Paygilant Autonomous Mobile Payments Fraud Prevention - Solution White Paper - Mobile Payments You Can Trust

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Mobile Payments You Can Trust

Paygilant Autonomous Mobile

Payments Fraud Prevention

Solution White Paper

November 2017

1

1 Introduction and Scope

The mobile payments market is growing at an exponential rate as consumers and merchants

alike are adopting new payments and m-commerce solutions as they emerge. With mobile

payments becoming mainstream, fraud will continue to shift to the mobile channel and

threaten this sensitive ecosystem. Banks and mobile payment providers are challenged with

elevating the security of their money transfer and payment solutions while providing a smooth

user experience and maintaining trust.

Paygilant’s on-device mobile payments fraud prevention solution stops fraudulent transactions

at the pre-transactional phase and allows a smooth payment experience. This document covers

the use cases, architecture and benefits of the Paygilant solution.

2 Paygilant, Mobile Payments You Can Trust

Mobile payments fraud is rapidly increasing, as additional mobile payment solutions reach the

market and offer more value to consumers in the form of in store and mobile payments, P2P

money transfer and mobile wallets. Mobile payment providers, card issuers and merchants

alike are challenged with securing their applications and payment channels against device theft,

new account fraud and account take over fraud while providing consumers with the shortest,

seamless payment experience.

In today’s mobile payments environment, this is not an easy task and the approaches differ

from mobile payment provider to another: some mobile payment providers choose to accept

transactions with a small amount always, without any risk assessment while transactions with

high amounts are authenticated always, disregarding the risk level. Other providers choose to

authenticate every transaction and some choose to allow all without any risk assessment. This

creates a lose-lose situation where fraud losses and operational costs are increasing for certain

providers, while for others the adoption of mobile payments is limited due to high

authentication rate.

Paygilant’s on-device solution for mobile payments and money transfer provides the peace of

mind mobile payment providers and banks so desire without impacting the user experience,

while reducing their Total Cost of Ownership (TCO).

2

Autonomous Risk Assessment for Mobile Payments

Paygilant’s mobile fraud prevention solution is a combination of

smart, independent and compact on-device risk engine and powerful

backend analytics to support it. Paygilant’s SDK carries with it the

intelligence required to perform the risk assessment on the device

itself, without involving any backend in the process.

Paygilant’s risk assessment process is based on proprietary transaction-behavioral maps. These

multi-dimensional maps represent the purchasing patterns/behavior of customers and are a

fundamental pillar in Paygilant’s solution. The transaction behavior maps are generated using a

Depth of Field (DOF) approach taken from digital photography and unfold unique capabilities:

They incorporate an extensive amount of identity verification data into the risk assessment

process, all the while remaining compact in size and efficient in processing time, enabling the

risk assessment process to occur on the mobile device itself. Paygilant’s transaction behavioral

maps are constantly updated and maintained over time, thus detecting 3x more fraud then

traditional systems.

Performing the risk assessment on the device itself is key to a winning solution:

• Wealth of Identity Verification data:

By performing the risk assessment on the mobile device itself Paygilant uses a wide set

of identity verification data without extracting any sensitive information from the

device, avoiding data protection considerations.

• Early Detection:

Paygilant identifies the fraud attempts out of the genuine majority at the pre-

transactional phase, providing valuable early detection.

• Decentralized Risk Assessment Environment:

Today’s cyber environment is extremely dynamic. The arms race between hackers and

security solutions is always on the go and no organization is completely safe against

hacker attacks such as: APT attacks, social engineering, trojan horses, watering hole

attacks - which target a specific organization for information theft or ransomware.

The risk for backend based mobile payments prevention solutions is extremely high. If

compromised, such solutions risk failure in delivering anti-fraud protection for an

unknown period of time and exposing the entire user base information to hackers.

