North American Energy - Positioned as a Key Growing Supplier of Global Energy Demand: A Game Changer for US Energy Infrastructure - Goldman Sachs ...

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

North American Energy Positioned as a Key Growing Supplier of Global Energy Demand: A Game Changer for US Energy Infrastructure GS ENERGY & INFRASTRUCTURE TEAM April 2022

Table of Contents

1

Setting the Stage

2 North America as a Supply Solution

3 Energy Equity Markets

4 Midstream Offers Unique Exposure

5 Evaluating Terminal Value Concerns

6 Natural Gas & Decarbonization

7 Appendix & Disclosures

Goldman Sachs Asset Management 21

Setting the Stage

Goldman Sachs Asset Management 3Energy & Equity Market Backdrop

We believe that a combination of fundamental and technical factors have created a very constructive

landscape for commodity prices and energy equities over the next decade

Due to the Russia/Ukraine crisis, policy makers are increasingly focused on securing

Energy Security is Top Priority reliable long-term energy with North America uniquely positioned as the key supplier.

Years of underinvestment led to tight supply and demand prior to Russia/Ukraine conflict;

Potential Long-Term Commodity Strength replacing lost Russian supply could result in years of elevated commodity prices.

Inflationary periods are historically constructive for energy equities; during the 2003-2008

Macroeconomic Tailwinds inflationary cycle, the energy sector outperformed the S&P 500 by 130%.

Investor interest has picked up and the sector may continue to benefit from a growth-to-

Shifting Equity Market Sentiment value shift, in addition to a rationalization of energy underexposure across portfolios.

Management teams have transformed balance sheets by cutting capital spending and

Reform in Public Energy Equities focusing on maximizing free-cash-flow, reducing leverage, and driving shareholder value.

The European energy crisis highlights that fossil fuels and renewables need to co-exist to

Re-Evaluation of Terminal Values maintain reliable/secure supply with reasonable consumer prices amid growing demand.

Sources: Goldman Sachs Asset Management and Bloomberg. Data as of March 31, 2022. The economic and market forecasts presented herein are for informational purposes as of the date of this

presentation. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this presentation. Goldman Sachs does not provide accounting, tax or legal

advice. Please see additional disclosures at the end of this presentation. Past performance does not guarantee future results, which may vary.

Goldman Sachs Asset Management 4Global Oil Market Supply & Demand is Tight

Demand recovery has outpaced supply, which has been further stressed by the Russian invasion of

Ukraine; global inventories are now at the lowest level in more than a decade

Demand (-3% vs. 2019 Levels) Supply (-8% vs. 2019 Levels)

U.S. OIL DEMAND (MMBPD) OPEC+ & NORTH AMERICA OIL PRODUCTION (MMBPD)1

Actual 2019 Average Actual 2019 Average

25 65

60

20

55

15

50

10

45

5 40

Jan-20 May-20 Sep-20 Jan-21 May-21 Sep-21 Jan-22 Jan-20 May-20 Sep-20 Jan-21 May-21 Sep-21 Jan-22

INDIA OIL DEMAND (THOUSAND METRIC TONNES) GLOBAL OIL INVENTORIES (MMBBLS)

Actual 2019 Average Actual 2010-2019 Average

14,000 2.8

11,000 2.6

8,000 2.4

5,000 2.2

2,000 2.0

Jan-20 Apr-20 Jul-20 Oct-20 Jan-21 Apr-21 Jul-21 Oct-21 Jan-22 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Sources: Goldman Sachs Asset Management, Bloomberg, and International Energy Agency (IEA). Latest available data as of March 31, 2022. Past performance does not guarantee future results,

which may vary.

Goldman Sachs Asset Management 5Oil Supply is Concentrated in Potentially Problematic Regions

As recent conflict has shown, the world’s oil trade is overly reliant on countries that may be prone to

geopolitically motivated supply-side disruptions, such as Russia

2019 NET TRADE BALANCE (MMBPD)

15

Net Oil Exporting Regions

10

5

13.0 8.4 4.6 3.3

0

-3.4 -4.0 -7.1 -10.3 -11.7

-5

-10

Net Oil Importing Regions

-15

Middle East Russia Africa North America Japan India Other China Europe

Sources: Goldman Sachs Asset Management, Bloomberg, and BP Statistical Review. Data as of March 31, 2022, unless otherwise noted. Past performance does not guarantee future results, which

may vary.

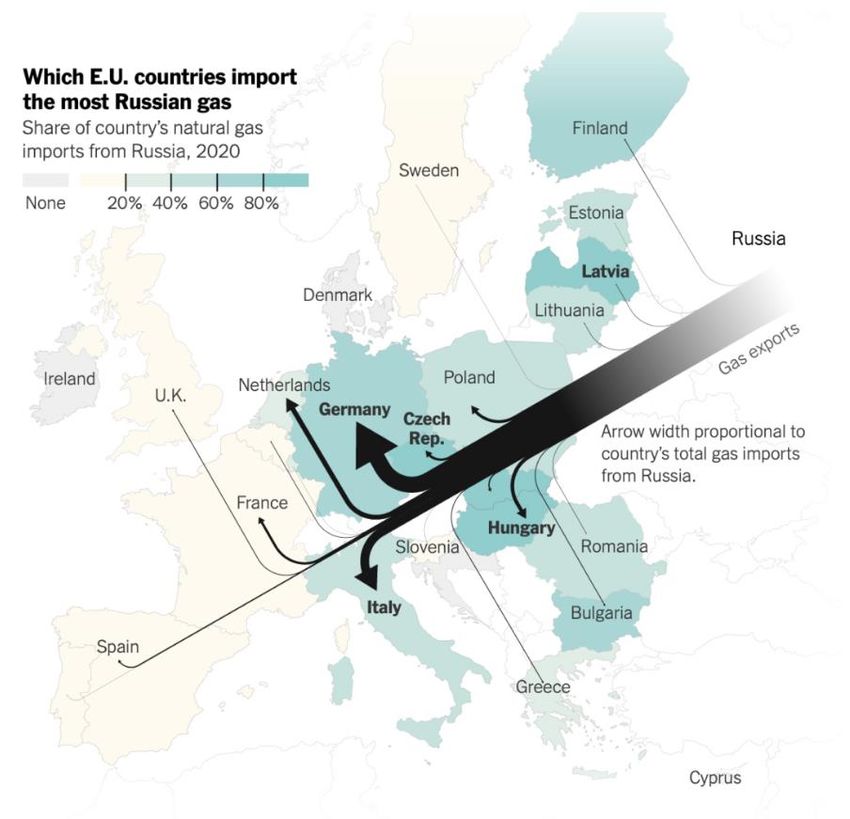

Goldman Sachs Asset Management 6European Gas Supply is Overly Dependent on Russia

Russia services 33% of European natural gas demand and recent conflict has added further stress to

an already undersupplied market, with UK energy bills set to rise 54% in April

RUSSIAN GAS SHARE IN EU + UK DEMAND (2001-2021) RUSSIAN GAS REFLECTS 50%+ SHARE FOR MANY EU COUNTRIES1

40%

30%

20%

10%

26% 25% 29% 37% 32%

0%

2001 2009 2014 2019 2021

In an effort to lessen the energy price burden on consumers, EU governments have proposed gas-tax relief programs, in addition to

announcing the construction of new LNG terminals and pursuing diplomatic efforts to secure oil & gas supply outside of Russia.

