MNI RBA Review - May 2022 - May 2022 Contents MNI POV (Point Of View)

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

MNI RBA Review - May 2022

Meeting Date: Tuesday 3 May 2022

Link To Statement: https://www.rba.gov.au/media-releases/2022/mr-22-12.html

Contents

• Page 2: RBA 3 May 2022 Meeting Statement

• Page 3-4: RBA Governor Lowe’s Post-Meeting Address

• Page 5: RBA STATE OF PLAY: RBA Could Take Rates To 2.5%, Says Lowe

• Page 6-10: Sell-Side Analyst Views

MNI POV (Point Of View): Curveball

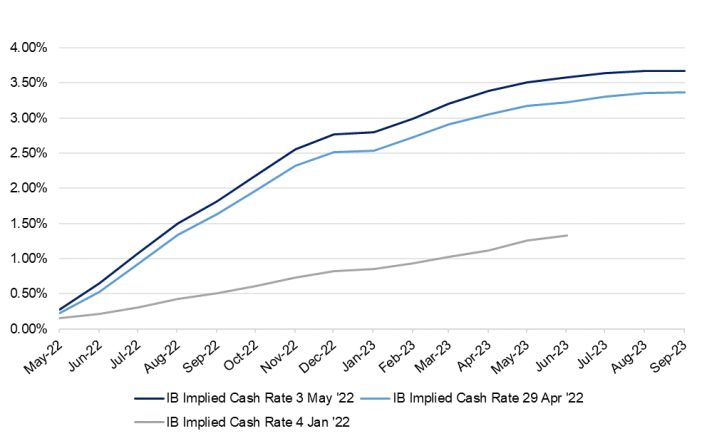

The RBA delivered a surprise 25bp cash rate hike (consensus looked for 15bp) in May, with an identical move in

the rate paid on E/S balances (to 0.25%). Liquidity in the system means that the cash rate should operate shy of

the 0.35% target (the norm in the post-QE era). The Bank flagged more notable wage growth unearthed via its

liaison scheme, after Q122 CPI data provided clear signals re: strengthening upward price pressures, pushing the

RBA into action ahead of the Q122 WPI print. The Bank also outlined a passive runoff of bonds held on its B/S,

matching expectations. Market pricing provides a more hawkish view than several points of reference that the RBA

disclosed, with cash rate expectations, as viewed via Tuesday’s IB strip settlement levels, ratcheting higher post-

decision, leaving terminal cash rate expectations above 3.50%. For reference, the Bank revealed that its new round

of economic forecasts is based on a year-end cash rate of 1.50-1.75%, with Governor Lowe pointing to a more

“normal” level of interest rates being ~2.50%. Market pricing still looks very aggressive in this context, but as we

have noted previously, this doesn’t mean that there is an obvious trigger point to trigger receive side interest.

Fig. 1: The Evolution Of Cash Rate Expectations in ‘22

Lowe stressed that the Bank is not on a pre-set path,

while noting “further increases in interest rates will be

necessary over the months ahead.” He pointed to a

sense of data dependence, although inflation dynamics

clearly provide a front-loaded possibility when it comes

to tightening. The Bank’s projections included a 2ppt

mark up in underlying inflation expectations for

calendar ’22 (to ~4.75%), with expectations for

headline and underlying inflation to only move down to

the upper boundary of the Bank’s target range by mid

’24. This was a major hawkish twist and came

alongside the concession that the medium-term nature

of the RBA’s inflation goal “does not require an

immediate return of the inflation rate to target because

our monetary policy framework intentionally allows for flexibility and some variability… But we do need to ensure

that the inflation rate tracks back to the target range of 2-3 % over time.” The Bank also marked its unemployment

track lower, while it lowered GDP growth expectations on the Chinese COVID situation and Ukraine conflict.

Lowe suggested that the 25bp hike was a case of “business as usual,” although most of the sell-side have touched

on the potential for a 40bp hike, perhaps as soon as June, which would move the cash rate target back to the

traditional 25bp multiples and fully reverse the emergency cuts provided in March 2020. The RBA now has ample

time to provide intra-meeting messaging if it so chooses. Some sell-side names remain cognisant of the potential

for the level of household debt to cap the terminal rate in the high 1s or low 2s. Past RBA research has pointed to

most households being able to cope with 200bp of tightening and Governor Lowe’s rhetoric suggests that the RBA

will look to push past the lower end of the current terminal rate expectations, if given the chance.