In Paygilant’s solution, every mobile device running a Paygilant protected mobile

payments application carries its own specific risk engine. This creates a decentralized

3

environment, in which there is no one central backend risk engine containing all the

records of all the users, but rather millions of distributed risk engines, all containing the

information of one specific user at a time. Unlike current solutions, this game-changing

approach diffuses hacker attack scenarios on the Paygilant solution, since it will take

hackers substantial efforts and a long time to attempt and breach each and every

mobile device. In addition, since Paygilant doesn’t collect and store any sensitive or

identifiable information in its backend system, the risk of exposing the entire user base

to theft doesn’t exist.

Smooth Payment Experience

Risk Based Authentication

In today’s mobile payment environment, strong customer

authentication is required at a large scale. This results in a

cumbersome experience for end users as well as increased

operational load.

Paygilant’s risk assessment solution eliminates this burden by analyzing the risk of every

transaction separately and flagging just those which are deemed as fraudulent. This way,

customers are asked to authenticate only in risky situations, payment abandonment is

reduced and customer loyalty is increased.

Unified Risk Assessment for All Cards

Paygilant’s solution performs its risk assessment process on all the cards the end user has

defined in the mobile application, regardless of the card type or brand. Paygilant’s solution

keeps track of all the end user’s transactions and correlates the shopping patterns per card.

Immediate Response, No Latency

Paygilant acknowledges that transaction abandonment can happen very quickly, therefore our

solution is designed with a smooth and seamless user experience in mind.

The fact that Paygilant performs its risk assessment process on the mobile device itself

eliminates any latency or communication issues and allows the risk assessment and

authentication process to complete in milliseconds, increasing customer satisfaction and

loyalty.

4

Face Recognition Authentication

Paygilant uses the most advanced authentication methods available to determine the user’s

real identity. In case a transaction is deemed as high risk, the user will be asked to identify

herself using a face recognition authentication process.

60% TCO Reduction

By authenticating a small percentage of the transactions and

minimizing potential issues at the point of checkout, Paygilant’s

solution reduces customer service and fraud department load and

cuts related TCO costs by approx. 60%.

Paygilant guides your way in a sea of uncertainty and protects your mobile

payments solution from fraud

3 Use Cases and Liability Shift Considerations

The following use cases are handled by Paygilant’s solution:

1. In-store transactions– mobile payments using contactless (NFC), QR code, Bluetooth

performed in the store with the end user present via a mobile wallet or other merchant specific

application. These types of transactions are currently considered Card Present transactions and

the fraud liability lies on the issuer.

2. Mobile payment transactions performed via mobile wallet providers. Mobile payments

performed online via a mobile wallet application or other merchant specific application. These

are currently considered as Card Not Present Transactions and the liability shift is with the

merchant.

Paygilant offers a 3rd model for Payment Processors who integrate the Paygilant solution into

their application: Paygilant Protected Mobile Payments. In this scenario, the Payment

processor offers Paygilant’s solution built-in for fraud prevention and offers a liability shift for

the merchants for the CNP transactions.

5

4 Common Attack Vectors

Paygilant fraud prevention solution covers the following attack vectors:

1. Account Take Over -

In this scenario the end user’s card and credentials have been stolen by a fraudster (by

malware, phishing, etc) and the fraudster is attempting a fraudulent transaction using

those details.

Paygilant’s solution protects against such scenarios by examining the user’s known

purchasing habits, as well as the user’s known devices. Mobile payments which are out

of the normal purchasing habits or from unknown devices will increase the risk score of

the transaction.

2. Fraudulent Device/SIM Swap Fraud -

To protect against scenarios where fraudsters are attempting transactions from new

devices or are have swapped the SIM, Paygilant captures a unique snapshot of the end

user’s device, called Customer Identity Verification (CIV) and stores the CIV at the

Paygilant backend server. The CIV binds the user’s ID to the device so that whenever an

end user is attempting a transaction from a new device it’s CIV is verified.

3. Device Theft -

In this scenario a fraudster is attempting a fraudulent transaction from the end user’s

genuine device. Paygilant protects against such scenarios by examining the user’s known

purchasing habits.