Sources: Goldman Sachs Asset Management, International Energy Agency (IEA), EuroStat, and British Department for Business - Energy & Industrial Strategy. Data as of March 31, 2022, unless

otherwise noted. 1Includes both piped and liquefied natural gas and excludes Austria as it did not report the source of its natural gas imports; data of December 2022.

Goldman Sachs Asset Management 7Renewables Are Not A Stand-Alone Solution

Renewables alone can’t satisfy the world’s energy needs due to intermittency issues, hidden costs,

and potential geopolitical considerations

Intermittency Issue Hidden Costs Geopolitical Concerns

• Output from renewable sources, such • LCOE1, a common measure of • Select countries control significant

as wind and solar, is dictated by renewables cost, does not account for material/resources needed to scale

weather. high associated costs of transmission renewables.

and back-up generation.

• Utility scale battery economics are • China is the top producer of Rare

currently prohibitively expensive to be • Intermittency increases the associated Earth elements and is also the leading

solely relied upon. costs of integration into the grid. processor of all key mineral inputs.

• Fossil fuels are required as a back-up • This cost is generally assumed by • The majority of Cobalt production is

source to maintain reliable and households in the form of levies and controlled by DR Congo & Russia.

consistent energy supply. taxes on energy bills.

• Concentration may result in

unintended environmental, cost,

labor and geopolitical implications

Sources: Goldman Sachs Asset Management, Bloomberg, Energy Information Administration (EIA), and International Energy Agency (IEA). Data as of March 31, 2022. 1Levelized cost of energy (LCOE):

a measure of the average net present cost of electricity generation for a generating plant over its lifetime. Past performance does not guarantee future results, which may vary.

Goldman Sachs Asset Management 8U.S. LNG Presents a Tremendous Green Opportunity

Increasing U.S. LNG capacity in order to replace coal usage has the potential to be the leading

solution for CO2 emissions reduction across the world

The Demand Emissions Reduction Impact of This Potential U.S.

LNG Solution is Equivalent To:

• There is currently 175 billion cubic feet per day (Bcf/d) of

coal-to-gas switching demand in the world.

Electrifying every U.S. passenger

A Potential Plan vehicle

• Quadruple U.S. LNG capacity to 55 Bcf/d1 by 2030 to

replace international coal.

• This initiative could be fully funded by the natural gas

industry. Powering every home in America with

rooftop solar and backup battery packs

The Result

• By 2030, this scenario would reduce international CO2

emissions by an additional -1.1 billion metric tons (Bmt) per

Adding 54,000 industrial scale windmills,

year.2

doubling U.S. wind capacity

• U.S. citizens could be paid for this initiative (tax revenues

and an additional $75 Bn in royalties3), rather than paying

for it.

COMBINED

Sources: Goldman Sachs Asset Management, EQT Corporation, ICCT, International Energy Agency (IEA), ICF Update to the life-cycle analysis of GHG emissions for U.S. LNG exports analysis. Latest

data available as of March 31, 2022. 1Including current capacity, capacity under construction, and future new capacity. 2Assuming 3 bcfd under construction, and 40 bcfd additional capacity by 2030.

3Incremental cumulative royalties above 2021 levels from 2022-2030 assuming 20% of revenue @ $3.75 / mcf. The economic and market forecasts presented herein are for informational purposes as of

the date of this presentation. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this presentation.

Goldman Sachs Asset Management 92

North America as a

Supply Solution

Goldman Sachs Asset Management 10North America is a Key Growing Provider of Energy

Resource abundance and relative stability, has positioned North America to play an even larger role in

the global energy market as governments seek safe and reliable long-term supply solutions

Crude Oil Natural Gas

• North America is currently a top oil producing region, • North America is also rich in natural gas resource and has

producing nearly 17% of the global oil supply. grown production by 50% over the last decade

• Third most oil rich continent in the world with more than 240 • North America is a leading provider of LNG and has grown

billion barrels of proved oil reserves. export capacity by more than 600% since 2017.

Refined Products Natural Gas Liquids (NGLs) / Petrochemicals

• North America boasts one of the world’s most complex • World’s largest producer of NGLs, producing 7 MMbpd; three

refining systems, refining nearly 19 millions of barrels per day. times that of Saudi Arabia, the second largest producer.

• The system allows North America the ability to be a top global • One of the lowest cost producers of petrochemicals, the

supplier of finished products (gasoline, diesel, etc.). feedstock to thousands of consumer goods (i.e. plastics).

Sources: Goldman Sachs Asset Management, BP Statistical Review, and the International Energy Agency (IEA). Data as of March 31, 2022, unless otherwise noted. NGLs: Natural gas liquids (i.e.

ethane, propane, butane, isobutene, pentane, etc.). The economic and market forecasts presented herein are for informational purposes as of the date of this presentation. There can be no assurance

that the forecasts will be achieved. Please see additional disclosures at the end of this presentation. Goldman Sachs does not provide accounting, tax or legal advice. Please see additional disclosures at

the end of this presentation. Past performance does not guarantee future results, which may vary.

Goldman Sachs Asset Management 11North American Oil: Abundant, Reliable, and Responsible

North America has a significant amount of proved, untapped oil reserves, presenting a strong

opportunity to backfill lost Russian production and help other countries diversify energy supply

TOP 5 OIL PRODUCERS (MMBPD) PROVED OIL RESERVES (BILLIONS OF BBLS)

North America 16.9 Venezuela 303.8

Saudi Arabia 10.1 Saudi Arabia 297.5

Russia 10.1 North America 242.9

Iraq 4.4

Iran 157.8

China 3.8

Iraq 145.0

0 4 8 12 16 20

0 70 140 210 280 350

We’d highlight that while Venezuela is an oil resource rich country, output is very low given years of sanctions, corruption, and political

instability. We believe it is very unlikely that Venezuela can reintroduce oil to the market in a meaningful way over the near-to-medium term.

Sources: Goldman Sachs Asset Management and Bloomberg. Top 5 Producing countries Data as of December 31, 2020. The economic and market forecasts presented herein are for informational

purposes as of the date of this presentation. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this presentation.

Goldman Sachs Asset Management 12Natural Gas: Ability to Provide Significant Gas to Europe

Since 2017, the U.S. has grown natural gas production by 50% and liquefied natural gas (LNG)

export by capacity by more than 600%, making it the largest global LNG exporter

U.S. NATURAL GAS PRODUCTION (BCF/D) U.S. LNG EXPORTS (BCF/D)

110 12

+50% Growth in Production Since 2012 +608% Growth in Export Capacity Since 2017

95 9

80 6

65 3

50 0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 Feb-17 Dec-17 Oct-18 Aug-19 Jun-20 Apr-21 Feb-22

North America has spent billions of dollars on LNG infrastructure over the last 5+ years in order to mobilize natural gas resources, which have a

strong long term-demand outlook with the commodity being categorized as a “cleaner” fossil fuel by some European countries.

