Market Navigator from the Investment Advisory Group Truist Advisory Services, Inc.

←

→

Page content transcription

If your browser does not render page correctly, please read the page content below

Market Navigator

from the Investment Advisory Group

Truist Advisory Services, Inc.

November 2, 2022

Securities and insurance products and services –

• Are not FDIC or any other government agency insured

• Are not bank guaranteed

• May lose value

Monthly letter

The Jekyll and Hyde market continues. After the worst Our view is supported by the recent inversion of the 3-

month since the pandemic in September, stocks roared month/10-year U.S. Treasury yield curve, which followed

back in October with the S&P 500 gaining 8%. The Dow the 2-/10-year yield curve earlier this year, the sharp

Jones Industrial Average jumped 14%, its best month since slowdown in the housing market, and the negative trend in

1976. At the end of October, we used the sharp bounce the Conference Board’s Index of Leading Economic

to further downgrade equities to less attractive, move Indicators. Collectively, these indicators suggest

to a value tilt, upgrade fixed income and extend recession risks remain elevated.

duration given much more attractive yields.

Risk/reward more favorable in bonds

Keith Lerner, CFA, CMT In last month’s letter, as stocks closed at the lows for the

Co-Chief Investment Officer year, we discussed that markets had become the most On a fundamental basis, although stocks have become

Chief Market Strategist stretched to the downside, or oversold, since mid-June, cheaper on an absolute basis this year, they have

Senior Managing Director and expected a reprieve. While we saw a rebound play out actually become more expensive relative to bonds

over the past month, our core view for choppy markets, up given the sharp rise in interest rates. We see the

in quality and defensive positioning over the next six to 12 risk/reward for fixed income relative to equities as much

” At the end of October, we

used the sharp bounce to

months, remains intact. improved given these higher yields alongside a wide range

of potential market outcomes and our expectation for

further downgrade equities Part of the recent rally for stocks has been based on the slower economic growth in 2023. Indeed, the weight of the

to less attractive and move possibility that the Federal Reserve (Fed) pivots to a less evidence in our work suggests recession risks over the

towards a value tilt. We also aggressive monetary stance. While we have anticipated next 12 months remain elevated as does downside risk to

upgraded our fixed income such a discussion to energize a short-term rally, even corporate profits.

view and extended duration if the Fed does pivot or inflation softens, it wouldn’t be

given much more attractive

a cure-all over the intermediate term. One only needs to Even if corporate earnings for the next year stay close to

”

yields.

look back to 2000 or 2008 to see that a shift in Fed policy current consensus expectations, instead of lower as we

alone is not always enough to stop an economy on a anticipate, consistent with a slower economy, applying

downward trajectory or start a new bull market. an optimistic market valuation assumption (17x to 18x

for the S&P 500 up from the current 16.7x) suggests the

Indeed, monetary policy works with a lag. And with the

upside in equities from current levels is limited to

most aggressive U.S. and global central bank monetary

tightening cycle in 40 years underway, this is likely to 5% to 8%, while high quality bonds are yielding

weigh on the economy into 2023. around 4%, with arguably a lot less downside risk.

Continued on the next pageMonthly letter continued

Although the current rally could extend further given markets are in a Upgraded fixed income and extended duration

positive seasonal period and the fear of missing out may lead some

investors to chase prices higher into year end, this is not enough to offset Yields in the fixed income space are productive again given the sharp

our more cautious intermediate-term stance given rising recession risks upward move in interest rates, especially in the high-quality sectors. Year

and weakening fundamentals. to date, yields have risen for U.S. Treasuries across most of the curve

and are flirting with 15-year highs.

Upgraded value style

Moreover, during periods of economic stress, high quality fixed

Within our equity outlook, we upgraded our view on value relative to income, and specifically longer-duration U.S. government bonds,

growth to more attractive from neutral. Our sector strategy continues to tends to outperform shorter alternatives as demand for safe haven

favor market segments that have larger weights in the value style, such as

assets strengthens. Additionally, the recalibration in yields puts

industrials, energy, health care, and consumer staples. Conversely, the

intermediate and longer-duration bonds in a far better position to deliver

growth style remains heavily influenced by the technology and

more compelling income and portfolio ballast in the event of decelerating

communications services sectors, which make up more than 50% of the

economic activity.

index; relative earnings and price trends remain weak, and valuations are not

compelling for these sectors. Moreover, value’s relative price trends are

Quick note on the U.S. midterm elections

improving after more than a decade of underperformance.

The U.S. midterm elections are here, and this often creates many questions

Maintain less attractive view of international markets surrounding market implications. Our main mantra over the past decade is

what happens in Washington matters, but collectively factors outside of

While U.S. markets rallied strongly last month, emerging markets were down

Washington matter more. Indeed, where we are in the business cycle, as

by 3%. Relative earnings and price trends remain weak. In China, President

well as monetary policy, geopolitical issues, valuations, and other factors can

Xi Jinping officially secured his third five-year term during the Chinese

all be significant drivers of the markets. The election is unlikely to

Communist Party’s 20th National Congress. This also resulted in more

meaningfully change the near-term trajectory of the economy given the

concentrated leadership with Xi loyalists as well as a doubling down on

aforementioned extreme tightening cycle that is already in the pipeline nor

policies less market friendly and more unpredictable. International developed

change the near-term trajectory of corporate fundamentals. We will be

markets have fared better recently, but economic challenges and geopolitical

hosting a special post-election call on November 10 to discuss potential

concerns remain.

policy and market implications from the results. Please reach out to

your Truist advisor to learn more.

Keith Lerner, CFA, CMT

Co-Chief Investment Officer

Chief Market Strategist

Senior Managing DirectorAsset class view, forecasts & valuation*

On October 28, we downgraded our view of equity to Less Attractive from Neutral and upgraded our view of fixed income to More Attractive from

Neutral. Additionally, within equity, we upgraded our view of value relative to growth to More Attractive from Neutral. With this publication, we are

upgrading our forecasted 2022 GDP growth range to 0.8% - 1.7% from 0.4% to 1.6%.

