomoya Matsumoto. "Mobile money, remittances, and household welfare: panel evidence from rural Uganda." World Development 79 (2016): 127-137.

© Bill & Melinda Gates Foundation | April 2021 1701 02 03 04 05 06 07 08 09 10 11 12 13

Mobile Money and Risk Sharing Against Village Shocks

MOBILE MONEY USERS SMOOTH CONSUMPTION IN THE PRESENCE OF

VILLAGE-LEVEL SHOCKS

Authors: Emma Riley

Journal: Journal of Development Economics, 2018

Research Design: This study Descriptive Impact Impact

uses a household survey to

Remittance Transactions Shocks and Consumption Remittances

examine the impact of mobile

money on household • The consumption level of mobile money users are • In general, mobile money users are 15 percentage

consumption in the presence • 67% of households have sent unaffected by the shock. points more likely to receive remittances compared to

of a village-wide rainfall shock. remittances • Households that live in villages without any mobile non-users.

In particular, the paper

• 82% of households have received money users experience a 7% decrease in • Following a shock, mobile money users receive

investigates the spillover

effects of mobile money to remittances consumption in the presence of a shock. US$10 more in remittances compared to non-users.

non-mobile money users when • Non-users that live in villages with mobile money This is approximately 4% of the median household’s

they reside in the same village users do not significantly differ from non-users that per capita income in 20131.

as mobile money users. Means of Sending Remittances

live in villages without any mobile money users. The results suggest that in the presence of a shock,

Panel Survey Dates: • 40% of households sent remittances mobile money users are not more likely to receive

The results suggest that although mobile money

2008 – 2013 (3 waves) physically via friends and family remittances, but the value of remittances received

users are able to smooth consumption in the

Country: Tanzania presence of a shock, non-mobile money users do not significantly increases.

Sample: 3,265 households in benefit from living in the same village with others that

26 districts use mobile money; that is, there are no spillover

Likelihood to Receive Remittances

Contribution: Examines the effects of mobile money detected.

spillover effects of mobile Consumption Levels After Negative Shock

money; that is, whether mobile

money users share their

35% 33%

of HH used mobile Non-User HH Non-User HH

remittances in the presence of money to send Mobile Money in Villages in Villages

a village-level shock. Sheds Users With Mobile Without Mobile 18%

remittances

light on how new technologies Money Money

affect traditional risk sharing

agreements. 7% 7%

Unaffected

Drop Drop

Users Non-Users

1. Only data from 2013 are used for these results.Citation: Riley, Emma. "Mobile money and risk sharing against village shocks." Journal of Development Economics 135 (2018): 43-58.

© Bill & Melinda Gates Foundation | April 2021 1801 02 03 04 05 06 07 08 09 10 11 12 13

Cashing In (and Out)

MOBILE MONEY LEADS TO A REALLOCATION OF LABOR FROM BUSINESS

TO AGRICULTURE FOR MICRO-ENTREPRENEURS IN MALAWI

Authors: Shilpa Aggarwal, Valentina Brailovskaya, and Jonathan Robinson

Journal: American Economic Association Papers and Proceedings, 2020

Research Design: The Impact Impact Impact Impact

intervention assisted randomly

Savings Labor Supply Deposits Interpersonal Transfers

selected micro-entrepreneurs in

opening mobile money 83% of exposed micro- Mobile money led micro-entrepreneurs exposed to the Micro-entrepreneurs The mobile money

accounts. Training modules on entrepreneurs reported intervention to work less in their primary business and more exposed to the intervention accounts led to a 25%

mobile money features were using mobile money on their farm. were 55-80% more likely to increase in the share of

provided, withdrawal fees were accounts for long-term make a deposit. exposed micro-

waived, and firms were savings and 12% for short- entrepreneurs making

encouraged to save using the The share of exposed micro-entrepreneurs working in their

term money storage, primary business decreased by 8.5% relative to the control The value of deposits transfers to people outside

accounts.

compared to 32% of group. Exposed: 75%. Unexposed: 82%. increased 67-83% for of the household.

Dates: July 2017 – Aug. 2019 unexposed micro- exposed micro- • Exposed: 55%

Country: Malawi entrepreneurs for any entrepreneurs relative • Unexposed: 44%

The share of exposed micro-entrepreneurs working on their

form of savings. to the control group.