Sources: Goldman Sachs Asset Management, Bloomberg, and Energy Information Administration (EIA). Data as of March 31, 2022. The economic and market forecasts presented herein are for

informational purposes as of the date of this presentation. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this presentation.

Goldman Sachs Asset Management 13U.S. LNG: Ability to Meaningfully Expand Export Capacity

EU is beginning to mobilize to increase LNG import capacity and recently announced a deal with the

US to import 1.5 Bcf/d of LNG this year and ramp to 5 Bcf/d by 2030

U.S. LNG CAPACITY PROJECTIONS (BCF/D)

Potential Capacity To Supply Europe

There is 3.3 Bcf/d of capacity under construction and 4.0 Bcf/d with high probability of proceeding to FID. We estimate there’s an additional 9 -

14 Bcf/d of potential capacity, but project construction will be largely contingent upon receiving firm long-term purchase agreements.

Sources: Goldman Sachs Asset Management and Energy Information Agency (EIA). Latest data available as of March 31, 2022. Bcf/d: Billion cubic feet per day.

Goldman Sachs Asset Management 14Refined Products: North America Is the Leading Exporter

North America, the largest exporter of refined products, has a unique ability to deliver consumable

liquids (gasoline, diesel, etc.)

2019 REFINERY CAPACITY THROUGHPUT (MMBPD) TRANSPORTATION FUEL IMPORTS & EXPORTS (KBPD)

20 4,000

1.5 MMbpd Net Exporter

15 2,500

10 1,000

5 -500

19.0 13.4 5.8 5.1 3.0

0 -2,000

North America China Russia India Japan 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019 2021

Sources: Goldman Sachs Asset Management, BP Statistical Review, EIA, and Bloomberg. Data as of March 31, 2022, unless otherwise noted. MMbpd: Millions of barrels per day. Kbpd: Thousands of

barrels per day. The economic and market forecasts presented herein are for informational purposes as of the date of this presentation. There can be no assurance that the forecasts will be achieved.

Please see additional disclosures at the end of this presentation.

Goldman Sachs Asset Management 15NGLs & Petrochemicals: Largest Producer & Cost Leader

North America is the leading producer of NGLs, the feedstock for thousands of consumer goods (i.e.

plastics) and is also one of the lowest cost petrochemical producers

TOP 5 NGL PRODUCERS (MMBPD) GLOBAL ETHYLENE CASH COST ($/TONNE)

8 Saudi

(Ethane) $165

Canada

(Ethane) $315

6

U.S. $385

(Ethane)

4 Europe $705

(Naptha)

China $1,055

(CoalTO)

2

NE Asia $1,140

(Naptha)

5.7 1.7 0.6 0.5 0.5 China

0 $2,047

(MTO)

North America Saudi Arabia UAE Russia Qatar

There is a strong relationship between petrochemicals demand and GDP growth (2.5x GDP growth between 1970-2015). Assuming even 50%

of this relationship going forward, implies meaningful demand growth for NGLs as incomes rise in developing economies.

Source: Goldman Sachs Asset Management, U.S. Energy Information Administration (EIA), International Energy Agency (IEA), and Citi Group. Latest data available as of March 31, 2022. NGLs: Natural

gas liquids (i.e. ethane, propane, butane, isobutene, pentane, etc.)

Goldman Sachs Asset Management 163

Energy Equity

Markets

Goldman Sachs Asset Management 17Energy Equities Have Outperformed But Remain Cheap

On a price basis, Energy has outperformed the S&P 500 Index by 81% since the start of 2021,

however, the sector is still down 21% from 2014 highs, while the S&P 500 is up 131%

Price Performance 2021 2022 YTD Price Performance 2021 2022 YTD

Energy Select Sector Index (IXE) +47% +38% Alerian Midstream Energy Index (AMNA) +30% 22%

S&P 500 Index +27% -5% S&P 500 Index +27% -5%

Delta +20% +43% Delta +3% +27%

BROAD ENERGY VALUATIONS (EV/EBITDA SPREAD TO S&P 500)1 MIDSTREAM VALUATION (EV/EBITDA SPREAD TO S&P 500)2

EV/EBITDA Spread to S&P 500 10-Year Avg. Spread EV/EBITDA Spread to S&P 500 10-Year Avg. Spread

4.0x 12.0x

-2.3x Discount vs. 10-Year Average -5.1x Discount vs. 10-Year Average

0.0x 6.0x

-4.0x 0.0x

-8.0x -6.0x

-12.0x -12.0x

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Sources: Goldman Sachs Asset Management, Bloomberg, and Wells Fargo. Data as of March 31, 2022. 1Broad Energy valuations represented through the Energy Select Sector Index (IXE). 2Midstream

valuations represented through the Alerian MLP Index (AMZ) as MLPs have historically comprised the majority of midstream market cap. Past performance does not guarantee future results, which

may vary.

Goldman Sachs Asset Management 18Significant Capital Discipline Has Led to Record FCF

Energy companies are focused on reducing spending, increasing free-cash-flow (FCF) and driving

shareholder value through debt reduction, dividend increases and share buybacks

BROAD ENERGY CAPITAL SPENDING ($ BILLIONS) MIDSTREAM CAPITAL SPENDING ($ BILLIONS)

$100 $100

Expected to be Down 22% Since 2019 Expected to be Down 43% Since 2019

$75 $75

$50 $50

$25 $25

$59 $74 $82 $52 $49 $64 $49 $56 $51 $38 $31 $29

$0 $0

2017 2018 2019 2020 2021 2022E 2017 2018 2019 2020 2021 2022E

BROAD ENERGY FREE-CASH-FLOW YIELDS MIDSTREAM FREE-CASH-FLOW YIELDS

FCF Yield (%) $/bbl FCF Yield (%) $/bbl

12.0% $120 12.0% $120

Avg. Brent Oil Price Avg. Brent Oil Prices

9.0% $90 8.0% $90

6.0% $60 4.0% $60

0.9% 7.6% 11.4% 9.4%

3.0% $30 0.0% $30

-1.2% -1.1%

1.6% 3.7% 2.2% 3.2% 9.8% 10.1%

0.0% $0 -4.0% $0

2017 2018 2019 2020 2021 2022E 2017 2018 2019 2020 2021 2022E

Sources: Goldman Sachs Asset Management, Wells Fargo and Bloomberg. Data as of March 31, 2022. Broad Energy is represented through the top 15 constituents of the Energy Select Sector Index

(IXE). Midstream is represented through the top 15 constituents of the Alerian Midstream Energy Index (AMNA). Past performance does not guarantee future results, which may vary.