Tactical outlook (3-12 months) Long-term capital market assumptions (10 yr)+

Less More Expected Expected

Asset classes Attractive Attractive Equity Return Risk

Equity Global equity 5.75% 16.3%

Fixed income U.S. large cap 6.00% 15.2%

Cash U.S. small cap 7.50% 19.0%

Less More International developed markets 5.50% 17.5%

Global equity Attractive Attractive Emerging markets (EM) 5.50% 24.0%

U.S. large cap Expected Expected

U.S. mid cap Fixed income Return Risk

U.S. small cap Intermediate-term municipals 1.25% 3.5%

International developed markets U.S. core taxable bonds 1.50% 3.4%

Emerging markets (EM) U.S. government bonds 1.00% 3.9%

Value style relative to growth U.S. IG corporate bonds 2.25% 6.0%

Less More

U.S. HY corporate bonds 3.75% 9.0%

U.S. fixed income Attractive Attractive

U.S. government Key IAG 2022 forecasts

U.S. mortgage-backed securities Global GDP forecast* 3.2%

U.S. investment grade corporate (IG) U.S. GDP 0.8% - 1.7%

U.S. high yield corporates (HY) Year-end Fed Funds rate range 4.25% - 4.50%

Leveraged loans 10-yr U.S. Treasury yield 3.50% - 4.50%

Duration S&P 500 12-month forward EPS** $232.35

*IMF forecast **FactSet consensus estimates

Global equity market valuation S&P 500 MSCI ACWI MSCI EAFE MSCI EM

Current price-to-earnings (P/E) ratio 16.7x 14.1x 11.6x 9.9x

10-year average P/E ratio 17.1x 15.6x 14.3x 11.8x

10-year high P/E ratio 23.4x 20.8x 18.2x 17.0x

For domestic use only

10-year low P/E ratio 11.8x 11.4x 10.3x 8.9x

Past performance does not guarantee future results. Keep in mind that investing involves risk. The value of your investment will fluctuate over time, and you may gain or lose money.

*In this document, we express our high-level investment strategy views without portfolio context constraints. We aim to represent relative opportunities within each broader asset class. This allows us to signal what we are watching

and where things are changing at the margin within positions that may differ from our asset allocation guidance and Strategy Portfolios. Long-term expected risk, return and correlation statistics are derived from the Portfolio & Market Strategy

team’s capital market assumptions process and are not guaranteed. Secular trends, such as demographics, global debt, inflation, etc. are initially assessed to determine the impact on global markets over the next decade. With an understanding of

the current stage of the business cycle, a combination of quantitative and fundamental techniques is used to further analyze factors that include, but are not limited to: (1) the outlook for asset class return drivers; (2) the probability of sustained

returns; (3) absolute and relative valuation measures; (4) the impact of economic drivers on asset class assumptions and (5) changes in investor sentiment and liquidity. +Capital market assumptions are reviewed and/or modified at least once a

year and are currently as of 2020.

Investment and insurance products – Are not FDIC or any other government agency insured | are not bank guaranteed

| may lose valueSector Strategy

Our current sector strategy has a mix of defensive and cyclical exposure. We maintain our long-standing overweight to the energy sector and our

quantitative and qualitative work is favorable on industrials. Additionally, we are overweight the more defensive consumer staples and health care

sectors, which should hold better in a choppy macro environment and where technical trends remain strong.

Last Updated = 11/2/2022

Tactical outlook

S&P 500

(3-12M)

Sector sector T F V Comments

Under- Over-

weight weight weight

Energy 5.4% ● + + - Relative price trends for the sector have been stronger, and technical trends are positive overall. A supportive

demand/supply backdrop and positive fundamentals should continue to support the sector.

Industrials 8.2% ● +

The sector has improved in our quantitative work as relative price trends have been strong and fundamentals are

attractive.

Health Care 15.3% ● + - - Technical trends are strong, and we expect the sector to hold up well in a choppier market environment given its

defensive characteristics.

Consumer Staples 6.9% ● + - Relative price trends and technicals have improved, and the sector is supported by its defensive characteristics amid

heightened geopolitical and global growth risks.

Utilities 3.0% ● Technical trends have weakened recently, and fundamentals and valuations are mixed, warranting a neutral view.

Financials 11.4% ●

Relative price and earnings trends have improved, but a flattening yield curve and risks to the economy keep us

neutral.

Consumer Discretionary 11.2% ● + Despite strong fundamentals, relative price trends have weakened, and mixed valuations keep us neutral.

Materials 2.6% ● - + Technical trends have been more mixed recently. While valuations are attractive, fundamentals are more challenged.

Information Technology 25.9% ● -

Relative price trends have been weaker recently. While valuations have improved, they are not cheap. Policy

continues to be a risk.

Real Estate* 2.6% ● - + Weak technical trends, mixed fundamentals, and a challenging macro backdrop warrant an underweight position.

Communication Services 7.5% ● - - + Although valuations for the sector are attractive, relative performance has been weak due to underperformance from

some of the larger names in the sector.

For domestic use only. All information supplied or obtained from this page is for informational purposes only and should not be considered investment advice or guidance, an offer of or a solicitation of an offer to buy or sell a security, or

a recommendation or endorsement by TAS of any security or investment strategy. The information and material presented in this commentary are for general information only and do not specifically address individual investment

objectives, financial situations or the particular needs of any specific person who may receive this commentary and are subject to change without notice. Truist makes no guarantees that information supplied is accurate, complete, or

timely, and does not provide any warranties regarding results obtained from its use. *Real Estate/REITs – Our asset class views can differ at times from our sector strategy as the latter has a much heavier emphasis on price

momentum, whereas fundamentals play a greater role in our asset class views.

T = Technical. This factor has the greatest focus in our overall methodology with an emphasis on relative price trends

F = Fundamentals. Includes earnings and sales trends, with an emphasis on recent changes to estimates

V = Valuation. Inputs include current/historical and absolute/relative to the overall market

+ Top Tier, -Bottom Tier, Middle Tier; Data Source: Truist IAG, FactSet.W E E K LY M A R K E T

Performance summary

M Oas

N I Tof

O ROctober 31, 2022

Index % Total Return MTD QTD YTD 1 Yr Rates (%) 10/31/22 6/30/22 3/31/22 12/31/21 9/30/21

MSCI ACWI (net) 6.03 6.03 -21.14 -19.96 Fed Funds Target 3.25 1.75 0.50 0.25 0.25

S&P 500 8.10 8.10 -17.70 -14.61 Libor, 3-Month 4.46 2.28 0.96 0.20 0.13

MSCI EAFE (net) 5.38 5.38 -23.17 -23.00 T-Bill, 3-Month 3.99 1.64 0.51 0.05 0.03

MSCI Emerging Markets (net) -3.10 -3.10 -29.42 -31.03

2-Year Treasury 4.48 2.93 2.28 0.72 0.28

Dow Jones Industrials 14.07 14.07 -8.42 -6.74

Bloomberg Aggregate -1.30 -1.30 -15.72 -15.68 5-Year Treasury 4.24 3.00 2.42 1.26 0.99

ICE BofA US High Yield 2.85 2.85 -12.19 -11.45 10-Year Treasury 4.07 2.97 2.32 1.51 1.52

Bloomberg Municipal Bond Blend 1-15 30-Year Treasury 4.20 3.12 2.45 1.90 2.09

-0.38 -0.38 -9.56 -8.94

Year Bloomberg Aggregate (YTW) 5.01 3.72 2.92 1.75 1.56

ICE BofA Global Government xUS (USD Bloomberg Municipal Bond Blend 1-15

-0.02 -0.02 -27.03 -27.92 3.88 2.82 2.36 0.87 0.84

Unhedged) Year

ICE BofA Global Government xUS (USD ICE BofA US High Yield 9.05 8.93 6.02 4.31 4.08