4. MITM/Application Tampering

Paygilant protects against fraudulent mobile payment applications and mobile malware

which are programmed to bypass the bank’s payment application and communicate

directly with the bank’s server. Paygilant’s tokenization protection generates a token

per each transaction using the unique end-user’s private map. The token is verified

against the exact same map which is created in the Paygilant backend server. The

combination of the transaction parameters with the map prevents the alteration of the

transaction and MITM attacks.

5. New Account Fraud-

In this scenario a new user is trying to open an account in the mobile payment

application and the provider has no previous known information on this user. Paygilant

6

protects against such scenarios using its face recognition authentication. The user will

be required to provide a photo ID of herself during the registration process and this

photo ID will be matched against a Selfie to validate the user’s identity.

6. Contactless Relay Attacks-

Paygilant protects against contactless relay attacks using its extensive risk assessment

model. Paygilant’s solution will identify that the fraudster’s transaction is not in-line

with the genuine user’s transaction behavior maps and will flag it as high risk. In

addition, Paygilant’s face recognition authentication can be invoked to verify the user’s

identity.

5 Technical Overview

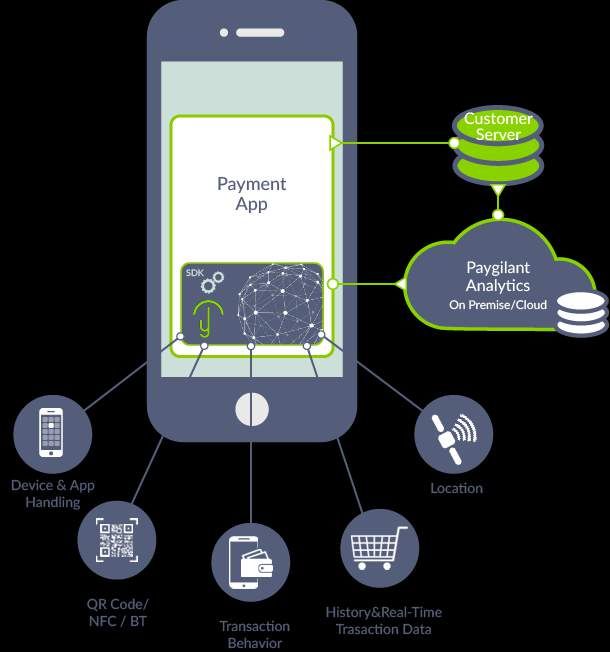

Paygilant’s mobile payments anti-fraud solution introduces a ground-breaking approach to

mobile fraud prevention. The solution is composed of two main parts:

1. Paygilant SDK - a tailored-for-mobile component which resides on the mobile device and

performs the risk assessment per every transaction. The SDK carries with it the “brain

power” needed to perform the risk assessment itself and is responsible to identify the

data elements which are relevant for risk assessment process.

The SDK also launches the face recognition authentication process for high risk

transactions, if the provider decides to incorporate this authentication method in the

solution.

2. Paygilant Services - a backend component, either an on-premise server or cloud, which

maintains Paygilant’s machine learning algorithms and constantly updates the mobile

component with up-to-date maps.

7

Figure 1: High Level Architecture

On-Device Risk Evaluation

Paygilant’s risk evaluation process is invoked when a mobile payment or money transfer is

attempted by the end user. The application sends Paygilant’s SDK with the transaction

information and an action is taken based on Paygilant’s risk evaluation.