Goldman Sachs Asset Management 19Crude Oil Prices Are Expected To Remain High

Constructive commodity outlook should continue to support earnings growth for energy equities,

further strengthening their ability to drive shareholder value

GOLDMAN SACHS GLOBAL INVESTMENT RESEARCH (GIR) BRENT CRUDE OIL PRICE FORECASTS

Prior to February 24, 2022 Russian Invasion After February 24, 2022 Russian Invasion

Period % Change

(Reflects Price Forecast as of January 17, 2022) (Reflects Latest Price Forecast as of March 31, 2022)

2Q 2022 $95 $125 +32%

3Q 2022 $100 $125 +25%

4Q 2022 $100 $125 +25%

1Q 2023 $105 $115 +10%

2Q 2023 $105 $115 +10%

3Q 2023 $105 $115 +10%

4Q 2023 $105 $115 +10%

2022 Average1 $98 $125 +27%

2023 Average $105 $115 +10%

Sources: Goldman Sachs Asset Management, Goldman Sachs Global Investment Research (GIR). Data as of March 31, 2022 unless otherwise noted. 12022 average covers 2Q 2022 through 4Q 2022

forecasts. The economic and market forecasts presented herein are for informational purposes as of the date of this presentation. Any reference to a specific company or security does not constitute a

recommendation to buy, sell, hold or directly invest in the company or its securities. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this

presentation. Past performance does not guarantee future results, which may vary.

Goldman Sachs Asset Management 20Investor Interest Is Returning to the Energy Sector

The largest energy sector ETF has seen AUM growth of nearly 500% in the last 2 years; driven

heavily by investor flows ($13.9 Bn)1

ETF PERFORMANCE & ASSETS UNDER MANAGEMENT ENERGY SECTOR AS A PERCENTAGE OF THE S&P 500 INDEX

Share Price Increase AUM Growth Tech Energy

600% 50.0%

40.0%

400%

28.1%

30.0%

200%

20.0%

0%

10.0%

3.7%

-200% 0.0%

Feb-20 Jun-20 Oct-20 Feb-21 Jun-21 Oct-21 Feb-22 1995 1998 2001 2004 2007 2010 2013 2016 2019 2022

We expect that energy will continue to benefit from the growth-to-value trade and will see additional interest as the world’s perception around

energy security/terminal value, shifts and money managers rationalize underweight energy exposure.

Sources: Goldman Sachs Asset Management, U.S. Capital Advisors, and Bloomberg. Data as of March 31, 2022. 1Investor money flow figures provided by U.S. Capital Advisors; data as of February, 28,

2022. The economic and market forecasts presented herein are for informational purposes as of the date of this presentation. There can be no assurance that the forecasts will be achieved. Please see

additional disclosures at the end of this presentation.

Goldman Sachs Asset Management 21Energy Has Historically Outperformed During Rising Inflation

Oil & gas stocks historically outperform broader equity markets during periods of inflation, which may

act as an additional tailwind for the sector

U.S. CONSUMER PRICE INDEX (CPI) URBAN CONSUMERS

16.0%

12.0%

8.0%

4.0%

0.0%

-4.0%

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Inflationary Period1 Oil & Gas Sector Return S&P 500 Index Return Oil & Gas Sector Outperformance

1969- 1981 +383% +120% +263%

1987-1990 +80% +57% +23%

2003-2008 +145% +15% +130%

Sources: Goldman Sachs Asset Management, Bloomberg, and Professor Kenneth French and the Tuck School of Business at Dartmouth College. Data as of December 31, 2021. 1Inflationary years

defined through consecutive periods of sustained inflation over 2%. Past performance does not guarantee future results, which may vary.

Goldman Sachs Asset Management 224

Midstream Offers Unique

Exposure

Goldman Sachs Asset Management 23North American Energy Infrastructure (Midstream)

Critical assets servicing the growing need for North American energy, offering strong yields supported

by robust FCF and moderate beta to commodity prices

Sector Takeaways

Midstream Fundamentals are the Healthiest on Record: 5-7%

Dividend

• Higher oil & natural gas prices have supported strong earnings growth and FCF has inflected Yields

meaningfully higher (sector is trading with ~10% FCF yields).

• Capital return to shareholders has been prioritized with dividend growth expectations in the double digits

for years to come.

Midstream Offers Unique Asset Class Attributes:

• Highest yielding income equity sector (6%+) with ability to keep pace, or exceed inflation expectations. ~10%

Free-Cash-Flow

• Provides exposure to the long-term North American energy opportunity and 0.5 beta to oil prices. Yields

• May be a relative beneficiary during inflationary periods given contract inflation escalators and fixed cost

structures that may provide operating leverage.

Midstream Valuations Cheap on All Metrics and Fund Flow Activity Has Resumed:

• Trading at a deep valuation discount (P/E, EV/EBITDA, FCF Yield, etc.) relative to history, other income

oriented equities, and broader equity markets. $921M

YTD Net Money

• Fund flows to energy sector have returned, with midstream seeing $921 million in this year alone. Flows

Sources: Goldman Sachs Asset Management, Bloomberg, and Wells Fargo. Data as of March 31, 2022. Free-cash-flow: operating cash flow less capital expenditures (CAPEX). Free-cash-flow yield:

free-cash-flow divided by equity value. MMbpd: Million barrels per day. Please see appendix & disclosures for additional information on asset classes. The economic and market forecasts presented

herein are for informational purposes as of the date of this presentation. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this presentation.

Past performance does not guarantee future results, which may vary.

Goldman Sachs Asset Management 24Fundamentals Strongest on Record

Earnings growth and CAPEX reductions have provided a pathway to strong FCF generation, which is

being used to lower leverage and return shareholder capital through dividend growth and buybacks

TOP 15 U.S. MIDSTREAM EBITDA ($ BILLIONS) TOP 15 U.S. MIDSTREAM FREE-CASH-FLOW ($ BILLIONS)

$65 $50

$60 $30

$55 $10

$18 $38 $33 $33

-$1

$52 $53 $57 $62 $63

$50 -$10

2019 2020 2021 2022E 2023E 2019 2020 2021E 2022E 2023E

TOP 15 U.S. MIDSTREAM LEVERAGE (DEBT/EBITDA) TOP 15 U.S. MIDSTREAM AGGREGATE DPS ($ BILLIONS)

5.0 x $30

4.5 x

$25

4.0 x

$20

3.5 x

4.5x 4.5x 4.0x 3.8x 3.6x $27 $22 $20 $22 $24

3.0 x $15

2019 2020 2021 2022E 2023E 2019 2020 2021 2022E 2023E

Sources: Goldman Sachs Asset Management and Bloomberg. Data as of March 31, 2022. The economic and market forecasts presented herein are for informational purposes as of the date of this

presentation. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this presentation. Past performance does not guarantee future results,

which may vary.

Goldman Sachs Asset Management 25One Of The Highest Yielding Sectors

Sector yields of approximately 6% (underpinned by strong FCF) which is five times that of the S&P

500, and more than double the Utilities and REIT sectors

INCOME-ORIENTED ASSET CLASS YIELDS

Equity Markets Fixed Income Markets

10.0% Positive Inflation

Adjusted Yields

7.5%

5.0% 2022 Inflation

Estimate: 5.0%1

2.5%

Negative Inflation

Adjusted Yields

0.0%

MLPs Energy Infra. Global REITs Utilities S&P 500 High Yield Investment Municipal

C-Corps Infrastructure Bonds Grade Bonds Bonds

Sources: Goldman Sachs Asset Management, Goldman Sachs Global Investment Research (GIR), Bloomberg, and Wells Fargo. Data as of March 31, 2022. 12022 inflation estimate provided by

Goldman Sachs Investment Research. MLPs are represented by the Alerian MLP (AMZ) Index. C-Corps are represented by the C-Corp structured companies in the Alerian Midstream Energy Index

(AMNA). The economic and market forecasts presented herein are for informational purposes as of the date of this presentation. There can be no assurance that the forecasts will be achieved. Please

see additional disclosures at the end of this presentation. Past performance does not guarantee future results, which may vary.