0.59 0.59 -10.60 -10.30

Hedged)

JP Morgan EMBI Global Diversified 0.15 0.15 -23.83 -24.19 Currencies 10/31/22 6/30/22 3/31/22 12/31/21 9/30/21

Euro ($/€) 0.99 1.05 1.11 1.14 1.16

Yen (¥/$) 148.64 135.86 121.37 115.16 111.57

Pound ($/£) 1.15 1.21 1.32 1.35 1.35

Commodities 10/31/22 6/30/22 3/31/22 12/31/21 9/30/21

Crude Oil (WTI) 86.53 105.76 100.28 75.21 75.03

Gold 1,641 1,807 1,954 1,829 1,757

Volatility 10/31/22 6/30/22 3/31/22 12/31/21 9/30/21

CBOE VIX 25.88 28.71 20.56 17.22 23.14

U.S. style % total returns (S&P indexes) S&P 500 sector % total returns

Month YTD MTD YTD

Value Core Growth Value Core Growth

68.6

11.50 8.10 4.49 Large -6.97 -17.70 -27.29

25.0 13.9

9.0 12.0 9.7 7.8 9.0 2.1

0.1 0.2 2.0

11.53 10.52 9.43 Mid -7.94 -13.27 -18.45 -3.9 -4.6

-11.8 -9.7 -4.6

-26.1 -16.9

-29.7 -27.4

-39.0

14.41 12.37 10.04 Small -8.46 -13.66 -18.82 Comm Cons Disc Cons Energy Financials Health Industrials Info Tech Materials Real Estate Utilities

Services Staples Care

Data Source: Truist IAG, FactSet.

Disclosures – All information is as of title date unless otherwise noted. You cannot invest directly in an index. This document was prepared for clients of Truist Bank for informational purposes only. This material may not be suitable for all investors and may

not be redistributed in whole or part. Neither Truist Financial Corporation, nor any affiliates make any representation or warranties as to the accuracy or merit of this analysis for individual use. Information contained herein has been obtained from sources

believed to be reliable, but are not guaranteed. Comments and general statistics are based on information available at the time of writing and believed to be accurate; are for informational purposes only, are not intended as individual or specific advice, may

not represent the opinions of the entire firm and may not be relied upon for future investing. The views expressed may change at any time. The information provided in this report should not be considered a recommendation to purchase or sell any financial

instrument, product or service sponsored or provided by Truist Financial Corporation or its affiliates or agents. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment

decisions. Past returns are not indicative of future results. An investment cannot be made into an index. ©2020 Truist Financial Corporation. and Truist are service marks of Truist Financial Corporation. All rights reserved.

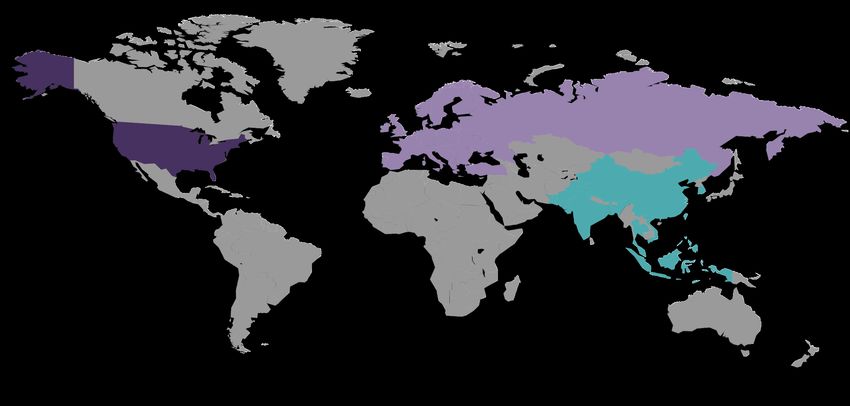

Securities and insurance products and services: Are not FDIC or any other government agency insured | are not bank guaranteed | may lose valueGlobal growth – Asian growth rates slowest since the global financial crisis

United States

Emerging Asia

2021 2022

2021 2022

5.7%

0.8% - 1.7% 5.9%

3.8%

U.S. recession risks have increased above a 50%

probability due to hotter near-term inflation and

correspondingly higher interest rates. Europe The Chinese Communist

Party’s 20th Congress

2021 2022 confirmed Xi Jinping’s

2022 GDP

unprecedented third-term

($104 trillion total) 5.3%

presidency. The zero-COVID

policy is expected to stay

much longer than initially

2.3%

19% 24% anticipated, curtailing Chinese

growth rates. The Common

Prosperity push is also

31% 26% expected to accelerate during

Xi’s third term.

The leadership crisis in Europe took another turn; the U.K.’s

prime minister resigned after an embarrassing U-turn in her plan for

unfunded fiscal stimulus. Italy elected a far-right coalition

government, and nationalist Sweden Democrats supported

U.S. Europe EM Asia Rest of the World Sweden’s new coalition government.

Data source: Truist IAG, 2022 global macro estimates from the International Monetary Fund, regional growth estimates from

Bloomberg. Europe includes developed countries and economies considered to be “emerging,” such as Russia, Turkey, and Ukraine.Inflation remains problematic globally, especially in Germany

U.S. inflation Germany inflation

10% 12%

10%

8%

8%

6% 6%

4% 4%

2%

2%

0%

0% -2%

2019 2020 2021 2022 2019 2020 2021 2022

U.K. inflation France inflation

12% 7%

10%

5%

8%

6% 3%

4%

1%

2%

0% -1%

2019 2020 2021 2022 2019 2020 2021 2022

Data source: Truist IAG, Bloomberg, data as of 10/26/2022Global interest rates spiked and have since pulled back on central bank

pivot hope

U.S. 10-year U.K. 10-year

5% +285 bps 5%

+315 bps

4% 4%

3% 3%

2% 2%

1% 1%

0% 0%

Feb-21 Jun-21 Oct-21 Feb-22 Jun-22 Oct-22 Feb-21 Jun-21 Oct-21 Feb-22 Jun-22 Oct-22

Italy 10-year Germany 10-year

6% 3%

+353 bps +262 bps

5%

2%

4%

3% 1%

2%

0%

1%

0% -1%

Feb-21 Jun-21 Oct-21 Feb-22 Jun-22 Oct-22 Feb-21 Jun-21 Oct-21 Feb-22 Jun-22 Oct-22

Data source: Truist IAG, Bloomberg, Data as of 10/28/2022Despite a possible global dovish pivot, the impact from the sharpest global

monetary tightening cycle in decades is still ahead for economies

The equity markets rallied as global monetary policy Number of central banks hiking minus easing

appeared to be shifting in a more dovish direction.