1|Page

Business Address - MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DB

RBA 3 May 2022 Meeting Statement

At its meeting today, the Board decided to increase the cash rate target by 25 basis points to 35 basis points. It

also increased the interest rate on Exchange Settlement balances from zero per cent to 25 basis points.

The Board judged that now was the right time to begin withdrawing some of the extraordinary monetary support

that was put in place to help the Australian economy during the pandemic. The economy has proven to be resilient

and inflation has picked up more quickly, and to a higher level, than was expected. There is also evidence that

wages growth is picking up. Given this, and the very low level of interest rates, it is appropriate to start the process

of normalising monetary conditions.

The resilience of the Australian economy is particularly evident in the labour market, with the unemployment rate

declining over recent months to 4 per cent and labour force participation increasing to a record high. Both job

vacancies and job ads are also at high levels. The central forecast is for the unemployment rate to decline to

around 3½ per cent by early 2023 and remain around this level thereafter. This would be the lowest rate of

unemployment in almost 50 years.

The outlook for economic growth in Australia also remains positive, although there are ongoing uncertainties about

the global economy arising from: the ongoing disruptions from COVID-19, especially in China; the war in Ukraine;

and declining consumer purchasing power from higher inflation. The central forecast is for Australian GDP to grow

by 4¼ per cent over 2022 and 2 per cent over 2023. Household and business balance sheets are generally in good

shape, an upswing in business investment is underway and there is a large pipeline of construction work to be

completed. Macroeconomic policy settings remain supportive of growth and national income is being boosted by

higher commodity prices.

Inflation has picked up significantly and by more than expected, although it remains lower than in most other

advanced economies. Over the year to the March quarter, headline inflation was 5.1 per cent and in underlying

terms inflation was 3.7 per cent. This rise in inflation largely reflects global factors. But domestic capacity

constraints are increasingly playing a role and inflation pressures have broadened, with firms more prepared to

pass through cost increases to consumer prices. A further rise in inflation is expected in the near term, but as

supply-side disruptions are resolved, inflation is expected to decline back towards the target range of 2 to 3 per

cent. The central forecast for 2022 is for headline inflation of around 6 per cent and underlying inflation of around

4¾ per cent; by mid 2024, headline and underlying inflation are forecast to have moderated to around 3 per cent.

These forecasts are based on an assumption of further increases in interest rates.

The Bank's business liaison suggests that wages growth has been picking up. In a tight labour market, an

increasing number of firms are paying higher wages to attract and retain staff, especially in an environment where

the cost of living is rising. While aggregate wages growth was subdued during 2021 and no higher than it was prior

to the pandemic, the more timely evidence from liaison and business surveys is that larger wage increases are now

occurring in many private-sector firms.

Given both the progress towards full employment and the evidence on prices and wages, some withdrawal of the

extraordinary monetary support provided through the pandemic is appropriate. Consistent with this, the Board does

not plan to reinvest the proceeds of maturing government bonds and expects the Bank's balance sheet to decline

significantly over the next couple of years as the Term Funding Facility comes to an end. The Board is not currently

planning to sell the government bonds that the Bank purchased during the pandemic.

The Board is committed to doing what is necessary to ensure that inflation in Australia returns to target over time.

This will require a further lift in interest rates over the period ahead. The Board will continue to closely monitor the

incoming information and evolving balance of risks as it determines the timing and extent of future interest rate

increases.

A media and markets briefing, including a question and answer session, will be held at 4pm AEST today with the

audio broadcast live on www.rba.gov.au.

2|Page

Business Address - MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBRBA Governor Lowe’s Post-Meeting Address

Thank you for joining us this afternoon. I would like to use this opportunity to explain the Reserve Bank Board's

decision today and to answer your questions.

Today, the Board decided to increase the cash rate target by 25 basis points to 35 basis points and to increase the

rate paid on Exchange Settlement balances from 0 per cent to 25 basis points. It also decided to not reinvest the

proceeds of the Bank's government bond holdings as they mature.

These decisions reflect a judgement by the Board that it is now time to begin withdrawing some of the extraordinary

monetary support that was put in place to help the Australian economy during the pandemic. Two considerations

are particularly relevant here. The first is that the economy has been very resilient, unemployment is low and

economic growth is expected to be strong this year. The second is that inflation has picked up more quickly, and to

a higher level, than was expected and there is evidence that labour costs are increasing more quickly. In these

circumstances, the Board judged that it was appropriate to start the process of normalising monetary conditions.