Goldman Sachs Asset Management 26Energy Exposure With Moderate Commodity Price Beta

Midstream sector can provide access to the growing story around North American energy resources

with moderate commodity price correlation

MIDSTREAM SECTOR’S 10-YEAR CORRELATION WITH VARIOUS ASSET CLASSES (WEEKLY CALCULATION)

1.0x

0.8x

0.70x

0.5x 0.61x 0.59x 0.59x 0.56x

0.53x 0.50x

0.41x

0.3x

0.28x

0.0x

0.05x

-0.03x

-0.3x -0.13x

-0.19x

-0.5x

Global Value Global High Yield S&P Crude Growth REITs Utilities Gold Muni IG U.S. Dollar

Infra. Equities Equities Bonds 500 Oil Equities Bonds Bonds

Sources: Goldman Sachs Asset Management and Bloomberg. Data as of December 31, 2021. The economic and market forecasts presented herein are for informational purposes as of the date of this

presentation. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this presentation. Past correlations are not indicative of future correlations,

which may vary. Past performance does not guarantee future results, which may vary.

Goldman Sachs Asset Management 27Business Models May Be a Relative Beneficiary of Inflation

Inflation escalation clauses and fixed cost structures may boost operating margins for midstream

companies

Potential Investment Case for the Midstream Sector

• We believe the midstream sector is poised to fare better during an inflationary environment given:

• Inflation escalators integrated into tariff-setting mechanisms.

• Largely fixed cost structures that may potentially provide operating leverage and improved operating margins.

• Linked to the oil & gas sector, which historically outperformed during inflationary periods.

• Attractive dividend yields that may have room to grow and keep pace, or exceed, inflation.

Type of Asset Potential Inflation Mitigants

Refined Petroleum Product Pipelines Tariffs linked to Producers Price Index (PPI + 0.78%)

Gathering & Processing Contracts include Consumer Price Index (CPI) escalators

Tariffs established via rate cases using cost-of-service methodology – allows for return on & of

Natural Gas Pipelines (FERC-Regulated)

capital + expense pass-through

Sources: Goldman Sachs Asset Management and public company filings. Data as of March 31, 2022. The economic and market forecasts presented herein are for informational purposes as of the date

of this presentation. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this presentation.

Goldman Sachs Asset Management 285

Evaluating Terminal

Value Concerns

Goldman Sachs Asset Management 29Oil: A Critical Global Commodity

Recent energy crisis has precipitated a change in perception of fossil fuels with the reality of rising

consumer power prices being weighed against the pace of decarbonization initiatives

We believe there is significant support, and growth, for oil demand through 2035 with peak oil proponents yet to offer a

credible pathway for sustained population & prosperity growth without simultaneous increases in energy consumption.

Growth in Population & Prosperity

• The majority of the world’s population (63%) consumes less than 4 barrels of oil per person, annually.

• For context, the developed world (U.S. Europe, Japan, etc.) consumes 10-21 barrels of oil per person, annually.

• World population expected to grow to 8.8 billion by 2035 vs. 7.6 billion in 2019.

• Rising population & prosperity increases oil demand, a trend we expect to continue, and be particularly strong in China & India.

• Growing electric vehicle (EV) penetration is not a threat to oil demand growth in our view (example: Norway).

Sources: Goldman Sachs Asset Management, U.S. Census Bureau, and BP Statistical Review. Latest year-end data available as of March 31, 2022. The economic and market forecasts presented

herein are for informational purposes as of the date of this presentation. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this presentation.

Goldman Sachs Asset Management 30Majority of the World Is Still “Energy Poor”

63% of the world’s population has per capita oil consumption of less than 4.0 bbls; a normalization to

even half that of Western Europe, suggests significant long-term demand growth

PER CAPITA OIL CONSUMPTION (BARRELS PER YEAR)

25 Canada | 23.3 bbls

South Asia

U.S. | 21.6 bbls Africa

India

20 Central Asia

China

South America

15 LATAM & Carribbean

SE Asia

Japan | 11.0 bbls

Eastern Europe

Western Europe | 9.9 bbls

10 West Asia

Western Europe

South East Asia | 5.8 bbls Japan

Oceania

5 China | 3.7 bbls

Middle East

Africa | 1.1 bbls India | 1.4 bbls USA

Canada

0

0 10 20 30 40 50 60 70 80 90 100

% of Global Population

As a point of reference, on an annual basis, Western Europe consumes 9.9 barrels of oil per person, while the U.S. consumes 21.6

barrels per person, and Japan consumes 11.0 barrels per person.

Sources: Goldman Sachs Asset Management and BP Statistical Review. Latest year-end data available as of March 31, 2022.

Goldman Sachs Asset Management 31Oil Consumption Directly Correlated With Rising Prosperity

Rising prosperity globally has historically driven oil demand, a trend which we believe will continue to

support growth in global oil consumption going forward

INCOME AND OIL CONSUMPTION (1999) INCOME AND OIL CONSUMPTION (2019)

Number of Countries Per Zone Zone of Convergence Number of Countries Per Zone Zone of Convergence

125 125

0 1 6 0 0 0 5 1

Per Capita Oil Consumption

Per Capita Oil Consumption

25 25

1 13 26 0 0 7 40 0

5 5

0 14 China 2 0

6 15 0 0

1 1 India

4 0 0 0 0 3 0 0

0 0

$100 $1,000 $10,000 $100,000 $1,000,000 $100 $1,000 $10,000 $100,000 $1,000,000

Per Capita Income Per Capita Income

From 1999-2019, the number of countries with per capita incomeGrowing Share of Electric Vehicles ≠ Collapse in Oil Demand

Using Norway as an example, EV sales have reached over 60% of total car sales, representing 16%

of the total fleet, however, oil demand today in the country is actually higher than 2016

NORWAY OIL CONSUMPTION & ELECTRIC VEHICLE SHARE

Oil Consumption (12-Month Moving Avg.) EV Share of New Car Sales (12-Month Moving Avg.) EV Share of Total Car Fleet

260 80%

Norway Oil Consumption (Kbpd)

240 60%

Electric Vehicle Share

220 40%

200 20%

180 0%

2016 2017 2018 2019 2020 2021

It’s important to highlight that passenger vehicles comprise only a small percentage of total oil demand, and the fleet (including ICEs) is still

growing. This, paired with increased demand from non-passenger vehicles has kept oil consumption flat.

Sources: Goldman Sachs Asset Management and Morgan Stanley. Data as of February 28, 2022. The economic and market forecasts presented herein are for informational purposes as of the date of

this presentation. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this presentation.