Australia and Canada raised rates less than

expected. And while the European Central Bank EM DM Net hiking

30

delivered another jumbo hike, its guidance suggested

a slightly less hawkish stance. Furthermore, there’s 25

some indication that the Federal Reserve (Fed) is set

to slow the pace of increases. 20

As in the developed markets, there seemed to be a 15

dovish shift among emerging markets central banks.

10

Brazil kept rates unchanged, and the Bank of Mexico

announced that it was nearing the end stages of its 5

tightening cycle.

0

Regardless, monetary policy works with a lag, and we

expect the aggressive tightening that has already -5

occurred to weigh on economic growth well into 2023.

-10

-15

Net easing

-20

-25

-30

2018 2019 2020 2021 2022

Data source: Truist IAG, Haver. Series constructed using predominantly countries in the MSCI All Country World Index

EM = Emerging markets; DM = Developed markets

Past performance does not guarantee future results.Stronger U.S. dollar against emerging markets currencies with renewed

selloff in Chinese renminbi after the Chinese Communist Party Congress

The U.K.’s Prime Minister, Liz Truss, resigned, and Rishi Sunak replaced her. Developed markets currencies had a relief rally to acknowledge the U.K.’s

return to economic orthodoxy with the leadership change. In contrast, emerging markets currencies turned lower on the outcome of the 20th Chinese

Communist Party Congress – with Xi Jinping securing his unprecedented third-term presidency and appointing loyalists to key positions.

U.S. dollar indexes versus developed and emerging markets currencies

44

114 Developed (l-axis) Emerging (r-axis)

110

47

106

50

102

Appreciation

98 53

94

56

90 Depreciation

86 59

Nov-21 Dec-21 Feb-22 Apr-22 Jun-22 Aug-22 Oct-22

Data source: Truist IAG, Bloomberg, Developed: U.S. dollar spot index rate (left-axis), Emerging: Bloomberg custom index for emerging markets currencies including currencies of BRL, CLP, COP, MXN, PEN, CZK,

HUF, ILS, PLN, RON, RUB, ZAR, TRY, INR, IDR, KRW, MYR, PHP, SGD, THB (inverse –right axis). Data as of 10/31/2022U.S. economy is vulnerable as tightening financial conditions and inflation

weigh on economic growth; now looking for sluggishness through 2023

Financial conditions have quickly tightened as the Federal Reserve (Fed) has dramatically increased interest rates to combat inflation. The likely result is

slower growth through at least 2023, making the U.S. vulnerable to a recession within the next year. While it isn’t necessarily inevitable, there is now a

high probability of a recession in the next 12 months.

Growth of gross domestic product (GDP) by year

2022

Average 2010-2019 = 2.3% Forecast range

0.8% to 1.7%

5.7%

2023 range

2.7% 2.7% 2.9%

2.3% 1.7% 2.3% -0.5% to 1.0%

1.8% 2.3% 2.3%

1.5%

-3.4%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022f 2023f

Data source: Truist IAG, Bureau of Economic Analysis, IHS Markit. Change in real gross domestic product year over year, actual for 2010 through 3Q2022.

f = Truist IAG forecast for 4Q2022 through 2023The four primary indicators used to date a U.S. recession suggest the

economy is slowing, though not yet in a recession

The National Bureau of Economic Research Business Cycle Dating Committee is the official arbiter of the business cycle. It calls a recession based on

many factors, including four primary indicators – industrial production, nonfarm payrolls, real personal consumption expenditures, and real personal

income excluding transfer receipts. These indicators are considered coincidental, as opposed to leading, but currently suggest the U.S. is not yet in a

recession.

Big 4 indicators of economic activity since January 2020 (indexed)

Production Employment Real consumer spending Real income

110

105

100

95

Employment now above

90 pre-pandemic level

85

80

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32

Number of months

Data source: Truist IAG, Bloomberg. Monthly data through September 2022.Recession risks over the next 12 months have risen sharply

Although no single indicator is perfect, below are some of the most common recession flags and their current status. The majority of these recession flags

are now signaling a moderate-to-high probability of a recession in the next 12 months.

Select indicators Recession condition flag Current

status

Yield curve (3M/10Yr Treasuries) Inversion (3-month yield greater than 10-year)

Intermediate yield curve (2/10Yr) Inversion (2-year yield greater than 10-year)

Change in Fed funds rate Year-over-year increase with a 12-month lag

Credit spreads Increases for 3 months in a row

ISM Manufacturing Index Activity contracts for 3 months in a row

New building permits Year-over-year declines greater than 9% for 3 months

Leading Economic Indicators Declines four consecutive months

Unemployment rate Increases for 3 months in a row

Weekly jobless claims Year-over-year increase greater than 20%

Crude oil Year-over-year increase greater than 50%

Data source: Truist IAG. Red denotes a higher recession probability for the respective indicator, yellow denotes moderate recession probability, and green denotes low recession probability. Recession condition flags

shown are simplified; most include multi-part signals. Current status as of October 31, 2022.Rising concerns that a recession will be needed to tame inflation

Historically, once inflation is above 5%, it has generally taken a recession to bring it back down. There are unique circumstances this cycle given the

pandemic and supply chain challenges. So, while it could be different this time, elevated inflation and the Fed’s aggressive policy stance indicate risks are

elevated.

Consumer inflation year-over-year change

16%

12%

8%

Inflation = 5%

4%

0%

-4%

1950 1962 1974 1986 1998 2010 2022

Data source: Truist IAG, Bloomberg, Haver. Consumer inflation is measured using the Consumer Price Index (CPI). Shaded areas represent recessions.The Fed follows through with fourth-straight “supersized” rate hike to combat

inflation

The Fed increased its target range for the Federal

Federal funds target

funds rate by three-quarters of a point (0.75%) to a

range of 3.75% to 4.00%. That’s the fourth Tightening Cycles Market implied rate

8%

supersized rate hike.

Additionally, markets expect the Federal funds target

to be 4.50% by year-end 2022. 7%

6%

Market

5% expects 4.50%

by year end

4%

3%

2%

1%

0%

'92 '94 '96 '98 '00 '02 '04 '06 '08 '10 '12 '14 '16 '18 '20 '22

Data source: Truist IAG, Federal Reserve Board. Year-end upper bound figures shown.The job market is still holding up well

Initial jobless claims measure the number of people

U.S. initial jobless claims (in millions)

that are involuntarily out of work and are a leading

economic indicator. After steadily recovering from the Initial jobless claims

pandemic, initial claims continue to run near the pre-

7 Pre-pandemic all-time high (695,000)

pandemic three-year average.

Pre-pandemic 3-year average (228,000)

6

5

217,000 in the

4

latest week

3

2

1

0

'20 '21 '22

Data source: Truist IAG, Bloomberg, Department of Labor. Weekly data through October 22, 2022.Economic expansionary periods far exceed recessionary periods

While recessions vary in length and severity, they Average length of economic expansions and recessions

tend to be relatively brief episodes when compared to since 1950 (in months)

expansions.