I acknowledge that this increase in interest rates comes earlier than the guidance the Bank was providing during

the dark days of the pandemic. During that period, especially in 2020, the national health situation was precarious

and the economic outlook was dire and clouded by great uncertainty. The Board wanted to do everything it could to

help the country get through that difficult period. In those unprecedented times, we judged that the economic

damage from the pandemic was likely to require that interest rates remain at very low levels for years.

As things have turned out, the economy has been much more resilient than was expected, which is clearly a

welcome development. The combination of fiscal and monetary support has worked and the development of

vaccines in record time has allowed our society to return to more normal functioning earlier than was thought

possible. Australians have also proven to be resilient and have adapted to the changed circumstances. As a result

of these developments, unemployment has come down quickly. The unemployment rate now stands at 4 per cent.

It is expected to decline further to around 3½ per cent over the course of this year, which would be the lowest level

in nearly 50 years. Labour force participation has also risen to a record level and a higher share of working-age

Australians has jobs than ever before. The economy is expected to grow strongly this year, with our central forecast

being for GDP growth of a little above 4 per cent.

This resilience of the economy means that the record low interest rates are no longer needed.

The other major development has been on the inflation front. Over the year to the March quarter, CPI inflation was

5.1 per cent and in underlying terms inflation was 3.7 per cent. These numbers are lower than inflation rates in

most other advanced economies, but they are higher than we have experienced for many years and higher than we

were expecting.

The main driver of the higher inflation has been global developments, with a series of major global supply shocks

pushing prices up. Over the past two years, COVID-19 has interrupted supply chains and continues to do so, with

the recent lockdowns in some Chinese cities again disrupting production and transport. On top of this, Russia's

invasion of Ukraine has resulted in sharp increases in the prices of oil and gas, base metals and many agricultural

commodities. These shocks to global prices inevitably flow through to higher inflation in Australia.

But the higher inflation outcomes have a domestic component as well. There are a number of areas where strong

demand is putting pressure on available capacity, with many firms reporting difficulty in hiring workers with the right

skills. This pressure on capacity is reflected in the broadening of the areas in which prices are rising more quickly

than they have for some time. Firms in a range of industries are now indicating that they are prepared to pass cost

increases through to consumer prices.

Looking forward, we expect a further increase in the inflation rate as the effects of global developments wash

through the year-ended figures. We then expect inflation to start moderating as some of the supply disruptions are

resolved and/or as prices settle at a higher level – for inflation to stay high, prices need to keep increasing at a fast

rate, not only settle at a high level. An offsetting influence over time will be stronger growth in labour costs as the

labour market tightens. Our central forecast – which is based on an assumption of further interest rate increases –

3|Page

Business Address - MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBis that underlying inflation will decline to the top of the target band in 2024. If interest rates were to remain

unchanged, inflation would be higher than this.

Over recent years, the Board has placed considerable emphasis on trends in growth in labour costs when making

its decisions. This is because, over the medium term, there is a strong link between the inflation rate and the rate of

growth of labour costs. Given that we operate a flexible medium-term inflation target, we are generally prepared to

look through year-to-year variability in the inflation rate caused by supply-side shocks or exchange rate

movements. This is because if these shocks do not flow through to a persistent change in growth of labour costs,

inflation should return to a lower rate once the effect of the shock passes. But if supply-side shocks do lead to a

persistent shift in labour cost growth, inflation will not return to where it was before.

This focus on trends in labour costs was evident in the Board's communication after the previous meeting when we

stated that over coming months we would be assessing important additional evidence on both inflation and the

evolution of labour costs.

The evidence that we have received since then on inflation is clear. It was high. And higher than expected. On

labour costs, while the various data on labour costs for the March quarter compiled by the ABS are yet to be

released, other evidence received over the past month through our business liaison and various business surveys

has indicated that there is now stronger upward pressure on labour costs and that this is likely to continue. We

expect to see this in the ABS data in the period ahead. In a tight labour market, some firms are paying higher

wages to attract and retain staff. This is especially so given that inflation is high and workers are experiencing cost

of living pressures. There is still considerable inertia in the wages system from multi-year enterprise agreements

and current public sector wages policies, but the direction of change is now clear.

Given this evidence on inflation and wages and the very low level of interest rates, the Board decided that now was

the right time to start the process of normalising interest rates.