Goldman Sachs Asset Management 33Oil: Long-Term Demand Through 2035

We do not have near-term peak oil demand concerns and expect global oil demand to hit 108 million

barrels per day by 2035 – approximately 12% above 2019 levels

2035 CRUDE OIL DEMAND BRIDGE (MMBDP)

135

120

-9.4

13.6

105 -1.7

7.8

90

98.2 110.1 108.4

75

2019 Population Living EVs 2035 EVs 2035

Growth Standards (Developed Nations) (Ex. China EV Impact) (China)

We expect growing world population and rising per capita income to drive oil demand higher by ~21 MMbpd while EV usage in developed

markets displaces ~9 MMb/d of demand and EV adoption in China could result in an additional ~1.7 MMbpd of declines.

Sources: Goldman Sachs Asset Management, OPEC+, International Energy Agency (IEA) and BP Statistical Review. Latest year-end data available as of March 31, 2022. MMb/d: Millions of barrels per

day. The economic and market forecasts presented herein are for informational purposes as of the date of this presentation. There can be no assurance that the forecasts will be achieved. Please see

additional disclosures at the end of this presentation.

Goldman Sachs Asset Management 346

Natural Gas &

Decarbonization

Goldman Sachs Asset Management 35Natural Gas Has Proven Effective in Lowering Emissions

The U.S. has led all countries across the globe in CO2 emission reductions since 2005, with the

majority of this effort achieved by coal-to-gas switching in over 200 locations

EXAMPLE OF COAL-TO-GAS SWITCHING1 U.S. CO2 REDUCTION BY SOLUTION 2005-20192 CO2 REDUCTION 2005 – 20193 (MMT OF CO2)

MT CO2e/GWH1

1,400

Country CO2 Reduction

1,200

United States -959

1,031

1,000 United Kingdom -188

60% reduction in CO2 Italy -147

from switching to gas Solar

800 31% Germany -144

Coal-to Gas-

600 Japan -122

Switching

61%

Ukraine -120

395

400

Wind Spain -104

8%

200 France -77

Venezuela -51

0

Coal Natural Gas Greece -39

Sources: Goldman Sachs Asset Management, EQT Corporation, Energy Information Administration (EIA), International Energy Agency (IEA). Latest year-end data available as of March 31, 2022. MMT

of CO2: Million Metric Tons of CO2. 1EIA electricity data and power plant emissions 2020, EIA carbon dioxide emissions coefficients, EIA average operating heat rate. 2Data obtained from EIA’s U.S.

Energy-Related Carbon Dioxide Emissions, 2019 report, splitting wind and solar proportionally to their increased in power generation from 2005 to 2019 per EIA’s renewable generation data. 3Data

obtained from IEA World Energy outlook 2021; EIA emissions data; EIA form 80 retired plant data and EQT analysis.

Goldman Sachs Asset Management 36Coal-To-Natural Gas Projects Have Had A Substantial Impact

Projects to replace coal plants with natural gas plants have proved to be the most effective emissions

reduction effort when compared to the leading green projects globally

IMPACT OF LARGE GREEN PROJECTS GLOBALLY: ANNUAL MMT OF CO2 REDUCED FROM 2005-2019

600

400

200

0

U.S. Coal-to-Gas Switching 1 Germany Energiewende 2 China's Three Gorges 3 Brazil Hydro 4

U.S. Coal-to-Gas Switching Germany Energiewende China’s Three Gorges

• Replaced >200 coal plants • ~30,000 windmills & 2 million • Hydroelectric gravity dam

since 2005 solar arrays installed5

• Government funded: $37 Bn8

• Projects completed by natural • Government funded: ~$80 Bn6

gas industry • Largest power plant in the

• Electricity costs up 3x since world

• Natural gas run 50% more 20007

efficiently than coal plants

Sources: Goldman Sachs Asset Management, EQT Corporation, IEA World Energy outlook 2021, EIA, Germany’s Federal Ministry for Economic Affairs and Energy, S&P Global, BDEW Bundesverband

der Energie, German Wind Energy Association (BWE), Clean Energy Wire, and Reuters. Latest year-end data available as of March 31, 2022. MMT of CO2: Million Metric Tons of CO2. 1Total CO2

emissions variation between 2005 and 2019 according to EIA report. 2Germany’s CO2 emissions reduction from 2005 to 2020 (from 997 to 749 MtCO2) based on Federal Ministry For Economic Affairs

And Climate Action data. 3China’s Three Gorges Dam 110 TWh generation in 2020 assumed to replace coal which has a carbon intensity factor of 1.15 MtCO2/TWh. 4Brazil hydro generation growth

between 2005 and 2020 was 60 TWh assumed to replace coal which has a carbon intensity factor of 1.15 MtCO2/TWh. 5Per Germany’s wind Energy association and Clean Energy Wire. 6Estimated

Germany’s climate financing from 2011 through 2021. 7Price index x3 in 2019 compared to 2000 based on BDEW data. 8China's Three Gorges Dam, including resettling the 1.3 million people it

displaced, cost 254.2 billion yuan ($37.23 billion), according to the Xinhua news agency.

Goldman Sachs Asset Management 37Potential Emissions Reduction From Coal-to-Gas Switching

We estimate that coal-to-gas switching represents a 30-40 Bcf/d potential opportunity for natural gas /

LNG exporting nations; to put this in context, total global trade in LNG averaged 47 Bcf/d in 2020

COAL-TO-GAS SWITCHING CO2 EMISSIONS BRIDGE (MILLION TONNES)

Total CO2

Emissions From

8,000

~1,400 MM Tonnes of CO2

U.K., Italy,

Other* Reduction From Coal-to- France, Spain, &

Gas Switching Netherlands

Japan

6,000

India

4,000

China

2,000

0

Current CO2 From Coal CO2 Reduction From CO2 From Coal Power Equivalent CO2

Power 30% Coal-to-Gas Post Coal to Gas Emissions

Switching Switching

If the largest coal-fired power producing countries switched 30% of generation from coal to natural gas, reduction would be equivalent to

UK, Italy, France, Spain & Netherlands all eliminating 100% of their CO2 emissions.

Sources: Goldman Sachs Asset Management and BP Statistical Review. Latest year-end data available as of March 31, 2022. Bcf/d: Billions of cubic feet per day. LNG: Liquefied natural gas. These

examples are for illustrative purposes only and are not actual results. If any assumptions used do not prove to be true, results may vary substantially. The economic and market forecasts presented

herein are for informational purposes as of the date of this presentation. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this presentation.

Goldman Sachs Asset Management 38Renewable Power Generation Suffers From Intermittency

Low wind output in Europe caused a spike in gas usage, which coupled with gas supply disruption

from the Russian/Ukraine conflict, is expected to result in a 54% increase in UK energy bills in April

EUROPEAN WIND GENERATION & NATURAL GAS PRICES

Megawatts 4-Week Average Daily European Wind Generation 3-Month Rolling Avg. TTF Natural Gas Prices TTF Natural Gas Prices

24,000 €40

18,000 €30

12,000 €20

6,000 €10

0 €0

Dec-20 Mar-21 Jun-21 Sep-21 Dec-21 Mar-22

Sources: Goldman Sachs Asset Management and Bloomberg. Data as of March 31, 2022. Past performance does not guarantee future results, which may vary.