55.6

10.3

Expansionary periods Recessionary periods

Data source: Truist IAG, Bloomberg, National Bureau of Economic Research.U.S.-led global market rebound

Global equities S&P 500

105 105

100 100

95 95

90 90

85 85

80 80

75 75

70 70

Jan-22 Apr-22 Jul-22 Oct-22 Jan-22 Apr-22 Jul-22 Oct-22

International developed markets Emerging markets

105 105

100 100

95 95

90

90

85

85

80

80 75

75 70

70 65

Jan-22 Apr-22 Jul-22 Oct-22 Jan-22 Apr-22 Jul-22 Oct-22

Data source: Truist IAG, FactSet, MSCI

Global equites = MSCI ACWI; International developed markets = MSCI EAFE; Emerging markets = MSCI EM; Index prices are in U.S. dollars and indexed to 100.

Past performance does not guarantee future results.The S&P 500 rebounded from levels consistent with a mild recession

After trading down about 25% from its January peak

S&P 500 price with implied downside based on median

– which is close to the median decline during past

recessions—stocks rebounded in the back half of

and average declines

4800

October.

4300

“Median" recession decline

3800 = -24% or implied S&P 500 level of ~3650

Pre-pandemic peak

3300 “Average" recession decline

= -29% or implied S&P 500 level of ~3400

2800

2300

1800

2019 2020 2021 2022

Data source: Truist IAG, FactSet. Past performance does not guarantee future results.Upside for the S&P 500 is likely capped in the 3950 to 4200 range given a

confluence of fundamental and technical resistance

From a fundamental perspective, even if we apply an S&P 500

optimistic valuation assumption of 17x to 18x to

current forward consensus earnings, which also S&P 500 200-day moving average

appear too high, the upside for the market from

current levels is likely capped in the 3950 to 4200

4,800

range.

4,700

Moreover, the downward sloping 200-day moving 4,600

average is currently just above 4100. This is also an 4,500

important technical resistance level. 4,400

Conversely, the market has strong fundamental 4,300 Top of range

support at a P/E of around 15x to 15.5x, and near the 4,200 ~3950-4200=

October lows, stocks were pricing in a mild recession. 4,100 17x to 18x P/E

4,000

3,900

3,800

3,700

Bottom of

3,600

3,500 ~3500-3600

3,400 15x to 15.5x

3,300

3,200

3,100

3,000

Oct 20 Jan 21 Apr 21 Jul 21 Oct 21 Jan 22 Apr 22 Jul 22 Oct 22

Data source: Truist IAG, FactSet. Past performance does not guarantee future results.Equity valuations are likely capped, and downside earnings risks remain

After declining to 15.2x, the S&P 500’s forward P/E rebounded to 16.7x, near the 10-year average of 17x. Valuations are likely capped in the 17x to 18x

range, which we view as optimistic, considering downside risks to earnings alongside a slowing economy and elevated inflation. Moreover, the 10-year

U.S. Treasury rate is about double its 10-year average and has risen more than one percent since stocks last traded at 18x in August.

S&P forward P/E likely capped in S&P 500 consensus earnings estimates

the 17x-18x range

2022 EPS estimates 2023 EPS estimates

25 Pandemic overshoot

Stimulus/record low $255

24

rates

23 $250

22

21 17x = 10-year average $245

20 18x = August 2022 peak

$240

19

18 $235

17

16.7 $230

16

15 $225

15.2

14

13 $220

12

11 $215

10 $210

2012 2014 2016 2018 2020 2022 Dec-21 Feb-22 Apr-22 Jun-22 Aug-22 Oct-22

Data source: Truist IAG, FactSet.

Past performance does not guarantee future results.Positive seasonality and depressed sentiment biggest assets for bull case

but investors still facing a challenging macro and fundamental backdrop

This year has been far from average, but the final two months of a midterm election year have tended to be a strong period for stocks. Given many

investors have had a tough year and are now underinvested in stocks, a further rally could spark a fear of missing out and an upside overshoot. Still, while

this is a possibility, it is not enough to offset our more cautious intermediate-term stance given rising recession risks and weakening fundamentals.

Average S&P 500 calendar path during % Individual investors bullish

midterm election years (AAII sentiment)

(Since 1950)

60%

57%

7%

50%

6%

5%

40%

4%

3%

30%

2% 27%

1%

20%

0%

-1%

10%

-2%

Mar-20 Aug-20 Jan-21 Jun-21 Dec-21 May-22 Oct-22

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Data source: Truist IAG, FactSet. Past performance does not guarantee future results.Bond yields are now competitive with earnings yield

The gap between bond yields and the earnings yield for stocks, which is the inverse of the P/E ratio, has closed dramatically. This simply means that

there is now more competition for stocks than there has been for more than a decade. This has put downward pressure on equity valuations.

Bond yields are now competitive with earnings yield

14%

S&P 500 trailing earnings yield U.S. investment grade corporate bonds U.S. 1-year Treasury

12%

10%

8%

6%

4%

2%

0%

2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Data source: Truist IAG, FactSet.

Past performance does not guarantee future resultsWe see better opportunities below the market’s surface with the average

stock at more attractive valuations

The average stock, as proxied by the S&P 500 Equal Weight Index, is trading at a very reasonable forward P/E of 14.4x. This benchmark gives an equal

weighting to each stock in the index. Therefore, it is less influenced by a few mega cap growth stocks that are still trading at more expensive valuations.

S&P 500 Equal Weight Index – forward P/E

24.0

22.0

20.0

18.0

16.0

14.0

14.4

12.0 13.2

12.9

10.0 11.3

8.0

2016 2017 2018 2019 2020 2021 2022

Data source: Truist IAG, FactSet. *Average stock proxied by the Invesco S&P 500 Equal Weight Index ETF

Past performance does not guarantee future resultsLarge cap value relative price trends are improving

Our sector strategy continues to favor market segments that have larger weights in the value style, such as industrials and health care. Conversely, the

growth style remains heavily influenced by the technology and communications services sectors, which make up more than 50% of the index; relative

earnings and price trends remain weak, and valuations are not compelling for these sectors.

Large cap value price trends relative to growth improving

after more than a decade of underperformance

115 Value price relative to growth

105

95

85

75

65

55

45

35

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Data source: Truist IAG, FactSet.

Past performance does not guarantee future resultsReiterate our negative view on emerging markets equities

Emerging markets have underperformed by 28% since we shifted to less attractive in May 2021. While markets are oversold and due for a bounce, we

continue to have a negative view given declining profits trends and less friendly market-based polices.