We also decided that we would not reinvest the proceeds of maturing government bonds. This means that our bond

holdings and balance sheet will decline as bonds mature. Our balance sheet will also decline substantially in 2023

and 2024 as banks repay the funding made available under the Term Funding Facility. This contraction of our

balance sheet will contribute to some tightening of financial conditions in Australia and so assist with the return of

inflation to target. The Board currently has no plans to sell the government bonds it purchased during the pandemic

and intends to allow the portfolio to run down in a predictable way as bonds mature. This decision to proceed with

quantitative tightening does not rule out a return to quantitative easing sometime in the future, should

circumstances require that.

Given the outlook for the economy and inflation, further normalisation of interest rates will be required. In making its

decisions, the Board will continue to be guided by the evidence on both inflation and the labour market. We will also

continue to be flexible and responsive to changing circumstances. We will do what is necessary to ensure that

inflation outcomes are consistent with the medium-term inflation target. This does not require an immediate return

of the inflation rate to target because our monetary policy framework intentionally allows for flexibility and some

variability in inflation from year to year. But we do need to ensure that the inflation rate tracks back to the target

range of 2 to 3 per cent over time. This would be harder to achieve if the inflation psychology in Australia were to

shift in a durable way due to the recent higher inflation outcomes. The decision to move today, rather than wait,

should help on this front.

In making our decisions over coming months, we need to navigate through some considerable uncertainties.

Globally, it remains uncertain how the supply-side problems will be resolved and developments in Ukraine are

unpredictable. Another source of uncertainty is how household spending in advanced economies responds to the

decline in real wages, as wages growth has not kept pace with the higher inflation. Also, we have no contemporary

experience to guide us with how labour costs and prices in Australia will behave at an unemployment rate below 4

per cent. It is also relevant that households have much more debt than previously, and many households have

never experienced rising interest rates. So this is another aspect that we will be watching carefully.

Notwithstanding these uncertainties, I expect that further increases in interest rates will be necessary over the

months ahead. The Board is not on a pre-set path and will be guided by the evidence and data as it takes the

necessary steps to achieve the medium-term inflation target and support full employment in Australia.

4|Page

Business Address - MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBMNI STATE OF PLAY: RBA Could Take Rates To 2.5%,

Says Lowe

By Lachlan Colquhoun

SYDNEY (MNI) - Reserve Bank of Australia Governor Philip Lowe said on Tuesday that official interest rates could

reach between 1% and 1.5% by the end of this year and as high as 2.5% as the bank enters a tightening cycle.

Responding to questions after the RBA increased the Official Cash Rate to 0.35% from a record low 0.10%, its first

hike in over a decade and towards the upper end of expectations, Lowe said that it was “not unreasonable to

expect” that the normalisation of monetary policy would see the OCR at 2.5%, although he declined to say how

long it might take to get there.

“It will depend how long these issues (around inflation) resolve,” said Lowe. “There are reasons to believe that

inflation will moderate, but the labour market is also tightening.”

Lowe said that that “we all knew interest rates couldn’t stay at these rates forever” and that it was now time to

normalise policy and move away from emergency settings adopted during the pandemic.

“This is good news,” he said.

The RBA also announced that it will not reinvest the proceeds from maturing government bonds acquired during its

recent bond buying program, with the expectation that the Bank’s balance sheet will decline significantly in coming

years given that the withdrawal of the recent “extraordinary monetary support” is now appropriate.

The rate on Exchange Settlement balances, which are used to settle interbank transactions, will also rise by 25

basis points in line with the increase in the OCR, from the previous zero. Maintaining the 10-basis-point spread

between the two rates was deemed to appropriate due to the continued high level of ES balances, in line with

discussions mentioned in previous RBA minutes, Lowe said.

NOT BEHIND THE CURVE

Lowe said he did not accept that the RBA had been “behind the curve” on interest rates and that the Bank had

wanted to see ample evidence before changing policy. He also declined to specify a level for neutral interest rates.

Lowe however said he had been “shocked” by the latest inflation data last week, which showed CPI inflation at

5.1% and underlying inflation, the bank’s preferred measure, at 3.7%, the first time it had been in the RBA’s 2% to

3% target range since December 2010.

The RBA’s move saw the AUD add USD0.01 to AUD0.71 to the dollar, and came as Australia is in the midst of a

hard fought election campaign with polls set for May 21. (See MNI STATE OF PLAY: RBA Ponders Election-Eve

Rate Rise.)