Sample: 480 Micro- farm increased by 110% relative to the control group. Exposed micro-

entrepreneurs Exposed: 44%. Unexposed: 21%. entrepreneurs sent on

Exposed micro- average US$11 and

Context: The sample consisted Productive Activities

entrepreneurs made on received US$9.50,

of micro-entrepreneurs in urban Use of MM Accounts

Malawi that had less than 3

Primary Business Farming average 11 deposits compared to average

employees. Additionally, mobile 83% 82% amounting to US$90, deposits of US$90.

money use in Malawi is modest. 75% relative to their average

+110% daily profits of about

Contribution: One of the first -8.5% Post-Intervention

mobile money randomized

44% US$2.50.

32% There continued to be

experiments among micro-

12% 21% substantial usage in mobile

entrepreneurs. Additionally, one

of the only studies to find money accounts even after

impacts driven by savings rather Any Form Short- Long- the withdrawal fee waiver

Savings Term Term

than interpersonal transactions. Savings Savings Unexposed Exposed Unexposed Exposed was removed.

Unexposed Exposed

Aggarwal, Shilpa, Valentina Brailovskaya, and Jonathan Robinson. "Cashing In (and Out): Experimental Evidence on the Effects of Mobile Money in Malawi.” AEA Papers and Proceedings 110 (2020): 599-604.

© Bill & Melinda Gates Foundation | April 2021 1901 02 03 04 05 06 07 08 09 10 11 12 13

Migration, Money Transfers, and Mobile Money

DEMAND FOR MOBILE MONEY IN NIGER

Authors: Jenny C. Aker, Silvia Prina, and C. Jamilah Welch

Journal: American Economic Association Papers and Proceedings, 2020

Research Design: This study Descriptive Descriptive Descriptive Descriptive Key Insight

surveys households on

Mobile Phone Ownership Remittances Remittances Migration Patterns Willingness to Pay Mobile

migration, remittances, and

willingness to pay for mobile 84% of households in 68% of households How do respondents 54% of households had at Money Fees (via

money1. In addition, surveys the sample own mobile received remittances. receive remittances? least one seasonal migrant Behavioral Game Theory

are conducted on all money phones, and in general, and 17% had a permanent Experiment)

• Friend or Family

transfer service providers in 9% of households in Niger migrant. Approximately 50% of the

Member: 74%

Niger. have used mobile money. sample is willing to pay the

• Domestic Money

Dates: 2017 actual cost of sending the

Transfer Provider: 34%

transfer, yet only 3% use

Country: Niger • Bus: 8% this channel.

Sample: 460 households and • Mobile Money: 3%

45 money transfer service

providers

Context: Niger is one of the

most financially excluded

countries in sub-Saharan 84%

Africa. 54%

Contribution: Explores mobile 17% 50%

money adoption patterns in

Niger and provides evidence

on the willingness to pay for

mobile money services.

9% 68% 3%

Mobile Mobile Willing Actually

Phone Money to Pay Use

Ownership Use

1. Willingness to pay was observed using a behavioral game. Aker, Jenny C., Silvia Prina, and C. Jamilah Welch. “Migration, Money Transfers and Mobile Money: Evidence from Niger.” AEA Papers and Proceedings 110 (2020): 589-93.

© Bill & Melinda Gates Foundation | April 2021 2001 02 03 04 05 06 07 08 09 10 11 12 13

Does Mobile Money Use Increase Firms’ Investment?

DOES MOBILE MONEY USE INCREASE FIRMS’ INVESTMENT?

EVIDENCE FROM ENTERPRISE SURVEYS IN KENYA, UGANDA, AND TANZANIA

Authors: Asif Islam, Silvia Muzi, and Jorge Luis Rodriguez Meza

Journal: Small Business Economics, 2018

Research Design: This study Descriptive Descriptive Impact Impact

used the World Bank’s

Adoption of Mobile Money Reasons Firms Adopt Mobile Money Investment Ways Mobile Money is

Enterprise Surveys to examine

the relationship between 54% of firms in the sample used Mobile money use by Used and Investment

mobile money use and firm mobile money to conduct a manufacturing and service

Kenya Of the firms who adopt

outcomes. financial transaction. firms is associated with

mobile money there is a:

Year: 2012 Main Reason for Main Reason for a 16% increase in the

Adopting Not Adopting likelihood of investing. • 27% increase in the

Countries: Kenya, Uganda, likelihood of investing for

and Tanzania Satisfy Customers Payments firms that used mobile

Sample: 1,228 firms 54% Request Too Large money to pay suppliers

Context: The sample of firms Used Mobile • 21% increase in

are in the manufacturing and Money likelihood of investing for

Tanzania

service sector and have 5 or firms that receive mobile

more employees. Main Reason for Main Reason for payments from

Adopting Not Adopting customers

Contribution: Examines the

relationship between mobile Adopter Characteristics Reduce Customers +16% in the • 17% increase in the

money use by firms and Transaction Costs Do Not Use likelihood likelihood of investing for

On average, firms that adopt

private investment, and does firms that make payments

mobile money are: of investing

so by comparing across

to employees using

countries. • Smaller Uganda mobile money

• Younger

Main Reason for Main Reason for

• Concentrated in Adopting Not Adopting

the service sectors

Reduce Suppliers

• Located in the main business Transaction Costs Do Not Use

or capital cities.