Emerging markets price relative to S&P 500

112

109

106

103

100

97

94

91

88 Reduced EM to

85 underweight

82

79

76

73

70

67

64 New lows

61

Jan-21 Apr-21 Jul-21 Oct-21 Jan-22 Apr-22 Jul-22 Oct-22

Data source: Truist IAG, FactSet. Past performance does not guarantee future results

Emerging markets = MSCI Emerging MarketsMarkets have done fine under a wide range of partisan control scenarios;

factors outside of Washington tend to have a greater market impact

Markets have shown positive returns under various

Average annual S&P 500 returns under partisan control

political control scenarios in Washington. However, we

would be careful not to over extrapolate this as other

factors beyond Washington’s control impact markets, 13.7% 13.6%

such as valuations, the business cycle, and monetary 13.0% 12.9%

policy.

Our view is the most aggressive monetary tightening

cycle over the past forty years, a slowing economy,

and how quickly inflation slows down will be a larger 9.8%

influence on markets and the business cycle over the

next year.

4.9%

*

R Senate D Senate R Congress R Congress D Congress D Congress

D House R House D President R President D President R President

R President D President

Data source: Truist IAG, Strategas

Period includes (1933-2019, excl. 2001-2002)

Past performance does not guarantee future results.Stocks have risen in the 12 months following every midterm election since

1942, but what may be different than past instances is a recession next year

Historically, the S&P 500 has risen in the 12 months following each of the past 20 midterm election years. However, there has never been a recession in

the third year of a presidential cycle, which is looking like an increasing probability in 2023.

S&P 500 price return # of recessions starting in year of

12-month period following midterm election the presidential cycle*

35%

30% 9

25%

20%

5

15%

10%

1

5%

0

0% Year 1 Year 2 Year 3 Year 4

'42 '46 '50 '54 '58 '62 '66 '70 '74 '78 '82 '86 '90 '94 '98 '02 '06 '10 '14 '18

Data source: Truist IAG, Strategas

*Financial Crisis/Great Recession considered Jan 2008 (Year 4) start; data since 1929

Past performance does not guarantee future results.The most aggressive central bank tightening cycle during a midterm election

year in more than 40 years is set to weigh on economic growth next year

Midterm election years - Net Fed actions

(Percentage points tightening/easing)

5.0% 100 bps of additional tightening

through year end would push 2022

4.0% tightening to the highest on record

Net tightening

3.0%

2.0%

1.0%

0.0%

-1.0%

Net easing

-2.0%

-3.0%

-4.0%

-5.0%

'62 '66 '70 '74 '78 '82 '86 '90 '94 '98 '02 '06 '10 '14 '18 '22

Data source: Truist IAG, Strategas

Past performance does not guarantee future results.Bringing income back to fixed income – at a cost

This year has hosted the sharpest drawdown for the Bloomberg U.S. Aggregate Bond Index (Agg) since its inception in 1976. However, the move to

higher yields (i.e., lower prices) leaves the benchmark more capable of providing critical income and portfolio stability going forward. The total return

outlook for bonds is closely related to their starting yields. The Agg’s 5.0% current yield to worst is the first time the starting yield is above 4% since 2009.

U.S. Agg annual returns U.S. Agg 5-year average returns by starting

30% yield range

14.1%

20%

The Agg index is

currently yielding 5.0%

10% 9.4%

6.9%

0% 5.6%

3.2%

2.3%

-10%

The Agg is on pace for back-to-back negative

annual returns for the first time on record

-16% 10%

-20%

1977 1982 1987 1992 1997 2002 2007 2012 2017 YTD Starting yield ranges for the Agg index

2022

Data Source: Truist IAG, Bloomberg

Data as of 10/31/20222- and 10-year U.S. Treasury yields are at the highest levels since 2007

The highest yields currently reside between 1- and 3-year maturities, creating a compelling entry point for passive income investors seeking productive,

high-quality opportunities. However, the sharp rise in longer-dated yields, coupled with rising global economic risks, has restored significant value in

duration over the past 18 months. In the year ahead, we expect the end of the Fed’s hiking cycle, cooler inflation readings, and slower economic activity to

support better total returns within high quality fixed income.

U.S. Treasury yields

2-year 10-year

5%

4%

3%

2%

1%

0%

2006 2008 2010 2012 2014 2016 2018 2020 2022

Data Source: Truist IAG, Bloomberg

Data as of 10/31/2022

Past performance does not guarantee future results.Fed’s favorite yield curve gauge flashing ominous signal

As forecasted, the 3-month/10-year yield curve inverted for the first time since February 2020, a rare development that has reliably signaled future

economic slowdowns. The yield differential between the 3-month U.S. Treasury bill and 10-year U.S. Treasury note is the Fed’s preferred gauge of

financial conditions, lending additional weight to this curve’s signal. The latest inversion highlights investors’ deepening concerns that the Fed’s efforts to

curb inflation will soon create a significant drag on the U.S. economy.

Yield curve comparison (in basis points)

250

3-month/10-year 2-year/10-year

200

150

100

50

0

-50

-100

2017 2018 2019 2020 2021 2022

Data Source: Truist IAG, Bloomberg

Data as of 10/31/2022

Past performance does not guarantee future resultsRelative value in fixed income

Many fixed income asset classes have yields at or Current yield vs. 10-year range

near 10-year highs – from high-quality sectors, such

Range Current Yield

as U.S. Treasuries and mortgage-backed securities,

10%

to high yield corporate bonds and preferreds.

With growing risks to the U.S. economy, our focus 8%

has turned more towards higher quality fixed income

– an important source of ballast for portfolios.

5%

While yields have become more attractive for higher

risk fixed income sectors, spreads in general are 3%

susceptible to further widening given tightening

financial conditions and higher risks of an economic

slowdown. 0%

-3%

Munis

HY corp

EM loc cur

U.S. TIPS

U.S. core taxable

IG corp

Intl dev mrkts

HY muni

MBS

Lev loans

EM hard cur

U.S. 10-yr Treasury

Preferreds

High quality Higher risk

Data source: Truist IAG, FactSet, yield to worst shown except for preferreds and EM bond indices (yield to maturity).

U.S. 10-Yr Treasury = Bloomberg U.S. Treasury Bellwethers (10-Yr), U.S. Core Taxable = Bloomberg U.S. Aggregate, Municipals = Bloomberg Municipal Bond 1-15 Year, U.S. Corporates = Bloomberg U.S. Corporate IG,

MBS = Bloomberg U.S. MBS, Intl Dev Mkts = ICE BofA Global Government ex U.S. (U.S.D hedged), HY Corp = ICE BofA U.S. High Yield, Lev Loans = S&P/LSTA U.S. Leveraged Loan 100 Index, HY Muni = Bloomberg

Municipal High Yield, Preferreds = ICE BofA Fixed Rate Preferred, EM Hard Cur = JP Morgan EMBI Global Diversified, EM Loc Cur = JP Morgan GBI-EM Global Diversified. Past performance does not guarantee future

results. Investing in the bond market is subject to certain risks, including market, interest rate, issuer and inflation risk – investments may be worth more or less than the original cost when redeemed. The value of most

bond strategies and fixed income securities are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and more volatile than securities with shorter durations –

bond prices generally fall as interest rates rise, and values rise when interest rates decline. Past performance does not guarantee future results.Longer duration tends to outperform as economic activity slows

High quality fixed income with greater interest rate

U.S. government bond index returns by maturity

sensitivity (i.e., longer duration) tends to provide

better performance as the U.S. economy decelerates. Bloomberg U.S. Government Bond 1-3 Year Index

Given the sharp rise in U.S. Treasury yields over the

Bloomberg U.S. Government Bond Index

past three months and our outlook for rising

economic risks, the forward-looking total return Bloomberg U.S. Government: Long Bond Index

outlook for longer duration, high quality fixed income

has improved significantly. 15.4%

14.5%

11.9%

10.8%

10.1%

7.9%

7.3%

6.3%

5.5%

Since 1976 (annualized) During PMI slowdowns (avg) Last 6 recessions (avg)

Data Source: Truist IAG, Bloomberg

Data as of 10/31/2022.