In response to questions, Lowe emphasised the independence of the central bank, with the RBA now expecting

underlying inflation to reach 4.75% this year. This was based on an assumption of further interest rate rises, without

which inflation would be higher.

FORECASTS UPDATED ON FRIDAY

The RBA’s most recent Monetary Policy Statement, released in February, forecast underlying inflation at 3.25% in

June, followed by a fall back to 2.75% by the end of the year. The next statement, with updated forecasts, is due on

Friday.

The RBA has insisted that wages growth would be key to any policy change, and Lowe said that this metric had

risen above the 2% range and was “moving into the 3% range” based on evidence from the Bank’s liaison program.

5|Page

Business Address - MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBSell-Side Analyst Views

ANZ: Lowe is focused on the need to “normalise” interest rate settings. He sees this as being a cash rate of around

2.5%, which is broadly consistent with where we think the cash rate will get to by mid-2023. We still think the cash

rate will eventually need to lift to 3 point something, albeit not for some time. The RBA is not inclined to “deviate”

from moves of 25bp in coming months, unless “there is a very strong argument to do so.” In the Q&A of his post-

meeting press conference, RBA Governor Lowe was asked where interest rates might eventually get to. He noted

that he has highlighted in the past that it is “not unreasonable to expect” interest rates to eventually get back to

2.5%. He gave no “prediction” on how quickly this might occur.

• In terms of the path of normalisation, Lowe made it clear in his prepared remarks that: The Board is not on

a pre-set path and will be guided by the evidence and data as it takes the necessary steps to achieve the

medium-term inflation target and support full employment in Australia.

• One clue to the possible path is the interstate track assumed in the forecasts. Lowe noted that this is a

cash rate of 1½%-1¾% by the end of 2022 and 2½% for the end of 2023. What will ultimately determine

where interest rates get to is how the “considerable uncertainties” are resolved.

• Lowe was asked whether a move of 15 or 40bpover even 50bp was considered. He responded by saying

the Board wanted to “get back to normal and business as usual.” This suggests moves of 25bp increments

will be the starting point for each decision, though we expect at some point we will get an adjustment that

‘rounds’ the cash rate to the nearest 0.25bp increment.

Barclays: The tone of the statement clearly suggests to us that more hikes are likely to follow. Since the RBA has

started increasing the cash rate much later than its peers, we do not expect the bank to pause between hikes until

it reaches a certain threshold. We expect the bank to increase the cash rate relatively aggressively until the OCR

reaches the pre-COVID level of 1.50%. We expect this to be reached by Q3, with a 25bp increase in June, followed

by 90bp of hikes in Q3.

• After reaching 1.50%, however, we think the RBA will wait to assess the macroeconomic data, given the

large uncertainty around imported inflation as well as the impact of aggressive hiking for the first time since

since 2010. We now see the cash rate reaching 1.75% by end of 2022 (compared with our previous

forecast of 1.50%. We expect this cycle to end at 2.0%, by Q1 23, despite Governor Lowe's comments that

the Board does not see OCR rising to 2.50% over time as being unreasonable.

• The timing decision was likely a result of higher inflation and some evidence of rising wage pressures, as

growth had already been strong through last year.

• We think future decisions on the cash rate will also be dependent on inflation. Governor Lowe said that the

Board needs to "ensure that the inflation rate tracks back to the target range of 2 to 3 per cent over time".

• While the bank's inflation forecasts are very high, we note that the RBA sees a large part of this as

reflecting the current global inflationary outlook. On domestic inflation, the bank seems is much less

aggressive than banks such as the RBNZ, although it acknowledged that domestic capacity constraints are

"increasingly playing a role" and "firms are more prepared to pass the cost increases" to consumers.

Further, the RBA says that as supply disruptions are resolved, inflation should come back to target range of

2-3%, though the bank likely sees it happening much later in its forecast trajectory.

• We think the bank will have room to pause between hikes across Q422-Q123. However, we do not think

that the next few data releases, on wages, GDP or inflation are likely to alter the course of hikes over the

next few months at least, as the bank already expects strong growth, high inflation and gradually increasing

wage growth. Therefore, we see continuous hikes till Q322, with the cash rate reaching 1.50% by end of

Q3. We also see no need for a faster pace of hikes as the Governor mentioned in the press conference

that the Board does not think that it is "playing catch up" on rates.