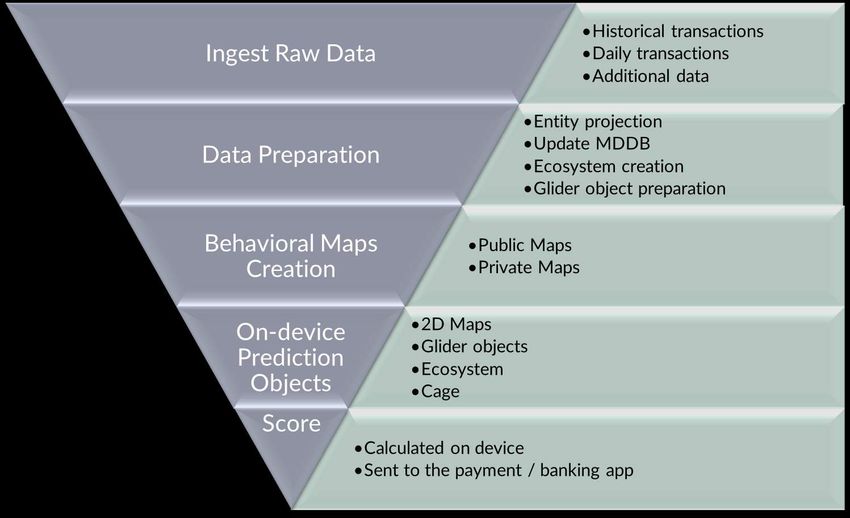

Transaction Behavioral Maps

Paygilant’s risk evaluation process takes into account all the

key information which is relevant for an accurate detection.

Paygilant’s Behavioral Maps are an essential concept in

Paygilant’s solution. The Behavioral Maps represent the

purchasing patterns/behavior of a specific customer and her

nearest neighbors and are created using Paygilant's proprietary machine learning algorithms.

The behavioral maps typically comprise a large amount of information but must be compact

8

enough since they are securely transmitted to the mobile device. To achieve this Paygilant

utilizes its depth of field (DOF) approach from digital photography to compress the information

so that complex calculations that do not require work intensive CPU and memory. A Behavioral

Map shows a clear, high resolution picture of the different risk zones and is a key factor in

determining the risk of a specific transaction and has the following key characteristics:

- User specific: each map is unique, calculated and maintained on a per user basis, therefore

representing a transaction risk level for each customer’s transaction.

- Lightweight: Resolution variations enable maintaining only the necessary data, reducing

the map's weight to a bare minimum.

- Dynamic: As the purchase behavior changes, the map will be modified.

Paygilant Ecosystem

An additional factor in the risk evaluation process is the Paygilant

Ecosystem. Per each user, Paygilant stores the following

characteristics:

For payments:

1. Known User Merchants – merchants visited and shopped

at by the end user

2. Nearest Neighbors Merchants – Merchants with similar characteristics to the

merchants visited by the end user

3. Nearest Neighbors End Users – end users with similar characteristics to a specific

account

For money transfer:

1. Known User Payees – individuals who’ve previously received money transfers from

this account.

2. Nearest Neighbors Payees – Payees who have similar characteristics to Known

Payees

3. Nearest Neighbors End Users – end users with similar characteristics to a specific

account

Using this information, the Paygilant ecosystem influences the risk evaluation process, based on

the fraud and genuine patterns of each merchant or user in each category.

The Paygilant Ecosystem is updated regularly.

9Paygilant Insight

Paygilant Insight enables fraud detection even when

minimal transaction history is available. It tracks and

monitors transactions made by the end user and

sequences of transactions and logs them to create

transaction pattern history. In addition, this element

examines the transitions between merchants and

merchant statistics in the population.

This allows Paygilant to generate a reliable risk assessment for transactions when minimal

transaction history is available. Another valuable benefit is since keeping the end user’s

transaction history is always up to date on the device itself, with no syncing time needed.

Paygilant Risk Hedging

Paygilant offers its customers the option to define certain policies

which take precedenance to the risk scoring process. i.e.

customers can choose to elevate the security level of certain

transactions regardless of the Paygilant risk evaluation. In this case

Paygilant will still analyze the transaction and will determine its

risk level, but will take action based on the pre-defined policy.

Figure 6: Risk Assessment Overview

10Paygilant’s SDK Security

Paygilant’s SDK and behavioral maps are protected by multi-layer security controls. Security

was built into the SDK component from the ground up, to protect against tampering, forging

and bypass and ensure the safe use of the mobile payment application as well as the user

privacy. In addition, the maps data is scrambled and obfuscated which makes it unreadable to

anyone but the Paygilant system. No private or sensitive data is stored as the maps are a

mathematical calculation which represents the purchasing behavioral of the customer.