Goldman Sachs Asset Management 39Associated Costs Are Still High For Renewables

In our view, levelized cost of energy (LCOE), a common measure of renewables cost, is an incomplete

metric as it does not account for high associated costs of transmission and back-up generation

LEVELIZED COST OF ENERGY ($/MWH) POWER PRICES AND % OF RENEWABLE GENERATION

Onshore Wind Offshore Wind Utility PV (Solar)

$400 € 0.40

Greater dependence on renewable power has a direct relationship with

higher consumer prices with an R2 = 0.456

$300 € 0.30 Germany

European Power Prices

Denmark

Belgium

Ireland

Spain

United Kingdom

Austria Italy

Portugal

$200 € 0.20 France Luxembourg

Czech Republic

Finland

Slovakia Cyprus Sweden Greece

Slovenia Poland

Latvia Romania

Norway Netherlands

Estonia

Iceland Croatia

$100 € 0.10 Hungary

Bulgaria Turkey

North Macedonia

Ukraine

$0 € 0.00

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 0.0% 20.0% 40.0% 60.0%

% of Power Generation From Renewable Sources (Wind & Solar)

Sources: Goldman Sachs Asset Management, BP Statistical Review, Eurostat, and BloombergNEF. Latest year-end data available as of March 31, 2022. Past performance does not guarantee future

results, which may vary.

Goldman Sachs Asset Management 40Geopolitics of Renewables May Also Be Problematic

Select countries control significant material and resources needed to scale renewables, and

accelerated agendas may have unintended environmental, cost, labor and geopolitical implications

SHARE OF TOP COUNTRIES IN PRODUCTION & PROCESSING OF KEY ENERGY TRANSITION MATERIALS

Minerals Production

Minerals Top 3 Producing Countries % of Supply from Top Country % of Supply from Top 3 Countries

Copper Chile, Peru, China 28% 48%

Nickel Indonesia, Philippines, Russia 33% 56%

Cobalt DR Congo, Russia, Australia 69% 77%

Rare Earths China, US, Myanmar 60% 84%

Lithium Australia, Chile, China 52% 87%

Minerals Processing

Minerals Top 3 Processing Countries % of Processing by Top Country % of Processing by Top 3 Countries

Copper China, Chile, Japan 40% 56%

Nickel China, Indonesia, Japan 35% 58%

Cobalt China, Finland, Belgium 65% 80%

Rare Earths China, Malaysia, Estonia 87% 100%

Lithium China, Chile, Argentina 58% 97%

In our view, there needs to be an appropriate balance between renewable and fossil fuel energy sources in order to ensure safe, reliable, and

affordable energy for decades to come. We believe the recent global energy crisis may have shed light on this reality.

Sources: Goldman Sachs Asset Management and International Energy Agency (IEA). Latest year-end data available as of March 31, 2022. Past performance does not guarantee future results,

which may vary.

Goldman Sachs Asset Management 417

Appendix &

Disclosures

Goldman Sachs Asset Management 42General Definitions

It is not possible to invest directly in an unmanaged index.

Midstream: Midstream investments include both Master Limited Partnership (MLP) and C-Corporation (C-Corp) structured companies that are engaged in the treatment, gathering,

compression, processing, transportation, transmission, fractionation, storage and terminalling of natural gas, natural gas liquids, crude oil, refined products or coal. Midstream

companies may also operate ancillary businesses including marketing of energy products and logistical services.

Upstream: exploration & production companies (E&Ps); generally engaged in the exploration, recovery, development and production of crude oil, natural gas and natural gas

liquids.

MLPs Only – Alerian MLP Total Return Index (AMZ) – the leading gauge of energy Master Limited Partnerships (MLPs). The float-adjusted, capitalization-weighted index, whose

constituents represent approximately 85% of total float-adjusted market capitalization, is disseminated real-time on a price-return basis (AMZ) and on a total-return basis (AMZX).

“Alerian MLP Index”, “Alerian MLP Total Return Index”, “AMZ” and “AMZX” are trademarks of Alerian and their use is granted under a license from Alerian or “Source: Alerian”.

MLPs + C-Corps – Alerian Midstream Energy Index (AMNAX) – a broad-based composite of North American energy infrastructure companies. The capped, float-adjusted,

capitalization-weighted index, whose constituents earn the majority of their cash flow from midstream activities involving energy commodities, is disseminated real-time on a price-

return basis (AMNA) and on a total-return basis (AMNAX).

Broad Energy Equities – Energy Select Sector Index (IXE) – a modified market capitalization-based index intended to track the movements of companies that are components of

the S&P 500 and are involved in the development or production of energy products.

Utilities – PHLX Utility Sector Index (UTY) – a market capitalization-weighted index composed of geographically diverse public utility stocks.

Real Estate Investment Trusts (REITS) – FTSE/NAREIT North America Index – gauges the performance of companies that develop and own real estate in North America.

10 Year Treasury – BofA Merrill Lynch US Treasuries (10Y) Index – an unmanaged index that tracks the performance of the three most recently issued 10-year US Treasury notes.

Natural Gas – N G1 Contract – tracks the one m

onth forward natural gas fu tures tradin gin units o f 10,000 m

illion British ther m

al unites ( mmBt u ). The price is based on delivery at

the Henry Hub in Louisiana.

WTI Crude Oil – CL1 Contract – tracks the one month forward WTI crude oil futures contracts that trade in units of 1,000 barrels, and the delivery point is Cushing, Oklahoma, which

is also accessible to the international spot markets via pipelines.

Brent Crude Oil – CO1 Contract – tracks the one month forward price of Brent crude oil. Current pipeline export quality Brent blend as supplied at Sullom Voe. ICE Brent Futures is

a deliverable contract based on EFP delivery with an option to cash settle.

Real Asset Classes: Real assets are often defined as physical or tangible assets that tend to provide a “real return,” often linked to inflation. This definition encompasses a wide

range of potential investments, including real estate, infrastructure, timberlands, agrilands, commodities, precious metals, and natural resources.

Stocks: Stock investments are subject to market risk, which means that the value of the securities may go up or down in response to the prospects of individual companies,

particular sectors and/or general economic conditions.

Bonds: Fixed income investing involves interest rate risk. When interest rates rise, bond prices generally fall.

High Yield: Below investment grade (high yield) bonds are more at risk of default and are subject to liquidity risk.

Goldman Sachs Asset Management 43General Definitions

Free Cash Flow (FCF): Operating Cash flow less Capital Expenditures (CAPEX). Free cash flow is the cash a company produces through its operations, less the cost of

expenditures on assets. In other words, free cash flow (FCF) is the cash left over after a company pays for its operating expenses and capital expenditures.

Capital Expenditures (CAPEX): Funds used by a company to acquire, upgrade, and maintain physical assets such as property, buildings, an industrial plant, technology, or

equipment.