Islam, Asif, Silvia Muzi, and Jorge Luis Rodriguez Meza. "Does mobile money use increase firms’ investment? Evidence from Enterprise Surveys in Kenya, Uganda, and Tanzania." Small Business Economics 51, no. 3 (2018): 687-708.

© Bill & Melinda Gates Foundation | April 2021 2101 02 03 04 05 06 07 08 09 10 11 12 13

Can Mobile-linked Bank Accounts Bolster Savings?

CAN MOBILE-LINKED BANK ACCOUNTS BOLSTER SAVINGS?

EVIDENCE FROM A RANDOMIZED TRIAL IN SRI LANKA

Authors: Suresh De Mel, Craig McIntosh, Ketki Sheth, and Christopher Woodruff

Journal: NBER Working Paper, 2018

Research Design: The Impact Impact Empirical Insight

randomized intervention

Partner Bank and Other Formal Bank Deposits Total Savings What if the intervention

introduced a novel savings

account mobile-deposit service The intervention led to a 44% increase in the amount of total savings deposited to the Total savings (formal and targeted women or those

provided by a partnering bank. partner bank. Mobile deposits accounted for less than half of this increase2. informal) were unaffected by who lived 2-5 km from a

Randomly selected individuals the intervention suggesting bank?

were mailed offer letters to that percentage gains in

participate. Those who accepted formal savings, as well as

were provided assistance opening

Women and Savings

Amount Deposited to Partner Bank via the partner bank, were not

a bank account, as well as given The intervention could

Mobile Money in Local Currency meaningful increases.

a mobile phone, SIM card, and potentially increase total

demonstration of the service. savings by 23% for women

Funds could be deposited without Transaction Fees relative to the unexposed

a transaction fee1. group.

Additional randomization

Intervention Active: December

assigned individuals to one

2011 – May 2013

of four exposed groups that Distance and Savings

Country: Sri Lanka (Central) differed by transaction fee

Households who live 2–5 km

Context: Formal savings are (0-8%).

widely available in Sri Lanka;

away from a bank branch saw

The level of transaction fee a 79% increase in the amount

however, informal saving methods

are commonly used.

(ranging from 0–8%) did not deposited to the partner bank

lead to differences in the and a 26% increase in formal

Sample Size: 1,908 individuals

demand for the mobile- deposits relative to the

Contribution: One of the first deposit service. unexposed group.

experiments to use mobile phone-

linked bank accounts to Both frequent and infrequent mobile-deposit users preferred the traditional

encourage savings, and in

method of deposits, implying that transaction costs are not a barrier to the use

particular formal savings.

of savings accounts.

1. Additional randomization varied based on the level of transaction fee, but most impact results compare participants without a transaction fee to the non-exposed group. 2. The intervention only provided the mobile-deposit service for the partner bank.

De Mel, Suresh, Craig McIntosh, Ketki Sheth, and Christopher Woodruff. ”Can Mobile-Linked Bank Accounts Bolster Savings? Evidence from a Randomized Controlled Trial in Sri Lanka.” NBER Working Paper, 2018.

© Bill & Melinda Gates Foundation | April 2021 2201 02 03 04 05 06 07 08 09 10 11 12 13

Transaction Networks

MOBILE MONEY LEADS TO MORE RECIPROCAL TRANSACTIONS IN KENYA

Authors: William Jack, Adam Ray, and Tavneet Suri

Journal: American Economic Review, 2013

Research Design: This study Descriptive Impact Impact Impact

surveyed households across

All M-PESA Transactions Remittances Reciprocity Types of Transactions

Kenya on detailed remittance

information, such as means of Reciprocal Transactions: 21% Receive The likelihood of M-PESA users to Households that use M-PESA are

and reason for the transfer. In Non-reciprocal Transactions: 61% of M-PESA users receive conduct a reciprocal transfer is 17%, more likely to send remittances for

addition, the entire network of 79% remittances compared to 24% of compared to 4% of non-users. regular support, credit

M-PESA agents were arrangements, and emergency help.

non-users

surveyed.

22% of all M-PESA User Send Composition of Transactions

Survey Dates:

Transactions are Reciprocal. 63% of M-PESA users send • 50% of an M-PESA user’s

Households: Sept. 2008 – transactions are sent as regular

Dec. 2009 This 22% is composed of: remittances compared to 29% of

Regular Support: 42% non-users support, vs. 61% of a non-user’s.