The Map update is initiated by Paygilant’s back end using notifications. In order to overcome

situations where notifications are disabled, a fail-safe mechanism on the SDK triggers periodic

polling if no update is received.

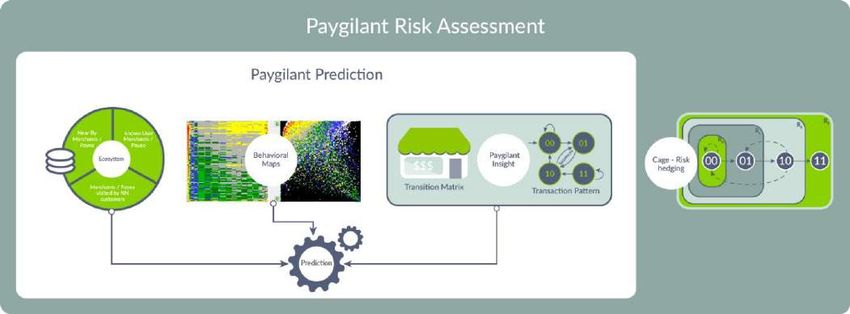

Paygilant Analytics

Big Data analytics, Machine Learning and High Availability

Whether as an on-premise installation or as a managed service, Paygilant uses a strong backend

infrastructure to perform its core machine learning algorithms. Paygilant’s backend runs on a

big-data platform, for high performance and continuous analytics.

Multi-Dimensional database

Transactions which are relevant for the system’s operation are held in a Multi-Dimensional

Database (MDDB). The MDDB is constantly updated with new transactions, making it up-to-

date with current trends.

Paygilant Behavioral Maps are created at the MDDB, as the final product. Once a day, the

MDDB processes all the new transactions and generates new transaction behavioral maps. The

up-to-date maps are downloaded into the end user’s device, constantly improving the risk

evaluation process.

Map Creation and Update Component

Behavioral Maps are securely stored in the system, structured in such a way that expedites

creation, updating and extraction. The maps are updated every time the MDDB is modified by the

Map Creation and Update (MCU) component. Behavioral maps are stored and processed on the big-

data platform.

Map State Tracker

11The maps are updated with every new transaction made by the end user, which requires

constant validation of the latest maps residing on the end user’s mobile device.

The Maps State Tracker (MST) is responsible for monitoring the mobile device’s current state

and ensuring that it is up-to-date with the most current map. Once a map is updated by the

MCU, the MST will track the map provisioning state. MST stores the state of each map and

exposes an API with the KPIs for monitoring the system's status. MST is updated when a map is

created or modified ensuring the successful provisioning of the map.

The following diagram shows the distribution of tasks and responsibilities between the

Paygilant SDK and the Paygilant server-side analytics:

Paygilant Analytics

Paygilant SDK

126 Summary

As mobile payments applications establish a stronger footprint in our everyday lives, the mobile

fraud rates will keep increasing. Mobile payment providers are challenged with providing the

adequate security levels while maintaining a smooth and seamless payment experience.

Paygilant’s mobile payments anti-fraud solution introduces an advanced approach to mitigating

mobile payments fraud – risk assessment using a smart and compact risk engine integrated into

the mobile payment application, with a powerful analytics platform which generates end users’

private and public maps. Along with Paygilant’s advanced face recognition authentication, fraud

prevention happens in real time, with minimal end user engagement and a seamless payment

experience.

7 About Paygilant

Paygilant’s mission is to deliver a vigilant solution against mobile payments fraud. Paygilant

disruptive technology makes in-store contactless payments or mobile payments easy and

secure, increasing customer loyalty and reducing friction.

Paygilant is recognized by industry leaders as a pioneer. Founded in 2014, we have received the

EU Commission Horizon 2020 grant, participated in Citi’s Innovation Lab and IBM Alpha Zone,

and more. We have been recently chosen by The Mobile Wallet in India to protect its mobile

wallet application and the best is yet to come.

13You can also read