EV/EBITDA: Enterprise Value (EV) divided by earnings before interest, taxes, depreciation, and amortization (EBITDA). EV is calculated as follows: Market Capitalization +

Preferred Shares + Minority Interest + Debt – Total Cash.

CAGR: Compound annual growth rate is a business and investing specific term for the geometric progression ratio that provides a constant rate of return over the time period.

Volatility: a statistical measure of the dispersion of returns for a given security or market index.

Share Buyback: Issuer buys back its own outstanding shares to reduce the number of shares available on the open market

OPEC+: Organization of Petroleum Exporting Countries, and Russia.

Spread: A spread is the difference between two numbers, usually between two types of yields such as the yield of a security above a 10 year treasury bill.

Basis point (BPS): refers to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th o f 1%, or 0.01%, or 0.0001, and is

used to denote the percentage change in a financial instrument.

Correlation: is a measure of the amount to which two investments vary relative to each other.

Goldman Sachs Asset Management 44General Disclosures

Views are as of April 6, 2022 unless noted otherwise and are subject to change in the future.

Master Limited Partnerships ("MLPs") may be generally less liquid than other publicly traded securities and as such can be more volatile and involve higher risk. Investments in

securities of an MLP involve risks that differ from investments in common stocks, including risks related limited control and limited rights to vote on matters affecting the MLP, risks

related to potential conflicts of interest between the MLP and the MLP’s general partner, cash flow risks, dilution risks and risks related to the general partner’s right to require unit

holders to sell their common units at an undesirable time or price. MLPs are also generally considered interest-rate sensitive investments. During periods of interest rate volatility,

these investments may not provide attractive returns.

The Global Industry Classification Standard (“GICS”) was developed by and is the exclusive property and a service mark of MSCI Inc. (“MSCI”) and S&P Global Market Intelligence

(“S&P”) and is licensed for use by Goldman Sachs. Neither MSCI, S&P, nor any other party involved in making or compiling the GICS or any GICS classifications makes any

express or implied warranties or representations with respect to such standard or classification (or the results to be obtained by the use thereof), and all such parties hereby

expressly disclaim all warranties of originality, accuracy, completeness, merchantability and fitness for a particular purpose with respect to any of such standard or classification.

Without limiting any of the foregoing, in no event shall MSCI, S&P, any of their affiliates or any third party involved in making or compiling the GICS or any GICS classifications have

any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even i f notified of the possibility of such damages.

Investments in MLPs are subject to certain risks, including risks related to limited control and limited rights to vote, potential conflicts of interest, cash flow risks, dilution risks, limited

liquidity and risks related to the general partner’s right to force sales at undesirable times or prices.

MLPs may also involve substantially different tax treatment than other equity-type investments, and such tax treatment could be disadvantageous to certain types of investors, such

as retirement plans, mutual funds, charitable accounts, foreign investors, retirement accounts or charitable entities. In addition, investments in MLPs may trigger state tax reporting

requirements. Generally, a master limited partnership (“MLP”) is treated as a partnership for Federal income tax purposes. Therefore, investors in an MLP may be subject to certain

taxes in addition to Federal income taxes, including state and local income taxes imposed by the various jurisdictions in which the MLP conducts business or owns property. In

addition, certain tax-exempt investors in an MLP, such as tax-exempt foundations and charitable lead trusts, may incur unrelated business taxable income (“UBTI”) with respect to

their investment. UBTI may result in increased Federal, and possibly state and local, tax costs, and may also result in additional filing requirements for tax exempt investors. Non-US

investors may be subject to US taxation on a net income basis and have US filing obligations as a result of investing in MLPs. The tax reporting information for MLPs generally is

provided to investors on an annual IRS Schedule K-1, rather than an IRS Form 1099. To the extent the Schedule K-1 is delivered after April 15, you may be required to request an

extension to file your tax returns.

Exposure to the commodities markets may subject an investor to greater volatility than investments in traditional securities.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by Goldman Sachs Asset Management to buy, sell, or hold any security.

Views and opinions are current as of the date of this presentation and may be subject to change, they should not be construed as investment advice.

References to indices, benchmarks or other measures of relative market performance over a specified period of time are provided for your information only and do not imply that the

portfolio will achieve similar results. The index composition may not reflect the manner in which a portfolio is constructed. While an adviser seeks to design a portfolio which reflects

appropriate risk and return features, portfolio characteristics may deviate from those of the benchmark.

Economic and market forecasts presented herein reflect a series of assumptions and judgments as of the date of this presentation and are subject to change without notice. These

forecasts do not take into account the specific investment objectives, restrictions, tax and financial situation or other needs of any specific client. Actual data will vary and may not be

reflected here. These forecasts are subject to high levels of uncertainty that may affect actual performance. Accordingly, these forecasts should be viewed as merely representative

of a broad range of possible outcomes. These forecasts are estimated, based on assumptions, and are subject to significant revision and may change materially as economic and

market conditions change. Goldman Sachs has no obligation to provide updates or changes to these forecasts. Case studies and examples are for illustrative purposes only.

Goldman Sachs Asset Management 45General Disclosures

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED

OR UNLAWFUL TO DO SO.

Prospective investors should inform themselves as to any applicable legal requirements and taxation and exchange control regulations in the countries of their citizenship, residence

or domicile which might be relevant.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down

as well as up. A loss of principal may occur.

Goldman Sachs does not provide legal, tax or accounting advice, unless explicitly agreed between you and Goldman Sachs (generally through certain services offered only to clients

of Private Wealth Management). Any statement contained in this presentation concerning U.S. tax matters is not intended or written to be used and cannot be used for the purpose

of avoiding penalties imposed on the relevant taxpayer. Notwithstanding anything in this document to the contrary, and except as required to enable compliance with applicable

securities law, you may disclose to any person the US federal and state income tax treatment and tax structure of the transaction and all materials of any kind (including tax opinions

and other tax analyses) that are provided to you relating to such tax treatment and tax structure, without Goldman Sachs imposing any limitation of any kind. Investors should be

aware that a determination of the tax consequences to them should take into account their specific circumstances and that the tax law is subject to change in the future or

retroactively and investors are strongly urged to consult with their own tax advisor regarding any potential strategy, investment or transaction.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research

or investment advice. This material has been prepared by Goldman Sachs Asset Management and is not financial research nor a product of Goldman Sachs Global Investment

Research (GIR). It was not prepared in compliance with applicable provisions of law designed to promote the independence of financial analysis and is not subject to a prohibition on

trading following the distribution of financial research. The views and opinions expressed may differ from those of Goldman Sachs Global Investment Research or other departments

or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or selling any securities. This information may not be current

and Goldman Sachs Asset Management has no obligation to provide any updates or changes.

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and assumed

without independent verification, the accuracy and completeness of all information available from public sources.

GSAM leverages the resources of Goldman Sachs & Co. LLC subject to legal, internal and regulatory restrictions.

Goldman Sachs & Co. LLC, member FINRA.

Date of First Use: April 6, 2022

Compliance Code : 275255-OTU-1588266

Goldman Sachs Asset Management 46You can also read