CBA: The RBA has made a massive upward revision to their inflation forecast profile, which indicates they are

likely to take monetary policy to a contractionary setting. We have revised our profile for the cash rate and now

expect further 25 basis point rate hikes in June, July, August and November 2022 that would see the cash rate

target end the year at 1.35%. We then expect a further 25 basis point rate hike in February 2023 that would see the

cash rate target at 1.60%. From there we have the key policy rate on hold over 2023.

6|Page

Business Address - MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DB• Reading between the lines, the RBA has simply been caught off guard by the strength of the Q1 22 CPI

data (note, in his post‑statement conference the Governor described the Q1 22 CPI data as ‘a shock’). As

such, the Board decided that it could no longer afford to wait to raise the cash rate. In the grand scheme of

things waiting one more month to raise the cash rate would not have changed the economic outlook. But

clearly the inflation data last week put the RBA in an uncomfortable place, which is why they delivered a

rate hike today.

• The RBA have massively upwardly revised their forecast profile for both headline and underlying inflation.

The RBA now expect underlying inflation of ‘around’ 4¾% in 2022. Their previous forecast from the

February Statement on Monetary Policy was underlying inflation of 2¾% in 2022. A 200bp increase in their

inflation profile over 2022 is a radical revision. Indeed it indicates the RBA has completely changed their

view on the outlook for inflation. The RBA appear like inflation fighters now, much like many of their other

central bank counterparts.

• We are disappointed in some aspects of the RBA’s communication today. Having stressed the importance

of the need to conclude that inflation is ‘sustainably within the target range’ before raising the cash rate for

the past few years, the word sustainable didn’t appear once in the Governor’s Statement today.

• Our estimate of the neutral cash rate remains at just 1.25%, so our updated forecast means that we now

expect the RBA to take policy restrictive, but not materially so. The RBA still wants the Australian economy

to remain strong and their aim is to see annual wages growth reset upwards to around ~3½% (well above

the pre‑pandemic norm of 2¼%). We believe they will achieve this outcome on the basis that the tightening

cycle is not overly aggressive.

Goldman Sachs: The rate increase was larger than widely expected and priced by financial markets, and was

framed around the withdrawal of ‘extraordinary’ pandemic-related monetary support and stronger-than-expected

inflation. The latter was characterised as ‘largely reflecting global factors’ although the RBA did emphasise very

recent stronger signals on private-sector wages growth from its business liaison program (in the absence of hard

data). The RBA also flagged a significant upgrade to forecast inflation was calibrated on ‘an assumption of further

increases in interest rates’ (to 1.5/1.75% by end-22 and 2.50% by end-23).

• Looking ahead, today’s hawkish shift in the RBA’s reaction function points to a faster pace of policy

normalization in 2022. We now expect the RBA to lift the policy rate to 2.6% by December 2022 and lean

towards the normalization being front-loaded via back-to-back 50bp hikes in June/July and a series of

monthly 25bp increases from August to December. We expect the RBA to maintain the policy rate at 2.60%

beyond 2022 - broadly in line with our estimate of 'neutral' (2.50%). While this represents a very rapid

policy tightening over the coming year, our recent analysis suggests the Australian economy will be able to

absorb materially higher interest rates in the near-term - although we see longer-term risks around the

residential housing market.

ING: Looking ahead, there are some hints that the RBA is now committed to a period of rising rates. The RBA's

expectation for both headline and core inflation is that even by the middle of 2024, inflation would still be at the very

top of the RBA's inflation rate target. That doesn't necessarily imply that rates will be on an upwards path until then,

given the lags involved in monetary policy, but it does suggest that rates will not be cut before this time.

• At first glance, it feels as if the RBA is now committed to a slow but steady ratcheting up of monetary policy

rather than a Fed-style front-loaded hiking cycle. But equally, given how misleading central bank guidance

has been in recent years, it feels too soon to be taking a firm view on the future path for rates.

J.P.Morgan: Today’s tightening saw the last guidance dominoes fall. The board had planned last month to wait for

both CPI and wage data before acting, with the latter not due until after this meeting. But in tracking “progress

toward full employment and evidence on prices and wages” since the last meeting, Governor Lowe declared in

today’s impromptu speech that the evidence on prices “is clear. It was high”. The bank is now seemingly placing

greater weight on its liaison feedback suggesting a sharp uplift is imminent, such that the independent value of the

official labour cost/wage data has been further dialed down. The statement removes reference to wage growth

being below target-consistent levels, and there is also now more acknowledgement of a potential feedback loop

from prices back into wages. The previously required lift-off thresholds on official wage data (3%, etc.) aren’t

viewed as necessary any more: “the direction of change is now clear”.