Agents: March 2010

Credit Arrangements: 14% • 11% of an M-PESA user’s

Country: Kenya transactions are credit

Emergency Help: 11% Likelihood of Conducting

Sample: 2,017 households Remittances Reciprocal Transfer arrangements, compared to

and 7,700 agents No Particular Reason: 19% 6% of a non-user’s.

Context: 70% of Kenya’s adult Other: 14% 17% • An M-PESA user’s transactions

population had adopted M- that are sent as emergency help

PESA 11% of Non-M-PESA User 63% 61%

do not significantly differ from a

Contribution: This paper Transactions are Reciprocal. non-user’s. 11% of a nonuser’s

extends the evidence on This 11% is composed of: 29% 24% transactions are sent as

M-PESA mobile money 4%

Regular Support: 53% emergency help.

transactions and risk sharing

by investigating the Emergency Help: 13% This suggests that M-PESA users

characteristics of interpersonal Credit: 4% Non- M-PESA Non- M-PESA are shifting away from regular

Non-M-PESA M-PESA

transactions and examining No Particular Reason: 22% M-PESA User M-PESA User

User User

support transfers and toward credit

the types of transactions that User User transfers, and possibly emergency

are conducted. Other: 8%

Receive Send support transfers.

Jack, William, Adam Ray, and Tavneet Suri. "Transaction networks: Evidence from mobile money in Kenya." American Economic Review 103, no. 3 (2013): 356-61.

© Bill & Melinda Gates Foundation | April 2021 2301 02 03 04 05 06 07 08 09 10 11 12 13

Payment Mechanisms and Anti-Poverty Programs

PAYMENT MECHANISMS AND ANTI-POVERTY PROGRAMS:

EVIDENCE FROM A MOBILE MONEY CASH TRANSFER EXPERIMENT IN NIGER

Authors: Jenny C. Aker, Rachid Bounmijel, Amanda McClelland and Niall Tierney

Journal: Economic Development and Cultural Change, 2016

Research Design: The intervention varied the Impact Impact Impact

delivery mechanism of an unconditional cash

Uses of the Transfer Food Security Children and Nutritional Status

transfer program in Niger following the

2009/2010 drought and food crisis. The delivery Households that received the cash transfer Households that received the cash transfer Although children in the mobile money

mechanisms varied as follows: cash delivered in via mobile money purchased a more diverse via mobile money had a more diverse diet transfer group ate slightly larger and more

an envelope, received a mobile phone along with set of goods compared to the other exposed than both groups that received the cash diverse meals, their nutritional status was

having the cash delivered in an envelope, and groups1: transfer manually. unchanged.

cash delivered via mobile money transfer. All

participants in the intervention received a cash • Compared to households that received This score was .28-.51 points higher. • Children in households that received the

transfer, so there was no pure unexposed group. the cash manually, mobile money transfer Households that received cash manually cash transfer via mobile money ate an

recipients purchased .78 more types of had a diet diversity score of 3.17 out of 12. additional 1/3 of a meal compared to both

Intervention Active:

May 2010 – May 2011

goods. groups that received the cash transfer

• Compared to households that received a manually. Children in the group that

Country: Niger received cash manually ate 3.17 meals

mobile phone, along with the cash in Increase in Diversity of Food

Sample: 1,152 Households in 96 villages by Mobile Money per day on average.

hand, mobile money transfer recipients

Context: Within Niger, there is high rainfall purchased .85 more types of goods. • Children in mobile money transfer

variability, which has led to at least 7 droughts households also ate more diverse meals

between 1980 and 2010. During the 2010

• Households that received cash manually

purchased 4.32 types of goods on relative to the group that received a

drought, 2.7 million people were classified as

average. +0.51 mobile phone along with the manual

vulnerable to extreme food insecurity. Agriculture

is the primary income source for 97% of +0.28 cash transfer. Their diet diversity score

households. was 12-14% higher.

Contribution: Disentangles the impact of

Relative to Relative to

technology from the transfer mechanism.

Households that Households that

Received Transfer Received Transfer

Manually Manually

+

Received a Mobile

Phone

1. Households were surveyed on which goods and services they purchased, but not on a full expenditure and income module. Aker, Jenny C., Rachid Boumnijel, Amanda McClelland, and Niall Tierney.

"Payment mechanisms and antipoverty programs: Evidence from a mobile money cash transfer experiment in Niger." Economic Development and Cultural Change 65, no. 1 (2016): 1-37.

© Bill & Melinda Gates Foundation | April 2021 24You can also read