Past performance does not guarantee future results.Muni-to-U.S. Treasury ratios improving amid higher rate volatility

Munis in the 10- to 30-year maturity range currently

Muni yields as a % of U.S. Treasury Yields

offer the best valuation relative to U.S. Treasuries;

however, we recommend patience with respect to 9/30/2021 12/31/2021 10/31/2022

adding extreme levels of duration exposure. Shorter-

dated ratios have improved but remain expensive 137%

relative to their long-run averages.

We expect relative strength in tax-exempt munis to

continue, underpinned by low issuance, improved

muni-to-U.S. Treasury ratios, and the layer of

insulation munis can provide from U.S. Treasury

volatility.

87%

83%

78%

72% 74% 74%

67% 69% 68%

63%

59%

43% 44%

32%

1-year 3-year 7-year 10-year 20-year

Data Source: Truist IAG, Bloomberg. Interest income may be subject to the federal alternative minimum tax. Other state and local taxes may apply.

Past performance does not guarantee future results.Publication details

Contributors

Keith Lerner, CFA, CMT Chip Hughey, CFA Wasif Latif

Co-Chief Investment Officer, Managing Director, Managing Director,

Chief Market Strategist Fixed Income Portfolio Strategy

Michael Skordeles, AIF® Eylem Senyuz Shelly Simpson, CFA, CAIA

Senior U.S. Macro Strategist, Senior Global Macro Strategist, Senior Investment Strategy

Portfolio & Market Strategy Portfolio & Market Strategy Analyst,

Portfolio & Market Strategy

Jeff Terrell, CFA Dylan Kase, CFA Emily Novick, CFA, CFP®

Senior Investment Strategy Senior Investment Strategy Senior Portfolio Construction

Analyst, Analyst, Analyst,

Portfolio & Market Strategy Portfolio & Market Strategy Portfolio & Market Strategy

Evan Moog, CFA Editors

Fixed Income Investment

Analyst, Oliver Merten, CFA, CFP®

Fixed Income Strategy Managing Director,

Investment Communications

Additional contributors to sector strategy

Scott Yuschak, CFA Adam White, CFA, CMT Julie Parham

Managing Director, Senior Equity Strategy Analyst, Manager,

Equity Strategies Equity Strategies Investment CommunicationsTruist Wealth – Investment Advisory Group

Keith Lerner, CFA, CMT Oscarlyn Elder, CFA, CAIA

Co-Chief Investment Officer Co-Chief Investment Officer

Chief Market Strategist Senior Managing Director

Senior Managing Director

Portfolio & market strategy Equity strategies Manager research Alternative investments Private equity & credit

Wasif Latif Scott Yuschak, CFA Ric Mayfield, CFA, CAIA Spencer Boggess Ravi Ugale

Managing Director, Portfolio Managing Director, Equity Managing Director, Manager Managing Director, Alternative Managing Director, Private Equity &

Strategy Strategies Research Investments Credit

Mike Skordeles, AIF® Charles Redding Kelly Frohsin, CIMA®, CFP® Mohan Badgujar Will Repath

Senior U.S. Macro Strategist Senior Equity Strategy Analyst Senior Manager Research Senior Alternative Investments Analyst Senior Private Equity & Credit Analyst

Analyst

Eylem Senyuz Adam White, CFA, CMT Rich Cheung Julian Partridge

Senior Global Macro Strategist Senior Equity Strategy Analyst Chris Hett, CFA Senior Alternative Investments Analyst Private Equity & Credit Analyst

Senior Manager Research Len Lebov Dylan Thompson

Jeff Terrell, CFA Marty Stamps Analyst

Senior Investment Strategy Analyst Senior Equity Strategy Analyst Senior Alternative Investments Analyst Private Equity & Credit Analyst

Alison Majors, AIF®, CFA,

Shelly Simpson, CFA, CAIA John Meza CFP®, Senior Manager Colin Fox, CTFA Diverse asset managers

Senior Investment Strategy Analyst Senior Equity Strategy Analyst Research Analyst Alternative Investments Analyst

Sabrina Bowens-Richard, CFA, CAIA

Emily Novick, CFA, CFP® Scott Reynolds Benardo Richardson Ryan Taylor, CFA, CAIA Senior Investment Solutions Specialist

Senior Portfolio Construction Investment Advisory Associate Manager Research Analyst Alternative Investments Analyst

Carlton Reed

Analyst Investment Advisory Associate

Diane Schmidt Haley Lawson

Dylan Kase, CFA Fixed income strategies Senior Manager Research Investment Advisory Associate

Senior Investment Strategy Analyst Analyst

Chip Hughey, CFA

Managing Director, Fixed Thomas Toman Investment communications Sustainable investing/ESG

Income Manager Research Analyst

Oliver Merten, CFA, CFP® Colleen Silver, CFA

Elsa Wartner, CFA, CIMA® Managing Director, Investment Senior Investment Solutions Specialist