7|Page

Business Address - MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DB• While seemingly a second-order detail, staying at unconventional bp increments on the cash rate is

significant in adding yet another dimension of uncertainty in an environment where there is already quite a

bit to start with. In Q&A, Lowe argued that a 25bp hike as seen today is a return to business as usual, but

policy settings work in levels not changes, and we can only presume that landing at a half-way house this

month was intended to give optionality for a 40bp follow-up move in June, and so a return to the normal

0.25%-pt step-ladder (0.75%).

• Lowe’s speech flagged “further increases in interest rates will be necessary over the months ahead. The

board is not on a pre-set path and will be guided by the evidence and data” to support the inflation target

and full employment. This is likely to exacerbate the pull-forward of market economists’ calls for 2022.

• While the “timing and extent” of tightening is supposed to be data-dependent, the board’s guidance and

framework on this has been backsliding, so a preference for getting closer to neutral seems dominant over

the dataflow for now. We change our forecast 25bp hike in June to 40bp, which would return the cash rate

to its pre-pandemic setting of 0.75%. We also add another 25bp hike forward to July, so the cash rate

would be 1.25% in August, and 1.5% at November (previously 1%). At some point the medium-term

inflation drivers will matter again, as will the level of the cash rate vs neutral, and so we maintain our

forecast for the terminal rate at 2.25%. Governor Lowe reiterated today his view that a real cash rate of

zero or positive is more “normal”, implying a rough destination of 2.5% for the cash rate, though did say this

was hedged by uncertainty on productivity.

• In our view the neutral rate is 1.75%, with a bit of an upside risk skew. The economy entered COVID at

0.75%; the COVID easing should therefore be undone very soon. The domestic data don’t suggest

unemployment is well below NAIRU as it is in other economies, but it should be moving a bit below NAIRU

over the coming year, which requires getting into restrictive territory. These details will presumably matter

more for where the cash rate settles in 2023/4.

NAB: With the RBA today slightly surprising by raising the cash rate target to 0.35% (NAB 0.25%), we have

correspondingly revised up our expectations for the cash rate profile. We continue to see further 25bp increases in

June, July, August and November taking the target to 1.35% by year-end (previously 1.25%).

• The RBA’s move reflected significant revisions to the Bank’s inflation forecasts – on the back of Q1 CPI –

and our own expectations for inflation also continue to evolve. The Bank also lowered its forecast

unemployment rate to 3.5% for 2023, closer to NAB’s outlook.

• The RBA drew on liaison evidence of a pick-up in wage growth, ahead of the Q1 WPI release this month.

We see a gradual pickup in wages, supporting steady rate rises in 2022. We then see three further cash

rate increases in 2023 and two increases in 2024, taking the target to 2.60%.

RBC: The RBA hiked by 25bp following its May meeting taking the cash rate to 0.35% with the rate on ES balances

lifting to 0.25% from 0%. While we (and the market) were expecting a +15bp move today quickly followed by

another 25bp in June, the RBA opted to move a little faster as it begins policy normalization. We commend this

move and see it as prudent. It sends a stronger message at the start of policy normalization and lift-off. In the press

conference this afternoon in answer to our question, the Governor noted that the decision to move by 25bp rather

than +15bp or +40bp was “not a compromise” and was mostly the “standard” quantum outside of shocks and

signalled a return to “business as usual”. He hinted at a preference for this size move again in the months ahead.

The 25bp decision did not appear to reflect any greater emphasis on the rate on ES balances.

• In line with the global trend and step up in the pace of tightening with merit in moving to a more neutral

stance sooner rather than later, we expect multiple follow-up hikes in the months ahead as alluded to in

this week’s Snapshot. We bring forward some tightening. Even at the current level, settings remain

extraordinarily accommodative and clearly inconsistent with the tightening labour market, forward indicators

of strength and further likely lift in inflation.

• Accordingly, we expect a series of 25bp hikes at every meeting until Nov, effectively a further 150bp of

tightening. This would put the cash rate at 1.85% by the end of this year. Near term, there is a risk of 40bp

in June but our sense from the Governor’s press conference was a preference for 25bp moves. Against the

backdrop of a step up and front loading of hikes by its dollar bloc cousins (including the Fed tomorrow

8|Page

Business Address - MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBnight), a desire to move to 2.5%, and inflation forecasts that assume that, our revised profile brings forward

our 75bp in 2023/early 2024 and lifts terminal slightly to 1.85% (from 1.75%).