Evan Moog, CFA Manager Research Analyst Communications

Fixed Income Investment

Analyst Samuel Grelck Julie Parham

Investment Advisory Associate Investment Communications Manager

All teammates listed except Grelck, Meza, Partridge, Reed, Stamps, and Thompson are investment adviser representatives

of Truist Advisory Services, Inc.Disclosures Advisory managed account programs entail risks, including possible loss of principal and may not be suitable for all investors. Please speak to your advisor to request a firm brochure which includes program details, including risks, fees and expenses. International investments are subject to special risks, such as political unrest, economic instability, and currency fluctuations. Emerging Markets – Investing in the securities of such companies and countries involves certain considerations not usually associated with investing in developed countries, including unstable political and economic conditions, adverse geopolitical developments, price volatility, lack of liquidity, and fluctuations in currency exchange rate. Truist Wealth is a name used by Truist Financial Corporation. Banking products and services, including loans, deposit accounts, trust and investment management services provided by Truist Bank, Member FDIC. Securities, brokerage accounts, insurance/annuities offered by Truist Investment Services, Inc. member FINRA, SIPC, and a licensed insurance agency where applicable. Life insurance products offered by referral to Truist Insurance Holdings, Inc. and affiliates. Investment advisory services offered by Truist Advisory Services, Inc., Sterling Capital Management, LLC, and affiliated SEC registered investment advisers. Sterling Capital Funds advised by Sterling Capital Management, LLC. While this information is believed to be accurate, Truist Financial Corporation, including its affiliates, does not guarantee the accuracy, completeness or timeliness of, or otherwise endorse these analyses or market data. While this information is believed to be accurate, Truist Financial Corporation, including its affiliates, does not guarantee the accuracy, completeness or timeliness of, or otherwise endorse these analyses or market data. The opinions and information contained herein have been obtained or derived from sources believed to be reliable, but Truist Financial Corporation makes no representation or guarantee as to their timeliness, accuracy or completeness or for their fitness for any particular purpose. The information contained herein does not purport to be a complete analysis of any security, company, or industry involved. This material is not to be construed as an offer to sell or a solicitation of an offer to buy any security. Opinions and information expressed herein are subject to change without notice. TIS and/or its affiliates, including your Advisor, may have issued materials that are inconsistent with or may reach different conclusions than those represented in this commentary, and all opinions and information are believed to be reflective of judgments and opinions as of the date that material was originally published. TIS is under no obligation to ensure that other materials are brought to the attention of any recipient of this commentary. Comments regarding tax implications are informational only. Truist and its representatives do not provide tax or legal advice. You should consult your individual tax or legal professional before taking any action that may have tax or legal consequences. Investments involve risk and an investor may incur either profits or losses. Past performance should not be taken as an indication or guarantee of future performance. TIS/TAS shall accept no liability for any loss arising from the use of this material, nor shall TIS/TAS treat any recipient of this material as a customer or client simply by virtue of the receipt of this material. The information herein is for persons residing in the United States of America only and is not intended for any person in any other jurisdiction. Investors may be prohibited in certain states from purchasing some over-the-counter securities mentioned herein. The information contained in this material is produced and copyrighted by Truist Financial Corporation and any unauthorized use, duplication, redistribution or disclosure is prohibited by law. TIS/TAS’s officers, employees, agents and/or affiliates may have positions in securities, options, rights, or warrants mentioned or discussed in this material. Asset classes are represented by the following indexes. An investment cannot be made directly into an index. S&P 500 Index is comprised of 500 widely-held securities considered to be representative of the stock market in general. Equity is represented by the MSCI ACWI captures large and mid cap representation across 23 Developed Markets (DM) and 24 Emerging Markets (EM) countries*. With 2,757 constituents, the index covers approximately 85% of the global investable equity opportunity set Fixed Income is represented by the Barclays Aggregate Index. The index measures the performance of the U.S. investment grade bond market. The index invests in a wide spectrum of public, investment-grade, taxable, fixed income securities in the United States – including government, corporate, and international dollar-denominated bonds, as well as mortgage-backed and asset-backed securities, all with maturities of more than 1 year.

Disclosures Commodities are represented by the Bloomberg Commodity Index which is a composition of futures contracts on physical commodities. It currently includes a diversified mix of commodities in five sectors including energy, agriculture, industrial metals, precious metals and livestock. The weightings of the commodities are calculated in accordance with rules that ensure that the relative proportion of each of the underlying individual commodities reflects its global economic significance and market liquidity. Cash is represented by the ICE BofAML U.S. Treasury Bill 3 Month Index which is a subset of the ICE BofAML 0-1 Year U.S. Treasury Index including all securities with a remaining term to final maturity less than 3 months. U.S. Large Cap Equity is represented by the S&P 500 Index which is an unmanaged index comprised of 500 widely-held securities considered to be representative of the stock market in general. U.S. Mid Cap is represented by the S&P MidCap 400® provides investors with a benchmark for mid-sized companies. The index, which is distinct from the large-cap S&P 500®, measures the performance of mid-sized companies, reflecting the distinctive risk and return characteristics of this market segment. U.S. Small Cap Core Equity is represented by the S&P 600 Small Cap Index which is a measure of the performance of the small-cap segment of the U.S. equity universe International Developed Markets is represented by the MSCI EAFE Index is an equity index which captures large and mid cap representation across 21 Developed Markets countries* around the world, excluding the U.S. and Canada. With 921 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country. Emerging Markets is represented by the MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries*. With 1,125 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country. Value is represented by the S&P 500 Value Index which is a subset of stocks in the S&P 500 that have the properties of value stocks. Growth is represented by the S&P 500 Growth Index which is a subset of stocks in the S&P 500 that have the properties of growth stocks. U.S. Government Bonds are represented by the Bloomberg U.S. Government Index which is an unmanaged index comprised of all publicly issued, non-convertible domestic debt of the U.S. government or any agency thereof, or any quasi-federal corporation and of corporate debt guaranteed by the U.S. government U.S. Mortgage-Backed Securities are represented by the U.S. Mortgage-Backed Securities (MBS) Index which covers agency mortgage-backed pass-through securities (both fixed-rate and hybrid ARM) issued by Ginnie Mae (GNMA), Fannie Mae (FNMA), and Freddie Mac (FHLMC). U.S. Investment Grade Corporate Bonds are represented by the Bloomberg U.S. Corporate Investment Grade Index which is an unmanaged index consisting of publicly issued U.S. Corporate and specified foreign debentures and secured notes that are rated investment grade (Baa3/BBB- or higher) by at least two ratings agencies, have at least one year to final maturity and have at least $250 million par amount outstanding. The S&P U.S. REIT index measures the investable universe of publicly traded real estate investment trusts domiciled in the United States U.S. High Yield Corp is represented by the ICE BofAML U.S. High Yield Index tracks the performance of below investment grade, but not in default, U.S. dollar denominated corporate bonds publicly issued in the U.S. domestic market, and includes issues with a credit rating of BBB or below, as rated by Moody’s and S&P. Floating Rate Bank Loans are represented by the Credit Suisse Leveraged Loan Index. The index represents tradable, senior-secured, U.S.-dollar-denominated non-investment-grade loans. Global Equity is represented by the MSCI All World Country (ACWI) Index which is defined as a free float-adjusted market capitalization-weighted index that is designed to measure the equity market performance of developed and emerging markets. The MSCI ACWI Index consists of 48 country indices comprising 24 developed markets countries and 24 emerging markets countries. Emerging Markets Equity is represented by the MSCI EM Index which is defined as a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets countries Intermediate Term Municipal Bonds are represented by the Bloomberg Municipal Bond Blend 1-15 Year (1-17 Yr) is an unmanaged index of municipal bonds with a minimum credit rating of at least Baa, issued as part of a deal of at least $50 million, that have a maturity value of at least $5 million and a maturity range of 12 to 17 years.

You can also read