Societe Generale: At the media and markets briefing, Governor Lowe gave more detailed information about the

future path of policy rates. He first said that it would not be unreasonable for policy rates to return to 2.50%,

suggesting that the RBA's estimate of the neutral policy rate is around 2.50%. He added that the RBA's

macroeconomic forecasts assume a cash rate target at 1.50-1.75% by the end of this year, which implicitly serves

as the equivalent of the Fed's dot plot in our opinion. He said that the RBA opted for a 25bp hike instead of a 40bp

hike to give a signal that everything is getting back to normal, and that the size of the rate hike in the future had not

been decided yet.

• In turn, we now provide new forecasts on the future path of RBA rate hikes. We think that the RBA will

raise the policy rates to the neutral level of 2.50% within a year, i.e. in 2Q23. We assume that the neutral

rate of 2.50% will also be the RBA's terminal rate for the current rate-hike cycle. We also expect that the

RBA will implement a 25bp hike every month until 3Q of this year (i.e. the policy rate will reach 1.35% in

September), thus restoring the central bank's credibility as a fighter of inflation and also to keep up with the

anticipated ‘big steps' to be implemented by the Fed. Our RBA policy rate forecasts for the next 12 months

are as follows: 0.60% in 2Q22 (end-of-quarter), 1.35% in 3Q22, 1.60% in 4Q22, 2.00% in 1Q23, and 2.50%

in 2Q23.

TD Securities: The Bank's commentary and some hefty upward revisions to its inflation forecasts lent a hawkish

tone, which cemented further cash rate increases. The Bank's announcement on not reinvesting maturing bond

lines was not a surprise, and neither was the Bank retaining the 10bps corridor between the cash rate target and

the Exchange Settlement deposit rate floor. The Bank expects the cash rate at the end of this year to be around

1.50-1.75%. We now expect the RBA to deliver a 40bps hike at the June meeting followed by 25bps hikes in July,

Aug, Nov and Dec. This would take the target cash rate to 1.75% by year-end. The risks are the RBA could deliver

50bps hikes at the Aug and/or Nov meetings implying a year-end cash rate of 2% or higher.

Westpac: The task of reducing underlying inflation over that 18 month period from 4.75% to 3.0% overwhelms the

previously expected task of holding it steady over the period at 2.75%.

• We do not know where the Board expects underlying inflation at end 2023 but it seems entirely reasonable

that the detailed forecasts to be released on May 6 will indicate that underlying inflation by end 2023 will

still be above the Board’s target range of 2-3% (probably 3.25%). This observation explains why the Board

surprised today by lifting the cash rate a little further than the 15 basis points expected by the market and

many analysts including Westpac. It also signals that the Board should be prepared to “front load” its

tightening cycle to convince households and business that it is committed to achieving that formidable goal

of returning inflation back to the target band (admittedly to the outer limit) by mid-2024.

• In the press conference the Governor revealed the interest rate path that was used to arrive at the

forecasts. He noted that the cash rate profile was 1.5%-1.75% by end 2022 and 2.5% by end 2023, most

likely the base terminal rate. He also noted that the choice of 25 basis points was a return to “business as

usual” signalling that increments of 25 basis points might be considered the base case.

• We are not convinced that the next move will be 25 basis points. Consistent with our previous forecast that

the Board would want to reach a cash rate of 50 basis points by June we expected 15 basis points in May

to be followed by 25 basis points in June. But that was before we saw the formidable challenge that the

Board believes it has to return inflation to within the band over the next 2 years. A larger increase in the

cash rate than 25 basis points is likely to be seen by the Board as necessary to convince agents that it is

serious about the challenge and to accelerate the unwinding of the emergency measures that saw 65 basis

points of rate cuts in 2020. We have chosen 40 basis points rather than 50 basis points purely because we

expect that “business as usual” is increments of 25 basis points on a base of multiples of 25 basis points

(in line with the practices of most other central banks). It is better to slightly trim the largest expected

increase in the cycle rather than reduce any subsequent moves to that 15 basis points that was rejected at

today’s meeting.

9|Page

Business Address - MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DB• We continue to disagree with the Board’s base case and the market’s expectation that the tightening cycle

will extend into the second half of 2023.

10 | P a g e

Business Address - MNI Market News, 5th Floor, 69 Leadenhall Street, London, EC3M 2DBYou can also read